U.S. Mini Fridge Market Size, Share, Trends, and Growth Analysis Report, Segmented by Type, Technology, Distribution Channel, and Country – Industry Forecast From 2026 to 2034

U.S. Mini Fridge Market Report Summary

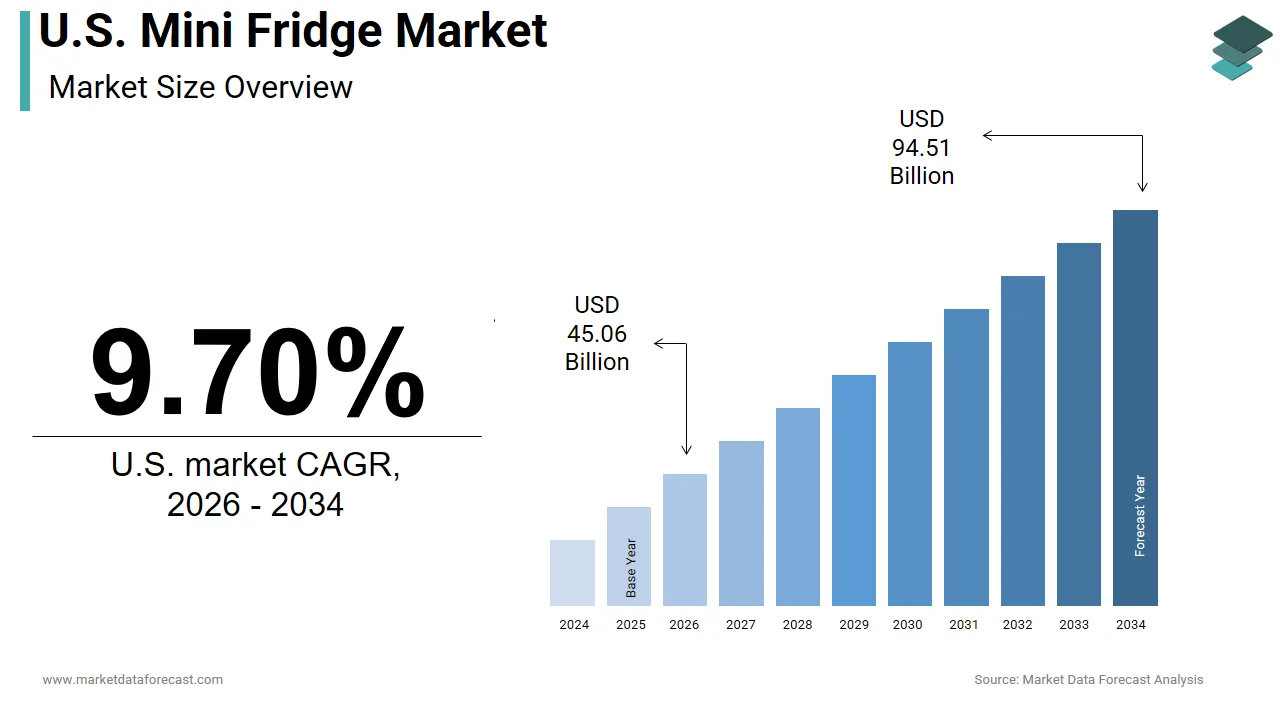

The U.S. mini fridge market was valued at USD 41.08 billion in 2025 and is projected to grow from USD 45.06 billion in 2026 to USD 94.51 billion by 2034, registering a CAGR of 9.70% from 2026 to 2034. Market growth is driven by increasing demand for compact refrigeration solutions, rising urbanization, and growing adoption of space-saving appliances across residential and commercial environments. Mini fridges are widely used in dormitories, offices, hotels, recreational spaces, and small apartments due to their portability, convenience, and energy efficiency. Increasing consumer preference for smart appliances, expansion of e-commerce retail channels, and rising demand for premium compact cooling solutions are further supporting market expansion across the United States.

Key Market Trends

- Rising demand for compact and space-saving refrigeration appliances.

- Increasing adoption of energy-efficient and smart mini fridges.

- Growing popularity of portable cooling solutions for dormitories and offices.

- Expansion of online retail channels for home appliance purchases.

- Increasing focus on premium designs and multifunctional compact refrigerators.

Segmental Insights

- Based on type, the cube mini fridge segment dominated the U.S. mini fridge market in 2025 by accounting for 51.9% market share, driven by affordability, compact size, and strong suitability for small living spaces such as dorm rooms and studio apartments.

- Based on technology, the compressor technology segment led the market by capturing 46.8% share in 2025, supported by superior cooling performance, energy efficiency, and the ability to maintain stable temperatures across varying environmental conditions.

- Based on distribution channel, the online retail segment held a significant share of the market in 2025, driven by consumer convenience, broad product availability, competitive pricing, and increasing adoption of e-commerce platforms for appliance purchases.

Regional Insights

- The United States continues to witness strong demand for mini fridges due to rising urban housing trends, increasing student populations, and expanding use of compact appliances in hospitality and commercial settings. Growing preference for energy-efficient appliances and smart home integration is further contributing to long-term market growth across the country.

Competitive Landscape

The U.S. mini fridge market is characterized by strong competition among global appliance manufacturers and home electronics companies focusing on energy-efficient technologies, compact product innovation, and smart cooling solutions. Market participants are emphasizing product customization, premium aesthetics, and expansion of online distribution networks to strengthen market positioning. Strategic partnerships, new product launches, and investments in energy-saving refrigeration technologies are shaping competitive dynamics across the market.

Prominent companies operating in the U.S. mini fridge market include Stanley Black & Decker, Inc., Viking Range, LLC, Midea Group, Samsung, Whirlpool Corporation, WHYNTER LLC, BSH Hausgeräte GmbH, Hisense, Haier Group Corporation, and Electrolux AB.

U.S. Mini Fridge Market Size

The size of the U.S. mini fridge market was worth USD 41.08 billion in 2025. The market is anticipated to grow at a CAGR of 9.70% from 2026 to 2034 and be worth USD 94.51 billion by 2034 from USD 45.06 billion in 2026.

The mini fridge is for personal use in limited spaces, such as dormitories, offices, bedrooms, and recreational vehicles. These units typically range from 1.7 to 4.5 cubic feet in capacity and serve as supplementary cooling solutions alongside primary household refrigerators. According to the National Center for Education Statistics, approximately 19.5 million students were enrolled in degree-granting postsecondary institutions in the fall of 2022, creating a substantial base of potential consumers residing in campus housing where shared kitchen facilities are common. Furthermore, the shift towards remote work has altered residential dynamics, with many individuals repurposing living spaces for professional use. The rise of single-person households also contributes significantly to this sector. Additionally, the popularity of gaming rooms and home entertainment centers has spurred demand for specialized mini fridges capable of storing snacks and drinks within easy reach. Manufacturers are responding by integrating smart features and aesthetic designs that appeal to younger demographics.

MARKET DRIVERS

Surge in Higher Education Enrollment and Student Housing Demand

The continuous growth in higher education enrollment and student housing demand is positively impacting the growth of the United States mini fridge market. Most university dormitories and off-campus student housing units do not provide full-sized kitchens or refrigerators in individual rooms, necessitating the purchase of compact cooling appliances. The total enrollment in postsecondary institutions is projected to remain robust, with millions of students residing on or near campus each academic year. This consistent influx of new students creates a recurring demand cycle for mini fridges as each incoming class requires essential furnishings for their living spaces. The National Apartment Association notes that student housing developments are increasingly designed with micro living spaces in mind, further cementing the need for space-saving appliances. Parents and students often view mini fridges as essential items for storing meals, snacks, and beverages, reducing reliance on expensive campus dining plans. The durability and energy efficiency of these units are key purchasing factors as students seek reliable options that last throughout their academic tenure.

Expansion of Remote Work and Home Office Infrastructure

The widespread adoption of remote work has fundamentally changed home environments is also enhancing the growth of the United States mini fridge market. As professionals spend more time working from home, the desire for convenient access to refreshments without leaving the workspace has increased. This shift has led to the renovation of spare rooms and living areas into functional offices where a full-sized refrigerator is impractical due to space constraints. The Society for Human Resource Management reports that employee well-being and ergonomic home setups are becoming priorities for employers, who sometimes provide stipends for home office equipment, including appliances. Additionally, the rise of content creators and streamers who operate from home studios has created a niche market for aesthetically pleasing and quiet-running units that do not interfere with audio recording. These users often prefer retro or sleek designs that complement their video backgrounds. The integration of smart technology, such as temperature control via mobile apps,, appeals to tech-savvy remote workers.

MARKET RESTRAINTS

Stringent Energy Efficiency Regulations and Compliance Costs

The stringent energy efficiency regulations imposed by federal and state authorities, thereby increasing manufacturing costs and limiting design flexibility, are limiting the growth of the United States mini fridge market. The Department of Energy has implemented rigorous standards for refrigeration products to reduce overall energy consumption and environmental impact. Compliance with these regulations often necessitates the use of advanced compressors, better insulation materials, and sophisticated control systems, which raise production costs. These increased costs are frequently passed on to consumers, making mini fridges more expensive and potentially dampening demand among price-sensitive segments such as students. Small manufacturers may struggle to absorb these costs or invest in the necessary research and development to meet the new standards, leading to market consolidation. The California Energy Commission also enforces additional state-specific requirements that are often more stringent than federal laws, creating complexity for national distribution. Manufacturers must navigate a patchwork of regulations that increase administrative burdens and supply chain complexities. Furthermore, the push for eco-friendly refrigerants such as hydrocarbons requires redesigning internal components to ensure safety and performance. While these regulations benefit the environment in the long term, they pose short-term challenges to market growth by raising entry barriers and retail prices.

Limited Storage Capacity and Functional Limitations

The inherent limitation of storage capacity in mini fridges restricts their utility and prevents them from replacing primary refrigeration units for many households. The limited storage capacity and functional limitations are additionally inhibiting the growth of the United States mini fridge market. Most mini fridges offer between 1.7 and 4.5 cubic feet of space, which is insufficient for storing fresh produce, meats, and dairy products for more than a few days. This functional constraint limits the target audience primarily to individuals with minimal food storage needs or those using the unit as a secondary appliance. The absence of advanced features, such as ice makers, water dispensers, and precise humidity controls, further reduces their appeal compared to full-sized models. Many consumers view mini fridges as temporary solutions rather than long-term investments, leading to lower brand loyalty and higher replacement rates. Additionally, the small evaporator coils in these units can lead to uneven cooling and frost buildup, requiring frequent manual defrosting, which inconveniences users. These operational drawbacks discourage broader adoption among general households. While niche markets such as gamers and office workers appreciate the convenience, they represent a fraction of the total appliance market.

MARKET OPPORTUNITIES

Integration of Smart Technology and IoT Connectivity

The integration of smart technology and Internet of Things connectivity is solely to contribute to new opportunities for the growth of the United States mini fridge market. Modern consumers increasingly seek connected appliances that offer convenience and control through smartphone applications. The sales of smart home devices continue to grow, with users expecting seamless integration across their digital ecosystems. Mini fridges equipped with Wi-Fi capabilities allow users to monitor internal temperatures, adjust settings remotely, and receive alerts for door openings or maintenance needs. This feature is particularly appealing to parents monitoring college students' usage or office managers ensuring inventory levels. Some advanced models include interior cameras that enable users to check contents while shopping, reducing food waste and improving convenience. The adoption of voice assistant compatibility with platforms like Amazon, Alexa, and Google Assistant enhances user experience by allowing hands-free operation. Manufacturers can leverage these technologies to command premium prices and attract tech-savvy demographics, such as young professionals and gamers. The willingness to pay for smart home features is highest among millennials and Gen Z consumers, who form the core demographic for mini fridges. Additionally, smart diagnostics can predict maintenance issues, extending product lifespan and improving customer satisfaction. Data collected from connected devices can also provide manufacturers with valuable insights into usage patterns, enabling better product development and targeted marketing.

Growth in Personalized and Aesthetic Design Trends

The growing emphasis on personalized and aesthetic design to enhance brand appeal is also a primary factor to fuel the growth of the United States mini fridge market. Consumers increasingly view appliances as extensions of their personal style, particularly in visible spaces like living rooms, offices, and gaming setups. Manufacturers can capitalize on this trend by offering mini fridges in a variety of colors, finishes, and styles, including vintage, retro modern, minimalist, and themed designs. Collaborations with popular franchise artists and influencers can create limited edition models that generate buzz and drive sales among dedicated fan bases. The gaming community represents a particularly attractive segment with users seeking fridges that match their setup aesthetics, such as RGB lighting and branded exteriors. Customizable panels and interchangeable doors allow users to personalize their units further, fostering emotional connection and brand loyalty. Retailers can also offer bundling options with accessories, such as cup holders, openers, and LED lights to enhance the overall appeal.

MARKET CHALLENGES

Supply Chain Disruptions and Raw Material Volatility

The supply chain disruptions and volatility in raw material prices are one of the major challenges for the growth of the United States mini fridge market. The production of refrigeration appliances relies heavily on steel, aluminum, copper, and plastics, all of which have experienced fluctuating costs due to global economic uncertainties. The Producer Price Index for metal and metal products has shown considerable variability, impacting manufacturing expenses. These cost fluctuations make it difficult for manufacturers to maintain consistent pricing strategies and profit margins. Additionally, logistical bottlenecks such as port congestion and shipping container shortages have delayed the delivery of components and finished goods. The supply chain inconsistencies continue to affect inventory levels and lead times for consumer electronics and appliances. These delays can result in stockouts during peak demand periods, such as the back-to-school season, leading to lost sales opportunities. Manufacturers must also navigate geopolitical tensions and trade policies that affect the sourcing of components like semiconductors used in smart mini fridges. The shortage of chips has previously impacted the production of connected appliances, forcing companies to scale back features or delay launches. Furthermore, labor shortages in the manufacturing and transportation sectors exacerbate these issues, increasing operational costs. However, these adaptations require significant capital investment and strategic planning.

Environmental Concerns and Refrigerant Phase Downs

The environmental concerns regarding refrigerants and the phase-down of hydrofluorocarbons are another factor contributing to the decline in the growth of the United States mini fridge market in the coming years. Traditional refrigerants, such as HFC 134a, contribute to global warming, prompting regulatory bodies to mandate a transition to climate-friendly alternatives. According to the Environmental Protection Agency, the American Innovation and Manufacturing Act aims to reduce the production and consumption of HFCs by 85% over the next 15 years. This transition requires manufacturers to redesign cooling systems to accommodate new refrigerants, such as hydrocarbons, which are flammable and require enhanced safety measures. Implementing these changes involves substantial research and development costs as well as retooling of production facilities. Consumers may also exhibit hesitation towards new refrigerant technologies due to safety perceptions, despite their environmental benefits. The International Institute of Refrigeration notes that the shift to natural refrigerants requires strict adherence to safety standards to prevent fire hazards. Additionally, the disposal of old mini fridges poses environmental challenges as improper handling can release harmful substances into the atmosphere. Recycling programs are not uniformly available across all states, leading to inconsistent compliance and environmental impact. Manufacturers must also educate consumers on the benefits of eco-friendly models to overcome resistance to change. Failure to adapt quickly to these regulatory requirements can result in penalties and loss of access. Balancing environmental responsibility with cost effectiveness and consumer safety remains a delicate task.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Technology, Distribution Channel, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled |

|

SEGMENTAL ANALYSIS

By Type Insights

The cube mini fridge segment was the largest by holding 51.9% of the United States mini fridge market share in 2025, with its affordability, compact size, and suitability for small living spaces. These units typically range from 1.7 to 2.5 cubic feet, making them ideal for dorm rooms, office cubicles, and small apartments where floor space is at a premium. This large student population creates consistent annual demand for entry-level cooling solutions that fit within strict dimensional limits imposed by university housing policies. The low price point of cube fridges, which often ranges from 80 to 150 dollars, makes them accessible to budget-conscious consumers, such as students and young professionals. Retailers frequently promote these units during back-to-school seasons, further boosting their visibility and sales volume. The simplicity of design in cube fridges also appeals to users who require basic cooling without advanced features. Cube fridges meet this need by providing sufficient storage for beverages and snacks without occupying valuable living area. Their lightweight nature facilitates easy transport and relocation, which is beneficial for renters and students who move frequently. The widespread availability of cube fridges across various retail channels ensures that they remain the go-to choice for first-time buyers and those seeking supplemental cooling.

The under-the-counter mini fridge segment is expected to grow at the fastest CAGR of 11.2% from 2026 to 2034, with the rising trend of home renovation and integrated kitchen designs. Consumers are increasingly seeking seamless aesthetics in their living spaces, leading to the adoption of built-in appliances that blend with cabinetry. The remodeling spending in the United States reached record highs in recent years, with homeowners investing heavily in kitchen upgrades that prioritize functionality and style. Under-counter fridges offer a sophisticated solution for storing wine, beverages, and perishables without disrupting the visual flow of the kitchen or entertainment area. The growing popularity of home bars and entertainment zones has further fueled demand for these specialized units. As per the Wine Institute, wine consumption in the US remains robust, with many households installing dedicated wine coolers that often fall under the counter category. These units feature advanced temperature control zones and quiet operation, making them suitable for open-plan living areas. Manufacturers are responding by offering customizable panel-ready options that allow the fridge to match existing cabinet finishes. The increase in disposable income among middle and upper-class households enables investment in premium appliances that enhance home value. Additionally, the rise of smart home integration allows these fridges to connect with home automation systems, appealing to tech-savvy homeowners. The shift towards indoor entertaining post-pandemic has also accelerated the adoption of under-the-counter units for convenient guest service.

By Technology Insights

The compressor technology segment was the largest by accounting for 46.8% of the United States mini fridge market share in 2025 due to its superior cooling performance, energy efficiency, and ability to maintain consistent temperatures in varying ambient conditions. The compressor-based refrigeration remains the most efficient method for household cooling applications for the majority of Energy Star-certified appliances. This efficiency is important for consumers who operate mini fridges continuously, leading to lower electricity bills and reduced environmental impact. The reliability of compressor technology ensures a longer lifespan for the appliance, which is a key consideration for buyers seeking long-term value. As per the Appliance Magazine, compressor units are preferred in warmer climates where ambient temperatures can exceed 80 degrees Fahrenheit, as they maintain internal cooling effectiveness better than alternative technologies. Furthermore, advancements in inverter compressor technology have reduced noise levels, addressing a common consumer complaint associated with traditional models. The widespread manufacturing infrastructure for compressors allows for economies of scale, keeping production costs competitive. Most major brands prioritize compressor technology for their mid-sized and cube models, ensuring broad market availability. The ability of compressor fridges to function effectively in unconditioned spaces such as garages and offices further enhances their utility.

The thermoelectric technology segment is growing at the fastest CAGR of 7.8% during the forecast period. Thermoelectric coolers use the Peltier effect to transfer heat, eliminating the need for compressors and refrigerants, which results in completely vibration-free and quiet performance. The demand for quiet home office appliances has surged, as remote workers seek to minimize distractions in their work environments. Thermoelectric mini fridges are ideal for bedrooms, nurseries, and studios, where noise sensitivity is high. Additionally, the absence of harmful refrigerants aligns with growing consumer preference for sustainable products. The Environmental Protection Agency highlights the benefits of reducing hydrofluorocarbon usage, encouraging the adoption of alternative cooling methods. Thermoelectric units are also lighter and more compact, making them popular for portable applications such as car travel and outdoor activities. The rise in recreational vehicle ownership and camping trends has boosted demand for portable cooling solutions that can run on direct current power. Although thermoelectric fridges have limited cooling capacity compared to compressor models, their niche advantages in specific use cases drive their rapid adoption. Manufacturers are improving the efficiency of thermoelectric modules through better heat sink designs and insulation materials.

By Distribution Channel Insights

The online retail segment held a significant share of the United States mini fridge market in 2025 by convenience extensive product selection and competitive pricing. Consumers prefer purchasing appliances online due to the ability to compare features, read reviews, and find the best deals without visiting multiple physical stores. Major platforms, such as Amazon, Best Buy, and Walmart, offer vast inventories of mini fridges from various brands by allowing consumers to find specific sizes, styles, and features easily. The availability of detailed product descriptions and customer feedback helps buyers make informed decisions by reducing the perceived risk of online purchasing. Home delivery services eliminate the logistical challenge of transporting bulky items, which is particularly appealing to students and urban residents without vehicles. Retailers have invested heavily in logistics and last-mile delivery capabilities, ensuring faster and more reliable shipping options. Promotional events such as Prime Day and Black Friday further drive online sales through significant discounts and bundled offers. The integration of augmented reality tools on some platforms allows users to visualize how a mini fridge will fit in their space, enhancing confidence in purchase decisions. The ease of return policies offered by major online retailers also mitigates concerns about product suitability.

The specialty stores segment is expected to grow at the fastest CAGR of 8.1% from 2026 to 2034 due to the increasing demand for premium, customized, and high-end models. These stores include dedicated appliance showrooms, home decor boutiques, and specialty electronics retailers that offer curated selections and expert advice. The consumers are increasingly visiting specialty showrooms to select appliances that match specific design aesthetics and functional requirements for custom home projects. Specialty stores provide a tactile shopping experience where customers can assess build quality, finish, and noise levels before purchasing, which is crucial for high-end under-the-counter and retro-styled units. The rise of interior design consciousness has led consumers to seek unique appliances that serve as statement pieces rather than purely functional items. Staff expertise in these stores helps customers navigate complex features, such as dual zone cooling and smart connectivity, ensuring satisfaction with premium purchases. Additionally, specialty stores often offer white-glove delivery and installation services, which appeal to affluent buyers seeking convenience. The ability to order custom panels and finishes exclusively through specialty channels further differentiates this segment.

COMPETITIVE LANDSCAPE

The competition in the United States mini fridge market is intense and characterized by the presence of established global appliance manufacturers alongside specialized niche brands. Major players compete based on product innovation, price affordability, and brand reputation while striving to differentiate through design and technology. Price competition is particularly fierce in the entry-level cube segment, where margins are thin and volume is high. The premium under-counter segment competes on features such as dual zone cooling and custom panel readiness. Retailers play an important role in shaping competitive dynamics by offering exclusive models and promotional bundles during peak seasons like back-to-school. Online platforms have lowered barriers to entry, allowing smaller brands to gain visibility through targeted digital marketing. Supply chain efficiency and inventory management are critical competitive advantages that determine the ability to meet seasonal demand spikes. Companies also compete on sustainability credentials, with Energy Star ratings becoming a key decision factor for consumers.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. mini fridge market include

- Stanley Black & Decker, Inc. (U.S.)

- Viking Range, LLC (U.S.)

- Midea Group

- SAMSUNG

- Whirlpool Corporation (U.S.)

- WHYNTER LLC (U.S.)

- BSH Hausgeräte GmbH

- Hisense

- Haier Group Corporation

- Electrolux AB

TOP PLAYERS IN THE MARKET

- Haier maintains a robust presence in the United States mini fridge market through its diverse portfolio of compact refrigeration solutions under brands such as Haier and GE Appliances. The company focuses on innovation by integrating smart technology and energy-efficient compressors into its cube and under-counter models. Haier actively collaborates with university housing providers to offer tailored solutions that meet specific dormitory requirements. The company also invests in sustainable design practices, ensuring compliance with stringent environmental regulations. Their strategic emphasis on direct-to-consumer sales channels further strengthens brand visibility and customer engagement in the competitive US appliance landscape.

- Midea is a key contributor to the United States mini fridge market, offering a wide range of compact cooling appliances known for reliability and affordability. The company serves various segments, including student housing offices and recreational vehicles, through partnerships with major retailers and online platforms. The company focuses on developing Energy Star-certified products that align with consumer preferences for cost-effective and eco-friendly appliances. Midea also engages in original equipment manufacturing for several prominent American brands, thereby expanding its indirect market reach. Recent investments in automated production facilities have improved product quality and consistency.

- Whirlpool Corporation plays a significant role in the United States mini fridge market by delivering high-quality compact refrigeration units under its flagship brand and others like Amana. The company leverages its extensive retail relationships and service network to ensure widespread availability and customer support. Whirlpool has recently focused on integrating smart home capabilities into its mini fridge lineup, allowing users to monitor temperature and receive maintenance alerts via mobile applications. The corporation emphasizes durability and performance, catering to consumers who view mini fridges as long-term investments. Recent initiatives include launching retro-styled models that appeal to design-conscious buyers seeking aesthetic differentiation. Whirlpool also prioritizes sustainability by using recyclable materials and energy-efficient technologies in its manufacturing processes.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States mini fridge market primarily employ product differentiation strategies by introducing smart features and unique aesthetic designs to appeal to diverse consumer segments. Companies focus on energy efficiency to comply with regulatory standards and attract environmentally conscious buyers. Strategic partnerships with universities and property management firms help secure bulk contracts for student housing and apartment complexes. Manufacturers also expand their online presence through direct-to-consumer platforms and collaborations with major e-commerce retailers to enhance accessibility. Investment in supply chain localization reduces dependency on imports and mitigates logistical risks. Brands leverage social media marketing and influencer collaborations to target younger demographics, such as students and gamers. Continuous innovation in cooling technology ensures quieter operation and better temperature control.

MARKET SEGMENTATION

This research report on the U.S. mini fridge market has been segmented and sub-segmented into the following categories.

By Type

- Portable

- Residential

- Commercial

- Cube

- Residential

- Commercial

- Mid-sized

- Residential

- Commercial

- Under-the-Counter

- Residential

- Commercial

By Technology

- Compressor

- Absorption

- Thermoelectric

By Distribution Channel

- Specialty Stores

- Hypermarkets

- Online

- Others

By Country

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

What is the U.S. mini fridge market?

The U.S. mini fridge market includes compact refrigerators designed for personal use in dorms, offices, bedrooms, and small spaces, offering portable cooling solutions across the United States.

Why is the U.S. mini fridge market growing?

The U.S. mini fridge market is growing due to urbanization, demand for space-saving appliances, rising student populations, remote work trends, and consumer preference for convenience and energy efficiency.

Who buys mini fridges from the U.S. mini fridge market?

Students, renters, office workers, travelers, seniors, and small business owners purchase from the U.S. mini fridge market for dorms, offices, bedrooms, hotels, and compact living spaces.

What types of mini fridges are in the U.S. mini fridge market?

The U.S. mini fridge market includes freestanding fridges, under-counter models, thermoelectric coolers, compressor-based units, beverage centers, and compact refrigerators with freezers for personal use.

How does space-saving design impact the U.S. mini fridge market?

Space-saving design drives the U.S. mini fridge market as urban consumers seek compact appliances for small apartments, dorm rooms, offices, and limited kitchen space without sacrificing cooling performance.

What challenges face the U.S. mini fridge market?

Challenges in the U.S. mini fridge market include energy efficiency regulations, competition from full-size refrigerators, quality concerns with budget models, and limited storage capacity for larger households.

Which demographic uses the U.S. mini fridge market most?

College students, young professionals, renters, and seniors represent the largest demographics in the U.S. mini fridge market due to their need for compact, affordable cooling solutions.

How does energy efficiency affect the U.S. mini fridge market?

Energy efficiency shapes the U.S. mini fridge market through demand for Energy Star-rated models, lower electricity consumption, eco-friendly refrigerants, and cost-saving long-term operating expenses.

What role does portability play in the U.S. mini fridge market?

Portability is central to the U.S. mini fridge market, offering lightweight designs, easy mobility, compact dimensions, and flexibility for use in dorms, offices, RVs, and hotel rooms.

Is the U.S. mini fridge market competitive?

Yes, the U.S. mini fridge market is highly competitive with major appliance brands, budget manufacturers, private label products, feature innovation, and pricing strategies targeting diverse consumer segments.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com