U.S. Life Insurance Market Size, Share, Trends & Growth Forecast Report By Product Type, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Life Insurance Market Report Summary

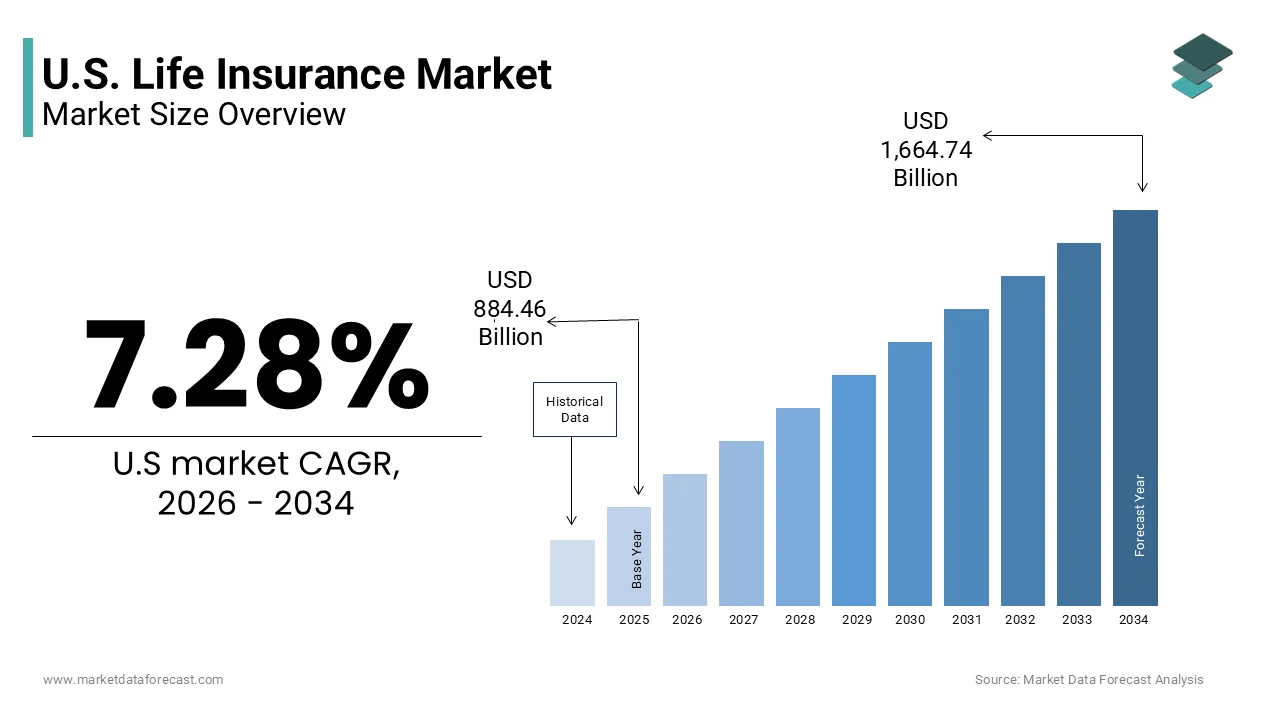

The U.S. life insurance market was valued at USD 884.46 billion in 2025, is estimated to reach USD 948.85 billion in 2026, and is projected to reach USD 1,664.74 billion by 2034, growing at a CAGR of 7.28% during the forecast period. Market growth is driven by increasing awareness regarding financial protection, rising demand for retirement planning solutions, and growing adoption of long term wealth management products. Life insurance policies play a critical role in providing financial security, income replacement, and investment benefits for individuals and families. The increasing integration of digital insurance platforms, AI driven underwriting, and personalised policy offerings is further supporting strong market expansion across the United States.

Key Market Trends

- Rising awareness regarding financial security and family protection is driving market growth.

- Increasing demand for retirement and long term financial planning solutions is boosting policy adoption.

- Growing use of digital insurance platforms and online policy management is supporting market expansion.

- Expansion of AI based underwriting and personalized insurance offerings is enhancing customer experience.

- Innovation in flexible premium structures and hybrid insurance investment products is influencing market development.

Segmental Insights

- Based on product type, the life insurance premiums segment accounted for 45.3% of the U.S. life insurance market share in 2025. This dominance is attributed to increasing policy purchases for financial protection, wealth preservation, and retirement planning purposes.

Regional Insights

- The U.S. life insurance market is experiencing steady growth across the country, supported by rising disposable incomes, increasing financial literacy, and growing awareness regarding risk management and future financial security. The adoption of digital insurance technologies and customer centric policy solutions is further strengthening market development.

Competitive Landscape

The U.S. life insurance market is highly competitive, with key players focusing on digital transformation, customer focused insurance solutions, and expansion of investment linked products to strengthen their market position. Companies are investing in AI based underwriting, mobile insurance platforms, and personalized financial planning services. Prominent players in the U.S. life insurance market include MetLife, Prudential Financial, New York Life Insurance Company, Northwestern Mutual, MassMutual, State Farm, AIG, Lincoln Financial Group, Principal Financial Group, and Guardian Life Insurance Company.

U.S. Life Insurance Market Size

The U.S. life insurance market size was valued at USD 884.46 billion in 2025, is estimated to reach USD 948.85 billion in 2026, and is projected to reach USD 1,664.74 billion by 2034, growing at a CAGR of 7.28% from 2026 to 2034.

The life insurance is providing monetary protection to beneficiaries upon the death of the insured. As per the Life Insurance Marketing and Research Association, approximately 54% of Americans currently hold some form of life insurance coverage. This penetration rate reflects a deep cultural emphasis on familial responsibility and long-term financial planning. The average household debt continues to rise, with the Federal Reserve Bank of New York stating that total household debt reached 17.29 trillion dollars in the fourth quarter of 2023. This economic backdrop drives the necessity for coverage that can offset mortgages, education costs, and final expenses. Furthermore, the aging population creates a sustained demand for estate planning tools and wealth transfer mechanisms. As per the United States Census Bureau, individuals aged 65 and older are projected to nearly double from 58 million in 2022 to 83 million by 2050.

MARKET DRIVERS

Rising Household Debt Levels Driving Coverage Needs

The escalating burden of household debt for increased demand is leveraging the growth of the United States life insurance market. Consumers recognize the necessity of protecting their families from financial hardship in the event of premature death. As per the Federal Reserve Bank of New York, mortgage debt alone accounts for the largest share of household liabilities, totaling 12.13 trillion dollars in late 2023. This substantial obligation compels homeowners to secure term life policies that align with the duration of their loans. Additionally, student loan debt remains a significant concern, with the Department of Education reporting that borrowers owe approximately 1.6 trillion dollars nationwide. Young adults often purchase coverage to ensure that co-signers or family members are not burdened by these obligations. The cost of living increases further exacerbates the need for income replacement. According to the Bureau of Labor Statistics, the consumer price index rose by 3.4% over the 12 months ending in January 2024, eroding purchasing power and increasing the amount of coverage required to maintain standard of living. Funeral expenses also contribute to this demand, with the National Funeral Directors Association stating that the median cost of a funeral with viewing and burial exceeded 7,800 dollars in 2023. These financial pressures create a compelling case for life insurance as a risk management tool. Insurers respond by offering flexible term products that cater to specific debt repayment timelines.

Demographic Shifts and Aging Population Dynamics

The growing aging population is additionally accelerating the growth of the United States life insurance market. As per the United States Census Bureau, the number of residents aged 65 and older is expected to reach 83 million by 2050, representing a substantial increase from current levels. This cohort often seeks permanent life insurance products, such as whole life or universal life to facilitate estate planning and wealth transfer. The desire to leave a financial legacy for heirs drives demand for policies with cash value accumulation features. According to the Society of Actuaries, longevity risk is a growing concern among retirees who wish to ensure their assets outlast their lifespans. Life insurance provides a tax efficient mechanism for transferring wealth outside of probate, appealing to high net worth individuals. Furthermore, the baby boomer generation holds significant wealth, with the Federal Reserve indicating that households headed by those aged 55 to 64 hold the highest median net worth. These individuals utilize life insurance to equalize inheritances among beneficiaries or to cover potential estate taxes. The increasing prevalence of chronic diseases among older adults also heightens awareness of mortality risks. The chronic diseases, such as heart disease and diabetes, which account for 6 of 10, leading causes of death. This health landscape encourages older consumers to secure coverage while they are still insurable. Insurers adapt by developing products with accelerated underwriting processes that cater to senior applicants.

MARKET RESTRAINTS

Consumer Perception of High Costs and Affordability Barriers

A widespread perception that life insurance is prohibitively expensive is hindering the growth of the United States life insurance market. Many consumers overestimate the cost of premiums by leading to hesitation or avoidance of purchase. As per a survey by LIMRA, 40% of Americans believe life insurance is more expensive than it actually is, with many estimating costs to be three times higher than reality. This misperception prevents millions of households from obtaining necessary coverage. The economic uncertainty following periods of inflation further exacerbates this issue, as families prioritize immediate expenses over long term financial protection. According to the Bureau of Labor Statistics, real wages have struggled to keep pace with inflation in recent years, reducing disposable income available for insurance premiums. Younger demographics, in particular, face budget constraints due to student loans and entry level salaries. The Institute for Life Insurance Information notes that millennials often delay purchasing coverage due to competing financial priorities. Additionally, the complexity of policy options can overwhelm consumers, leading to decision paralysis. Many individuals find it difficult to distinguish between term and permanent insurance, resulting in inaction. As per the American Council of Life Insurers, nearly 40 million households lack any form of life insurance despite having dependents. This protection gap highlights the impact of affordability concerns and knowledge deficits.

Complexity of Underwriting Processes and Administrative Friction

The traditional underwriting process remains a formidable barrier to entry for many potential policyholders, which is also restricting the growth of the United States life insurance market. Lengthy application procedures requiring medical exams and extensive documentation deter consumers seeking convenience and speed. The customer satisfaction with life insurance purchases is often impacted by the time required to complete underwriting, which can take several weeks. In an era dominated by instant digital services, this delay creates friction and leads to abandonment of applications. Younger consumers accustomed to seamless online experiences find the traditional model outdated and cumbersome. The requirement for paramedical exams introduces logistical challenges, including scheduling conflicts and privacy concerns. According to a study by Deloitte, nearly 30% of applicants drop out during the underwriting phase due to the inconvenience of medical testing. This attrition rate represents a significant loss of potential premium revenue for insurers. Furthermore, inconsistent underwriting standards across different carriers create confusion for agents and customers alike. The lack of standardized data sharing mechanisms slows down the verification of medical records and financial history. The regulatory variations between states add another layer of complexity to the approval process. Insurers are beginning to adopt accelerated underwriting models that utilize predictive analytics and electronic health records. However, adoption rates vary, and many companies still rely on manual reviews.

MARKET OPPORTUNITIES

Integration of Predictive Analytics and Accelerated Underwriting

The adoption of predictive analytics and accelerated underwriting technologies for expansion and efficiency gains is setting up new opportunities for the growth of the United States life insurance market. Insurers are leveraging big data to assess risk more accurately and quickly without requiring traditional medical exams. As per McKinsey and Company, insurers using advanced analytics can reduce underwriting time from weeks to minutes, significantly improving customer experience. This technological shift appeals to younger demographics, who value speed and convenience. By utilizing nontraditional data sources such as prescription history, motor vehicle records, and credit scores, carriers can make informed decisions with minimal friction. This approach also reduces operational costs by minimizing the need for manual reviews and third party vendors. As per the Society of Actuaries, predictive models improve risk selection accuracy by leading to better loss ratios and profitability. Insurers that invest in these technologies gain a competitive advantage by offering faster issuance and lower premiums for healthy applicants. The integration of artificial intelligence further enhances fraud detection and compliance monitoring. This technological evolution enables carriers to serve underserved segments, such as gig economy workers and freelancers who may lack traditional medical records.

Expansion into Wellness Programs and Preventive Care Initiatives

The integration of wellness programs into life insurance policies to engage customers and improve risk profiles is also to fuel the growth of the United States life insurance market. Insurers are increasingly offering incentives such as premium discounts, gift cards, and wearable devices to policyholders who maintain healthy lifestyles. As per Deloitte, interactive life insurance policies that reward healthy behaviors are gaining traction among millennial and Gen Z consumers. These programs foster ongoing engagement between insurers and clients, shifting the relationship from transactional to relational. According to a report by Swiss Re, wellness initiatives can lead to a 10% to 15% reduction in mortality risk for participants. This proactive approach aligns with broader societal trends toward preventive healthcare and personal well-being. Wearable technology integration allows for real time tracking of health metrics, providing valuable data for personalized recommendations. As per the International Data Corporation, shipments of wearable devices continue to grow, facilitating wider adoption of these programs. Insurers benefit from improved customer retention and enhanced brand loyalty through these value-added services. Furthermore, wellness programs differentiate carriers by attracting health-conscious consumers. The data collected through these initiatives also refines actuarial models, enabling more precise pricing.

MARKET CHALLENGES

Regulatory Compliance and Evolving Legal Frameworks

Navigating the complex and evolving regulations for providers is to pose as a major challenge for the growth of the United States life insurance market. Insurers must comply with varying state laws regarding policy provisions, marketing practices, and consumer protections. Each state has its own insurance department with distinct regulatory requirements by creating a fragmented compliance environment. This lack of uniformity increases operational costs and administrative burdens for national carriers. Recent developments in data privacy laws further complicate operations, particularly regarding the use of consumer data in underwriting and marketing. The California Consumer Privacy Act and similar legislation in other states impose strict guidelines on data collection and usage. The compliance with these regulations requires significant investment in legal expertise and technology infrastructure. Failure to adhere to these standards can result in hefty fines and reputational damage. Additionally, regulators are scrutinizing the use of algorithms and artificial intelligence to ensure fairness and prevent discrimination. There is increasing focus on algorithmic bias in financial services by prompting insurers to audit their models regularly. Changing tax laws also impact the attractiveness of certain life insurance products for estate planning purposes. Insurers must remain agile to adapt to these regulatory shifts while maintaining profitability.

Cybersecurity Threats and Data Privacy Vulnerabilities

The escalating cybersecurity threats due to the vast amounts of sensitive personal and medical data it stores is another attribute to impede the growth of the United States life insurance market. Insurers are prime targets for cybercriminals seeking to exploit personally identifiable information for identity theft and fraud. As per the Identity Theft Resource Center, the financial services sector experienced a significant increase in data breaches in recent years, with millions of records compromised. These incidents undermine consumer trust and expose companies to substantial legal and financial liabilities. The cost of remediation includes forensic investigations, notification expenses, and potential regulatory fines. According to IBM Security, the average cost of a data breach in the financial sector exceeds 5 million dollars, making it one of the most expensive industries to protect. Life insurers must invest heavily in advanced security measures such as encryption, multi factor authentication, and continuous monitoring. The rise of remote work has expanded the attack surface, creating additional vulnerabilities in network infrastructure. Regulatory bodies are imposing stricter data protection requirements, forcing insurers to enhance their cybersecurity posture. Failure to protect customer data can result in loss of business and damage to brand reputation. The interconnected nature of digital platforms increases the risk of systemic failures. Insurers must balance the need for data accessibility with robust security protocols. Managing these cyber risks requires ongoing vigilance and adaptation to emerging threats.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.28% |

| Segments Covered | By Product Type and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | MetLife, Prudential Financial, New York Life Insurance Company, Northwestern Mutual, MassMutual, State Farm, AIG, Lincoln Financial Group, Principal Financial Group, and Guardian Life Insurance Company |

SEGMENTAL ANALYSIS

By Product Type Insights

The life insurance premiums segment was accounted in holding 45.3% of the United States life insurance market share in 2025 due to the fundamental human need for income replacement and financial security for dependents. As per the study, term life insurance remains the most purchased product type, accounting for approximately 58% of individual life insurance coverage in force. The primary driver is the widespread ownership of mortgages and other long-term debts that require protection. The mortgage debt stands at 12.13 trillion dollars, compelling borrowers to secure coverage that matches their liability duration. Furthermore, the cultural expectation of providing for children’s education and spouse’s retirement fuels demand. Life insurance offers a guaranteed payout that ensures these obligations are met regardless of economic conditions. The simplicity of term products makes them accessible to a broad demographic, from young professionals to middle aged homeowners. Insurers have streamlined distribution channels by making purchase easier through digital platforms. The online sales of life insurance have grown significantly by attracting younger buyers, who prefer self-service options.

The annuity premiums and deposits segment is projected to expand at a CAGR of 6.8% from 2026 to 2034 with the aging population’s urgent need for guaranteed income streams in retirement. As per the United States Census Bureau, the number of Americans aged 65 and older is projected to reach 83 million by 2050, creating a massive cohort seeking financial stability. Traditional pension plans have largely disappeared from the private sector by shifting the burden of retirement income planning to individuals. According to the Employee Benefit Research Institute, only 17% of private sector workers have access to defined benefit plans, forcing reliance on personal savings and annuities. Fixed annuities provide a predictable payout that protects against longevity risk by ensuring retirees do not outlive their assets. As per the Insured Retirement Institute, annuity sales have surged as consumers seek refuge from market volatility. The rise of registered index linked annuities provides participation in market gains with downside protection, appealing to cautious investors. This demographic shift toward retirement age ensures sustained demand for annuity products. Insurers are responding with innovative features such as long term care riders by enhancing the value proposition. The structural need for retirement income security positions annuities as the most dynamic growth area in the sector.

COMPETITIVE LANDSCAPE

The competition in the United States life insurance market is intense and characterized by a mix of established mutual insurers stock companies and emerging insurtech firms. Major players differentiate themselves through financial strength brand reputation and comprehensive product offerings. Mutual insurers emphasize policyholder dividends and long term stability appealing to conservative consumers. Stock companies focus on innovation and diverse investment options to attract growth oriented clients. The rise of digital natives disrupts traditional models by offering simplified term policies with rapid issuance. Incumbents respond by investing in technology to match the speed and convenience of newer entrants. Price competition remains fierce in the term life segment where products are largely commoditized. However, differentiation occurs through service quality claims handling efficiency and additional benefits such as wellness programs. Distribution channels vary significantly with independent agents captive agents and direct online platforms vying for customer attention. Regulatory compliance costs create barriers to entry but also standardize market practices. Consolidation trends continue as larger entities acquire smaller firms to gain technological advantages and expand reach.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. life insurance market are

- MetLife

- Prudential Financial

- New York Life Insurance Company

- Northwestern Mutual

- MassMutual

- State Farm

- AIG

- Lincoln Financial Group

- Principal Financial Group

- Guardian Life Insurance Company

Top Players in the Market

- New York Life Insurance Company stands as a mutual insurer dedicated to providing financial security through diverse life insurance and annuity products. The company leverages its strong financial ratings to maintain consumer trust and attract risk averse clients seeking stability. Recent actions include significant investments in digital transformation initiatives that streamline policy administration and enhance customer service experiences. New York Life actively expands its suite of retirement income solutions to address the needs of an aging population. The company also strengthens its distribution network by supporting independent financial advisors with comprehensive training and technology tools. These efforts reinforce its reputation for reliability and long term value. Community engagement programs further bolster its brand image and foster deep connections with policyholders. This holistic approach ensures sustained relevance in a competitive landscape while prioritizing policyholder dividends and financial strength.

- Northwestern Mutual operates as a leading provider of whole life insurance and wealth management services with a focus on holistic financial planning. The company distinguishes itself through a direct writer model that employs exclusive financial representatives to build lasting client relationships. Recent strategies involve integrating sophisticated digital platforms that allow clients to monitor their policies and financial goals in real time. Northwestern Mutual has expanded its offerings in disability income insurance and long term care solutions to provide comprehensive protection. The firm invests heavily in cybersecurity measures to protect sensitive client data and maintain operational integrity. Its strong capital position enables consistent dividend payments which enhance customer loyalty and retention. Northwestern Mutual continues to innovate in estate planning tools helping clients navigate complex tax environments.

- MetLife Inc is a global insurance provider with a substantial presence in the United States life insurance and annuities sector. The company offers a wide range of products including term life universal life and variable annuities to diverse customer segments. MetLife has recently focused on enhancing its digital capabilities to improve customer engagement and simplify policy management processes. The firm utilizes artificial intelligence to optimize underwriting decisions and detect fraudulent activities efficiently. Strategic partnerships with fintech companies enable MetLife to offer innovative embedded insurance solutions through third party platforms. The company also prioritizes environmental social and governance initiatives to align with evolving investor and consumer expectations. MetLife continues to refine its group benefits portfolio serving employers who seek comprehensive employee wellness packages. These actions strengthen its competitive position and drive sustainable growth in the domestic market.

Top Strategies Used by Key Market Participants

Key players in the United States life insurance market primarily focus on digital transformation to enhance customer experience and operational efficiency. Insurers invest heavily in artificial intelligence and machine learning to streamline underwriting processes and reduce issuance time. Accelerated underwriting models utilize nontraditional data sources to assess risk without requiring medical exams. Companies expand their product portfolios to include wellness linked policies that reward healthy behaviors with premium discounts. Strategic partnerships with fintech firms enable the integration of insurance into broader financial ecosystems. Insurers also prioritize cybersecurity measures to protect sensitive customer data and maintain regulatory compliance. Direct to consumer channels are strengthened through user friendly online platforms that facilitate easy purchase and management. Personalization driven by data analytics allows for tailored recommendations and improved customer retention. Mergers and acquisitions help consolidate market presence and acquire specialized technological capabilities.

MARKET SEGMENTATION

This research report on the U.S. life insurance market is segmented and sub-segmented into the following categories.

By Product Type

- Life Insurance Premiums

- Annuity Premiums and Deposits

- Accident and Health Premiums

- Others

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

1. What is the U.S. life insurance market?

The U.S. life insurance market includes companies that provide financial protection products designed to offer monetary benefits to beneficiaries in the event of the policyholder’s death.

2. What are the major types of life insurance policies available in the U.S.?

Major policy types include term life insurance, whole life insurance, universal life insurance, variable life insurance, and group life insurance plans.

3. What factors are driving the growth of the U.S. life insurance market?

Rising awareness about financial security, increasing healthcare costs, growing middle class income, and demand for retirement planning solutions are major growth drivers.

4. What is term life insurance?

Term life insurance provides coverage for a fixed period and offers death benefits if the policyholder passes away during the policy term.

5. What is whole life insurance?

Whole life insurance provides lifelong coverage along with a cash value component that can accumulate over time.

6. How is technology transforming the life insurance industry?

Digital platforms, artificial intelligence, data analytics, and automated underwriting systems are improving customer experience and operational efficiency.

7. Who typically purchases life insurance policies?

Life insurance is commonly purchased by working professionals, parents, business owners, retirees, and individuals seeking financial protection for dependents.

8. What challenges affect the U.S. life insurance market?

Challenges include changing regulatory requirements, rising fraud risks, low insurance awareness among younger populations, and economic uncertainty.

9. How does life insurance support financial planning?

Life insurance helps provide income replacement, debt coverage, estate planning benefits, retirement support, and financial stability for beneficiaries.

10. Who are the leading companies in the U.S. life insurance market?

Major companies include MetLife, Prudential Financial, New York Life Insurance Company, and Northwestern Mutual.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com