U.S. Luxury Goods Market Size, Share, Trends & Growth Forecast Report Segmented By Product Type (Clothing and Apparel, Footwear, Leather Goods, Jewelry, Watches, Beauty and Personal Care, Eyewear, Home Décor and Fine Living Items), End-User, Distribution Channel and Country – Industry Analysis From 2026 to 2034

U.S. Luxury Goods Market Report Summary

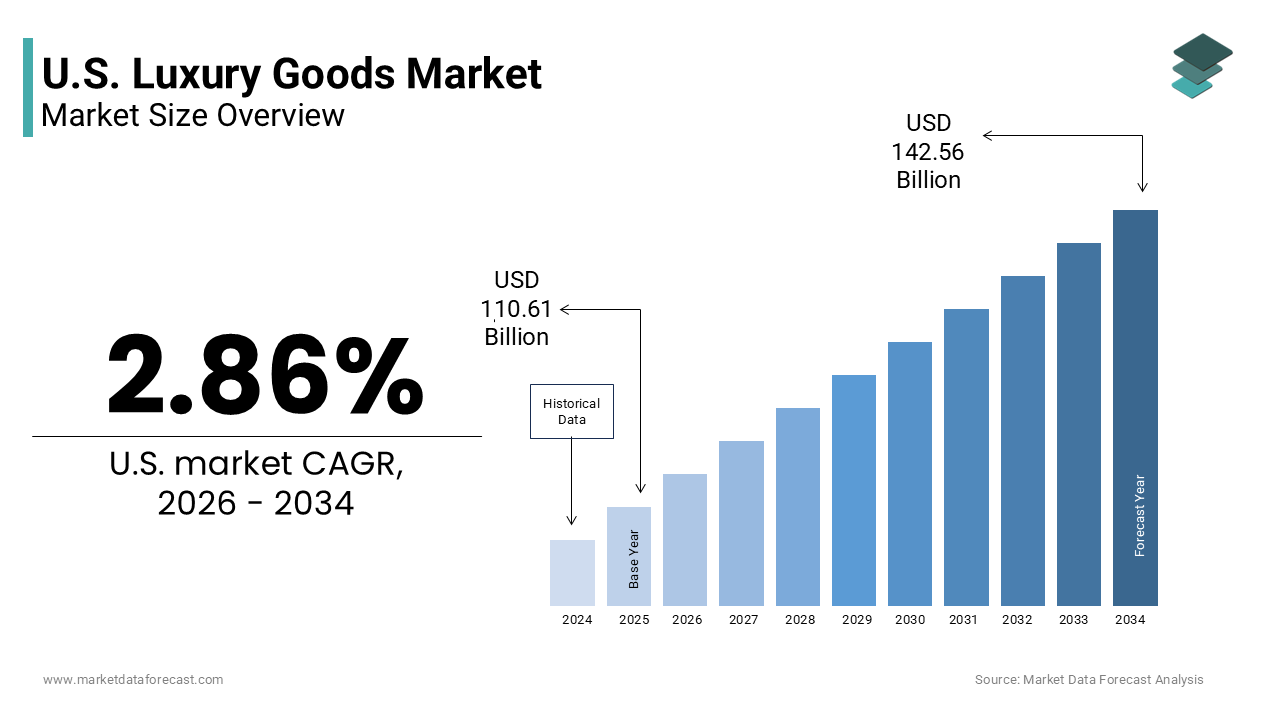

The U.S. luxury goods market was valued at USD 110.61 billion in 2025, is estimated to reach USD 113.77 billion in 2026, and is projected to reach USD 142.56 billion by 2034, growing at a CAGR of 2.86% during the forecast period from 2026 to 2034. The growth of the U.S. luxury goods market is driven by the rising affluent population, increasing demand for premium and exclusive products, and growing consumer preference for personalized luxury experiences. Expanding digital integration, strong adoption of omnichannel retail strategies, and increasing investments in sustainable luxury offerings are further accelerating market growth. Moreover, the growing popularity of luxury beauty products, rising influence of social media and celebrity endorsements, and increasing adoption of digital shopping platforms are supporting the expansion of the U.S. luxury goods market.

Key Market Trends

- Rising demand for sustainable and ethically sourced luxury products driven by environmentally conscious consumers.

- Growing popularity of digital luxury shopping and omnichannel retail experiences among affluent customers.

- Increasing adoption of AI-driven personalization and virtual luxury shopping experiences by premium brands.

- Strong focus on limited-edition collections and exclusive product launches to maintain brand desirability and exclusivity.

- Expansion of the luxury resale and pre-owned goods market supported by circular fashion trends and sustainability awareness.

Segmental Insights

- Based on product type, the leather goods segment dominated the U.S. luxury goods market and held the largest share in 2025. The segment’s dominance is attributed to the strong demand for premium handbags, wallets, and accessories that symbolize status, craftsmanship, and long-term investment value.

- The beauty and personal care segment is projected to witness the fastest CAGR during the forecast period owing to increasing consumer spending on premium skincare and cosmetics, rising influence of social media beauty trends, and growing demand for luxury wellness and self-care products.

- Based on end user, the women segment accounted for the leading share of the U.S. luxury goods market in 2025. The dominance of this segment is driven by higher engagement with luxury fashion, beauty, jewelry, and accessories categories, along with increasing financial independence among female consumers.

- The men segment is anticipated to register notable growth during the forecast period due to the growing acceptance of luxury fashion and grooming among male consumers, rising demand for premium streetwear and accessories, and increasing influence of celebrity-driven fashion trends.

- Based on distribution channel, the single brand stores segment held the major share of the U.S. luxury goods market in 2025 owing to their ability to provide immersive brand experiences, personalized customer service, and exclusive product offerings.

- The online stores segment is expected to witness rapid growth during the forecast period because of increasing consumer preference for digital shopping convenience, advancements in luxury e-commerce platforms, and rising integration of virtual try-on and augmented reality technologies.

Regional Insights

The United States dominated the North American luxury goods market and accounted for a major share in 2025, supported by its large affluent population, strong consumer spending capacity, and globally influential fashion and retail ecosystem. California remains a major contributor to the U.S. luxury goods market due to its concentration of affluent consumers, luxury retail hubs, and strong celebrity and entertainment influence. New York, Washington, and Oregon are also witnessing notable growth driven by increasing demand for premium fashion products, expanding luxury retail infrastructure, and rising digital luxury shopping adoption.

Competitive Landscape

The U.S. luxury goods market is highly competitive and characterized by the presence of leading global luxury conglomerates, heritage fashion houses, and emerging premium lifestyle brands competing through exclusivity, craftsmanship, digital innovation, and sustainability initiatives. Leading companies are focusing on expanding omnichannel retail capabilities, strengthening digital engagement strategies, investing in sustainable sourcing practices, and launching limited-edition collections to enhance brand value. Strategic collaborations with celebrities, influencers, and fashion designers, along with investments in immersive luxury retail experiences, are further strengthening market positioning across diverse consumer demographics. Prominent players in the U.S. luxury goods market include LVMH Moët Hennessy Louis Vuitton, Kering SA, Hermès International S.A., Chanel Limited, Compagnie Financière Richemont S.A., Prada Group, Burberry Group plc, Giorgio Armani S.p.A., Ralph Lauren Corporation

U.S. Luxury Goods Market Size

The U.S. Luxury Goods Market size was valued at USD 110.61 billion in 2025 and is anticipated to reach USD 113.77 billion in 2026 from USD 142.56 billion by 2034, growing at a CAGR of 2.86% during the forecast period from 2026 to 2034.

Luxury goods are a sophisticated ecosystem of high-value personal items and experiences that signify status, exclusivity, and superior craftsmanship. This field covers diverse categories including leather goods fine jewelry haute couture watches and premium beauty products. The market is characterized by its resilience and ability to adapt to shifting consumer preferences while maintaining an aura of desirability. The demographic foundation of the premium retail sector remains fundamentally strong. According to research, the U.S. high-net-worth individual (HNWI) population expanded by 7.6% to reach 7.9 million people, providing a highly resilient base of core luxury consumers. Consumer sentiment benchmarks from the Saks Global Luxury Pulse survey show a resilient core demographic, with 58% of surveyed luxury consumers stating an intent to maintain or increase their luxury retail spending heading into major seasonal shopping window. This consolidation of spending among affluent demographics underscores the market's reliance on deep engagement with core clientele rather than broad volume expansion. The definition of luxury continues to evolve integrating digital experiences and sustainable practices into the core value proposition.

MARKET DRIVERS

Rising Affluent Population Drives Consistent Demand

The substantial growth in the high net worth individual population is the main engine propelling the United States luxury goods market. This creates a stable and expanding base of consumers with significant disposable income. This demographic shift ensures a steady demand for high value items regardless of broader economic fluctuations. Research shows that North America led global wealth expansion with its high-net-worth individual population rising by 7.3%, outpacing steady gains in alternative regions like Asia-Pacific and Latin America. Within the largest individual wealth markets, the United States was the clear leader, adding 562,000 new millionaires as the country's high-net-worth individual population expanded to a total of 7.9 million. This influx of wealth directly correlates with increased spending power in the luxury segment. These individuals are not only increasing in number but are also demonstrating a willingness to invest in tangible assets such as jewelry and watches which serve as stores of value. The concentration of wealth in the United States provides a unique advantage for luxury brands operating in this region. As the number of affluent consumers grows so does the competition for their attention leading to enhanced service offerings and exclusive experiences. This dynamic fosters a loyal customer base that prioritizes quality and heritage over price sensitivity. The sustained growth in this demographic segment acts as a buffer against market volatility ensuring long term stability for luxury retailers.

Digital Integration Enhances Customer Engagement and Sales

The rapid adoption of digital technologies and e commerce platforms has become a major accelerator of the United States luxury goods market. This enables brands to reach consumers through seamless omnichannel experiences. Digital integration allows for personalized interactions and broader accessibility which are essential for engaging modern luxury shoppers. Strategic forecasting from Luxe Digital notes that online luxury sales are on a trajectory to comprise 30% of the total global luxury market, underscoring a permanent shift in how premium consumers interact with luxury brands. According to sources, the U.S. luxury e-commerce landscape continues to show double-digit resilience, expanding significantly past historical $20 billion baselines as digital channels capture greater market share. Brands are leveraging artificial intelligence and data analytics to offer customized recommendations and virtual try on experiences which enhance customer satisfaction. This technological advancement allows luxury brands to maintain exclusivity while expanding their reach. The ability to engage with customers through social media and digital campaigns has also become vital for brand building. Younger consumers particularly expect a robust digital presence and interactive content from luxury brands. This driver ensures that luxury retailers remain relevant in an increasingly digital world.

MARKET RESTRAINTS

Economic Volatility and Inflationary Pressures Restrain Spending

Economic instability and persistent inflationary pressures are hindering the growth of the United States luxury goods market. This erodes consumer confidence and reduces discretionary spending power. While affluent consumers are less sensitive to price changes prolonged economic uncertainty can lead to more cautious purchasing behavior. A study shows that while inflation is expected to remain relatively moderated in the first half of 2026, brewing trade policy updates could trigger a secondary inflationary pickup in the second half, creating a volatile environment for liquidity-driven consumer spending. Retail data compiled by Fashion Dive indicates that apparel, accessories, and footwear spending experienced sluggish, single-digit growth in early 2025, lagging behind macro consumer retail spending across the United States as buyers prioritized essential goods. This decline indicates that even in the luxury segment consumers are becoming more selective. The threat of tariffs also poses a challenge with luxury brands bracing for potential disruptions due to trade policies. These tariffs can lead to increased prices which may dampen demand. Consumers are hitting pause on purchases as they assess the economic landscape. This restraint forces brands to reconsider pricing strategies and value propositions. The uncertainty surrounding economic growth makes long term planning difficult for retailers. As a result the market faces headwinds that require strategic adaptation to maintain growth trajectories.

Counterfeit Goods Undermine Brand Integrity and Revenue

The proliferation of counterfeit luxury goods is a major restraint to the United States luxury goods market. This dilutes brand exclusivity and causes significant revenue losses. Counterfeit products not only divert sales from authentic brands but also damage the reputation and perceived value of luxury items. Annual enforcement reports from U.S. Customs and Border Protection (CBP) highlight that federal authorities seize tens of millions of counterfeit goods each year, representing an estimated manufacturer's suggested retail price (MSRP) of over $5.4 billion had the items been genuine. This vast volume of fake goods highlights the scale of the problem. Data from the Organization for Economic Co-operation and Development (OECD) estimates that the global trade in counterfeit goods exceeds $450 billion annually; this deep illicit network infiltrates modern e-commerce channels and poses an ongoing threat to brand protection teams. Research reveals a distinct generational shift in retail habits, with roughly 40% of younger Gen Z and Millennial consumers admitting to having purchased a counterfeit or "superfake" luxury product, heavily driven by social media commerce. This high rate of participation in the counterfeit market undermines the efforts of legitimate brands to maintain exclusivity. The presence of fake goods also complicates supply chain management and intellectual property protection. Luxury companies feel the impact of the counterfeit underground economy in various ways all of which serve as a detriment to their brand equity as noted by Stefanini. The fight against counterfeiting requires substantial investment in technology and legal resources. This restraint challenges the core value proposition of luxury which is based on authenticity and craftsmanship.

MARKET OPPORTUNITIES

Sustainability Initiatives Create New Growth Avenues

The increasing consumer demand for sustainable and ethically produced luxury goods paves the way for the expansion of the United States luxury goods market. This aligns brand values with contemporary social responsibilities. Sources confirm that sustainability and transparent supply chains have transcended temporary trend status to become permanent, structural cornerstones of the modern luxury market. This shift allows brands to attract environmentally conscious consumers who prioritize transparency and ethical sourcing. The main driver of this growth is sustainability as consumers seek to reduce waste and adopt circular purchasing habits. Brands that successfully integrate sustainable practices into their operations can differentiate themselves in a crowded market. Eco luxury fashion trends are gaining traction with recycled materials and circular fashion models becoming more prevalent as highlighted by Salfi Studio. This opportunity extends to product innovation and supply chain optimization. By embracing sustainability luxury brands can enhance their reputation and build deeper connections with customers. The demand for green luxury is expected to continue growing providing a stable platform for long term expansion. This trend also opens up new markets among younger demographics who are highly aware of environmental issues.

Expansion of Digital and Omnichannel Retail Experiences

The continued evolution of digital retail and omnichannel strategies offers a substantial opportunity for the United States luxury goods market. This enhances customer convenience and engagement. Brands that effectively integrate online and offline channels can provide a superior shopping experience that drives loyalty and sales. New luxury retail square footage increased by 65.1 percent in the first half of 2025 indicating a strategic expansion of physical presence alongside digital growth as per JLL. This hybrid approach allows customers to interact with brands in multiple ways. The United States online luxury fashion retail market is evolving rapidly requiring brands to invest heavily in digital infrastructure. Digital transformation enables personalized marketing and improved customer service through data analytics. This opportunity allows brands to reach wider audiences and gather valuable consumer insights. The use of augmented reality and virtual reality in retail experiences further enhances engagement. Brands can offer virtual try ons and immersive storytelling which enrich the customer journey. This digital expansion also facilitates global reach allowing US brands to connect with international customers. The integration of technology into retail operations is essential for staying competitive.

MARKET CHALLENGES

Supply Chain Disruptions Impact Product Availability

Supply chain disruptions continue to hamper the growth of the United States luxury goods market. This affects product availability and increases operational costs. The reliance on global sourcing and artisanal production methods makes the luxury sector vulnerable to logistical bottlenecks. Other expected challenges include the threat of fresh strikes by US dockworkers and global airfreight capacity restraints. These issues can lead to delays in product delivery and increased shipping costs. Supply chain challenges have emerged as a key issue because many luxury brands rely on artisanal production methods which are difficult to scale. Increasing customer demand and current global uncertainties have made supply chain management a strategic core function which poses major challenges for luxury brands. The complexity of managing a global supply network requires robust risk management strategies. Geopolitical tensions further exacerbate these challenges by creating uncertainty in trade routes. Brands must invest in supply chain resilience to mitigate these risks. This challenge requires continuous adaptation and investment in logistics infrastructure.

Geopolitical Tensions and Trade Policy Uncertainty

Geopolitical tensions and uncertain trade policies are a major challenge to the United States luxury goods market. This creates an unpredictable business environment. Tariffs and trade restrictions can significantly impact the cost structure and profitability of luxury brands. Luxury retail trends are heavily influenced by the need to navigate US tariffs and global trade tensions. Major players like Chanel Louis Vuitton and Gucci are adjusting their pricing and supply chains in response to these pressures. The threat of tariffs to disrupt the market is unlike any seen since the Great Recession or Covid. This uncertainty makes it difficult for brands to plan long term strategies. Geopolitics and luxury supply chains are closely linked with resilience becoming a key focus in 2025. Trade policies can change rapidly affecting import export dynamics. This challenge requires brands to be agile and responsive to regulatory changes. The impact of trade wars can extend beyond direct costs to affect consumer sentiment. Brands must diversify their supply chains to reduce dependence on single sources. This geopolitical landscape adds a layer of complexity to market operations.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 2.86% |

| Segments Covered | By Product Type, End-User, Distribution Channel and Region. |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | United States, Canada, Mexico |

| Market Leaders Profiled | LVMH Moët Hennessy Louis Vuitton, Kering SA, Hermès International S.A., Chanel Limited, Compagnie Financière Richemont S.A., Prada Group, Burberry Group plc, Giorgio Armani S.p.A., Ralph Lauren Corporation, Tapestry, Inc., Capri Holdings Limited, The Estée Lauder Companies Inc., Rolex SA, Tiffany & Co., Salvatore Ferragamo S.p.A., Moncler S.p.A., Brunello Cucinelli S.p.A., Dolce & Gabbana S.r.l., Versace, and Valentino S.p.A. |

SEGMENTAL ANALYSIS

By Product Type Insights

In 2025, leather goods held the majority share of the United States luxury goods market. They achieved this due to their status as entry-level luxury items and strong brand heritage. The dominance of this category is also driven by the high perceived value and versatility of products such as handbags wallets and small leather accessories which serve as visible symbols of status. The resilience of this segment is evident in its ability to withstand economic fluctuations as consumers view high quality leather goods as investment pieces rather than disposable fashion. In the United States the demand for exclusive and limited edition leather items remains robust with waitlists for popular bags extending several months. This scarcity model drives desire and maintains high price points. Furthermore the secondary market for luxury leather goods is thriving with platforms reporting that handbags are the most resold luxury item indicating strong retained value. This factor encourages primary market purchases as consumers recognize the long term utility and resale potential of these products. The craftsmanship associated with luxury leather goods also appeals to consumers seeking authenticity and durability in an era of fast fashion fatigue.

On the other hand, the beauty and personal care segment is predicted to witness the highest CAGR of 8.5% from 2026 to 2034 due to the democratization of luxury and the rise of premium skincare routines. This segment is outpacing other segments because of its accessibility and frequent purchase cycle. The driving force behind this expansion is the increasing willingness of younger consumers to invest in high end skincare and cosmetics as affordable indulgences. The influence of social media and beauty influencers has also accelerated this growth by educating consumers about the benefits of luxury formulations. Brands like La Mer and Sisley have successfully expanded their reach through digital channels making premium products more accessible to a broader audience. Additionally the integration of technology such as AI driven skin analysis tools in retail stores enhances the customer experience and drives conversion. The trend towards clean and sustainable beauty further boosts this segment as luxury brands reformulate products to meet ethical standards. This combination of accessibility innovation and health consciousness ensures that beauty and personal care remains the fastest growing category in the luxury sector.

By End User Insights

The women segment led the United States luxury goods market and accounted for a 60.4% share in 2026. This dominance of the segment was driven by traditional gender roles in fashion and beauty consumption as well as the increasing financial independence of female consumers. The breadth of product categories available to women including apparel accessories jewelry and beauty creates multiple touchpoints for engagement and spending. The rise of female executives and entrepreneurs has also contributed to this trend as women seek luxury items that reflect their professional status and personal style. Furthermore women are more likely to purchase luxury gifts for others expanding their impact on market volume. Brands have responded by tailoring marketing campaigns and product offerings to empower female consumers and address their specific needs. The emotional connection women often form with luxury brands fosters long term relationships and repeat purchases. This deep engagement ensures that the women’s segment remains the cornerstone of the US luxury goods market.

But the men’s segment is estimated to register the fastest CAGR of 7.2% between 2026 and 2034 owing to shifting societal norms around masculinity and the increasing interest of male consumers in fashion grooming and accessories. The driving factor behind this growth is the normalization of male engagement with beauty and fashion products which were previously considered feminine domains. The influence of male celebrities and influencers on social media has also played a crucial role in shaping trends and encouraging experimentation with luxury brands. Additionally the rise of streetwear and casual luxury has made high end fashion more approachable for men who prefer comfort and versatility. Brands like Gucci and Dior have successfully tapped into this market by launching dedicated men’s lines and marketing campaigns that resonate with modern male identities. The expansion of product ranges to include jewelry and handbags for men further diversifies spending opportunities. This cultural shift combined with targeted marketing strategies ensures that the men’s segment continues to expand at a rapid pace.

By Distribution Channel Insights

The single brand stores segment remained the largest by securing a 41.4% share of the United States luxury goods market in 2025. This prominence of the segment was supported by its ability to provide immersive brand experiences and exclusive product offerings. These flagship locations serve as physical manifestations of brand heritage and craftsmanship allowing customers to engage with products in a controlled environment. The dominance of this channel is driven by the high touch nature of luxury shopping where personalized service and immediate product availability are paramount. Single brand stores also offer exclusive items and limited editions that are not available through other channels creating a sense of urgency and exclusivity. In the United States cities like New York Los Angeles and Miami have become hubs for luxury flagship stores attracting both domestic and international shoppers. The ability of these stores to host events and launch parties further strengthens brand loyalty and community engagement. Additionally the integration of digital technologies in stores such as virtual mirrors and interactive displays enhances the shopping experience. This blend of physical presence and technological innovation ensures that single brand stores remain the preferred channel for luxury consumers seeking authenticity and prestige.

The online stores segment is anticipated to witness the fastest CAGR of 12.5% over the forecast period. This rapid expansion of the segment is propelled by the increasing comfort of consumers with digital transactions and the enhanced capabilities of e commerce platforms. The driving factor behind this trend is the convenience and accessibility offered by online channels which allow consumers to browse and purchase products from anywhere at any time. The use of artificial intelligence and data analytics enables personalized recommendations and targeted marketing which improve conversion rates. Additionally the development of secure payment systems and efficient logistics networks has reduced barriers to online luxury shopping. Younger consumers particularly Millennials and Gen Z prefer digital channels for their seamless integration with social media and mobile devices. Brands have responded by creating sophisticated websites and apps that offer virtual try ons and augmented reality experiences. The ability to reach customers beyond geographic constraints also expands market reach. This combination of technological advancement and changing consumer preferences ensures that online stores continue to grow at the fastest rate in the luxury distribution landscape.

COUNTRY ANALYSIS

The United States dominated the global luxury goods market and held a share of 25.6% in 2025. This growth of the US market was propelled by the country’s large affluent population robust consumer confidence and strong cultural influence on global fashion trends. The market status in the United States is characterized by a high degree of sophistication and maturity with consumers demanding exceptional quality service and exclusivity. The main factors behind this leadership include the concentration of high net worth individuals. The Capgemini Research Institute's World Wealth Report 2025 reveals that the U.S. high-net-worth individual (HNWI) population reached 7.9 million in 2024, a growth surge driven by robust equity market returns and economic resilience. This wealthy demographic provides a stable base for luxury spending regardless of broader economic conditions. Additionally the United States is home to major luxury retail hubs such as Fifth Avenue in New York and Rodeo Drive in Los Angeles which attract millions of tourists and shoppers annually. The cultural diversity of the US population also contributes to varied tastes and preferences driving innovation and product diversity among luxury brands. The strong intellectual property protection laws in the US also encourage brands to invest heavily in marketing and retail infrastructure. Furthermore the integration of advanced technologies in retail operations enhances the customer experience and drives efficiency. This combination of wealth infrastructure and innovation ensures that the United States remains the central pillar of the global luxury goods industry.

COMPETITIVE LANDSCAPE

The competition in the United States luxury goods market is intense and characterized by the presence of established global conglomerates alongside niche independent brands. Major players like LVMH Kering and Richemont dominate the landscape through extensive portfolios of iconic labels that cater to diverse consumer segments. These giants leverage their financial resources to secure prime retail locations and execute large scale marketing campaigns that reinforce brand prestige. Independent brands compete by offering unique designs and personalized services that appeal to consumers seeking exclusivity beyond mainstream offerings. The rise of digital channels has lowered barriers to entry allowing emerging designers to reach audiences directly through social media and e-commerce platforms. This democratization of access has increased competitive pressure on traditional houses to innovate and engage customers in new ways. Price competition is minimal as brands focus on value proposition through quality craftsmanship and heritage. However competition for talent and creative directors is fierce as companies seek visionary leaders who can drive brand relevance. The market also sees competition from the secondary sector where resale platforms challenge primary sales by offering sustainable and affordable alternatives. This dynamic environment requires constant adaptation and strategic innovation to maintain market position.

KEY MARKET PLAYERS

Some of the promising companies that are playing a dominating role in the U.S. luxury goods market include

- LVMH Moët Hennessy Louis Vuitton

- Kering SA

- Hermès International S.A.

- Chanel Limited

- Compagnie Financière Richemont S.A.

- Prada Group

- Burberry Group plc

- Giorgio Armani S.p.A.

- Ralph Lauren Corporation

- Tapestry, Inc.

- Capri Holdings Limited

- The Estée Lauder Companies Inc.

- Rolex SA

- Tiffany & Co.

- Salvatore Ferragamo S.p.A.

- Moncler S.p.A.

- Brunello Cucinelli S.p.A.

- Dolce & Gabbana S.r.l.

- Versace

- Valentino S.p.A.

Top Players in the US Luxury Goods Market

LVMH Moët Hennessy Louis Vuitton

LVMH maintains a commanding presence in the United States through its diverse portfolio of iconic brands including Louis Vuitton Dior and Tiffany and Co. The conglomerate recently invested heavily in expanding its retail footprint by opening flagship stores in key urban centers such as New York and Los Angeles. These locations serve as experiential hubs that reinforce brand heritage while integrating digital innovations to enhance customer engagement. LVMH has also focused on strengthening its supply chain resilience to ensure product availability amidst global disruptions. The company actively collaborates with local artisans and sponsors cultural events to deepen its connection with American consumers. By leveraging data analytics for personalized marketing LVMH continues to attract younger demographics who value exclusivity and authenticity. Its strategic acquisitions of emerging luxury labels further diversify its offerings and solidify its leadership position in the dynamic US market landscape.

Kering Group

Kering strengthens its position in the United States by leveraging its powerhouse brands Gucci Saint Laurent and Bottega Veneta which resonate deeply with American fashion sensibilities. The group has prioritized sustainability initiatives aligning with the growing consumer demand for ethical luxury practices in the US market. Recent actions include the launch of circular economy programs and the use of eco friendly materials across its product lines. Kering has also enhanced its digital capabilities by investing in advanced e commerce platforms and virtual reality experiences to engage tech savvy customers. The company frequently collaborates with American artists and designers to create limited edition collections that generate buzz and drive sales. By focusing on brand distinctiveness and creative excellence Kering ensures its labels remain desirable among affluent US consumers. Its commitment to transparency and social responsibility further builds trust and loyalty within the competitive American luxury sector.

Chanel Limited

Chanel operates as a privately held entity in the United States allowing it to maintain strict control over brand image and distribution strategies. The company focuses on exclusivity by limiting product availability and maintaining premium pricing which enhances perceived value among American consumers. Recent efforts include the renovation of historic flagship stores in major cities to provide immersive luxury experiences that reflect the brand’s timeless elegance. Chanel has also expanded its beauty and fragrance offerings which serve as accessible entry points for new customers in the US market. The brand actively engages in high profile cultural sponsorships and fashion shows that reinforce its status as a symbol of sophistication. By investing in artisanal craftsmanship and preserving traditional techniques Chanel appeals to consumers seeking authenticity and quality. Its strategic focus on long term brand equity rather than short term gains ensures sustained relevance and desirability in the evolving American luxury landscape.

Top Strategies Used by Key Market Participants

Key players in the United States luxury goods market employ several strategic initiatives to maintain competitiveness and drive growth. Digital transformation remains a primary focus as brands invest in e commerce platforms and omnichannel experiences to reach wider audiences. Companies leverage artificial intelligence and data analytics to personalize customer interactions and optimize inventory management. Sustainability has become a core strategy with firms adopting eco friendly materials and transparent supply chains to appeal to conscious consumers. Brand heritage preservation is another critical approach where companies emphasize craftsmanship and storytelling to differentiate themselves. Strategic partnerships with influencers and celebrities help brands connect with younger demographics and generate social media buzz. Expansion into secondary markets through outlet stores and resale platforms allows companies to capture value from pre owned items. Additionally firms focus on exclusive product launches and limited editions to create urgency and maintain high demand. These strategies collectively enable luxury brands to adapt to changing consumer preferences while preserving their elite status in the competitive American market environment.

MARKET SEGMENTATION

This research report on the U.S. luxury goods market has been segmented based on the following categories.

By Product Type

- Clothing and Apparel

- Footwear

- Leather Goods (Bags and Small Leather Accessories)

- Jewelry

- Watches

- Beauty and Personal Care (Fragrances, Cosmetics, Skincare)

- Eyewear

- Home Décor and Fine Living Items

By End User

- Women

- Men

- Unisex

By Distribution Channel

- Single Brand Stores

- Multi-Brand Stores

- Online Stores

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com