- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

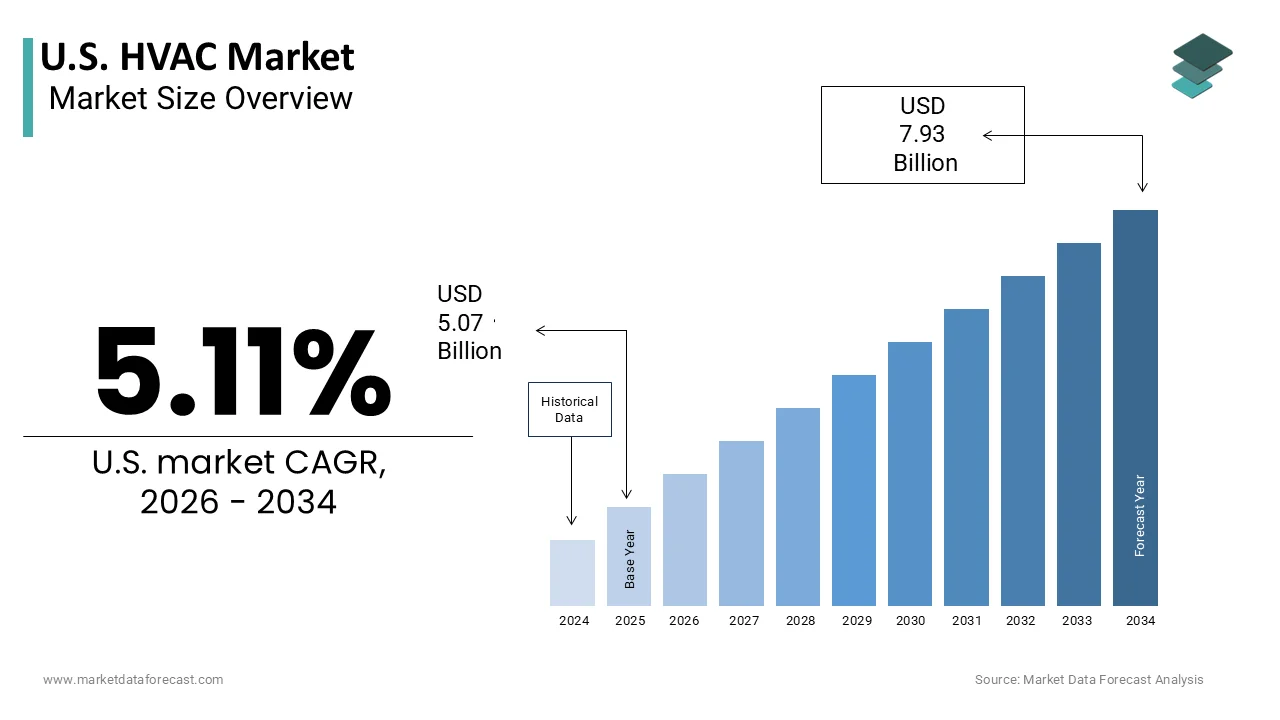

Market Size, 2025

$5.07 BnMarket Estimate, 2026

$5.33 BnMarket Forecast, 2034

$7.93 BnCAGR, 2026–2034

5.11%U.S. HVAC Market Size

The U.S. HVAC Market was valued at USD 5.07 billion in 2025, is estimated to reach USD 5.33 billion in 2026, and is projected to reach USD 7.93 billion by 2034, growing at a CAGR of 5.11% from 2026 to 2034.

The heating, ventilation,n and air conditioning are the systems and technologies designed to regulate indoor environmental quality, including temperature, relative humidity, and air purity across residential, commercial, and industrial sectors. The definition extends beyond simple climate control to include integrated smart building solutions that optimize energy consumption and operational performance. Consumer and corporate engagement with these systems is heavily influenced by regulatory mandates and technological advancements in sustainability. According to the United States Census Bureau, there are approximately 140 million housing units in the nation, many of which require regular maintenance or replacement of aging climate control infrastructure. Furthermore, data from the Bureau of Labor Statistics indicates that employment in the installation, maintenance,ce and repair of mechanical equipment continues to grow, row reflecting the labor-intensive nature of this sector. The increasing frequency of extreme weather events has heightened the necessity for reliable and resilient HVAC systems. As per the Environmental Protection Agency, heating and cooling account for nearly 50% of the energy used in a typical American home, underscoring the significant impact of these systems on national energy consumption. The transition toward electrification and decarbonization is reshaping product development priorities. Manufacturers are focusing on heat pump technologies and variable refrigerant flow systems to meet stringent federal guidelines.

MARKET DRIVERS

Stringent Government Regulations and Energy Efficiency Standards

The federal and state-level mandates aimed at reducing carbon emissions and improving energy efficiency for the adoption of advanced HVAC technologies are fuelling the growth of the United States HVAC market. The implementation of stricter minimum efficiency standards forces manufacturers and consumers to replace outdated equipment with high-performance alternatives. According to the Department of Energy, new efficiency standards for residential central air conditioners and heat pumps took effect in 2023, requiring a minimum seasonal energy efficiency ratio of 14.3 or 15.2, depending on the region. This regulatory shift drives significant replacement demand as older units no longer comply with legal requirements for installation. As per data from the Environmental Protection Agency, through the Energy Star program, has helped Americans save billions of dollars on utility bills by promoting certified high-efficiency products. The Inflation Reduction Act further accelerates this trend by providing tax credits and rebates for homeowners who install qualified energy-efficient HVAC systems. These financial incentives lower the upfront cost barrier, making premium technologies more accessible to a broader consumer base. State-level initiatives, such as California’s Title 24 building standards, also push for deeper reductions in energy use. Compliance with these regulations is not optional, creating a consistent baseline for market activity. Manufacturers must continuously innovate to meet these evolving benchmarks, ensuring a steady pipeline of upgraded products.

Increasing Frequency of Extreme Weather Events and Climate Variability

The rising incidence of extreme weather conditions, including heat waves, cold snaps, and humidity fluctuation,s drives urgent demand for reliable and robust HVAC systems, which is also elevating the growth of the United States HVAC market. Consumers and businesses are increasingly prioritizing climate resilience to maintain safe and comfortable indoor environments amidst unpredictable outdoor conditions. According to the National Oceanic and Atmospheric Administration, the United States experienced 18 separate billion-dollar weather and climate disasters in 2022, highlighting the growing volatility of regional climates. Prolonged periods of excessive heat increase the load on the cooling systems,s leading to higher failure rates and the need for replacements. As per data from the Centers for Disease Control and Prevention, extreme heat is a leading cause of weather-related mortality, emphasizing the critical role of air conditioning in public health. The expansion of habitable zones in previously cooler regions due to warming trends also increases the installation base for cooling equipment. Homeowners are investing in higher capacity units and backup systems to ensure continuity during power outages or extreme stress on the grid. Commercial entities similarly upgrade their infrastructure to protect assets and ensure business continuity. The psychological impact of climate anxiety further motivates proactive upgrades rather than reactive repairs. Insurance companies are also beginning to incentivize resilient infrastructure through premium discounts.

MARKET RESTRAINTS

High Initial Installation Costs and Economic Sensitivity

The substantial capital investment required for the purchase and installation of modern HVAC systems for many residential and small commercial consumers is restraining the growth of the United States HVAC market. High efficiency units often come with premium price tags that can be prohibitive for budget-constrained households. According to the Bureau of Labor Statistics, the average cost for installing a new central air conditioning system ranges from 3000 to 7000 dollars, depending on capacity and complexity. This financial burden is exacerbated by inflationary pressures on materials and labor, which have increased overall project costs. The rising interest rates have made financing options more expensive, discouraging discretionary upgrades and delaying necessary replacements. Many consumers opt to repair existing inefficient units rather than invest in new technology due to immediate cash flow constraints. The lack of standardized pricing across contractors also creates uncertainty and hesitation among buyers. Economic downturns further suppress demand as households prioritize essential expenditures over home improvement projects. Small businesses operating on thin margins may also defer infrastructure upgrades to preserve liquidity. While government incentives exist, they often require upfront payment with reimbursement later, which does not alleviate immediate cash flow issues. The perceived complexity of navigating rebate programs also deters participation. This economic sensitivity limits the rate of adoption for advanced technologies and slows the overall turnover of the installed base.

Acute Shortage of Skilled Labor and Technical Expertise

The shortage of qualified technicians and installers, which impacts service quality,y is impeding the growth of the United States HVAC market. The retirement of experienced workers, combined with the insufficient influx of new talent, creates difficulties in system installation and maintenance. According to the Associated Builders and Contractors, the construction industry needs to attract approximately 546000 additional workers beyond the normal hiring pace to meet demand in the coming years. This labor gap leads to longer wait times for customers and increased labor costs, which are passed on to consumers. The average age of skilled tradespeople is rising,g indicating an impending workforce crisis. The technical complexity of modern HVAC systems, ms requiring knowledge of electronics, refrigerants, and smart controls, raises the barrier to entry for recruits. Delays in installation can discourage consumers from proceeding with purchases, particularly during peak seasons. Poor installation practices due to inexperienced labor can also lead to system inefficiencies and premature failures, damaging brand reputation. The inability to scale service operations limits the capacity of manufacturers and distributors to expand their reach. Addressing this shortage requires significant investment in vocational training and apprenticeship programs.

MARKET OPPORTUNITIES

Integration of Smart Home Technology and IoT Connectivity

The proliferation of Internet of Things devices and smart home ecosystems to offer connected and intelligent climate control solutions is creating new opportunities for the growth of the United States HVAC market. Consumers are increasingly seeking systems that provide remote monitoring, automated adjustments, and energy usage insights through mobile applications. According to Statista, the number of smart home households in the United States is projected to reach 85 million by 202,5 creating a vast installed base for compatible HVAC equipment. Smart thermostats and connected HVAC units allow users to optimize energy consumption based on occupancy patterns and weather forecasts. The sales of smart home devices continue to grow, driven by the desire for convenience and cost savings. Manufacturers can leverage this trend by developing proprietary platforms that integrate seamlessly with popular voice assistants and home automation hubs. The data generated by these systems enables predictive maintenance, allowing service providers to address issues before they result in breakdowns. This shift from reactive to proactive service models creates new revenue streams for contractors and manufacturers. Enhanced user interfaces and personalized comfort settings improve customer satisfaction and brand loyalty. The ability to demonstrate tangible energy savings through real-time data appeals to environmentally conscious consumers. Partnerships with technology firms can accelerate innovation and expand market reach.

Expansion of Heat Pump Adoption Through Electrification Initiatives

The strategic shift toward electrification and decarbonization for the widespread adoption of heat pump technology is also expected to spur the growth of the United States HVAC market. Heat pumps provide both heating and cooling using electricity, making them a key solution for reducing reliance on fossil fuels. The heat pump sales globally are surging,g with the United States emerging as a major growth market due to policy support. The Inflation Reduction Act provides significant financial incentives for homeowners to switch from gas furnaces to electric heat pumps. As per data from the Rocky Mountain Institute, replacing gas heating with heat pumps can reduce household carbon emissions by up to 5,0% depending on the local grid mix. Modern cold climate heat pumps are now efficient enough to operate effectively in colder regions,ons expanding their geographical applicability. Utilities and state governments are launching rebate programs to encourage conversion,sion further driving demand. Manufacturers are responding by expanding their heat pump portfolios with models designed for specific climate zones. The dual functionality of these systems offers a value proposition by eliminating the need for separate heating and cooling units. Educational campaigns by industry associations are helping to dispel myths about heat pump performance in winter. The alignment of environmental goals with economic benefits creates a favorable environment for growth.

MAJOR CHALLENGES

Supply Chain Disruptions and Raw Material Volatility

The complex global supply chain for components, such as semiconductors, copper, aluminum, and rare earth metals,s is one of the major challenges for the growth of the United States HVAC market. Disruptions in these supply chains due to geopolitical tensions, NS trade policies, and logistical bottlenecks pose significant challenges to production and delivery. According to the Institute for Supply Management, manufacturing sectors have faced persistent delays in sourcing key materials, affecting lead times and inventory levels. Fluctuations in commodity prices directly impact manufacturing costs and profit margins. The producer price index for metal and mineral products has shown considerable volatility,y creating uncertainty for long-term contracts. The dependence on single-source suppliers for specialized components exacerbates vulnerabilities to regional disruptions. Tariffs on imported materials further increase costs, forcing companies to reassess sourcing strategies. Inventory management becomes challenging as businesses strive to balance stock levels against uncertain supply conditions. Delays in component availability can halt production lines and delay project completion,s leading to customer dissatisfaction. The transition to new refrigerants also requires changes in manufacturing processes and supply chains, adding complexity. Companies must invest in diversifying supplier bases and enhancing logistics resilience. However, these measures require significant capital and time. Navigating this volatile landscape requires agility and strategic foresight to maintain operational continuity.

Transition to Environmentally Friendly Refrigerants and Compliance Costs

The mandated phase-down of hydrofluorocarbons and the transition to low global warming potential refrigerants are expected to inhibit the growth of the United States HVAC market. Regulatory frameworks such as the American Innovation and Manufacturing Act require a gradual reduction in the production and consumption of certain refrigerants. Manufacturers must invest heavily in research and development to create systems compatible with new refrigerants such as R 454B and R 32. The transition requires retraining of technicians and updates to safety standards due to the flammability of some alternative refrigerants. The cost of compliance includes redesigning products, updating manufacturing facilities,s and educating the workforce. Existing inventory of older refrigerants may become stranded assets requiring careful management. The complexity of handling mildly flammable refrigerants raises liability and insurance concerns for contractors. Consumers may face higher costs for new systems that incorporate advanced safety features. The lack of universal standardization in some regions adds to the confusion and logistical burden. Ensuring a smooth transition without disrupting service availability is a delicate balancing act.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Implementation Type, Service Type, System Type, End User, Application Vertical, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Carrier Corporation, Trane Technologies plc, Daikin Industries Ltd., Johnson Controls International plc, Lennox International Inc., Rheem Manufacturing Company, Mitsubishi Electric Corporation, LG Electronics Inc., Panasonic Corporation, |

SEGMENTAL ANALYSIS

By Implementation Type Insights

The retrofit buildings segment was the largest by occupying 46.2% of the United States HVAC market share in 2025, with the vast existing infrastructure of aging residential and commercial properties that require system upgrades or replacements. The advanced age of the current building stock, which necessitates frequent maintenance and eventual replacement of inefficient units,s is fuelling the growth of the segment. According to the United States Census Bureau, the median age of owner-occupied housing units in the United States is approximately 39 years, indicating a significant portion of homes have HVAC systems nearing or exceeding their typical lifespan of 15 to 20 years. This demographic reality creates a consistent and large-scale demand for replacement services rather than new installations. Government incentives, such as tax credits for replacing older equipment, further accelerate this trend by reducing the financial burden on homeowners. The increasing cost of energy also motivates property owners to invest in high-efficiency retrofits to lower utility bills. Commercial building owners are similarly driven by stricter environmental regulations and corporate sustainability goals that mandate the modernization of legacy systems. The complexity of retrofitting often requires specialized expertise, which supports higher service margins.

The new construction segment is projected to witness the fastest CAGR of 5.4% in the coming years due to ongoing residential housing developments and commercial infrastructure projects despite broader economic fluctuations. The primary driver is the persistent shortage of housing inventory, which has spurred increased building activity across various regions. According to the United States Census Bureau, there were approximately 1.4 million housing starts in 2023, reflecting robust demand for new residential units. Each new unit requires a complete HVAC installation, creating a direct correlation between construction activity and market growth. The adoption of smart home technologies in new constructions is rising, with builders integrating advanced climate control systems as standard features to attract buyers. Modern building codes also mandate higher efficiency standards for newbuilds,s compelling developers to install premium HVAC systems. The growth of industrial facilities such as warehouses and data centers further contributes to this segment. These structures require specialized climate control solutions that drive demand for commercial-grade equipment. The shift toward green building certifications like LEED encourages the use of sustainable HVAC technologies in new projects.

By Service Type Insights

The installation and replacement services segment accounted in holding 44.3% of the United States HVAC market share in 2025, with the need to install new systems in both construction and retrofit scenarios. The initial setup of HVAC units in new buildings and the replacement of outdated systems in existing structures. According to the study, employment in the installation,n maintenance, and repair of mechanical equipment is projected to grow faster than the average for all occupations,s reflecting the labor-intensive nature of these services. The mandatory replacement of non-compliant equipment due to changing efficiency standards. The implementation of new minimum efficiency standards for central air conditioners and heat pumps has triggered a wave of replacements, as older units can no longer be installed legally. The high capital cost of HVAC equipment means that professional installation is essential to ensure warranty validity and optimal performance. Consumers rarely attempt DIY installation due to the complexity and safety risks involved,d ensuring steady demand for licensed contractors. The seasonal nature of HVAC demand also leads to spikes in installation activity during extreme weather periods. Commercial projects often involve large-scale installations that contribute significantly to revenue volume. The integration of smart technologies requires specialized installation skills, further reinforcing the need for professional services.

The maintenance and repair services segment is likely to witness the fastest CAGR of 6.8% from 2026 to 2034 with the increasing emphasis on system longevity and operational efficiency. The primary driver is the growing awareness among homeowners and facility managers that regular maintenance prevents costly breakdowns and extends equipment life. As per data from the Joint Center for Housing Studies at Harvard University, the aging housing stock requires more frequent repairs and upkeep, leading to sustained demand for service contracts. The rise of smart HVAC systems enables predictive maintenance,e allowing providers to address issues before they escalate. This shift from reactive to proactive service models creates recurring revenue streams for service providers. Commercial entities are increasingly adopting comprehensive maintenance agreements to ensure business continuity and comply with insurance requirements. The shortage of skilled labor also drives up the cost of emergency repairs, rs making preventive maintenance a more attractive option.Subscription-basedd maintenance plans are gaining popularity, offering customers peace of mind and priority service.

By System Type Insights

The cooling systems segment led the market and is anticipated to continue its lead in the U.S. market during the forecast period as rising temperatures across the country make air conditioning an essential utility. The domination of this segment is fueled by the geographic distribution of the population, with significant concentrations in the South and Southwest, where cooling is essential for habitability. According to the Energy Information Administration, 88% of U.S. households use air conditioning, and it accounts for about 19% of total electricity consumption in the residential sector. The increasing frequency and intensity of heatwaves due to climate change further amplify the demand for reliable and efficient cooling solutions. According to the Centers for Disease Control and Prevention, extreme heat is a leading cause of weather-related deaths in the U.S., making effective cooling critical for public health. The replacement of older, less efficient units with high SEER-rated systems is driven by both regulatory standards and consumer desire for lower energy bills. The growth of multi-family housing and commercial spaces with large glass facades increases the cooling load, requiring robust systems. Manufacturers are innovating with inverter technology and smart controls to enhance cooling performance while minimizing energy consumption. The universal need for thermal comfort during summer months ensures consistent demand. This segment benefits from the mandatory nature of cooling in many building codes. The cultural expectation of indoor comfort sustains the leadership of cooling systems.

On the other hand, the ventilation and indoor air quality (IAQ) systems segment is expected to be the fastest-growing system type in the U.S. during the forecast period, due to the recognition that proper ventilation and air filtration are essential for reducing the transmission of airborne pathogens and improving overall occupant health. According to the American Society of Heating, Refrigerating, and Air-Conditioning Engineers, standards 62.1 and 62.2 provide the recognized requirements for ventilation and IAQ, which have seen increased adoption in local building codes. The adoption of HEPA filters, UV germicidal irradiation, and energy recovery ventilators is becoming standard in new constructions and retrofits. According to the Environmental Protection Agency, levels of indoor air pollutants are often two to five times higher than outdoor levels, leading to increased demand for purification and monitoring solutions. The rise of remote work has led homeowners to invest in healthier home environments, including advanced ventilation systems. Commercial buildings are upgrading HVAC systems to meet WELL Building Standard certifications, which prioritize air quality. The integration of IAQ sensors with smart HVAC controls allows for real-time monitoring and adjustment of air quality parameters. Government grants for school and hospital upgrades often include IAQ improvements. These factors collectively ensure that the ventilation and IAQ segment expands rapidly as health becomes a primary driver for HVAC investment.

By End User and Application Vertical Insights

The residential segment held a significant share of the United States HVAC market in 202,5 with the sheer volume of single-family homes and multi-family units requiring climate control solutions. This segment accounts for the majority of HVAC sales due to the widespread ownership of private residences and the universal need for comfort. According to the United States Census Bureau, there are approximately 140 million housing unithe countryuntryr,y each representing a potential customer for HVAC products and services. The high rate of home ownership, which encourages investment in long-term improvements, such as HVAC upgrades. The homeowner spending on repairs and improvements reached record levels in recent years, with HVAC systems being a top priority. The emotional value placed on home comfort drives consumers to prioritize reliable and efficient climate control. The prevalence of extreme weather events further reinforces the necessity of robust residential HVAC systems. Government rebates for residential energy efficiency upgrades also stimulate demand in this sector. The fragmentation of the residential market allows for a diverse range of products from budget-friendly units to premium smart systems. Retail channels and local contractors play a crucial role in reaching this broad consumer base. The consistent turnover of housing stock and the aging of existing systems ensure a steady flow of replacement demand.

The data centers segment is likely to grow at the fastest CAGR of 9.5% from 2026 to 2034, with the explosive expansion of digital infrastructure and cloud computing services. The increasing demand for data storage and processing power, fueled by artificial intelligence, the Internet of Things, and 5G technologies. According to the International Energy Agency, data centers consumed approximately 200 terawatt hours of electricity globally,y with the United States accounting for a significant share due to its tech industry concentration. The number of data center facilities in the US is growing rapidly, requiring sophisticated cooling solutions to manage heat generated by high-density servers. Traditional air conditioning is often insufficient for modern data centers, leading to the adoption of advanced cooling technologies such as liquid cooling and precision air handling. The need for uninterrupted operation mandates redundant and highly reliable HVAC systems,s driving investment in premium equipment. Energy efficiency is critical in data centers to reduce operational costs and meet sustainability goals, ls prompting the use of innovative cooling strategies. The expansion of hyperscale data centers by major tech companies further amplifies demand. Regulatory pressures regarding energy consumption in commercial facilities also push for efficient cooling solutions.

COMPETITIVE LANDSCAPE

The competitive landscape of the United States HVAC market is characterized by intense rivalry among established global corporations and specialized regional manufacturers. Large players leverage extensive distribution networks and brand recognition to maintain dominance, while niche firms compete on customization and local service quality. The market is fragmented with numerous independent contractors influencing purchasing decisions through recommendations. Price competition is moderate in the premium segment,where value-oriented brandss compete aggressively on cost. Regulatory compliance drives innovation as companies strive to meet stringent efficiency standards. The rise of smart home technology has introduced new competitors from the tech sector, adding complexity to the landscape. Supply chain reliability has become a key differentiator following recent global disruptions. Companies must balance product innovation with operational efficiency to sustain profitability. Customer service and warranty support play crucial roles in building long-term loyalty. The transition to sustainable refrigerants requires significant investment, creating barriers for smaller entities.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. HVAC Market include

- Carrier Corporation

- Trane Technologies plc

- Daikin Industries Ltd.

- Johnson Controls International plc

- Lennox International Inc.

- Rheem Manufacturing Company

- Mitsubishi Electric Corporation

- LG Electronics Inc.

- Panasonic Corporation

- Bosch Thermotechnology (Robert Bosch GmbH)

- AAON Inc.

- Honeywell International Inc.

TOP LEADING PLAYERS IN THE MARKET

- Carrier Global Corporation is a pioneering leader in the U.S. HVAC market with a comprehensive portfolio of heating, cooling,g and ventilation solutions. The company leverages its extensive brand recognition to serve residential, commercial, industrial, and other sectors effectively. Carrier strengthens its market position by investing heavily in smart building technologies and digital connectivity platforms. The company recently expanded its production capacity of high-efficiency heat pumps to meet growing demand for electrification. Carrier focuses on sustainability by developing low global warming potential refrigerant systems. Its robust distribution network ensures widespread availability and service support. These strategic initiatives reinforce its reputation for innovation and reliability while addressing evolving regulatory standards and customer preferences for energy-efficient climate control solutions.

- Trane Technologies plc is a major player in the US HVAC industry known for its advanced commercial and residential climate control systems. The company provides integrated solutions that enhance energy efficiency and indoor air quality for diverse applications. Trane strengthens its market position through continuous research and development in thermal management technologies. The company recently launched new variable refrigerant flow systems designed for superior performance in extreme weather conditions. Trane focuses on digital services such as remote monitoring and predictive maintenance to improve customer experience. Its commitment to sustainability includes setting ambitious carbon reduction goals for operations and products. These efforts enable Trane to maintain a competitive edge and drive growth in the dynamic HVAC sector.

- Daikin Comfort Technologies North America Inc is a prominent manufacturer in the U.S. HVAC market specializing in innovative air conditioning and heating equipment. The company offers a wide range of products, including ductless mini splits and central air systems,s tailored for American homes. Daikin strengthens its market position by expanding its manufacturing facilities in Texas to increase local production capabilities. The company recently introduced inverter-driven systems that offer enhanced energy savings and quieter operation. Daikin focuses on customer education and dealer training to ensure proper installation and maintenance. Its emphasis on quality and durability builds strong brand loyalty among consumers. These actions demonstrate Daikin's commitment to providing reliable and efficient comfort solutions for the US market.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States HVAC market employ diverse strategies to maintain a competitive advantage and drive growth. Product innovation remains central with companies developing energy-efficient and environmentally friendly systems. Brands focus on digital transformation by integrating smart controls and IoT connectivity for enhanced user experience. Strategic acquisitions help expand product portfolios and enter new market segments effectively. Sustainability initiatives are increasingly important as consumers demand low-carbon solutions. Companies leverage data analytics to optimize supply chains and predict maintenance needs. Omnichannel distribution ensures seamless access to products for both professionals and consumers. Training programs for technicians build brand loyalty and ensure proper installation. Marketing campaigns emphasize reliability and cost savings to attract value-conscious buyers. These strategies collectively help brands differentiate themselves and capture value in a regulated market.

MARKET SEGMENTATION

This research report on the U.S. HVAC market is segmented and sub-segmented into the following categories.

By Implementation Type

- Retrofit Buildings

- New Construction

By Service Type

- Installation and Replacement Services

- Maintenance and Repair Services

By End User and Application Vertical

- Residential

- Data Centers

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States