U.S Insurance Brokerage Market Size, Share, Trends & Growth Forecast Report - Segmented By Pollutant, End-User, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Insurance Brokerage Market Report Summary

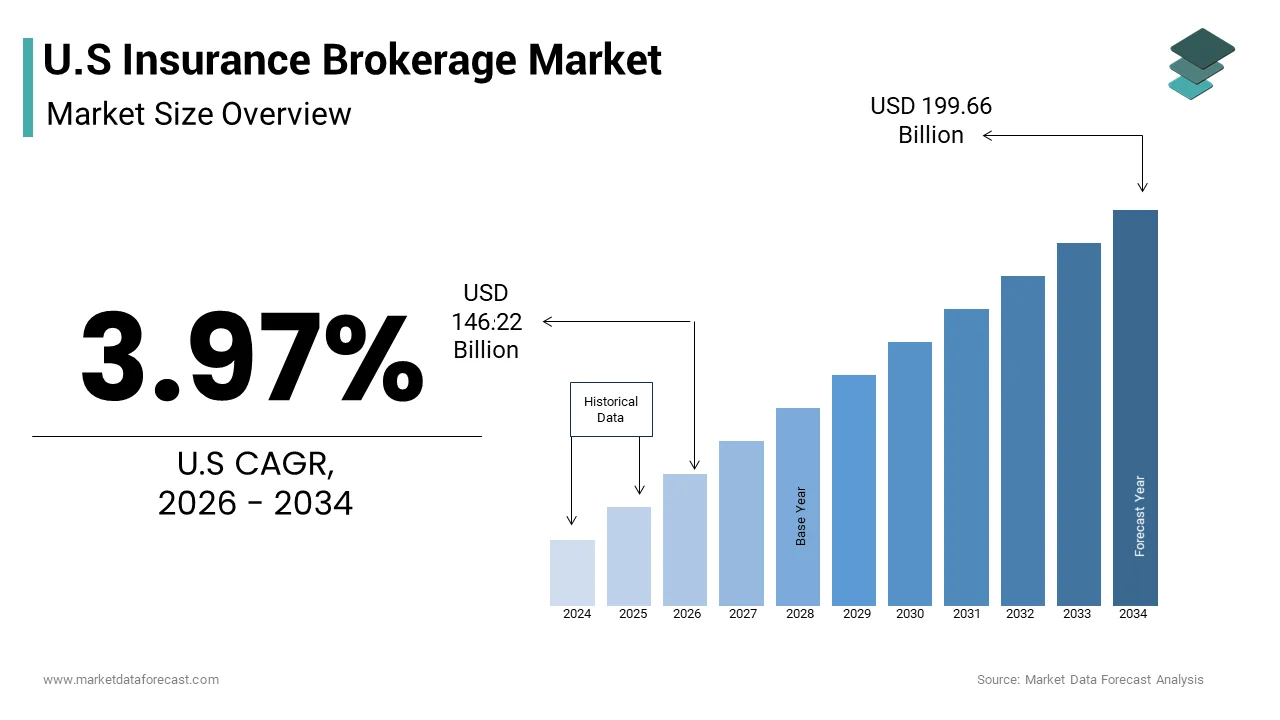

The U.S. insurance brokerage market was valued at USD 140.64 billion in 2025 and is anticipated to reach USD 146.22 billion in 2026 and USD 199.66 billion by 2034, growing at a CAGR of 3.97% during the forecast period. The growth of the market is driven by increasing demand for customized insurance solutions, rising business risk exposure, and the growing complexity of insurance products across commercial and personal lines. The expansion of digital brokerage platforms, increasing regulatory compliance requirements, and the need for professional risk management and advisory services are further supporting market growth across the United States.

Key Market Trends

- Growing adoption of digital insurance brokerage platforms to streamline policy comparison, management, and customer engagement.

- Increasing demand for specialized risk advisory services driven by evolving cybersecurity, climate, and liability risks.

- Rising merger and acquisition activity among brokerage firms to expand geographic reach and service portfolios.

- Greater use of data analytics, artificial intelligence, and automation to improve underwriting support and customer experience.

- Expanding focus on small and medium-sized enterprises seeking tailored insurance coverage and risk management solutions.

SEGMENTAL INSIGHTS

Based on brokerage type, the retail brokerage segment accounted for the largest share of the U.S. insurance brokerage market in 2025. The segment’s dominance is attributed to its direct engagement with businesses and individual clients, offering personalized insurance solutions, policy management services, and risk assessment expertise across a wide range of insurance products.

Based on client type, the small and medium-sized enterprises (SMEs) segment held the leading share of the market in 2025. The growth of this segment is driven by increasing awareness of business risks, growing regulatory requirements, and rising demand for cost-effective insurance coverage tailored to the needs of expanding enterprises.

REGIONAL INSIGHTS

The United States continues to strengthen its position as the largest insurance brokerage market in North America, supported by its highly developed financial services sector and strong insurance penetration rates. Market growth is fueled by increasing demand for commercial insurance, a sophisticated risk management ecosystem, and ongoing investments in digital insurance technologies. The presence of a large number of businesses, evolving regulatory frameworks, and growing demand for specialized insurance products further contribute to the market’s expansion across the country.

COMPETITIVE LANDSCAPE

The U.S. insurance brokerage market is highly competitive and characterized by the presence of global brokerage leaders and rapidly expanding regional firms. Market participants are focusing on strategic acquisitions, digital transformation initiatives, enhanced customer service capabilities, and specialized consulting offerings to strengthen their competitive position. The growing emphasis on data-driven risk assessment, industry-specific insurance solutions, and integrated advisory services continues to shape the competitive landscape. Key players operating in the market include Marsh McLennan, Aon plc, Willis Towers Watson (WTW), Arthur J. Gallagher & Co., Brown & Brown Inc., HUB International, Lockton Companies, USI Insurance Services, Truist Insurance Holdings, Acrisure, Alliant Insurance Services, Hilb Group, Ryan Specialty Group, NFP Corp., BXS Insurance, PCF Insurance Services, AssuredPartners, Amwins Group, INSURICA, and Risk Strategies Company.

U.S Insurance Brokerage Market Size

The U.S insurance brokerage market size was valued at USD 140.64 billion in 2025 and is anticipated to reach USD 146.22 billion in 2026 to reach USD 199.66 billion by 2034, growing at a CAGR of 3.97% during the forecast period from 2026 to 2034.

MARKET OVERVIEW

As per the National Association of Insurance Commissioners, the total net premiums written in the U.S. reached approximately 1.4 trillion USD in recent years, which indicates the massive scale of risk exposure that brokers help manage. According to the Bureau of Labor Statistics, employment for insurance sales agents including brokers is projected to grow by 6% from 2022 to 2032, which is faster than the average for all occupations. This growth trajectory reflects the enduring necessity for human expertise in navigating intricate policy terms and conditions. Furthermore, according to the Federal Reserve, household debt in the U.S. stood at 17.5 trillion USD in the fourth quarter of 2023, which drives the need for protective financial instruments. The intricate nature of modern liabilities such as cyber threats and supply chain disruptions necessitates professional guidance to ensure adequate coverage. Brokers serve as essential advisors who translate technical insurance language into actionable business strategies for clients across various industries.

MARKET DRIVERS

Increasing Complexity of Commercial Risks Drives Demand for Specialized Brokerage Services

The rising complexity of commercial risks is a major factor fuelling the expansion of the U.S. insurance brokerage market as businesses face multifaceted threats that standard policies cannot adequately address. Modern enterprises operate in an environment characterized by interconnected supply chains, digital dependencies, and evolving regulatory landscapes, which create unique vulnerabilities requiring bespoke insurance solutions. According to the Cybersecurity and Infrastructure Security Agency, ransomware attacks in the U.S. increased by 18% in 2023 compared to the previous year, which has intensified the demand for specialized cyber liability coverage. Corporate clients increasingly rely on brokers to navigate these intricate risk profiles because traditional underwriting models often fail to capture the nuances of emerging threats such as intellectual property theft or business interruption due to geopolitical instability. According to the National Association of Manufacturers, small and medium sized manufacturers face an average of 200 cyberattacks per day, which necessitates expert guidance in securing appropriate coverage. Additionally, according to the Occupational Safety and Health Administration, there were 5,903 fatal work injuries in private industry in 2022, which highlights the persistent need for comprehensive workers compensation and liability insurance. Brokers provide value by conducting thorough risk assessments and negotiating terms that align with specific operational realities. This specialized advisory role becomes indispensable as companies seek to protect their assets against non-traditional risks that are difficult to quantify and insure through automated platforms. The depth of knowledge required to structure these complex programs ensures that businesses continue to prioritize professional brokerage services over direct purchasing channels.

Rising Regulatory Compliance Requirements Necessitate Expert Intermediary Guidance

The tightening regulatory framework governing various industries in the U.S. significantly propels the demand for insurance brokerage services as organizations struggle to maintain compliance with evolving legal standards, which is further boosting the U.S. market expansion. Regulatory bodies frequently update mandates related to environmental protection, healthcare, data privacy, and corporate governance, which directly impact insurance requirements and liability exposures. As per the Department of Health and Human Services, there were 725 reported healthcare data breaches affecting 500 or more individuals in 2023, which has led to stricter enforcement of privacy laws and higher penalties for non compliance. Companies must secure specialized liability coverage to protect against potential lawsuits and regulatory fines, which requires the expertise of brokers who understand the intersection of law and insurance. The Environmental Protection Agency finalized new methane emission standards in late 2023, which imposes additional compliance burdens on energy and manufacturing sectors, thereby increasing their need for environmental impairment liability insurance. Brokers assist clients in interpreting these regulations and identifying coverage gaps that could result in significant financial penalties. Furthermore, according to the Securities and Exchange Commission, new climate related disclosure rules introduced in 2024 compel public companies to assess and report on climate risks, driving demand for directors and officers liability insurance. The intricate nature of these compliance obligations means that internal risk managers often lack the specialized knowledge required to secure optimal coverage. Insurance brokers bridge this gap by providing insights into regulatory trends and helping organizations structure policies that meet legal requirements while minimizing costs. This dynamic ensures a steady demand for professional brokerage services as regulatory scrutiny continues to intensify across multiple sectors.

MARKET RESTRAINTS

Talent Shortage and Retention Issues Constrain Operational Scalability

The U.S. insurance brokerage market faces significant constraints due to a persistent shortage of skilled professionals, which hampers the ability of firms to scale operations and meet growing client demands. The industry struggles to attract younger demographics who often perceive insurance as a traditional and less dynamic career path compared to technology or finance sectors. According to the Bureau of Labor Statistics, the median age of insurance sales agents is 47.5 years, which indicates an aging workforce that is nearing retirement without sufficient replacement from younger generations. This demographic imbalance creates a knowledge gap as experienced brokers retire, taking with them valuable client relationships and institutional expertise. According to the Independent Insurance Agents and Brokers of America, 40% of insurance agencies faced difficulties in hiring qualified staff in 2023, which limits their capacity to onboard new clients and expand service offerings. The complexity of modern insurance products requires extensive training and certification, which can take several years to complete, thereby slowing the pipeline of new talent. Additionally, high turnover rates in entry level positions exacerbate the problem as firms invest resources in training employees who may leave for other industries. According to the Society for Human Resource Management, the average cost to hire an employee is 4,129 USD, which adds financial pressure on brokerage firms struggling to fill vacancies. This talent crunch forces companies to limit their growth ambitions or rely on overtime from existing staff, which can lead to burnout and reduced service quality. Without a robust strategy to attract and retain talent, the market faces structural limitations that impede its ability to fully capitalize on emerging opportunities.

Cybersecurity Vulnerabilities Threaten Client Data Integrity and Trust

Cybersecurity vulnerabilities are further hampering the expansion of the U.S. insurance brokerage market, which is making them attractive targets for malicious actors. Insurance brokers collect and store confidential information including financial records, health details, and proprietary business strategies, which, if compromised, can lead to severe reputational damage and legal liabilities. As per the Identity Theft Resource Center, the number of data compromises in the U.S. reached 3,205 in 2023, affecting over 353 million individuals, which highlights the pervasive nature of cyber threats. A single breach can erode client trust and result in the loss of long term relationships, which are the foundation of the brokerage business model. According to the Federal Trade Commission, fines totaling over 1.2 billion USD were imposed for data privacy violations in 2023, which demonstrates the severe financial consequences of inadequate security measures. Brokerage firms often operate with limited IT budgets compared to larger technology companies, making it challenging to implement state of the art security protocols. Additionally, the rise of remote work has expanded the attack surface as employees access sensitive systems from various locations and devices. According to the Verizon Data Breach Investigations Report, 74% of all breaches involved the human element including errors and social engineering, which underscores the difficulty in maintaining strict security hygiene. Clients are increasingly demanding assurances regarding data protection before engaging with brokers, which adds operational complexity and cost. Failure to demonstrate robust cybersecurity measures can result in lost business opportunities and increased insurance premiums for the brokers themselves. This constant threat landscape requires continuous investment in security infrastructure, which strains resources and diverts attention from core business activities.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence Enhances Underwriting Efficiency and Personalization

The integration of artificial intelligence presents a significant opportunity for the U.S. insurance brokerage market by enabling more efficient underwriting processes and highly personalized customer experiences. Advanced algorithms can analyze vast datasets to identify risk patterns and predict potential losses with greater accuracy than traditional methods, allowing brokers to offer more competitive and tailored policies. According to the McKinsey Global Institute, artificial intelligence could deliver up to 1.2 trillion USD in annual value for the global insurance industry through improved efficiency and risk assessment. Brokers who adopt these technologies can process applications faster, reduce manual errors, and provide real time quotes, which enhances client satisfaction and retention. According to the National Association of Insurance Commissioners, 60% of insurers are already using some form of AI for fraud detection, which helps brokers mitigate risks and lower costs for their clients. Furthermore, AI driven chatbots and virtual assistants can handle routine inquiries, freeing up human brokers to focus on complex advisory roles and strategic planning. This technological shift allows firms to scale their operations without proportionally increasing headcount, thereby improving profit margins. Additionally, predictive analytics can help brokers identify cross selling opportunities by analyzing client behavior and life events, which leads to higher revenue per customer. The ability to offer dynamic pricing based on real time data such as telematics in auto insurance or IoT sensors in commercial property insurance creates new value propositions for clients. Embracing AI enables brokers to transition from transactional intermediaries to strategic partners who provide proactive risk management advice. This transformation not only differentiates firms in a crowded market but also aligns with the expectations of digitally savvy customers who demand speed and precision in their interactions.

Expansion Into Underserved Niche Markets Drives Revenue Diversification

Expanding into underserved niche markets is another lucrative opportunity for the U.S. insurance brokerage market as mainstream segments become increasingly saturated and competitive. Specialized sectors such as cannabis, renewable energy, and gig economy platforms present unique risk profiles that require tailored insurance solutions, which generalist brokers often overlook. As per the National Cannabis Industry Association, the legal cannabis market in the U.S. is projected to reach 40 billion USD by 2025, creating a substantial demand for specialized liability and property coverage that few carriers currently offer. Brokers who develop expertise in these emerging industries can command higher fees and build loyal client bases due to the scarcity of knowledgeable providers. Similarly, according to the Bureau of Labor Statistics, the number of gig workers in the U.S. has grown to 59 million individuals, representing 36% of the workforce, which creates a need for portable benefits and flexible insurance products. Traditional policies are often ill suited for these non traditional employment arrangements, leaving a gap that innovative brokers can fill. Additionally, the renewable energy sector is expanding rapidly, with the Department of Energy stating that solar power capacity in the U.S. increased by 20% in 2023, which drives demand for construction and operational risk coverage. By focusing on these niches, brokers can differentiate themselves from competitors and reduce reliance on volatile mainstream markets. This strategy also allows firms to build deep industry knowledge that creates barriers to entry for rivals. Diversifying into these high growth areas ensures long term sustainability and opens new revenue streams that are less susceptible to economic cycles affecting traditional industries.

MARKET CHALLENGES

Data Privacy Regulations Impose Complex Compliance Burdens

Navigating the complex landscape of data privacy regulations is a major challenge for the U.S. insurance brokerage market as firms must comply with a patchwork of state and federal laws that govern the handling of personal information. The absence of a unified federal privacy statute means that brokers operating in multiple states must adhere to varying requirements, which increases operational complexity and legal costs. As per the International Association of Privacy Professionals, complying with the California Consumer Privacy Act alone can cost companies up to 1.5 million USD annually due to the need for specialized legal counsel and technical upgrades. Other states such as Virginia, Colorado, and Connecticut have enacted their own privacy laws with differing definitions of personal data and consumer rights, which creates a fragmented compliance environment. Brokers must continuously update their data handling practices, consent mechanisms, and security protocols to avoid penalties which can reach thousands of dollars per violation. The Federal Trade Commission actively enforces these regulations and has increased its scrutiny of data practices in the financial services sector including insurance. Additionally, clients are becoming more aware of their privacy rights and may request data deletion or opt out of data sharing, which complicates record keeping and risk assessment processes. The cost of implementing compliant systems is particularly burdensome for smaller brokerage firms that lack the resources of larger competitors. Failure to comply can result in significant fines and reputational damage, which can deter potential clients. This regulatory fragmentation forces brokers to invest heavily in compliance infrastructure rather than innovation or customer acquisition. The ongoing evolution of privacy laws means that this challenge will persist and likely intensify, requiring continuous adaptation and resource allocation.

Economic Volatility Impacts Client Spending and Risk Appetite

Economic volatility poses a significant challenge to the U.S. insurance brokerage market as fluctuations in inflation, interest rates, and employment levels directly influence client spending and risk appetite. During periods of economic uncertainty, businesses and individuals tend to reduce discretionary spending and may opt for minimal coverage or higher deductibles to lower premium costs. According to the Bureau of Labor Statistics, the inflation rate in the U.S. averaged 4.1% in 2023, which increased operational costs for businesses and reduced disposable income for households. This financial pressure leads to higher policy cancellation rates and slower renewal growth as clients scrutinize their insurance expenses more closely. Additionally, economic downturns can result in increased claims frequency as businesses cut corners on safety maintenance or delay necessary repairs to save money. According to the National Council on Compensation Insurance, workers compensation claim frequencies increased by 5% in 2023, partly due to staffing shortages and increased workplace stress associated with economic pressures. Brokers face the dual challenge of retaining clients who are seeking to reduce costs while also managing rising premiums driven by inflationary pressures on repair and medical costs. According to the Federal Reserve, interest rates remained elevated throughout 2023, which increased the cost of capital for insurance carriers leading to harder market conditions and stricter underwriting standards. This environment makes it difficult for brokers to negotiate favorable terms for their clients, which can strain relationships. Furthermore, economic instability can lead to business closures and bankruptcies, which result in lost revenue for brokerage firms. Navigating this volatile landscape requires brokers to demonstrate clear value and help clients optimize their risk management strategies without compromising essential protection.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.97% |

| Segments Covered | By Brokerage, Client, and By Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

| Regions Covered | California, Washington, Oregon, New York & Rest of the United States |

| Market Leaders Profiled | Marsh McLennan (Marsh), Aon plc, Willis Towers Watson (WTW), Arthur J. Gallagher & Co., Brown & Brown Inc., HUB International, Lockton Companies, USI Insurance Services, Truist Insurance Holdings, Acrisure, Alliant Insurance Services, Hilb Group, Ryan Specialty Group, NFP Corp., BXS Insurance, PCF Insurance Services, AssuredPartners, Amwins Group, INSURICA, Risk Strategies Company |

SEGMENTAL ANALYSIS

By Brokerage Insights

The retail brokerage segment dominated the market by accounting for the largest share of the U.S. insurance brokerage market in 2025. The dominance of retail brokerage segment in the U.S. market is attributed to its direct engagement with end users and comprehensive service offerings for both personal and commercial lines. The retail brokerage segment maintains its leadership position by catering to a vast and diverse client base that requires personalized attention and customized insurance programs. As per the Independent Insurance Agents and Brokers of America, independent retail agents represent approximately 80% of all insurance agencies in the U.S., which demonstrates their pervasive presence in the market. These firms build long term relationships with clients by providing ongoing advisory services that extend beyond initial policy placement. According to the National Association of Insurance Commissioners, personal lines premiums which are predominantly sold through retail channels accounted for nearly 50% of total net premiums written in 2023. This substantial volume underscores the critical role retail brokers play in distributing auto, home, and life insurance products. Furthermore, retail brokers offer value added services such as claims assistance and risk assessments, which enhance client retention and loyalty. The Bureau of Labor Statistics indicates that the majority of insurance sales agents work in agencies that primarily serve retail clients, which reinforces the segment's structural dominance. Retail brokers also benefit from local market knowledge, allowing them to navigate regional regulatory nuances and carrier preferences effectively. This localized expertise enables them to secure competitive rates and coverage terms that digital platforms often cannot match. The trust established through face to face interactions remains a significant competitive advantage in an industry where complex financial decisions are made. Consequently, the retail segment continues to command the largest share of the market, driven by its ability to deliver high touch service and comprehensive risk management solutions to a broad spectrum of policyholders.

On the other hand, the wholesale brokerage segment is estimated to record a CAGR of 8.2% during the forecast period in the U.S. market owing to the increasing complexity of specialized risks and the need for access to non admitted markets. As per the National Association of Mutual Insurance Companies, the excess and surplus lines market in the U.S. grew by 12% in 2023, reaching approximately 90 billion USD in premiums. This expansion is fueled by emerging risks such as cyber liability, environmental impairment, and professional indemnity, which require specialized underwriting expertise. Wholesale brokers act as critical intermediaries connecting retail agents with surplus lines carriers who have the flexibility to craft bespoke policies for unique exposures. According to the Insurance Information Institute, cyber insurance premiums written through surplus lines channels increased by 25% in 2023, reflecting the heightened awareness of digital threats among businesses. Wholesale brokers possess the technical knowledge to assess these complex risks and negotiate terms with niche carriers that specialize in hard to place accounts. Additionally, the construction and energy sectors are increasingly relying on wholesale brokers to secure coverage for large scale projects with significant liability exposures. According to the Associated General Contractors of America, construction spending reached 2.1 trillion USD in 2023, driving demand for specialized builders risk and contractor liability policies. Wholesale brokers facilitate access to capacity in these segments by leveraging their relationships with global reinsurers and specialty insurers. This ability to provide coverage for non standard risks positions wholesale brokerage as a vital component of the insurance ecosystem. As risks become more sophisticated, the reliance on wholesale expertise will continue to drive robust growth in this segment.

By Client Insights

The small and medium sized enterprises segment led the market by holding the leading share of the U.S. market in 2025. The dominance of the small and medium sized enterprises segment is driven by the sheer volume of these businesses in the U.S. and the regulatory mandates that require them to carry specific insurance coverages. As per the Small Business Administration, there are 33.2 million small businesses in the U.S., which account for 99.9% of all US businesses. This vast number creates a massive addressable market for insurance brokers who provide essential services such as workers compensation, general liability, and property insurance. Many states legally mandate workers compensation insurance for businesses with employees, which ensures a consistent demand for brokerage services. The Bureau of Labor Statistics reports that small businesses employ nearly half of the private sector workforce, which increases their exposure to employment related liabilities and the need for appropriate coverage. Additionally, lenders often require commercial property and casualty insurance as a condition for business loans, which further drives adoption of brokerage services. According to the Federal Reserve, small business loan outstanding amounts reached 1.1 trillion USD in 2023, highlighting the financial interdependence that necessitates insurance protection. Brokers play a crucial role in helping SMEs navigate these requirements by identifying compliant and cost effective solutions. The complexity of managing multiple policies across different carriers makes brokers valuable partners for business owners who lack internal risk management expertise. Furthermore, the high turnover rate of small businesses means that new entities are constantly entering the market, creating a steady stream of potential clients. This dynamic environment ensures that the SME segment remains the largest contributor to brokerage revenues.

However, the individual client segment is the fastest growing segment in the U.S. insurance brokerage market and is estimated to showcase a CAGR of 7.2% during the forecast period owing to the changing demographics and increasing demand for personalized financial protection. The individual segment is experiencing rapid growth due to the aging population in the U.S. and the corresponding increase in demand for health and life insurance products. As per the U.S. Census Bureau, the number of Americans aged 65 and older is projected to reach 95 million by 2060, representing nearly 23% of the population. This demographic shift drives significant demand for Medicare supplement insurance, long term care coverage, and life insurance policies that provide financial security for retirees. According to the Centers for Medicare and Medicaid Services, national health expenditures are expected to grow at an average annual rate of 5.4% through 2031, which increases the financial burden on individuals and families. Brokers help individuals navigate the complex healthcare landscape by identifying affordable coverage options and explaining benefit structures. Additionally, the rising cost of prescription drugs and medical procedures encourages individuals to seek supplemental insurance policies that cover out of pocket expenses. As per the Kaiser Family Foundation, average annual premiums for employer sponsored health insurance increased by 7% in 2023, prompting some individuals to explore alternative coverage through brokers. Furthermore, the uncertainty surrounding social security benefits motivates older adults to purchase annuities and life insurance products to ensure income stability in retirement. Brokers provide personalized advice on these financial instruments, helping clients align their insurance choices with their long term goals. The increasing prevalence of chronic diseases among the aging population also drives demand for critical illness and disability insurance. These factors collectively contribute to the robust growth of the individual client segment in the insurance brokerage market.

U.S. COUNTRY ANALYSIS

The U.S. is likely to expand its footprint in the regional insurance brokerage market over the next few years, holding the dominant position in North America due to its mature financial infrastructure and high insurance penetration rates. One of the primary driving factors is the robust legal environment that mandates various forms of insurance coverage for businesses and individuals. According to the Insurance Information Institute, the U.S. insurance industry wrote 1.4 trillion USD in net premiums in 2023, reflecting the extensive coverage requirements across the economy. Mandatory auto insurance laws in all 50 states ensure a consistent baseline demand for personal lines brokerage services. Additionally, the complex regulatory framework governing healthcare, employment, and environmental compliance drives demand for specialized commercial insurance solutions. The Department of Labor enforces strict workers compensation regulations which require most employers to carry coverage, thereby sustaining demand for brokerage services. Another significant driver is the high level of litigiousness in the U.S., which increases the need for liability protection. According to the Judicial Conference of the U.S., there were over 400,000 civil cases filed, which underscores the high risk of litigation faced by corporations.

COMPETITIVE LANDSCAPE

The competition in the U.S. insurance brokerage market is characterized by a highly fragmented landscape with a mix of large global firms and numerous independent agencies. Major players compete on the basis of service quality technological innovation and industry specialization. The market sees intense rivalry as firms strive to differentiate themselves through value added services such as risk consulting and claims advocacy. Consolidation remains a dominant trend as larger entities acquire smaller brokers to expand their footprint and capabilities. This activity intensifies competition by creating economies of scale and broader service portfolios. Independent agencies counter this by offering personalized service and local market expertise which appeals to small and medium sized enterprises. Technological advancement is a key competitive frontier with firms investing in digital platforms to enhance customer experience and operational efficiency. The rise of insurtech startups introduces new competitive pressures by offering streamlined and cost effective solutions. Traditional brokers respond by integrating these technologies into their existing frameworks. Regulatory compliance also plays a crucial role in shaping competitive dynamics as firms must navigate complex legal requirements. Those who can effectively manage compliance while delivering innovative solutions gain a competitive advantage. The market is further influenced by changing consumer preferences towards transparency and convenience. Firms that adapt to these trends by providing flexible and accessible services are better positioned to succeed. Overall the competitive environment drives continuous improvement and innovation across the sector.

KEY MARKET PLAYERS

A few of the market players that are dominating the U.S insurance broker market are

- Marsh McLennan (Marsh)

- Aon plc

- Willis Towers Watson (WTW)

- Arthur J. Gallagher & Co.

- Brown & Brown Inc.

- HUB International

- Lockton Companies

- USI Insurance Services

- Truist Insurance Holdings

- Acrisure

- Alliant Insurance Services

- Hilb Group

- Ryan Specialty Group

- NFP Corp.

- BXS Insurance

- PCF Insurance Services

- AssuredPartners

- Amwins Group

- INSURICA

- Risk Strategies Company

Top Players In The Market

- Marsh McLennan stands as a preeminent global professional services firm with a significant footprint in the U.S. insurance brokerage sector. The company provides strategic advice and risk management solutions to a diverse clientele ranging from multinational corporations to small businesses. Its contribution to the market is defined by its comprehensive suite of services including cyber risk analytics and health benefits consulting. Recent actions to strengthen its position include substantial investments in artificial intelligence and data analytics platforms. These technological enhancements enable clients to better predict and mitigate emerging risks. The firm also focuses on expanding its digital capabilities to offer seamless client experiences. By integrating advanced modeling tools into its brokerage services Marsh McLennan enhances its ability to deliver tailored insurance programs. This approach solidifies its reputation as a leader in innovative risk solutions. The company continues to prioritize sustainability and environmental social and governance criteria in its advisory services. These initiatives align with the evolving expectations of corporate clients and regulatory bodies. Through continuous innovation and strategic partnerships Marsh McLennan maintains its competitive edge in the dynamic U.S. market.

- Aon plc is a leading global professional services firm that delivers a broad range of risk and human capital solutions to clients in the U.S.. The company plays a pivotal role in the insurance brokerage landscape by offering specialized expertise in reinsurance and commercial risk management. Aon contributes to the market by leveraging its global network to provide localized insights and scalable solutions. Recent efforts to bolster its market position include the integration of advanced predictive analytics into its underwriting processes. This technology allows for more accurate risk assessment and pricing strategies. The firm has also expanded its health solutions portfolio to address the growing demand for employee wellness programs. Aon actively engages in strategic collaborations with insurtech startups to enhance its digital offerings. These partnerships facilitate the development of innovative products that meet the changing needs of modern businesses. The company emphasizes diversity and inclusion in its workforce which enhances its ability to serve a diverse client base. By focusing on client centric innovation and operational excellence Aon reinforces its status as a key player in the U.S. insurance brokerage sector.

- Arthur J Gallagher and Co is a prominent global insurance brokerage and risk management services provider with a strong presence in the U.S.. The company is known for its customer centric approach and extensive network of independent offices. Its contribution to the market lies in its ability to provide personalized service and specialized industry knowledge. Recent actions to strengthen its position include a series of strategic acquisitions of regional brokers. These acquisitions expand its geographic reach and enhance its service capabilities in niche markets. The firm also invests heavily in technology to streamline operations and improve client engagement. By implementing digital tools for policy management and claims processing Arthur J Gallagher improves efficiency and responsiveness. The company prioritizes employee development and training to ensure high levels of service quality. This focus on human capital helps retain top talent and maintain strong client relationships. Arthur J Gallagher also emphasizes corporate social responsibility through various community initiatives. These efforts enhance its brand reputation and foster trust among clients and stakeholders. Through consistent growth and strategic innovation the company continues to be a major force in the U.S. insurance brokerage market.

Top Strategies Used By Key Market Participants

Key players in the U.S. insurance brokerage market primarily employ mergers and acquisitions to expand their service offerings and geographic reach. This strategy allows firms to integrate specialized expertise and access new client bases efficiently. Companies also invest heavily in digital transformation by adopting artificial intelligence and data analytics to enhance risk assessment capabilities. These technologies enable faster processing times and more accurate pricing models which improve customer satisfaction. Strategic partnerships with insurtech startups are another common approach to innovate product offerings and stay competitive. Firms focus on developing proprietary platforms that provide seamless user experiences and real time insights. Additionally there is a strong emphasis on talent acquisition and retention to maintain high service standards. Training programs and competitive compensation packages help attract skilled professionals who can navigate complex regulatory environments. Diversification into niche markets such as cyber insurance and environmental liability is also a prevalent strategy. This approach reduces dependency on traditional lines of business and captures emerging opportunities. Finally companies prioritize environmental social and governance initiatives to align with client values and regulatory expectations. These comprehensive strategies ensure sustained growth and resilience in a dynamic market landscape.

MARKET SEGMENTATION

This research report on the U.S insurance broker market is segmented and sub-segmented into the following categories.

By Brokerage Type

- Retail Brokerage

- Wholesale Brokerage

- Reinsurance Brokerage

- Bancassurance Brokerage Services

By Client Type

- Individuals

- Small & Medium-Sized Enterprises (SMEs)

- Large Corporations

- Public Sector Entities

By Insurance Line

- Life Insurance

- Health Insurance

- Property & Casualty (Motor, Home, Commercial, Liability)

- Specialty Lines (Cyber, Pet, Marine, Travel)

By Distribution Channel

- Traditional Face-to-Face

- Digital / Online Platforms

- Affinity & Embedded Partnerships

- Bancassurance Partnerships

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

What is fueling the growth of the U.S. insurance brokerage market?

Increasing demand for risk management solutions and growing insurance complexity are fueling market growth.

What does the U.S. insurance brokerage market encompass?

The market encompasses intermediary services that help individuals and businesses select, purchase, and manage insurance policies.

Which insurance brokerage segment generates the highest revenue in the U.S.?

Commercial insurance brokerage generates the highest revenue due to strong demand from businesses across industries.

Why are insurance brokers important in the U.S. insurance industry?

Insurance brokers provide expert advice, compare coverage options, and help clients secure suitable insurance solutions.

How is digital transformation reshaping the U.S. insurance brokerage market?

Digital platforms, AI-powered analytics, and online policy management tools are improving customer experience and operational efficiency.

What factors are increasing demand for insurance brokerage services in the U.S.?

Rising regulatory requirements, evolving business risks, and growing demand for customized insurance coverage are increasing demand.

What challenges are influencing the U.S. insurance brokerage market?

Market competition, regulatory compliance requirements, and changing customer expectations are key challenges.

How are data analytics impacting the insurance brokerage industry?

Data analytics helps brokers assess risks more accurately and deliver personalized insurance recommendations.

What is the future outlook for the U.S. insurance brokerage market?

The market is expected to grow steadily with increasing adoption of digital insurance solutions and expanding risk advisory services.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com