- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

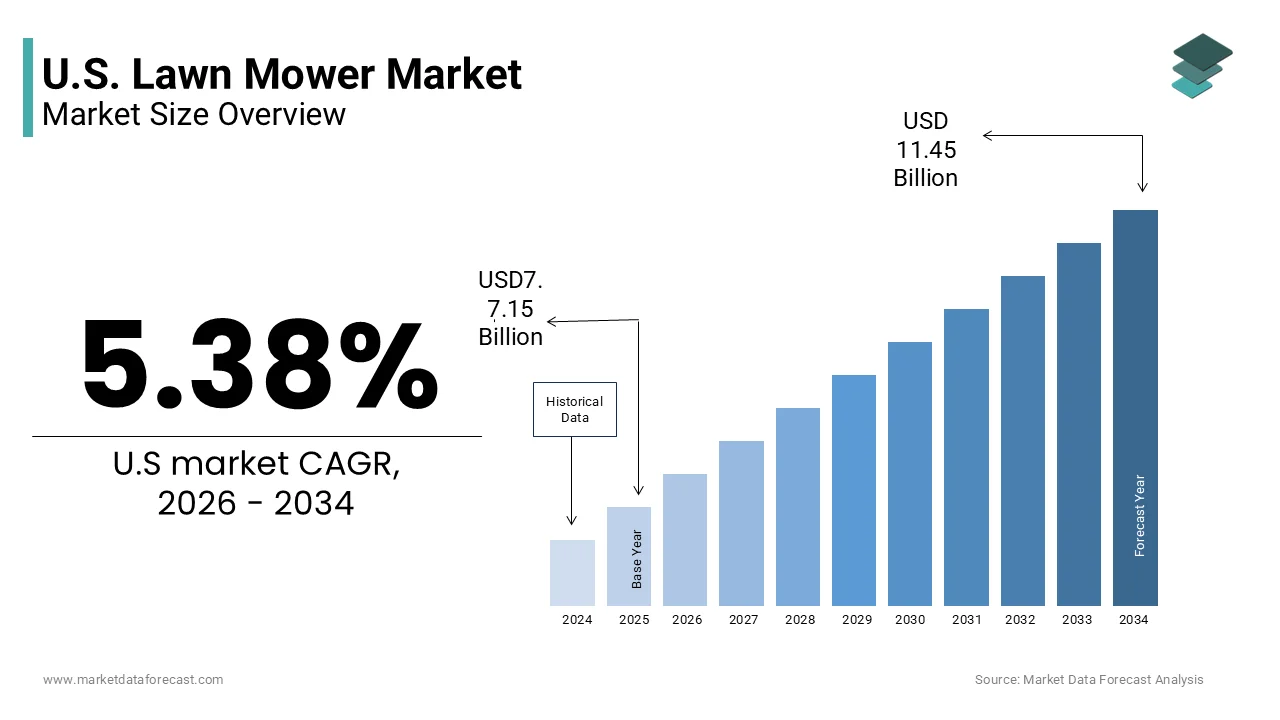

Market Size, 2025

$7.15 BnMarket Estimate, 2026

$7.53 BnMarket Forecast, 2034

$11.45 BnCAGR, 2026–2034

5.38%U.S. Lawn Mower Market Report Summary

The U.S. lawn mower market was valued at USD 7.15 billion in 2025, is estimated to reach USD 7.53 billion in 2026, and is projected to reach USD 11.45 billion by 2034, growing at a CAGR of 5.38% during the forecast period. Market growth is driven by increasing residential landscaping activities, rising demand for garden maintenance equipment, and growing consumer interest in outdoor aesthetics. Lawn mowers are widely used for maintaining lawns in residential and commercial spaces. The expansion of suburban housing and advancements in battery powered and automated mowing technologies are further supporting steady market growth in the United States.

Key Market Trends

- Rising demand for residential landscaping and garden maintenance is driving market growth.

- Increasing adoption of battery powered and electric lawn mowers is boosting demand.

- Growing interest in outdoor living and home improvement is supporting market expansion.

- Expansion of smart and robotic lawn mower technologies is enhancing product innovation.

- Technological advancements in energy efficiency and automation are improving performance.

Segmental Insights

- Based on product type, the petrol lawn mowers segment held a major share of the U.S. lawn mower market in 2025. This dominance is attributed to their high power output, durability, and suitability for larger lawns.

- Based on end user, the residential segment dominated the U.S. lawn mower market in 2025, driven by increasing home ownership, suburban development, and regular lawn maintenance needs.

Regional Insights

- The United States is expected to remain the primary growth engine for the North America lawn mower market over the forecast period, supported by strong consumer demand, advanced product adoption, and ongoing residential development.

Competitive Landscape

The U.S. lawn mower market is highly competitive, with key players focusing on product innovation, automation, and expansion of product portfolios to strengthen their market position. Companies are investing in electric and robotic mowers, smart technologies, and sustainable solutions. Prominent players in the U.S. lawn mower market include Deere & Company, The Toro Company, Husqvarna AB, Stanley Black & Decker, and American Honda Motor Co., Inc..

U.S. Lawn Mower Market Size

The U.S. lawn mower market was valued at USD 7.15 billion in 2025, is estimated to reach USD 7.53 billion in 2026, and is projected to reach USD 11.45 billion by 2034, growing at a CAGR of 5.38% from 2026 to 2034.

According to the U.S. Census Bureau, there are approximately 82 million single-family homes in the country, many of which feature private lawns requiring regular upkeep. The market is characterized by a shift towards environmentally friendly technologies driven by regulatory pressures and consumer awareness. As per the Environmental Protection Agency, garden equipment engines produce up to 5% of the nation's air pollution, prompting a transition towards electric alternatives. The definition of the market extends beyond hardware to include after-sales services, spare parts, and digital connectivity features that enhance user experience. Technological advancements in automation and battery efficiency are reshaping product offerings and consumer preferences. The interplay between housing trends, environmental regulations, and technological innovation defines the current operational landscape. Stakeholders are increasingly focusing on sustainability and convenience to meet evolving customer expectations. The market also includes a robust segment for commercial landscaping equipment, which supports the professional service industry. The integration of smart technologies, such as GPS mapping and remote control capabilities, is beginning to influence purchasing decisions among tech-savvy consumers.

MARKET DRIVERS

Expansion of Suburban Housing and Residential Landscaping

The expansion of suburban housing and the associated demand for residential landscaping is one of the key factors propelling the growth of the U.S. lawn mower market. As urban populations migrate to suburban areas in search of larger living spaces, the number of properties with private lawns continues to grow. According to the U.S. Census Bureau, new residential construction starts reached a seasonally adjusted annual rate of 1,502,000 units in March 2026, with a significant portion dedicated to single-family detached homes in suburban zones. These properties typically feature larger yards that require regular maintenance, driving the need for efficient and reliable lawn care equipment. The cultural importance of lawn aesthetics in American suburbs encourages homeowners to invest in high-quality mowers to maintain curb appeal and property value. As per the National Association of Home Builders, landscaping is considered a key factor in home buyer decisions, influencing the willingness of owners to purchase premium equipment. The trend towards outdoor living spaces further amplifies the demand for well-maintained lawns as families spend more time in their backyards. Manufacturers are responding by developing user-friendly models with advanced features, such as self-propulsion and mulching capabilities. The steady growth of the housing market ensures a consistent baseline demand for both replacement and new purchases. This demographic shift towards suburban living creates a sustained market for residential lawn care solutions. The emphasis on home improvement and exterior aesthetics reinforces the necessity of lawn mowers in household budgets.

Regulatory Push towards Electric and Battery Powered Equipment

The regulatory push towards electric and battery-powered equipment significantly drives the U.S. lawn mower market by encouraging the adoption of cleaner alternatives to gas-powered machines. Federal and state governments are implementing stricter emissions standards to reduce air pollution and noise levels in residential areas. According to the Environmental Protection Agency, one hour of operating a new gasoline lawn mower emits the same amount of volatile organic compounds and nitrogen oxide as driving a new car 45 miles. Several states, such as California and New York, have introduced legislation to phase out the sale of new gas-powered lawn equipment within the next decade. As per the California Air Resources Board, the transition to zero-emission outdoor power equipment is expected to improve local air quality and public health. These regulatory mandates compel manufacturers to accelerate the development and marketing of battery-electric and corded-electric mowers. Consumers are increasingly aware of the environmental benefits of electric models, which offer quieter operation and lower maintenance requirements. The availability of federal and state incentives for purchasing eco-friendly equipment further stimulates demand. Retailers are expanding their inventory of electric options to comply with upcoming regulations and meet consumer preference. This regulatory environment creates a favorable landscape for the growth of the electric lawn mower segment. The shift towards sustainability aligns with broader societal values and drives long-term market transformation.

MARKET RESTRAINTS

High Initial Costs of Advanced and Electric Models

High initial costs of advanced and electric lawn mower models are hindering the expansion of the U.S. lawn mower market. Battery-powered and robotic mowers often carry price tags that are substantially higher than traditional gas-powered equivalents, due to the cost of lithium-ion batteries and sophisticated electronics. According to the Bureau of Labor Statistics, the consumer price index for all urban consumers rose 3.5% over the last 12 months, reflecting the increased production costs associated with new technologies. For many households, particularly those with smaller lawns, the premium price of electric models may not be justified by the perceived benefits. As per the National Retail Federation, price sensitivity remains a key factor in purchasing decisions for home improvement products, with many consumers opting for lower-cost entry-level options. The additional expense of purchasing spare batteries or charging stations further adds to the total cost of ownership. While electric mowers offer lower operating costs over time, the upfront investment acts as a barrier to widespread adoption. Economic uncertainty and inflationary pressures exacerbate this issue by reducing disposable income for non-essential upgrades. Manufacturers face challenges in balancing advanced features with affordability to capture a broader market segment. Until prices become more competitive with gas-powered alternatives, the high cost will remain a persistent constraint. This financial barrier restricts market penetration among middle- and lower-income demographics.

Maintenance Complexity and Battery Life Concerns

Maintenance complexity and concerns regarding battery life present a major restraint on the U.S. lawn mower market, particularly for electric and robotic models. Consumers are often hesitant to switch from gas-powered mowers due to familiarity with their maintenance routines and perceived reliability. According to Consumer Reports, most homeowners find their rechargeable mower battery lifespan sits between 2 and 4 years, with high-quality versions lasting up to 5 years. The limited lifespan of lithium-ion batteries, which typically last three to five years, raises concerns about long-term value and environmental waste. As per the Institute of Electrical and Electronics Engineers, recycling infrastructure for large lithium-ion batteries is still developing, creating uncertainty about proper disposal and environmental impact. Robotic mowers require regular software updates, sensor cleaning, and boundary wire maintenance, which can be technically challenging for some users. The perception that electric mowers lack the power and endurance of gas models for larger or thicker lawns further discourages adoption. Service networks for electric and robotic equipment are less established than those for traditional engines, making repairs inconvenient and costly. These technical and logistical hurdles create hesitation among potential buyers who prioritize ease of use and durability. Until battery technology improves and maintenance processes are simplified, these concerns will continue to restrain market growth. The lack of standardized battery platforms across brands also limits consumer flexibility.

MARKET OPPORTUNITIES

Integration of Smart Technology and Robotics

The integration of smart technology and robotics presents a significant opportunity for the U.S. lawn mower market to enhance convenience and user experience. Robotic lawn mowers equipped with GPS navigation, artificial intelligence, and smartphone connectivity allow for autonomous operation and remote monitoring. According to the International Federation of Robotics, consumer service robots for domestic tasks experienced a solid growth rate of 11%, with close to 20 million units sold in 2024. Smart mowers can map lawns, optimize cutting patterns, and adjust schedules based on weather conditions, providing a hassle-free maintenance experience. As per the Consumer Technology Association, the Internet of Things ecosystem in home gardening is expanding with devices that integrate with smart home platforms for seamless control. The ability to monitor battery status, receive maintenance alerts, and customize cutting heights via mobile apps appeals to tech-savvy homeowners. Manufacturers are developing models with improved obstacle detection and multi-zone capabilities to handle complex landscapes. The convenience of autonomous mowing aligns with busy lifestyles and the growing interest in smart home innovations. Early adopters are willing to pay a premium for these advanced features, creating a lucrative niche market. The potential for software updates and over-the-air improvements extends the product lifecycle and enhances customer loyalty. This technological evolution transforms lawn care from a chore into a managed service. The expansion of 5G networks further supports the connectivity and performance of smart lawn equipment.

Growth in Commercial Landscaping and Professional Services

The growth in commercial landscaping and professional services offers a notable opportunity for the U.S. lawn mower market to expand beyond residential consumers. The increasing outsourcing of lawn care by homeowners, businesses, and municipalities drives demand for high-performance commercial-grade equipment. According to the National Association of Landscape Professionals, the landscaping services industry has a market size of $188.8 billion in 2025. Professional landscapers require durable and efficient mowers capable of handling large areas and frequent use, creating a steady demand for zero-turn radius and stand-on mowers. As per the Bureau of Labor Statistics, employment of grounds maintenance workers is projected to grow 4% through the decade, supporting the expansion of commercial fleets. The shift towards sustainable practices in commercial landscaping encourages the adoption of electric and hybrid models to meet corporate environmental goals. Municipalities are also investing in eco-friendly equipment to reduce noise and emissions in public parks and spaces. Manufacturers can capitalize on this trend by offering specialized commercial lines with enhanced durability and service support. The professional segment is less price-sensitive and prioritizes productivity and reliability, ensuring higher margins for manufacturers. Partnerships with landscaping companies and rental agencies provide channels for bulk sales and brand visibility. This B2B opportunity diversifies revenue streams and reduces dependence on seasonal residential sales. The emphasis on efficiency and sustainability in professional services drives innovation in commercial equipment.

MARKET CHALLENGES

Supply Chain Disruptions and Raw Material Scarcity

Supply chain disruptions and raw material scarcity present a major challenge to the U.S. lawn mower market by affecting production timelines and cost structures. The industry relies on global supplies of steel, aluminum, plastics, and electronic components, which have faced significant bottlenecks in recent years. According to the Institute for Supply Management, the manufacturing sector showed a contraction in early 2026, with the PMI at 49.1%, indicating persistent challenges in sourcing critical parts. The reliance on overseas manufacturing, particularly in Asia, exposes companies to geopolitical tensions, trade tariffs, and logistics delays. As per the Federal Reserve Bank of New York, global supply chain pressure indices reflect ongoing logistical hurdles that impact import-dependent industries. The increased cost of raw materials forces manufacturers to either absorb margins or pass costs to consumers, which can dampen demand. Lead times for new equipment orders have extended, causing frustration among dealers and customers who expect immediate availability. The unpredictability of supply chains complicates inventory management and financial planning for businesses. Manufacturers struggle to forecast demand accurately amidst uncertain supply conditions, leading to stockouts or excess inventory. The cost of expedited shipping and alternative sourcing strategies erodes profitability. These disruptions hinder the ability of companies to launch new products and meet seasonal peaks. Until supply chains stabilize, the industry will face ongoing operational inefficiencies and margin pressure. The scarcity of rare earth metals for batteries also poses long-term risks.

Seasonal Demand Fluctuations and Weather Dependency

Seasonal demand fluctuations and weather dependency pose a significant challenge to the U.S. lawn mower market by creating volatility in sales and revenue. The demand for lawn mowers is heavily concentrated in the spring and summer months when grass growth is most active. According to the National Oceanic and Atmospheric Administration, March 2024 was the warmest March on record globally, which can significantly impact the timing and volume of sales. Unusually wet or cold seasons can delay the start of the mowing season, reducing consumer urgency to purchase new equipment. As per the National Retail Federation, retailers face challenges in managing inventory levels to match unpredictable seasonal demand, leading to potential overstock or stockouts. The short selling window puts pressure on manufacturers and distributors to maximize sales during peak periods, while minimizing costs during off-seasons. Weather extremes, such as hurricanes or heatwaves, can also disrupt supply chains and retail operations. The reliance on seasonal sales makes it difficult for companies to maintain steady cash flow throughout the year. Manufacturers must invest in diverse product portfolios, such as snow blowers, to balance seasonal revenue, but this requires additional resources. The unpredictability of weather due to climate change further complicates planning and forecasting. This seasonal nature limits the ability of the market to achieve consistent growth and stability.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.38% |

| Segments Covered | By Product Type, End User, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Deere & Company, The Toro Company, Husqvarna AB, Stanley Black & Decker Outdoor (MTD), and American Honda Motor Co., Inc. |

SEGMENTAL ANALYSIS

By Product Type Insights

The petrol lawn mowers segment held the major share of the U.S. lawn mower market in 2025. The growth of the petrol segment in the U.S. market is attributed to the extensive land area associated with American suburban homes that often feature expansive lawns requiring high-performance equipment. According to the U.S. Census Bureau, the median square floor area for new single-family homes was 2,176 square feet in late 2025, where grass growth seasons are long and vigorous. Petrol engines provide the consistent torque and runtime necessary to handle thick grass and uneven terrain, without the limitation of battery life or cord length. As per the Outdoor Power Equipment Institute, petrol-powered equipment continues to account for the majority of unit sales, due to its proven durability and lower upfront cost compared to advanced electric alternatives. Homeowners and professional landscapers value the ability to refuel quickly and continue work uninterrupted, which is critical during peak mowing seasons. The established infrastructure for fuel distribution and engine repair services further supports the prevalence of petrol mowers. Many consumers are accustomed to the maintenance routines of gas engines and perceive them as more robust for heavy-duty tasks. The widespread availability of spare parts and qualified technicians ensures that petrol mowers remain a practical choice for millions of users. This combination of performance, convenience, and familiarity ensures that petrol mowers maintain their market leadership despite the emergence of new technologies.

On the other hand, the robotic lawn mower segment is a promising segment and is estimated to register a CAGR of 19.2% during the forecast period owing to the increasing consumer demand for automation and convenience in home maintenance tasks. According to the International Federation of Robotics, sales of consumer service robots for domestic tasks grew by 11% in 2024, as technology becomes more affordable and user-friendly. Robotic mowers offer the benefit of autonomous operation, allowing homeowners to save time and effort while maintaining a consistently manicured lawn. As per the Consumer Technology Association, advancements in GPS navigation, obstacle detection, and smartphone connectivity have enhanced the reliability and appeal of robotic units. The integration of smart home ecosystems enables users to schedule mowing sessions, monitor progress, and receive alerts remotely. The growing popularity of smart homes among millennials and Gen Z consumers drives the acceptance of automated gardening solutions. Manufacturers are introducing models with improved battery life and cutting efficiency, which address previous limitations regarding lawn size and complexity. The environmental benefits of electric-powered robotic mowers also align with sustainability trends, attracting eco-conscious buyers. The reduction in noise pollution compared to petrol mowers makes them suitable for densely populated neighborhoods. These factors collectively propel the robotic segment at a faster pace, as consumers prioritize lifestyle convenience and technological innovation.

By End User Insights

The residential segment led the market by capturing the major share of the U.S. lawn mower market in 2025. The growth of the residential segment in the U.S. market can be credited to the vast number of single-family homes and the cultural emphasis on property aesthetics. According to the U.S. Census Bureau, the homeownership rate in the U.S. was 65.3% in early 2026, with a significant majority featuring private outdoor spaces that require regular care. The American dream narrative often includes a well-kept lawn as a symbol of pride and community standards, which motivates homeowners to invest in quality equipment. As per the National Association of Realtors, curb appeal is a critical factor in property valuation, influencing residents to prioritize lawn maintenance. The DIY culture in the U.S. encourages homeowners to perform their own landscaping tasks, rather than hiring professionals for routine mowing. The availability of a wide range of residential mowers, from push reels to riding models, caters to diverse budget and property size needs. Seasonal promotions and retail accessibility make it easy for consumers to purchase and replace equipment. The emotional connection to home ownership fosters a willingness to spend on tools that enhance the living environment. This segment benefits from consistent replacement cycles as equipment wears out or becomes obsolete. The sheer volume of residential properties ensures that this group remains the primary driver of lawn mower sales.

However, the commercial and government end-user segment is experiencing rapid growth and is predicted to record a CAGR of 7.4% during the forecast period owing to the expansion of professional landscaping services and public infrastructure maintenance. According to the National Association of Landscape Professionals, the median company in the landscape industry reported sales growth of 8.5% in recent studies. Professional landscapers require high durability and high-performance equipment, such as zero-turn radius mowers and stand-on units, to handle large areas efficiently. As per the Bureau of Labor Statistics, employment in landscaping and groundskeeping services is projected to grow, supporting the demand for commercial-grade machinery. Government initiatives to improve public parks and green spaces also contribute to procurement activities. The shift towards sustainable practices in commercial sectors encourages the adoption of electric and low-emission models to meet environmental regulations. Municipalities are increasingly investing in fleet modernization to reduce noise and emissions in urban areas. The professional segment values productivity and total cost of ownership, which drives the purchase of premium equipment. Contractual obligations for regular maintenance ensure steady demand for replacements and upgrades. These factors collectively ensure that the commercial and government segment expands as institutional spending on groundskeeping increases.

COUNTRY LEVEL ANALYSIS

The U.S. is expected to maintain its status as the primary engine for the North American lawn mower market for the next few years. According to the U.S. Census Bureau, the seasonally adjusted annual rate for housing completions reached 1,366,000 units in March 2026, which creates a foundational demand for lawn care equipment that is unmatched in other developed nations. The domestic market benefits from a robust manufacturing and distribution network that ensures wide availability of products across various price points. As per the Environmental Protection Agency, regulatory pressures to reduce emissions from small off-road engines are shaping the transition towards electric and battery-powered alternatives. Consumer preferences are shifting towards convenience and sustainability, influencing product development and marketing strategies. The presence of major global brands and innovative startups fosters a competitive environment that drives technological advancement. The seasonal nature of the market requires strategic inventory management and promotional planning by retailers. The integration of smart technologies and robotics is beginning to transform traditional lawn care practices. The resilience of the housing market supports steady demand for both new and replacement equipment. The U.S. serves as a trendsetter for lawn care innovations, influencing global product standards. The combination of cultural habits, regulatory frameworks, and technological adoption ensures that the U.S. maintains its dominant position in the global lawn mower market.

COMPETITIVE LANDSCAPE

The competition in the U.S. lawn mower market is characterized by intense rivalry among established global brands and emerging technology focused startups who compete on innovation price and brand loyalty. The market structure is moderately consolidated with key players holding significant influence over specific segments such as robotic or commercial mowers. Competitive intensity is driven by the rapid adoption of electric and autonomous technologies which require substantial research and development investments. Regulatory compliance regarding emissions and noise levels serves as a barrier to entry for smaller competitors without adequate resources. Established players leverage their extensive dealer networks and after sales service capabilities to maintain customer trust. Price competition is fierce in the entry level residential segment while premium sectors focus on advanced features and durability. The rise of direct to consumer sales channels disrupts traditional retail models forcing companies to adapt their distribution strategies. The focus on sustainability and smart home integration is becoming a key differentiator. Overall the competitive landscape requires continuous adaptation to technological advancements and shifting consumer preferences for eco friendly and automated solutions.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. lawn mower market include

- Deere & Company

- The Toro Company

- Husqvarna AB

- Stanley Black & Decker Outdoor (MTD)

- American Honda Motor Co., Inc.

Top Players in the Market

- Deere and Company is a dominant force in the U.S. lawn mower market renowned for its John Deere brand which symbolizes quality and durability. The company offers a comprehensive range of residential and commercial mowers including riding zero turn and robotic models. Deere strengthens its market position by integrating advanced technologies such as GPS guided mowing and autonomous capabilities into its equipment. The company recently expanded its electric vehicle lineup to address environmental concerns and regulatory pressures. Deere leverages its extensive dealer network to provide superior customer service and support. Its focus on innovation and sustainability ensures that it remains a preferred choice for homeowners and professional landscapers seeking reliable and efficient turf care solutions.

- Husqvarna Group is a leading global manufacturer of outdoor power products with a significant presence in the U.S. lawn mower market. The company offers a diverse portfolio including walk behind riding and robotic mowers under brands such as Husqvarna and Craftsman. Husqvarna strengthens its market position by pioneering automation technology with its Automower series which leads the robotic segment. The company recently invested in battery powered platforms to reduce emissions and noise pollution. Husqvarna focuses on digital connectivity allowing users to control mowers via smartphone apps. Its commitment to sustainability and user friendly design appeals to modern consumers. These initiatives enable Husqvarna to maintain a competitive edge in the evolving landscape of smart and eco friendly lawn care.

- The Toro Company is a prominent player in the US lawn mower market known for its innovative and high performance turf maintenance equipment. The company serves both residential and professional customers with a wide array of mowers including recycler super recycler and time cutter models. Toro strengthens its market position through continuous product development and strategic acquisitions that expand its technology portfolio. The company recently introduced smart sprinkler and mower integration systems to enhance overall lawn care efficiency. Toro focuses on durability and ease of use which builds strong brand loyalty among users. Its investment in electric and hybrid technologies aligns with industry trends towards sustainability. These efforts ensure that Toro remains a key contributor to the advancement of lawn care solutions in the U.S..

Top Strategies Used by Key Market Participants

Key players in the U.S. lawn mower market primarily employ strategies such as electrification automation and digital integration to strengthen their market position. Companies frequently invest in developing battery powered and robotic mowers to comply with environmental regulations and meet consumer demand for convenience. This approach allows them to capture early adopters and differentiate their offerings from traditional gas powered alternatives. Strategic partnerships with technology firms help implement smart features such as app control and GPS navigation. By focusing on sustainable materials and energy efficient designs companies align with corporate social responsibility goals. Additionally manufacturers expand their distribution channels through online platforms and specialized dealers to reach broader audiences. Product diversification into related outdoor power equipment also enhances cross selling opportunities. These combined strategies enable market participants to maintain competitiveness and drive growth in a technologically advancing industry landscape.

US Lawn Mower Market News

- In March 2023, Deere, an equipment giant, launched new autonomous ZTrak mowers for commercial use. This launch is anticipated to boost automation and strengthen the Us lawn mower markett presence

- In June 2023, Husqvarna, a power tool maker, expanded its battery powered mower lineup with new models. This expansion is anticipated to meet eco demands and strengthen the Us lawn mower markett presence

- In September 2023, Toro, a turf specialist, introduced smart irrigation integration for its robotic mowers. This introduction is anticipated to enhance efficiency and strengthen the Us lawn mower markett presence

- In January 2024, Deere, a leading brand, partnered with tech firms for AI driven lawn care solutions. This partnership is anticipated to improve intelligence and strengthen the Us lawn mower markett presence

- In May 2024, Husqvarna, a global supplier, acquired a robotics startup to enhance Automower technology. This acquisition is anticipated to advance innovation and strengthen the Us lawn mower markett presence

MARKET SEGMENTATION

This research report on the U.S. lawn mower market is segmented and sub-segmented into the following categories.

By Product Type

- Manual

- Electric

- Petrol

- Robotics

- Other Product Types

By End User

- Residential

- Commercial or Government

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States