U.S. Home Security Market Size, Share, Trends & Growth Forecast Report Segmented By End-User (Wired Systems, Wireless Systems, Hybrid Systems), Component, System Type, Service Type and Country – Industry Analysis From 2026 to 2034

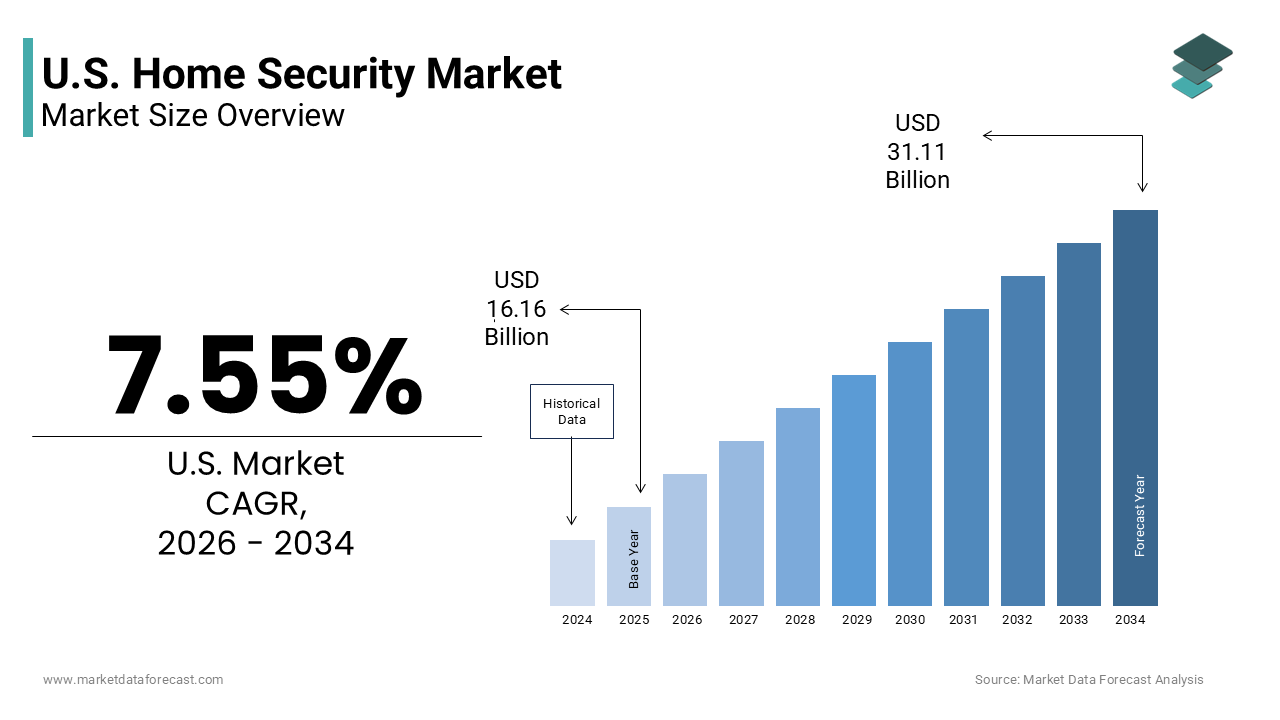

Market Size, 2025

$16.16 BnMarket Estimate, 2026

$17.38 BnMarket Forecast, 2034

$31.11 BnCAGR, 2026–2034

7.55%U.S. Home Security Market Report Summary

The U.S. home security market was valued at USD 16.16 billion in 2025, is estimated to reach USD 17.38 billion in 2026, and is projected to reach USD 31.11 billion by 2034, growing at a CAGR of 7.55% during the forecast period from 2026 to 2034. The growth of the U.S. home security market is driven by rising concerns regarding property crime and package theft, increasing smart home adoption, and growing demand for connected security solutions. Expanding integration of artificial intelligence-enabled surveillance systems, increasing adoption of wireless and DIY security systems, and rising consumer preference for remote monitoring capabilities are further accelerating market growth. Moreover, advancements in predictive analytics, expansion of flexible subscription-based security services, and increasing investments in smart home ecosystems are supporting the expansion of the U.S. home security market.

Key Market Trends

- Rising adoption of smart security devices including video doorbells, wireless cameras, and smart locks integrated with voice assistants.

- Growing consumer preference for DIY home security systems with flexible subscription and self-monitoring capabilities.

- Increasing use of artificial intelligence and predictive analytics for facial recognition, anomaly detection, and intelligent alerts.

- Strong focus on wireless and hybrid security systems offering scalability, remote access, and easy installation.

- Expansion of home automation integration combining security, lighting, climate control, and energy management solutions.

Segmental Insights

- Based on system type, the wireless systems segment dominated the U.S. home security market and held the largest share in 2025. The segment’s dominance is attributed to ease of installation, flexibility for renters and homeowners, compatibility with smart home ecosystems, and increasing demand for DIY security solutions.

- The hybrid systems segment is projected to witness the fastest CAGR during the forecast period owing to the growing preference for combined wired and wireless reliability, enhanced scalability, and improved security redundancy across large residential properties.

- Based on component, the cameras segment accounted for the leading share of the U.S. home security market in 2025. The dominance of this segment is driven by increasing concerns regarding package theft and burglary, strong demand for visual verification systems, and advancements in high-definition and AI-powered surveillance technologies.

- The sensors segment is anticipated to register notable growth during the forecast period due to increasing adoption of environmental monitoring devices including smoke, water leak, carbon monoxide, and motion sensors integrated into holistic home safety ecosystems.

- Based on service type, the professional monitoring segment held the major share of the U.S. home security market in 2025 owing to growing consumer preference for 24/7 emergency response services, enhanced reliability, and insurance incentives associated with professionally monitored systems.

- The self-monitoring segment is expected to witness rapid growth during the forecast period because of lower operational costs, no-contract flexibility, growing smartphone-based monitoring adoption, and increasing consumer demand for autonomous home security management.

Regional Insights

The United States maintained a dominant position in the North American home security market in 2025, supported by high homeownership rates, widespread broadband penetration, and strong consumer awareness regarding residential safety and smart home technologies. California remains a major contributor to the U.S. home security market due to its high smart home adoption rates, strong technology infrastructure, and increasing investments in connected home ecosystems. New York, Washington, and Oregon are also witnessing notable growth driven by increasing urbanization, rising concerns regarding package theft, and growing consumer demand for advanced home automation and surveillance solutions.

Competitive Landscape

The U.S. home security market is highly competitive and characterized by the presence of established professional monitoring providers, smart home technology firms, and DIY security solution providers competing through innovation, ecosystem integration, and subscription flexibility. Leading companies are focusing on expanding AI-driven surveillance capabilities, strengthening cybersecurity frameworks, investing in wireless and cloud-based technologies, and enhancing interoperability with broader smart home platforms. Strategic collaborations with technology providers, insurance companies, and telecommunications firms are further strengthening market positioning across residential security segments. Prominent players in the U.S. home security market include ADT Inc., Vivint Smart Home, Inc., SimpliSafe, Inc., Ring LLC, Google Nest, Alarm.com Holdings, Inc., Brinks Home Security, Frontpoint Security Solutions, LLC, Abode Systems, Inc., Johnson Controls International plc, Honeywell International Inc., and Bosch Security

U.S. Home Security Market Size

The U.S. home security market size was valued at USD 16.16 billion in 2025 and is anticipated to reach USD 17.38 billion in 2026 from USD 31.11 billion by 2034, growing at a CAGR of 7.55% during the forecast period from 2026 to 2034.

The U.S. home security market encompasses a comprehensive ecosystem of hardware, software, and monitoring services designed to protect residential properties from unauthorized access, theft, fire, and environmental hazards. This sector integrates traditional alarm systems with modern smart home technologies, including internet-connected cameras, motion sensors, smart locks, and video doorbells. The U.S. market is characterized by a shift from professional installation and long-term contracts toward DIY solutions and flexible subscription models. As per the Federal Bureau of Investigation, there were approximately 238,000 reported cases of burglary in the U.S. in 2022, indicating a persistent need for protective measures despite overall declining crime rates in certain categories. The psychological impact of property crime drives consumer behavior significantly. According to the Pew Research Center, nearly 60% of Americans express concern about package theft, which has spurred the adoption of porch cameras and smart delivery boxes. The proliferation of broadband internet and smartphone penetration facilitates remote monitoring and real-time alerts, enhancing user engagement. Insurance companies also influence the market by offering premium discounts for homes equipped with certified security systems. The integration of artificial intelligence allows for advanced features such as facial recognition and anomaly detection. Regulatory frameworks regarding data privacy and surveillance vary by state, affecting product deployment strategies. This market serves as a critical component of the broader smart home industry, influencing consumer confidence and property values. The convergence of safety, convenience, and connectivity defines the current landscape.

MARKET DRIVERS

Rising Concerns over Property Crime and Package Theft

Rising concerns over property crime and package theft is a key factor propelling the growth of the U.S. home security market. Although violent crime rates have fluctuated, property-related offenses remain a significant concern for homeowners, particularly in urban and suburban areas. According to the Federal Bureau of Investigation, property crime accounted for the majority of reported offenses in recent years, with larceny-theft being the most prevalent category. The surge in e-commerce has exacerbated issues related to package theft, also known as porch piracy. As per the Consumer Electronics Association, over 40% of American households have experienced package theft, prompting the installation of video doorbells and outdoor cameras. These devices provide visual evidence and deter potential thieves through visible presence. The psychological sense of vulnerability drives consumers to seek proactive solutions rather than reactive measures. Neighborhood watch programs and community apps like Nextdoor amplify awareness of local incidents, further stimulating demand. Homeowners perceive security systems as essential tools for safeguarding assets and ensuring family safety. The visibility of security cameras acts as a deterrent, reducing the likelihood of attempted break-ins. Insurance providers often require or incentivize these installations, leading to higher adoption rates. The tangible threat of loss, combined with the availability of affordable technology, creates a robust demand environment. Consequently, the fear of crime remains a dominant driver sustaining market growth.

Integration of Smart Home Automation and Connectivity

Integration of smart home automation and connectivity significantly propels the expansion of the U.S. home security market by offering enhanced convenience and control. Modern consumers seek seamless integration between security devices and other smart home components, such as lighting, thermostats, and voice assistants. According to the Consumer Technology Association, shipments of smart home devices reached record levels in 2023, with security cameras and smart locks leading the category. The ability to monitor and control home systems remotely via smartphones appeals to tech-savvy demographics. As per Statista, over 50 million US households utilize some form of smart home technology, creating a fertile ground for security product adoption. Interoperability standards, such as Matter, enable devices from different manufacturers to work together, enhancing user experience. The convenience of automating security routines, such as arming alarms when leaving home, adds value beyond mere protection. Voice control integration with platforms like Amazon Alexa and Google Assistant allows for hands-free operation. The aesthetic appeal of sleek, wireless devices also influences purchasing decisions. Consumers view security systems as part of a holistic smart living experience rather than isolated safety tools. This convergence drives cross-selling opportunities and increases customer retention. The ease of installation and user-friendly interfaces lower barriers to entry. Thus, the synergy between security and automation sustains market momentum.

MARKET RESTRAINTS

Data Privacy Concerns and Cybersecurity Vulnerabilities

Data privacy concerns and cybersecurity vulnerabilities significantly restrain the growth of the U.S. home security market by eroding consumer trust. The increasing connectivity of security devices exposes them to potential hacking and unauthorized access. According to the Federal Trade Commission, complaints regarding identity theft and fraud involving smart devices have risen sharply in recent years. High-profile breaches, where hackers accessed live camera feeds or stored footage, have garnered media attention, causing public apprehension. As per the Internet of Things Security Foundation, many inexpensive smart security devices lack robust encryption and regular software updates, making them easy targets for cybercriminals. Consumers worry about the misuse of personal data collected by these devices, including video recordings and usage patterns. The lack of standardized regulations for data handling across manufacturers creates uncertainty. Some users hesitate to install indoor cameras due to fears of surveillance abuse. The complexity of securing home networks against intrusions requires technical knowledge that average consumers may lack. Negative publicity surrounding privacy violations can dampen sales and slow adoption rates. Manufacturers face pressure to invest heavily in cybersecurity measures, which increases costs. The balance between functionality and privacy remains a delicate issue. Until robust security standards are universally adopted and enforced, consumer skepticism will persist. This restraint limits the potential market size, particularly among privacy-conscious individuals.

High Costs of Professional Monitoring and Installation

High costs of professional monitoring and installation pose a significant barrier to entry for many potential customers in the U.S. home security market. Traditional security systems often require substantial upfront payments for equipment and professional installation fees. According to HomeAdvisor, the average cost to install a hardwired security system ranges from 600 to 1,500 USD, excluding monthly monitoring fees. These initial expenses can be prohibitive for budget-conscious homeowners and renters. As per the Bureau of Labor Statistics, inflationary pressures on household budgets have led consumers to prioritize essential spending over discretionary items like premium security services. Monthly monitoring subscriptions, which can range from 20 to 60 USD, add to the long-term financial burden. Many consumers perceive these recurring costs as unnecessary, especially when DIY alternatives offer similar features at lower prices. The requirement for long-term contracts with early termination fees further discourages adoption. Renters who move frequently find it difficult to justify investing in permanent installations. The total cost of ownership, including maintenance and potential upgrades, adds to the financial strain. While financing options exist, they often involve interest charges that increase the overall expense. The perception of high value versus cost leads some consumers to opt for basic standalone devices instead of comprehensive systems. This financial constraint limits market penetration among lower-income demographics.

MARKET OPPORTUNITIES

Expansion of Artificial Intelligence and Predictive Analytics

Expansion of artificial intelligence and predictive analytics presents a substantial opportunity for the U.S. home security market. AI-driven features, such as facial recognition, person detection, and behavior analysis, enhance the accuracy and utility of security systems. According to the National Institute of Standards and Technology, advancements in computer vision have significantly reduced false alarms by distinguishing between humans, animals, and vehicles. This improvement increases user trust and reduces notification fatigue. As per the Brookings Institution, AI-enabled security systems can predict potential threats by analyzing patterns and anomalies in real time. For instance, systems can alert homeowners if a stranger loiters near the property for an extended period. The integration of machine learning allows devices to adapt to user habits and optimize settings automatically. Smart cameras can identify familiar faces and only send alerts for unknown individuals, enhancing privacy and relevance. The ability to search video footage using natural language queries improves usability. Manufacturers can offer premium subscription tiers based on advanced AI features, creating new revenue streams. The growing sophistication of AI algorithms enables more proactive security measures. This technological evolution attracts tech enthusiasts and early adopters willing to pay for superior performance. The potential for continuous improvement through software updates ensures long-term engagement. By leveraging AI, companies can differentiate their products in a crowded market.

Growth in DIY Security Solutions and Flexible Subscriptions

Growth in DIY security solutions and flexible subscriptions offers a promising avenue for expanding the customer base in the U.S. home security market. Consumers increasingly prefer self-installation options that are easy to set up and do not require professional assistance. According to Parks Associates, over 40% of US broadband households use DIY security systems, citing ease of use and lower costs as primary reasons. The availability of wireless and battery-powered devices simplifies installation, allowing renters and homeowners to customize their setups. As per the Consumer Electronics Show, trends indicate a shift toward no-contract monthly subscriptions that allow users to cancel or pause services at any time. This flexibility appeals to younger demographics and those with transient lifestyles. The modular nature of DIY systems enables users to start with basic components and expand over time. Retail partnerships with big-box stores and online platforms increase accessibility and visibility. The reduction in hardware costs due to mass production makes these systems more affordable. Marketing campaigns emphasizing empowerment and simplicity resonate with modern consumers. The ability to integrate with existing smart home ecosystems enhances appeal. This model lowers the barrier to entry and encourages trial. By catering to the demand for autonomy and flexibility, companies can capture a larger share of the market. The trend towards democratization of security technology supports sustained growth.

MARKET CHALLENGES

Fragmentation and Lack of Interoperability Standards

Fragmentation and lack of interoperability standards is a major challenge to the U.S. home security market by complicating the user experience and limiting device compatibility. The market features a wide array of proprietary protocols and ecosystems that often do not communicate seamlessly with each other. According to the Zigbee Alliance, despite efforts to create universal standards, many devices remain locked within specific manufacturer ecosystems. This fragmentation forces consumers to choose between brands or use multiple apps to control different devices. As per a Consumer Reports survey, confusion over compatibility is a top reason for hesitation in purchasing smart home security products. The introduction of the Matter standard aims to address this issue, but adoption has been gradual and inconsistent. Older devices may not support new protocols, leading to obsolescence and waste. Integrators and installers face difficulties in designing cohesive systems for clients with mixed preferences. The lack of uniformity increases support costs and customer frustration. Manufacturers may resist open standards to maintain lock-in and recurring revenue from proprietary accessories. This competitive dynamic hinders the development of a unified smart home environment. Consumers seeking comprehensive solutions may delay purchases until compatibility improves. The industry must collaborate to establish and enforce robust interoperability guidelines. Until then, fragmentation will remain a significant hurdle to widespread adoption and satisfaction.

Regulatory Compliance and Legal Liability Issues

Regulatory compliance and legal liability issues pose significant challenges to manufacturers and service providers in the U.S. home security market. Laws regarding surveillance data storage, consent, and sharing vary widely across states and municipalities. According to the Electronic Frontier Foundation, several states have enacted strict laws requiring explicit consent before recording audio or video in private spaces. Companies must navigate this complex legal landscape to avoid fines and lawsuits. As per the American Civil Liberties Union, concerns about government access to private security footage have led to calls for stricter regulations on data retention and sharing. Manufacturers must ensure their products comply with evolving privacy laws, such as the California Consumer Privacy Act. Failure to protect user data can result in class-action lawsuits and reputational damage. The liability for false alarms that trigger emergency response resources also poses financial risks. Some jurisdictions impose fines for excessive false alarms, placing a burden on homeowners and providers. The legal uncertainty surrounding AI-driven decisions, such as automated police dispatch, adds another layer of complexity. Companies must invest in legal counsel and compliance teams to mitigate risks. The cost of adhering to diverse regulatory requirements increases operational expenses. Small players may struggle to keep up with changing laws, leading to market consolidation. Balancing innovation with legal responsibility remains a critical challenge for the industry.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.55% |

| Segments Covered | By System Type, Component, Service Type, End-User and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | ADT Inc., Vivint Smart Home, Inc., SimpliSafe, Inc., Ring LLC, Google Nest, Alarm.com Holdings, Inc., Brinks Home Security, Frontpoint Security Solutions, LLC, Abode Systems, Inc., Johnson Controls International plc, Honeywell International Inc., and Bosch Security Systems. |

SEGMENTAL ANALYSIS

By System Type Insights

The wireless systems segment accounted for 64.6% of the U.S. market share in 2025. The growth of the wireless systems segment in the U.S. market is attributed to the ease of installation and compatibility with modern smart home ecosystems. Ease of installation and flexibility for renters and homeowners drive the domination of wireless systems in the U.S. home security market. Traditional wired systems require professional drilling and cabling, which can be invasive and costly. According to Parks Associates, over 70% of DIY security system buyers cite easy installation as the primary reason for choosing wireless options. These systems often use adhesive mounts or simple screw fixtures, allowing users to set up sensors and cameras in minutes. As per the National Apartment Association, nearly 35% of US households are renters who prefer non-permanent security solutions that can be easily moved to new residences. Wireless systems eliminate the risk of damaging walls or violating lease agreements. The modular nature of these devices allows users to start with a basic kit and expand coverage as needed. This scalability appeals to budget-conscious consumers who want to spread costs over time. The absence of complex wiring reduces the likelihood of installation errors, ensuring reliable performance. Manufacturers design these products with user-friendly apps that guide setup processes, further simplifying adoption. The convenience of self-installation aligns with the fast-paced lifestyles of modern consumers. This accessibility broadens the market beyond traditional homeowners to include students and young professionals. Consequently, the plug-and-play nature of wireless systems sustains their market leadership.

On the other end, the hybrid systems segment is the fastest growing segment and is anticipated to grow at a CAGR of 13.3% during the forecast period owing to the desire for robust security without the limitations of purely wired or wireless setups. A balance of reliability and expandability drives the rapid growth of hybrid systems in the U.S. home security market. Wired connections offer superior stability and power consistency for critical components like control panels and main sensors, while wireless modules allow for easy expansion. According to the Security Industry Association, hybrid installations have increased by 15% annually as consumers seek best-of-both-worlds solutions. As per the Electronic Security Association, professional installers recommend hybrid systems for larger homes where wireless signal strength may vary. The wired backbone ensures that essential alarms function even during Wi-Fi outages or interference. Wireless additions enable users to monitor peripheral areas, such as garages, sheds, or gates, without running new cables. This combination provides a layered defense strategy that enhances overall security posture. Homeowners appreciate the redundancy offered by hybrid architectures, which mitigates single points of failure. The ability to upgrade specific parts of the system without replacing the entire infrastructure extends the product lifecycle. Installers benefit from reduced labor costs compared to full wired setups while maintaining high service quality. The versatility of hybrid systems appeals to both new constructions and retrofit projects. This adaptability supports diverse architectural styles and security needs. The growing complexity of home layouts necessitates flexible yet reliable solutions. Thus, hybrid systems capture a growing share of the premium market segment.

By Component Insights

The cameras segment dominated the market by holding 41.4% of the U.S. market share in 2025. The dominance of cameras segment in the U.S. market is driven by the high consumer demand for visual verification and deterrence. Visual verification and deterrence of criminal activity drive the domination of cameras in the U.S. home security market. Visible cameras act as a powerful psychological deterrent to potential intruders, reducing the likelihood of break-ins. According to a University of North Carolina at Charlotte study on burglars, 60% of offenders said they would seek an alternative target if they observed surveillance cameras. This preventive effect makes cameras a primary choice for homeowners seeking proactive security. As per Ring Neighbors app data, communities with high camera adoption rates report lower incidences of package theft and vandalism. The ability to record evidence aids law enforcement in identifying and prosecuting suspects. High-definition video quality and night vision features ensure clear footage in various lighting conditions. Two-way audio capabilities allow homeowners to communicate with visitors or warn off trespassers remotely. The tangible sense of security provided by visual monitoring appeals to families and pet owners. Insurance companies often offer discounts for homes with visible surveillance systems. The widespread availability of affordable, high-quality cameras has democratized access to this technology. Consumers perceive cameras as essential tools for protecting property and loved ones. The continuous improvement in image resolution and field of view enhances effectiveness. Thus, the proven deterrent value sustains the leading position of cameras.

On the other side, the sensors segment is a promising segment and is estimated to witness a CAGR of 12.5% during the forecast period in the U.S. market. The expansion of environmental and life safety monitoring drives the rapid growth of sensors in the U.S. home security market. Modern security systems increasingly incorporate sensors for smoke, carbon monoxide, water leaks, and temperature changes. According to the National Fire Protection Association, home fire deaths decreased by 50% since 1980, partly due to widespread smoke detector usage. As per the Insurance Information Institute, water damage is one of the most common home insurance claims, prompting adoption of leak sensors. These devices provide early warnings, preventing catastrophic damage and saving lives. Smart sensors can automatically shut off water mains or alert emergency services, enhancing response times. The integration of these sensors into security platforms offers a holistic safety solution. Homeowners value the peace of mind knowing their property is protected from multiple threats. The aging population increases demand for fall detection and health monitoring sensors. Regulatory codes in some states mandate interconnected smoke and CO alarms, driving replacements. The affordability of wireless environmental sensors encourages whole-home coverage. Insurance discounts for monitored life safety devices further incentivize purchases. The shift from reactive to preventive safety measures supports sensor growth. This broader definition of security expands the market beyond intrusion detection. The critical nature of life safety ensures sustained demand for advanced sensors.

By Service Type Insights

The professional monitoring segment occupied 54.9% of the U.S. market share in 2025. The growth of the professional monitoring segment in the U.S. market is attributed to assurance of immediate response and reliability. The assurance of immediate emergency response and reliability drives the domination of professional monitoring in the U.S. home security market. Homeowners value the knowledge that trained professionals are watching their systems around the clock. According to the Security Industry Association, professionally monitored systems result in faster police response times compared to self-monitored alternatives. As per the Federal Emergency Management Agency, verified alarms receive higher priority from law enforcement agencies, reducing response delays. The ability to contact homeowners and verify emergencies before dispatching authorities prevents false alarm fines. This layer of verification enhances credibility and cooperation with local police departments. Professional monitoring centers are equipped with backup power and communication lines, ensuring operation during outages. The peace of mind provided by constant oversight is invaluable for families with elderly members or young children. Insurance companies often require professional monitoring for premium discounts, validating its importance. The expertise of monitoring agents in handling diverse emergencies, from medical crises to fires, adds value. Consumers trust established providers with proven track records of reliability. The subscription model ensures consistent revenue for providers, allowing for continuous service improvement. The critical nature of emergency response sustains the leading position of professional monitoring. The human element provides a safety net that technology alone cannot replicate.

However, the self-monitoring segment is the fastest growing segment and is expected to exhibit a CAGR of 15.4% during the forecast period. Cost savings and no-contract flexibility drive the rapid growth of self-monitoring in the U.S. home security market. Self-monitoring eliminates monthly fees associated with professional services, appealing to budget-conscious consumers. According to Parks Associates, over 60% of DIY security users choose self-monitoring to avoid long-term contracts. As per the Consumer Federation of America, the average annual savings from self-monitoring exceed 200 USD compared to professional plans. This financial benefit attracts renters and young homeowners with limited disposable income. The freedom to cancel or pause services without penalty enhances user control. Mobile apps provide all necessary tools for monitoring and managing alerts effectively. The transparency of pricing models builds trust with customers. The ability to customize notification settings allows for personalized experiences. Users appreciate the autonomy of deciding when to contact authorities. The rise of reliable cellular and Wi-Fi connections ensures timely alert delivery. The democratization of security technology empowers individuals to take charge of their safety. This shift towards consumer control drives rapid adoption. The economic advantages of self-monitoring make it accessible to a broader audience. The flexibility aligns with modern preferences for subscription freedom. Thus, cost and convenience fuel the growth of self-monitoring.

REGIONAL ANALYSIS

The U.S. held the largest share of the North American home security market in 2025 and serves as the global leader in adoption and innovation. The country's market status is characterized by high homeownership rates, substantial disposable income, and a strong culture of personal safety. The prevalence of single-family homes drives significant demand for comprehensive security solutions. Dominance driven by high homeownership and safety culture defines the U.S. home security market. The vast number of single-family homes provides a large base for security installations. According to the U.S. Census Bureau, the homeownership rate stands at approximately 65%, creating a stable demand for permanent security systems. As per a Gallup Poll, safety and security rank among the top concerns for American homeowners, influencing purchasing decisions. The cultural emphasis on individual responsibility for property protection drives proactive adoption of security technologies. The widespread availability of credit and financing options facilitates upfront purchases. The strong real estate market encourages sellers to install security systems to enhance property value. The influence of media and community apps raises awareness of local crime trends, stimulating demand. The robust retail infrastructure ensures easy access to security products. The high penetration of broadband internet supports connected security devices. This combination of structural and cultural factors ensures that the U.S. remains the dominant force in the regional market. The continuous innovation in smart home technology reinforces this leadership. The strategic focus on personal safety sustains high market activity.

COMPETITIVE LANDSCAPE

The competition in the U.S. home security market is characterized by intense rivalry among established monitoring companies and agile technology firms striving to offer superior protection and convenience. Major players compete based on system reliability ease of installation and integration with smart home platforms. The market features a mix of traditional providers with long term contracts and newer entrants offering flexible no contract DIY solutions. Companies differentiate themselves through unique hardware features such as high definition video and artificial intelligence driven detection. Strategic alliances with telecommunications and insurance providers help firms expand their reach and offer bundled services. Price competitiveness remains a key factor particularly in the DIY segment where hardware costs are low. Brand trust and customer service quality are critical for retaining subscribers in the professional monitoring sector. The rise of big tech companies entering the space disrupts traditional models with ecosystem lock in strategies. Intellectual property related to software and connectivity protocols serves as a competitive barrier. This dynamic environment drives continuous innovation and price adjustments benefiting consumers with diverse and affordable options. The ability to adapt to technological trends determines long term success.

KEY MARKET PLAYERS

Some of the promising companies that are playing a dominating role in the U.S. home security market include

- ADT Inc.

- Vivint Smart Home, Inc.

- SimpliSafe, Inc.

- Ring LLC

- Google Nest

- Alarm.com Holdings, Inc.

- Brinks Home Security

- Frontpoint Security Solutions, LLC

- Abode Systems, Inc.

- Johnson Controls International plc

- Honeywell International Inc.

- Bosch Security Systems

Top Players in the US Home Security Market

ADT Inc

ADT Inc remains a cornerstone of the U.S. home security industry by providing comprehensive professional monitoring and installation services. The company leverages its extensive brand recognition and vast network of authorized dealers to serve millions of residential customers. Recent actions include a strategic partnership with Google to integrate Nest products into ADT systems enhancing smart home capabilities. ADT has also expanded its DIY offerings through the ADT Self Setup program to capture younger demographics. The firm invests heavily in cybersecurity measures to protect customer data and ensure system reliability. By combining traditional monitoring with modern smart technology ADT maintains its relevance in a rapidly evolving market. The company continues to focus on customer retention through improved service quality and innovative product bundles. These efforts solidify its position as a trusted provider of home safety solutions.

Amazon.com Inc

Amazon.com Inc significantly influences the market through its Ring brand which pioneered the video doorbell category. The company integrates security devices with its Alexa ecosystem creating a seamless smart home experience for users. Recent developments involve the expansion of Ring Always Home Cam and enhanced neighborhood safety features via the Ring Neighbors app. Amazon leverages its massive logistics network to ensure rapid delivery and easy access to security products. The firm focuses on affordable pricing and subscription based revenue models through Ring Protect plans. By prioritizing user friendly interfaces and cloud storage solutions Amazon drives widespread adoption of self monitored security systems. The integration of artificial intelligence for person detection enhances device utility. These strategies strengthen Amazon's dominance in the DIY security segment and expand its footprint in connected home technologies.

SimpliSafe Inc

SimpliSafe Inc contributes to the market by offering flexible no contract home security systems that emphasize ease of use. The company targets consumers seeking professional grade protection without long term commitments or high installation costs. Recent actions include the launch of advanced outdoor cameras and smart locks that integrate with major smart home platforms. SimpliSafe has enhanced its mobile app functionality to provide real time alerts and remote system control. The firm focuses on transparent pricing and exceptional customer support to build trust and loyalty. By avoiding aggressive sales tactics SimpliSafe appeals to tech savvy homeowners who value autonomy. The company continuously updates its sensor technology to improve accuracy and reduce false alarms. These initiatives reinforce its reputation as a leading provider of accessible and reliable DIY home security solutions.

Top Strategies Used by Key Market Participants

Key players in the U.S. home security market primarily employ strategies focused on product innovation and strategic partnerships to maintain competitive advantage. Companies invest heavily in research and development to create advanced sensors cameras and artificial intelligence driven analytics. Strategic collaborations with technology giants enable integration with broader smart home ecosystems enhancing user convenience. Firms prioritize flexible subscription models including no contract options to attract budget conscious and renter demographics. Marketing efforts emphasize ease of installation and user friendly mobile applications to appeal to DIY enthusiasts. Providers also focus on cybersecurity enhancements to protect customer data and build trust. Expansion into professional monitoring services for DIY systems creates hybrid revenue streams. Customer retention is driven by bundled services and responsive support teams. These strategic initiatives enable firms to differentiate their offerings and respond effectively to changing consumer preferences in the dynamic home security sector.

MARKET SEGMENTATION

This research report on the U.S. home security market has been segmented based on the following categories.

By System Type

- Wired Systems

- Wireless Systems

- Hybrid Systems

By Component

- Alarms

- Cameras

- Sensors

- Control Panels

- Access Controls

By Service Type

- Professional Monitoring

- Self-Monitoring

- Home Automation Integration

By End User

- Residential

- Small Business

- Enterprise

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com