U.S. Hydrogen Market Size, Share, Trends & Growth Forecast Report Segmented By Generation Type (Gray Hydrogen, Blue Hydrogen, Green Hydrogen),Application, Storage, Transportation and Country – Industry Analysis From 2026 to 2034

U.S. Hydrogen Market Report Summary

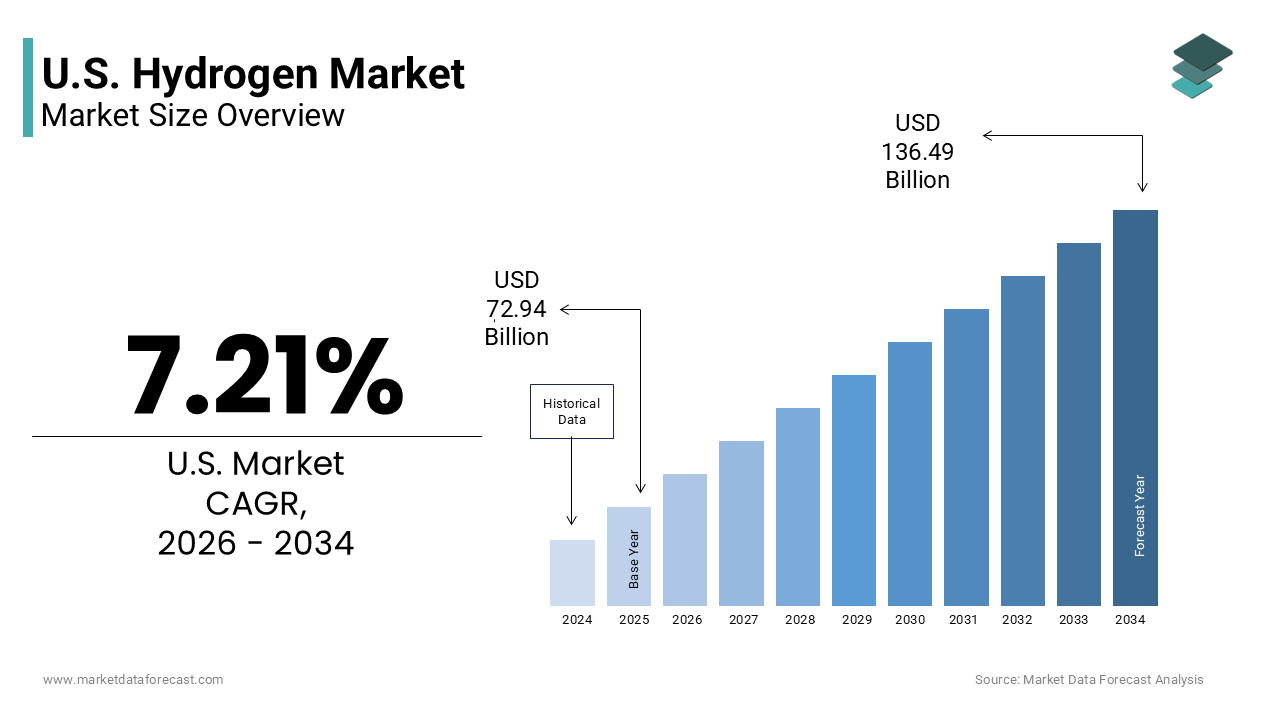

The U.S. hydrogen market was valued at USD 72.94 billion in 2025, is estimated to reach USD 78.20 billion in 2026, and is projected to reach USD 136.49 billion by 2034, growing at a CAGR of 7.21% during the forecast period from 2026 to 2034. The growth of the U.S. hydrogen market is driven by increasing federal incentives for clean hydrogen production, rising industrial decarbonization initiatives, and expanding investments in renewable energy infrastructure. Growing adoption of hydrogen across heavy industries, increasing development of hydrogen fuel cell transportation systems, and rising integration of carbon capture technologies are further accelerating market growth. Moreover, advancements in electrolyzer technologies, expansion of hydrogen refueling infrastructure, and increasing focus on grid-scale renewable energy storage are supporting the expansion of the U.S. hydrogen market.

Key Market Trends

- Rising adoption of green hydrogen projects supported by federal tax credits and renewable energy integration initiatives.

- Growing deployment of hydrogen fuel cell technologies in heavy-duty transportation and logistics applications.

- Increasing investments in carbon capture-enabled blue hydrogen production facilities across industrial hubs.

- Strong focus on hydrogen infrastructure development including pipelines, storage systems, and refueling corridors.

- Expansion of power-to-gas technologies utilizing excess renewable electricity for hydrogen generation and energy storage.

Segmental Insights

- Based on generation type, the gray hydrogen segment dominated the U.S. hydrogen market and held the largest share in 2025. The segment’s dominance is attributed to its established production infrastructure, abundant natural gas availability, cost-effectiveness, and extensive industrial utilization across ammonia production and petroleum refining sectors.

- The green hydrogen segment is projected to witness the fastest CAGR during the forecast period owing to increasing federal policy support under the Inflation Reduction Act, declining renewable energy costs, and growing corporate commitments toward carbon neutrality and clean energy adoption.

- Based on application, the chemical and refinery segment accounted for the leading share of the U.S. hydrogen market in 2025. The dominance of this segment is driven by extensive hydrogen utilization in ammonia synthesis, hydrocracking, desulfurization processes, and other industrial chemical manufacturing applications.

- The mobility segment is anticipated to register notable growth during the forecast period due to increasing deployment of hydrogen fuel cell trucks and buses, expansion of hydrogen refueling stations, and rising demand for zero-emission heavy-duty transportation solutions.

Regional Insights

The United States maintained a strong position in the global hydrogen market in 2025, supported by extensive industrial infrastructure, strong government policy support, and increasing investments in clean energy technologies. California remains a major contributor to the U.S. hydrogen market due to its aggressive zero-emission vehicle mandates, extensive hydrogen refueling infrastructure, and large-scale renewable energy projects. Texas and Gulf Coast regions continue to play a prominent role owing to their established hydrogen production infrastructure, strong petrochemical industries, and expanding blue hydrogen projects with carbon capture technologies. Washington, Oregon, and New York are also witnessing notable growth driven by increasing renewable energy integration, clean transportation initiatives, and hydrogen infrastructure investments.

Competitive Landscape

The U.S. hydrogen market is highly competitive and characterized by the presence of industrial gas companies, energy corporations, clean technology developers, and hydrogen infrastructure providers competing through technological innovation, strategic partnerships, and infrastructure expansion initiatives. Leading companies are focusing on expanding green hydrogen production capacities, strengthening electrolyzer manufacturing capabilities, investing in hydrogen mobility solutions, and integrating carbon capture technologies into existing hydrogen production systems. Strategic collaborations with industrial customers, renewable energy providers, and transportation companies are further strengthening market positioning across the emerging U.S. hydrogen economy. Prominent players in the U.S. hydrogen market include Air Liquide, Linde plc, Air Products and Chemicals, Inc., Plug Power Inc., Bloom Energy Corporation, Cummins Inc., Ballard Power Systems, Chevron Corporation, Exxon Mobil Corporation, Shell plc, FuelCell Energy, Inc., and Nel ASA.

U.S. Hydrogen Market Size

The U.S. hydrogen market size was valued at USD 72.94 billion in 2025 and is anticipated to reach USD 78.20 billion in 2026 from USD 136.49 billion by 2034, growing at a CAGR of 7.21% during the forecast period from 2026 to 2034.

The U.S. hydrogen market is likely to witness progressive expansion over the next few years, transforming into a cornerstone of the national clean energy transition. This versatile element serves as a critical decarbonization tool for hard to abate sectors such as heavy industry, long haul transportation, and power generation. The market is currently dominated by gray hydrogen produced from natural gas via steam methane reforming but is rapidly shifting toward low carbon blue and green hydrogen derived from renewable electrolysis and carbon capture technologies. As per the U.S. Department of Energy, the U.S. currently produces approximately 10 million metric tons of hydrogen annually, primarily for industrial applications like ammonia production and petroleum refining. The geographic concentration of production facilities is aligned with existing industrial clusters in the Gulf Coast and Midwest regions, where infrastructure and feedstock availability are optimal. According to the Energy Information Administration, the industrial sector accounts for nearly 95% of current hydrogen consumption, highlighting the deep integration of this fuel into manufacturing processes. The Inflation Reduction Act has introduced significant tax credits for clean hydrogen production, accelerating investment in electrolyzer manufacturing and project development. Regulatory frameworks are evolving to define standards for clean hydrogen certification, ensuring environmental integrity. The interplay between federal incentives, technological advancements, and corporate sustainability goals defines the current trajectory of the hydrogen industry in the U.S.

MARKET DRIVERS

Federal Tax Credits under the Inflation Reduction Act Stimulate Investment

The implementation of the Section 45V Clean Hydrogen Production Tax Credit under the Inflation Reduction Act is primarily driving the expansion of the U.S. hydrogen market by providing substantial financial incentives for low carbon hydrogen production. This legislation offers up to 3 dollars per kilogram for hydrogen produced with near zero greenhouse gas emissions, making green and blue hydrogen economically competitive with fossil fuel based alternatives. As per the U.S. Department of the Treasury, this tax credit structure is designed to scale domestic clean hydrogen production to 10 million metric tons by 2030 and 20 million metric tons by 2040. The tiered credit system rewards producers who achieve lower carbon intensity scores, encouraging the adoption of renewable energy sources and carbon capture technologies. This regulatory certainty has triggered a wave of announced projects and final investment decisions across multiple states. Companies are accelerating plans for electrolyzer facilities and retrofitting existing steam methane reformers with carbon capture systems to qualify for these benefits. The credit also stimulates demand for ancillary services such as renewable energy procurement and engineering construction. By reducing the levelized cost of clean hydrogen, the policy effectively bridges the price gap with conventional fuels. This financial support mechanism ensures that hydrogen remains a viable component of the national decarbonization strategy. The long term visibility of these incentives allows for robust planning and capital allocation in the emerging hydrogen economy.

Industrial Decarbonization Mandates Drive Demand in Heavy Sectors

Stringent environmental regulations and corporate net zero commitments are driving significant demand for clean hydrogen in heavy industrial sectors such as steel, cement, and chemical manufacturing, which is further boosting the U.S. market expansion. These industries face immense pressure to reduce scope 1 and scope 2 emissions as traditional fossil fuel processes become increasingly unsustainable under new climate policies. As per the Environmental Protection Agency, the industrial sector contributes approximately 23% of total U.S. greenhouse gas emissions, which is requiring a shift toward low carbon feedstocks and fuels. Hydrogen serves as a direct replacement for coal in steel production through direct reduced iron methods, and it replaces natural gas in high temperature heating applications. Major steelmakers and chemical producers have announced pilot projects and commercial scale initiatives to integrate hydrogen into their operations. The American Iron and Steel Institute highlights that hydrogen based steelmaking could reduce industry emissions by up to 90% compared to traditional blast furnace methods. Refineries are also increasing hydrogen usage for hydrocracking and desulfurization processes to meet cleaner fuel standards. The availability of clean hydrogen allows these sectors to maintain productivity while complying with evolving environmental standards. Government grants and loan programs further support the deployment of hydrogen technologies in industrial settings. This regulatory and operational imperative ensures that industrial applications remain a cornerstone of hydrogen demand growth in the U.S.

MARKET RESTRAINTS

High Production Costs Limit Commercial Viability

The elevated cost of producing clean hydrogen, particularly green hydrogen via electrolysis, constitutes a significant restraint for the U.S. market despite recent policy incentives. While the Levelized Cost of Hydrogen for gray hydrogen remains low due to abundant natural gas resources, green hydrogen costs are still substantially higher due to electricity prices and capital expenditures for electrolyzers. As per the National Renewable Energy Laboratory, the cost of green hydrogen ranges from 4 to 6 dollars per kilogram depending on renewable energy availability and electrolyzer efficiency, compared to 1 to 2 dollars per kilogram for gray hydrogen. This price disparity makes it challenging for clean hydrogen to compete in price sensitive markets without sustained subsidies. The volatility of renewable energy prices and the intermittent nature of solar and wind power further complicate cost stability for electrolysis operations. High upfront capital costs for electrolyzer installations and balance of plant infrastructure require significant financing, which can be prohibitive for smaller developers. The lack of economies of scale in domestic electrolyzer manufacturing keeps equipment prices elevated compared to international competitors. Until production costs decrease through technological advancements and scaled manufacturing, clean hydrogen will struggle to achieve widespread adoption in non-subsidized sectors. This economic barrier restricts the market potential to early adopters and government supported projects. Consequently, cost competitiveness remains a critical hurdle for the broader commercialization of the hydrogen economy.

Insufficient Infrastructure Hinders Distribution and Storage

The lack of dedicated infrastructure for hydrogen transportation, storage and refueling poses a major restraint to the expansion of the U.S. hydrogen market. Unlike natural gas or electricity, hydrogen requires specialized pipelines, tanks, and dispensing stations due to its low volumetric energy density and high flammability. As per the Pipeline and Hazardous Materials Safety Administration, the U.S. has approximately 1600 miles of dedicated hydrogen pipelines mostly concentrated in industrial clusters along the Gulf Coast, leaving vast regions without access. The absence of a nationwide pipeline network forces reliance on truck transport, which is inefficient and costly for large volumes. Storage challenges are exacerbated by the need for high pressure compression or cryogenic liquefaction, both of which consume significant energy and increase operational costs. Retail refueling stations for fuel cell electric vehicles are sparse, limiting consumer adoption and fleet expansion. The permitting process for new hydrogen infrastructure is complex and time consuming, involving multiple regulatory agencies and safety standards. The chicken and egg dilemma between supply and demand discourages private investment in infrastructure without guaranteed off take agreements. This infrastructural deficit creates logistical bottlenecks that hinder the seamless integration of hydrogen into the national energy system. Overcoming these barriers requires coordinated public private investment and standardized regulatory frameworks.

MARKET OPPORTUNITIES

Expansion of Heavy Duty Transportation Fleet Applications

The deployment of hydrogen fuel cell technology in heavy duty transportation presents a significant opportunity for the U.S. market, as battery electric solutions face limitations in range and charging time for long haul applications. Hydrogen fuel cell electric vehicles offer rapid refueling and extended range, making them ideal for trucks, buses, and rail locomotives that operate on fixed routes or require high uptime. As per the California Air Resources Board, the state has mandated that all new drayage trucks be zero emission by 2035, creating a substantial market for hydrogen powered freight vehicles. Several major logistics companies have initiated pilot programs using hydrogen fuel cell trucks to evaluate performance and operational efficiency. The federal government is investing in hydrogen refueling corridors along major interstate highways to support long distance transport. The Port of Los Angeles and other key logistics hubs are exploring hydrogen solutions for cargo handling equipment and terminal trucks. These initiatives demonstrate the practical viability of hydrogen in demanding transportation sectors. The growing emphasis on supply chain decarbonization encourages shippers and carriers to adopt clean fuel alternatives. Technological improvements in fuel cell durability and efficiency are reducing total cost of ownership, making hydrogen trucks more competitive. This shift toward heavy duty applications opens a lucrative segment for hydrogen producers and infrastructure developers.

Integration with Renewable Energy for Grid Stability

The integration of hydrogen production with renewable energy systems offers a promising opportunity for grid stability and energy storage in the U.S. Electrolyzers can utilize excess electricity generated during periods of high solar or wind output to produce hydrogen, effectively storing surplus energy for later use. As per the Federal Energy Regulatory Commission, the increasing penetration of variable renewable energy sources creates a need for flexible load resources that can balance supply and demand. Hydrogen production facilities can act as dispatchable loads, absorbing excess power and preventing curtailment of renewable assets. The stored hydrogen can then be converted back to electricity via fuel cells or turbines during peak demand periods, or used as a feedstock for industrial processes. This power to gas model enhances the reliability of the electrical grid and maximizes the utilization of renewable infrastructure. Utilities and independent power producers are exploring hybrid projects that combine solar or wind farms with onsite electrolysis. The ability to monetize excess renewable energy through hydrogen production improves the economics of renewable projects. Government incentives for energy storage and clean fuels further support this integration. This synergy between hydrogen and renewables positions the technology as a key enabler of a resilient and decarbonized energy system.

MARKET CHALLENGES

Regulatory Uncertainty Regarding Clean Hydrogen Definitions

Ambiguity surrounding the definition and certification of clean hydrogen creates significant challenges for investors and producers in the U.S. market. The criteria for determining carbon intensity thresholds and eligible energy sources for the Section 45V tax credit have been subject to intense debate and regulatory delays. As per the Internal Revenue Service, proposed guidelines on additive attribution and hourly matching requirements for renewable energy have raised concerns about project feasibility and compliance costs. Industry stakeholders argue that strict hourly matching rules could limit the availability of qualified renewable energy and increase production costs unnecessarily. The lack of final clarity hinders final investment decisions, as companies hesitate to commit capital without knowing if their projects will qualify for full tax benefits. Inconsistent state level regulations further complicate the landscape, creating a fragmented market environment. The uncertainty affects supply chain planning and contract negotiations with off takers who require guaranteed clean credentials. Delays in regulatory finalization slow down project timelines and increase development risks. The need for a clear and pragmatic framework is essential to unlock the full potential of the hydrogen economy. Without resolved definitions, the market faces stagnation and reduced investor confidence. This regulatory limbo remains a persistent obstacle to rapid market expansion.

Competition from Established Fossil Fuel Alternatives

Intense competition from established fossil fuel alternatives poses a major challenge to the widespread adoption of hydrogen in the U.S. energy market. Natural gas remains abundant and inexpensive in the U.S., providing a cost effective solution for heating, power generation, and industrial processes. As per the U.S. Energy Information Administration, natural gas prices have remained relatively low due to shale production enhancements, making it difficult for hydrogen to compete on price alone. Existing infrastructure for natural gas is extensive and well understood, reducing switching costs for end users. Many industrial facilities are reluctant to retrofit equipment for hydrogen use due to high capital expenditures and operational disruptions. The maturity of battery electric vehicle technology in the light duty sector also competes with hydrogen for transportation market share. Consumers and businesses often prefer proven technologies with lower upfront costs and established supply chains. The entrenched position of fossil fuels creates high barriers to entry for hydrogen in mainstream applications. Overcoming this competition requires not only cost reductions but also demonstrable performance advantages and regulatory mandates that favor low carbon options. The dominance of incumbent energy sources slows the transition to hydrogen and limits its market penetration. This competitive landscape necessitates strategic differentiation and targeted policy support for hydrogen technologies.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.21% |

| Segments Covered | By Generation Type ,Application, Storage, Transportation and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Air Liquide, Linde plc, Air Products and Chemicals, Inc., Plug Power Inc., Bloom Energy Corporation, Cummins Inc., Ballard Power Systems, Chevron Corporation, Exxon Mobil Corporation, Shell plc, FuelCell Energy, Inc., and Nel ASA. |

SEGMENTAL ANALYSIS

By Generation Type Insights

The gray hydrogen segment captured the highest share of the U.S. market in 2025. The growth of the gray hydrogen segment in the U.S. market can be credited to its established production infrastructure and lower cost compared to low carbon alternatives. This type of hydrogen is produced primarily through steam methane reforming using natural gas, which is abundant and inexpensive in the U.S. As per the U.S. Energy Information Administration, natural gas prices have remained historically low due to shale gas production, making gray hydrogen the most economically viable option for industrial applications. The existing network of steam methane reformers across the Gulf Coast and Midwest regions provides a reliable supply chain that meets current industrial demand without requiring significant capital investment in new technologies. Industries such as ammonia production and petroleum refining rely on gray hydrogen because of its consistent quality and availability. The maturity of this technology ensures high operational efficiency and minimal downtime, which is critical for continuous industrial processes. Regulatory frameworks have historically favored conventional production methods, allowing gray hydrogen to dominate the market share. The lack of carbon pricing mechanisms in many jurisdictions further enhances the cost competitiveness of gray hydrogen. These factors collectively maintain gray hydrogen as the cornerstone of the U.S. hydrogen industry despite growing environmental concerns.

However the green hydrogen segment is estimated to showcase a promising CAGR in the U.S. market during the forecast period owing to the federal incentives under the Inflation Reduction Act and the increasing availability of renewable energy sources. The Section 45V tax credit provides up to 3 dollars per kilogram for hydrogen produced with near zero emissions, making green hydrogen economically competitive. As per the Department of Energy, the cost of renewable electricity from solar and wind has decreased significantly, enabling cheaper electrolysis operations. Several states with abundant renewable resources, such as Texas and California, are launching large scale green hydrogen projects to leverage these incentives. The commitment of major corporations to net zero emissions is driving demand for clean hydrogen in hard to abate sectors. Technological advancements in electrolyzer efficiency are reducing capital costs and improving production rates. Government grants and loan guarantees further support the development of green hydrogen facilities. The alignment of policy support with technological progress positions green green hydrogen for rapid expansion. These factors collectively establish green hydrogen as the fastest growing segment in the U.S. market.

By Application Insights

The chemical and refinery segment dominated the market by capturing the leading share of the U.S. market in 2025. The growth of the chemical and refinery segment in the U.S. market is attributed to the extensive use of hydrogen in ammonia production and petroleum refining processes. Ammonia is a key ingredient in fertilizers and industrial chemicals, requiring large volumes of hydrogen for synthesis. As per the U.S. Geological Survey, the U.S. produces millions of tons of ammonia annually, relying heavily on hydrogen as a primary feedstock. Petroleum refineries utilize hydrogen for hydrocracking and desulfurization to produce cleaner fuels that meet environmental standards. The mandatory reduction of sulfur content in gasoline and diesel fuels has increased hydrogen demand in the refining sector. The established infrastructure for hydrogen distribution within industrial clusters ensures reliable supply for these critical applications. The integration of hydrogen into chemical synthesis processes is well understood and optimized for efficiency. Regulatory requirements for cleaner fuels further reinforce the demand for hydrogen in refineries. These factors collectively establish the chemical and refinery sector as the dominant application for hydrogen in the U.S.

On the other side, the mobility segment is experiencing the fastest growth in hydrogen application and is predicted to register a healthy CAGR in the U.S. market during the forecast period owing to the adoption of fuel cell electric vehicles in heavy duty transportation. Hydrogen fuel cells offer superior range and refueling speed compared to battery electric vehicles, making them ideal for trucks, buses, and logistics fleets. As per the California Air Resources Board, the state has mandated zero emission standards for drayage trucks, creating a substantial market for hydrogen powered vehicles. Several major logistics companies are piloting hydrogen fuel cell trucks to evaluate performance and operational efficiency. Federal investments in hydrogen refueling corridors along interstate highways support long distance transport. The Port of Los Angeles and other key hubs are exploring hydrogen solutions for cargo handling equipment. These initiatives demonstrate the viability of hydrogen in demanding transportation sectors. The growing emphasis on supply chain decarbonization encourages carriers to adopt clean fuel alternatives. These factors position mobility as the fastest growing application segment for hydrogen in the US.

COMPETITIVE LANDSCAPE

The competitive landscape of the U.S. hydrogen market is characterized by intense rivalry among established industrial gas companies technology innovators and energy giants who strive to dominate the emerging clean fuel sector. Major competitors differentiate themselves through technological expertise production scale and strategic alliances rather than price alone due to the nascent stage of the market. The shift toward low carbon hydrogen has intensified competition for federal tax credits and government grants which are critical for project viability. Firms are increasingly investing in research and development to improve electrolyzer efficiency and reduce capital costs. Regulatory frameworks such as the Inflation Reduction Act shape competitive dynamics by rewarding producers with lower carbon intensity scores. Supply chain resilience has become a critical differentiator as companies secure access to renewable energy and specialized components. Collaborative efforts between producers and end users are becoming more common to drive innovation and secure long term contracts. This dynamic environment requires continuous adaptation and strategic investment to maintain relevance and profitability in a rapidly evolving energy market structure driven by sustainability mandates.

KEY MARKET PLAYERS

Some of the promising companies that are playing a dominating role in the U.S. hydrogen market include

- Air Liquide

- Linde plc

- Air Products and Chemicals, Inc.

- Plug Power Inc.

- Bloom Energy Corporation

- Cummins Inc.

- Ballard Power Systems

- Chevron Corporation

- Exxon Mobil Corporation

- Shell plc

- FuelCell Energy, Inc.

- Nel ASA

Top Market Players

Air Products and Chemicals Inc

Air Products and Chemicals Inc is a global leader in industrial gases with a significant footprint in the U.S. hydrogen market. The company operates extensive steam methane reforming facilities and is actively developing large scale blue and green hydrogen projects. Recent actions include advancing the Port Arthur Blue Hydrogen project in Texas which aims to capture millions of tons of carbon dioxide annually. Air Products leverages its expertise in gas separation and liquefaction to optimize hydrogen distribution and storage. The company collaborates with energy firms to secure renewable power for electrolysis initiatives. Strategic investments in infrastructure enhance supply reliability for industrial customers. By integrating carbon capture technologies Air Products strengthens its position as a provider of low carbon hydrogen solutions. These efforts align with national decarbonization goals while maintaining operational excellence and customer satisfaction across diverse industrial sectors.

Plug Power Inc

Plug Power Inc specializes in building an end to end green hydrogen ecosystem focusing on production storage and delivery for mobility and stationary applications. The company operates a network of hydrogen fueling stations primarily serving material handling equipment such as forklifts in warehouses. Recent actions include the construction of multiple green hydrogen production plants across the U.S. to support its growing customer base. Plug Power integrates electrolyzer manufacturing with renewable energy procurement to ensure sustainable fuel sources. The company partners with logistics providers to expand the adoption of fuel cell electric vehicles. Strategic acquisitions enhance its technological capabilities in liquid hydrogen handling and dispensing. By offering comprehensive solutions Plug Power strengthens its market presence. These initiatives drive the transition to clean energy in the transportation and industrial sectors while supporting corporate sustainability objectives.

Cummins Inc

Cummins Inc is a major player in the U.S. hydrogen market through its Accelera by Cummins brand which focuses on zero emission power technologies. The company designs and manufactures proton exchange membrane and alkaline electrolyzers for green hydrogen production. Recent actions include the expansion of its electrolyzer manufacturing facility in Minnesota to meet increasing domestic demand. Cummins integrates hydrogen fuel cells into its power generation and transportation portfolios offering versatile energy solutions. The company collaborates with original equipment manufacturers to deploy fuel cell systems in heavy duty trucks and buses. Strategic investments in research and development improve the efficiency and durability of hydrogen technologies. By leveraging its global engineering expertise Cummins strengthens its competitive position. These efforts support the widespread adoption of hydrogen as a clean energy carrier across various industrial and commercial applications.

Top Strategies Used by Key Market Participants

Key players in the U.S. hydrogen market primarily employ strategies focused on vertical integration and strategic partnerships to secure supply chains and accelerate deployment. Companies are investing heavily in electrolyzer manufacturing and renewable energy assets to produce cost competitive green hydrogen. Collaborations with industrial off takers ensure long term demand stability for clean fuel projects. Diversification into blue hydrogen with carbon capture allows firms to leverage existing natural gas infrastructure while reducing emissions. Expansion of refueling networks supports the adoption of fuel cell vehicles in transportation sectors. Lobbying efforts aim to shape favorable regulatory frameworks and secure government funding. These strategic moves collectively strengthen market positions by addressing technical economic and policy challenges inherent in the emerging hydrogen economy landscape today.

MARKET SEGMENTATION

This research report on the U.S. hydrogen market has been segmented based on the following categories.

By Generation Type

- Gray Hydrogen

- Blue Hydrogen

- Green Hydrogen

By Application

- Energy

- Power Generation

- CHP

- Mobility

- Chemical & Refinery

- Petroleum Refinery

- Ammonia Production

- Methanol Production

By Storage

- Physical

- Material-based

By Transportation

- Long Distance

- Short Distance

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com