U.S. Frozen Pizza Market Size, Share, Trends & Growth Forecast Report By Type, By Distribution Channel, By Product, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Frozen Pizza Market Size

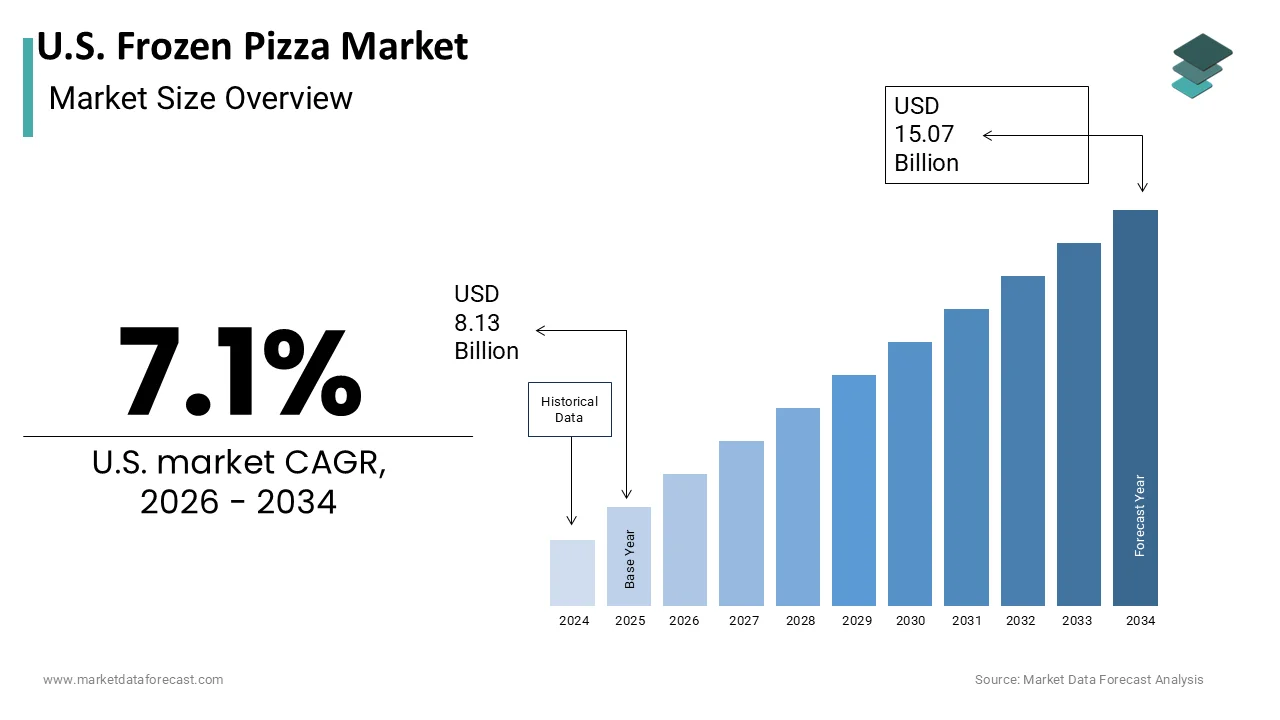

The U.S. Frozen Pizza Market was valued at USD 8.13 billion in 2025, is estimated to reach USD 8.71 billion in 2026, and is projected to reach USD 15.07 billion by 2034, growing at a CAGR of 7.1% from 2026 to 2034.

Frozen pizza is defined as a pre-prepared meal product that requires minimal preparation time, typically involving baking or microwaving, and serves as a staple for quick dinners and casual gatherings. This category has transcended its historical perception as a low-quality emergency meal to become a sophisticated culinary option featuring artisanal crusts, premium toppings, and health-conscious formulations. The cultural integration of pizza in American diets is profound, with data from the USDA indicating that approximately 11 percent of the US population consumes pizza on any given day. This high frequency of consumption underscores the deep-rooted demand for convenient, ready-to-eat solutions. Furthermore, the proliferation of single-person households, which the US Census Bureau states now accounts for approximately 29 percent of all households, drives the need for portion-controlled and easily storable meal options. The operational efficiency of frozen logistics allows for widespread distribution across urban and rural landscapes, ensuring consistent availability. As consumers increasingly balance professional commitments with domestic responsibilities, the reliance on shelf-stable, high-quality meal solutions intensifies. The market thus operates at the intersection of convenience, affordability, and evolving gastronomic expectations, reflecting a sector that is resilient to economic fluctuations while remaining sensitive to nutritional trends and ingredient transparency demands.

MARKET DRIVERS

Rising Demand for Convenience Amidst Busy Lifestyles

The accelerating pace of modern life in the country is a key factor for the sustained growth of the United States frozen pizza market. Consumers are increasingly prioritizing time-saving meal solutions without compromising on taste. Dual-income households have become the norm, with the Bureau of Labor Statistics indicating that in married-couple families with children under 18, both parents are employed in 67 percent of cases. This demographic shift significantly reduces the time available for meal preparation, thereby elevating the appeal of ready-to-cook options that can be prepared in under 20 minutes. The psychological burden of decision-making after a long workday, often referred to as decision fatigue, further propels individuals toward familiar and easy-to-prepare foods like frozen pizza. Additionally, the rise of remote work has blurred the lines between professional and personal time, leading to irregular eating schedules where quick meals are preferred over elaborate cooking processes. Data from the American Time Use Survey reveals that Americans spend an average of 0.67 hours (approximately 40 minutes) per day on food preparation and cleanup, highlighting the time constraints faced by the average consumer. Frozen pizza addresses this constraint effectively by offering a complete meal solution that requires minimal effort. The product’s ability to provide immediate satiety with negligible preparation time aligns perfectly with the contemporary consumer’s value proposition of convenience. As urbanization continues to increase, with over 80 percent of the US population residing in urban areas as per the US Census Bureau, the demand for fast, efficient, and reliable meal options remains robust, solidifying the role of frozen pizza as a dietary staple for busy Americans.

Expansion of Premium and Artisanal Product Offerings

The transformation of frozen pizza from a commodity item to a premium culinary experience is a significant growth enabler for the United States frozen pizza market. This shift is fueled by manufacturers introducing high-quality ingredients and gourmet flavors that rival restaurant offerings. Consumers are increasingly willing to pay a premium for products that feature organic cheeses, grass-fed meats, and ancient grain crusts, reflecting a broader trend toward indulgence and quality in home dining. This shift is supported by data from the Specialty Food Association, which notes that sales of specialty foods, including premium frozen items, have grown consistently, with consumers prioritizing clean labels and authentic tastes. The introduction of wood-fired style crusts and internationally inspired toppings such as prosciutto, arugula, and truffle oil has elevated the perceived value of frozen pizza. Major retailers have responded by expanding their premium private label offerings, which now compete directly with established national brands. According to a study, private label products have seen an annual global sales growth of 4.3 percent year over year, indicating strong consumer acceptance of high-quality retail alternatives. This democratization of gourmet dining allows consumers to enjoy restaurant-quality meals at a fraction of the cost, appealing to budget-conscious yet quality-driven shoppers. The innovation in packaging technology also plays a crucial role, with advanced freezing techniques preserving the texture and flavor of fresh ingredients more effectively than in the past. The demand for diverse and sophisticated frozen pizza options is expanding as home cooks become more culinarily sophisticated. Consequently, market growth is being driven by value addition rather than just volume.

MARKET RESTRAINTS

Health Consciousness and Nutritional Concerns

Growing consumer awareness regarding health and nutrition is a major limitation for the United States frozen pizza market. This trend often conflicts with the traditional profile of frozen pizza as a high-sodium and high-calorie food item. Public health initiatives and dietary guidelines have increasingly emphasized the reduction of processed food intake, leading many consumers to scrutinize ingredient lists more closely. The Centers for Disease Control and Prevention states that more than 40 percent of American adults are obese, a statistic that has spurred a nationwide movement toward healthier eating habits and weight management. Frozen pizza, traditionally perceived as a nutrient-poor convenience food, faces skepticism from health-conscious demographics who prioritize whole foods and minimal processing. The high sodium content in many frozen pizzas, which can exceed 700 milligrams per serving, poses a particular concern for individuals managing hypertension or cardiovascular health. As per the American Heart Association, the ideal daily sodium limit is 1,500 milligrams for most adults, though federal guidelines set a maximum ceiling of 2,300 milligrams, meaning a single serving of frozen pizza can contribute a significant portion of this allowance. This nutritional profile discourages regular consumption among health-aware consumers, who may opt for fresh alternatives or homemade versions where they can control ingredient quality. Furthermore, the presence of preservatives and artificial additives in standard frozen pizzas contradicts the clean label trend that dominates current food purchasing decisions. Manufacturers are attempting to reformulate products. However, the entrenched perception of frozen pizza as an unhealthy option remains a barrier to broader adoption among wellness-oriented segments, limiting market penetration in this growing demographic.

Volatility in Raw Material Costs and Supply Chain Disruptions

Volatility in raw material costs, specifically wheat, dairy, and tomato products, is heavily impacting the United States frozen pizza market. These increased costs constrain profit margins and force price hikes that may dampen consumer demand. Agricultural commodities are subject to fluctuating prices due to weather conditions, geopolitical tensions, and supply chain bottlenecks, creating an unstable cost environment for manufacturers. The US Department of Agriculture reports that dairy prices, a critical component for cheese toppings, have experienced significant variability, with milk prices fluctuating by up to 15 percent in recent years due to feed costs and production levels. Similarly, wheat prices, essential for crust production, are influenced by global export restrictions and climate-related crop failures, leading to unpredictable input costs. These fluctuations compel manufacturers to either absorb the costs, thereby reducing profitability, or pass them on to consumers through higher retail prices, which can reduce sales volume in a price-sensitive market. Additionally, supply chain disruptions, such as those caused by labor shortages in transportation and logistics, further exacerbate these challenges. The American Trucking Associations indicate that the trucking industry faces a shortage of over 80,000 drivers, leading to delays and increased freight costs. These logistical hurdles affect the timely distribution of perishable ingredients and finished goods, potentially resulting in stockouts or increased waste. The cumulative effect of rising input costs and logistical inefficiencies creates a challenging operating environment, forcing companies to navigate a delicate balance between maintaining product quality, managing costs, and keeping prices competitive for consumers.

MARKET OPPORTUNITIES

Innovation in Plant-Based and Dietary-Specific Formulations

The development of plant-based and dietary-specific formulations offers a substantial opportunity for the United States frozen pizza market. These products cater to the growing number of consumers with specific dietary restrictions or ethical preferences. The rise of veganism and flexitarianism has created a demand for dairy-free cheeses and meat alternative toppings that do not compromise on taste or texture. According to Gallup, approximately 3 percent of Americans identify as vegan and 5 percent as vegetarian, representing a significant and growing niche market. Furthermore, the prevalence of gluten intolerance and celiac disease, which affects about 1 in 133 Americans as per the Celiac Disease Foundation, drives the need for certified gluten-free crust options. Manufacturers who invest in research and development to create high-quality plant-based cheeses using nuts, soy, or oats can capture this underserved segment. The success of plant-based meat alternatives, with sales reaching 1.4 billion dollars as reported by the Plant Based Foods Association, demonstrates the viability of this market. By integrating these alternatives into frozen pizza offerings, brands can appeal to health-conscious and ethically motivated consumers who previously excluded frozen pizza from their diets. Additionally, the keto and low-carb trends present another avenue for innovation, with cauliflower and almond flour crusts gaining popularity. Retailers are increasingly dedicating shelf space to these specialized products, recognizing their high growth potential. Expanding the product portfolio to include these diet-specific options allows companies to diversify their revenue streams and build brand loyalty among niche consumer groups who are often willing to pay a premium for products that align with their lifestyle choices.

Integration of Smart Packaging and Sustainability Initiatives

The integration of smart packaging and sustainability initiatives opens the door for manufacturers to differentiate their brands and appeal to environmentally conscious consumers, which is expected to boost the expansion of the United States frozen pizza market. As environmental awareness grows, shoppers are increasingly favoring brands that demonstrate a commitment to reducing their ecological footprint. The Environmental Protection Agency states that containers and packaging make up a major portion of municipal solid waste, prompting consumers to seek recyclable or compostable alternatives. Frozen pizza brands that transition to recyclable cardboard boxes and reduce plastic usage can enhance their brand image and attract eco-friendly buyers. Furthermore, the adoption of smart packaging technologies, such as QR codes that provide transparency regarding ingredient sourcing and carbon footprint, can build trust and engagement with modern consumers. A study by IBM indicates that 62 percent of consumers are willing to change their shopping habits to reduce environmental impact, highlighting the commercial value of sustainability. Companies that invest in biodegradable films or reusable packaging systems can position themselves as leaders in corporate social responsibility. Additionally, smart packaging can offer functional benefits, such as indicators that show optimal cooking times or freshness levels, enhancing the user experience. By aligning product development with sustainability goals, manufacturers can not only comply with emerging regulatory standards but also tap into a growing segment of consumers who prioritize ethical consumption. This strategic shift towards greener practices offers a competitive advantage in a crowded market, fostering long-term brand loyalty and opening new avenues for marketing and customer engagement.

MARKET CHALLENGES

Intense Competition from Private Label Brands

The intense competition posed by private-label brands is hindering the growth of the United States frozen pizza market. Store brands are improving in quality and decreasing in price. As a result, they are steadily eroding the market share of national brands. Retailers such as Walmart, Kroger, and Costco have invested heavily in their private label portfolios, offering products that closely mimic the taste and quality of premium national brands at a lower price point. According to a study, private label products now account for over 20 percent of total grocery sales, with the frozen food category seeing particularly strong growth in store brand penetration. This trend is driven by inflationary pressures that make consumers more price-sensitive and willing to switch from established brands to cheaper alternatives. National brands struggle to justify their price premiums when private label options offer comparable quality, forcing them to engage in costly promotional activities that squeeze margins. The agility of private label manufacturers allows them to quickly adapt to trending flavors and dietary preferences, further challenging the innovation lead of national players. Additionally, the exclusive availability of private label products in major retail chains gives these retailers significant leverage in shelf placement and visibility, often relegating national brands to less prominent positions. This dynamic creates a persistent pressure on national brands to continuously innovate and justify their value proposition, while also managing costs to remain competitive. The dominance of private labels in the value segment limits the growth potential for national brands in this price tier, requiring them to focus on premiumization and niche markets to maintain relevance and profitability in an increasingly crowded and competitive landscape.

Regulatory Pressures and Labeling Requirements

Navigating the complex landscape of regulatory pressures and labeling requirements is an ongoing challenge for the United States frozen pizza market. Government agencies are imposing stricter standards on ingredient disclosure, nutritional claims, and food safety. The Food and Drug Administration has updated labeling regulations to require clearer information on added sugars, sodium, and serving sizes, compelling manufacturers to reformulate products or adjust packaging, which incurs additional costs. Compliance with these regulations requires significant investment in legal expertise, quality control, and packaging redesign. Furthermore, the increasing scrutiny of health claims, such as natural or organic, means that manufacturers must ensure rigorous substantiation to avoid legal repercussions and consumer backlash. The Federal Trade Commission monitors advertising practices closely, penalizing companies that make misleading claims about the health benefits of their products. Additionally, state-level regulations, such as California’s Proposition 65, which requires warnings for products containing certain chemicals, add another layer of complexity for national distributors. These regulatory burdens are particularly challenging for smaller manufacturers who may lack the resources to ensure full compliance across multiple jurisdictions. The constant evolution of food safety standards, driven by incidents of contamination or recalls, also necessitates robust tracking and tracing systems, increasing operational costs. Failure to comply can result in hefty fines, product recalls, and damage to brand reputation, which can be difficult to repair. The cost of compliance in the frozen pizza sector continues to rise as consumers become more informed and regulatory bodies become more stringent. Consequently, this poses a persistent challenge to profitability and operational efficiency.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Distribution Channel, Product, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Nestlé S.A., Conagra Brands, Inc., Schwan’s Company, General Mills, Inc., Dr. Oetker GmbH, Bellisio Foods, Inc., Home Run Inn Frozen Foods, Palermo Villa, Inc., Screamin’ Sicilian (Palermo’s Pizza), Totino’s (General Mills, Inc.), DiGiorno (Nestlé S.A.), California Pizza Kitchen, Inc. |

SEGMENTAL ANALYSIS

By Type Insights

The non-vegetarian toppings segment led the United States frozen pizza market by capturing a 61.5% share in 2025. This leading position of the segment was attributed to the deep-rooted cultural preference for meat as a primary protein source in American diets. Pepperoni remains the most popular pizza topping in the nation, with data from YouGov indicating that 64 percent of Americans state they like this topping choice. This preference is reinforced by the widespread availability and affordability of processed meats such as sausage, bacon, and ham, which are staples in the US food supply chain. The USDA reports that the average American consumes approximately 222 pounds of red meat and poultry annually, highlighting the centrality of meat in daily nutrition. Frozen pizza manufacturers leverage this demand by offering generous portions of high-quality meats that appeal to families and individual consumers seeking satiety. The perception of meat-topped pizzas as more substantial and fulfilling compared to vegetarian options further solidifies their market leadership. Additionally, marketing campaigns by major brands often feature meat-heavy varieties as their flagship products, reinforcing consumer association between pizza and meat. The consistency in taste and texture provided by standardized meat toppings also reduces the risk for consumers trying new brands, fostering brand loyalty. The non-vegetarian segment will continue to hold its dominant position in the US, driven by high consumption rates. Furthermore, this position is solidified by established supply chains and consumer habits that prioritize protein-rich meals. The top position of the non-vegetarian segment is further sustained by the perceived value and satiety associated with meat toppings, which consumers view as offering a more complete and satisfying meal experience. In an economic environment where consumers are increasingly mindful of spending, the ability of a single frozen pizza to serve as a hearty dinner for multiple people enhances its appeal. Meat toppings are often perceived as higher-value ingredients compared to vegetables, justifying a slightly higher price point while still maintaining affordability relative to dining out. Data from the Bureau of Labor Statistics shows that food at home prices have risen, prompting consumers to seek cost-effective yet filling meal options. Non-vegetarian pizzas provide a high-calorie and high-protein content that aligns with the dietary needs of active individuals and families. The psychological satisfaction derived from consuming savory, umami-rich meats also plays a crucial role in repeat purchases. Manufacturers often bundle meat toppings with cheese and sauce in ways that maximize flavor impact, creating a sensory experience that vegetarian options struggle to replicate without significant innovation. This combination of nutritional density, perceived value, and sensory appeal ensures that non-vegetarian frozen pizzas remain the preferred choice for the majority of consumers, driving consistent sales volume and market share leadership.

The vegetarian toppings segment is predicted to witness the highest CAGR of 7.3% during the forecast period due to a significant shift toward health-conscious eating and plant-based diets. Consumers are increasingly aware of the health risks associated with high consumption of processed meats, leading them to seek alternatives that offer similar convenience with better nutritional profiles. The Centers for Disease Control and Prevention highlights that chronic diseases linked to diet, such as heart disease and diabetes, are leading causes of death in the US, motivating many to reduce meat intake. As a result, the demand for vegetable-loaded pizzas featuring spinach, mushrooms, peppers, and onions has surged. Data from the Plant Based Foods Association indicates that plant-based food sales have grown by 15 percent in recent years, outpacing total food sales. This trend is particularly strong among millennials and Gen Z consumers, who prioritize wellness and sustainability in their purchasing decisions. Frozen pizza manufacturers are responding by introducing vibrant, nutrient-dense vegetarian options that appeal to these demographics. The use of organic and locally sourced vegetables further enhances the appeal of these products, aligning with the clean label movement. The vegetarian segment is poised for sustained growth as health awareness continues to rise. It is capturing market share from traditional meat-based offerings. Technological advancements in plant-based ingredients are accelerating the growth of the vegetarian frozen pizza segment, enabling manufacturers to create flavorful and textured toppings that rival meat counterparts. Innovations in plant-based cheeses and meat analogues have expanded the variety of vegetarian options available, attracting flexitarians who seek to reduce meat consumption without sacrificing taste. The development of cashew-based mozzarella and pea protein sausages has enhanced the culinary appeal of vegetarian pizzas, making them a viable option for diverse palates. Furthermore, the introduction of global flavors such as Mediterranean vegetables, Indian spiced potatoes, and Asian inspired stir fry toppings has diversified the vegetarian portfolio, appealing to adventurous eaters. Retailers are dedicating more shelf space to these innovative products, recognizing their potential to drive traffic and increase basket size. The versatility of vegetable toppings allows for endless combinations, encouraging experimentation and repeat purchases. As culinary creativity in the vegetarian space expands, the segment is expected to continue its rapid growth, driven by continuous product innovation and evolving consumer preferences for diverse and exciting plant-based meal solutions.

By Distribution Channel Insights

The offline distribution channel segment held the majority share of the United States frozen pizza market in 2025. This supremacy of the segment was credited to the extensive and well-established retail infrastructure that ensures immediate product availability. Supermarkets, grocery stores, and convenience stores are the primary points of purchase for frozen foods, with a significant share of households that shop at supermarkets weekly. The tactile nature of shopping allows consumers to inspect packaging, check expiration dates, and make impulse purchases based on visual appeal and promotional displays. Frozen pizza aisles are strategically located in high-traffic areas, maximizing visibility and accessibility. The ability to physically select products provides a sense of control and confidence for consumers, particularly when trying new brands or flavors. Additionally, the immediate gratification of taking a product home for same-day consumption aligns with the spontaneous nature of meal planning for many families. The widespread presence of retail outlets across urban, suburban, and rural areas ensures that frozen pizza is accessible to a broad demographic. Loyalty programs and in-store promotions further incentivize offline purchases, driving repeat business. Physical retail remains the cornerstone of grocery shopping in the US. Therefore, the offline channel will continue to dominate, supported by its convenience, accessibility, and established consumer habits. Consumer trust and brand visibility play crucial roles in sustaining the dominance of the offline distribution channel for frozen pizza. Established brands invest heavily in shelf placement and in-store marketing to maintain top-of-mind awareness among shoppers. Eye-level placement and end cap displays significantly influence purchasing decisions, with studies showing that products placed at eye level sell more than those on lower shelves. The physical presence of brands in stores reinforces their credibility and reliability, assuring consumers of product quality and safety. Regular interactions with store staff and the ability to seek recommendations also enhance the shopping experience, building long-term loyalty. Furthermore, offline retailers often feature exclusive bundles and discounts that are not available online, attracting price-sensitive consumers. The sensory experience of seeing and touching the product, combined with the immediacy of purchase, creates a compelling value proposition that online channels struggle to replicate. The integration of digital tools such as scan and go technologies in physical stores further enhances the offline experience, blending convenience with traditional shopping benefits. This synergy ensures that offline channels remain the preferred choice for the majority of frozen pizza consumers.

The online distribution segment is estimated to register the fastest CAGR of 9.9% from 2026 to 2034, owing to the rapid expansion of e-commerce platforms and increased digital penetration among consumers. The convenience of browsing a wide variety of products from home, coupled with the ability to compare prices and read reviews, has attracted a growing number of shoppers to online grocery platforms. The proliferation of smartphones and high-speed internet has made online shopping accessible to a broader demographic, including older adults who previously relied on physical stores. Online retailers offer personalized recommendations and targeted promotions based on purchase history, enhancing customer engagement and retention. The ability to schedule deliveries at convenient times further adds to the appeal, particularly for busy professionals and families. As digital literacy increases and consumer comfort with online transactions grows, the online channel is poised for continued expansion, capturing market share from traditional offline retailers. Advancements in cold chain logistics and last-mile delivery services are critical drivers of the rapid growth in the online frozen pizza segment. Improvements in insulated packaging and refrigerated transportation ensure that frozen products arrive at consumers' doorsteps in optimal condition, addressing previous concerns about product quality and safety. Major retailers and third-party delivery services have invested heavily in infrastructure to support frozen food delivery, with companies like Amazon Fresh and Walmart Grocery expanding their cold chain capabilities. The integration of real-time tracking and temperature monitoring technologies provides transparency and reassurance to consumers, enhancing trust in online purchases. Furthermore, the rise of subscription models for regular grocery deliveries encourages habitual online shopping, increasing the frequency of frozen pizza purchases. The online channel will continue to grow as logistical efficiencies improve and delivery costs decrease. This shift offers a seamless and reliable alternative to traditional shopping methods.

By Product Insights

The regular frozen pizza segment was the largest in the United States market by occupying a 44.5% share in 2025. This prominence of the segment was supported by its affordability and broad appeal to mass market consumers. Regular frozen pizzas are priced competitively, making them an accessible option for budget-conscious families and individuals. The Bureau of Labor Statistics notes that food inflation has prompted many households to seek cost-effective meal solutions, boosting sales of value-oriented products. Regular pizzas often feature standard ingredients such as pepperoni, cheese, and sausage, which are familiar and widely accepted by consumers. The economies of scale achieved by large manufacturers allow for lower production costs, which are passed on to consumers in the form of lower retail prices. Promotional activities such as buy one get one free offers and multi-pack discounts further enhance the value proposition, driving volume sales. The widespread availability of regular frozen pizzas in all types of retail outlets, from discount stores to supermarkets, ensures maximum reach and accessibility. This segment benefits from strong brand recognition and loyal customer bases built over decades, making it a staple in many households. As economic pressures persist, the demand for affordable and reliable meal options will continue to support the dominance of the regular frozen pizza segment. Consistency and familiarity are key factors driving the leadership of the regular frozen pizza segment. Consumers value the predictable taste and texture of standard pizzas, which provide a sense of comfort and reliability. Major brands have refined their recipes over the years to deliver a consistent experience that meets consumer expectations. This reliability reduces the perceived risk of purchase, encouraging repeat buys and brand loyalty. The standardization of ingredients and cooking instructions ensures that every pizza meets quality standards, regardless of where it is purchased. Family traditions and nostalgic associations with certain brands also play a role in maintaining the popularity of regular frozen pizzas. Many consumers grew up eating these products and continue to purchase them for their own families, perpetuating intergenerational brand loyalty. The simplicity of regular pizzas also appeals to children and picky eaters, who may be resistant to more complex or exotic flavors. This broad acceptance across age groups and demographics ensures a stable and large customer base. As long as consumers prioritize familiarity and consistency in their meal choices, the regular frozen pizza segment will remain the market leader.

The gourmet frozen pizza segment is anticipated to witness the fastest CAGR of 6.1% over the forecast period. This quick surge of the segment is propelled by the trend toward premiumization and consumer desire for culinary exploration. Shoppers are increasingly willing to pay higher prices for pizzas that feature artisanal crusts, specialty cheeses, and unique toppings such as fig jam, goat cheese, and prosciutto. The Specialty Food Association reports that premium food sales have outpaced overall food sales, reflecting a shift toward quality and indulgence. Gourmet pizzas offer a restaurant-quality experience at home, appealing to foodies and consumers seeking to elevate their dining experiences. The use of high-quality, often organic or locally sourced ingredients enhances the perceived value and taste of these products. Manufacturers are collaborating with renowned chefs and restaurants to create exclusive lines, adding credibility and excitement to the segment. The variety of flavors and textures available in gourmet pizzas encourages experimentation and repeat purchases. As consumers become more adventurous in their eating habits, the demand for sophisticated and diverse frozen pizza options continues to rise, driving rapid growth in this segment. The integration of health and wellness attributes into gourmet frozen pizzas is another significant driver of its fast growth. Many gourmet brands focus on clean labels, organic ingredients, and diet-specific formulations such as gluten-free or keto-friendly options. This alignment with health-conscious trends attracts consumers who seek indulgence without compromising on nutritional values. Data from the International Food Information Council shows that a majority of consumers are trying to limit or avoid certain ingredients, such as artificial preservatives and high fructose corn syrup, favoring natural and wholesome alternatives. Gourmet pizzas often feature whole-grain crusts, vegetable-based sauces, and lean proteins, catering to these preferences. The transparency in sourcing and ingredient listing builds trust and loyalty among health-conscious shoppers. Furthermore, the positioning of gourmet pizzas as occasional treats rather than everyday meals allows consumers to justify the higher price point and calorie content. The intersection of indulgence and wellness is becoming increasingly important. As a result, the gourmet segment is well-positioned for sustained growth, appealing to a discerning and health-conscious consumer base.

COUNTRY LEVEL ANALYSIS

United States Frozen Pizza Market Analysis

The United States dominated the North American frozen pizza market and captured a 82.8% share in 2025. This position of the U.S. market is driven by its vast population and entrenched culinary culture. The market status is characterized by high maturity and intense competition, with established players continuously innovating to maintain relevance in a saturated environment. The position of the US is underpinned by its robust agricultural sector, which ensures a steady supply of key ingredients such as wheat, dairy, and tomatoes. The USDA indicates that the US is one of the largest producers of dairy and ranks in the top five globally for wheat production, providing a competitive advantage in raw material sourcing and cost management. This domestic supply chain resilience supports the industry's ability to meet high domestic demand efficiently. The cultural ubiquity of pizza in the US, where it is consumed by millions daily, creates a stable baseline demand that is resilient to economic downturns. The market is further strengthened by advanced logistics and distribution networks that ensure nationwide availability. As the primary driver of innovation and trend-setting in the frozen food sector, the US influences global market dynamics. The continued evolution of consumer preferences toward convenience, quality, and health ensures that the US market remains dynamic and influential, setting benchmarks for product development and marketing strategies worldwide. In addition, the primary driving factor for the US frozen pizza market is the convergence of convenience culture and demographic shifts toward smaller household sizes. With the US Census Bureau reporting that single-person households now constitute nearly 29 percent of all households, there is a heightened demand for portion-controlled and easy-to-prepare meals. Frozen pizza fits this need perfectly, offering a complete meal with minimal effort. Additionally, the dual income phenomenon, where both parents work in 67 percent of married-couple families with children, as per the Bureau of Labor Statistics, limits time for cooking, further boosting reliance on convenience foods. The economic factor also plays a crucial role, with inflation driving consumers to seek value-oriented meal solutions that are cheaper than dining out but more enjoyable than basic staples. The average American spends 0.67 hours (approximately 40 minutes) a day on food preparation and cleanup, as noted by the American Time Use Survey, highlighting the time poverty that fuels this market. Furthermore, the technological advancements in freezing and packaging have improved product quality, making frozen pizza a viable alternative to fresh takeout. These factors combined create a robust ecosystem where frozen pizza thrives as an essential component of the American diet, driven by structural lifestyle changes and economic realities.

COMPETITIVE LANDSCAPE

The competition in the United States frozen pizza market is intense and characterized by a mix of established multinational corporations and agile private label brands. Major players compete fiercely on product quality, ty innovat, and price to capture the attention of discerning consumers. The market sees continuous launches of premium and gourmet options as brands strive to elevate their image beyond basic convenience food. Private labels have gained significant traction by offering comparable quality at lower prices,s forcing national brands to justify their premiums through superior ingredients and unique flavors. Innovation in health-conscious formulations, such as plant-based meats and cauliflower crusts, has become a key battleground for differentiation. Supply chain efficiency and logistical capabilities are critical competitive advantages,s ensuring consistent availability and cost management. Marketing efforts focus heavily on digital engagement and sustainability narratives to build emotional connections with shoppers. This dynamic environment drives constant evolution, requiring companies to adapt quickly to changing consumer preferences and economic conditions to maintain their competitive edge and market relevance.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. The frozen pizza market includes

- Nestlé S.A.

- Conagra Brands, Inc.

- Schwan’s Company

- General Mills, Inc.

- Dr. Oetker GmbH

- Bellisio Foods, Inc.

- Home Run Inn Frozen Foods

- Palermo Villa, Inc.

- Screamin’ Sicilian (Palermo’s Pizza)

- Totino’s (General Mills, Inc.)

- DiGiorno (Nestlé S.A.)

- California Pizza Kitchen, Inc.

TOP LEADING PLAYERS IN THE MARKET

- Nestlé USA maintains a formidable presence through its iconic DiGiorno and Tombstone brands, which are staples in American freezers. The company focuses heavily on product innovation to cater to evolving consumer preferences for premium and convenient meals. Recent initiatives include the expansion of their rising crust varieties and the introduction of plant-based options to capture health-conscious demographics. Nestlé leverages its extensive distribution network to ensure widespread availability across diverse retail channels. The company invests significantly in marketing campaigns that emphasize quality ingredients and family-friendly meal solutions. Nestlé continuously refines its recipes and packaging technologies. This ensures products remain competitive and appealing to modern households seeking taste and convenience.

- Conagra Brands strengthens its position with a robust portfolio featuring Red Baron and Freschetta, which are recognized for their value and variety. The company actively engages in strategic branding efforts to rejuvenate legacy products and attract younger consumers. Recent actions include the launch of innovative flavor profiles and limited edition offerings that generate buzz and drive trial. Conagra prioritizes supply chain efficiency to maintain competitive pricing and consistent product availability. The firm also emphasizes sustainability initiatives in its packaging to align with the environmental concerns of modern shoppers. Conagra balances affordability with quality improvements to resonate with budget-conscious families. Furthermore, they are expanding their appeal through targeted digital marketing and retail partnerships that improve engagement in the competitive frozen aisle.

- Dr. Oetker operates as a key competitor with its premium Ristorante and Giuseppe Pizzeria lines, which target discerning consumers seeking authentic Italian experiences. The company distinguishes itself through high-quality ingredients and sophisticated flavor combinations that mimic restaurant-style pizzas. Recent strategies involve expanding its gourmet offerings and introducing organic certifications to appeal to health-conscious shoppers. Dr. Oetker invests in advanced freezing technologies to preserve texture and freshness, ensuring a superior eating experience. The brand focuses on niche marketing campaigns that highlight culinary craftsmanship and heritage. By maintaining a strong presence in the premium segment, Dr. Oetker captures market share from consumers willing to pay more for elevated quality. Their commitment to innovation and quality consistency reinforces their reputation as a leader in the upscale frozen pizza category.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States frozen pizza market primarily employ product innovation and premiumization strategies to differentiate their offerings and capture higher value segments. Companies frequently introduce artisanal crusts, organic ingredients, and unique global flavors to appeal to sophisticated palates. Another major strategy involves expanding plant-based and dietary-specific portfolios to cater to vegan, gluten-free, and keto-conscious consumers. Strategic partnerships with retailers for exclusive private label production help manufacturers secure shelf space and volume sales. Digital marketing and social media engagement are utilized extensively to build brand loyalty and reach younger demographics. Additionally, firms invest in sustainable packaging solutions to address environmental concerns and enhance brand image. Price optimization through promotional bundles and multi-pack discounts remains crucial for maintaining competitiveness in the value segment while driving household penetration and repeat purchases across diverse consumer groups.

MARKET SEGMENTATION

This research report on the U.S. frozen pizza market is segmented and sub-segmented into the following categories.

By Type

- Non-Vegetarian Toppings

- Vegetarian Toppings

- Vegan Toppings

By Distribution Channel

- Offline

- Supermarkets and Hypermarkets

- Convenience Stores

- Specialty Stores

- Others

- Online

By Product

- Regular Frozen Pizza

- Premium/Gourmet Frozen Pizza

- Gluten-Free Frozen Pizza

- Stuffed Crust Frozen Pizza

- Thin Crust Frozen Pizza

- Others

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com