U.S. Footwear Market Size, Share, Trends & Growth Forecast Report By Product Type, By Material Type, By Distribution Channel, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Footwear Market Size

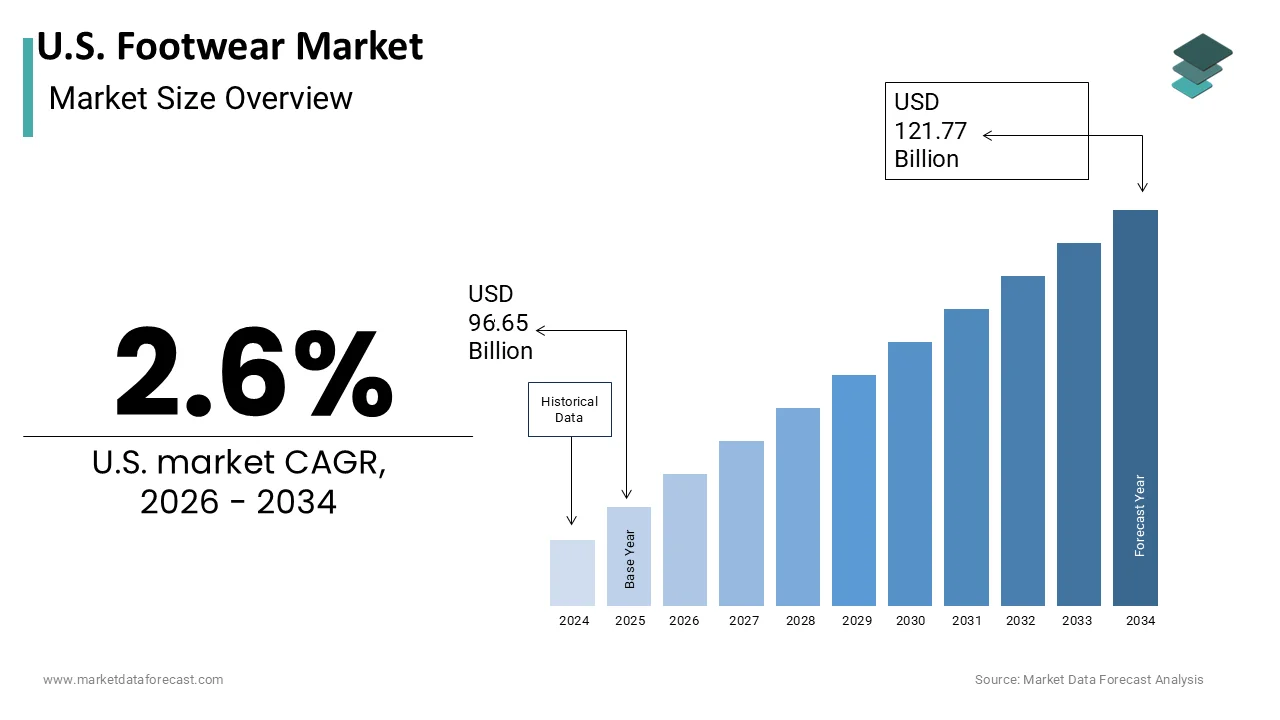

The U.S. Footwear Market was valued at USD 96.65 billion in 2025, is estimated to reach USD 99.16 billion in 2026, and is projected to reach USD 121.77 billion by 2034, growing at a CAGR of 2.6% from 2026 to 2034.

Footwear refers to garments worn on the feet, typically designed for protection against environmental hazards (such as rough terrain or cold), stability, and comfort. This field is deeply influenced by lifestyle trends, health consciousness, and fashion sensibilities rather than functioning solely as a basic necessity. The fundamental role of footwear in daily life ensures consistent demand across all demographic segments. According to consumer data from the Bureau of Labor Statistics, the average American household allocates nearly $480 annually to footwear purchases, reflecting the category's robust and consistent position within non-discretionary personal expenditures. The aging population further amplifies the need for orthopedic and comfort-focused designs as mobility issues become more prevalent. Projections from the U.S. Census Bureau indicate that the number of Americans aged 65 and older is on track to reach an estimated 84.3 million by 2060, driving a massive, structurally sound market for supportive, ergonomic, and fall-preventative footwear.

Additionally, the rise of remote work has shifted consumer preferences towards comfortable yet presentable footwear suitable for home and hybrid work environments. This shift has spurred innovation in materials and design, leading to the development of hybrid styles that blend aesthetic appeal with functional support. The market is thus defined by a convergence of health awareness, technological advancement, and changing work cultures where consumer choices are increasingly driven by the desire for versatility and well-being rather than traditional fashion cycles alone.

MARKET DRIVERS

Rising Health Consciousness and Participation in Fitness Activities

The increasing emphasis on health and wellness, coupled with high participation rates in fitness activities, es is a key driver for the growth of the athletic and performance footwear segment within the United States footwear market. Consumers are increasingly recognizing the importance of proper footwear in preventing injuries and enhancing performance during physical activities. According to the Sports and Fitness Industry Association (SFIA), over 75% of Americans participate in fitness activities or sports annually, with massive baseline categories like fitness walking and jogging driving an unyielding demand for specialized athletic footwear. Running remains one of the most popular activities. This high replacement frequency drives consistent volume sales for major brands. Furthermore, the trend towards cross-training and high-intensity interval training has expanded the need for versatile footwear that supports multiple types of movement. The American Podiatric Medical Association (APMA) emphasizes that wearing anatomically appropriate footwear is critical to reducing structural strain and preventing common overuse injuries like plantar fasciitis and shin splints. This medical endorsement encourages consumers to invest in high-quality footwear rather than opting for cheaper alternatives.

Additionally, corporate wellness programs and community fitness events further promote an active lifestyle,s thereby sustaining demand. The integration of smart technology in shoes for tracking steps and performance metrics also appeals to tech-savvy fitness enthusiasts. These factors collectively ensure that the athletic footwear segment remains a dominant force in the market.

Influence of Streetwear Culture and Sneakerhead Phenomenon

The pervasive influence of streetwear culture and the sneakerhead phenomenon greatly fuels demand in the United States footwear market. This demand is particularly high within the casual and luxury segments. Sneakers have transcended their athletic origins to become symbols of status, identity,y and cultural expression. Cowen & Co. framed sneakers as a legitimate alternative asset class, mapping a secondary market trajectory projected to climb to $30 billion globally by 2030. Limited edition releases and collaborations between major brands and celebrities or designers create hype and urgency among consumers. Social media platforms play a crucial role in amplifying this trend, nd with influencers showcasing rare collections and styling tips to millions of followers. This cultural shift has led traditional fashion houses to enter the sneaker market, blurring the lines between high fashion and streetwear. The emotional connection consumers feel towards specific brands and models fosters deep loyalty and repeat purchases. Furthermore, the customization options offered by brands allow individuals to create unique pairs, enhancing the personal value of the product. This cultural momentum ensures that the casual footwear segment continues to experience robust growth driven by social validation and artistic expression.

MARKET RESTRAINTS

Volatility in Raw Material Prices and Supply Chain Disruptions

The fluctuation in raw material prices and ongoing supply chain disruptions are significant barriers to the profitability and stability of the United States footwear market. Key materials such as leather, er rubber, and synthetic fabrics are subject to global commodity price swings which directly impact manufacturing costs. Data from the Bureau of Labor Statistics indicates that core manufacturing input categories, including synthetic polymers and rubber commodities, have faced distinct price volatility, directly impacting raw material overhead for the footwear assembly sector. These cost increases are often difficult to pass on to price-sensitive consumers, leading to compressed profit margins for manufacturers and retailers. The pandemic exposed vulnerabilities in global supply chains, with port congestion and shipping delays affecting the timely delivery of goods. The Federal Reserve Bank of New York’s Global Supply Chain Pressure Index marks a severe re-escalation in logistical volatility, with shipping tensions spiking the index and significantly lengthening international transit lead times. Footwear companies relying on just-in-time inventory systems have faced stockouts and an inability to meet sudden spikes in demand.

Additionally, trade policies and tariffs on imports from key manufacturing hubs such as Vietnam and China add another layer of complexity and cost. These factors create uncertainty in production planning and pricing strategies, making it difficult for companies to maintain consistent product availability. Small and medium-sized enterprises are particularly vulnerable as they lack the bargaining power to negotiate better terms with suppliers. Consequently, the industry faces challenges in maintaining competitive pricing while ensuring quality and reliability.

Environmental Regulations and Sustainability Compliance Costs

Strict environmental regulations and the high costs associated with sustainability compliance are major limitations for manufacturers within the United States footwear market. Consumers and regulatory bodies are increasingly demanding eco-friendly practices, which require substantial investments in sustainable materials and production processes. Global life-cycle assessments show that with global footwear manufacturing scaling past 20 billion pairs annually, the industry presents a massive post-consumer waste challenge, as a vast majority of worn shoes ultimately end up in municipal landfills. New state-level regulations aimed at reducing plastic waste and promoting circular economy principles require companies to redesign products and implement recycling programs. These additional expenses strain budgets, particularly for smaller brands that operate on thin margins. Furthermore,e the lack of standardized definitions for terms like sustainable and eco-friendly creates confusion and potential legal risks for marketers. The Federal Trade Commission enforces strict guidelines on environmental marketing claims, requiring companies to substantiate their assertions with scientific evidence. Failure to comply can result in hefty fines and reputational damage.

Additionally, the limited availability of scalable, sustainable materials poses a challenge for mass production. Companies must balance the demand for green products with the economic reality of higher production costs. This regulatory landscape creates a complex operating environment where innovation is necessary but financially burdensome.

MARKET OPPORTUNITIES

Expansion of Direct-to-Consumer E-Commerce Platforms

The expansion of direct-to-consumer e-commerce platforms offers a significant opportunity for footwear brands to enhance customer engagement and improve profit margins, which is expected to propel the growth of the United States footwear market. By bypassing traditional retail intermediaries, companies can establish direct relationships with consumers, rs allowing for greater control over branding and data collection. This shift enables brands to offer personalized shopping experiences through virtual-on technologies and AI-driven recommendations. Shopify demonstrates that customer interactions with product pages utilizing augmented reality (AR) content yield a 94% higher conversion rate on average compared to standard listings, dramatically elevating buyer confidence and reducing return rates. Direct-to-consumer models also allow for faster feedback loops, enabling companies to respond quickly to changing trends and consumer preferences. The ability to collect first-party data helps in creating targeted marketing campaigns that resonate with specific demographics. Furthermore, subscription services for children's footwear or running shoes provide recurring revenue streams and enhance customer loyalty. The reduction in overhead costs associated with physical retail spaces allows brands to invest more in product innovation and digital marketing. As logistics networks improve and delivery speeds increase, the appeal of online shopping continues to grow. This digital transformation offers a pathway for brands to differentiate themselves and capture market share in an increasingly competitive landscape.

Innovation in Sustainable and Circular Footwear Solutions

The growing consumer demand for sustainable and circular footwear solutions paves the way for manufacturers to innovate and differentiate their offerings, which is anticipated to boost the expansion of the United States footwear market. Environmental consciousness is increasingly influencing purchasing decisions, with many consumers seeking products that minimize ecological impact. In response, several footwear brands have introduced shoes made from recycled ocean plastic, mushroom leather, and other biobased materials. The Ellen MacArthur Foundation highlights that transitioning to a circular economy model designed to eliminate waste and circulate materials can unlock over a trillion dollars in global economic value while drastically decreasing dependence on virgin resources. Brands that adopt take-back programs, where customers return old shoes for recycling, build stronger loyalty and trust. By investing in sustainable technologies, companies can appeal to the discerning demographic of millennials and Generation Z. Additionally,y regulatory pressures regarding waste management are expected to tighten, en making early adoption of circular practices a strategic advantage. Collaborations with material science startups can lead to breakthroughs in biodegradable soles and uppers. This shift not only mitigates environmental impact but also opens new avenues for brand storytelling and market leadership in the green economy.

MARKET CHALLENGES

Counterfeit Products and Intellectual Property Theft

The prevalence of counterfeit products and intellectual property theft is an impediment to the integrity and profitability of the United States footwear market. Fake footwear not only undermines brand reputation but also poses safety risks to consumers due to inferior materials and construction. Joint market data published by the OECD and EUIPO reveals that counterfeit footwear leads global seizure cases within the multi-billion-dollar illicit fashion trade, inflicting severe revenue losses on legitimate manufacturers. Online marketplaces have exacerbated this issue by providing easy access to fake products that closely mimic authentic designs. Enforcement data from U.S. Customs and Border Protection (CBP) highlights the staggering scale of intellectual property theft, with officers intercepting millions of counterfeit apparel and footwear items annually at national ports of entry. Consumers often struggle to distinguish between genuine and fake items, especially when purchasing online, leading to dissatisfaction and erosion of brand trust. Legal efforts to combat counterfeiting are costly and time-consuming, with varying degrees of success across different jurisdictions.

Additionally,y the rapid pace of design replication means that new styles are copied almost immediately after launch, reducing the window for exclusive sales. This constant threat forces companies to invest heavily in anti-counterfeit technologies such as holograms and blockchain verification. However, these measures add to production costs and complexity. The presence of counterfeits also distorts market data and consumer perception,n making it difficult for brands to accurately assess demand and plan production.

Labor Shortages and Skilled Workforce Gaps

Labor shortages and gaps in skilled workforce availability are a persistent challenge for the footwear retail and manufacturing sectors in the country, which negatively impacts the expansion of the United States footwear market. The market relies heavily on retail staff for customer service and specialized workers for custom fitting and repair services. Seasonal hiring data tracked by the National Retail Federation (NRF) underscores the industry's massive scale, with major retailers routinely looking to onboard over 500,000 workers during peak shopping seasons to handle logistical and storefront demands. This shortage impacts the quality of customer experience and operational efficiency in physical stores. Additionally, ly the decline in vocational training for cobblers and shoe repair technicians has led to a scarcity of skilled labor for maintenance and customization services. Long-term projections from the Bureau of Labor Statistics highlight the consolidation of legacy craft sectors, indicating that specialized shoe and leather repair roles remain a highly niche, stable field matching a small but dedicated consumer demand for high-end product restoration. This trend limits the ability of brands to offer value-added services such as resoling and refurbishing, which are becoming increasingly important in the context of sustainability. High turnover rates in retail positions further exacerbate the problem, leading to increased recruitment and training costs. Companies are struggling to find employees with the necessary product knowledge and soft skills to engage effectively with customers. The reliance on temporary or part-time workers often results in inconsistent service quality. Addressing these labor challenges requires significant investment in training programs and employee retention strategies, which can strain resources,s particularly for smaller retailers.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Material Type, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, and the rest of the United States |

| Market Leaders Profiled | Nike, Inc., Adidas AG, Puma SE, Skechers U.S.A., Inc., Under Armour, Inc., New Balance Athletics, Inc., VF Corporation, Wolverine World Wide, Inc., Deckers Outdoor Corporation, Crocs, Inc., ASICS Corporation, Steve Madden Ltd. |

SEGMENTAL ANALYSIS

By Product Type Insights

The non-athletic footwear segment dominated the United States market and accounted for a 61.3% share in 2025. This dominance of the segment was driven by its essential role in daily professional, social, and casual activities. Unlike athletic shoes, which are often reserved for specific activities, non-athletic footwear, including loafers, boots, sandals, and dress shoes, is required for everyday wear across various settings. The Bureau of Labor Statistics confirms that while the average full-time employee logs roughly 8 hours of daily work, a widespread post-pandemic shift toward hybrid structures and casual dress codes has heavily decentralized traditional expectations for formal business footwear. This consistent requirement ensures a steady baseline demand that surpasses the intermittent usage patterns of specialized sports shoes. Furthermore, re the diversity of styles within this segment allows consumers to own multiple pairs for different occasions, such as work parties and casual outings. The fashion industry continuously introduces new trends in non-athletic designs, encouraging frequent updates and replacements. This higher frequency of purchase drives revenue and volume dominance. Additionally, the aging population requires supportive yet stylish non-athletic options for daily mobility, further cementing this segment's leadership through demographic necessity and lifestyle integration.

Furthermore, the top position of the non-athletic footwear segment is further reinforced by the shift towards hybrid work models, which have blurred the lines between formal and casual attire. Consumers now seek versatile footwear that is comfortable enough for home use yet presentable for occasional office visits or video calls. Brands have responded by introducing hybrid designs such as dress sneakers and ergonomic loafers that cater to this new normal. This trend reduces the need for separate categories of strictly formal or strictly casual shoes, consolidating demand into the non-athletic segment. Additionally, the rise of remote work has decreased the wear and tear on traditional dress shoes but increased the desire for high-quality, comfortable alternatives that can be worn for longer periods indoors. The ability of non-athletic footwear to adapt to these changing lifestyle dynamics ensures its continued relevance and market leadership. Consumers are willing to invest in premium non-athletic pieces that offer durability and comfort for all-day wear, driving value growth in this dominant segment.

On the contrary, the athletic footwear segment is anticipated to witness the fastest CAGR of 5.5% from 2026 to 2034 due to the increasing participation in health and fitness activities among Americans. According to the Sports and Fitness Industry Association (SFIA), over 75% of the U.S. population participates in fitness or sports activities annually, establishing a massive, highly resilient baseline of consumer demand for performance-driven shoes. This widespread adoption of active lifestyles creates a consistent and growing demand for specialized performance footwear. Running remains the most popular activity. This high replacement cycle ensures recurring revenue for athletic brands. Furthermore,e the trend toward cross-training and high-intensity interval training has expanded the need for versatile athletic shoes that support multiple types of movement.

Additionally, corporate wellness programs and community fitness events promote active living, further sustaining demand. The integration of smart technology in athletic shoes for tracking performance metrics also appeals to tech-savvy consumers. These factors collectively fuel the rapid growth of the athletic footwear segment as health consciousness becomes a central pillar of the American lifestyle.

This fast-growing segment is pushed forward by the pervasive influence of sneaker culture and strategic celebrity collaborations. Athletic shoes have transcended their functional purpose to become symbols of status and cultural expression. Limited edition releases and collaborations between major brands and celebrities or designers create hype and urgency among consumers. Social media platforms amplify this trend with influencers showcasing rare collections to millions of followers. This cultural shift has led traditional fashion houses to enter the athletic footwear space, blurring the lines between sportswear and high fashion. The emotional connection consumers feel towards specific brands fosters deep loyalty and repeat purchases. Furthermore, re-customization options allow individuals to create unique pairs, enhancing personal value. This cultural momentum ensures that the athletic footwear segment continues to experience robust growth driven by social validation and artistic expression rather than just utility.

By Material Type Insights

The leather segment led the United States footwear market and captured a 33.7% share in 2025. This leading position of the segment was attributed to its unparalleled durability, comfort,t and premium aesthetic appeal. Consumers associate leather with quality and longevity,ity making it the preferred choice for formal boots and high-end casual shoes. The U.S. Department of Agriculture (USDA) confirms that the United States is one of the world's largest producers of raw cattle hides. However, because the vast majority are exported for overseas tanning, the global footwear industry relies on international processing hubs to convert these hides into finished material. A study demonstrates that premium leather footwear can last up to 10 years with proper maintenance, significantly outlasting most synthetic alternatives. This long lifespan justifies the higher initial cost for many consumers who view leather shoes as long-term investments. Research highlights that genuine leather possesses natural breathability, allowing it to regulate temperature and dissipate moisture to enhance foot comfort during extended wear. This functional benefit is particularly valued in professional settings where shoes are worn for long hours.

Additionally, leather ages gracefully,y developing a unique patina that adds character and value over time. This perception drives demand in the premium segment, which contributes significantly to market revenue. Furthermore, the advancements in tanning technologies have made leather more resistant to water and stains, addressing previous maintenance concerns. These factors collectively sustain the dominance of leather as the primary material in the US footwear market.

Moreover, the domination of the leather segment is further supported by a well-established supply chain and manufacturing infrastructure in the United States. Decades of expertise in leather processing and shoe-making have created a robust ecosystem that ensures consistent quality and availability. This skilled labor force enables manufacturers to produce high-quality leather footwear efficiently, meeting domestic demand. Major footwear brands have long-standing relationships with leather suppliers, ensuring priority access to premium hides. This stability reduces supply chain risks and allows for consistent product offerings.

Additionally, the presence of specialized tanneries in states like Wisconsin and New York provides localized sourcing options that reduce transportation costs and environmental impact. The Leather Industries of America organization advocates for sustainable practices that enhance the reputation of US leather globally. This strong infrastructure supports innovation in leather treatments and finishes, allowing brands to differentiate their products. The reliability of the leather supply chain, in combination with consumer trust in the material, ensures its continued leadership in the footwear market.

But the fabric material segment is likely to experience the fastest CAGR of 6.2% during the forecast period due to the increasing consumer preference for lightweight and breathable footwear suitable for active and casual lifestyles. Fabric shoes offer superior flexibility and ventilation compared to traditional materials, making them ideal for warm climates and intense physical activities. Innovations in textile technology have enhanced the durability and water resistance of fabrics,s addressing previous limitations. These advancements have expanded the application of fabric beyond athletic shoes to include casual and work footwear. Additionally, ly the softness and adaptability of fabric break-in in time, appealing to consumers who prioritize immediate comfort. The rise of remote work has further accelerated this trend as individuals seek comfortable yet presentable footwear for home and virtual meetings. These factors collectively drive the rapid expansion of the fabric segment.

A further key factor accelerating the growth of the fabric segment is the strong alignment with sustainability initiatives and the use of recycled materials. Consumers are increasingly environmentally conscious and prefer footwear made from eco-friendly sources. Major footwear brands have committed to using recycled polyester and nylon derived from plastic bottles and fishing nets in their fabric collections. This environmental benefit resonates with millennial and Generation Z consumers who prioritize ethical consumption. Brands like Allbirds and Rothys have built their entire business models around sustainable fabric footwear, gaining significant market share.

Additionally, the government incentives for using sustainable materials further support this trend. The ability to recycle fabric shoes at the end of their life cycle also appeals to eco-conscious buyers. As regulatory pressures regarding plastic waste tighten, the adoption of fabric materials offers a viable solution for brands aiming to meet sustainability goals. This strategic alignment with environmental values ensures the continued rapid growth of the fabric segment.

By Distribution Channel Insights

The online sales segment was the largest by occupying a 31.5% share of the United States footwear market in 2025 because of the unparalleled convenience and extensive product variety they offer. Consumers can browse thousands of styles, es compare prices, and read reviews from the comfort of their homes, eliminating the need for physical store visits. This shift is driven by the busy lifestyles of modern consumers who value time efficiency. Online platforms also offer detailed product information, including size guides and material descriptions, which help consumers make informed decisions. The ability to access global brands and niche products further enhances the appeal of online shopping.

Additionally, flexible return policies have reduced the perceived risk of buying shoes online, increasing consumer confidence. Major retailers have invested in user-friendly websites and mobile apps that streamline the shopping experience. The integration of customer service chatbots and virtual assistants provides immediate support, addressing queries and issues promptly. These factors collectively sustain the dominance of online sales as the primary distribution channel for footwear in the United States.

In addition, the leadership of the online sales channel is further reinforced by the integration of advanced digital technologies such as augmented reality and artificial intelligence. These tools enhance the shopping experience by allowing consumers to visualize how shoes will look on their feet and receive personalized recommendations. Virtual try-on technologies have mitigated the hesitation associated with buying footwear online, reducing return rates. AI-driven algorithms analyze browsing history and purchase behavior to suggest relevant products, improving discovery and satisfaction. Online platforms also leverage data analytics to optimize inventory management and pricing strategies, es ensuring competitive offers. Subscription services for children's footwear or running shoes provide recurring revenue streams and enhance customer loyalty. The seamless integration of social media shopping allows users to purchase directly from advertisements, simplifying the journey from discovery to checkout. These technological advancements create a compelling value proposition that attracts and retains customers, ensuring the continued dominance of the online sales channel.

On the other hand, the footwear specialists segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 4.8% between 2026 and 2034, owing to the demand for expert guidance and specialized product offerings that general retailers cannot provide. Specialty stores employ trained staff who can assess foot structure and recommend appropriate shoes,s ensuring optimal comfort and health. These stores often carry niche brands and orthopedic options that are unavailable in mass market outlets. The personalized service includes gait analysis and custom fitting, ing which enhances customer satisfaction and loyalty. Additionally, all specialty retailers offer repair and maintenance services, extending the life of footwear and adding value. The rise of running clubs and fitness communities has also boosted demand for specialized athletic footwear available at dedicated stores. These factors collectively drive the rapid growth of the footwear specialists channel as consumers seek tailored solutions for their unique needs.

This rapid growth is largely propelled by the focus on premium and niche brand experiences that appeal to discerning consumers. Specialty stores curate collections of high-end and exclusive brands that cater to specific lifestyles and aesthetics. Specialty retailers create immersive shopping environments with knowledgeable staff who can tell the story behind each brand. This experiential retail approach builds emotional connections and justifies premium pricing. Consumers value the exclusivity and authenticity offered by specialty stores, which differentiates them from generic online platforms.

Additionally, these stores often host events and workshops that engage the local community,y fostering brand loyalty. The ability to touch and feel high-quality materials before purchase remains a significant advantage for specialty retailers. As consumers become more educated about footwear craftsmanship and heritage, the demand for specialized retail experiences continues to rise. This focus on quality and exclusivity ensures the continued rapid expansion of the footwear specialists channel.

COUNTRY MARKET ANALYSIS

U.S. Footwear Market Analysis

The United States outperformed other regions in the North American footwear market and captured a 80.8% share in 2025. This expansion of the US market was supported by the country's large population, high disposable income, and advanced retail infrastructure. The market status is characterized by a mature yet dynamic environment where innovation and consumer preferences drive continuous evolution. According to U.S. Census Bureau estimates, the national population has surpassed 342 million, with a highly dynamic consumer base actively participating in macro fitness and lifestyle fashion trends. The high prevalence of health awareness campaigns has educated consumers about the importance of proper footwear,r leading to increased demand for athletic and orthopedic shoes. The Centers for Disease Control and Prevention (CDC) indicates that while nearly half of U.S. adults meet federal aerobic exercise benchmarks, less than 25% achieve the full recommended combination of aerobic and strength training, highlighting an ongoing need for health advocacy and high-performance footwear.

Additionally, the United States has a robust regulatory framework enforced by the Consumer Product Safety Commission, which ensures product safety and quality by building consumer trust. The presence of major global headquarters and innovative startups fosters intense competition, resulting in a wide array of product options. High disposable income levels allow consumers to purchase multiple pairs for different occasions, contributing to market volume. The trend towards sustainability is particularly strong, with many brands adopting eco-friendly materials and practices. Furthermore, the rise of e-commerce and digital marketing has transformed the retail landscape, enabling direct-to-consumer engagement. These structural, demographic, and economic factors solidify the United States as the leading market for footwear in the region,n with sustained growth potential driven by health consciousness and technological advancements.

COMPETITIVE LANDSCAPE

The competition in the United States footwear market is intense and characterized by a mix of established global conglomerates and agile niche brands. Major players leverage their extensive distribution networks and brand recognition to maintain dominance, while newer entrants disrupt the market with innovative, sustainable solutions. The rivalry is further amplified by the increasing convergence of performance technology and fashion, where aesthetic appeal competes with functional benefits. Companies are constantly innovating to offer lightweight, durable, and eco-friendly materials to meet diverse consumer needs. Price competition is fierce, particularly in the mass market segment where private labels offer affordable alternatives. Traditional brands face pressure to adapt to digital-first strategies and direct-to-consumer models that enhance customer retention. The threat of substitution from alternative footwear types also influences competitive dynamics. Brand loyalty is cultivated through transparent communication and social advocacy initiatives. Regulatory compliance and product safety serve as critical factors in building consumer trust. Overall, the market demands continuous adaptation to technological trends and societal values to sustain competitive advantage and profitability in this evolving industry landscape.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. Footwear Market include

- Nike, Inc.

- Adidas AG

- Puma SE

- Skechers U.S.A., Inc.

- Under Armour, Inc.

- New Balance Athletics, Inc.

- VF Corporation

- Wolverine World Wide, Inc.

- Deckers Outdoor Corporation

- Crocs, Inc.

- ASICS Corporation

- Steve Madden Ltd.

TOP LEADING PLAYERS IN THE MARKET

- Nike Inc remains a dominant force in the United States footwear landscape by consistently driving innovation in athletic performance and lifestyle design. The company leverages its strong brand equity to connect with consumers through compelling storytelling and high-profile athlete endorsements. Recently,y Nike has focused on digital transformation by enhancing direct-to-consumer platforms and mobile applications to offer personalized shopping experiences. The corporation actively invests in sustainable manufacturing processes,s such as the Move to Zero initiative, which aims to reduce carbon emissions and waste. By introducing advanced materials like Flyknit and Air technology,gy Nike maintains its reputation for quality and performance. These strategic efforts strengthen customer loyalty and ensure the brand remains at the forefront of both sports and fashion trends in the competitive US market.

- Adidas AG contributes significantly to the US footwear market by blending athletic functionality with streetwear culture and sustainability initiatives. The company is renowned for its Boost technology and collaborations with high-profile designers and celebrities that drive consumer excitement. Recently,y Adidas has prioritized circular economy principles by launching footwear made from recycled ocean plastics and other sustainable materials. The brand actively engages with younger demographics through social media campaigns and community events that promote inclusivity and creativity. Adidas also strengthens its position by expanding its direct-to-consumer channels and improving supply chain efficiency. These actions enhance brand relevance and appeal to environmentally conscious consumers while maintaining a strong presence in both performance sports and casual lifestyle segments across the United States.

- VF Corporation plays a pivotal role in the US footwear market through its diverse portfolio of iconic brands, including Vans T, Timberland, and The North Face. The company focuses on delivering specialized footwear that caters to outdoor enthusiasts and urban consumers. Recently,y VF Corporation has invested heavily in digital capabilities and data analytics to better understand consumer preferences and optimize inventory management. The corporation emphasizes sustainability by setting ambitious goals for reducing environmental impact across its supply chain. VF also strengthens its market position by expanding retail presence in key urban locations and enhancing e-commerce platforms. By leveraging the unique identities of its brands, VF Corporation captures diverse market segments and fosters deep connections with consumers who value authenticity, durability,lity and style in their footwear choices.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States footwear market employ several strategic initiatives to maintain competitiveness and drive growth. Product innovation remains a primary strategy with companies investing heavily in advanced materials and sustainable technologies to appeal to environmentally conscious consumers. Brands are increasingly adopting direct-to-consumer models and subscription services to enhance customer convenience and loyalty. Digital marketing and social media engagement are crucial for connecting with younger demographics and building brand communities. Strategic partnerships with athletes and influencers help amplify brand visibility and credibility. Companies are also focusing on supply chain resilience by diversifying sourcing and implementing automation. Price competitiveness is maintained through efficient operations and private label offerings. Regulatory compliance and transparency in sustainability claims are prioritized to build consumer trust. These strategies collectively enable companies to adapt to evolving preferences and strengthen their market presence effectively.

MARKET SEGMENTATION

This research report on the U.S. footwear market is segmented and sub-segmented into the following categories.

By Product Type

- Athletic Footwear

- Non-Athletic Footwear

By Material Type

- Leather

- Rubber

- Plastic

- Fabric

- Others

By Distribution Channel

- Online Sales

- Footwear Specialists

- Supermarkets & Hypermarkets

- Brand Outlets

- Others

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com