U.S. Dog Food Market Size, Share, Trends & Growth Forecast Report By Pet Food Product, By Distribution Channel, and By Country (California, Texas, Florida, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Dog Food Market Size

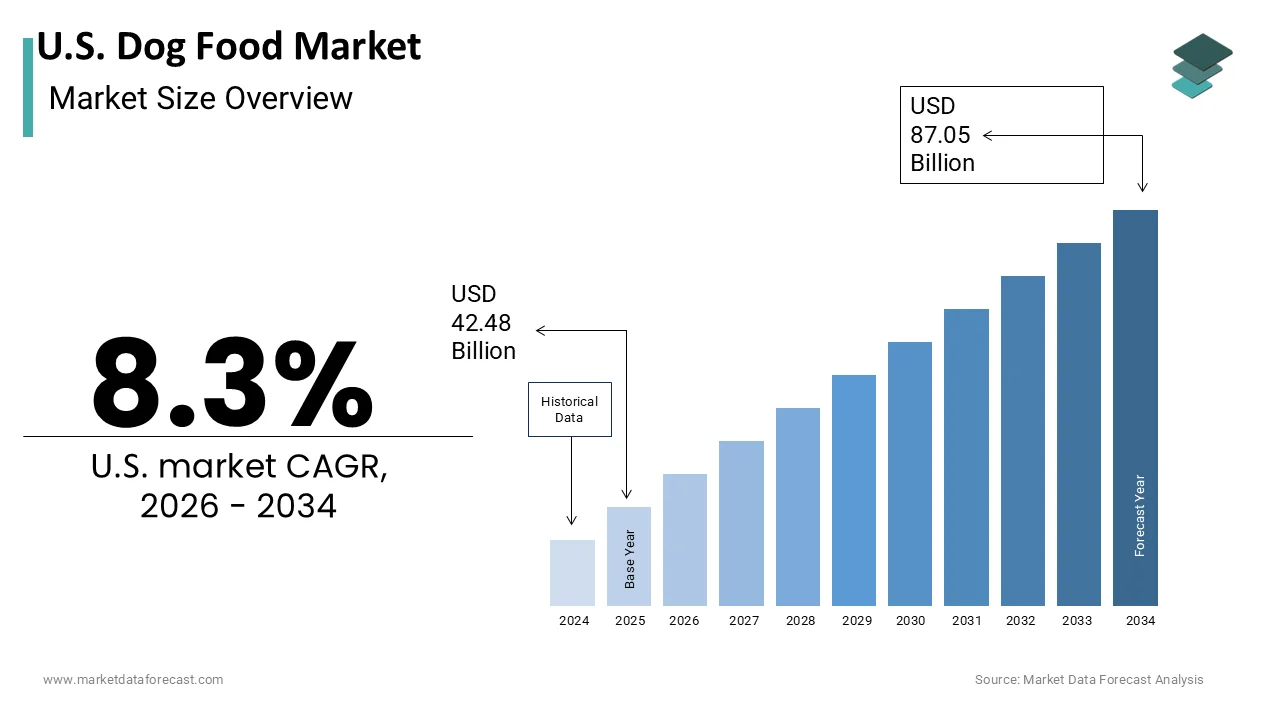

The U.S. Dog Food Market is projected to grow from USD 42.48 billion in 2025 to USD 46.00 billion in 2026 and reach USD 87.05 billion by 2034, registering a CAGR of 8.3% during the forecast period from 2026 to 2034.

The dog food is a nutritional product, specifically formulated for canine consumption. As per the American Pet Products Association, approximately 65% of US households own a pet, with dogs being the most common companion animal, totaling nearly 70 million households. This high penetration rate creates a stable and resilient consumer base that prioritizes quality and health outcomes. The agricultural sector supplies significant volumes of poultry, bees,f and grains, which serve as primary ingredients in commercial dog food formulations, ns ensuring a robust domestic supply chain. Regulatory oversight by the Association of American Feed Control Officials establishes standardized definitions and labeling requirements by ensuring product safety and nutritional adequacy. The shift toward transparency in sourcing and ingredient quality reflects changing consumer preferences for clean-label products. Economic stability and disposable income levels directly influence purchasing power, allowing owners to invest in higher-value nutritional options.

MARKET DRIVERS

Humanization of Pets and Premiumization Trends Drive Demand

The profound trend of pet humanization, as owners increasingly view their dogs as children or family members deserving of high-quality nutrition, is accelerating the growth of the United States dog food market. This emotional bond translates into a willingness to spend on premium products that mirror human dietary standards, such as organic grain-free and limited ingredient diets. The research firm's spending on premium and super premium dog food has outpaced overall growth, reflecting this shift in consumer behavior. Owners are actively seeking products with recognizable whole food ingredients,s avoiding artificial preservatives, colors, or fillers that were once standard in conventional kibble. The rise of social media and online communities further amplifies awareness of nutritional best practices, encouraging owners to make informed choices based on veterinary advice and peer recommendations. This demographic shift is particularly evident among millennials and Gen Z consumers who prioritize sustainability and ethical sourcing in their purchasing decisions. The availability of specialized diets for specific health conditions, such as weight management, joint support, and sensitive stomachs, caters to the individualized needs of each pet. Retailers respond by expanding shelf space for natural and holistic brands, creating a competitive environment that fosters innovation.

Increasing Veterinary Awareness of Preventive Nutrition

The growing veterinary emphasis on preventive healthcare through proper nutrition for specialized and therapeutic dog food formulations, which is ascribed in boosting the growth of the United States dog food market. Veterinarians play a crucial role in educating pet owners about the link between diet and long-term health outcomes, such as obesity, diabetes, and dental disease. The regular wellness visits provide opportunities for professionals to recommend prescription diets and high-quality commercial foods that support specific physiological needs. The rising prevalence of chronic conditions in dogs due to sedentary lifestyles and overfeeding necessitates dietary interventions that manage calorie intake and nutrient balance. Prescription diets for kidney disease, allergies,s and gastrointestinal issues require precise formulation and often command higher prices, es contributing to market value growth. Pet owners trust veterinary recommendations,ons leading to increased adoption of science-based nutrition brands that invest heavily in clinical research and testing. The integration of nutritional counseling into routine veterinary care ensures that dogs receive appropriate diets throughout their life stages, from puppyhood to senior years. This professional endorsement validates the efficacy of premium products and encourages compliance among owners seeking to extend their pets' lifespan.

MARKET RESTRAINTS

Volatility in Raw Material Costs Impacts Pricing Stability

The volatility of raw material prices, as ingredients, such as meat, poultry, grains, and vegetables, are subject to fluctuating agricultural commodities, which is majorly hindering the growth of the United States dog food market. Climate change, diseases, and geopolitical events can disrupt supply chains, leading to sudden increases in input costs that manufacturers struggle to absorb. The prices for key ingredients like corn, soybean meal, and chicken have experienced notable swings in recent years, affecting production margins for pet food companies. Small and mid-sized brands with less purchasing power are particularly vulnerable to these fluctuations,s limiting their ability to compete with larger conglomerates. The reliance on specific protein sources makes formulations susceptible to shortages during outbreaks of animal diseases such as avian influenza. Supply chain disruptions also affect the availability of packaging material,s further compounding cost pressures. Consumers who are price sensitive may switch to lower-cost alternatives or private-label brands during periods of inflation, reducing revenue for premium manufacturers.

Regulatory Complexity and Labeling Standards Create Compliance Burdens

The strict regulatory requirements and complex labeling standards impose substantial compliance costs and operational constraints is hampering the growth of the United States dog food market. The Association of American Feed Control Officials sets guidelines for ingredient definitions, nutritional adequacy, and labeling claims, which vary by state and require careful adherence to avoid legal penalties. Manufacturers must ensure that their products meet safety standards for contaminants such as mycotoxins, heavy metals, and Salmonella, requiring rigorous testing and quality control protocols. The introduction of new regulations regarding sustainable sourcing and environmental impact adds another layer of complexity for companies seeking to produce eco-friendly products. Misleading claims about health benefits or ingredient origins can lead to class action lawsuits and reputational damage, forcing brands to invest heavily in legal and regulatory affairs. The process of approving new ingredients or formulations is time-consuming and expensive, limiting the speed of innovation. Small businesses often lack the resources to navigate these regulations effectively, thereby creating barriers to entry. Inconsistencies between federal and state regulations further complicate distribution strategies for national brands. These regulatory pressures increase operational costs and slow down time to market for new products.

MARKET OPPORTUNITIES

Expansion of Fresh and Frozen Food Delivery Services

The rapid growth of fresh and frozen dog food delivery services by offering convenient and highly nutritious alternatives to traditional kibble is setting up new opportunities for the growth of the United States dog food market. These subscription-based models provide pre-portioned meals made from human-grade ingredients that are lightly cooked or raw, preserving nutrients and enhancing palatability. The claims related to digestive issues and allergies are common, prompting owners to seek cleaner and more digestible food options. Fresh food companies leverage digital platforms to customize meal plans based on bree,d age, weight, and activity level,l creating a personalized experience that builds strong customer loyalty. The direct-to-consumer model eliminates retail intermediaries, enabling brands to capture higher margins and gather valuable data on consumer preferences. The convenience of home delivery appeals to busy urban professionals who prioritize pet health but lack time for meal preparation. Investment in cold chain logistics and packaging technology ensures product freshness and safety during transit. The visual appeal of fresh ingredients shared on social media drives organic marketing and brand awareness. This segment attracts younger demographics willing to pay a premium for perceived health benefits and convenience.

Integration of Functional Ingredients for Health Benefits

The incorporation of functional ingredients, such as probiotics, omega fatty acids, and antioxidants, is more likely to create new opportunities for the growth of the United States dog food market. Consumers are increasingly interested in proactive health management, ent seeking foods that support immunity,nity joint health, skin, coat condition,n and cognitive function. The demand for functional pet food ingredients is rising as owners look for holistic solutions that reduce the need for supplements and veterinary interventions. Brands that transparently list these beneficial ingredients and explain their scientific basis can command premium pricing and build trust with educated consumers. The development of specialized formulas for senior dogs focusing on mobility and brain health addresses the needs of an aging pet population. Innovations in ingredient processing allow for the retention of bioactive compounds that enhance efficacy. Collaborations with veterinary nutritionists validate health claims and provide credibility to marketing messages. The trend toward preventive care aligns with the inclusion of functional ingredients, making them a key selling point in retail and online channels. Educational campaigns help consumers understand the long-term benefits of these additions, driving adoption.

MARKET CHALLENGES

Prevalence of Counterfeit and Substandard Products

The presence of counterfeit and substandard dog food products to brand integrity and consumer safety is one of the major challenges for the growth of the United States dog food market. Illicit manufacturers produce fake versions of popular premium brands using inferior or unsafe ingredients that can cause serious health issues for dogs. The intellectual property theft and counterfeiting in the pet food sector have increased with online marketplaces serving as primary distribution channels for these illicit goods. Consumers who unknowingly purchase counterfeit products may experience negative health outcomes for their pets, leading to loss of trust in the brand and potential legal liabilities for the manufacturer. The difficulty in verifying authenticity on third-party platforms complicates enforcement efforts and allows counterfeiters to operate with impunity. Legitimate companies must invest in advanced anti-counterfeiting technologies such as QR codes and holographic seals to protect their products. These measures add to operational costs and require continuous monitoring and updates. The reputational damage from counterfeit incidents can be long-lasting, affecting sales and brand equity. The fragmentation of the online retail landscape makes it challenging to track and remove fake listings effectively.

Supply Chain Disruptions and Logistics Hurdles

The supply chain disruptions and logistics hurdles to the consistent availability and affordability of is expected to impede the growth of the United States dog food market. Dependence on global sourcing for certain ingredients and packaging materials makes the industry vulnerable to international trade disputes,s port congestion, and transportation delays. As per the US Census Bureau,u import and export fluctuations have impacted the timely delivery of components, ts causing stockouts and production slowdowns for major manufacturers. Just-in-time inventory models used by many companies leave little buffer for unexpected disruptions, leading to empty shelves and frustrated consumers. Labor shortages in the manufacturing and transportation sectors further exacerbate these issues, leading to increased lead times and operational costs. The concentration of production facilities in specific regions creates single points of failure that can disrupt national supply chains during local emergencies. Manufacturers face pressure to diversify sourcing and increase inventory levels, ls which ties up capital and reduces efficiency. The inability to guarantee product availability affects retailer relationships and consumer loyalty. These logistical challenges require significant investment in supply chain resilience and alternative distribution strategies.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Pet Food Product, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Texas, Florida, New York, and the rest of the United States |

| Market Leaders Profiled | Mars, Incorporated, Nestlé Purina PetCare Company, Hill’s Pet Nutrition, Inc., The J.M. Smucker Company, Blue Buffalo Co., Ltd. (General Mills, Inc.), Freshpet, Inc., Diamond Pet Foods, Inc., WellPet LLC, Champion Petfoods LP, Merrick Pet Care, Inc., Natural Balance Pet Foods, Inc., Spectrum Brands Holdings, Inc. |

SEGMENTAL ANALYSIS

By Pet Food Product Insights

The pet food product segment was the largest by occupying 44.3% of the US dog food market share in 2025, with a fundamental daily necessity for canine survival and health maintenance. The dog owners spend the largest portion of their annual pet care budget on food, reflecting its status as a non-negotiable expense. The average dog consumes approximately one to three cups of dry food or multiple cans of wet food daily,y depending on size and activity level, creating high volume consumption rates. This consistent usage pattern ensures that food remains the primary revenue driver for manufacturers and retailers alike. The sheer number of dogs in US households amplifies this effect,t with millions of pets requiring daily feeding. The recurrence of purchase cycles, typically every two to four weeks for dry food and weekly for fresh or canned options, generates reliable cash flow for industry participants. Brand loyalty is particularly strong in this category as owners hesitate to switch diets due to potential digestive issues,s further stabilizing market share for established players.

The pet nutraceuticals and supplements segment is expected to grow at the fastest CAGR of 8.1% from 2026 to 20,34 with the increasing focus on preventive healthcare and longevity for companion animals. Owners are proactively seeking solutions to support joint health, digestion,n immunity, and skin condition to avoid costly veterinary treatments later in life. The claims for chronic conditions such as arthritis and allergies are rising, ng prompting owners to invest in daily supplements like glucosamine, chondroitin, and probiotics. The humanization trend extends to health management, ent with owners applying their own wellness routines to their pets, including the use of vitamins and functional additives. Veterinary recommendations play a crucial role in this growth as professionals increasingly prescribe or recommend specific supplements to manage age-related issues. The availability of palatable forms such as chews and soft gels improves compliance, making it easier for owners to administer daily doses. The perception of supplements as essential rather than optional is shifting,g driving consistent recurring revenue for brands.

By Distribution Channel Insights

The supermarkets and hypermarkets segment was the largest by holding a dominant share of the US dog food market in 2025 due to their widespread presence and the convenience of one-stop shopping for household needs. Consumers prefer purchasing pet food alongside groceries to save time and reduce trips to multiple stores. The extensive network of these retailers ensures that dog food is accessible to a broad demographic across urban, suburban,n and rural areas. Competitive pricing and frequent promotions attract budget-conscious shoppers who prioritize value and availability. The ability to physically inspect products before purchase builds trust and allows for immediate acquisition without waiting for delivery. Private label brands offered by these retailers provide affordable alternatives that appeal to price-sensitive consumers. The consistent foot traffic in supermarkets ensures high visibility for dog food products on shelves.

The online channel segment is likely to register the fastest CAGR of 4.3% during the forecast period, with the convenience of home delivery and the popularity of subscription services. Busy consumers appreciate the ability to order heavy bags of food online and have them delivered directly to their doorsteps, eliminating the physical burden of transport. The e-commerce sales continue to rise across all categories, with pet supplies being a significant contributor due to the recurring nature of purchases. Subscription models offered by platforms like Chewy and Amazon provide automatic replenishment, ensuring that owners never run out of food, while often offering discounts for loyalty. The vast selection available online allows consumers to access niche and premium brands that may not be stocked in local stores. Detailed product descriptions and customer reviews help buyers make informed decisions,s enhancing trust in online purchases.

COMPETITIVE LANDSCAPE

The competitive landscape of the United States dog food market is characterized by intense rivalry among multinational conglomerates and agile niche brands that strive to differentiate through quality and specialization. Major competitors compete on factors such as ingredient transparency, nutritional science, and brand heritage rather than price alone due to the emotional connection owners have with their pets. The shift toward premiumization has intensified competition for high-value segments such as fresh frozen and holistic diets. Firms are increasingly investing in marketing and digital platforms to build direct relationships with consumers and gather data on preferences. Regulatory standards regarding labeling and safety shape competitive dynamics by favoring companies with robust quality control systems. Supply chain resilience has become a critical differentiator as disruptions highlight the importance of reliable sourcing and manufacturing capabilities. Collaborative efforts between manufacturers and retailers are becoming more common to secure shelf space and promote new products.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. Dog Food Market include

- Mars, Incorporated

- Nestlé Purina PetCare Company

- Hill’s Pet Nutrition, Inc.

- The J.M. Smucker Company

- Blue Buffalo Co., Ltd. (General Mills, Inc.)

- Freshpet, Inc.

- Diamond Pet Foods, Inc.

- WellPet LLC

- Champion Petfoods LP

- Merrick Pet Care, Inc.

- Natural Balance Pet Foods, Inc.

- Spectrum Brands Holdings, Inc.

TOP LEADING PLAYERS IN THE MARKET

- Mars Petcare US operates as a dominant force in the domestic dog food landscape, pe owning iconic brands such as Pedigree, ree Royal Canin, and Blue Buffalo. The company leverages its extensive manufacturing network and distribution capabilities to serve diverse consumer segments, from value-oriented to premium, specialized nutrition. Recent actions include significant investments in veterinary dietary solutions and the expansion of fresh food production facilities to meet growing demand for human-grade options. Mars focuses on personalized nutrition through digital platforms that offer tailored feeding recommendations based on individual pet profiles. Strategic acquisitions of emerging health-focused brands strengthen its portfolio against competitors. The company prioritizes sustainability initiatives within its supply chain to appeal to environmentally conscious consumers.

- Nestlé Purina PetCare maintains a strong presence in the US market through its broad portfolio of trusted brands, including Pro Plan,n PurinaOneOd Beneful. The company utilizes advanced research and development capabilities to create science-backed formulations that support specific life stages and health conditions. Recent initiatives focus on expanding its fresh and frozen food offerings through the Toppers and Just Right lines to capture the premiumization trend. Purina invests heavily in sustainable packaging innovations and responsible sourcing practices to enhance brand reputation. The company engages directly with veterinarians and breeders to promote evidence-based nutrition standards. Strategic partnerships with retail giants ensure widespread product availability and prominent shelf placement.

- General Mills Inc contributes significantly to the US dog food market primarily through its ownership of the Blue Buffalo brand, which pioneered the natural and holistic segment. The company focuses on delivering high-quality ingredients without artificial preservatives or by-product meals, appealing to health-conscious pet owners. Recent actions include the expansion of Blue Buffalo’s product line to include specialized formulas for sensitive stomachs and weight management. General Mills leverages its robust supply chain infrastructure to ensure consistent product quality and availability across retail channels. The company invests in marketing campaigns that emphasize transparency and ingredient sourcing to build consumer trust. Strategic collaborations with independent retailers and online platforms enhance market penetration.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States dog food market primarily employ strategies focused on product innovation and premiumization to maintain competitive advantages. Companies are increasingly investing in research and development to create specialized formulas, such as grain-free, limited-ingredient,t and fresh food options that cater to specific health needs. Strategic acquisitions of niche brands allow firms to expand their portfolios and reach diverse consumer segments quickly. Digital transformation initiatives enhance direct-to-consumer engagement through personalized nutrition platforms and subscription services. Sustainability efforts, including eco-friendly packaging and responsible sourcing,g appeal to environmentally conscious buyers. Partnerships with veterinarians and breeders validate product efficacy and build trust. These strategic moves collectively strengthen market positions by addressing economic health and ethical challenges inherent in the modern pet care industry landscape today.

MARKET SEGMENTATION

This research report on the U.S. dog food market is segmented and sub-segmented into the following categories.

By Pet Food Product

- Dry Dog Food

- Wet Dog Food

- Treats & Snacks

- Veterinary Diets

- Pet Nutraceuticals & Supplements

- Organic & Natural Dog Food

By Distribution Channel

- Supermarkets & Hypermarkets

- Specialty Pet Stores

- Online Channels

- Convenience Stores

- Veterinary Clinics

- Others

By Country

- California

- Texas

- Florida

- New York

- Rest of the United States

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com