U.S. Electric Vehicle Market Size, Share, Trends & Growth Forecast Report Segmented By Vehicle Type (Passenger Car, Commercial Vehicle), Propulsion Type, Drive Type, Range, Component and Country – Industry Analysis From 2026 to 2034

U.S. Electric Vehicle Market Report Summary

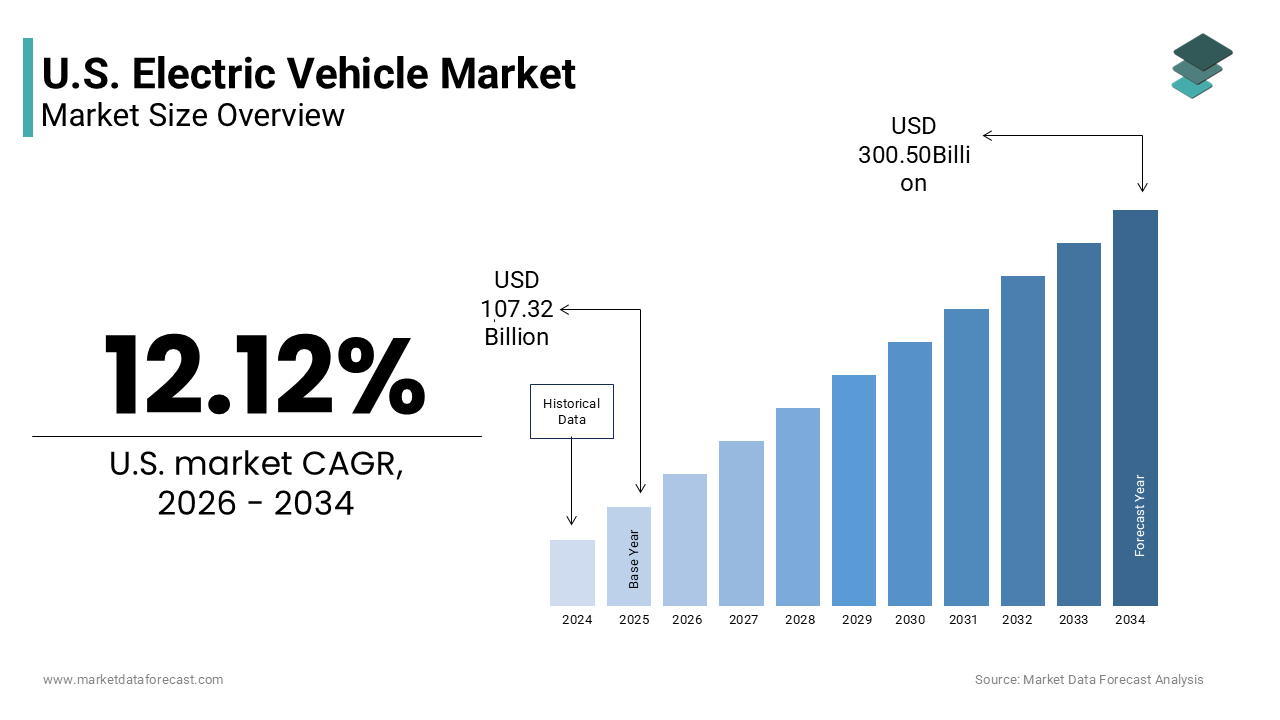

The U.S. electric vehicle market was valued at USD 107.32 billion in 2025, is estimated to reach USD 120.33 billion in 2026, and is projected to reach USD 300.50 billion by 2034, growing at a CAGR of 12.12% during the forecast period from 2026 to 2034. The growth of the U.S. electric vehicle market is driven by federal incentives, advancements in battery technology, and expanding charging infrastructure. Additionally, increasing environmental concerns, regulatory mandates, and the shift toward sustainable mobility are further accelerating market growth.

Key Market Trends

- Strong rise in battery electric vehicle (BEV) adoption due to zero-emission benefits

- Expansion of charging infrastructure networks across highways and urban areas

- Increasing focus on vehicle-to-grid (V2G) technology and energy integration

- Growing demand for electric commercial vehicles and fleet electrification

- Rising investments in battery innovation and domestic supply chain development

Segmental Insights

- Based on vehicle type, the passenger car segment was the largest and held a significant share of the U.S. electric vehicle market in 2025. The segment’s dominance is attributed to the wide availability of EV models, strong consumer adoption, and government incentives targeting individual buyers.

- Based on propulsion type, the battery electric vehicle (BEV) segment accounted for the largest share, driven by advancements in battery efficiency, lower maintenance costs, and increasing consumer preference for fully electric mobility.

- Based on drive type, the all-wheel drive segment dominated the market, supported by consumer demand for enhanced performance, safety, and traction across diverse weather conditions.

- Based on component, the battery pack and high voltage segment was the largest, due to the critical role of batteries in determining vehicle cost, performance, and driving range.

Regional Insights

The U.S. electric vehicle market is witnessing strong growth across regions such as California, New York, Washington, and other states, supported by government incentives, infrastructure expansion, and high consumer awareness. The country remains a global leader due to technological innovation, strong policy support, and increasing investments in clean energy ecosystems.

Competitive Landscape

The U.S. electric vehicle market is highly competitive, characterized by the presence of established automakers and innovative new entrants. Companies are focusing on battery innovation, software integration, and infrastructure development to strengthen their market position. Prominent players in the U.S. electric vehicle market include Tesla, Inc., General Motors Company, Ford Motor Company, Rivian Automotive, Inc., Lucid Group, Inc., Volkswagen AG, Hyundai Motor Company, Kia Corporation, Nissan Motor Co., Ltd., and BMW AG.

U.S. Electric Vehicle Market Size

The U.S. electric vehicle market size was valued at USD 107.32 billion in 2025 and is anticipated to reach USD 120.33 billion in 2026 from USD 300.50 billion by 2034, growing at a CAGR of 12.12% during the forecast period from 2026 to 2034.

According to the Alliance for Automotive Innovation, the number of publicly available charging outlets in the U.S. has reached 236,945 and this reflects a concerted effort to support widespread adoption. Consumer acceptance is increasingly influenced by the total cost of ownership rather than just the upfront purchase price. As per the Environmental Protection Agency, transportation accounts for 29% of total greenhouse gas emissions in the U.S., making electrification a critical component of national climate strategies. The automotive industry is undergoing a structural transformation with legacy manufacturers retooling factories and new entrants disrupting traditional supply chains. Federal incentives, such as tax credits under the Inflation Reduction Act, further accelerate consumer interest. The definition of this market extends beyond passenger cars to include light commercial vehicles and buses, which are gradually integrating electric powertrains. This holistic transition involves collaboration between automakers, utility companies, and government agencies to create a sustainable ecosystem. The interplay of policy, technology, and consumer behavior defines the current trajectory of the U.S. electric vehicle market.

MARKET DRIVERS

Federal Incentives and Regulatory Mandates Accelerate Adoption

Federal incentives and stringent regulatory mandates are majorly driving the growth of the U.S. electric vehicle market. The Inflation Reduction Act introduced significant tax credits for qualified electric vehicles, which substantially lower the effective purchase price for consumers. According to the Internal Revenue Service, the point of sale credit effectively reduced the price of an electric vehicle by $7,500 on the spot if eligibility requirements were met, though this provision was largely transitioned to a loan interest deduction under new legislative guidance in late 2025. This financial incentive directly addresses the higher upfront cost barrier associated with electric vehicles compared to internal combustion engine counterparts. Furthermore, the Environmental Protection Agency has implemented stricter emissions standards that compel automakers to increase their electric vehicle production volumes to avoid penalties. These regulations create a compliant environment where manufacturers are motivated to innovate and expand their electric offerings. As per the National Highway Traffic Safety Administration, corporate average fuel economy standards have been tightened, requiring improved efficiency across fleet averages. State-level initiatives, such as zero-emission vehicle mandates in California and other participating states, which is further reinforcing this trend. These policies collectively create a favorable economic and regulatory landscape that encourages both supply-side investment and demand-side uptake. The certainty provided by long-term regulatory frameworks allows manufacturers to plan capital expenditures with confidence. This alignment of fiscal benefits and legal requirements ensures sustained momentum in the transition towards electrified transportation across the U.S.

Advancements in Battery Technology and Charging Infrastructure Boost Confidence

Technological advancements in battery energy density and the expansion of charging infrastructure are further fuelling the expansion of the U.S. electric vehicle market. Modern lithium-ion batteries now offer greater range and faster charging times, which alleviate range anxiety, a primary concern for potential buyers. According to Xweather, new electric vehicles in the U.S. modeled for 2026 have reached a median range of 250 miles per charge, making them viable for daily commuting and long-distance travel. Simultaneously, the proliferation of fast charging networks enables quicker replenishment of battery levels comparable to refueling conventional vehicles. The Bipartisan Infrastructure Law allocated billions of dollars for the National Electric Vehicle Infrastructure formula program, which aims to establish a nationwide network of chargers along major highways. As per the Federal Highway Administration, recent updates to guidance in August 2025 allow states to seek flexibility regarding the strict 50-mile spacing requirements along designated highways once they achieve fully built-out certification. Improved battery longevity and reduced degradation rates also contribute to higher residual values, making electric vehicles more attractive from a total cost of ownership perspective. Automakers are investing heavily in solid-state battery research, which promises even greater safety and performance improvements. These technological strides, combined with visible infrastructure development, create a robust ecosystem that supports mainstream adoption. The tangible improvements in convenience and reliability drive consumer preference away from traditional fossil fuel vehicles.

MARKET RESTRAINTS

High Upfront Costs and Affordability Constraints Limit Mass Market Penetration

Despite incentives, the high upfront cost of electric vehicles remains a significant restraint for the U.S. electric vehicle market expansion. The initial purchase price of most electric models exceeds that of comparable internal combustion engine vehicles, primarily due to the expensive battery packs. According to Cox Automotive, the average transaction price for a new electric vehicle in March 2026 was $54,508, compared with about $50,000 for a new gas-powered vehicle. While tax credits mitigate this gap, they do not eliminate it entirely, particularly for lower-income households who may not have sufficient tax liability to claim the full credit. The cost of raw materials, such as lithium, cobalt, and nickel, continues to fluctuate, impacting manufacturing expenses. As per the Bureau of Labor Statistics, producer price indexes for battery components have shown volatility, affecting final vehicle pricing. Additionally, insurance premiums for electric vehicles are often higher due to specialized repair requirements and limited availability of qualified technicians. This financial burden discourages potential buyers who prioritize immediate affordability over long-term savings. The lack of affordable entry-level models in certain segments further restricts market expansion. Until economies of scale and technological innovations drive down production costs significantly, the high entry price will continue to restrain widespread adoption among diverse demographic groups in the U.S.

Inadequate Charging Infrastructure in Rural and Multi-Unit Dwelling Areas

The inadequacy of charging infrastructure in rural areas and multi-unit dwelling complexes poses a substantial restraint on the U.S. electric vehicle market. While urban centers and highway corridors see improved coverage, many rural communities lack reliable access to public charging stations. According to the Alliance for Automotive Innovation, half of all registered electric vehicles are concentrated in just 42 counties, representing only 1.4% of all counties in the U.S. Furthermore, individuals living in apartments, condominiums, and other multi-unit dwellings frequently lack access to home charging solutions, which are crucial for convenient overnight charging. As per the National Renewable Energy Laboratory, a significant portion of the housing stock in the U.S. does not have dedicated parking with electrical outlets. This infrastructure gap creates a disparity in adoption rates between homeowners with garages and renters or those in dense urban environments without private charging options. The installation of charging infrastructure in existing buildings involves complex logistical and financial challenges, including upgrading electrical grids and securing homeowner association approvals. Without equitable access to charging facilities, a large segment of the population remains excluded from the electric vehicle transition. This structural deficiency hinders the market from achieving true mass adoption and perpetuates reliance on conventional vehicles in underserved communities.

MARKET OPPORTUNITIES

Expansion of Electric Vehicle Fleet and Commercial Logistics

The expansion of electric vehicle fleets in commercial logistics and public transportation is a significant opportunity for market growth. Businesses are increasingly electrifying their delivery vans, trucks, and service vehicles to reduce operational costs and meet corporate sustainability goals. According to the Environmental Protection Agency, light-duty trucks, including sport utility vehicles and pickup trucks, accounted for 37% of transportation greenhouse gas emissions in 2022, making them prime targets for electrification. Companies, such as Amazon and FedEx, have committed to purchasing thousands of electric delivery vehicles driving demand for specialized commercial models. This shift creates opportunities for manufacturers to develop durable, high-capacity vehicles tailored for last-mile delivery and long-haul transport. Government fleets, including postal services and municipal buses, are also transitioning to electric powertrains supported by federal grants and state mandates. As per the Federal Transit Administration, investments in low or no-emission bus programs are accelerating the replacement of diesel buses with electric alternatives. The total cost of ownership for commercial electric vehicles is often lower due to reduced fuel and maintenance expenses, providing a compelling business case. This B2B segment offers stable volume demand that can help manufacturers achieve economies of scale. The development of depot charging solutions and fleet management software further enhances the viability of electric commercial operations. Capitalizing on this sector allows the industry to diversify beyond consumer passenger cars and establish a robust foundation for sustainable logistics.

Integration of Vehicle to Grid Technology and Energy Services

The integration of vehicle-to-grid technology offers a prominent opportunity for the U.S. electric vehicle market by turning cars into mobile energy storage units. Vehicle-to-grid systems allow electric vehicles to discharge electricity back to the grid during peak demand periods, providing stability and resilience to the power network. According to the Department of Energy, this bidirectional flow of energy can help integrate renewable sources, such as solar and wind, by storing excess generation. Utility companies are exploring pilot programs that compensate electric vehicle owners for participating in demand response initiatives. This creates a new revenue stream for consumers and enhances the value proposition of owning an electric vehicle. As per the North American Electric Reliability Corporation, the increasing penetration of distributed energy resources requires flexible assets to maintain grid reliability. Electric vehicles equipped with vehicle-to-grid capabilities can serve as decentralized power plants supporting local grids during outages or stress events. Automakers are beginning to incorporate bidirectional charging hardware in new models, enabling these functionalities. The synergy between the automotive and energy sectors opens avenues for innovative service models, including virtual power plants. By leveraging the battery capacity of millions of vehicles, the industry can contribute to a more sustainable and resilient energy infrastructure. This convergence positions electric vehicles as key components of the broader clean energy ecosystem.

MARKET CHALLENGES

Supply Chain Vulnerabilities and Critical Mineral Sourcing

Supply chain vulnerabilities related to critical mineral sourcing present a major challenge for the U.S. electric vehicle market. The production of electric vehicle batteries relies heavily on minerals, such as lithium, nickel, cobalt, and graphite, which are concentrated in a few countries. According to the U.S. Geological Survey, the U.S. depends largely on imports for these essential materials, creating exposure to geopolitical risks and trade disruptions. Efforts to domesticate supply chains through mining and processing facilities are underway but face lengthy permitting processes and environmental scrutiny. As per the Department of the Interior, establishing new mines in the U.S. can take over a decade due to regulatory hurdles. This lag between demand growth and supply expansion leads to bottlenecks and price volatility. Manufacturers struggle to secure long-term contracts for raw materials, which impacts production planning and cost stability. The concentration of refining capacity in specific regions further complicates efforts to diversify supply sources. Trade policies and international relations significantly influence the availability and cost of these inputs. Ensuring a secure and ethical supply chain requires substantial investment in domestic processing capabilities and recycling technologies. Until these structural issues are resolved, the industry remains susceptible to external shocks that can hinder growth and increase costs for consumers.

Grid Capacity Constraints and Energy Demand Management

Grid capacity constraints and the management of increased energy demand pose a significant challenge to the widespread adoption of electric vehicles in the U.S. The simultaneous charging of millions of electric vehicles could strain existing electrical infrastructure, particularly during peak hours. According to the Edison Electric Institute, utilities must invest billions of dollars in grid upgrades to accommodate the additional load from electrified transportation. Without smart charging solutions and time-of-use rates, uncoordinated charging could lead to localized overloads and reliability issues. As per the North American Electric Reliability Corporation, the transition to electric vehicles requires careful planning to ensure that generation, transmission, and distribution systems can handle the increased demand. Rural grids with older infrastructure are particularly vulnerable to capacity limitations. The variability of renewable energy sources adds complexity to managing this new load effectively. Utilities face the challenge of balancing supply and demand while maintaining affordability for all customers. Delayed infrastructure upgrades could result in charging delays and reduced consumer confidence. Coordinating between automakers, utility providers, and regulators is essential to develop strategies for load management and grid modernization. The pace of grid enhancement must match the rate of electric vehicle adoption to prevent systemic failures. This infrastructural bottleneck requires proactive investment and policy support to ensure a seamless transition.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 12.12% |

| Segments Covered | By Vehicle Type, Propulsion Type, Drive Type, Range, Component and Country |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Countries Covered | Tesla, General Motors, Ford, Rivian, Lucid Group, Volkswagen, Hyundai, Kia, Nissan, and BMW, which are driving innovation, production expansion, and technological advancements in the EV ecosystem. |

| Market Leaders Profiled | Archer-Daniels-Midland Company, Ag Processing Inc., Avril Group, Biodiesel Bilbao S.L., Cargill Inc., Emami Agrotech Ltd, FutureFuel Chemical Company, G-Energetic Biofuels Private Limited, Louis Dreyfus Company, Münzer Bioindustrie GmbH, Renewable Energy Group, VERBIO Vereinigte BioEnergie AG, Wilmar International Limited and World Energy LLC |

SEGMENTAL ANALYSIS

By Vehicle Type Insights

The passenger cars segment held the dominating share of the U.S. electric vehicle market in 2025. The dominance of this segment is fueled by the increasing availability of electric sedans, sport utility vehicles, and crossovers that cater to diverse lifestyle needs. According to the Alliance for Automotive Innovation, electric vehicles represented 9.6% of new light-duty vehicle sales in 2025, with total electric registrations for the year reaching 1,511,549 units. The expansion of charging infrastructure in residential and public areas supports the daily usage patterns of private car owners. As per the U.S. Department of Energy, the growing network of Level 2 and DC fast chargers enhances the convenience of owning an electric passenger car. Government incentives, such as federal tax credits, are primarily targeted at individual buyers, further stimulating demand in this segment. Automakers are heavily investing in marketing campaigns that highlight the performance and environmental benefits of electric passenger cars. The shift in consumer preference towards sustainable transportation options without compromising on luxury or utility ensures that passenger cars remain the cornerstone of the electric vehicle market. This segment benefits from established distribution channels and strong brand loyalty among existing automotive customers.

However, the commercial vehicle segment is estimated to register the fastest CAGR of 19.2% during the forecast period in the U.S. market owing to the stringent emissions regulations and the economic advantages of electrifying fleet operations. Logistics companies and municipal agencies are increasingly adopting electric vans, trucks, and buses to reduce operational costs and meet sustainability targets. According to the Environmental Protection Agency, recent standards have catalyzed widespread use of clean technologies, achieving a 99% reduction of common vehicle tailpipe pollutants over historical benchmarks. The Total Cost of Ownership for commercial electric vehicles is becoming increasingly competitive due to lower fuel and maintenance expenses compared to diesel counterparts. As per the American Trucking Associations, major logistics providers have announced ambitious goals to electrify their fleets, driving substantial procurement volumes. Federal grants and state-level incentives specifically designed for commercial electrification further accelerate adoption. The development of specialized electric commercial models with higher payload capacities and longer ranges addresses previous limitations. Urban delivery services benefit from zero-emission zones, which restrict access for conventional vehicles. These factors collectively propel the commercial segment at a faster pace as businesses recognize the strategic and financial benefits of transitioning to electric powertrains.

By Propulsion Type Insights

The battery electric vehicles segment led the market by accounting for the largest share of the U.S. market in 2025 due to the advancements in battery technology that have significantly increased driving range and reduced charging times. According to the International Energy Agency, electric car sales continued their rapid growth in 2025, climbing over 20% to more than 20 million units globally, which represents around 25% of all new car sales. The absence of an internal combustion engine simplifies the drivetrain, resulting in lower maintenance requirements and quieter operation. As per the U.S. Department of Energy, the expanding network of high-speed charging stations alleviates range anxiety, making battery electric vehicles viable for long-distance travel. Federal tax credits often favor pure electric models over hybrids, providing a financial incentive for buyers. Automakers are committing to all-electric futures with many announcing plans to phase out internal combustion engines entirely. The environmental consciousness of American consumers aligns with the zero-tailpipe emission profile of battery electric vehicles. This segment benefits from continuous innovation in energy density and thermal management systems. The strong policy support and consumer preference for clean energy solutions ensure that battery electric vehicles maintain their leading position in the market.

On the other end, the plug-in hybrid electric vehicle segment is experiencing rapid growth and is estimated to register a promising CAGR of 13.3% during the forecast period owing to the flexibility of having both an electric motor and an internal combustion engine, which eliminates range anxiety. According to the Alliance for Automotive Innovation, hybrid market share in the U.S. grew by 3.7 percentage points during the 2025 period. The ability to switch between power sources provides versatility for long road trips and daily urban driving. As per the Environmental Protection Agency, plug-in hybrids qualify for partial federal tax credits, making them an attractive option for budget-conscious buyers. Automakers are introducing more plug-in hybrid models across various segments, including SUVs and trucks, to capture this demand. The existing familiarity with gasoline engines reduces the learning curve for new users. Regulatory frameworks in several states recognize plug-in hybrids as partial zero-emission vehicles, encouraging their adoption. This segment appeals to rural residents and those in multi-unit dwellings where charging is challenging. The combination of electric efficiency and gasoline reliability ensures that this propulsion type grows rapidly as a bridge toward full electrification.

By Drive Type Insights

The all-wheel drive systems segment dominated and accounted for the leading share of the U.S. market in 2025. The dominance of all-wheel drive systems segment in the U.S. market can be credited to the consumer preference for enhanced traction, stability, and performance in diverse weather conditions. According to the Alliance for Automotive Innovation, all-wheel drive configurations are standard or popular options in premium electric SUVs and trucks, which represent a significant portion of new registrations. American consumers, particularly in regions with harsh winters, value the safety and control provided by all-wheel drive configurations. As per the National Highway Traffic Safety Administration, vehicles with better traction systems demonstrate improved safety metrics in adverse weather conditions. The dual motor setup in all-wheel drive electric vehicles also offers superior acceleration and handling dynamics, which appeal to performance-oriented buyers. Automakers leverage this configuration to differentiate their high-end models from entry-level rear or front wheel drive variants. The increasing popularity of electric pickup trucks and large SUVs further boosts the demand for all-wheel drive systems. This segment benefits from the perception of all-wheel drive as a premium feature that justifies higher price points. The technological ease of implementing all-wheel drive in electric platforms ensures its continued dominance in the market.

On the other end, the rear wheel drive segment is experiencing the fastest growth within the U.S. electric vehicle market and is predicted to expand at a CAGR of 16.1% during the forecast period due to the architectural advantages of dedicated electric vehicle platforms, which often place the primary motor on the rear axle for optimal weight distribution and handling. According to automotive engineering studies, rear wheel drive configurations allow for tighter turning radii and improved dynamic performance, which enhances the driving experience. Many new entrants and legacy automakers are launching entry-level and mid-tier electric sedans and crossover models with rear wheel drive as the base configuration. As per the Society of Automotive Engineers, rear wheel drive layouts simplify the front suspension design, allowing for more interior space and storage capacity. This efficiency in design reduces manufacturing costs, making rear wheel drive models more affordable for mainstream consumers. The success of popular rear wheel drive electric models has shifted consumer perception away from the traditional association of rear wheel drive with only luxury or performance vehicles. The modular nature of electric skateboards allows manufacturers to easily upgrade rear wheel drive models to all-wheel drive by adding a front motor. This flexibility encourages automakers to standardize rear wheel drive as the foundational architecture. The combination of cost efficiency, performance benefits, and spacious interiors ensures that the rear wheel drive segment expands rapidly.

By Component Insights

The battery pack and high voltage segment led the market with the highest share of the U.S. market in 2025. The growth of the battery pack and high voltage segment in the U.S. market is driven by the fact that the battery pack represents the most expensive single component in an electric vehicle, accounting for a significant portion of the total manufacturing cost. According to the U.S. Department of Energy, advancements in lithium-ion battery technology have led to increased energy densities and reduced costs per kilowatt-hour. High voltage components, such as inverters, onboard chargers, and power distribution units, are essential for managing the flow of electricity efficiently. As per the International Council on Clean Transportation, the supply chain for battery materials and components is a focal point of industrial policy and investment in the U.S. The demand for larger battery packs to support longer ranges in SUVs and trucks further drives volume growth. Manufacturers are investing heavily in domestic battery production facilities to secure supply and reduce reliance on imports. The complexity of high voltage systems requires specialized engineering and manufacturing capabilities, creating high barriers to entry. This segment benefits from continuous innovation in thermal management and safety systems. The strategic importance of batteries in the electrification transition ensures that this component segment remains the largest and most influential in the market.

However, the motor and powertrain segment is anticipated to showcase a promising CAGR of 15.5% during the forecast period owing to the rising need for efficient and compact propulsion systems. This growth is fueled by innovations in electric motor design, such as permanent magnet synchronous motors and induction motors, which offer high power density and efficiency. According to the Society of Automotive Engineers, advancements in motor technology are enabling smaller and lighter powertrains that improve vehicle range and handling. The integration of motor controllers and transmission systems into single units known as e-axles is gaining popularity due to space-saving benefits. As per the U.S. Department of Energy, research into rare earth-free motor technologies is accelerating to reduce dependency on critical minerals. The demand for high performance motors in commercial vehicles and luxury passenger cars drive investment in this segment. Manufacturers are focusing on improving the efficiency of power electronics to minimize energy loss during conversion. The trend towards multi-motor configurations in all-wheel drive vehicles also increases the volume of motors required per vehicle. The shift towards standardized modular powertrain components allows for economies of scale and faster production rates. These technological and manufacturing advancements ensure that the motor and powertrain segment grows at a robust pace supporting the overall expansion of the electric vehicle industry.

REGIONAL ANALYSIS

The U.S. is projected to experience a dynamic shift in its electric vehicle landscape over the next few years as it navigates evolving federal incentives and expanding infrastructure. According to the International Energy Agency, electric car sales in the U.S. saw a 2% decline in the second half of 2025, largely resulting from domestic policy changes regarding federal tax credits. The Inflation Reduction Act has reshaped the supply chain by incentivizing domestic battery production and mineral sourcing. As per the U.S. Department of Energy, the nation is investing billions in charging infrastructure to support widespread adoption. The presence of major automakers and innovative startups fosters a competitive landscape that drives technological advancement. Consumer awareness and environmental consciousness are rising influencing purchasing decisions across demographic groups. The market is supported by a robust ecosystem of suppliers, utilities, and technology providers. Regulatory pressures to reduce greenhouse gas emissions continue to shape industry strategies and product offerings. The U.S. plays a pivotal role in setting global trends for electric vehicle technology and policy. The combination of market size, technological leadership, and policy support ensures that the U.S. remains a central driver of global electric vehicle growth.

COMPETITIVE LANDSCAPE

The competition in the U.S. electric vehicle market is characterized by intense rivalry between legacy automakers and innovative new entrants who compete on technology price and brand loyalty. The market structure is becoming increasingly fragmented as more manufacturers introduce electric models across various segments. Competitive intensity is driven by the race to achieve superior battery range charging speed and autonomous driving features. Innovation in software defined vehicles plays a vital role as firms seek to differentiate through user experience and over the air updates. Regulatory compliance regarding emissions and domestic content requirements serves as a barrier to entry for some international competitors. Established players leverage their extensive dealer networks and manufacturing scale to compete with direct to consumer brands. Customer loyalty is maintained through ecosystem services such as charging networks and mobile applications. Price wars are emerging as production scales up and incentives fluctuate. The focus on supply chain resilience and domestic sourcing is becoming a key differentiator. Overall the competitive landscape requires continuous adaptation to technological advancements and shifting policy environments.

KEY MARKET PLAYERS

A few of the major companies in the U.S. electric vehicle market include

- Tesla, Inc.

- General Motors Company

- Ford Motor Company

- Rivian Automotive, Inc.

- Lucid Group, Inc.

- Volkswagen AG

- Hyundai Motor Company

- Kia Corporation

- Nissan Motor Co., Ltd.

- BMW AG

Top Players in the U.S. electric vehicle market

Tesla Inc

Tesla Inc is a pioneering force in the global electric vehicle market renowned for its advanced battery technology and autonomous driving capabilities. The company has established a robust supercharger network that enhances user convenience and reduces range anxiety for drivers worldwide. Tesla recently expanded its manufacturing footprint with new gigafactories to increase production capacity and meet surging global demand. The company continues to innovate with software updates that improve vehicle performance and safety features over the air. Tesla also focuses on energy storage solutions which complement its automotive business. Its direct to consumer sales model bypasses traditional dealerships allowing for greater control over customer experience. These strategic initiatives solidify Tesla's position as a leader in sustainable transportation and energy innovation.

Volkswagen AG

Volkswagen AG is a major global automaker aggressively transitioning its portfolio towards electrification with significant investments in electric vehicle platforms. The company leverages its modular electric drive matrix to produce a wide range of electric models across various brands. Volkswagen recently partnered with other manufacturers to standardize charging technology and expand infrastructure accessibility. The company is investing heavily in battery cell production through joint ventures to secure supply chains and reduce costs. Volkswagen focuses on sustainability by aiming for carbon neutrality in its production processes. Its strong presence in Europe and growing footprint in North America and China ensure broad market reach. These efforts demonstrate Volkswagen's commitment to leading the industry shift towards clean mobility.

BYD Company Limited

BYD Company Limited is a leading manufacturer of electric vehicles and batteries with a vertically integrated business model that controls key components. The company produces a diverse range of electric cars buses and commercial vehicles catering to global markets. BYD recently expanded its international presence by launching new models in Europe and Southeast Asia. The company invests heavily in research and development for blade battery technology which offers enhanced safety and efficiency. BYD also supplies batteries to other automakers strengthening its role in the broader electric vehicle ecosystem. Its ability to manufacture critical components in house allows for cost competitiveness and rapid innovation. These strategies enable BYD to maintain a strong competitive edge in the rapidly evolving global electric vehicle landscape.

Top Strategies Used by Key Market Participants

Key players in the U.S. electric vehicle market primarily employ strategies such as vertical integration strategic partnerships and infrastructure development to strengthen their market position. Companies frequently invest in domestic battery production facilities to secure supply chains and qualify for federal tax credits. This approach reduces dependency on foreign suppliers and lowers manufacturing costs. Strategic collaborations with technology firms enhance autonomous driving capabilities and software integration. By focusing on proprietary charging networks firms improve customer convenience and brand loyalty. Product diversification is another crucial strategy as companies expand into trucks SUVs and commercial vehicles to capture broader segments. Additionally firms prioritize sustainable manufacturing practices to align with regulatory standards and consumer expectations. These combined strategies enable market participants to maintain competitiveness and drive growth in a dynamic industry landscape.

MARKET SEGMENTATION

This research report on the U.S. electric vehicle market has been segmented based on the following categories.

By Vehicle Type

- Passenger Car

- Commercial Vehicle

By Propulsion Type

- Battery Electric Vehicle (BEV)

- Hybrid Electric Vehicle ( HEV)

By Drive Type

- All Wheel Drive

- Front Wheel Driv

- Rear Wheel Drive

By Range

- Up to 150 Miles

- 151-300 Miles

- Above 300 Miles

By Component

- Battery Pack & High Voltage Component

- Motor

- Brake, Wheel & Suspension

- Body & Chassis

- Low Voltage Electric Component

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com