U.S Gaming Market Size, Share, Trends & Growth Forecast Report - Segmented By Platform, Revenue Model, Genre, Gamer Demographic, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S Gaming Market Size

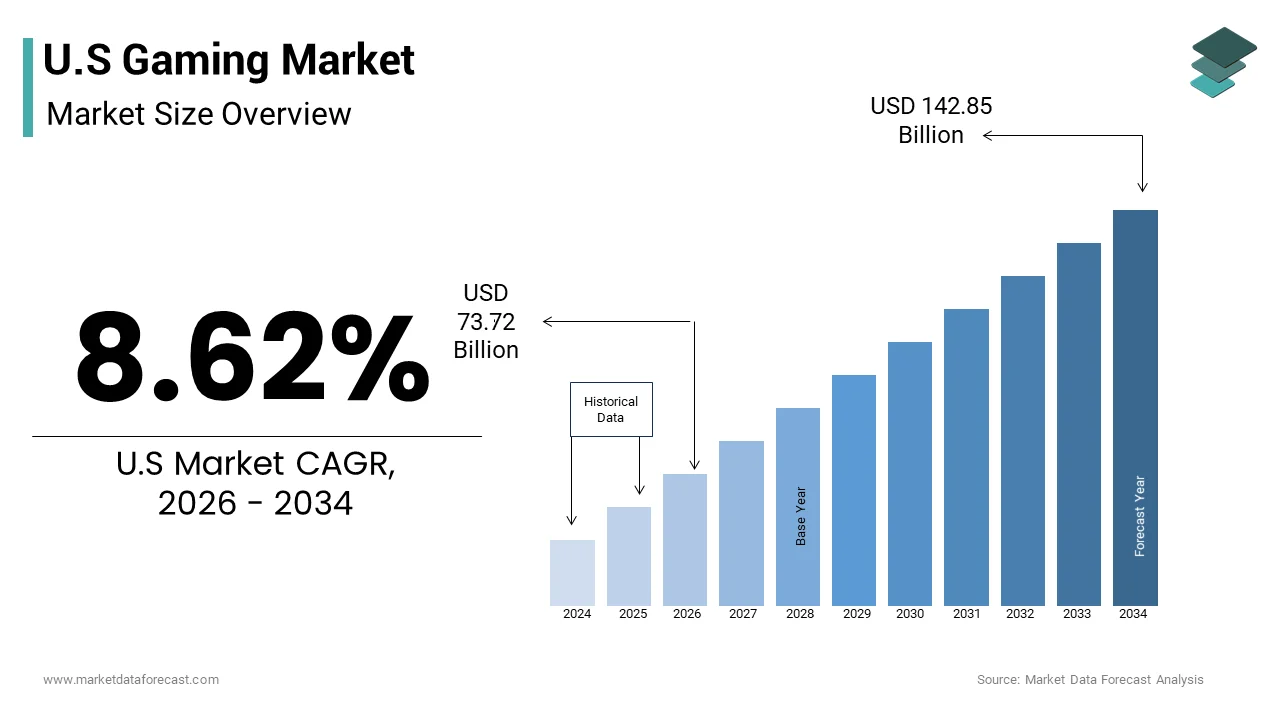

The U.S gaming market size was valued at USD 67.87 billion in 2025 and is anticipated to reach USD 73.72 billion in 2026 to reach USD 142.85 billion by 2034, growing at a CAGR of 8.62% during the forecast period from 2026 to 2034.

Current Market Overview and Definition

The gaming is the development distribution and consumption of interactive entertainment software across consoles personal computers and mobile devices. As per the Entertainment Software Association, approximately 65% of Americans play video games regularly indicating deep cultural integration. The definition of this market extends beyond traditional retail sales to include digital downloads subscription services and in game microtransactions which now constitute the majority of revenue streams. According to a study, nearly 90% of teenagers report playing video games suggesting that future consumer bases are already established. The industry is defined by rapid technological innovation including cloud gaming virtual reality and artificial intelligence integration which continuously reshape user experiences. Hardware manufacturers software developers and platform holders operate within a complex ecosystem driven by intellectual property licensing and network effects. The employment in software publishing and related gaming sectors has grown significantly reflecting the labor intensive nature of modern game development. The market is also characterized by intense competition for user attention amidst a saturated content.

MARKET DRIVERS

Ubiquitous Mobile Device Penetration Expands Accessibility

The widespread adoption of smartphones and tablets are lowering barriers to entry and enabling casual play anywhere, which is a significant factor propelling the growth of the United States gaming market. Mobile gaming has democratized access to interactive entertainment allowing individuals who do not own dedicated consoles or high-end PCs to participate actively. As per the research, approximately 85% of American adults own a smartphone providing a massive installed base for mobile game developers. This ubiquity facilitates impulse downloads and frequent short session play which drives high engagement metrics and ad-based revenue models. The convenience of mobile platforms appeals to broader demographics including older adults and non-traditional gamers, who prefer intuitive touch controls over complex controller inputs. The integration of social features within mobile apps further enhances retention by allowing users to compete with friends and family seamlessly. Additionally, the improvement in mobile hardware capabilities enables more sophisticated graphics and gameplay mechanics narrowing the quality gap with traditional platforms.

Immersive Social Connectivity Enhances User Retention

The evolution of video games into social platforms, where players interact collaborate and compete in real time by fostering strong community bonds is additionally leveraging the growth of the United states gaming market. Modern multiplayer titles function as virtual gathering spaces that transcend geographical limitations offering shared experiences that rival traditional social activities. As per the Entertainment Software Association, nearly 70% of gamers play with others online emphasizing the social dimension of gaming. This connectivity increases user stickiness as players invest time in building relationships and reputations within these digital ecosystems. The rise of cross platform play allows friends to connect regardless of their chosen hardware further expanding the potential player pool for any given title. The integration of voice chat streaming tools and emotes facilitates richer communication making gaming a primary mode of socialization for many younger demographics. Furthermore, the emergence of esports and live service events creates communal moments that drive spikes in engagement and media coverage. These social dynamics transform gaming from a solitary activity into a collective cultural phenomenon ensuring sustained interest and recurring revenue through battle passes and cosmetic items that signal status within the community.

MARKET RESTRAINTS

Regulatory Scrutiny on Monetization Practices Limits Revenue Models

The increasing regulatory scrutiny regarding loot boxes microtransactions and predatory monetization strategies by threatening established revenue streams is restraining the growth of the United States gaming market. Legislators and consumer advocacy groups argue that certain game mechanics resemble gambling and exploit vulnerable populations particularly minors. As per the Federal Trade Commission there is growing momentum for stricter guidelines on transparency and age verification in digital purchases. This regulatory pressure forces developers to redesign economic systems potentially reducing average revenue per user. Several states have introduced bills aiming to ban or restrict loot boxes citing concerns over psychological manipulation and financial harm. According to the Electronic Frontier Foundation ambiguous legal frameworks create uncertainty for publishers who must navigate varying state laws while maintaining profitability. The potential for federal intervention adds risk to long term planning and may discourage investment in live service models that rely heavily on randomized rewards. Furthermore, negative public perception surrounding pay to win mechanics can damage brand reputation and lead to boycotts or reduced player acquisition. Companies must balance monetization goals with ethical considerations and compliance costs which can stifle innovation and limit the flexibility of game design. This evolving legal landscape requires constant adaptation and legal oversight adding operational burdens that constrain market expansion.

High Development Costs and Technical Complexity Restrict Entry

The escalating costs associated with developing high fidelity video games and increasing financial risk for publishers is also impeding the growth of the United States gaming market. Modern AAA titles require hundreds of millions of dollars in investment covering advanced graphics engine licensing motion capture technology and large multidisciplinary teams. This financial intensity limits the number of projects that studios can undertake simultaneously and encourages risk aversion in creative decisions. The complexity of modern hardware architectures necessitates extensive optimization efforts further prolonging development cycles and delaying time to market. According to industry analysis delays in major releases often result in significant stock price volatility for publicly traded companies reflecting investor sensitivity to execution risks. Smaller independent developers struggle to compete with the production values of major studios limiting their ability to capture mainstream attention without substantial external funding. The need for continuous post launch support and content updates adds to the ongoing operational burden stretching resources thin.

MARKET OPPORTUNITIES

Cloud Gaming Infrastructure Unlocks New User Segments

The advancement of cloud gaming technology by allowing users to stream high quality games without owning expensive hardware is substantially to create new opportunities for the growth of the United States gaming market. This model shifts the computational load to remote servers enabling play on low end devices such as smart TVs tablets and basic laptops. The adoption of GeForce Now and similar services has grown substantially as internet infrastructure improves with 5G rollout enhancing latency and bandwidth capabilities. This accessibility appeals to casual gamers and those in rural areas who previously lacked access to next generation consoles or gaming PCs. According to the study, cloud gaming subscribers are increasingly likely to try new genres and titles due to the low commitment of subscription based access. Publishers can leverage this platform to revitalize older catalog titles and reach audiences who are hesitant to make large upfront hardware investments. The subscription model also provides predictable recurring revenue streams that stabilize cash flow compared to volatile unit sales. Furthermore, cloud platforms facilitate instant play trials reducing friction in the discovery process and encouraging impulse conversions.

Integration of Artificial Intelligence Enhances Personalization

The integration of artificial intelligence into game development and player experience to enhance engagement through personalized content and adaptive gameplay is another attribute to escalate the growth of the United States gaming market. AI algorithms can analyze player behavior in real time to adjust difficulty levels suggest relevant items and generate dynamic narrative elements that cater to individual preferences. AI driven personalization can increase customer satisfaction and retention by creating unique experiences for each user. This technology also accelerates development processes by automating asset creation testing and bug detection allowing studios to release content more frequently and efficiently. According to Unity Technologies developers using AI tools report significant reductions in production time enabling faster iteration and experimentation with new ideas. Generative AI can create infinite variations of levels characters and dialogue keeping the game world fresh and engaging for long term players. This capability supports live service models by providing a steady stream of novel content without proportional increases in manual labor. Furthermore, AI powered analytics help publishers understand churn risks and optimize marketing campaigns by identifying high value user segments.

MARKET CHALLENGES

Cybersecurity Threats and Data Privacy Concerns

The increasing frequency and sophistication of cyberattacks by threatening user data integrity and platform stability is one of the major challenges for the growth of United states gaming market. Online gaming platforms store vast amounts of personal and financial information making them attractive targets for hackers seeking to exploit vulnerabilities. The gaming related fraud and identity theft incidents have risen sharply causing significant financial losses and reputational damage to companies. Breaches can lead to loss of consumer trust resulting in churn and decreased willingness to engage in digital transactions. The implementation of robust security measures requires substantial investment in encryption multi factor authentication and continuous monitoring systems. The cost of data breaches in the entertainment sector remains among the highest across industries due to the complexity of digital ecosystems. Additionally, privacy regulations such as the California Consumer Privacy Act impose strict requirements on data handling forcing companies to navigate complex compliance landscapes. Failure to protect user data can result in hefty fines and legal action further straining resources. The anonymous nature of online interactions also facilitates harassment and cheating which undermines the competitive integrity of multiplayer games.

Talent Shortage and Workforce Retention Issues

The attracting and retaining skilled professionals due to intense competition for talent and demanding work conditions is also to act as a barrier for the growth of United States gaming market. The specialized nature of game development requires expertise in programming art design and audio engineering, which is in short supply relative to industry demand. As per the International Game Developers Association, many studios report difficulties in filling key roles leading to project delays and increased labor costs. The prevalence of crunch culture, where employees work excessive hours to meet deadlines has led to burnout and high turnover rates affecting morale and productivity. The workforce instability disrupts continuity in creative vision and technical execution compromising the quality of final products. Furthermore, the rise of remote work has expanded the talent pool but also intensified competition as companies vie for top candidates globally. Retaining experienced developers is crucial for maintaining institutional knowledge and ensuring the successful delivery of complex projects.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 8.62% |

| Segments Covered | By Platform, Revenue Model, Genre, Gamer Demographic and Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

| Regions Covered | California, Washington, Oregon, New York & Rest of the United States |

| Market Leaders Profiled | Activision Blizzard Inc., Electronic Arts Inc., Microsoft Corporation (Xbox Game Studios), Sony Interactive Entertainment LLC, Take-Two Interactive Software Inc., Epic Games Inc., Roblox Corp., Riot Games Inc., Nintendo Co., Ltd., Ubisoft Entertainment SA, Valve Corp., Square Enix Holdings Co., Ltd., Capcom Co., Ltd., Bungie Inc., Niantic Inc., Bethesda Softworks LLC, CD Projekt S.A., Nexon Co., Ltd., Zynga Inc., BioWare (U.S. studio) |

SEGMENTAL ANALYSIS

By Platform Insights

The mobile gaming segment was accounted in holding 56.4% of the United States gaming market share in 2025 with the unparalleled accessibility of smartphones and the widespread adoption of free to play models. The ubiquity of mobile devices allows users to engage with games during commutes breaks or downtime creating high frequency usage patterns that other platforms cannot match. The low barrier to entry as most consumers already own the necessary hardware is eliminating the need for expensive console or PC purchases. The mobile gaming revenue accounts for the largest share of total US gaming spending surpassing both console and PC segments combined. The ease of downloading games from app stores and the social integration of mobile titles encourage viral growth and sustained engagement. Additionally, the diversity of mobile games ranging from simple puzzles to complex strategy titles appeals to a broad demographic including non-traditional gamers. The continuous improvement in mobile processor capabilities and screen technology enhances the visual fidelity and performance of mobile games making them increasingly competitive with traditional platforms.

The console gaming segment is lucratively to witness a fastest CAGR of 9.2% from 2026 to 2034 with the release of next generation consoles and the expansion of subscription services. The launch of powerful systems, such as the PlayStation 5 and Xbox Series X has revitalized interest in high fidelity gaming experiences that offer superior graphics and immersive gameplay. The popularity of game pass style subscriptions, which provide access to extensive libraries of titles for a monthly fee encouraging higher engagement and retention. The subscription services have doubled their user base in recent years demonstrating the shift towards value-based consumption models. The exclusivity of major franchise titles on specific consoles drives brand loyalty and hardware upgrades among dedicated gamers. Furthermore, the integration of cloud gaming features within consoles allows users to stream games instantly adding flexibility and convenience to the traditional console experience.

By Revenue Model Insights

The in-app purchases and microtransactions segment was accounted in holding a dominant share of the United States gaming market in 2025 due to their ability to generate recurring income from a large base of free to play users. This model lowers the initial barrier to entry allowing millions of players to download and start playing games without upfront costs thereby maximizing the potential user base. The psychological appeal of personalization and status symbols within games drives players to make frequent small purchases that accumulate into substantial revenue streams. According to the Entertainment Software Association, a significant portion of gamers regularly spend money on in game content highlighting the acceptance of this monetization strategy. Developers utilize data analytics to tailor offers and incentives to individual player behaviors increasing conversion rates and average order values. The live service nature of many modern games ensures a constant flow of new content and events that stimulate ongoing spending. This model also allows for dynamic pricing and limited time offers that create urgency and drive impulse buys.

The subscription services segment is esteemed to witness a fastest CAGR of 10.6% during the forecast period with the consumer preference for predictable costs and access to diverse content libraries. Platforms, such as Xbox, Game Pass, PlayStation Plus, and EA Play offer subscribers unlimited access to hundreds of games for a fixed monthly fee providing exceptional value compared to purchasing individual titles. The number of gaming subscription subscribers in the US has grown substantially with double digit annual growth rates reflecting the shifting consumption habits of digital natives. This model appeals to cost conscious consumers, who prefer to rent access to games rather than own them permanently reducing the financial risk of trying new genres or titles. According to the study, and other tech giants entering the space the competition is intensifying which leads to better offerings and lower prices for consumers. The inclusion of day one releases for major franchises in subscription catalogs further incentivizes sign ups and reduces churn. Publishers benefit from steady recurring revenue and valuable data on player preferences which informs future development and marketing strategies. The integration of cloud gaming into subscription tiers enhances accessibility allowing users to play high end games on various devices without expensive hardware.

By Genre Insights

The action and shooter genres segment was the largest by holding a significant share of the US gaming market in 2025 due to their high engagement levels competitive nature and strong esports ecosystems. These titles often feature fast paced gameplay and skill-based mechanics that appeal to a wide demographic, particularly younger males, who constitute a significant portion of the gaming population. The social aspect of multiplayer shooters fosters strong communities and friend groups which drive retention and word of mouth promotion. The regular release of seasonal content updates and battle passes keeps the gameplay fresh and encourages continuous participation. Esports tournaments for shooter games attract massive viewership and sponsorship deals further cementing their cultural relevance and commercial viability. The technological advancements in graphics and physics engines enhance the realism and immersion of these games making them visually appealing and technically impressive. Additionally, the cross platform play feature allows friends to compete together regardless of their device increasing the overall player pool and matchmaking efficiency.

The role-playing games and massively multiplayer online games segment is likely to witness a fastest CAGR of 9.2% during the forecast period with the desire for immersive narratives and persistent virtual worlds. Players are increasingly seeking deep storytelling experiences and character customization options that allow for personal expression and long-term investment in game worlds. The integration of gacha mechanics and live service elements in RPGs has proven highly effective in monetizing player engagement. The social guild structures and cooperative raids in MMOs foster strong interpersonal bonds that enhance retention and community loyalty. The advancement in server technology allows for larger scale multiplayer interactions creating more dynamic and responsive game environments. Furthermore, the crossover of RPG elements into other genres such as action and strategy has broadened the appeal of role playing mechanics to a wider audience. The continuous expansion of these virtual worlds through downloadable content and seasonal events ensures that players remain engaged for years driving sustained revenue growth and establishing these genres as key pillars of future market expansion.

COMPETITIVE LANDSCAPE

The competition in the United States gaming market is intense and characterized by rapid technological innovation and aggressive consolidation among major corporations. Leading entities compete fiercely for user attention through exclusive content libraries superior hardware performance and innovative service models. The shift towards digital distribution has lowered barriers for entry yet increased pressure on visibility and discoverability within crowded storefronts. Subscription services have become a critical battleground where companies vie for subscriber loyalty by offering extensive catalogs and day one releases. Mobile gaming giants challenge traditional console manufacturers by capturing casual audiences with accessible free to play titles. Esports and streaming platforms further amplify competitive dynamics by creating communities around specific franchises and influencers. Regulatory scrutiny regarding data privacy and monetization practices adds complexity to strategic planning for all participants. Companies must balance creative risk with financial stability while navigating changing consumer preferences for social and interactive experiences. The convergence of gaming with other media forms such as film and music creates new opportunities for cross promotional activities.

KEY MARKET PLAYERS

A few of the market players that are dominating the U.S gaming market are

- Activision Blizzard Inc.

- Electronic Arts Inc.

- Tencent Holdings Limited

- Microsoft Corporation (Xbox Game Studios)

- Sony Interactive Entertainment LLC

- Take-Two Interactive Software Inc.

- Epic Games Inc.

- Roblox Corp.

- Riot Games Inc.

- Nintendo Co., Ltd.

- Ubisoft Entertainment SA

- Valve Corp.

- Square Enix Holdings Co., Ltd.

- Capcom Co., Ltd.

- Bungie Inc.

- Niantic Inc.

- Bethesda Softworks LLC

- CD Projekt S.A.

- Nexon Co., Ltd.

- Zynga Inc.

- BioWare (U.S. studio)

Top Players In The Market

- Microsoft Corporation significantly influences the global gaming landscape through its Xbox ecosystem and extensive cloud gaming infrastructure. The company has strengthened its position by acquiring major studios such as Activision Blizzard which brings iconic franchises into its portfolio. This strategic move expands its content library for Xbox Game Pass subscribers enhancing user retention and value proposition. Microsoft focuses on seamless cross platform integration allowing players to access games across consoles PCs and mobile devices via cloud streaming. Recent initiatives include advancing AI driven gaming experiences and improving network latency for cloud services. The corporation invests heavily in developer tools and partnerships to support independent creators ensuring a diverse range of titles. These efforts solidify its role as a leader in accessible and inclusive gaming entertainment while driving innovation in hardware and software integration globally.

- Sony Group Corporation remains a pivotal force in the global gaming industry through its PlayStation brand and commitment to high quality exclusive narratives. The company continues to deliver critically acclaimed single player experiences that define console generations and drive hardware sales. Sony has recently expanded its footprint in live service games and PC ports to reach broader audiences beyond its traditional console base. Investments in virtual reality technology with PlayStation VR2 demonstrate its dedication to immersive next generation gameplay. The firm strengthens its market position by fostering strong relationships with third party developers and securing timed exclusives for popular titles. Sony also enhances its subscription service offerings to compete effectively in the evolving digital landscape. These actions ensure sustained relevance and consumer engagement in a highly competitive global market environment.

- Tencent Holdings Limited operates as a dominant global entity in the gaming sector through vast investments in diverse studios and publishing rights. The company owns significant stakes in numerous international developers enabling it to influence trends across mobile PC and console platforms. Tencent strengthens its market position by facilitating global distribution of hit titles and providing financial resources for innovative projects. Its expertise in mobile gaming monetization and social integration drives high engagement rates worldwide. Recent actions include expanding cloud gaming capabilities and exploring metaverse related technologies to future proof its portfolio. The corporation leverages its massive user base from social media platforms to promote game launches effectively. These strategic moves allow the company to maintain a pervasive presence in the global gaming industry while adapting to shifting consumer preferences and technological advancements efficiently.

Top Strategies Used By Key Market Participants

Key players in the United States gaming market prioritize subscription based models to ensure recurring revenue streams and enhance customer retention rates. Companies aggressively pursue mergers and acquisitions to secure valuable intellectual property and expand their internal development capabilities significantly. Cross platform play integration is widely adopted to unify fragmented user bases and increase multiplayer engagement across different hardware systems. Publishers focus on live service operations by delivering continuous content updates seasonal events and battle pass to sustain long term player interest. Strategic partnerships with cloud infrastructure providers enable seamless streaming experiences that reduce hardware barriers for consumers. Investment in artificial intelligence improves game personalization non player character behavior and operational efficiency during development cycles. Marketing efforts increasingly leverage influencer collaborations and esports sponsorships to reach younger demographics effectively. These combined strategies allow firms to maximize lifetime value per user while adapting to rapid technological changes and evolving consumer expectations in the digital entertainment landscape.

MARKET SEGMENTATION

This research report on the U.S gaming market is segmented and sub-segmented into the following categories.

By Platform

- Mobile Gaming

- Console Gaming

- PC Gaming (Client and Browser)

- Cloud / Streaming Gaming

By Revenue Model

- In-App Purchases (IAP)

- Premium (Pay-to-Own)

- Subscription Passes

- Advertising-Supported

By Genre

- Action / Adventure

- Shooter

- Sports and Racing

- Role-Playing and MMO

- Casual / Puzzle

- Strategy and Card

- Other Genres

By Gamer Demographic

- Less Than 18 Years

- 18 -34 Years

- 35 -44 Years

- 45+ Years

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

What is currently driving growth in the United States gaming market?

Rising demand for digital entertainment and increasing adoption of online gaming are driving growth.

Why is the gaming industry expanding rapidly in the United States?

Technological advancements and growing player engagement are boosting market expansion.

How would you explain the gaming market in simple terms?

It involves the development, distribution, and consumption of video games.

Where is gaming most commonly experienced in the United States?

It is widely accessed through consoles, PCs, and mobile devices.

What makes gaming important in modern entertainment?

It offers interactive experiences and diverse content for users.

From a consumer perspective, is gaming a popular activity?

Yes, it is one of the leading forms of digital entertainment.

What challenges are affecting the United States gaming market?

High development costs and regulatory concerns are key challenges.

How is online connectivity influencing the gaming market?

Improved internet access is increasing multiplayer and cloud gaming adoption.

Which segments contribute the most to gaming market revenue?

Mobile gaming, console gaming, and PC gaming are major contributors.

Is the United States gaming market growing steadily?

Yes, it is expanding with increasing user base and content innovation.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com