U.S. EdTech Market Size, Share, Trends & Growth Forecast Report Segmented By Product Type (Hardware, Software, Content), Application and Country – Industry Analysis From 2026 to 2034

U.S. EdTech Market Report Summary

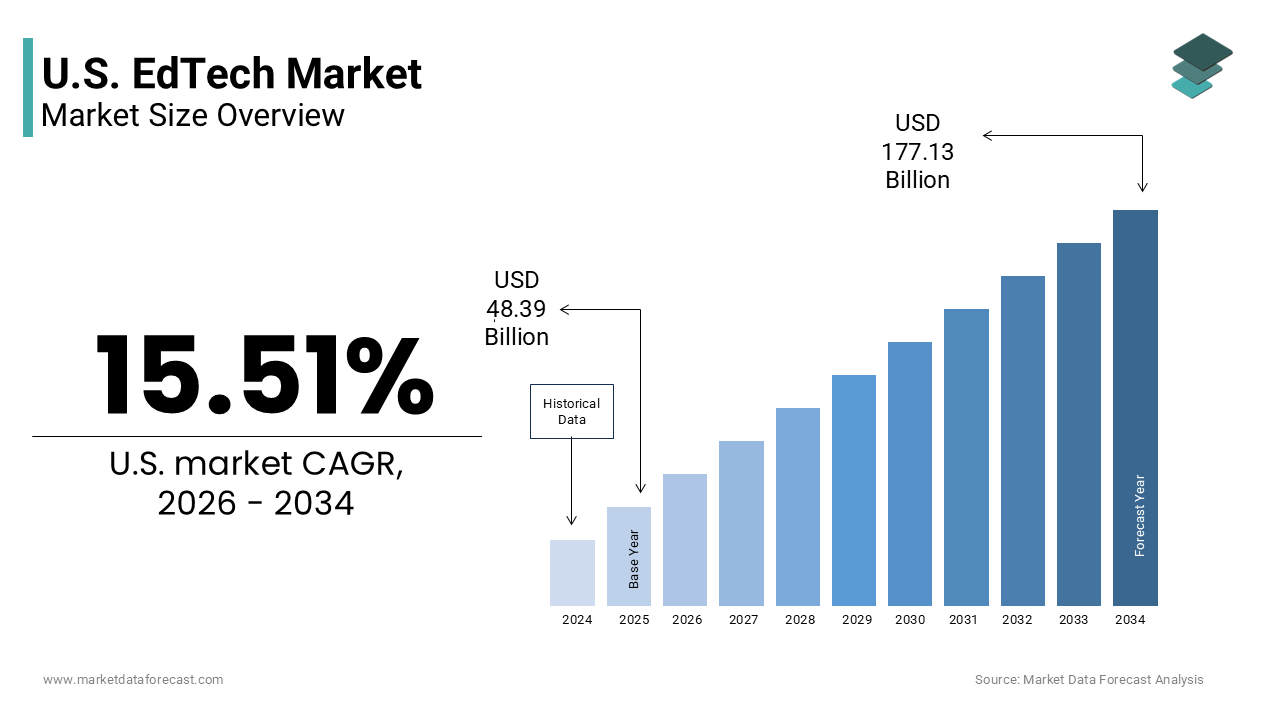

The U.S. EdTech market was valued at USD 48.39 billion in 2025, is estimated to reach USD 55.89 billion in 2026, and is projected to reach USD 177.13 billion by 2034, growing at a CAGR of 15.51% during the forecast period from 2026 to 2034. The growth of the U.S. EdTech market is driven by the increasing digital transformation in education, rising adoption of personalized learning platforms, and strong government support for technology-enabled learning infrastructure. The growing demand for adaptive learning systems, AI-powered tutoring solutions, and online skill development platforms is further accelerating market growth. Additionally, the expansion of hybrid learning models, increasing investments in digital education tools, and rising emphasis on workforce-oriented learning programs are strengthening the adoption of EdTech solutions across the United States.

Key Market Trends

- Rising adoption of AI-powered personalized learning and adaptive education platforms across K-12 and higher education institutions

- Increasing demand for online upskilling, microcredential, and workforce-oriented learning programs

- Growing use of cloud-based learning management systems and digital classroom solutions in schools and universities

- Strong focus on digital equity, broadband expansion, and universal device accessibility in public education

- Expansion of generative AI tools for tutoring, curriculum development, and automated assessment systems

Segmental Insights

- Based on product type, the software segment held the largest share of the U.S. EdTech market in 2025. The segment’s dominance is attributed to the increasing adoption of cloud-based learning management systems, virtual classroom platforms, adaptive assessment software, and data analytics tools that support personalized and scalable learning experiences.

- The content segment is projected to witness strong growth during the forecast period owing to the rising demand for standards-aligned digital curricula, AI-curated educational content, and interactive learning materials tailored to evolving educational requirements.

- Based on application, the K-12 segment dominated the U.S. EdTech market in 2025 due to the large-scale deployment of digital learning tools, widespread device distribution programs, and increasing integration of technology into classroom instruction and standardized assessments.

- The higher education segment is anticipated to grow at a notable pace during the forecast period owing to the rising adoption of online degree programs, AI-enabled student support systems, and workforce-aligned microcredential and upskilling platforms.

Regional Insights

The U.S. EdTech market is witnessing robust growth across California, Washington, Oregon, New York, and the rest of the United States, supported by the strong digital infrastructure, high institutional adoption of educational technologies, and increasing investments in AI-enabled learning ecosystems. California remains one of the leading regional markets owing to its concentration of technology companies, strong venture capital ecosystem, and early adoption of innovative digital learning solutions across educational institutions.

Competitive Landscape

The U.S. EdTech market is highly competitive and characterized by the presence of global technology companies, digital learning platforms, learning management system providers, and AI-driven educational solution developers competing through innovation, scalability, and personalized learning capabilities. Companies are increasingly focusing on AI integration, cloud-based learning environments, interoperability, workforce-oriented education, and data-driven instructional tools to strengthen their market position and improve learning outcomes. Prominent players in the U.S. EdTech market include Coursera Inc., Udemy Inc., Duolingo Inc., BYJU'S, Pearson plc, Blackboard Inc., Instructure Inc., Google LLC, Microsoft Corporation, 2U Inc., Chegg Inc., and Khan Academy.

U.S. EdTech Market Size

The U.S. EdTech Market size was valued at USD 48.39 billion in 2025 and is anticipated to reach USD 55.89 billion in 2026 from USD 177.13 billion by 2034, growing at a CAGR of 15.51% during the forecast period from 2026 to 2034.

According to the National Center for Education Statistics, over 96% of public schools in the United States provided students with school-issued devices in 2023, reflecting deep institutional integration of technology. As per the Federal Communications Commission, approximately 74% of school districts now meet the updated short-term benchmark of 1 Gbps per 1,000 students and staff, marking a significant advancement in high-speed connectivity. Furthermore, according to the Bureau of Labor Statistics, employment of instructional coordinators is projected to grow 1% from 2024 to 2034, which is slower than the average for all occupations. The Department of Education emphasizes that digital literacy is now embedded in state academic standards across 48 states, underscoring the systemic role of technology in modern pedagogy. This ecosystem continues to evolve in response to equity mandates, workforce readiness demands, and advances in artificial intelligence.

MARKET DRIVERS

Federal and State Funding Initiatives Accelerate Institutional EdTech Adoption

Sustained public investment through federal and state programs has significantly catalyzed EdTech deployment across U.S. educational institutions, which is a key factor propelling the growth of the U.S. EdTech market. The Elementary and Secondary School Emergency Relief Fund allocated over 190 billion dollars between 2020 and 2023, and as per the National Conference of State Legislatures, these funds provided critical support for equitable access to technology and broadband expansion across various states. Additionally, the Every Student Succeeds Act mandates that states allocate a portion of Title IV funds to support well-rounded education and digital learning, with forty-two states increasing their EdTech budgets by an average of 22% in 2023. These funds enabled schools to procure learning management systems, upgrade Wi-Fi networks, and train educators in digital pedagogy. The Government Accountability Office observes that districts receiving ESSER funding were three times more likely to implement data-driven instructional tools by 2023. This public financing not only bridges the digital divide but also creates predictable demand cycles that empower EdTech vendors to innovate with institutional scale in mind.

Rising Demand for Personalized and Competency Based Learning Models

Educators and administrators are increasingly adopting EdTech solutions that enable personalized and competency-based learning to address diverse student needs and improve outcomes, which is further contributing to the U.S. market expansion. According to the National Center for Education Statistics, 73% of public school teachers used adaptive learning software at least weekly in 2023 to tailor instruction based on real-time student performance data. Platforms that adjust content difficulty provide immediate feedback and identify learning gaps have demonstrated measurable efficacy, and as per a systematic review in Frontiers in Computer Science, AI-driven adaptive learning systems can significantly enhance mathematical performance and conceptual understanding across primary and secondary settings. The Department of Education’s National Education Technology Plan emphasizes mastery-based progression as a core principle driving adoption. Furthermore, according to the College Board, approximately 84% of high school students reported using generative AI for schoolwork tasks such as brainstorming and revising essays by late 2025. As accountability pressures mount and class sizes remain large, technology offers a scalable mechanism to deliver individualized support while maintaining rigorous academic standards.

MARKET RESTRAINTS

Persistent Digital Equity Gaps Limit Universal Access and Efficacy

Despite widespread device distribution, significant disparities in home internet access and digital literacy continue to undermine the effectiveness of EdTech across socioeconomic lines, which is a primary restraint to the U.S. market growth. According to the National Telecommunications and Information Administration, approximately 14 million school-age children in the United States still lack reliable high-speed internet at home, particularly in rural and low-income urban communities. As per the U.S. Census Bureau, approximately 95% of households with an annual income of $150,000 or more have a broadband subscription, while this rate drops significantly for lower-income households. This connectivity gap translates into learning loss, with the Department of Education documenting that students without home internet were twice as likely to fall behind in digital assignments during the 2022 to 2023 school year. Additionally, the National Center for Education Statistics finds that teachers in high-poverty schools are 30% less likely to receive adequate training in EdTech integration. Until universal access and professional development are achieved, EdTech risks exacerbating rather than alleviating educational inequity.

Fragmented Procurement Processes and Budget Constraints in Public Schools

The decentralized nature of U.S. public education creates significant barriers to consistent EdTech adoption due to fragmented decision-making and cyclical funding limitations, which is further hindering the U.S. market expansion. According to the Government Accountability Office, procurement authority for digital tools is distributed across over 13,000 independent school districts, each with its own budget cycle, curriculum priorities, and approval protocols. The National School Boards Association reports that the average district evaluates over twenty EdTech vendors annually but implements fewer than three due to compatibility concerns and limited technical support capacity. Furthermore, the Bureau of Labor Statistics notes that per pupil spending on instructional technology plateaued at 280 dollars in 2023 after post-pandemic spikes, highlighting fiscal constraints. The expiration of federal emergency relief funds has intensified this pressure, with the Education Commission of the States observing that thirty-seven states reduced EdTech line items in their 2024 education budgets. This environment discourages long-term platform investment and favors short-term, low-cost solutions that often lack interoperability or pedagogical depth.

MARKET OPPORTUNITIES

Integration of Generative AI for Real Time Tutoring and Curriculum Development

The incorporation of generative artificial intelligence into EdTech platforms offers a promising opportunity for the U.S. EdTech market. According to the National Institute of Standards and Technology, over 45% of U.S. school districts piloted AI-powered tutoring tools in 2023, with early results showing a 30% reduction in time spent on routine grading and lesson planning. These systems can generate customized practice problems, provide instant feedback on open-ended responses, and adapt explanations based on student misconceptions. As per a systematic review, AI-driven tools such as chatbots and intelligent tutoring systems hold meaningful potential for strengthening mathematics instruction by providing tailored feedback and adaptive challenges. Platforms like Khanmigo and Duolingo Max are already embedding large language models to simulate Socratic dialogue and scaffold critical thinking. As AI becomes more accurate and ethically governed, it can democratize access to high-quality tutoring, particularly in underserved subjects like advanced mathematics and computer science.

Expansion of Workforce Aligned Microcredential and Upskilling Platforms

The growing misalignment between academic preparation and labor market demands is fueling demand for EdTech solutions that deliver industry-recognized microcredentials and just-in-time upskilling, which is another prominent opportunity for the U.S. market. As per a survey of the workforce landscape, nearly every profession will require employees to have a basic level of technical expertise and digital skills by 2026. In response, EdTech providers are partnering with community colleges and employers to offer stackable credentials in cybersecurity, data analytics, and AI literacy. The U.S. Department of Commerce notes that enrollment in online microcredential programs grew by 41% in 2023, with corporate sponsorship covering costs for over half of participants. Platforms like Coursera and Guild Education integrate labor market data to recommend learning pathways aligned with local job openings. The National Governors Association reports that twenty-eight states have launched statewide upskilling initiatives using EdTech to close talent gaps in emerging sectors. This convergence of education and employment creates a sustainable revenue model beyond traditional institutional sales.

MARKET CHALLENGES

Escalating Data Privacy and Security Concerns Erode Institutional Trust

The collection and processing of sensitive student data by EdTech platforms have triggered growing scrutiny from parents, regulators, and school administrators, which is likely to challenge the U.S. EdTech market expansion. According to the Federal Trade Commission, high-profile cases involving companies like Illuminate Education and Disney were finalized in late 2025, highlighting ongoing enforcement regarding children's online privacy and data security. As per the Cybersecurity and Infrastructure Security Agency, hundreds of K-12 school districts were notified of pre-ransomware threats as of late 2024, emphasizing the persistent vulnerability of student information systems to cyberattacks. The Department of Education’s Student Privacy Policy Office notes that only 42% of districts conduct comprehensive data privacy audits before adopting new tools. High-profile breaches have intensified skepticism across the sector. Until vendors adopt transparent data governance frameworks and comply with state-specific regulations, trust in digital learning tools will remain fragile, particularly among privacy-conscious communities.

Teacher Resistance and Insufficient Professional Development Hinder Effective Implementation

Despite technological advancements, many educators remain hesitant to integrate EdTech due to inadequate training time and misalignment with instructional goals, which is further challenging the U.S. EdTech market growth. According to the National Center for Education Statistics, only 39% of teachers reported receiving more than ten hours of EdTech professional development in 2023, far below the twenty-five hours recommended by the International Society for Technology in Education for effective adoption. As per the Bureau of Labor Statistics, employment for instructional coordinators is projected to grow by only 1% through 2034, which may limit the availability of specialists who support teachers in digital implementation. Moreover, the RAND Corporation reports that 61% of educators feel EdTech tools are selected by administrators without classroom input, leading to low utilization. When platforms are not seamlessly integrated into lesson planning or fail to reduce workload, they become burdens rather than enablers. Sustainable EdTech success requires co-design with teachers, ongoing coaching, and recognition of pedagogical autonomy rather than top-down technology mandates.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 15.51% |

| Segments Covered | By Product Type, Application, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, and the rest of the United States. |

| Market Leader Profiled | Coursera Inc., Udemy Inc., Duolingo Inc., BYJU'S, Pearson plc, Blackboard Inc., Instructure Inc., Google LLC, Microsoft Corporation, 2U Inc., Chegg Inc., and Khan Academy |

SEGMENTAL ANALYSIS

By Product Type Insights

The software segment held 52.5% of the U.S. EdTech market share in 2025. The dominance of software segment in the U.S. market is driven by the shift toward cloud-based learning management systems, adaptive assessment platforms, and data analytics tools that enable personalized instruction at scale. The institutional mandate for interoperability and data-driven decision-making is further contributing to the dominance of software segment in the U.S. market. According to the U.S. Department of Education, over 85% of public school districts now require EdTech vendors to comply with interoperability standards to ensure seamless integration with student information systems. Additionally, the post-pandemic emphasis on hybrid learning has accelerated adoption of virtual classroom and collaboration software. The Federal Communications Commission reports that 91% of districts renewed or expanded their learning management system licenses in 2023. Software also offers recurring revenue models through subscription licensing, which aligns with predictable district budgeting cycles. As per the Bureau of Labor Statistics, spending on instructional software grew by 12.4% in 2023, reflecting its central role in modern pedagogy and assessment.

However, the content segment is on the rise and is estimated to expand at a CAGR of 17.4% during the forecast period in the U.S. market owing to the rising demand for standards-aligned digital curricula that support diverse learners and emerging academic priorities. According to the National Governors Association, 36 states adopted new science or computer science standards between 2021 and 2023, requiring updated instructional materials. In response, publishers have digitized and modularized content, allowing teachers to customize lessons by student need or language proficiency. The Department of Education’s Office of Educational Technology notes that districts using AI-curated open educational resources reduced curriculum procurement costs by up to 40% while improving alignment with state benchmarks. Additionally, the rise of social-emotional learning has spurred demand for digital SEL modules, with district adoption of evidence-based digital SEL content increasing significantly in 2023. As states mandate media literacy, climate education, and AI literacy, the market for agile, updatable digital content continues to expand rapidly.

By Application Insights

The K-12 segment dominated the market by accounting for 60.6% of the U.S. market share in 2025. The growth of the K-12 segment in the U.S. market is driven by the federal and state mandates for universal device access, standardized assessment, and digital literacy integration across public education. The Elementary and Secondary School Emergency Relief Fund allocated over 65 billion dollars specifically for K-12 technology between 2020 and 2023, according to the U.S. Department of Education, with funds used for devices, connectivity, and instructional software. Additionally, as per the National Conference of State Legislatures, annual statewide assessments are now administered digitally in nearly all states. The Federal Communications Commission notes that approximately 74% of school districts now meet the updated high-speed broadband goal of 1 Gbps per 1,000 users. Furthermore, according to the Bureau of Labor Statistics, there are approximately 3.8 million public school teachers in the U.S. who serve as primary users of EdTech tools, creating a vast and stable adoption base. These structural and regulatory factors ensure K-12 remains the core engine of the U.S. EdTech ecosystem.

On the other side, the higher education segment is predicted to witness a promising CAGR of 12.5% during the forecast period in the U.S. market owing to the convergence of workforce alignment, enrollment pressures, and AI integration in post-secondary institutions. As per the National Center for Education Statistics, a majority of colleges now offer microcredential programs in partnership with EdTech platforms to address shifting enrollment trends. As per a survey of employer requirements, nearly every profession will necessitate digital expertise and basic AI tool proficiency by 2026, driving student demand for stackable credentials. Additionally, generative AI has transformed teaching, and as per the College Board, nearly three-quarters of college faculty report that students are utilizing AI for essay writing and paraphrasing by 2026. Institutions are also investing in predictive analytics to improve retention, with early alert systems reducing dropout rates in first-year cohorts. As higher education redefines its value proposition, EdTech becomes central to innovation, affordability, and relevance.

COUNTRY ANALYSIS

The United States is projected to experience continued high institutional adoption and technological innovation within its EdTech sector over the next few years. As per the National Center for Education Statistics, over 96% of U.S. public schools provide students with school-issued devices, creating one of the world’s most digitized K-12 environments. A key driver is sustained public funding, with the U.S. Department of Education allocating over 190 billion dollars in emergency relief between 2020 and 2023, nearly 35% of which supported technology infrastructure. According to the Federal Communications Commission, approximately 74% of school districts now meet national broadband connectivity benchmarks of 1 Gbps per 1,000 users, enabling consistent digital learning. Furthermore, as per the Bureau of Labor Statistics, employment for instructional coordinators is projected to reach approximately 235,500 jobs by 2034. With strong venture capital activity, mission-driven startups, and policy alignment around digital equity, the United States remains the global epicenter of EdTech innovation, scale, and impact.

COMPETITIVE LANDSCAPE

Competition in the U.S. EdTech market is highly fragmented yet intensifying with thousands of vendors vying for attention across K 12 higher education and corporate learning segments. The landscape features a mix of established learning management systems agile startups and tech giants entering adjacent spaces. Differentiation hinges on pedagogical efficacy data privacy compliance interoperability and ease of teacher adoption rather than just features. Large players like Canvas and Google Classroom dominate infrastructure while niche providers compete on subject specific depth or AI innovation. Budget constraints and decentralized procurement create high barriers to scale yet also allow specialized solutions to thrive in targeted use cases. Trust is paramount with data breaches or algorithmic bias triggering swift backlash from parents and regulators. The expiration of federal emergency funding has intensified price sensitivity pushing vendors toward sustainable business models. Ultimately success requires balancing technological sophistication with educator input equitable design and demonstrable learning impact in a mission driven yet increasingly commercialized sector.

KEY MARKET PLAYERS

A few of the major companies in the U.S. EdTech Market include

- Coursera Inc.

- Udemy Inc.

- Duolingo Inc.

- BYJU'S

- Pearson plc

- Blackboard Inc.

- Instructure Inc.

- Google LLC

- Microsoft Corporation

- 2U Inc.

- Chegg Inc.

- Khan Academy

Top Players in the Market

Canvas by Instructure

Canvas by Instructure is a leading learning management system widely adopted across K 12 districts community colleges and universities throughout the United States. The platform serves as a central hub for course delivery assessment collaboration and analytics enabling seamless hybrid and remote learning experiences. Globally Canvas supports over thirty million users in more than eighty countries powering digital education in diverse institutional contexts. In recent years Instructure has strengthened its position by integrating artificial intelligence features such as automated grading suggestions and predictive course analytics. It also enhanced interoperability through compliance with OneRoster and LTI standards ensuring smooth data exchange with student information systems. The company launched Canvas Studio to support video based learning and expanded its mobile capabilities to improve accessibility. These innovations reinforce Canvas as a scalable secure and educator centric platform in an evolving digital learning landscape.

Khan Academy

Khan Academy is a nonprofit EdTech pioneer offering free high quality instructional content and personalized learning tools in mathematics science and humanities to students and teachers across the United States and worldwide. Its platform reaches over one hundred million learners globally and is integrated into curricula in thousands of U.S. schools. Khan Academy has significantly advanced equitable access by providing standards aligned resources in multiple languages with offline functionality for low connectivity environments. Recently the organization launched Khanmigo an AI powered teaching assistant that provides real time tutoring and lesson planning support while adhering to strict student privacy protocols. It also partnered with school districts to embed its mastery based learning model into daily instruction. These initiatives underscore Khan Academy’s mission to deliver world class education to anyone anywhere while setting benchmarks for ethical AI in education.

Chegg Inc

Chegg Inc operates a comprehensive suite of student support services including textbook rentals homework help writing assistance and career guidance tailored to higher education learners in the United States and internationally. The company plays a critical role in bridging academic gaps by offering on demand expert tutoring and study resources aligned with college curricula. Globally Chegg serves millions of students across North America Europe and Asia through localized content and adaptive learning tools. In response to evolving student needs Chegg has integrated generative AI into its platform to provide step by step explanations while maintaining academic integrity safeguards. It also expanded its internship and job matching services to connect learners with employers. Additionally Chegg strengthened data privacy measures to comply with evolving regulations and rebuild trust after past security concerns. These actions position Chegg as a holistic academic and career success partner for the modern student.

Top Strategies Used by the Key Market Participants

Key players in the U.S. EdTech market prioritize deep integration with school district data systems through compliance with interoperability standards like OneRoster and LTI to ensure seamless adoption. They embed artificial intelligence for personalized tutoring automated grading and predictive analytics while implementing strict student privacy safeguards. Companies form strategic partnerships with state education agencies and school districts to align content with academic standards and procurement cycles. Nonprofit and for profit entities alike invest in multilingual and offline capable platforms to address digital equity gaps. They expand beyond core products into adjacent services such as career readiness mental health support and teacher professional development to increase institutional stickiness. Subscription and freemium models are optimized for both district wide licensing and individual student affordability. Finally firms actively engage in policy advocacy and participate in federal grant programs to shape the regulatory and funding environment.

MARKET SEGMENTATION

This research report on the U.S. EdTech Market has been segmented based on the following categories.

By Product Type

- Hardware

- Software

- Content

By Application

- Preschool

- K-12

- Higher Education

- Others

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com