U.S. Energy Storage Market Size, Share, Trends & Growth Forecast Report By Technology, By Capacity Rating, By Application, By End User, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Energy Storage Market Size

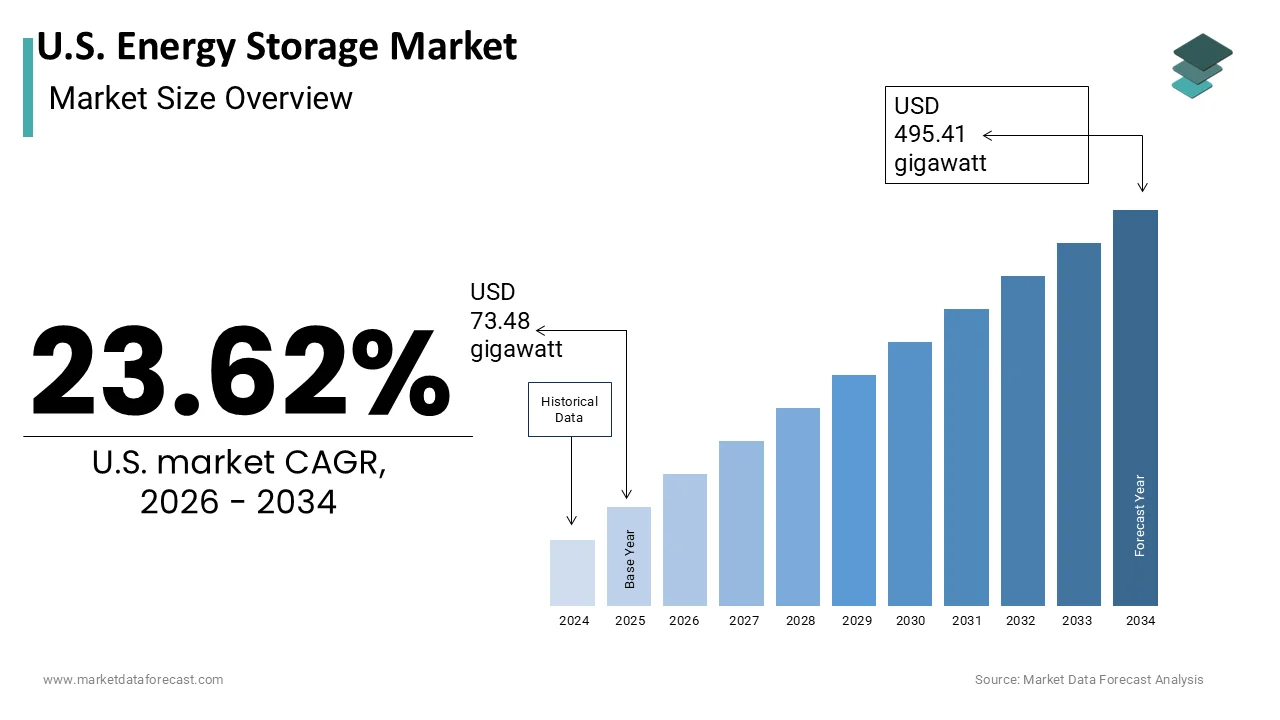

The U.S. Energy Storage Market was valued at 73.48 gigawatt in 2025, is estimated to reach 90.84 gigawatt in 2026, and is projected to reach 495.41 gigawatt by 2034, growing at a CAGR of 23.62% from 2026 to 2034.

Energy storage systems are defined as technologies that capture energy produced at one time for use at a later time, thereby decoupling energy generation from consumption. This capability is fundamental to addressing the intermittency inherent in solar and wind power generation. The strategic importance of this sector is underscored by the increasing frequency of extreme weather events, which strain grid reliability. According to the National Oceanic and Atmospheric Administration, the United States experienced 28 separate billion-dollar weather and climate disasters in 2023, highlighting the urgent need for resilient energy infrastructure. Furthermore, data verified by the U.S. Department of Energy indicates that over 70 percent of U.S. transmission lines are more than 25 years old, necessitating significant infrastructure modernization and upgrades to safely handle modern bidirectional power flows. The shift toward decentralized energy resources, such as rooftop solar panels, further complicates grid management without adequate storage solutions. As per the US Energy Information Administration, renewable sources accounted for approximately 21 percent of utility-scale electricity generation in 2022, a figure that continues to rise. This transition demands robust storage capabilities to maintain grid stability and ensure continuous power supply during peak demand periods or unexpected outages, positioning energy storage as a cornerstone of national energy security and sustainability goals.

MARKET DRIVERS

Acceleration of Renewable Energy Integration and Grid Modernization

The rapid expansion of renewable energy installations is pushing the United States energy storage market forward. Storage systems are essential for managing the variable nature of solar and wind power. Unlike conventional fossil fuel plants, renewable sources generate electricity intermittently, dependent on weather conditions and time of day. The US Energy Information Administration states that solar and wind capacity additions accounted for more than 70 percent of new utility-scale generating capacity in recent years. This surge in variable generation creates volatility in grid frequency and voltage, requiring immediate balancing services that batteries and other storage technologies provide efficiently. Federal initiatives such as the Inflation Reduction Act have accelerated this trend by providing investment tax credits for standalone energy storage projects, removing previous barriers that required storage to be paired directly with generation. According to the Department of Energy, the grid needs to triple its current transmission capacity by 2050 to meet decarbonization goals, a feat that is significantly aided by distributed storage solutions that reduce congestion on transmission lines. The ability of storage systems to absorb excess energy during periods of low demand and discharge it during peak hours enhances the overall efficiency and reliability of the grid. This operational flexibility is crucial for utilities aiming to retire coal and gas peaker plants, which are expensive and carbon-intensive. The demand for large-scale storage to prevent curtailment and ensure grid stability is becoming increasingly critical, driven by leading renewable adoption in states like California and Texas. Consequently, this is fueling substantial investment and deployment across the nation.

Increasing Frequency of Extreme Weather Events and Grid Resilience Needs

The surging incidence of extreme weather events and the resulting threat to grid reliability are among the leading growth factors for the adoption of energy storage systems in the region and for the overall United States energy storage market. Climate change has led to more frequent and severe hurricanes, wildfires, and winter storms, which frequently cause widespread power outages and damage critical infrastructure. The comprehensive macroeconomic data proving that weather and climate losses regularly exceed 100 billion dollars annually is maintained by the National Oceanic and Atmospheric Administration. Consumers and businesses are increasingly seeking energy independence and backup power solutions to mitigate the risks associated with grid failures. Residential battery storage systems, often paired with solar panels, offer a reliable source of electricity during outages, enhancing household resilience. According to the Lawrence Berkeley National Laboratory, the number of residential customers with solar plus storage systems has grown exponentially, driven by both economic incentives and the desire for security. Utilities are also investing in microgrids powered by energy storage to maintain critical services such as hospitals and emergency response centers during disasters. The Public Utility Commission in various states has mandated resilience planning that includes storage as a key component. This shift from viewing storage as merely an economic asset to recognizing it as a critical resilience tool has broadened its appeal and accelerated deployment. The imperative to harden the grid through decentralized storage solutions will continue to propel market growth as climate risks intensify. Hence, this shift ensures an uninterrupted power supply in an increasingly unpredictable environment.

MARKET RESTRAINTS

High Initial Capital Costs and Economic Viability Concerns

The high initial capital costs associated with energy storage systems remain a serious restraint to the growth of the United States energy storage market. This is despite the long-term benefits. The upfront investment required for purchasing and installing battery systems, particularly lithium-ion batteries, is substantial, posing a barrier for many residential consumers and smaller commercial entities. According to the National Renewable Energy Laboratory, the cost of battery storage systems can range from 300 to 600 dollars per kilowatt hour, depending on the scale and technology used. While prices have declined over the past decade, they remain prohibitive for widespread adoption without significant financial incentives. The volatility in raw material prices, particularly for lithium, cobalt, and nickel, further exacerbates cost uncertainties. The US Geological Survey notes that lithium prices have fluctuated dramatically due to supply chain constraints and surging demand from the electric vehicle sector, impacting battery manufacturing costs. Additionally, the complexity of financing these projects and the lack of standardized revenue models for standalone storage assets create financial risks for investors. Many potential users are deterred by the long payback periods, which can extend beyond 10 years in regions with low electricity price differentials. Although federal tax credits help mitigate these costs, they do not eliminate the initial cash flow burden. The high entry price will continue to limit market penetration, particularly among price-sensitive segments and in regions with less robust incentive structures. This situation will persist until economies of scale and technological advancements further reduce production costs.

Regulatory Uncertainty and Interconnection Bottlenecks

Regulatory uncertainty and complex interconnection processes are hampering the efficient deployment of these storage systems in the country, which in turn hinders the expansion of the United States energy storage market. The regulatory landscape for energy storage varies significantly across states, creating a fragmented market that complicates project development and investment decisions. While some states have clear mandates and compensation mechanisms for storage services, others lack defined frameworks, leading to ambiguity regarding revenue streams and operational rights. The Federal Energy Regulatory Commission has issued orders to improve participation of storage in wholesale markets, but implementation at the regional level remains inconsistent. According to the American Clean Power Association, interconnection queues for new energy projects, including storage, have reached record levels, with wait times extending to several years in some regions. These delays are caused by outdated grid study procedures and insufficient transmission infrastructure to accommodate new connections. The backlog hinders the timely commissioning of projects, increasing development costs and discouraging investment. Furthermore, differing safety standards and permitting requirements across jurisdictions add layers of complexity and cost for manufacturers and installers. The lack of uniform national standards for battery safety and recycling also creates compliance challenges. As per the Interstate Renewable Energy Council, streamlined permitting processes could reduce soft costs by up to 20 percent, yet progress in this area has been slow. Until regulatory harmonization and interconnection reforms are implemented, these structural barriers will continue to impede the rapid scaling of the energy storage market.

MARKET OPPORTUNITIES

Expansion of Vehicle-to-Grid Technology and Electric Vehicle Integration

The integration of electric vehicles with the grid through vehicle-to-grid technology offers a bright prospect for the United States energy storage market. The collective battery capacity of accelerating electric vehicle adoption represents a vast, distributed energy resource. This capacity can support grid stability. Data compiled by the U.S. Department of Energy indicates that domestic annual electric vehicle sales have surpassed 1 million units, building an escalating repository of distributed mobile storage assets across the power grid. Vehicle-to-grid systems allow electric vehicles to discharge stored energy back to the grid during peak demand periods, effectively turning cars into virtual power plants. This bidirectional flow of energy can reduce the need for stationary storage investments and provide ancillary services such as frequency regulation. Pilot programs in states like California and Maryland have demonstrated the technical feasibility and economic benefits of this approach. According to the Electric Power Research Institute, widespread adoption of vehicle-to-grid technology could provide up to 100 gigawatts of storage capacity by 2030, significantly enhancing grid flexibility. Automakers and utility companies are increasingly collaborating to develop compatible hardware and software solutions that facilitate seamless integration. Incentives for smart charging and bidirectional inverters are being introduced to encourage consumer participation. This synergy between the transportation and energy sectors not only optimizes asset utilization but also creates new revenue streams for electric vehicle owners. Vehicle-to-grid integration will unlock significant value as battery technology improves and charging infrastructure expands. This development transforms electric vehicles from mere consumers of electricity into active contributors to grid resilience and efficiency.

Development of Long-Duration Energy Storage Solutions

The development and commercialization of long-duration energy storage technologies offer a promising opportunity to address the limitations of current short-duration battery systems, which is anticipated to propel the expansion of the United States energy storage market. Lithium-ion batteries are effective for hourly shifting, but they are less suitable for storing energy over days or weeks. Such long-duration storage is necessary for deep decarbonization scenarios. Technologies such as flow batteries, compressed air energy storage, and green hydrogen are gaining traction for their ability to provide extended discharge durations. The Department of Energy has launched initiatives to support the demonstration of long-duration storage projects, aiming to reduce costs and prove viability at scale. According to the Long Duration Energy Storage Council, the market for long-duration storage could reach 40 to 80 billion dollars by 2030 as grids integrate higher shares of renewable energy. These technologies are particularly valuable in regions with seasonal variations in renewable generation, such as areas with low wind output in summer or reduced solar irradiance in winter. Several pilot projects are underway across the United States, testing the performance of iron air batteries and thermal storage systems. The ability to store energy for extended periods enhances grid reliability and reduces reliance on fossil fuel backups during prolonged low generation periods. These maturing, cost-competitive technologies will open new market segments and applications. Doing so will diversify the energy storage landscape and enable a more robust and flexible renewable energy infrastructure.

MARKET CHALLENGES

Supply Chain Vulnerabilities and Critical Mineral Dependencies

Vulnerability of its supply chain and heavy dependence on imported critical minerals are limiting the growth of the United States energy storage market. The production of lithium-ion batteries relies heavily on materials such as lithium, cobalt, nickel, and graphite, the processing of which is concentrated in a few countries, particularly China. The US Geological Survey indicates that the United States imports nearly all of its supply of graphite and a significant portion of its lithium and cobalt, creating strategic risks. Geopolitical tensions and trade restrictions can disrupt supply flows and lead to price spikes, affecting the availability and cost of battery systems. Recent global events have highlighted the fragility of these supply chains, prompting concerns about national security and energy independence. Efforts to domesticize supply chains are underway, but building mining and processing facilities takes years and faces environmental and regulatory hurdles. According to the International Energy Agency, global demand for critical minerals could quadruple by 2040, intensifying competition for resources. Diversifying supply sources and investing in recycling technologies are essential steps to mitigate these risks, but progress is slow. The lack of a robust domestic recycling infrastructure means that valuable materials are not being recovered efficiently, further exacerbating dependency on virgin materials. So, the US market remains vulnerable to price volatility and external shocks until it establishes a secure, resilient supply chain for battery materials. Without these upgrades, sustainable growth in the sector is hindered.

Technical Limitations and Safety Concerns

Technical limitations and safety concerns associated with energy storage technologies pose major obstacles to expansion and public acceptance within the United States energy storage market. Lithium-ion batteries, while dominant, are susceptible to thermal runaway, a condition where overheating leads to fires or explosions. High-profile incidents involving residential and utility-scale battery fires have raised awareness about safety risks and prompted stricter regulatory scrutiny. The National Fire Protection Association has developed specific codes for energy storage systems, but compliance adds complexity and cost to installations. Furthermore, the degradation of battery capacity over time affects the long-term performance and economic viability of storage assets. Most lithium-ion batteries lose significant capacity after 5 to 10 years, requiring replacement or repurposing. According to the Sandia National Laboratories, understanding and mitigating degradation mechanisms is critical for improving lifecycle costs and reliability. The lack of standardized testing and certification protocols for new storage technologies also hinders market confidence and adoption. Investors and consumers are often hesitant to adopt newer technologies due to uncertainties regarding performance and safety. Additionally, the disposal and recycling of spent batteries present environmental challenges that must be addressed to ensure sustainability. The industry faces the dual task of improving safety features and developing effective end-of-life management strategies. These technical and safety issues must be comprehensively resolved. Until then, they will remain barriers to widespread deployment and consumer trust in energy storage solutions.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Technology, Capacity Rating, Application, End User, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Tesla, Inc., Fluence Energy, Inc., The AES Corporation, NextEra Energy, Inc., LG Energy Solution Ltd., Samsung SDI Co., Ltd., BYD Company Limited, Siemens Energy AG, ABB Ltd., Panasonic Corporation, Stem, Inc., Enphase Energy, Inc. |

SEGMENTAL ANALYSIS

By Technology Insights

The battery segment led the United States energy storage market and captured a significant share in 2025. This leading position of the segment was attributed to its superior energy density, rapid response times, and declining costs. Also, this technology has become the standard for both utility-scale projects and residential applications because it efficiently handles the fast frequency regulation required by modern grids. According to the US Energy Information Administration, lithium-ion batteries accounted for approximately 90 percent of the total power capacity of newly installed energy storage systems in recent years. The scalability of battery systems allows them to be deployed in diverse settings, from small home units to massive grid-supporting installations. The manufacturing ecosystem for lithium-ion batteries has matured significantly, driven by the electric vehicle industry, which has created economies of scale that benefit stationary storage applications. Data from BloombergNEF indicates that the cost of lithium-ion battery packs has fallen by nearly 90 percent over the last decade, making them economically viable for widespread adoption. Furthermore, the modular nature of battery systems enables easier installation and maintenance compared to mechanical storage options. The ability to pair batteries directly with solar photovoltaic systems enhances their value proposition by maximizing self-consumption of renewable energy. As grid operators increasingly rely on fast-acting resources to balance supply and demand, the technical advantages of batteries ensure their continued dominance in the market landscape. Government policies and financial incentives have significantly reinforced the dominance of the battery segment in the United States energy storage market. The Inflation Reduction Act introduced a standalone investment tax credit for energy storage, which removed the previous requirement for storage to be paired with solar generation to qualify for federal incentives. This legislative change has unlocked substantial capital for standalone battery projects, accelerating deployment across various states. According to the Department of Energy, this policy shift is expected to drive billions of dollars in private sector investment into battery storage infrastructure over the next decade. State-level mandates, such as those in California and New York, further bolster demand by setting specific procurement targets for energy storage capacity. The California Public Utilities Commission has mandated the procurement of several gigawatts of storage to replace retiring gas peaker plants, primarily utilizing battery technology. These regulatory frameworks create a predictable market environment that encourages manufacturers and developers to focus on battery solutions. Additionally, federal research grants support advancements in battery safety and longevity, addressing key concerns among investors and consumers. The combination of federal tax credits and state mandates creates a robust financial foundation that sustains the leadership of battery technologies, ensuring they remain the preferred choice for meeting national energy storage goals.

The hydrogen energy storage segment is predicted to witness the highest CAGR of 34.3% from 2026 to 2034 due to its unique capability to provide long-duration and seasonal storage solutions. Unlike batteries, which are limited by discharge duration, hydrogen can store energy for weeks or months, making it ideal for balancing seasonal variations in renewable energy generation. The Department of Energy has identified hydrogen as a critical component of the national strategy to achieve net-zero emissions by 2050, highlighting its role in decarbonizing hard-to-abate sectors. According to the Hydrogen Council, long-duration storage needs will increase significantly as renewable penetration grows, creating a substantial market opportunity for hydrogen technologies. Green hydrogen, produced using excess renewable electricity through electrolysis, offers a carbon-free storage medium that can be converted back to electricity via fuel cells or turbines when needed. Pilot projects in states like Utah and California are demonstrating the feasibility of large-scale hydrogen storage in salt caverns and depleted gas fields. The ability to utilize existing natural gas infrastructure for hydrogen blending and transport further reduces deployment barriers. As the grid requires more flexibility to handle extended periods of low renewable output, hydrogen storage provides a scalable solution that complements short-duration battery systems, driving its rapid growth trajectory. Significant federal funding and industrial decarbonization initiatives are accelerating the growth of the hydrogen energy storage segment in the United States. The Bipartisan Infrastructure Law allocated 8 billion dollars to establish regional hydrogen hubs, which aim to demonstrate the commercial viability of hydrogen production, storage, and utilization. These hubs serve as test beds for integrating hydrogen storage into the broader energy system, fostering innovation and reducing technology risks. According to the Department of Energy, these investments are expected to leverage additional private capital, creating a robust ecosystem for hydrogen technologies. Industrial sectors such as steel, cement, and chemicals are exploring hydrogen storage as a means to secure reliable, clean energy supplies while reducing their carbon footprints. The availability of low-cost renewable energy in regions like the Midwest and Southwest supports the economic case for green hydrogen production and storage. Furthermore, collaborations between utility companies and industrial players are driving the development of hybrid systems that combine hydrogen storage with renewable generation. These partnerships facilitate knowledge sharing and standardization, which are essential for market expansion. As regulatory frameworks evolve to support hydrogen integration and carbon pricing mechanisms become more prevalent, the economic attractiveness of hydrogen storage will improve, fueling its status as the fastest-growing segment in the market.

By Capacity Rating Insights

The 10 to 100 MWh capacity segment dominated the United States energy storage market by accounting for a 38.6% share in 2025 because it offers an optimal balance between scale and flexibility for commercial and utility applications. This capacity range is sufficiently large to provide meaningful grid services such as frequency regulation and peak shaving, yet small enough to be deployed relatively quickly compared to massive utility-scale projects. According to the Federal Energy Regulatory Commission, many independent system operators prefer this size for distributed energy resource aggregations, which allow multiple smaller units to function as a single virtual power plant. Commercial and industrial facilities frequently adopt systems in this range to manage demand charges and enhance energy resilience without requiring extensive land use or complex permitting processes. Data compiled by the American Clean Power Association indicates that a significant portion of non-residential storage installations falls within mid-scale commercial capacity brackets, driven by the localized economic benefits of demand charge reduction, load shifting, and resilient backup power. The modularity of battery systems allows developers to scale projects to meet specific site constraints and energy needs, making this segment highly versatile. Additionally, the 10 to 100 MWh range aligns well with the output of medium-sized solar farms, facilitating efficient co-location and maximizing asset utilization. This strategic fit with existing infrastructure and market needs ensures the continued dominance of this capacity segment. Regulatory frameworks and market rules in various US states favor mid-scale energy storage deployments, reinforcing the leadership of the 10 to 100 MWh segment. Many state programs offer incentives and streamlined permitting processes for projects within this capacity range, recognizing their potential to enhance local grid reliability and defer transmission upgrades. For instance, the New York State Energy Research and Development Authority has implemented programs specifically targeting retail community-scale storage projects, which typically sit at or below the 5 MW / 20 MWh capacity threshold due to localized distribution network interconnection rules. According to the Interstate Renewable Energy Council, these targeted incentives reduce soft costs and accelerate project timelines, making mid-scale deployments more attractive to developers. Furthermore, interconnection standards for this capacity range are often less stringent than those for larger utility-scale projects, reducing administrative burdens and costs. The ability of these systems to participate in wholesale energy markets as aggregated resources also enhances their revenue potential, encouraging investment. Utilities are increasingly partnering with third-party developers to deploy mid-scale storage in strategic locations to address local congestion and voltage issues. This regulatory and operational support creates a favorable environment for the 10 to 100 MWh segment, ensuring it remains the primary choice for a wide array of energy storage applications across the country.

However, the above 100 MWh capacity segment is estimated to register the fastest CAGR of 32.1% during the forecast period. The urgent need for utility-scale integration to maintain grid stability amidst rising renewable energy penetration. Utilities require massive storage assets to manage intermittency and prevent curtailment as solar and wind farms come online. These renewable projects create a need for balancing power. According to the US Energy Information Administration, the average size of new battery storage projects has increased significantly, with many installations now exceeding 100 MWh to provide multi-hour discharge capabilities. These large-scale systems are essential for replacing conventional baseload power plants and providing critical inertia to the grid. States like Texas and California are leading this trend, with numerous gigawatt-hour-scale projects in development to support their ambitious renewable energy goals. The economic viability of these large projects is enhanced by their ability to participate in multiple revenue streams, including energy arbitrage, ancillary services, and capacity markets. The scalability of lithium-ion technology allows for the construction of these massive facilities, which are becoming integral components of the modern transmission network, driving rapid growth in this high-capacity segment. Economies of scale and continuous cost reductions are pivotal factors driving the rapid growth of the above 100 MWh energy storage segment. Large-scale projects benefit from lower per-unit costs for equipment, installation, and operation compared to smaller distributed systems. According to BloombergNEF, the levelized cost of storage for utility-scale projects has decreased substantially, making them competitive with traditional peaker plants in many regions. Developers can negotiate better pricing for bulk purchases of batteries and inverters, further enhancing project economics. The standardization of design and construction processes for large facilities also reduces development time and risks, attracting institutional investors seeking stable long-term returns. Federal investment tax credits apply to these large projects, significantly improving their financial metrics and accelerating deployment. Additionally, advancements in battery management systems allow for more efficient operation of large arrays, maximizing energy throughput and lifespan. The ability to spread fixed costs over a larger capacity base improves profitability, encouraging utilities and independent power producers to invest in mega projects. As technology matures and supply chains optimize, the cost advantage of large-scale storage will continue to widen, sustaining its position as the fastest-growing segment in the market.

By Application Insights

The renewable integration segment held the majority share of 48.9% of the United States energy storage market in 2025. This supremacy of the segment was credited to the critical need to manage the intermittency of solar and wind power. Renewable energy sources constitute a growing share of the electricity mix. Therefore, storage systems are essential for smoothing out fluctuations in generation and ensuring a stable power supply. According to the US Energy Information Administration, renewable sources generated over 20 percent of US electricity in 2022, a figure that is projected to rise significantly in the coming decades. Energy storage allows excess energy produced during peak generation periods to be stored and dispatched when generation is low, thereby maximizing the utilization of renewable assets. This capability reduces the need for curtailment, where renewable energy is wasted due to grid congestion or oversupply. States with high renewable penetration, such as California and Hawaii, rely heavily on storage to maintain grid reliability and meet clean energy targets. The technical ability of batteries to respond rapidly to changes in supply and demand makes them ideal for integrating variable renewable resources. Furthermore, co-locating storage with renewable generation facilities enhances project economics by allowing owners to capture higher-value energy during peak pricing periods. This strategic alignment with national decarbonization goals ensures that renewable integration remains the dominant application for energy storage technologies. Policy mandates and aggressive clean energy targets are fundamental drivers sustaining the leadership of the renewable integration application segment. Many states have enacted renewable portfolio standards that require utilities to source a specific percentage of their electricity from renewable sources, often accompanied by storage procurement requirements. For example, California’s mandate requires 100 percent clean electricity by 2045, necessitating massive investments in storage to support this transition. According to the National Conference of State Legislatures, over 30 states have established renewable energy goals, creating a consistent demand for storage solutions that facilitate renewable integration. Federal policies, including the Inflation Reduction Act, provide financial incentives for projects that pair storage with renewable generation, further encouraging this application. Utilities are compelled to invest in storage to comply with these regulations and avoid penalties, driving substantial market growth. Additionally, corporate sustainability commitments are pushing businesses to procure renewable energy coupled with storage to ensure reliable, clean power supplies. The alignment of regulatory frameworks, financial incentives, and corporate goals creates a robust ecosystem that prioritizes renewable integration, solidifying its position as the leading application segment in the energy storage market.

On the other hand, the peak shaving and demand charge management segment is anticipated to witness the fastest CAGR of 26.8% between 2026 and 2034. This quick surge of the segment is propelled by strong economic incentives for commercial and industrial users. Electricity tariffs often include demand charges based on the highest power usage during peak periods, which can constitute a significant portion of monthly bills. Energy storage systems allow businesses to discharge stored energy during these peaks, thereby reducing their maximum demand and lowering overall electricity costs. The return on investment for storage systems dedicated to demand charge management is often shorter than for other applications, encouraging rapid adoption among businesses seeking to optimize operational expenses. Retailers, data centers, and manufacturing facilities are increasingly installing storage to mitigate these costs, driven by the transparency of savings and predictable financial benefits. As electricity rates continue to rise, the economic case for peak shaving becomes even more compelling, fueling growth in this segment. Furthermore, advanced energy management software enables precise control of storage dispatch, maximizing savings and enhancing the value proposition for commercial and industrial customers. Grid congestion and the need to defer costly infrastructure investments are accelerating the growth of the peak shaving and demand charge management application. Utilities face increasing pressure to upgrade transmission and distribution networks to handle rising peak loads, which requires significant capital expenditure. Energy storage offers an alternative to non-wires by reducing peak demand on the grid, thereby deferring or eliminating the need for expensive infrastructure upgrades. Regulatory mechanisms in some states allow utilities to recover costs associated with storage deployments aimed at grid support, creating a favorable environment for this application. By reducing peak load, storage systems help stabilize voltage and frequency, enhancing overall grid performance. This benefit is particularly valuable in urban areas where space for new substations or lines is limited. The dual benefit of cost savings for consumers and grid relief for utilities drives collaborative projects and innovative tariff structures that encourage peak shaving. As grid congestion worsens with electrification and climate change, the strategic value of storage for demand management will continue to propel its rapid growth.

By End User Insights

The utility segment was the largest in the United States energy storage market and occupied a significant share in 2025. This prominence of large-scale procurement initiatives was supported by large-scale procurement initiatives aimed at enhancing grid reliability and meeting regulatory mandates. Utilities are responsible for maintaining the stability of the electrical grid, and energy storage has become a critical tool for managing supply and demand imbalances. According to the US Energy Information Administration, utility-scale storage installations account for the majority of deployed capacity, reflecting the sector’s dominant role in the market. Utilities invest in storage to replace aging fossil fuel peaker plants, which are expensive to operate and maintain. Storage systems provide similar grid services, such as frequency regulation and voltage support, but with greater efficiency and lower environmental impact. State regulations often require utilities to procure specific amounts of storage capacity, forcing significant investment in this segment. For instance, Pacific Gas and Electric and Southern California Edison have contracted for gigawatts of storage to support their renewable integration goals. The ability of utilities to spread costs across their rate base makes large-scale storage projects financially viable, ensuring steady demand. Furthermore, utilities possess the technical expertise and infrastructure necessary to integrate storage into the grid effectively, reinforcing their leadership in the market. Regulatory compliance and the ability to recover costs through rate bases are key factors driving the dominance of the utility end-user segment. Public utility commissions in many states allow utilities to include the costs of energy storage investments in their rate bases, enabling them to recover these expenses from customers over time. This regulatory framework reduces financial risk for utilities and encourages substantial investment in storage infrastructure. According to the National Association of Regulatory Utility Commissioners, many states have adopted policies that recognize storage as a legitimate grid asset eligible for cost recovery. This assurance of our revenue stream motivates utilities to pursue aggressive storage procurement strategies to meet clean energy mandates and reliability standards. Additionally, utilities are incentivized to invest in storage to avoid penalties associated with failing to meet renewable portfolio standards or reliability metrics. The structured nature of utility planning and procurement processes ensures a consistent pipeline of large-scale projects, sustaining the segment’s market leadership. As regulatory environments continue to evolve in favor of clean energy technologies, utilities will remain the primary drivers of energy storage deployment in the United States.

But the residential segment is likely to experience the fastest CAGR of 27.7% over the forecast period. This swift expansion of the segment is fueled by rising electricity costs and increasing concerns about power outages. Homeowners are increasingly adopting solar plus storage systems to reduce their reliance on the grid and protect against blackouts caused by extreme weather events. According to the Lawrence Berkeley National Laboratory, residential storage installations have experienced double-digit annual growth, heavily driven by consumer demand for localized energy independence, financial savings, and backup security. High electricity rates in states like California and Hawaii make the economic case for self-consumption of solar energy particularly strong, encouraging homeowners to install batteries. Marketing efforts by solar companies and battery manufacturers have also raised consumer awareness of the benefits of residential storage. The availability of financing options and leasing models has lowered the barrier to entry, making storage accessible to a broader range of households. As climate risks intensify and electricity prices remain volatile, the residential segment is poised for continued rapid expansion. Federal and state incentives play a crucial role in accelerating the growth of the residential energy storage segment. The Inflation Reduction Act provides a 30 percent investment tax credit for residential energy storage systems, significantly reducing the upfront cost for homeowners. According to the Solar Energy Industries Association, this incentive has spurred a surge in residential storage adoption across the country. Several states offer additional rebates and incentives, such as the Self Generation Incentive Program in California, which provides further financial support for battery installations. These programs make storage more affordable and improve the return on investment for homeowners. Net metering policies, although evolving, still encourage the pairing of storage with solar to maximize savings. Utility programs that compensate homeowners for exporting stored energy to the grid during peak times also enhance the economic viability of residential systems. The combination of federal tax credits, state rebates, and utility incentives creates a favorable financial environment that drives rapid growth in the residential sector. As more homeowners become aware of these benefits and technology costs continue to decline, the residential segment will maintain its status as the fastest-growing end-user category.

COUNTRY LEVEL ANALYSIS

United States Energy Storage Market Analysis

The United States was the top performer in the North American energy storage market and accounted for a 81.6% share in 2025. Its position is driven by a robust policy framework, technological innovation, and significant private sector participation. The market status reflects a transition from pilot projects to mainstream deployment, with energy storage becoming an integral part of grid planning and operations. According to the US Energy Information Administration, the United States has installed several gigawatts of energy storage capacity, with projections indicating exponential growth in the coming decade. The country’s leadership is underpinned by its advanced research institutions, which drive advancements in battery chemistry and grid integration technologies. The presence of major technology providers and developers fosters a competitive ecosystem that accelerates innovation and cost reduction. Federal initiatives, such as the Department of Energy’s Energy Earthshots, aim to further solidify this leadership by targeting specific cost and performance goals for storage technologies. The United States serves as a global benchmark for energy storage policy and deployment, influencing market trends worldwide. Its large and diverse grid offers unique challenges and opportunities that drive the development of versatile storage solutions, ensuring its continued dominance in the regional and global landscape. The main driving factor for the United States energy storage market is the confluence of state-level policy support and state-level mandates aimed at decarbonization. The Inflation Reduction Act has injected billions of dollars into the sector through tax credits and grants, stimulating unprecedented investment. According to modeling released by the U.S. Department of Energy, newly established federal incentives are projected to accelerate utility-scale storage installations to multiple times their baseline projections by 2030, outstripping a simple doubling curve. State laws, such as California’s mandate for 52,000 megawatts of storage by 2045, create long-term demand that drives long-term planning and procurement. The urgency of climate change mitigation, highlighted by the National Oceanic and Atmospheric Administration’s data on increasing extreme weather events, further compels the rapid adoption of storage for resilience. The economic competitiveness of storage, with costs falling by nearly 90percent over the last decade, as per BloombergNEF, makes it a viable alternative to traditional grid infrastructure. The integration of renewable energy, which accounted for over 20 percent of generation in 2022 according to the EIA, necessitates storage to manage intermittency. These factors, combined with a strong venture capital ecosystem and technological prowess, create a dynamic environment where the United States continues to lead in energy storage innovation and deployment, setting the pace for global market evolution.

COMPETITIVE LANDSCAPE

The competition in the United States energy storage market is characterized by intense rivalry among established technology providers, utilities, and emerging startups. Major players compete on technological innovation, cost efficiency, and project execution capabilities to capture market share. The landscape features a mix of integrated manufacturers who produce batteries and system integrators who assemble components from various suppliers. Differentiation is achieved through proprietary software platforms that optimize energy dispatch and asset performance. Price competition remains fierce as manufacturing declines and costs decline,ecline driven by economies of scale. Regulatory compliance and safety standards serve as critical barriers to entry, influencing competitive dynamics. Companies strive to build strong relationships with utilities and policymakers to secure favorable contract terms and incentives. The entry of new participants with novel technologies such as flow batteries and hydrogen storage adds complexity to the competitive environment. Collaboration between traditional energy firms and tech companies is increasing to leverage complementary strengths. This dynamic ecosystem drives continuous improvement in product quality and service offerings, ensuring that only the most adaptable and innovative firms thrive in the evolving market.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating rolU.S. the U.S. energy storage market include

- Tesla, Inc.

- Fluence Energy, Inc.

- The AES Corporation

- NextEra Energy, Inc.

- LG Energy Solution Ltd.

- Samsung SDI Co., Ltd.

- BYD Company Limited

- Siemens Energy AG

- ABB Ltd.

- Panasonic Corporation

- Stem, Inc.

- Enphase Energy, Inc.

TOP LEADING PLAYERS IN THE MARKET

- Tesla Inc maintains a prominent position in the United States energy storage market through its comprehensive portfolio of battery solutions for residential c, commercial, a, nd utility-scale applications. The company leverages its advanced lithium-ion battery technology and integrated software platforms to deliver reliable and efficient energy storage systems. Recent actions include the expansion of its megafactory in Lathrop, California, which significantly increases utility-scale auction capacity for utility-scale Megapack units. Tesla continues to innovate with improved battery chemistry and thermal management systems that enhance performance and safety. The company also integrates its storage products with solar offerings to provide holistic energy solutions for consumers. By scaling manufacturing and optimizing the supply chain,s Tesla strengthens its ability to meet growing demand while reducing costs. Its strong brand recognition and technological leadership enable it to influence market trends and set high standards for product quality and reliability in the rapidly evolving energy storage sector.

- Fluence Energy Inc operates as a leading global provider of energy storage products and services with a strong footprint in the United States market. The company offers a wide range of scalable solutions, including hardware and software, and digital applications that optimize grid performance and renewable integration. Fluence focuses on delivering intelligent energy storage systems that provide critical services such as frequency regulation and peak shaving. Recent strategic moves include expanding its manufacturing capabilities in the United States to reduce lead times and enhance supply chain resilience. The company actively collaborates with utilities and independent power producers to deliver large-scale projects that support grid stability. Fluence also invests heavily in research and development to improve battery lifecycle management and operational efficiency. By leveraging data analytics and artificial intelligence, Fluence enhances the value proposition of its storage assets. These efforts solidify its reputation as a trusted partner for complex energy storage deployments across various sectors.

- NextEra Energy Resources is a major developer and operator of enestorage, age projects in the United States, leveraging its extensive experience in renewable energy infrastructure. The company integrates large-scale battery storage systems with its wind and solar portfolios to enhance reliability and maximize asset value. It focuses on deploying utility-scale storage solutions that address grid congestion and support renewable energy integration. Recent initiatives include announcing significant investments in new battery projects across multiple states to meet rising demand for clean energy resources. The company utilizes its robust financial position and regulatory expertise to navigate complex permitting and interconnection processes efficiently. NextEra also explores innovative business models such as hybrid renewable plus storage facilities to optimize energy dispatch. By prioritizing sustainable development and grid modernization, NextEra reinforces its leadership role in the transition to a low-carbon energy system. Its strategic approach ensures consistent growth and contribution to the stability of the national electrical grid.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States energy storage market primarily focus on vertical integration to control supply chains and reduce manufacturing costs. Companies are increasingly establishing domestic production facilities to mitigate geopolitical risks and qualify for federal incentives. Strategic partnerships with utilities and renewable energy in the long term are common to secure long-term contracts and ensure project pipelines. Innovation in battery chemistry and software analytics is prioritized to enhance performance, safety, and lifecycle value. Firms also pursue mergers and acquisitions to expand technological capabilities and geographical diversification. Diversification into long-duration storage technologies allows participants to address emerging market needs for seasonal energy shifting. Additionally, companies invest in recycling infrastructure to create circular economies and comply with environmental regulations. Marketing efforts emphasize reliability, risk-aversion, and resilience to attract risk averse customers. These strategies collectively aim to strengthen competitive positioning and drive sustainable growth in a dynamic regulatory and economic landscape.

MARKET SEGMENTATION

This research report on the U.S. energy storage market is segmented and sub-segmented into the following categories.

By Technology

- Battery Storage

- Pumped Hydro Storage

- Thermal Energy Storage

- Compressed Air Energy Storage (CAES)

- Flywheel Energy Storage

- Hydrogen Energy Storage

By Capacity Rating

- Below 10 MWh

- 10–100 MWh

- Above 100 MWh

By Application

- Renewable Integration

- Peak Shaving & Demand Charge Management

- Grid Stability & Frequency Regulation

- Backup Power

- Electric Vehicle Charging Infrastructure

By End User

- Utility

- Residential

- Commercial & Industrial

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com