U.S. Laundry Detergent Market Size, Share, Trends & Growth Forecast Report Segmented By Product Type (Liquid Detergent, Laundry Pods), Distribution Channel and Country – Industry Analysis From 2026 to 2034

U.S. Laundry Detergent Market Report Summary

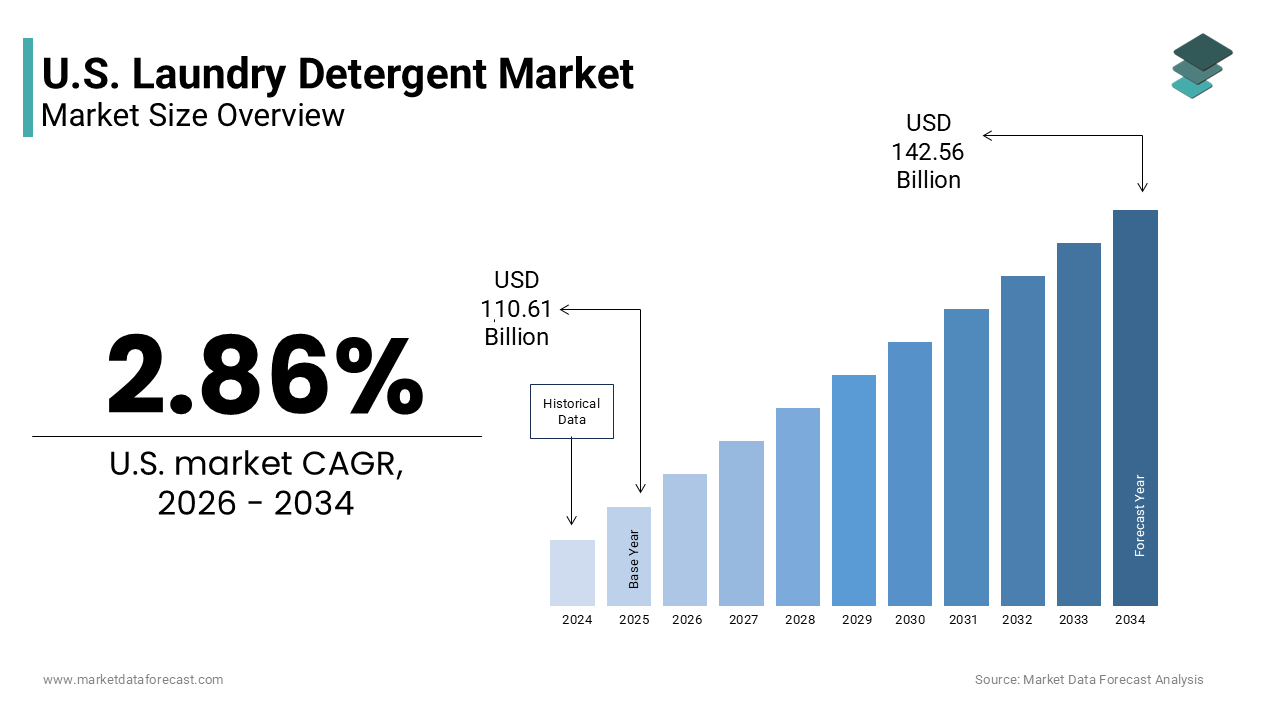

The U.S. laundry detergent market was valued at USD 19.12 billion in 2025, is estimated to reach USD 19.94 billion in 2026, and is projected to reach USD 27.95 billion by 2034, growing at a CAGR of 4.31% during the forecast period from 2026 to 2034. The growth of the U.S. laundry detergent market is driven by increasing consumer preference for concentrated and eco-friendly detergent formats, rising awareness regarding hygiene and fabric care, and growing demand for hypoallergenic and sensitive skin laundry solutions. Expanding adoption of cold-water washing detergents, increasing popularity of convenient laundry pod formats, and rising demand for sustainable packaging solutions are further accelerating market growth. Moreover, advancements in biodegradable formulations, expansion of direct-to-consumer subscription models, and growing focus on environmentally responsible cleaning products are supporting the expansion of the U.S. laundry detergent market.

Key Market Trends

- Rising demand for concentrated and eco-friendly detergent formats that reduce plastic waste and transportation emissions.

- Growing popularity of hypoallergenic, fragrance-free, and dye-free detergents among health-conscious consumers.

- Increasing adoption of laundry pods due to their convenience, precise dosing, and compact packaging.

- Strong focus on sustainable packaging innovations including water-soluble films and plastic-free detergent sheets.

- Expansion of direct-to-consumer subscription services offering personalized and convenient detergent delivery solutions.

Segmental Insights

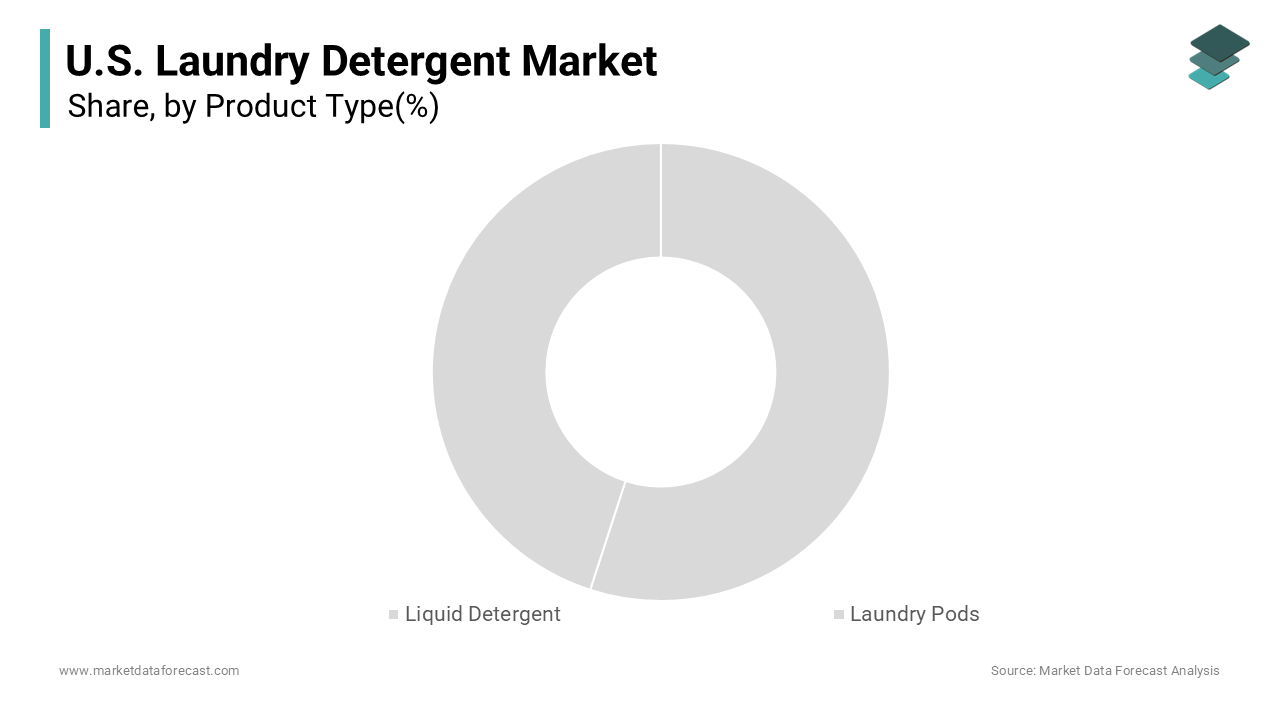

- Based on product type, the liquid detergent segment dominated the U.S. laundry detergent market and held the largest share in 2025. The segment’s dominance is attributed to its superior stain removal capabilities, compatibility with various washing conditions, ease of use, and strong consumer preference for fragrance-enhanced liquid formulations.

- The laundry pods segment is projected to witness the fastest CAGR during the forecast period owing to increasing consumer demand for convenience, accurate dosing, reduced product waste, and advanced multi-chamber pod technologies that combine detergent, stain remover, and fabric brightener functionalities.

- Based on distribution channel, the store-based retail segment accounted for the leading share of the U.S. laundry detergent market in 2025. The dominance of this segment is driven by strong consumer preference for immediate product availability, ability to compare products physically, and extensive retail presence across supermarkets, hypermarkets, and warehouse clubs.

- The non-store-based segment is anticipated to register notable growth during the forecast period due to the increasing popularity of e-commerce platforms, direct-to-consumer detergent brands, subscription delivery services, and rising consumer preference for convenient home delivery options.

Regional Insights

The United States dominated the North American laundry detergent market and accounted for a major share in 2025, supported by its large household base, high washing machine penetration, and strong consumer awareness regarding hygiene and fabric care. California remains a major contributor to the U.S. laundry detergent market due to its environmentally conscious consumer base, strong demand for sustainable cleaning products, and rapid adoption of eco-friendly packaging solutions. New York, Washington, and Oregon are also witnessing notable growth driven by increasing demand for premium and hypoallergenic detergents, expanding e-commerce penetration, and rising preference for sustainable household care products.

Competitive Landscape

The U.S. laundry detergent market is highly competitive and characterized by the presence of multinational consumer goods companies, eco-friendly detergent startups, and private label manufacturers competing through product innovation, sustainability initiatives, and pricing strategies. Leading companies are focusing on expanding concentrated detergent portfolios, investing in biodegradable formulations, strengthening direct-to-consumer distribution channels, and introducing plastic-free packaging innovations. Strategic partnerships with retailers, digital marketing campaigns, and investments in sustainable manufacturing practices are further strengthening market positioning across diverse consumer demographics.Prominent players in the U.S. laundry detergent market include Procter & Gamble, Unilever PLC, Henkel Corporation, Church & Dwight Co., Inc., The Clorox Company, Reckitt Benckiser Group plc, Colgate-Palmolive Company, Kao USA Inc., SC Johnson & Son, Inc., Seventh Generation, Inc., Method Products PBC, Sun Products Corporation, Amway Corporation, Dropps, Earth Friendly Products, Biokleen Industries, Inc., Persán S.A., Foca USA, RSPL Group, and Charlie

U.S. Laundry Detergent Market Size

The U.S. laundry detergent market size was valued at USD 19.12 billion in 2025 and is anticipated to reach USD 19.94 billion in 2026 from USD 27.95 billion by 2034, growing at a CAGR of 4.31% during the forecast period from 2026 to 2034.

Laundry detergent is a specialized cleaning agent, available in liquid, powder, or pod form, designed to remove dirt, stains, and odors from fabrics, primarily in washing machines. This sector is fundamentally anchored in household hygiene routines and textile maintenance rather than discretionary spending. The consistent demand arises from the biological necessity of removing dirt oils and pathogens from clothing and linens. The U.S. Census Bureau indicates there are approximately 131 million households in the nation, generating a consistent volume of laundry loads that sustains the baseline market for home care products. Moreover, the American Time Use Survey reveals that Americans spend an average of 2.01 hours per day on household activities, significantly higher than 45 minutes, with laundry and cleaning representing a core component of this daily routine. Furthermore the prevalence of home ownership influences washing habits as homeowners tend to wash larger loads less frequently compared to renters who may use communal facilities. Data from the Department of Energy and recent housing surveys indicates that approximately 85% of American homes possess an in-unit washing machine, while the remaining households rely on shared community facilities or services. The shift towards cold water washing has also impacted formulation requirements with manufacturers adapting enzymes to function effectively at lower temperatures. The Environmental Protection Agency notes that heating water accounts for about 90 percent of the energy used by a washing machine driving consumers toward detergents optimized for cold cycles. This transition reflects a broader convergence of convenience energy efficiency and cleaning efficacy defining the modern landscape of fabric care in the United States.

MARKET DRIVERS

Increasing Consumer Preference for Concentrated and Eco Friendly Formats

Consumers are increasingly shifting toward concentrated and eco-friendly detergent formats, which drives the growth of the United States laundry detergent market. This trend acts as a key catalyst for product innovation and market evolution in the country. Modern shoppers are increasingly aware of the environmental impact of traditional liquid detergents which often contain high water content and plastic packaging. According to data from the Environmental Protection Agency, the average American generates approximately 4.9 pounds of waste per day, with single-use plastic containers and packaging constituting the largest share of plastic trash entering municipal landfills. This awareness has spurred demand for ultra concentrated pods strips and powders that reduce plastic usage and transportation emissions. Additionally concentrated formulas require less storage space and offer precise dosing which minimizes product waste and overdose issues common with liquid pours. The Consumer Goods Forum highlights that corporate sustainability is a mainstream commercial imperative, aligning with broader consumer market studies which reveal that 82% of buyers are now actively willing to pay more for sustainably packaged goods. Manufacturers are responding by reformulating products to be biodegradable and free from phosphates and optical brighteners. This trend is further amplified by regulatory pressures in various states banning certain chemical ingredients. Consequently the market is witnessing a structural shift away from bulk liquids towards compact efficient and environmentally responsible alternatives that align with contemporary values of conservation and efficiency.

Rising Health Consciousness and Demand for Hypoallergenic Solutions

The growing emphasis on health and wellness has driven significant demand for hypoallergenic and sensitive skin laundry detergents, which further contributes to the expansion of the United States laundry detergent market. Consumers are becoming increasingly vigilant about the ingredients in household cleaning products due to concerns regarding skin irritation allergies and respiratory issues. Data from the Centers for Disease Control and Prevention highlights that diagnosed chronic skin conditions like eczema affect roughly 7.7% of U.S. adults and up to 12% of children, driving consistent market demand for dermatologically gentle home and cleaning solutions. raditional detergents often contain fragrances dyes and preservatives that can trigger adverse reactions leading consumers to seek out fragrance free and dye free alternatives. The National Eczema Association recommends specific laundry practices and products to manage symptoms further validating the need for specialized formulations. Research indicates that sales of free and clear detergents have grown at twice the rate of standard variants over the past five years. Parents are particularly proactive in choosing safe products for infants and toddlers whose skin is more permeable and sensitive. This health driven demand encourages manufacturers to invest in clinical testing and transparent labeling. Medical professionals continue to advocate for reduced chemical exposure in home environments. So, the segment for gentle and hypoallergenic detergents remains a robust driver of market growth.

MARKET RESTRAINTS

Volatility in Raw Material Costs and Supply Chain Disruptions

The volatility in raw material costs and ongoing supply chain disruptions are major restraints on the profitability and stability of the United States laundry detergent market. Key ingredients such as surfactants enzymes and packaging materials are derived from petrochemicals and agricultural sources which are subject to global price fluctuations. According to historical Bureau of Labor Statistics metrics, the producer price index for industrial chemicals faced severe double-digit volatility during peak inflationary cycles, which structurally altered the long-term production and baseline pricing frameworks for domestic consumer goods manufacturers. These rising input costs squeeze manufacturer margins as companies struggle to pass full price increases to price sensitive consumers. The Federal Reserve Bank of New York's Global Supply Chain Pressure Index reflects tightening logistics pipelines, climbing sharply to a multi-year high of 1.82 in early 2026 due to global geopolitical disruptions that have dramatically extended container shipping lead times. Additionally the reliance on specific geographic regions for specialty chemicals creates vulnerability to geopolitical tensions and trade policies. Small and medium sized brands are particularly affected as they lack the bargaining power to secure favorable terms with suppliers. Consequently the industry faces challenges in maintaining consistent pricing and product availability. These economic pressures limit the ability of manufacturers to invest in research and development or marketing initiatives thereby restraining overall market expansion and innovation potential.

Market Saturation and Intense Price Competition

Intense price competition and high saturation constrain the expansion of the United States laundry detergent market. Nearly every household purchases laundry detergent regularly resulting in a stable but stagnant volume demand that offers little room for expansion. This saturation leads to fierce competition among established brands and private labels for shelf space and consumer loyalty. Reports from the Private Label Manufacturers Association confirm that store-brand products reached a record $277 billion in sales, with retailers leveraging high-quality private label detergents as critical brand loyalty drivers to capture market share from budget-conscious shoppers. Major national brands often engage in promotional discounting to retain customers which erodes profit margins and devalues brand equity. This environment makes it difficult for new entrants to gain traction without substantial marketing investments. Furthermore the lack of differentiation in basic cleaning performance limits the effectiveness of product innovations in driving premiumization. Consumers frequently switch brands based on price promotions rather than brand loyalty creating a volatile revenue stream for manufacturers. This dynamic constrains the overall financial growth of the market despite steady consumption levels.

MARKET OPPORTUNITIES

Expansion of Direct to Consumer Subscription Models

The expansion of direct to consumer subscription models offers a significant opportunity for laundry detergent brands to enhance customer retention and stabilize revenue streams, which is expected to propel the growth of the United States laundry detergents market. Traditional retail channels are facing declining foot traffic as consumers increasingly prefer the convenience of home delivery for bulky and heavy items like detergent. Companies like Blueland and Tru Earth have capitalized on this trend by offering refillable systems and dissolvable strips delivered directly to subscribers doors. This model reduces packaging waste and ensures consistent product availability which appeals to environmentally conscious and busy consumers. The ability to customize delivery frequency allows users to manage inventory efficiently, reducing the likelihood of running out of essential supplies. Furthermore direct to consumer brands can gather valuable first party data on usage patterns which informs product development and targeted marketing. The elimination of intermediaries also allows for better margin control despite competitive pricing. As logistics networks improve and delivery speeds increase the appeal of subscription services continues to grow. This shift offers a pathway for brands to build deeper relationships with consumers and differentiate themselves in a crowded market through personalized and convenient service offerings.

Innovation in Water Soluble and Plastic Free Packaging

The growing demand for sustainable packaging solutions paves the way for innovation in water soluble and plastic free laundry detergent formats, which is likely to promote the expansion of the United States laundry detergent market. Consumers are actively seeking alternatives to traditional plastic jugs which contribute significantly to environmental pollution. According to the Ellen MacArthur Foundation only 14 percent of plastic packaging is collected for recycling globally highlighting the urgent need for circular solutions. Brands are responding by developing detergents encased in polyvinyl alcohol films that dissolve completely in water leaving no waste behind. The Biodegradable Products Institute certifies compostable packaging materials which helps brands validate their environmental claims and build trust with eco conscious shoppers. Additionally sheet detergents which come in cardboard boxes eliminate plastic entirely and reduce shipping weight leading to lower carbon emissions. The Federal Trade Commission Green Guides encourage accurate environmental marketing which supports brands that invest in genuine sustainability improvements. Retailers are also prioritizing shelf space for products with minimal environmental impact aligning with corporate sustainability goals. By pioneering these packaging innovations companies can capture a growing segment of the market that prioritizes ecological responsibility. This transition not only mitigates regulatory risks associated with plastic waste but also enhances brand reputation and loyalty among forward thinking consumers.

MARKET CHALLENGES

Regulatory Scrutiny and Chemical Safety Concerns

Increasing regulatory scrutiny and consumer concerns regarding chemical safety remain a significant challenge to the United States laundry detergent market. Government agencies and advocacy groups are closely monitoring the presence of potentially harmful substances such as 1 4 dioxane phosphates and synthetic fragrances in cleaning products. The California State Water Resources Control Board has implemented stringent limits on phosphate levels to protect water quality forcing manufacturers to reformulate products for specific markets. The Food and Drug Administration and the Environmental Protection Agency are also reviewing labeling requirements to ensure transparency regarding ingredient safety. Non compliance with evolving standards can result in costly recalls legal penalties and reputational damage. The Consumer Federation of America advocates for mandatory disclosure of all ingredients including fragrances which complicates proprietary formula protection. Additionally varying state level regulations create a complex compliance landscape for national brands requiring multiple product versions. These regulatory pressures increase research and development costs as companies strive to meet safety standards without compromising cleaning efficacy. Consumers are becoming more educated about toxicology leading to skepticism towards traditional formulations. This environment requires manufacturers to navigate a delicate balance between regulatory compliance consumer trust and product performance while managing increased operational complexities and costs.

Counterfeit Products and Brand Integrity Issues

The proliferation of counterfeit products slows down the expansion of the United States market. This presents a serious challenge to brand integrity and consumer safety. Illicit manufacturers produce fake versions of popular brands often using inferior or hazardous ingredients that fail to clean effectively and may cause skin irritation or damage washing machines. Online marketplaces have exacerbated this issue by providing easy access to fake products that closely mimic authentic packaging and branding. Consumers often struggle to distinguish between genuine and fake items especially when purchasing from third party sellers on e commerce platforms. This leads to dissatisfaction and erosion of trust in established brands when poor performance is mistakenly attributed to the original manufacturer. Legal efforts to combat counterfeiting are resource intensive and often yield limited results due to the decentralized nature of online sales. Additionally the presence of counterfeits distorts market data and consumer perception making it difficult for brands to accurately assess demand and plan production. Protecting brand identity and ensuring product authenticity requires significant investment in security features and monitoring technologies which adds to operational burdens.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.31% |

| Segments Covered | By Product Type, Distribution Channel and Region. |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | California, Washington, Oregon, New York, and the rest of the United States. |

| Market Leaders Profiled | Procter & Gamble, Unilever PLC, Henkel Corporation, Church & Dwight Co., Inc., The Clorox Company, Reckitt Benckiser Group plc, Colgate-Palmolive Company, Kao USA Inc., SC Johnson & Son, Inc., Seventh Generation, Inc., Method Products PBC, Sun Products Corporation, Amway Corporation, Dropps, Earth Friendly Products, Biokleen Industries, Inc., Persán S.A., Foca USA, RSPL Group, and Charlie’s Soap Inc. |

SEGMENTAL ANALYSIS

By Product Type Insights

The liquid detergent segment dominated the United States laundry detergent market and accounted for a 46.8% share in 2025. This dominance of the segment was driven by its superior versatility in treating a wide variety of stains and its effectiveness in pre treatment applications. Consumers prefer liquid formulations because they can be applied directly to stubborn stains such as grease oil and food residues before the wash cycle begins. According to the American Cleaning Institute, liquid detergents are highly recommended for oily and greasy stains because their fluid, surfactant-based composition allows them to penetrate fabric fibers and break down lipids more quickly than traditional powders. The ability to dissolve instantly in both cold and hot water makes liquids adaptable to various washing conditions without leaving residue. Data from the U.S. Department of Energy's consumer profiles notes that the average American household performs approximately 300 to 400 loads of laundry per year, creating a high-frequency usage cycle where convenience and formula efficacy are paramount. Liquid detergents are also compatible with high efficiency machines which require low sudsing formulas to prevent overflow and mechanical issues. Furthermore the ease of measuring and pouring liquids reduces user error compared to powders which can clump or spill. This combination of functional superiority and machine compatibility ensures that liquid detergent remains the dominant choice for the majority of consumers seeking reliable and versatile cleaning solutions.

Furthermore, the domination of the liquid detergent segment is further reinforced by consumer preference for enhanced fragrance options and sensory experiences during the laundry process. Liquid formulations allow manufacturers to incorporate a wider variety of scents and fragrance technologies that persist on fabrics after washing. The olfactory appeal of laundry products has become a significant purchasing driver with many shoppers selecting brands based on signature scents such as lavender ocean breeze or floral notes. Liquid detergents also offer the ability to include softening agents and brighteners that enhance the tactile and visual quality of clothes. This multi benefit approach appeals to consumers who view laundry as a holistic care routine rather than just a cleaning task. Marketing campaigns often emphasize the long lasting freshness provided by liquid pods and gels which resonates with busy households seeking efficient yet rewarding cleaning outcomes. The emotional connection to scent and the perception of superior performance sustain the market leadership of liquid detergents despite the emergence of alternative formats.

On the other hand, the laundry pods segment is predicted to witness the highest CAGR of 5.2% from 2026 to 2034 due to the convenience and precision dosing they offer to consumers with busy modern lifestyles. Pods eliminate the need for measuring pouring or guessing the correct amount of detergent reducing mess and waste. The pre measured nature of pods ensures optimal cleaning performance by preventing under dosing which leads to poor cleaning or over dosing which causes residue buildup. Additionally pods are lightweight and compact making them easier to store and transport compared to bulky liquid jugs. The rise of dual chamber and triple chamber pods that combine detergent stain remover and brightener in one unit further enhances their appeal by offering comprehensive cleaning in a single step. These factors collectively drive the rapid adoption of laundry pods among time constrained consumers.

Moreover, a further key factor driving the rapid growth of the laundry pods segment is the implementation of advanced safety innovations and child resistant packaging. Initial concerns regarding the safety of pods particularly among households with young children led to regulatory scrutiny and consumer hesitation. However manufacturers have responded by developing opaque bags and child resistant closures that significantly reduce the risk of accidental ingestion. The Consumer Product Safety Commission mandates specific labeling and packaging requirements that have restored consumer confidence in the product category. Major brands have invested heavily in public education campaigns to promote safe storage and usage practices further mitigating safety concerns. These safety and sustainability improvements have expanded the addressable market to include families who previously avoided pods due to safety risks. The laundry pod segment continues to experience robust growth as trust in the product category grows and packaging technology advances. This trend is driven by a combination of convenience, safety, and environmental responsibility.

By Distribution Channel Insights

The store based retail channels segment held the majority share of the United States laundry detergent market in 2025. This supremacy of the segment was credited to the immediate availability of products and the ability for consumers to evaluate them tangibly. Laundry detergent is a staple household item that consumers often purchase during regular grocery trips ensuring consistent foot traffic in supermarkets and big box stores. The physical presence of products allows shoppers to inspect packaging size scent descriptions and promotional offers before making a decision. Additionally the ability to take products home immediately satisfies urgent needs such as running out of detergent before a major wash day. Large retailers like Walmart Target and Kroger offer extensive assortments including private label and premium brands catering to diverse budget segments. The established supply chain infrastructure of brick and mortar stores ensures consistent stock levels and competitive pricing through economies of scale. Promotional activities such as buy one get one free deals further drive volume sales in physical stores. These factors collectively sustain the dominance of store based channels as the primary conduit for laundry detergent distribution.

In addition, the top position of the store based segment is further reinforced by consumer trust in established retail brands and the integration of loyalty programs that incentivize repeat purchases. Shoppers often rely on familiar retailers for quality assurance and consistent pricing reducing the perceived risk of purchasing counterfeit or substandard products. Major grocery chains offer digital coupons and personalized deals through mobile apps which encourage customers to choose specific detergent brands during their shopping trips. Physical stores also provide a platform for new product launches and sampling events allowing brands to introduce innovative formats directly to consumers. The tactile experience of smelling fragrances and comparing package sizes helps consumers make informed choices that align with their preferences. Additionally the integration of pharmacy and general merchandise sections in supercenters creates a one stop shopping experience that enhances convenience. These strategic advantages ensure that store based channels maintain their leading position by leveraging trust convenience and value driven incentives.

But the non store based channels segment is anticipated to witness the fastest CAGR of 7.8% over the forecast period owing to the convenience of home delivery and the popularity of subscription services that automate recurring purchases. Consumers increasingly prefer to avoid carrying heavy detergent bottles from stores opting instead for direct to door delivery. Amazon Subscribe and Save and other retailer programs offer discounts for automatic deliveries which incentivize customers to commit to long term purchases. Additionally online platforms provide access to a wider range of niche and eco friendly brands that may not be available in local stores. The ability to read detailed product reviews and compare prices instantly empowers consumers to make informed decisions. The rise of direct to consumer brands like Blueland and Tru Earth has further accelerated this trend by offering innovative plastic free solutions exclusively online. As digital literacy increases and mobile shopping becomes more prevalent the non store based channel continues to capture market share rapidly.

Moreover, a different factor accelerating the growth of non store based channels is the extensive access to specialized and eco friendly product varieties that appeal to conscious consumers. Online marketplaces serve as a hub for niche brands that focus on sustainable ingredients biodegradable packaging and hypoallergenic formulations. These specialized products are often marketed through digital channels where brands can educate consumers about their environmental benefits and ethical sourcing practices. Social media influencers and online communities play a significant role in promoting these brands creating awareness and driving traffic to e commerce sites. Online retailers also provide detailed ingredient lists and certification information which helps transparently communicate product values to skeptical buyers. The global reach of e commerce allows smaller brands to scale quickly without the burden of physical retail overhead. This dynamic ecosystem fosters innovation and competition driving the rapid growth of the non store based distribution channel as consumers prioritize sustainability and specialization.

COUNTRY ANALYSIS

The United States outperformed other countries in the North American laundry detergent market and accounted for a 82.4% share in 2025. This dominance is attributed to the country's large population high homeownership rates and advanced retail infrastructure. The market status is characterized by a mature yet dynamic environment where innovation and consumer preferences drive continuous evolution. According to the United States Census Bureau, there are approximately 131 million households in the country, each generating recurring laundry volumes that sustain a highly resilient baseline market for home care essentials. The high prevalence of automated washing machines ensures widespread access to convenient cleaning methods. Data from the U.S. Department of Energy's consumption metrics indicates that approximately 95% of American households possess an active, in-unit clothes washer, ensuring consistent consumer product engagement and predictable usage cycles. Additionally the United States has a robust regulatory framework enforced by the Environmental Protection Agency which ensures product safety and environmental compliance building consumer trust. The presence of major global conglomerates and innovative startups fosters intense competition resulting in a wide array of product options. High disposable income levels allow consumers to purchase premium and specialized detergents contributing to market value growth. The trend towards sustainability is particularly strong with many states implementing regulations on plastic waste and chemical ingredients. Furthermore the rise of e commerce and direct to consumer models has transformed the retail landscape enabling broader access to niche products. These structural demographic and economic factors solidify the United States as the leading market for laundry detergent in the region with sustained growth potential driven by health consciousness and technological advancements.

KEY MARKET PLAYERS

Some of the promising companies that are playing a dominating role in the U.S. Laundry Detergent Market include

- Procter & Gamble

- Unilever PLC

- Henkel Corporation

- Church & Dwight Co., Inc.

- The Clorox Company

- Reckitt Benckiser Group plc

- Colgate-Palmolive Company

- Kao USA Inc.

- SC Johnson & Son, Inc.

- Seventh Generation, Inc.

- Method Products PBC

- Sun Products Corporation

- Amway Corporation

- Dropps

- Earth Friendly Products

- Biokleen Industries, Inc.

- Persán S.A.

- Foca USA

- RSPL Group

- Charlie’s Soap Inc.

Top Players in the US Laundry Detergent Market

The Procter and Gamble Company

The Procter and Gamble Company maintains a formidable presence in the United States laundry detergent market through its iconic Tide brand which is synonymous with cleaning power. The company leverages extensive research and development to introduce advanced formulations such as cold water enzymes and stain fighting technologies. Recently Procter and Gamble has focused on sustainability by launching recyclable packaging and concentrated refills to reduce plastic waste. The corporation actively engages consumers through digital platforms and loyalty programs that enhance brand retention. By investing in supply chain efficiency and innovative product designs like Tide Pods the company ensures consistent quality and convenience. These strategic initiatives reinforce its leadership position while addressing evolving consumer demands for eco friendly and high performance cleaning solutions in a competitive retail environment.

Unilever PLC

Unilever PLC contributes significantly to the United States laundry detergent market with its diverse portfolio including Persil and Seventh Generation brands. The company emphasizes sustainable living and plant based ingredients appealing to environmentally conscious consumers. Recently Unilever has expanded its eco friendly offerings by introducing biodegradable formulas and plastic free packaging options. The brand actively promotes transparency in ingredient sourcing and manufacturing processes to build consumer trust. Unilever also strengthens its market position through strategic partnerships with retailers and e commerce platforms to enhance distribution reach. Their commitment to reducing carbon footprint and water usage aligns with global sustainability goals. By balancing performance with environmental responsibility Unilever captures a growing segment of shoppers who prioritize ethical consumption and effective cleaning capabilities in their household care routines.

Church and Dwight Co Inc

Church and Dwight Co Inc plays a pivotal role in the United States laundry detergent market through its Arm and Hammer brand which is recognized for value and reliability. The company focuses on providing affordable yet effective cleaning solutions using baking soda as a key ingredient. Recently Church and Dwight has innovated its product line with concentrated pods and odor eliminating technologies to meet modern consumer needs. The corporation invests in marketing campaigns that highlight the natural deodorizing properties of its products. By expanding its presence in online retail channels and offering bulk purchasing options the company enhances accessibility for budget conscious families. Their strategy of combining trusted heritage with modern convenience ensures strong customer loyalty. These efforts solidify its position as a leading provider of practical and economical laundry care products in the competitive US market landscape.

Top Strategies Used by Key Market Participants

Key players in the United States laundry detergent market employ several strategic initiatives to maintain competitiveness and drive growth. Product innovation remains a primary strategy with companies investing heavily in concentrated formulas and eco friendly packaging to appeal to sustainability minded consumers. Brands are increasingly adopting direct to consumer models and subscription services to enhance customer convenience and loyalty. Digital marketing and social media engagement are crucial for educating consumers about new technologies and benefits. Strategic partnerships with retailers help secure prominent shelf space and promotional opportunities. Companies are also focusing on supply chain resilience by diversifying sourcing and implementing automation. Price competitiveness is maintained through efficient operations and private label comparisons. Regulatory compliance and transparency in ingredient labeling are prioritized to build consumer trust. These strategies collectively enable companies to adapt to evolving preferences and strengthen their market presence effectively.

COMPETITIVE LANDSCAPE

The competition in the United States laundry detergent market is intense and characterized by a mix of established global conglomerates and agile niche brands. Major players leverage their extensive distribution networks and brand recognition to maintain dominance while newer entrants disrupt the market with innovative sustainable solutions. The rivalry is further amplified by the increasing convergence of cleaning efficacy and environmental responsibility where product safety and eco friendliness are key differentiators. Companies are constantly innovating to offer concentrated formats biodegradable materials and plastic free packaging to meet diverse consumer needs. Price competition is fierce particularly in the mass market segment where private labels offer affordable alternatives. Traditional brands face pressure to adapt to digital first strategies and direct to consumer models that enhance customer retention. The threat of substitution from alternative cleaning methods also influences competitive dynamics. Brand loyalty is cultivated through transparent communication and consistent performance. Regulatory compliance and ingredient transparency serve as critical factors in building consumer trust. Overall the market demands continuous adaptation to technological trends and societal values to sustain competitive advantage and profitability in this evolving industry landscape.

MARKET SEGMENTATION

This research report on the U.S. Laundry Detergent Market has been segmented based on the following categories.

By Product Type

- Liquid Detergent

- Laundry Pods

By Distribution Channel

- Store Based

- Non Store Based

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com