U.S. Eyewear Market Size, Share, Trends & Growth Forecast Report By Product Type, By Distribution Channel, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Eyewear Market Size

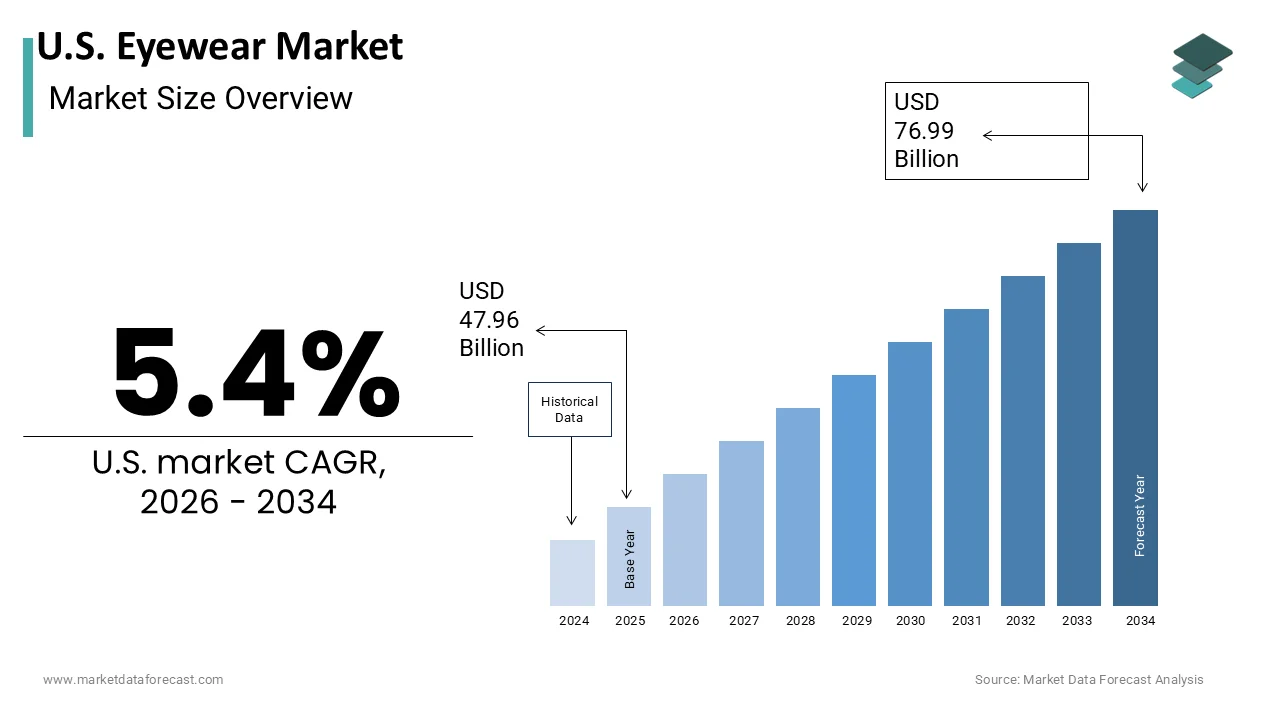

The U.S. Eyewear Market was valued at USD 47.96 billion in 2025, is estimated to reach USD 50.55 billion in 2026, and is projected to reach USD 76.99 billion by 2034, growing at a CAGR of 5.4% from 2026 to 2034.

Eyewear refers to any device worn on or over the eyes, serving purposes ranging from vision correction and eye protection to fashion, aesthetic enhancement, and, more recently, digital technology integration. This sector is deeply intertwined with public health devicephics and consumer lifestyle trends rather than functioning merely as a fashion accessory domain. The fundamental necessity for visual correction drives consistent demand across all age groups. Market tracking from The Vision Council shows that approximately 164 million U.S. adults use prescription eyewear, establishing a massive, non-discretionary consumer base for the optical industry. This physiological need ensures market resilience regardless of economic fluctuations. The aging population further amplifies this requirement as presbyopia and other age-related vision conditions become more prevalent. According to U.S. Census Bureau projections, the population aged 65 and older is expected to grow to over 84 million by 2060, driving unprecedented demand for progressive lenses, multifocals, and specialized geriatric eye care.

Additionally, clinical data emphasized by the American Optometric Association shows that prolonged device usage triggers Computer Vision Syndrome, mirroring consumer data from The Vision Council, which indicates that 65% of American adults experience active symptoms of digital eye strain. This phenomenon has spurred demand for specialized lenses with blue light filtering capabilities. The market is thus defined by a convergence of medical necessity and technological adaptation,n where consumer choices are increasingly influenced by health awareness and screen time management rather than aesthetic preferences alone.

MARKET DRIVERS

Rising Prevalence of Myopia and Digital Eye Strain Drives Prescription Lens Demand

The escalating incidence of myopia and digital eye strain is a key reason for the expansion of the prescription eyewear segment in the United States eyewear market. Modern lifestyles characterized by prolonged exposure to digital screens have fundamentally altered visual health patterns among both children and adults. Research published by the National Eye Institute reveals that myopia rates in the United States skyrocketed from 25% in the early 1970s to over 41% by the early 2000s, with contemporary epidemiological projections warning that half the global population could be myopic by 2050. This significant rise translates into a larger pool of individuals requiring corrective lenses at an earlier age. Furthermore, the American Optometric Association (AOA) confirms that prolonged near-work triggers Computer Vision Syndrome, with historical survey benchmarks showing 58% of adults experience active digital eye strain symptoms like dry eyes and blurred vision. These symptoms often necessitate the purchase of specialized eyewear equipped with anti-reflective coatings and blue light filtering technologies. According to longitudinal research from Common Sense Media, American teenagers spend an average of 7.5 hours per day on screens for entertainment alone, a heavy recreational load that compounds the risk of adolescent visual fatigue. This extensive usage accelerates the progression of myopia in younger demographics, creating a long-term customer base for eyewear retailers. Consequently, optical practitioners are seeing increased frequency in prescription updates, with many consumers requiring new glasses every 12 to 18 months, two years of the traditional two-year cycle. This accelerated replacement cycle directly boosts volume sales for manufacturers and retailers alike.

Growing Geriatric Population Increases Demand for Multifocal and Progressive Lenses

The demographic shift toward an older population in the country creates a robust and expanding demand for multifocal and progressive lenses, which fuels the growth of the United States eyewear market. As individuals age, the natural lens of the eye loses flexibility, leading to presbyopia, a condition that typically becomes noticeable after age 40. Projections from the U.S. Census Bureau indicate that the number of Americans aged 65 and older is on track to expand significantly, reaching an estimated 84.3 million by 2060 and driving an unprecedented structural demand for the geriatric vision market. This demographic expansion ensures a steady and growing customer base for vision-related solutions. Clinical data from the National Institute on Aging notes that nearly all adults will experience some degree of presbyopia after the age of 40, making the adoption of reading glasses, bifocals, or progressive lenses a near-universal milestone of middle age. Unlike single vision lenses, these advanced optical products command higher price points due to their complex manufacturing processes and customization requirements.

Additionally, older adults are more likely to suffer from multiple vision issues simultaneously,y such as cataract, glaucoma, macula, and macular degeneration. These conditions often require specialized lenses with specific tints or filters to enhance contrast and reduce glare. The combination of high prevalence rates,, and the technical s,,ophisticat, ion of required products drives revenue growth in the premium segment of the eyewear market.

MARKET RESTRAINTS

High Cost of Premium Eyewear and Limited Insurance Coverage Restricts Accessibility

The substantial financial burden associated with purchasing premium eyewear is a major impediment to market penetration, particularly among uninsured or underinsured populations, which restrains the expansion of the United States eyewear market. While basic vision correction is a medical necessity, the cost of frames and advanced lens technologies often exceeds the coverage limits of standard vision insurance plans. Consumer pricing reports indicate that the average cost of a pair of prescription glasses in the United States ranges from $200 to over $600 without insurance, varying heavily by retail channel, frame material, and specialized lens features. However, many standard vision insurance plans provide an annual frame allowance capping at $100 to $150, requiring consumers to rely on out-of-pocket spending or supplementary plan discounts to cover premium lens enhancements. Even among those with insurance, high deductibles and copayments can deter regular updates to prescriptions. This financial barrier lelow-quality over-the-counterlow quality, over the counter readers, which do not address individual astigmatism or pupillary distance needs. So, a significant portion of the population continues to use outdated or incorrect prescriptions,s which not only hampers market growth for premium products but also poses risks to long-term visual health and safety.

Competition from Online Retailers Undermines Traditional Brick-and-Mortar Profitability

The rapid ascent of direct-to-consumer online eyewear retailers has disrupted the traditional business model of brick-and-mortar optical stores, which has slowed down the growth of the United States eyewear market. This shift has created intense price competition and margin pressure. Online platforms offer significantly lower prices by eliminating overhead costs associated with physical retail spaces and intermediate supply chain layers. Major online players often sell complete prescription glasses for under $100, including basic lenses, which is substantially lower than the average retail price in physical stores. This price disparity forces traditional retailers to engage in aggressive discounting, which erodes profit margins. Furthermore, online retailers invest heavily in digital marketing and customer acquisition strategies that small independent opticians cannot match. This shift has led to the closure of numerous independent optical shops and consolidation within the industry. The inability of traditional retailers to compete on price while maintaining service quality creates a challenging environment for sustained growth. Consumers are becoming more price sensitive and less loyal to specific brands or stores, which complicates inventory management and sales forecasting for established market participants.

MARKET OPPORTUNITIES

Integration of Augmented Reality for Virtual Try-On Experiences Enhances Engagement

The adoption of augmented reality technology for virtual try-on experiences sets the stage for eyewear retailers to enhance customer engagement and reduce return rates, which is likely to promote the expansion of the United States eyewear market. As online shopping continues to grow, the inability to physically try on glasses remains a major hurdle for consumers. Augmented reality solutions allow users to visualize how different frames look on their faces in real time using smartphone cameras or webcams. Data from Shopify demonstrates that consumer interactions with product pages featuring 3D models and augmented reality (AR) content yield a 94% higher conversion rate on average compared to standard product pages, heavily boosting buyer confidence. This technology not only improves the online shopping experience but also builds consumer confidence in their purchase decisions. Major eyewear brands have integrated these tools into their mobile applications and websites,s resulting in increased time spent on site and higher average order values. By leveraging this technology, retailers can offer personalized recommendations based on face shape and skin tone, which enhances customer, satisfactry-try-onurthermore virtual try-on data provides valuable insights into consumer preferences, allowing companies to optimize their product assortments and marketing strategies. This technological integration bridges the gap between the convenience of online shopping and the tactile experience of physical retail,l creating a hybrid model that appeals to modern consumers.

Expansion into Sustainable and Eco-Friendly Eyewear Materials Attracts Conscious Consumers

The growing consumer preference for sustainable and eco-friendly products offers a lucrative opportunity for eyewear manufacturers to differentiate their brands and capture a niche but rapidly expanding market segment, which is expected to boost the growth of the United States eyewear market. Environmental consciousness is increasingly influencing purchasing decisions, particularly among millennials and Generation Z consumers who prioritize ethical production practices. A study established that 73% of global consumers would change their consumption habits to reduce environmental impact, a sentiment that continues to evolve as modern shoppers link sustainable products directly to persona, well-being. In response, several eyewear brands have intbio-basedrames mad,,e from bio-based plastics, recycled ocean plastics, and biodegradable materials such as wood, cotton acetate. The global nonprofit alliance Cascale (formerly the Sustainable Apparel Coalition) highlights that the fashion and accessories sectors, including eyewear, face intense institutional pressure to adopt rigorous circular economy principles and traceable supply chains. Brands that transparently communicate their sustainability efforts often enjoy higher brand loyalty and willingness to pay premium prices. By investing in sustainable materials and ethical manufacturing processes, eyewear companies can appeal to this discerning demographic. Additionally, ly regulatory pressures regarding plastic waste are expected to tighten while the adoption of eco-friendly materials is a strategic advantage. This shift not only mitigates environmental impact but also opens new avenues for innovation and brand storytelling.

MARKET CHALLENGES

Supply Chain Disruptions and Raw Material Volatility Impact Production Stability

Persistent supply chain disruptions and volatility in raw material prices are significant challenges to the stability and profitability of the eyewear manufacturing sector, which hinders the expansion of the United States eyewear market. The global nature of the eyewear supply chain means that components, such as metal alloys and glass lenses, es are sourced from various international suppliers,s making the industry vulnerable to geopolitical tensions and logistical bottlenecks. According to data from the Bureau of Labor Statistics, the Producer Price Index for plastic materials and resins experienced double-digit spikes in 2022, driven by volatile energy costs and global supply constraints that inflated manufacturing raw material overhead. These cost increases are often difficult to pass on to consumers in a highly competitive market, leading to compressed margins. Additionally, the semiconductor shortage has affected the production of smart eyewear and advanced manufacturing equipment, causing delays in product launches. Eyewear just-in-times relying on just in time inventory systems have faced stockouts and an inability to meet sudden spikes in demand. Furthermore, trade policies and tariffs on imports from key manufacturing hubs such as China and Italy add another layer of complexity and cost. These factors create uncertaan inty in production planning and pricing strategies, making it difficult for companies to maintain consistent product availability and competitive pricing.

Strict Regulatory Compliance and Evolving Safety Standards Increase Operational Costs

Navigating the complex landscape of regulatory compliance and evolving safety standards is an ongoing obstacle for eyewear manufacturers and retailers, which in turn holds back the growth of the United States eyewear market. The Food and Drug Administration (FDA) classifies prescription eyewear as Class I medical devices, which mandates that manufacturers comply with general regulatory controls, including facility registration and proper product labeling. Under FDA oversight, optical manufacturers must align operations with the Quality System Regulation (QSR) to ensure consistent product safety and defect prevention across the supply chain. Non-compliance can result in costly recalls and legal penalties.Additionallyy, the Federal Trade Commission (FTC) strictly enforces the updated Eyeglass Rule, which mandates that optometrists and ophthalmologists provide patients with their prescription copy immediately at no extra charge and retain signed confirmation of receipt for compliance. This regulation promotes competition but also increases administrative burdens for healthcare providers. State-level regulations vary significantly, with some states imposing additional licensing requirements for opticians and dispensers. Furthermore, the new standards for blue light filtering lenses and UV protection are being developed by organizations such as the American National Standards Institute. Keeping pace with these regulatory changes requires significant investment in legal counsel, quality assurance, and staff training. Failure to comply can damage brand reputation and result in loss of market access.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, and the rest of the United States |

| Market Leaders Profiled | EssilorLuxottica SA, Johnson & Johnson Vision Care, Inc., Alcon Inc., Bausch + Lomb Corporation, Safilo Group S.p.A., CooperVision, Inc., Warby Parker Inc., Marcolin S.p.A., De Rigo Vision S.p.A., Carl Zeiss AG, Hoya Corporation, Fielmann Group AG |

SEGMENTAL ANALYSIS

By Product Type Insights

The spectacles segment held the majority share of the United States eyewear market in 2025. This supremacy of the segment was credited to the widespread prevalence of refractive errors,s such as myopia,h hyperopia, and astigmatism. The non-invasive nature of spectacles makes them the preferred option for individuals seeking immediate vision correction without the risks associated with surgical procedures or the maintenance requirements of contact lenses. Moreover, spectacles serve a dual purpose as both medical devices and fashion accessories, allowing consumers to express personal style while addressing health needs. This high ownership rate is further supported by the increasing availability of affordable options through online retailers and warehouse clubs. The durability of modern frame materials such as titanium and acetate ensures longevity, but fashion trends encourage frequent updates. Consequently, the spectacle segment maintains its dominance through a combination of medical necessity,y aesthetic appeal, and consumer convenience.

In addition, the domination of the spectacles segment is further reinforced by continuous technological advancements in lens coatings and materials, which drive premiumization and higher revenue per unit. Consumers are increasingly investing in high-performance lenses that offer protection against blue light, UV radiation, and glare. The integration of photochromic technology, which allows lenses to darken automatically in sunlight, ht has also gained traction. These advanced features enhance visual comfort and eye health, making spectacles more than just a corrective tool. Additionally, high-index development of high-index lenses, which are thinner and lighter hass improved the aesthetic appeal of glasses for individuals with strong prescriptions. This shift towards value-added products encourages consumers to upgrade their eyewear more frequently. Manufacturanti-fog also focuses on anti-fog and scratch-resistant coatings, which extend the lifespan of the product. These innovations create a compelling value proposition that sustains consumer interest and drives market leadership for the spectacles segment.

Bscratch-resistant segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 4.2% from 2026 to 2034. This growth is primarily driven by the increasing adoption of daily disposable contact lenses, which offer superior hygiene and convenience compared to traditional reusable lenses. Consumers prefer these lenses because they eliminate the need for cleaning solutions and storage cases,s reducing the risk of eye infections. Daily disposables mitigate this risk by ensuring a fresh sterile lens is used every day. Furthermore,, ore the availability of specialized daily lenses for astigmatism and presbyopia has expanded the addressable market. CooperVision and Johnson and Johnson Vision have introduced advanced silicone hydrogel materials that allow higher oxygen permeability,ilit,y enhancing comfort for extended wear. This trend towards convenience and health safety fuels the rapid expansion of the contact lens segment.

Also keeping this segment in the lead is the rising popularity of cosmetic and colored contact lenses among younger demographics. These lenses allow users to change or enhance their eye color, serving as a fashion accessory rather than just a vision correction tool. Social media platforms and celebrity influence have played a crucial role in normalizing the use of colored lenses for aesthetic purposes. Instagram and TikTok have millions of posts featuring users experimenting with different eye colors, which drives demand among teenagers and young adults. Major brands like Acuvue and Freshlook have expanded their color palettes to include natural and vibrant shades, catering to diverse consumer preferences. This regulation has increased awareness about the importance of proper fitting and bysafet by educating the incidence of injuries from illegal, unregulated products. As consumer confidence in the safety and quality of cosmetic lenses grows, the segment continues to attract new users who may not require vision correction but desire the aesthetic benefits. This is an expansion into the beauty and fashion domain that accelerates the overall growth of the contact lens market.

By Distribution Channel Insights

In 2025, the retail stores segment remained the largest by occupying a substantial share of the United States eyewear market because of the critical need for professional fitting and personalized service. Unlike other consumer goods, eyewear requires precise measurements such as pupillary distance and vertex distance to ensure optimal vision correction. The tactile experience of trying on frames and receiving real-time feedback on fit and style is difficult to replicate online. Retail outlets, including independent optical shops and large chains like LensCrafters and Pearle Vision, offer comprehensive eye exams and on-site, can produce glasses within hours. This convenience and speed are significant advantages for consumers who need urgent replacements. Trust is another key factor as consumers feel more confident purchasing high-ticket items when they can interact with knowledgeable staff.

Additionally, many insurance plans are directly integrated with retail networks,s making the claims process seamless for customers. The ability to buy tickets immediately after purchase ensures comfort and reduces the likelihood of returns. These factors collectively sustain the dominance of retail stores in the eyewear distribution landscape.

Moreover, the established presence of major eyewear brands in physical retail locations reinforces consumer trust and drives the continued dominance of this channel. Companies like EssilorLuxottica have invested heavily in creating flagship stores and exclusive boutiques that offer a premium shopping experience. Consumers often associate physical stores with authenticity, reducing the fear of counterfeit products,s which is a concern in the online marketplace. Retail stores also serve as showrooms for new collections, allowing brands to launch products with impactful visual merchandising. Seasonal promotions and in store event,s further drive foot traffic and sales volume. Moreover,r the integration of omnichannel strategies, where customers can browse online and pick up in store, enhances the value proposition of physical locations. This hybrid approach leverages the strengths of both channels, but ultimately relies on the physical store for final conversion and fulfillment. The strong brand equity built over decades in physical retail environments creates a barrier to entry for pure play online competitor,s ensuring that retail stores maintain their leading position in the market.

On the contrary, the online stores segment is expected to exhibit a noteworthy CAGR of 6.5% during the forecast period. The main driver of this growth is the convenience of shopping from home combined with significantly lower prices compared to physical retailers. Direct-to-consumer brands like Warby Parker and Zenni Optical have disrupted the market by offering high-quality glasses at a fraction of traditional retail prices. These companies utilize vertical integration, direct-to-consumer passing savings directly to customers. The availability of virtual try-on tools has reduced the hesitation associated with buying glasses without physically trying them on. Furthermore, the ease of comparing prices and reading customer reviews empowers consumers to make informed decisions quickly. The subscription model for contact lenses has also gained popularity online,e with services like Hubble and SimpleContacts offering automatic deliveries at discounted rates. This recurring revenue model enhances customer retention and lifetime value. As logistics and return policies improve, the friction associated with online eyewear purchases continues to decrease,e fueling rapid channel growth.

Furthermore, the integration of telemedicine and digital prescription services is another critical factor accelerating the growth of online eyewear stores. The pandemic accelerated the adoption of remote healthcare services, and this trend has persisted in the eye care sector. Many online eyewear retailers have partnered with telehealth providers to offer seamless end-to-end solutions where patients can get examined online and immediately purchase glasses or contacts. This streamlined process reduces the time and effort required to acquire vision correction products. Additionally, mobile applications enable end-to-end users to scan their existing glasses to determine prescription details. Although this method is less accurate than a professional exam, it serves as a convenient option for minor updates. The combination of accessible digital healthcare and effective commerce platforms creates a powerful ecosystem that appeals. Although savvy consumers. Regulatory frameworks are evolving to support digital health initiatives. Hence, the online channel is poised to capture an even larger share of the eyewear-commerce.

COUNTRY MARKET ANALYSIS

U.S. Eyewear Market Analysis

The United States led the North American eyewear market and captured a 78.2% share in 2025. This dominance of the segment was attributed to the country's large population,n high healthcare expenditure,e and advanced optical infrastructure. The market status is characterized by a mature yet dynamic environment where innovation and consumer preferences drive continuous evolution. According to U.S. Census Bureau estimates, the national population has surpassed 342 million, with a steadily aging demographic and shifting lifestyle factors driving an unprecedented baseline demand for vision correction services and corrective lenses. The high prevalence of chronic diseases such as diabetes, which can affect vision,n further amplifies demand for specialized eyewear. The Centers for Disease Control and Prevention (CDC) reports that over 38 million Americans now have diabetes, significantly elevating the national risk for diabetic retinopathy and driving an essential medical mandate for regular ocular monitoring.

Additionally, sources indicate that U.S. adults average over 6 hours of dedicated daily screen time on digital devices, a profound lifestyle shift that directly accelerates consumer complaints of digital eye strain and fatigue. This extensive exposure drives demand for protective eyewear,r including blue light filtering glasses and computer glasses. The presence of major global eyewear conglomerates and a robust network of independent opticians ensures wide availability of products across urban and r,ural areas. High disposable income levels allow consumers to purchase multiple pairs of glasses for different occasions, contributing to market volume. The regulatory environment is stringent, ensuring high-quality standards that build consumer trust. Furthermore, the integration of insurance coverage for vision care through employers and government programs facilitates access to eyewear for millions of Americans. These structural, demographic, and economic factors solidify the United States as the leading market for eyewear in the region, with sustained growth potential driven by technological advancements and health awareness.

COMPETITIVE LANDSCAPE

The competition in the United States eyewear market is intense and characterized by a mix of established global conglomerates and agile direct-to-consumer startups. Major players leverage their extensive retail networks and brand recognition to maintain dominance, while newer entrants disrupt the market with competitive pricing and digital first approdirect-to-consumer is further amplified by the increasing convergence of fashion and healthcare, where aesthetic appeal competes with medical necessity. Companies are constantly innovating to differentiate digital-first offerings through advanced lens technologies and sustainable materials. Price competition is fierce, particularly in the online segment, where low overhead costs allow for aggressive discounting. Traditional retailers face pressure to enhance their in-store experiences and integrate digital tools to retain customers. The threat of substitution from laser eye surgery and alternative vision correction methods also influences competitive dynamics. Brand loyalty is instilled through personalized services and comprehensive eye care solutions. Regulatory compliance and insurance network partnerships serve as barriers to entry for smaller firms. Overall, the market demands continuous adaptation to technological trends and consumer preferences to sustain competitive advantage and profitability in this mature yet evolving industry landscape.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. Eyewear Market include

- EssilorLuxottica SA

- Johnson & Johnson Vision Care, Inc.

- Alcon Inc.

- Bausch + Lomb Corporation

- Safilo Group S.p.A.

- CooperVision, Inc.

- Warby Parker Inc.

- Marcolin S.p.A.

- De Rigo Vision S.p.A.

- Carl Zeiss AG

- Hoya Corporation

- Fielmann Group AG

TOP LEADING PLAYERS IN THE MARKET

- EssilorLuxottica stands as a dominant force in the United States eyewear landscape by integrating lens manufacturing with retail distribution. The company owns prominent retail chains such as LensCrss Hut, which provide extensive market reach. Recently, the corporation has focused on digital transformation by enhancing its online platforms and incorporating augmented reality tools for virtual try-ons. This strategic move aims to bridge the gap between physical and digital shopping experiences. EssilorLuxottica also invests heavily in sustainable initiatives, introducing eco-friendly frame materials to try-on and environmentally conscious consumers. Their continuous innovation in lens technology, including blue light filtering and photochromic options, ensures they remain at the forefront of health solutions. By leveraging its vertical integration model, the company maintains control over quality and supply chain efficiency. These efforts collectively strengthen their brand loyalty, ty, and operational resilience in a competitive market environment while addressing evolving consumer needs for convenience and sustainability.

- Johnson and Johnson Vision is a leading player in the contact lens segment of the United States market, known for its innovative daily disposable products. The company focuses on advancing and developing silicone hydrogel materials that enhance oxygen permeability. Recently, they have expanded their portfolio to include specialized lenses for astigmatism and presbyopia, catering to diverse patient needs. Johnson and Johnson Vision actively collaborates with eye care professionals to promote proper lens hygiene and fitting practices. Their commitment to education helps reduce infections and improve vaccinations. The company also leverages digital health platforms to streamline prescription management and reorder processes for consumers. By prioritizing clinical efficacy and user comfort, improve and maintain a strong reputation among optometrists and patients alike. Their strategic investments in manufacturing capabilities ensure consistent product availability and high-quality standards. These actions reinforce their position as a trusted provider of vision correction solutions in the United States.

- CooperCompanies operates primarily through its subsidiary CooperVisio,n which is a major high-quality provider to the contact lens market in the United States. The company is renowned for its MyDay and Biofinity lens brands, which offer moisture retention. CooperCompanies has recently emphasized sustainability by launching recycling programs for contact lens blisters and packaging. This initiative resonates with environmentally aware consumers and differentiates the brand from competitors. They also focus on professional engagement by providing educational resources and training for eye care practitioners. The direct-to-consumer strategies include subscription services that enhance customer convenience and retention. CooperCompanies continues to innovate with new lens designs that address specific visual impairments and direct-to-consumer, maintaining strong relationships with independent optometrists, ensuring widespread distribution and professional endorsement. Their agile approach to market trends allows them to quickly adapt to changing consumer preferences. These efforts solidify their reputation for quality and reliability in the vision care sector.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States eyewear market employ several strategic initiatives to maintain competitiveness and drive growth. Product innovation remains a primary strategy with companies investing heavily in advanced lens technologies such as blue light filtering and photochromic adaptations. These innovations address growing consumer concerns about digital eye strain and UV protection. Vertical integration is another critical approach where manufacturers control both production and retail distribution to optimize costs and ensure quality. Brands are increasingly adopting omnichannel retail models that seamlessly blend online and offline experiences to enhance customer convenience. Strategic acquisitions allow larger corporations to expand their product portfolios and enter new market segments efficiently. Sustainability initiatives are gaining prominence as companies introduce eco-friendly materials and recycling programs to appeal to environmentally conscious consumers. Partnerships with telehealth providers facilitate remote eye examinations and streamline prescription processes. Markeco focuses on personalization and digital engagement using augmented reality for virtual try-ons. These strategies collectively enable companies to adapt to evolving consumer preferences and technological advancements while strengthening their market presence.

U.S. EYEWEAR MARKET NEWS

- In March 2023, EssilorLuxottica, a global eyewear giant, launched a new augmented reality feature on its mobile app. This enhancement is anticipated to allow customers to virtually try on frames and strengthen the US eyewear market presence.

- In June 2023, Johnson and Johnson Vision, a contact lens manufacturer, introduced a new daily disposable lens for astigmatism. This launch is anticipated to address unmet patient needs and strengthen the UUS eyewear market presence.e

- In September 2023, CooperCompanies, a vision care leader, initiated a nationwide contact lens blister recycling program. This initiative is anticipated to boost sustainability credentials and strengthen the US eyewear market presence

- In January 2024, Warby Parker, a direct-to-consumer retailer, expanded its physical store footprint by opening fifty new locations. This expansion is anticipated to increase brand accessibility and strengthen the UUSeyewear market presence.e

- In May 2024, EssilorLuxottica, a direct-to-consumer corporation, partnered with a major telehealth provider for remote eye exams. This partnership is anticipated to streamline prescription access and strengthen the US eyewear market presence.

MARKET SEGMENTATION

This research report on the U.S. eyewear market is segmented and sub-segmented into the following categories.

By Product Type

- Spectacles

- Contact Lenses

- Sunglasses

By Distribution Channel

- Retail Users

- Online Stores

- Ophthalmic Clinics

- Others

ThisThisountry

- California

- WashinU.S.U.S.

- Oregon

- New York

- Rest of the United States

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com