U.S. Electronic Market Size, Share, Trends & Growth Forecast Report Segmented By Product Type (Electronic Devices, Home Appliances), Distribution Channel and Country – Industry Analysis From 2026 to 2034

U.S. Electronic Market Report Summary

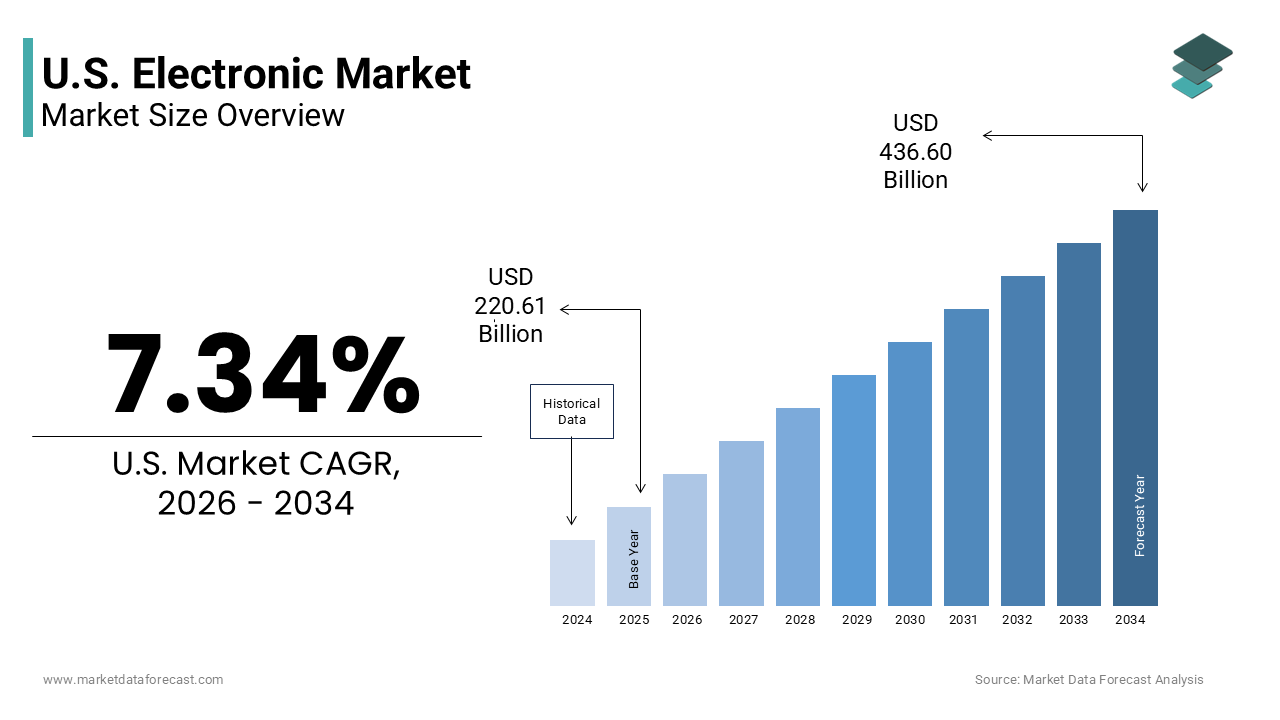

The U.S. electronic market was valued at USD 220.61 billion in 2025 and is anticipated to reach USD 237.99 billion in 2026 from USD 436.60 billion by 2034, growing at a CAGR of 7.88% during the forecast period from 2026 to 2034. The growth of the U.S. electronic market is driven by increasing adoption of artificial intelligence-enabled devices, rapid deployment of 5G infrastructure, and rising demand for connected consumer electronics. Expanding investments in edge computing technologies, increasing adoption of smart home ecosystems, and growing demand for advanced computing and communication devices are further accelerating market growth. Moreover, the expansion of domestic semiconductor manufacturing initiatives, rising adoption of circular electronics business models, and increasing integration of intelligent automation technologies are supporting the expansion of the U.S. electronic market.

Key Market Trends

- Rising integration of artificial intelligence processors and machine learning capabilities across consumer and enterprise electronic devices.

- Increasing deployment of 5G-enabled electronics including smartphones, wearables, laptops, and smart appliances.

- Growing adoption of edge computing technologies supporting industrial automation, healthcare, and smart infrastructure applications.

- Strong focus on sustainability through circular electronics programs, device refurbishment, and recycling initiatives.

- Expansion of cybersecurity features and embedded security architectures in connected consumer and industrial electronics.

Segmental Insights

- Based on product type, the computer segment dominated the U.S. electronic market and held the largest share in 2025. The segment’s dominance is attributed to widespread enterprise usage, increasing demand for remote and hybrid work solutions, rising adoption of AI-enabled computing systems, and continuous device replacement cycles across commercial and educational sectors.

- The digital camera and camcorder segment is projected to witness the fastest CAGR during the forecast period owing to the expansion of the creator economy, growing demand for professional content creation equipment, increasing social media monetization opportunities, and rising adoption of advanced imaging technologies.

- Based on home appliances, the refrigerator segment accounted for the leading share of the U.S. electronic market in 2025. The dominance of this segment is driven by its essential role in household food preservation, rising adoption of smart refrigerators, increasing energy efficiency improvements, and consistent replacement demand across residential consumers.

- The air conditioner segment is anticipated to register notable growth during the forecast period due to rising temperatures, increasing climate adaptation requirements, growing adoption of energy-efficient cooling systems, and expanding demand for smart air conditioning solutions with advanced air filtration capabilities.

- Based on distribution channel, the offline segment held the major share of the U.S. electronic market in 2025 owing to strong retail presence, consumer preference for product demonstrations, immediate product availability, and extensive after-sales support services offered through physical stores.

- The online segment is expected to witness rapid growth during the forecast period because of increasing e-commerce adoption, growing availability of direct-to-consumer sales models, expansion of digital payment solutions, and rising consumer preference for convenient online purchasing experiences.

Regional Insights

The United States maintained a strong position in the global electronics market in 2025, supported by advanced technological infrastructure, strong consumer spending, and a highly innovative semiconductor and electronics ecosystem. California remains a major contributor to the U.S. electronic market due to its concentration of leading technology companies, semiconductor innovation hubs, and strong consumer adoption of advanced electronics. Washington, New York, and Oregon are also witnessing notable growth driven by increasing investments in technology infrastructure, rising adoption of connected devices, and expanding demand for enterprise and consumer electronic solutions.

Competitive Landscape

The U.S. electronic market is highly competitive and characterized by the presence of global technology leaders, semiconductor manufacturers, consumer electronics companies, and enterprise hardware providers competing through innovation, ecosystem integration, and advanced product development. Leading companies are focusing on artificial intelligence integration, expanding semiconductor capabilities, strengthening cybersecurity features, investing in sustainable electronics initiatives, and enhancing connected device ecosystems. Strategic partnerships, product innovation, and vertical integration across hardware and software platforms are further strengthening market positioning across consumer and enterprise electronics categories. Prominent players in the U.S. electronic market include Apple Inc., Dell Technologies, HP Inc., Intel Corporation, NVIDIA Corporation, Advanced Micro Devices, Inc. (AMD), Qualcomm Incorporated, Texas Instruments Incorporated, Micron Technology, Inc., and Corning Incorporated.

U.S. Electronic Market Size

The U.S. electronic market size was valued at USD 220.61 billion in 2025 and is anticipated to reach USD 237.99 billion in 2026 from USD 436.60 billion by 2034, growing at a CAGR of 7.88% during the forecast period from 2026 to 2034.

The electronic is the design of devices and components that rely on semiconductor based circuitry to process transmit or store information or perform mechanical functions under electrical control. This includes consumer electronics computing hardware telecommunications infrastructure industrial automation systems and embedded electronics integrated into vehicles appliances and medical devices. Consumer behavior reveals deep integration with 76% of adults using multiple connected devices simultaneously according to the Pew Research Center. Regulatory frameworks, such as the CHIPS and Science Act further shape competitive dynamics by incentivizing domestic semiconductor production.

MARKET DRIVERS

The Pervasive Integration of Artificial Intelligence Into Consumer and Enterprise Devices

The artificial intelligence has ceased to be a peripheral feature and has become the operational core of nearly every new electronic device launched, which is majorly fuelling the growth of the United States electronic market. According to Stanford University’s AI Index Report, over 89% of newly released smartphones in 2023 featured dedicated neural processing units to enable on device machine learning for photography voice recognition and predictive text. The National Institute of Standards and Technology confirms that AI accelerated devices reduce inference latency by up to 92% compared to cloud dependent alternatives making them indispensable for autonomous systems. Consumer electronics manufacturers have responded with AI powered features such as adaptive battery management real time language translation and context aware user interfaces that increase perceived utility and justify premium pricing. This transformation is not merely technological but behavioral as users increasingly expect devices to anticipate needs automate routines and personalize experiences without explicit commands.

The Accelerating Deployment of 5G Infrastructure and Device Ecosystems

The nationwide rollout of fifth generation wireless networks by enabling new device categories enhancing performance expectations and rendering legacy hardware obsolete is accelerating the growth of the United States electronic market. According to the Federal Communications Commission, over 96% of the American population now has access to commercial 5G services with average download speeds exceeding three hundred megabits per second. This infrastructure leap has triggered a wave of device upgrades with Counterpoint Research reporting that 58 million 5G capable smartphones were activated in the United States during 2023 alone. Beyond handsets the impact permeates automotive telematics industrial sensors and home automation where low latency and high device density unlock capabilities previously constrained by network limitations. Consumer behavior reflects this shift with Parks Associates data indicating that households with 5G connectivity are two point three times more likely to invest in smart home electronics than those relying on 4G. Manufacturers are capitalizing on this by embedding 5G radios into laptops tablets wearables and even appliances creating an ecosystem where connectivity is assumed rather than optional.

MARKET RESTRAINTS

Persistent Global Semiconductor Supply Chain Fragility

Despite domestic reinvestment initiatives, the global semiconductor supply chain, which continues to be concentrated in geopolitically sensitive regions and subject to logistical hurdles is majorly limiting the growth of the United States electronic market. According to the Semiconductor Industry Association, over 78% of advanced logic chips consumed in the United States are still manufactured in Taiwan and South Korea creating strategic dependency. The problem is exacerbated by the industry’s reliance on just in time inventory models which leave minimal buffer for supply shocks. The Bureau of Economic Analysis confirms that inventory to sales ratios for electronic products remain at historic lows underscoring systemic vulnerability. Geopolitical tensions further compound risk with the Department of Commerce identifying over two hundred electronic components subject to potential export restrictions under current trade frameworks. While the CHIPS Act aims to mitigate this through domestic foundry investment, the Semiconductor Research Corporation estimates it will take until 2027 for new United States facilities to reach meaningful production scale.

Escalating E Waste Volumes and Regulatory Pressure on Disposal

The accelerating obsolescence cycle of electronic devices has generated unsustainable volumes of electronic waste placing mounting regulatory and reputational pressure on manufacturers and retailers. The escalating e-waste volumes and regulatory pressure in disposal is impeding th growth of the United States electronic market. The United States generated approximately 6.9 million tons of electronic waste in 2023 with only 15% formally recycled through certified channels. The remaining bulk ends up in landfills or informal recycling operations, where toxic materials, such as lead, mercury, and cadmium pose documented environmental and public health risks. State level legislation is intensifying with 25 states, now mandating producer responsibility for end of life device collection and recycling, as per a study. The Department of Justice has initiated enforcement actions against three major electronics retailers in the past 18 months for improper e-waste handling underscoring regulatory seriousness. This pressure is forcing manufacturers to redesign products for disassembly incorporate recycled materials and establish take back programs.

MARKET OPPORTUNITIES

Expansion of Edge Computing in Industrial and Smart Infrastructure Applications

The migration of data processing from centralized cloud environments to distributed edge devices is one of the major factors to set up new opportunities for the growth of the United States electronic market. The shift is particularly pronounced in smart city applications, where the Department of Energy reports that municipal utilities have installed over two million edge enabled grid monitoring devices to optimize energy distribution and detect outages in real time. The healthcare sector is following suit with the Food and Drug Administration clearing 37 new edge based medical diagnostic devices in 2023 that perform on site analysis without cloud connectivity. These applications demand specialized electronics including low power processors hardened memory modules and secure boot architectures creating high margin niches for component suppliers. Unlike consumer devices, which face saturation and replacement fatigue edge electronics serve mission critical functions in environments where reliability and speed are non-negotiable.

Strategic Reorientation Toward Circular Electronics and Device as a Service Models

Forward looking electronics firms are capitalizing on sustainability mandates and cost sensitivity by shifting from product ownership to service based models that retain control over device lifecycles and material recovery. The strategic reorientation toward cicular electronics and device as a service models is boosting the growth of the United States electronic market. Dell Technologies reported that its leasing programs grew by 38% in 2023 with clients citing predictable budgeting and reduced e waste as primary motivators. This model enables manufacturers to recover up to 90% of high value components such as rare earth magnets and gold plated connectors, as per data from the Institute of Scrap Recycling Industries. Consumer facing adaptations are emerging with Best Buy and Apple offering certified refurbished devices with full warranties capturing price sensitive segments while ensuring proper recycling of trade ins. Regulatory alignment is accelerating this shift with the Federal Trade Commission proposing new labeling standards in 2024 that require disclosure of repairability and expected service life.

MARKET CHALLENGES

Talent Shortage in Advanced Electronics Design and Embedded Systems Engineering

The deficit in specialized engineering talent particularly in fields, such as radio frequency design, embedded systems architecture, and semiconductor validation, which are essential for next generation product development is key challenge for the growth of the United States electronic market. The shortage is exacerbated by restrictive immigration policies with the Department of Homeland Security reporting a 34% decline in H 1B visas issued for electronics engineering roles since 2019. The consequences are tangible with the Semiconductor Research Corporation estimating that project delays due to staffing gaps cost the industry over four point two billion dollars in lost revenue in 2023 alone. Companies are responding with aggressive upskilling programs yet internal training can take 18 to 24 months to yield production ready engineers.

Rising Cybersecurity Vulnerabilities in Consumer and IoT Electronics

As electronic devices become increasingly interconnected and autonomous, they also become more attractive and vulnerable targets for cyberattacks creating systemic risk across consumer industrial and infrastructure domains. The rising cybersecurity vulnerabilities in consumer and IoT electronics is also to decline the growth of the United States electronic market. According to the Cybersecurity and Infrastructure Security Agency, over 83% of new consumer electronics released in 2023 contained at least one known exploitable vulnerability at launch with smart home devices and wearables being the most frequently compromised. Industrial systems are equally at risk with the Department of Energy documenting over twelve thousand attempted intrusions on grid connected control devices in 2023 alone. This lag exposes users to data theft device hijacking and even physical safety risks as demonstrated by recalls of vulnerable medical and automotive electronics. The regulatory response is intensifying with the National Telecommunications and Information Administration mandating minimum security standards for all federally procured electronics starting in 2025.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.38% |

| Segments Covered | By Type, Detector, Application and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Apple Inc., Dell Technologies, HP Inc., Intel Corporation, NVIDIA Corporation, Advanced Micro Devices, Inc., Qualcomm Incorporated, Texas Instruments Incorporated, Micron Technology, Inc., and Corning Incorporated. |

SEGMENTAL ANALYSIS

By Product Type Insights

The computer segment was accounted in holding 42.1% of the United States electronic devices market share in 2025. According to the Bureau of Labor Statistics, over 90% of professional roles in the United States now require daily computer interaction for core task execution making ownership non-discretionary. Premiumization also contributes with IDC data showing that average selling prices for laptops rose, since 2021 due to demand for higher performance processors larger memory capacities and AI enabled features. Corporations further drive replacement cycles with Gartner estimating that enterprises refresh employee devices every three years to maintain cybersecurity compliance and productivity standards. Unlike televisions or cameras computers are not passive consumption tools but active production platforms making them economically and socially irreplaceable.

The digital camera and camcorder segment is expected to grow at a fastest CAGR of 12.4% throughout the forecast period owing to the renaissance in professional and enthusiast content creation driven by the creator economy and platform monetization. As per the United States Bureau of Economic Analysis, over 2.7 million Americans now identify as full time content creators with 83 % investing in dedicated imaging hardware to differentiate output quality. YouTube’s Creator Economy Report notes that channels using interchangeable lens cameras receive higher viewer retention and ad revenue than smartphone only producers. The rise of short form cinematic platforms like TikTok and Instagram Reels has further elevated demand for shallow depth of field and cinematic frame rates that smartphones cannot reliably replicate.

By Distribution Channel Insights

The refrigerators segment was the largest by occupying 35.4% of the United States home appliances electronics market share in 2025 with the appliance’s non-negotiable role in food preservation household health and regulatory compliance. The average American household discards over 1000 dollars worth of perishable food annually without refrigeration making the appliance a financial necessity. Technological evolution has further entrenched its centrality with 64% of new refrigerators sold in 2023 featuring smart connectivity internal cameras and AI driven inventory management. Energy efficiency regulations have driven innovation with the Environmental Protection Agency noting that modern refrigerators consume less electricity than models from 2000, despite increased capacity and features. Replacement cycles remain steady at twelve to fifteen years according to AHAM data ensuring consistent demand even in economic downturns.

The air conditioner segment is lucratively growing at an anticipated CAGR of 18.2% throughout the forecast period owing to the intensifying climate volatility rising urban heat island effects and regulatory mandates for energy efficiency. The United States experienced its third hottest year on record in 2023 with over one hundred and twenty cities breaking all time temperature records triggering unprecedented demand for residential cooling. Health concerns, where smart air conditioners with integrated filtration reduce indoor particulate matter by up to 68% during wildfire season, according to a study. This emergence of climate adaptation regulatory alignment and health consciousness has transformed air conditioners from seasonal luxuries to year round essential infrastructure.

COMPETITIVE LANDSCAPE

The competition in the United States electronic market is defined by a tripartite struggle among vertically integrated giants agile niche innovators and private label disruptors each leveraging distinct advantages to capture consumer and enterprise wallet share. Legacy players rely on brand equity ecosystem integration and retail footprint to defend core categories while startups exploit white spaces in AI edge computing and sustainable design to carve defensible niches. Price competition is muted in premium segments where differentiation through silicon architecture software services and sustainability credentials justifies higher margins. Retailers exert growing influence through exclusive product launches data driven shelf allocation and in store experience zones that favor brands investing in co-marketing. Supply chain resilience has become a strategic weapon with companies that control semiconductor design or assembly gaining pricing and delivery advantages. Regulatory scrutiny around repairability data privacy and e waste is forcing redesigns that increase compliance costs but also create barriers to entry. Talent wars for AI and embedded systems engineers intensify as innovation velocity becomes the primary determinant of relevance.

KEY MARKET PLAYERS

Some of the promising companies that are playing a dominating role in the U.S. Electronic Market include

- Apple Inc.

- Dell Technologies

- HP Inc.

- Intel Corporation

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Qualcomm Incorporated

- Texas Instruments Incorporated

- Micron Technology, Inc.

- Corning Incorporated

Top Players in the United States Electronic Market

Apple Inc

Apple Inc maintains a formidable presence in the United States electronic market through its vertically integrated ecosystem of hardware software and services. The company continues to invest in silicon design with its M series chips enhancing performance and battery efficiency across MacBooks and iPads. In Asia Pacific, Apple operates premium retail stores in twelve countries and partners with local telecom providers to offer installment plans. It recently opened a dedicated R and D center in India to develop region specific features and expanded its trade in program in Japan and South Korea to boost device recycling and customer retention through upgrade incentives.

Samsung Electronics

Samsung Electronics dominates multiple categories including smartphones televisions and home appliances by blending hardware innovation with aggressive marketing. The company leverages its semiconductor division to ensure component security and cost control. In Asia Pacific Samsung operates manufacturing hubs in Vietnam and India and tailors product features to regional preferences such as dual SIM support and localized voice assistants. It recently launched a series of AI powered refrigerators and washing machines in Southeast Asia and partnered with Indonesian fintech firms to offer zero interest financing for premium electronics.

Dell Technologies

Dell Technologies holds strong influence in the computing and enterprise electronics segment through its direct sales model and customizable product configurations. The company prioritizes sustainability with closed loop recycling and carbon neutral shipping options. In Asia Pacific Dell supplies laptops and workstations to educational institutions and government agencies across Australia Singapore and Malaysia. It recently inaugurated a customer experience center in Tokyo to showcase AI ready workstations and launched a device as a service program in India targeting mid-sized enterprises seeking flexible IT procurement and lifecycle management.

Top Strategies Used by Key Market Participants

Product differentiation through proprietary silicon and ecosystem lock in remains central as companies embed custom processors and cross device interoperability to reduce churn. Strategic retail expansion includes experiential flagship stores and in store service desks to enhance tactile engagement and technical support. Partnerships with telecom carriers and fintech firms enable installment purchasing and trade in programs that lower entry barriers. Sustainability narratives are amplified through carbon neutral certifications recycled material usage and take back initiatives to align with regulatory and consumer expectations. Enterprise targeting focuses on device as a service models AI ready hardware and cybersecurity hardened endpoints to capture institutional budgets. Component vertical integration secures supply amid global shortages and reduces dependency on third party vendors. Software services and cloud subscriptions are bundled to increase lifetime customer value and recurring revenue.

MARKET SEGMENTATION

This research report on the U.S. Electronic Market has been segmented based on the following categories.

By Product Type

- Electronic Devices

- Television

- Computer

- Digital Camera & Camcorders

- Others (Audio & Video Products, Set-Top-Box, etc.)

- Home Appliances

- Refrigerator

- Washing Machine

- Air Conditioner

- Others

By Distribution Channel

- Offline

- Online

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

What is the U.S. Electronics Market?

The U.S. Electronics Market comprises the manufacturing, distribution, and sale of electronic devices, components, and systems used across consumer, industrial, healthcare, automotive, and telecommunications applications.

What factors are driving the growth of the U.S. Electronics Market?

Key growth drivers include technological advancements, increasing consumer demand for smart devices, growth in semiconductor applications, expansion of IoT technologies, and rising investments in automation.

What are the major segments of the U.S. Electronics Market?

The market is segmented into Sensors and Controls, Semiconductor Materials and Components, Security and Surveillance, Emerging Technologies, and Electronic Gadgets.

Who are the key players in the U.S. Electronics Market?

Major market participants include Apple Inc., Intel Corporation, NVIDIA Corporation, Dell Technologies, HP Inc., Qualcomm Incorporated, Texas Instruments Incorporated, Micron Technology, Inc., Corning Incorporated, and Advanced Micro Devices, Inc.

How is artificial intelligence influencing the electronics industry?

Artificial intelligence is increasing demand for advanced processors, sensors, data storage solutions, and intelligent electronic devices across various industries.

What role do semiconductors play in the U.S. Electronics Market?

Semiconductors are essential components used in consumer electronics, automotive systems, industrial automation, telecommunications equipment, and computing devices.

Which end use industries contribute significantly to market demand?

Major end use industries include consumer electronics, healthcare, automotive, aerospace and defense, industrial manufacturing, and telecommunications.

What challenges does the U.S. Electronics Market face?

Challenges include supply chain disruptions, semiconductor shortages, fluctuating raw material prices, cybersecurity concerns, and rapid technological changes.

How is the Internet of Things impacting the market?

The Internet of Things is driving the adoption of connected devices, smart sensors, automation systems, and advanced communication technologies.

What is the future outlook for the U.S. Electronics Market?

The market is expected to witness sustained growth due to increasing digitalization, advancements in artificial intelligence, expansion of 5G networks, and rising demand for smart electronic products.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com