- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

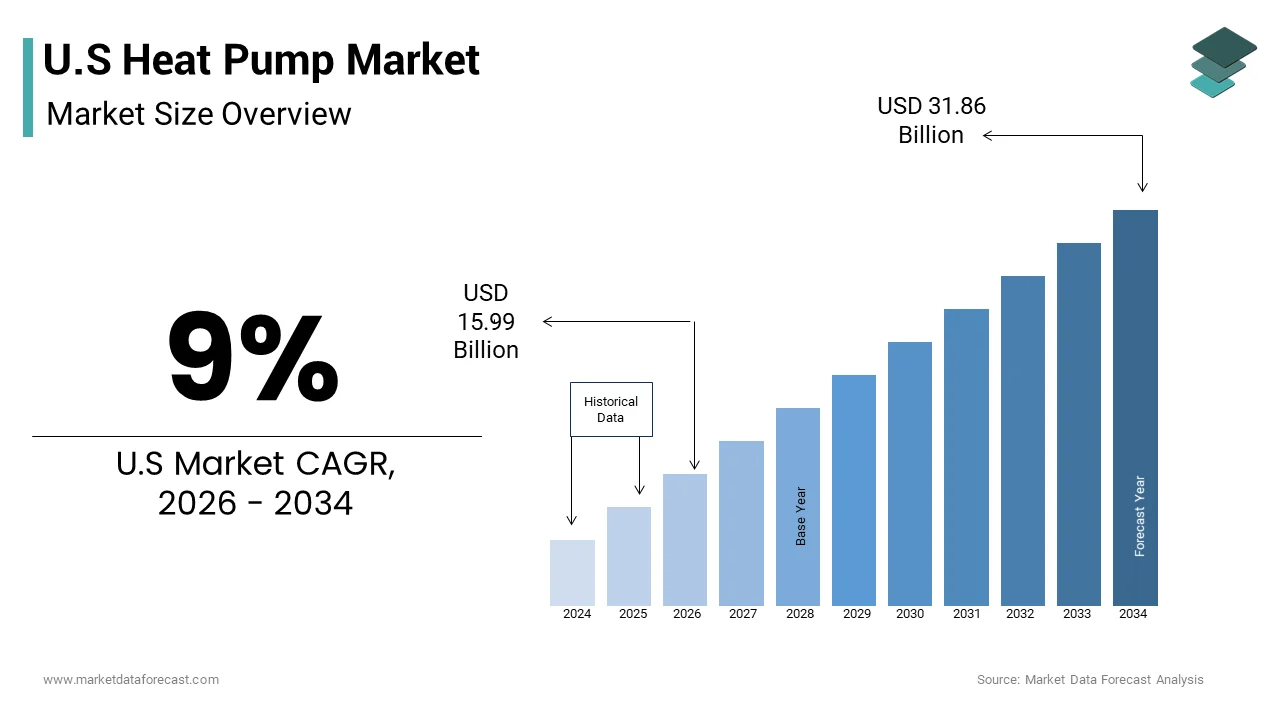

Market Size, 2025

$14.67 BnMarket Estimate, 2026

$15.99 BnMarket Forecast, 2034

$31.86 BnCAGR, 2026–2034

9%U.S. Heat Pump Market Report Summary

The U.S. heat pump market was valued at USD 14.67 billion in 2025 and is estimated to reach USD 15.99 billion in 2026, before expanding to USD 31.86 billion by 2034, registering a CAGR of 9.0% during the forecast period from 2026 to 2034. The U.S. heat pump market is gaining significant momentum as consumers, businesses, and governments accelerate the transition toward energy-efficient and low-carbon heating and cooling technologies. Rising electrification of residential and commercial buildings, favorable government incentives, and increasingly stringent energy efficiency regulations are driving product adoption nationwide. Technological advancements in cold-climate heat pumps, smart HVAC systems, and inverter-based compressors are further enhancing performance and reducing energy consumption. In addition, growing investments in sustainable building infrastructure, rising electricity grid modernization efforts, and increasing awareness of long-term energy savings are creating substantial growth opportunities across the United States.

Key Market Trends

- Growing replacement of conventional fossil fuel heating systems with high-efficiency electric heat pumps to support decarbonization goals.

- Rising adoption of smart heat pumps integrated with IoT connectivity, intelligent temperature controls, and home energy management systems.

- Increasing investments in cold-climate heat pump technologies designed to deliver reliable performance under extreme weather conditions.

- Expansion of federal and state incentive programs encouraging residential and commercial adoption of energy-efficient HVAC systems.

- Manufacturers are developing environmentally friendly refrigerants and high-performance inverter technologies to improve efficiency and reduce emissions.

Segmental Insights

Based on type, the air source segment dominated the U.S. heat pump market in 2025. The segment's leadership is driven by its cost-effectiveness, ease of installation, high energy efficiency, and broad applicability across residential and light commercial buildings, making it the preferred heating and cooling solution for a wide range of consumers.

Based on rated capacity, the up-to-10-kilowatts segment led the U.S. market in 2025 and is expected to maintain its dominant position throughout the forecast period. This leadership is supported by strong demand from single-family homes and small commercial buildings that require compact, energy-efficient heating and cooling systems.

Based on system design, the split-system heat pumps segment is projected to remain the preferred choice in the U.S. market over the coming years. Their flexibility, improved energy efficiency, quieter operation, and compatibility with existing HVAC infrastructure continue to drive widespread adoption.

Based on end user, the residential segment dominated the U.S. heat pump market in 2025 and is expected to retain its leading position. Rising homeowner investments in energy-efficient home upgrades, favorable tax incentives, and growing awareness of sustainable heating solutions continue to strengthen demand across the residential sector.

Regional Insights

The United States is expected to maintain its dominant position within the North American heat pump market throughout the forecast period, supported by the rapid transition from fossil fuel-based heating systems to electric heat pumps. Federal incentives, state-level clean energy initiatives, and stricter building energy codes are accelerating market adoption across residential, commercial, and institutional applications. Increasing investments in electrification, modern HVAC infrastructure, and carbon emission reduction strategies are further reinforcing market growth. Continuous technological innovation, expanding domestic manufacturing capabilities, and rising consumer awareness of energy-efficient heating and cooling solutions position the United States as a leading market for heat pump deployment.

Competitive Landscape

The U.S. heat pump market is highly competitive, with global HVAC manufacturers and regional technology providers competing through innovation, energy efficiency, and sustainable product development. Leading companies are investing in advanced compressor technologies, inverter-driven systems, smart climate control solutions, and environmentally friendly refrigerants to meet evolving consumer and regulatory requirements. Strategic partnerships, manufacturing capacity expansion, acquisitions, and investments in research and development remain central to strengthening market presence. Companies are also enhancing digital monitoring capabilities, predictive maintenance solutions, and connected HVAC ecosystems to improve customer experience and operational performance. As demand for high-efficiency heating and cooling systems continues to increase, market participants are focusing on innovation, sustainability, and product reliability to gain a competitive advantage.

Prominent players in the U.S. heat pump market include Trane Technologies plc, Johnson Controls International plc, Rheem Manufacturing Company, Lennox International Inc., Mitsubishi Electric US, Inc., Bosch Thermotechnology Corp., Emerson Electric Co., GE Appliances, Inc. (a Haier company), Nortek Air Management, Fujitsu General America, Inc., LG Electronics USA, Inc., WaterFurnace International, Inc., ClimateMaster, Inc., Goodman Manufacturing Co., L.P., Stiebel Eltron GmbH & Co. KG, and Samsung HVAC America, LLC.

U.S. Heat Pump Market Size

The U.S heat pump market size was valued at USD 14.67 billion in 2026 and is anticipated to reach USD 15.99 billion in 2026 to reach USD 31.86 billion by 2034, growing at a CAGR of 9% during the forecast period from 2026 to 2034.

According to the U.S. Department of Energy, heat pumps can deliver up to 3 times more energy than they consume from the electrical grid, highlighting their superior efficiency metrics. The current landscape is shaped by increasing consumer awareness regarding environmental sustainability and rising electricity costs compared to volatile natural gas prices. Regulatory frameworks at both federal and state levels are increasingly favoring electrification of buildings to meet carbon reduction targets. The infrastructure supporting these systems includes a growing network of certified installers and manufacturers adapting to new technological standards. Recent winters have tested the resilience of these systems in colder climates, prompting advancements in cold climate heat pump technology. The market operates within a complex regulatory environment involving building codes and energy efficiency standards that vary across states. Consumer preferences are shifting toward smart home integration, allowing for remote monitoring and optimized energy usage. This transition reflects a broader societal move toward decarbonization and energy independence.

MARKET DRIVERS

Federal Incentives and Tax Credit Programs Driving Adoption

The implementation of comprehensive federal incentive programs has significantly accelerated the adoption of heat pump systems across the U.S., which is a key market driver The Inflation Reduction Act introduced substantial tax credits and rebates for homeowners who upgrade to high-efficiency electric heat pumps. According to the Internal Revenue Service, eligible taxpayers can claim a tax credit of 30% of the cost for qualified heat pump installations, with a maximum annual limit of 2,000 dollars under the Energy Efficient Home Improvement Credit. This financial support reduces the upfront cost barrier, which has historically hindered widespread adoption. Additionally, the Home Electrification and Appliance Rebates program provides point-of-sale rebates for low- and moderate-income households, further enhancing affordability. These incentives are designed to stimulate demand and encourage the replacement of aging fossil fuel-based heating systems. State-level programs often complement federal initiatives, creating a layered support structure that maximizes consumer benefit. The availability of these funds has led to a surge in consumer inquiries and installation requests. Manufacturers and retailers have adjusted their marketing strategies to highlight these savings opportunities. The long-term operational savings, combined with immediate financial incentives, create a compelling value proposition for homeowners. This policy-driven demand is expected to sustain growth momentum as consumers become more aware of the available benefits. The strategic alignment of federal policy with consumer economic interests serves as a primary catalyst for market expansion.

Stringent Energy Efficiency Regulations and Building Codes

Increasingly stringent energy efficiency regulations and updated building codes are compelling developers and homeowners to adopt heat pump technology, which is further contributing to the expansion of the U.S. heat pump market. Federal and state governments are implementing stricter standards for heating and cooling equipment to reduce overall energy consumption and greenhouse gas emissions. As per the Department of Energy, new minimum efficiency standards for central air conditioners and heat pumps took effect in 2023, requiring higher seasonal energy efficiency ratios. These regulations effectively phase out less efficient models from the market, forcing consumers to choose advanced heat pump systems. Many states, including California and New York, have adopted ambitious building electrification mandates that prohibit or limit the installation of natural gas heaters in new construction. Local jurisdictions are updating building codes to require all-electric-ready infrastructure, which facilitates future heat pump installation. Compliance with these regulations is becoming a prerequisite for obtaining building permits and certificates of occupancy. Developers are integrating heat pumps into new projects to meet green building certifications such as LEED and Energy Star. The regulatory pressure extends to commercial buildings, where large property owners must comply with local emissions laws. This legislative framework creates a mandatory demand channel that operates independently of consumer preference. The consistent tightening of efficiency standards ensures that heat pumps remain the compliant choice for modern heating and cooling needs, driving sustained market growth.

MARKET RESTRAINTS

High Upfront Installation Costs and Economic Barriers

Despite long-term savings, the high upfront cost of purchasing and installing heat pump systems remains a significant restraint on market growth. The initial investment for a high-efficiency heat pump system, including labor and necessary electrical upgrades, often exceeds that of traditional gas furnaces. As per industry data, the average cost to install a central heat pump system in 2025 typically ranges from 9,000 to 20,000 dollars, depending on home size and complexity. This price disparity discourages price-sensitive consumers, particularly in regions where natural gas is inexpensive and readily available. Many older homes require extensive retrofitting, including upgraded electrical panels and improved insulation, to support heat pump operation efficiently. These additional renovation costs further inflate the total project expense, making it prohibitive for many homeowners. Financing options are not always accessible or well-understood by consumers, adding another layer of friction to the purchase decision. While rebates help mitigate these costs, they often require upfront payment with reimbursement occurring later, which poses cash-flow challenges for lower-income households. The perceived financial risk associated with such a significant capital expenditure leads some consumers to delay replacement until their existing systems fail completely. This reactive approach limits the proactive adoption of heat pumps and slows the overall market transition away from fossil fuels.

Shortage of Skilled Labor and Installation Expertise

A critical shortage of skilled HVAC technicians trained in heat pump installation and maintenance acts as a major bottleneck for market expansion. The transition to electric heating requires specialized knowledge that differs significantly from traditional gas furnace repair and installation. According to the Home Builders Institute, there were approximately 456,000 open construction sector jobs as of early 2024, reflecting a persistent labor shortage across the trades. This scarcity of qualified professionals leads to longer wait times for installation and increased labor costs, which are passed on to consumers. Improper installation can severely degrade system performance and efficiency, leading to customer dissatisfaction and negative perceptions of the technology. Training programs have not kept pace with the rapid growth in demand for heat pump services, resulting in a skills gap. Many existing technicians lack experience with variable speed compressors and advanced control systems inherent in modern heat pumps. This expertise deficit is particularly pronounced in rural areas, where access to specialized contractors is limited. The quality of installation directly impacts the reliability and lifespan of the equipment, making skilled labor essential. Without a robust workforce capable of delivering high-quality installations, the market cannot achieve its full potential. Industry stakeholders are investing in training initiatives, but the scale of the shortage remains a formidable challenge to seamless market growth.

MARKET OPPORTUNITIES

Expansion into Cold Climate Applications and Technology Advancements

Technological advancements enabling efficient operation in extreme cold conditions is a significant opportunity for market expansion in northern states. Historically, heat pumps struggled to maintain efficiency in temperatures below freezing, but recent innovations have overcome this limitation. According to recent research on cold climate performance, modern heat pumps can operate effectively at temperatures as low as -15°F, maintaining higher energy output compared to resistive electric heaters. This breakthrough opens up vast markets in the Northeast and Midwest, where heating demand is highest during winter months. Manufacturers are developing units with enhanced compressor technologies and improved defrost cycles to maintain performance in harsh weather. Consumer confidence in these systems is growing as real-world performance data demonstrates their reliability. Utility companies in cold states are promoting cold climate heat pumps as part of their electrification strategies, offering additional incentives for adoption. The ability to replace oil and propane heating systems in rural areas with electric heat pumps offers substantial environmental and economic benefits. This technological evolution allows heat pumps to compete directly with fossil fuel heaters in all geographic zones. The expanding addressable market due to cold climate capabilities drives new sales volumes and encourages further research and development. This opportunity transforms heat pumps from a niche product in mild climates to a universal heating solution.

Integration with Renewable Energy and Smart Grid Systems

The integration of heat pumps with renewable energy sources and smart grid technologies offers a compelling opportunity for the U.S. heart pump market. Heat pumps can be paired with rooftop solar photovoltaic systems to provide nearly free heating and cooling using self-generated electricity. According to the Solar Energy Industries Association, the growing adoption of residential solar panels creates a synergistic relationship with electric heat pumps, maximizing the utility of clean energy. Smart thermostats and grid-interactive controls allow heat pumps to adjust operation based on electricity prices and grid demand, optimizing energy usage. Utilities are piloting programs that reward customers for allowing remote adjustment of heat pump settings during peak demand periods, reducing strain on the grid. This flexibility supports the integration of intermittent renewable energy sources by shifting load to times of high solar or wind production. Homeowners benefit from reduced electricity bills through time-of-use rates and net metering arrangements. The convergence of electrification and digitalization enables a more resilient and sustainable energy ecosystem. This opportunity appeals to environmentally conscious consumers seeking to minimize their carbon footprint and energy costs. As smart home technology becomes mainstream, the seamless integration of heat pumps into connected home systems will drive further adoption. This strategic alignment with broader energy trends positions heat pumps as a key component of the future smart grid.

MARKET CHALLENGES

Supply Chain Volatility and Component Shortages

Persistent supply chain disruptions and shortages of critical components are majorly challenging the expansion of the U.S. heat pump market. The manufacturing of heat pumps relies on a complex global supply chain for semiconductors, copper, aluminum, and rare earth elements used in motors and compressors. According to the Bureau of Labor Statistics, producer price indices for HVAC equipment have shown significant volatility, reflecting fluctuations in raw material costs and logistical constraints. Delays in the availability of key parts, such as microchips and compressors, lead to extended lead times for manufacturers and distributors. This uncertainty makes it difficult for contractors to quote accurate prices and delivery dates to customers, causing project delays and cancellations. The reliance on imported components exposes the industry to geopolitical tensions and trade policy changes that can disrupt supply flows. Inventory management becomes challenging as companies struggle to balance stock levels against unpredictable supply availability. These disruptions increase operational costs and reduce profitability for manufacturers and dealers. The inconsistency in product availability undermines consumer confidence and slows down the replacement cycle of older systems. Resolving these supply chain vulnerabilities requires diversification of sourcing and investment in domestic manufacturing capabilities, which take time to implement. Until supply chains stabilize, the market will continue to face headwinds that constrain growth and increase costs for end users.

Consumer Misconceptions and Lack of Awareness

Widespread misconceptions about the performance and suitability of heat pumps in various climates hinder broader consumer acceptance and adoption, which is further challenging the U.S. market growth. Many homeowners believe that heat pumps are ineffective in cold weather or that they are too expensive to operate compared to natural gas. According to industry surveys, a significant portion of consumers remain unfamiliar with how heat pumps function or their specific advantages over traditional systems. This lack of awareness leads to hesitation and reliance on familiar but less efficient technologies. Misinformation regarding the noise levels and aesthetic impact of outdoor units also deters potential buyers. Educational gaps among general contractors and real estate agents further perpetuate these myths, as they often recommend traditional systems due to familiarity. Overcoming these deeply held beliefs requires extensive public education campaigns and demonstrable proof of performance. The complexity of explaining the technology and its benefits in simple terms poses a marketing challenge. Consumers often prioritize immediate comfort and reliability over long-term efficiency, making them risk-averse to new technologies. Addressing these perceptual barriers requires coordinated efforts from industry stakeholders, utilities, and policymakers to provide clear and accurate information. Without effective communication strategies, the market will struggle to convert interested prospects into actual customers, limiting its overall potential.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 9% |

| Segments Covered | By Type, Rated Capacity, System Design, End-User, and Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

| Regions Covered | California, Washington, Oregon, New York & Rest of the United States |

| Market Leaders Profiled | Trane Technologies plc, Johnson Controls International plc, Rheem Manufacturing Company, Lennox International Inc., Mitsubishi Electric US, Inc., Bosch Thermotechnology Corp., Emerson Electric Co., GE Appliances, Inc. (a Haier company), Nortek Air Management, Fujitsu General America, Inc., LG Electronics USA, Inc., WaterFurnace International, Inc., ClimateMaster, Inc., Goodman Manufacturing Co., L.P., Stiebel Eltron GmbH and Co. KG, Samsung HVAC America, LLC. |

SEGMENTAL ANALYSIS

By Type Insights

The air source segment dominated the market by holding the highest share of the U.S. market in 2025 due to their versatility, ease of installation, and cost-effectiveness compared to other technologies. They extract heat from the outside air, making them suitable for a wide range of climatic conditions across the country. Recent technological innovations have significantly improved the efficiency and reliability of air source heat pumps in cold climates, expanding their geographic applicability. According to environmental research, modern cold-climate air-source heat pumps can maintain efficient performance at temperatures as low as -15°F. These advancements include variable-speed compressors, enhanced refrigerant formulations, and improved defrost cycles that prevent ice buildup on outdoor coils. Such improvements have dispelled the myth that heat pumps are ineffective in northern states, opening up large markets in the Northeast and Midwest. Consumers in these regions are increasingly replacing oil and propane heating systems with electric heat pumps due to their superior efficiency and lower operating costs. The ability to provide consistent heating in extreme weather conditions has boosted consumer confidence and accelerated adoption rates. Utility companies in cold states are actively promoting these advanced units through rebate programs, recognizing their potential to reduce peak demand and greenhouse gas emissions. The continuous improvement in performance metrics ensures that air source heat pumps remain competitive with fossil fuel alternatives regardless of location. This technological evolution has transformed air source heat pumps from a niche product for mild climates into a viable mainstream heating solution for the entire U.S.

On the other side, the water source heat pumps segment is projected to be the fastest-growing segment in the U.S. market and witness a CAGR of 7.4% during the forecast period owing to their superior efficiency in commercial applications and increasing focus on sustainable building practices. Water source heat pumps offer exceptional energy efficiency by utilizing stable water temperatures from lakes, rivers, or municipal supplies as a heat exchange medium. According to the American Society of Heating, Refrigerating, and Air-Conditioning Engineers, water source systems can achieve efficiency levels significantly higher than traditional air source units by leveraging stable source temperatures. This performance advantage is particularly valuable in commercial and industrial sectors, where energy costs constitute a significant portion of operational expenses. The consistency of water temperature allows for more predictable and efficient operation year-round, reducing wear and tear on components. Large office complexes, hotels, and manufacturing facilities are increasingly adopting water source heat pumps to meet stringent energy codes and sustainability goals. The scalability of these systems allows for centralized management and optimized energy distribution across multiple zones. Government incentives for commercial building electrification further encourage the adoption of high-efficiency water-source technologies. The reduced carbon footprint associated with these systems aligns with corporate environmental, social, and governance commitments, driving investment in this segment. As businesses prioritize energy resilience and cost stability, water source heat pumps provide a reliable and efficient solution. The growing emphasis on green building certifications, such as LEED, also favors the installation of water source systems, contributing to their rapid growth trajectory.

By Rated Capacity Insights

The up-to-10-kilowatts capacity segment led the market in 2025 and is expected to maintain its dominant position in the U.S. for the next few years as residential demand for home electrification stays high. This capacity range is ideal for single-family homes and small apartments, which constitute the majority of the housing stock. The dominance of the up-to-10-kilowatts segment is directly linked to the vast number of single-family residences in the U.S. that require compact and efficient heating solutions. According to the U.S. Census Bureau, single-family homes represent approximately 80% of the total housing units in the country. Most of these homes have heating and cooling loads that fall within the up-to-10-kilowatts range, making this capacity the standard choice for replacements and new installations. The compact size of these units allows for easy installation in limited spaces, such as closets, attics, or exterior walls, without requiring major structural modifications. Homeowners prefer this capacity range due to its balance of performance and affordability, meeting the typical thermal needs of average-sized dwellings. The widespread availability of models in this capacity ensures competitive pricing and ample choice for consumers. Retrofitting older homes with energy-efficient heat pumps in this capacity range is a key strategy for reducing residential energy consumption. The simplicity of sizing and selecting units in this range simplifies the decision-making process for contractors and homeowners alike. This segment benefits from consistent demand, driven by the natural replacement cycle of aging HVAC equipment in the residential sector. The sheer volume of residential transactions ensures that this capacity segment remains the market leader.

However, the 10-to-20-kilowatts capacity segment is projected to show robust performance in the U.S. for the coming years as property owners increasingly upgrade to more powerful climate control systems. This growth is fueled by the increasing size of new homes and the retrofitting of larger existing properties. The growing trend toward larger single-family homes and luxury residences is driving demand for higher capacity heat pumps in the 10-to-20-kilowatts range. According to the National Association of Home Builders, the average size of a new single-family home completed in 2024 was 2,146 square feet, with many homes exceeding 2,500 square feet. Larger living spaces require more powerful heating and cooling systems to maintain comfortable indoor temperatures efficiently. Heat pumps in the 10-to-20-kilowatts range provide the necessary output to handle these increased loads without compromising performance. Luxury home buyers often prioritize advanced comfort features and zoned climate control, which are better supported by higher capacity units. These systems can integrate with sophisticated smart home technologies, allowing for precise temperature management in multiple rooms. The aesthetic appeal of larger outdoor units is also improving, with manufacturers designing sleeker and quieter models. The willingness of affluent consumers to invest in premium, high-capacity systems drives revenue growth in this segment. Additionally, the renovation of historic or large older homes often requires upgraded systems to meet modern comfort standards. This shift toward larger and more complex residential architectures ensures sustained growth for the 10-to-20-kilowatts capacity segment.

By System Design Insights

The split-system heat pumps are likely to remain the primary choice for the U.S. market over the next few years due to their compatibility with existing residential infrastructure. This design separates the indoor and outdoor units, offering flexibility in installation. The primary factor driving the dominance of split-system heat pumps is their seamless compatibility with the extensive ductwork infrastructure present in most American homes. According to the Department of Energy, approximately 66% of households in the U.S. use central systems, which frequently rely on air ducts. Split systems utilize these existing ducts to distribute conditioned air throughout the house, minimizing the need for costly and invasive renovations. This compatibility makes split systems the preferred choice for retrofitting older homes where installing new ductless mini-split systems would be impractical or aesthetically undesirable. Homeowners can replace their old furnace or air conditioner with a heat pump using the same distribution network, ensuring a smooth transition. The familiarity of contractors with split-system installation and maintenance further supports their prevalence. The availability of replacement parts and service expertise for split systems is widespread, reducing long-term ownership costs. This infrastructure advantage creates a high barrier to entry for alternative system designs that require different distribution methods. The ease of integration with existing home architecture ensures that split systems remain the default choice for the majority of residential upgrades. This structural alignment with the existing housing stock solidifies the leading position of split-system heat pumps.

On the other side, the monobloc heat pumps segment is anticipated to experience rapid growth in the U.S. for the next several years as they serve a critical need for homes that cannot easily accommodate ductwork. This growth is driven by their compact design and suitability for homes without existing ductwork. Monobloc heat pumps are gaining traction due to their ideal suitability for retrofitting homes that lack ductwork, such as historic properties and older additions. According to preservation organizations, millions of older homes in the U.S. require efficient heating solutions that do not compromise their architectural integrity. Monobloc units provide a minimally invasive solution by requiring only a small penetration for refrigerant lines and electrical connections. This preservation-friendly approach appeals to homeowners who value the aesthetic and historical significance of their properties. The compact outdoor unit can be placed discreetly, while the indoor handler distributes air through short ducts or directly into the space. The flexibility of monobloc systems allows for zoning capabilities, enabling different temperatures in different rooms. This feature enhances comfort and energy efficiency by avoiding heating or cooling unused spaces. The growing interest in preserving and renovating older homes drives demand for these specialized systems. Architects and designers are increasingly specifying monobloc heat pumps for renovation projects due to their visual appeal and functional benefits. The ability to provide modern comfort in heritage buildings without structural alteration is a unique value proposition. This niche but growing application area contributes significantly to the rapid expansion of the monobloc segment.

By End User Insights

The residential segment dominated the market in 2025 and is poised to lead the U.S. market for the next few years as federal and state programs continue to incentivize home energy efficiency. This is driven by high-volume sales to individual homeowners and strong policy support for home electrification. Federal and state policies aimed at electrifying residential buildings are the primary drivers of demand in the residential segment. As per federal environmental justice initiatives, programs like Justice40 prioritize funding for residential energy upgrades in disadvantaged communities. These initiatives provide substantial grants and rebates for homeowners to replace fossil-fuel heaters with electric heat pumps. The Inflation Reduction Act specifically targets residential consumers with tax credits that significantly reduce the net cost of installation. State-level bans on natural gas hookups in new construction further mandate the use of electric heating systems in residential developments. These policy measures create a guaranteed demand stream for residential heat pumps. Utilities are also implementing managed electrification programs that incentivize residential customers to switch to heat pumps to balance grid load. The alignment of public policy with consumer financial interests accelerates the adoption rate in the residential sector. Homeowners are increasingly aware of the environmental benefits of electrification, contributing to voluntary adoption. The cumulative effect of these initiatives ensures that the residential segment remains the largest contributor to market volume. The focus on equity and affordability in these policies broadens the market reach beyond affluent households.

However, the commercial segment is expected to see significant expansion in the U.S. during the forecast period as corporations strive to meet net-zero emissions targets. This growth is fueled by corporate sustainability goals and stringent building efficiency regulations. Corporate commitments to environmental, social, and governance criteria are driving rapid adoption of heat pumps in the commercial sector. According to global environmental disclosure data, thousands of companies have set science-based targets for reducing carbon emissions, including those from their building operations. Commercial real estate owners and tenants are replacing legacy HVAC systems with heat pumps to meet these ambitious sustainability goals. Green building certifications, such as LEED and the WELL Building Standard, reward the installation of high-efficiency electric heating systems. Investors are increasingly prioritizing properties with lower carbon footprints, influencing leasing and valuation decisions. The reputational benefit of operating green buildings attracts environmentally conscious tenants and employees. Companies are integrating heat pumps into their broader decarbonization strategies alongside renewable energy procurement. The transparency required by ESG reporting mandates accurate tracking of energy usage and emissions, which heat pumps facilitate. This strategic shift toward sustainability is not merely regulatory compliance but a core business objective. The commercial sector's ability to mobilize capital for large-scale retrofits accelerates the deployment of heat pump technology. This corporate drive ensures that the commercial segment grows at a faster pace than other end users.

COUNTRY ANALYSIS

U.S Heat Pump Market Analysis

The U.S. is likely to maintain its dominant regional position for the next few years due to the rapid transition from fossil fuel-based heating to electric heat pumps, driven by a confluence of policy, economic, and technological factors. The U.S. heat pump market is distinguished by a comprehensive policy framework that actively promotes electrification and energy efficiency. According to the Department of Energy, federal tax credits under the Inflation Reduction Act provide up to 2,000 dollars per year for heat pump installations, significantly lowering barriers to entry. This financial support is complemented by state-level rebates and incentives, creating a multi-layered support system. The market maturity is evident in the widespread availability of certified installers and a diverse range of product offerings from domestic and international manufacturers. The presence of established industry associations facilitates standard-setting and professional training, ensuring quality installations. Consumer familiarity with heat pump technology is growing, reducing resistance to adoption. The integration of heat pumps with the existing electrical grid infrastructure is well advanced, supporting large-scale deployment. The U.S. leads in innovation, with domestic companies developing advanced cold-climate models and smart controls. This combination of policy support, market maturity, and technological leadership positions the U.S. as the primary driver of heat pump adoption in the region. The scale of the US market influences global supply chains and pricing trends, reinforcing its central role.

COMPETITIVE LANDSCAPE

The competition in the U.S. heat pump market is intense and characterized by the presence of established global manufacturers and emerging regional players. Major corporations leverage their brand reputation extensive distribution networks and technological expertise to maintain dominant positions. The market sees continuous innovation as companies strive to offer higher efficiency ratings and better cold climate performance to meet stringent regulatory standards. Price competitiveness remains a key factor influencing consumer choices particularly in the residential segment where upfront costs are a primary concern. Companies differentiate themselves through superior customer service comprehensive warranty packages and integrated smart home technologies. The entry of new participants specializing in niche segments such as ductless mini splits adds further complexity to the competitive landscape. Strategic collaborations with utilities and government bodies provide certain players with advantageous positioning in incentive driven markets. Supply chain resilience and local manufacturing capabilities have become critical differentiators amidst global logistical challenges. The focus on sustainability and decarbonization drives competitive dynamics as firms align their offerings with environmental goals. This multifaceted competition fosters rapid technological advancement and improved product availability benefiting consumers while pushing companies to continuously innovate and optimize operations for sustained growth and market relevance.

KEY MARKET PLAYERS

A few of the market players that are dominating the U.S heat pump market are

- Carrier Global Corporation

- DAIKIN INDUSTRIES, Ltd.,

- Trane Technologies plc

- Johnson Controls International plc

- Rheem Manufacturing Company

- Lennox International Inc.

- Mitsubishi Electric US, Inc.

- Bosch Thermotechnology Corp.

- Emerson Electric Co.

- GE Appliances, Inc. (a Haier company)

- Nortek Air Management

- Fujitsu General America, Inc.

- LG Electronics USA, Inc.

- WaterFurnace International, Inc.

- ClimateMaster, Inc.

- Goodman Manufacturing Co., L.P.

- Stiebel Eltron GmbH and Co. KG

- Samsung HVAC America, LLC

Top Players In The Market

- Carrier Global Corporation remains a pivotal entity in the U.S. heat pump landscape leveraging its extensive distribution network and brand recognition. The company focuses on delivering high efficiency residential and commercial systems that align with evolving energy standards. Recent strategic moves include significant investments in manufacturing facilities to increase production capacity for cold climate heat pumps. Carrier has also expanded its digital services portfolio integrating smart controls that enhance user experience and system performance. These initiatives aim to solidify its reputation for reliability and innovation. The company actively collaborates with utilities to promote electrification programs driving consumer adoption. By prioritizing sustainable technologies and robust customer support Carrier strengthens its competitive position. Its commitment to research and development ensures continuous improvement in product efficiency and environmental impact. This holistic approach enables Carrier to maintain a strong foothold in the dynamic US market while addressing the growing demand for sustainable heating solutions.

- Trane Technologies plc plays a crucial role in the US heat pump sector by offering a comprehensive range of heating and cooling solutions for various applications. The company emphasizes energy efficiency and sustainability in its product design appealing to environmentally conscious consumers. Recent actions include the launch of advanced variable speed heat pumps that provide superior comfort and lower operating costs. Trane has also invested in training programs for HVAC professionals ensuring high quality installation and maintenance services. The company leverages its strong commercial presence to drive residential growth through brand trust and technical expertise. Strategic partnerships with technology firms enable the integration of artificial intelligence into system controls optimizing energy usage. Trane continues to expand its manufacturing capabilities to meet rising demand driven by federal incentives. These efforts enhance its market position by delivering reliable and innovative solutions. The focus on operational excellence and customer satisfaction reinforces its leadership in the competitive landscape.

- Daikin Comfort Technologies North America Inc contributes significantly to the US heat pump market through its specialized focus on inverter technology and energy efficient systems. The company offers a diverse portfolio of ductless and ducted heat pumps catering to both residential and light commercial sectors. Recent strategies involve expanding its local manufacturing footprint to reduce supply chain vulnerabilities and improve delivery times. Daikin has introduced new models with enhanced cold climate performance addressing the needs of consumers in northern regions. The company also emphasizes dealer support and training ensuring proper installation and optimal system performance. By focusing on technological innovation and customer education Daikin builds strong brand loyalty. Its commitment to sustainability is evident in the development of low global warming potential refrigerant systems. These initiatives help Daikin capture a growing share of the market as consumers seek reliable and eco friendly heating options. The company continues to invest in marketing and product development to strengthen its presence.

Top Strategies Used by Key Market Participants

Key players in the U.S. heat pump market primarily focus on product innovation to enhance energy efficiency and cold climate performance. Companies invest heavily in research and development to create advanced compressor technologies and smart control systems. Strategic expansion of manufacturing facilities within the country helps mitigate supply chain risks and reduces lead times. Partnerships with utility companies and government agencies facilitate the promotion of electrification programs and rebate initiatives. Brands also prioritize dealer training and certification programs to ensure high quality installation and maintenance services. Marketing efforts emphasize long term cost savings and environmental benefits to educate consumers and drive adoption. Mergers and acquisitions are utilized to broaden product portfolios and access new customer segments. Digital integration through smart home connectivity offers added value and distinguishes products in a competitive landscape. These strategies collectively enable companies to strengthen their market positions and respond effectively to regulatory changes and evolving consumer preferences in the dynamic heating and cooling industry.

MARKET SEGMENTATION

This research report on the U.S heat pump market is segmented and sub-segmented into the following categories.

By Source Type

- Air-Source

- Air-to-Air

- Air-to-Water

- Water-Source

- Surface Water

- Open Loop

- Ground / Geothermal Source

- Closed Loop Vertical

- Closed Loop Horizontal

- Direct Expansion

By Rated Capacity

- Up to 10 kW

- 10-20 kW

- 20-30 kW

- Above 30 kW

By System Design

- Split System

- Monobloc

- Hybrid Heat Pump

By End-User

- Residential

- Commercial

- Industrial

- Institutional

By Application

- Space Heating and Cooling

- Water Heating

- District Heating

- Process and Industrial Heating

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States