U.S E-Coat Market Size, Share, Trends & Growth Forecast Report Segmented By Type (Cathodic Epoxy, Cathodic Acrylic, Anodic), Technology Type, Application, And Country (California, Washington, Oregon, New York & Rest Of The United States) – Industry Analysis And Forecast, 2026 To 2034

Market Size, 2025

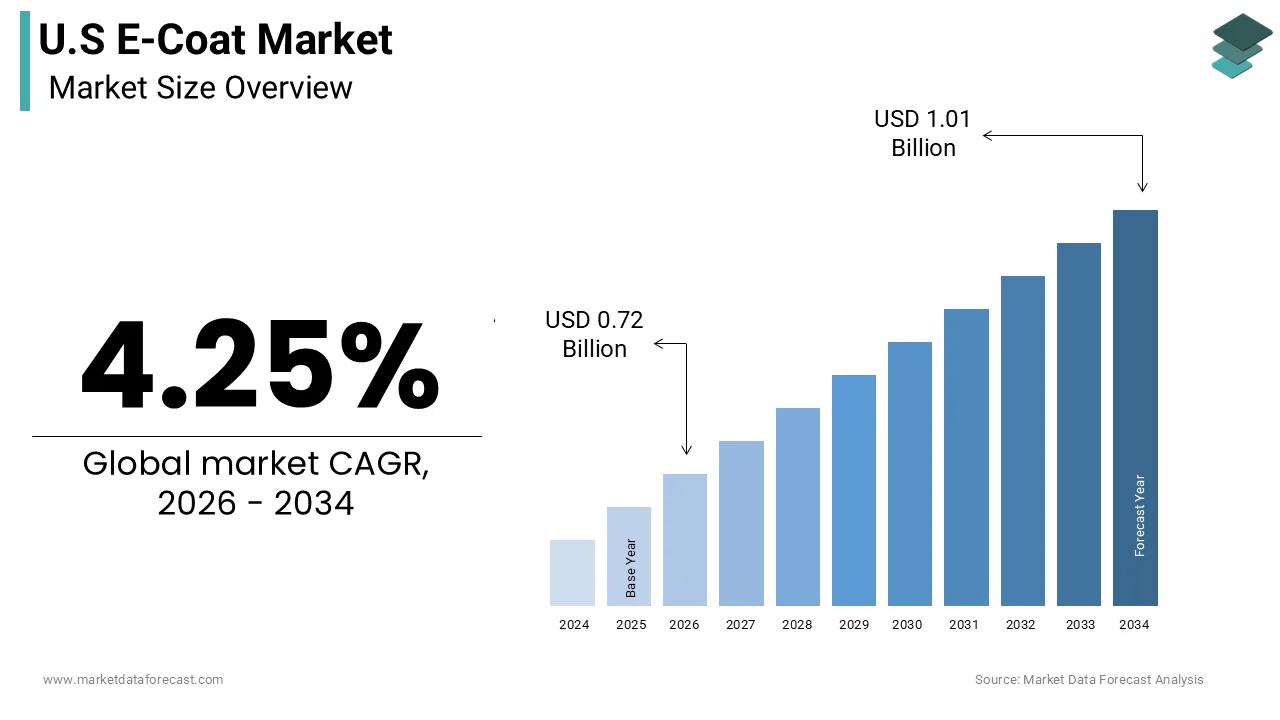

$0.69 BnMarket Estimate, 2026

$0.72 BnMarket Forecast, 2034

$1.01 BnCAGR, 2026–2034

4.25%U.S E-Coat Market Size

The U.S E-coat market size was calculated to be USD 0.69 billion in 2025 and is anticipated to be worth USD 1.01 billion by 2034, from USD 0.72 billion in 2026, growing at a CAGR of 4.25% during the forecast period.

The e-coat is the industrial application of electrocoating, a paint finishing process that utilizes electrical current to deposit organic coatings onto conductive surfaces. This technology is primarily employed for corrosion protection and aesthetic enhancement in high-volume manufacturing sectors, including automotive, aerospace, appliances, and heavy machinery. The process involves immersing parts in a water-based bath containing charged paint particles, which are attracted to the oppositely charged substrate, ensuring uniform coverage even in complex geometries and recessed areas. The adoption of water-based coating technologies has increased significantly, with e-coat representing a substantial portion of industrial finishes due to its low volatile organic compound emissions. The shift toward electric vehicles has further intensified the demand for advanced corrosion resistance as battery components and lightweight materials require specialized protective layers. According to the Department of Energy, the average lifespan of modern vehicles has extended to over 12 years, necessitating durable finishes that withstand harsh environmental conditions.

MARKET DRIVERS

Stringent Environmental Regulations And Volatile Organic Compound Limits

The implementation of stringent environmental regulations and limits on volatile organic compound emissions is majorly accelerating the growth of the United States e-coat market. Regulatory bodies, such as the Environmental Protection Agency, have established rigorous standards under the Clean Air Act to reduce hazardous air pollutants from industrial sources. The National Emission Standards for Hazardous Air Pollutants require major source facilities to reduce emissions by up to 90% compared to traditional solvent-based methods. This regulatory pressure drives manufacturers to adopt water-based electrocoating technologies, which emit significantly fewer volatile organic compounds. The push for green manufacturing practices also aligns with corporate sustainability goals, enhancing brand reputation. Manufacturers are investing in closed-loop systems that recycle rinse water and recover excess paint, further reducing environmental footprints. This regulatory framework ensures that ecoatt remains the preferred choice for industries seeking to balance productivity with ecological responsibility.

Growth Of The Automotive And Electric Vehicle Sectors

The robust growth of the automotive and electric vehicle sectors is attributed to the growth of the United States e-coat market. The transition toward electric mobility requires advanced corrosion protection for battery casings, chassis components, and lightweight aluminum structures. According to the Alliance for Automotive Innovation, electric vehicle sales in the United States are projected to account for 40% of new car sales by 2030. This shift drives demand for specialized eco-friendly formulations that offer superior adhesion and durability on diverse substrates. E coat provides uniform coverage essential for protecting intricate battery enclosures from moisture and salt corrosion. As per manufacturing trends, original equipment manufacturers are increasing production capacity to meet rising demand, leading to expanded coating facility investments. The complexity of electric vehicle architectures necessitates high-throughput power coatings that can penetrate deep into recessed areas. This structural change in vehicle design ensures sustained growth for the e-coat market. The emphasis on vehicle longevity and warranty performance further incentivizes the use of high-quality electrocoating.

MARKET RESTRAINTS

High Initial Capital Investment And Operational Costs

The substantial initial capital investment required for establishing e-coat facilities is hindering the growth of the United States e-coat market. Setting up an electrocoating line involves expensive infrastructure, including rectifiers, tanks, conveyors, ovens, and wastewater treatment systems. This high barrier to entry limits market participation to large corporations with significant financial resources. Small and medium-sized enterprises often struggle to justify these expenditures, despite the long-term benefits of improved corrosion resistance. The need for specialized technical expertise to manage bath chemistry and process parameters further adds to labor costs. The complexity of waste disposal and compliance with environmental regulations also imposes ongoing financial burdens. Facilities must invest in advanced filtration and recycling systems to meet discharge standards, increasing operational overhead.

Complexity Of Process Control And Maintenance Requirements

The technical complexity of process control and the rigorous maintenance requirements are inhibiting the growth of the United States-coat market. Maintaining consistent coating quality requires precise monitoring of bath parameters, such as pH, conductivity, temperature, and solid content. The deviations in these parameters can lead to defects, such as pinholes, roughness, roughnessss or poor adhesion. The need for continuous filtration and ultrafiltration to remove impurities adds to the operational burden. Skilled technicians are required to perform regular maintenance on rectifiers, pumps, and heat exchangers to prevent downtime. The sensitivity of the process to contamination from previous stages, such as cleaning and phosphating, necessitates strict quality assurance protocols. Training personnel to handle these complex systems requires significant time and resources. Furthermore, the disposal of sludge and spent bath solutions requires specialized handling to comply with environmental laws. These operational challenges deter some manufacturers from adopting Co-AT technology despite its performance benefits.

MARKET OPPORTUNITIES

Expansion Into Aerospace And Defense Applications

The expansion of e-coat technology into aerospace and defense applications is poised to pose as a major opportunity to bolster the growth of the United States e-coat market. These sectors demand exceptional corrosion resistance and durability for components exposed to extreme environmental conditions. E coat offers superior coverage for complex geometries found in aircraft structures and engine components. The ability of e coat to provide uniform thickness in recessed areas makes it ideal for intricate aerospace assemblies. Manufacturers are developing specialized formulations that meet military specifications for salt fog resistance and adhesion. The shift toward unmanned aerial vehicles and drones also creates new demand for lightweight protected structures. Collaborations between coating suppliers and aerospace primes facilitate the development of customized solutions. This strategic pivot allows e-coat providers to diversify beyond the automotive sector.

Development of Bio-Based and Sustainable Formulations

The development of bio-based and sustainable e coat formulations to align with evolving environmental standards is another attribute to drive the growth of the United States e coat market. Consumers and regulators are increasingly demanding products derived from renewable resources with reduced carbon footprints. Coating manufacturers are innovating with resins derived from plant oils and natural polymers to replace petroleum-based ingredients. The bio-based e-coats can reduce greenhouse gas emissions by up to 30% compared to conventional formulations. These eco-friendly options appeal to companies seeking to enhance their sustainability credentials and meet corporate social responsibility goals. The introduction of low-temperature cure e-coats also reduces energy consumption during the baking process. This innovation lowers operational costs and further minimizes environmental impact. Manufacturers that pioneer these green technologies can differentiate themselves in a competitive market. The opportunity extends to obtaining certifications such as USDA BioPreferred, which facilitates access to government contracts.

MARKET CHALLENGES

Fluctuation In Raw Material Prices And Supply Chain Disruptions

The substantial risks from fluctuations in raw material prices and global supply chain disruptions are a key challenge for the growth of the United States e-coat market. Key ingredients, such as epoxy, resins, acrylics, and pigments, are derived from petrochemical sources, which are subject to volatile market conditions. The reliance on international suppliers for specific additives exacerbates this issue as logistical hurdles delay shipments. These delays force manufacturers to hold higher inventory levels, tying up capital and increasing storage costs. Small and medium-sized enterprises are disproportionately affected as they lack the bargaining power to secure favorable contracts. The inability to pass these costs fully onto customers further squeezes profitability. Additionally, geopolitical tensions and trade policies can restrict access to critical materials. For instance, tariffs on imported chemicals add to production expenses. This financial pressure limits the ability of companies to invest in research and development. The unpredictability of input costs makes long-term planning difficult, forcing firms to adopt conservative growth strategies.

Competition From Alternative Coating Technologies

The intense competition from alternative coating technologies, such as powder coating and advanced liquid paints, offers distinct advantages in certain applications. The competition from alternative coating technologies is also inhibiting the growth of the United States e-coat market. Powder coating, for instance, provides thicker films and a wider range of aesthetic finishes without the need for solvents. Liquid spray coatings also remain popular for their flexibility and lower initial setup costs. The versatility of alternative technologies allows manufacturers to choose solutions that best fit their specific production needs. The continuous innovation in liquid coatings, such as water-borne high solids formulations, also challenges the dominance of e-coat. These alternatives often require less complex wastewater treatment systems, reducing operational burdens. The presence of viable substitutes limits the pricing power of the providers. Manufacturers must continuously demonstrate the unique benefits of electrocoating, such as uniform coverage and corrosion resistance, to retain customers.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.25% |

| Segments Covered | By Type, Technology Type, Application, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | PPG Industries, Axalta Coating Systems, Sherwin-Williams, BASF, Henkel, Nippon Paint Holdings, Kansai Paint, AkzoNobel, The Valspar Corporation, KCC Corporation, Covestro, Eastman Chemical Company, Hawking Electrotechnology Limited, PaintCoat Systems, AECI Industrial Chemicals |

SEGMENTAL ANALYSIS

By Type Insights

The cathodic epoxy segment was the largest by occupying 51.2% of the United States e-coat market share in 2025 due to its superior corrosion resistance and excellent adhesion properties on metal substrates. The exceptional corrosion resistance, which is essential for protecting vehicles and machinery from harsh environmental conditions, is also bolstering the growth of the segment. Cathodic epoxy coatings form a dense cross-linked network that acts as an effective barrier against moisture, salt, and chemicals. This performance exceeds that of anodic coatings and many alternative technologies. The automotive sector, which accounts for a large portion of e-coat consumption, relies heavily on cathodic epoxy to meet warranty requirements for rust prevention. The ability of cathodic epoxy to adhere strongly to steel and galvanized surfaces further enhances its appeal.

The cathodic acrylic segment is to grow at an anticipated CAGR of 5.8% during the forecast period with its superior UV stability and color retention capabilities, which are increasingly valued in exposed applications. Unlike epoxy coatings, which can chalk and degrade under sunlight, acrylics maintain their integrity and appearance over time. The automotive industry is also adopting acrylic primers for certain exterior components to enhance the overall finish quality. Cathodic acrylics provide a stable base that supports vibrant topcoats without compromising protection. The ability to formulate these coatings in various colors further adds to their versatility.

By Technology Type Insights

The epoxy coating segment accounted in holding 32.1% of the United States e-coat market share in 2025, with its status as an established industry standard with proven performance in critical applications. Automotive manufacturers have relied on epoxy coatings for decades to protect vehicle bodies from corrosion. This widespread adoption creates a stable and consistent demand for epoxy technologies. Data from historical performance records show that epoxy-coated vehicles exhibit significantly lower corrosion rates compared to those with alternative primers. The reliability of epoxy systems in meeting stringent industry specifications reinforces their continued use. The extensive knowledge base and technical support available for epoxy formulations further reduce implementation risks. Manufacturers are confident in the predictable outcomes of epoxy processes, which minimize production disruptions. The long-term validation of this technology ensures that it remains the default choice for new facilities. The inertia of existing infrastructure and trained personnel also supports its leadership. This entrenched position makes it difficult for newer technologies to displace epoxy in high-volume applications.

The acrylic coating technology segment is expected to register the fastest CAGR of 5.5% from 2026 to 2034, with the increasing demand for aesthetic quality and UV resistance in visible applications. Data from product testing shows that acrylic e-coats retain their visual properties longer than epoxies when exposed to outdoor conditions. Manufacturers are responding by switching to acrylic technologies to enhance product appeal. The ability to produce colored primers further adds value by reducing the number of topcoat layers required. This efficiency appeals to producers seeking to streamline operations. The versatility of acrylics in matching diverse design trends ensures their relevance. The growing emphasis on visual appeal in industrial products drives the adoption of acrylic technology.

By Application Insights

The passenger cars segment held a dominant share of the United States e coat market in 2025 with the high volume of vehicle production and strict regulatory standards for durability. According to the Alliance for Automotive Innovation, over 10 million passenger vehicles are produced annually in North America. Each of these vehicles requires a comprehensive e-coat application to meet federal safety and longevity expectations. Data from the Environmental Protection Agency mandates that vehicles must resist corrosion for extended periods to reduce waste and environmental impact. The scale of automotive manufacturing ensures consistent demand for e-coat materials. The integration of e-coat into automated assembly lines allows for efficient, high-speed application. This operational efficiency supports the massive throughput of car factories. The reliance on e-coat for structural integrity makes it indispensable. The sheer number of units produced sustains the leadership of this segment.

The automotive parts segment is expected to grow at the fastest CAGR of 6.2% during the forecast period, with the trend toward outsourcing component manufacturing to specialized suppliers. Original equipment manufacturers are increasingly relying on tier one and tier two suppliers for pre-coated parts. Suppliers are investing in dedicated e-coat lines to meet quality standards. The need for consistent corrosion protection across the supply chain drives this growth. The modular assembly approach requires parts to be protected before final integration. This shift increases the volume of parts processed through EE-coat facilities. The specialization of suppliers allows for higher efficiency and quality control. The expansion of the supplier network supports the rapid growth of this segment.

COMPETITION OVERVIEW

The competition in the United States e-coat market is intense and characterized by a mix of established global chemical giants and specialized regional providers. Large companies leverage their extensive resources to dominate through broad distribution networks and heavy investment in research and development. They continuously innovate to maintain relevance and protect their market positions against newer entrants. Independent suppliers often differentiate themselves by focusing on niche segments, such as specialized industrial coatings or custom formulation services. These smaller entities utilize personalized customer service to build strong relationships and foster loyalty. The barrier to entry is high due to the significant capital required for facility setup and regulatory compliance. Price competition is prevalent in standard applications, while premium brands compete on performance and sustainability credentials. Original equipment manufacturers play a crucial role by setting stringent quality standards that dictate supplier selection. Private label offerings are less common due to the technical complexity of e-coat formulations.

KEY MARKET PLAYERS

A few major players of the U.S E-coat market include

- PPG Industries

- Axalta Coating Systems

- Sherwin-Williams

- BASF

- Henkel

- Nippon Paint Holdings

- Kansai Paint

- AkzoNobel

- The Valspar Corporation

- KCC Corporation

- Covestro

- Eastman Chemical Company

- Hawking Electrotechnology Limited

- PaintCoat Systems

- AECI Industrial Chemicals

Top Strategies Used by Key Market Participants

Key players in the United States e-coat market employ several strategic initiatives to maintain competitiveness and drive growth. Product innovation remains a primary strategy with companies investing heavily in research and development to create low-energy and bio-based formulations. Brands frequently introduce items featuring enhanced corrosion resistance and UV stability to meet evolving industry standards. Digital transformation is another critical approach as firms implement smart manufacturing tools to optimize production efficiency. Companies utilize data analytics to monitor bath chemistry and predict maintenance needs. Strategic collaborations with automotive manufacturers help build credibility and customize solutions effectively. Sustainability initiatives are increasingly prominent, with firms adopting circular economy practices and reducing volatile organic compound emissions. Expansion into emerging sectors, such as electric vehicles, allows brands to capture new revenue streams. These multifaceted strategies enable market participants to adapt to regulatory changes and sustain long-term success in the dynamic industry landscape.

Leading Players in the United States E Coat Market

- PPG Industries Inc maintains a leading position in the United States e-coat market through its comprehensive portfolio of protective and marine coatings. The company serves diverse sectors, including automotive, aerospace, and general industrial applications, with advanced electrocoating solutions. Recent strategic initiatives include the development of low-temperature cure e-coats that reduce energy consumption for manufacturers. PPG actively invests in research and development to create bio-based formulations that align with sustainability goals. The corporation enhances its customer support by offering technical consulting and process optimization services. Its global supply chain ensures consistent product availability and quality.

- Axalta Coating Systems Ltd serves as a major player in the United States e-coat sector, specializing in high-performance liquid and powder coatings. The company leverages its strong presence in the automotive original equipment manufacturer market to drive demand for its electrocoating products. Recent actions to strengthen its position include the launch of next-generation cathodic epoxy primers with improved corrosion resistance. Axalta focuses on digital transformation by implementing smart manufacturing technologies to enhance production efficiency. The corporation collaborates closely with automakers to develop customized coating solutions for electric vehicle components. It emphasizes sustainability by reducing volatile organic compound emissions in its formulations. Axalta also expands its service network to provide faster response times and technical support.

- BASF SE holds a significant share in the United States e-coat market through its extensive chemical expertise and integrated production capabilities. The company offers a wide range of electrocoating materials designed for superior adhesion and durability. Recent strategies to strengthen its market position include the introduction of lightweight coating systems that support fuel efficiency in vehicles. BASF invests heavily in sustainable chemistry by developing raw materials from renewable resources. The corporation partners with industry leaders to create closed-loop recycling systems for coating processes. It focuses on operational excellence by optimizing supply chain logistics and reducing carbon footprints. BASF also provides comprehensive training programs for customers to ensure optimal application results.

MARKET SEGMENTATION

This research report on the US E-Coat market has been segmented and sub-segmented based on type, technology type, application & region.

By Type

- Cathodic Epoxy

- Cathodic Acrylic

- Anodic

By Technology Type

- Epoxy Coating Technology

- Acrylic Coating Technology

By Application

- Passenger Cars

- Commercial Vehicles

- Automotive Parts

- Heavy-Duty Equipment

By Region

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

1. What is the projected growth rate of the U.S. E-Coat market?

The market is expected to grow steadily during the forecast period due to increasing industrial production, rising vehicle manufacturing, and growing demand for corrosion-resistant coatings.

2. What are the key factors driving the growth of the U.S. E-Coat market?

Major growth drivers include expanding automotive production, stringent environmental regulations, increased use of advanced coating technologies, and growing demand for durable metal protection solutions.

3. Which industries are the major end-users of E-Coat in the United States?

Key end-users include automotive, construction, heavy equipment, appliances, aerospace, and industrial manufacturing sectors.

4. What are the main types of E-Coat used in the market?

The market primarily consists of cathodic E-Coat and anodic E-Coat systems, with cathodic E-Coat being the dominant technology due to its superior corrosion resistance.

5. Why is cathodic E-Coat more widely used than anodic E-Coat?

Cathodic E-Coat offers better corrosion protection, longer coating life, and improved performance in harsh environmental conditions, making it the preferred choice for automotive and industrial applications.

6. What role does the automotive industry play in the U.S. E-Coat market?

The automotive industry is the largest consumer of E-Coat technology, using it extensively for vehicle bodies, chassis components, and metal parts to enhance durability and corrosion protection.

7. What challenges are faced by E-Coat manufacturers in the United States?

Manufacturers face challenges such as fluctuating raw material prices, high equipment installation costs, energy consumption, and increasing competition from alternative coating technologies.

8. Which distribution channels are commonly used in the E-Coat market?

Direct sales to OEMs, industrial manufacturers, coating service providers, and authorized distributors are the primary distribution channels in the market.

9. What technological advancements are shaping the future of E-Coat solutions?

Advancements include improved resin technologies, enhanced energy-efficient coating processes, smart coating systems, automation, and environmentally sustainable formulations.

10. What are the future opportunities in the U.S. E-Coat market?

Future opportunities include increasing electric vehicle production, infrastructure development projects, demand for lightweight metal components, and the adoption of advanced industrial coating technologies.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com