U.S. Office Supplies Market Size, Share, Trends & Growth Forecast Report Segmented By Product Type (Computer and Printer Supplies, Desk Accessories), Application and Country – Industry Analysis From 2026 to 2034

U.S. Office Supplies Market Report Summary

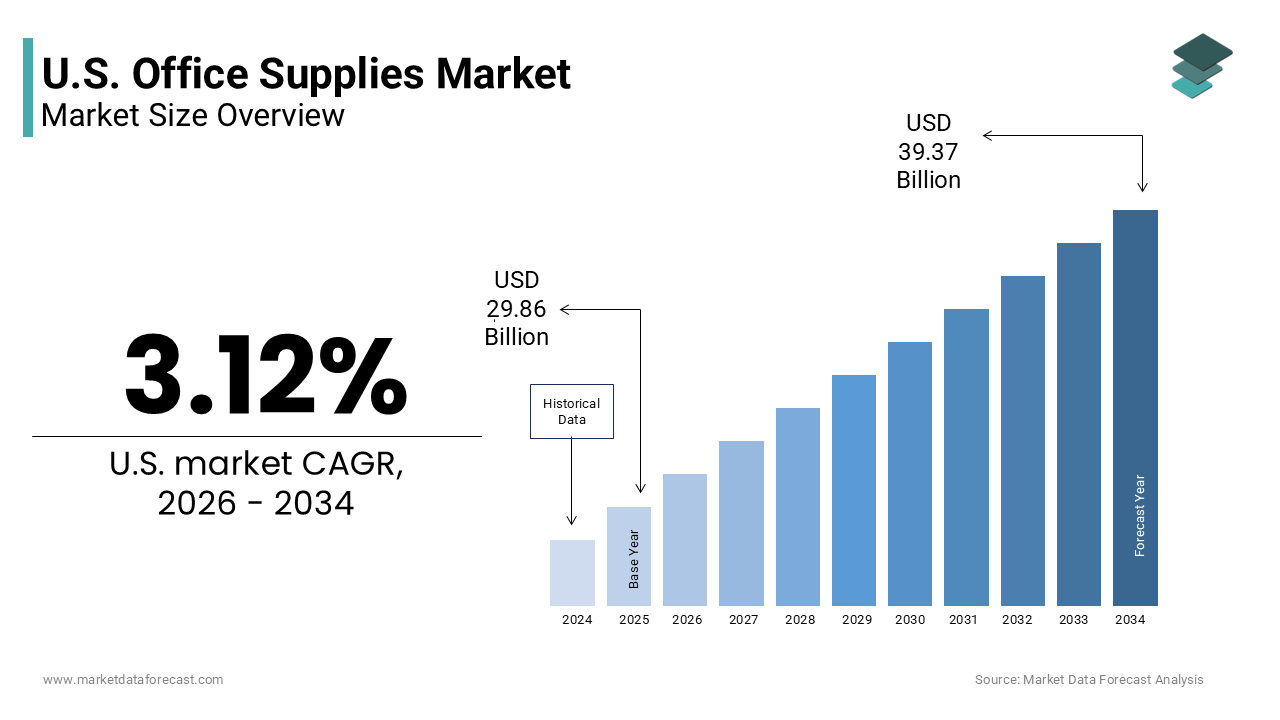

The U.S. office supplies market was valued at USD 29.86 billion in 2025, is estimated to reach USD 30.79 billion in 2026, and is projected to reach USD 39.37 billion by 2034, growing at a CAGR of 3.12% during the forecast period from 2026 to 2034. The growth of the U.S. office supplies market is driven by the expansion of hybrid work models, increasing number of remote workers, and rising formation of small businesses across the country. Growing demand for ergonomic office accessories, digital-compatible office products, and efficient workspace organization solutions is further accelerating market growth. Moreover, increasing adoption of sustainable office supplies, integration of smart technologies into office accessories, and rising investments in home office setups are supporting the expansion of the U.S. office supplies market.

Key Market Trends

- Rising demand for ergonomic desk accessories and workspace optimization products driven by the expansion of hybrid and remote work environments.

- Growing popularity of sustainable and eco-friendly office supplies made from recycled and biodegradable materials.

- Increasing integration of smart technologies such as digital notebooks and connected office accessories into modern workspaces.

- Strong focus on omnichannel retailing and e-commerce expansion by office supply companies to improve customer convenience.

- Expansion of home office product categories supported by the increasing number of freelancers, entrepreneurs, and gig economy workers.

Segmental Insights

- Based on product type, the computer and printer supplies segment dominated the U.S. office supplies market and held the largest share in 2025. The segment’s dominance is attributed to the continued reliance on printing and computing infrastructure across enterprises, educational institutions, and home office environments, along with recurring demand for ink cartridges, toner, paper, and related accessories.

- The ergonomic desk accessories segment is projected to witness the fastest CAGR during the forecast period owing to increasing awareness regarding workplace health, growing demand for comfortable home office setups, and rising adoption of productivity-enhancing workspace solutions.

- Based on application, the enterprise sector segment accounted for the leading share of the U.S. office supplies market in 2025. The dominance of this segment is driven by large-scale procurement activities by corporations, government agencies, and educational institutions requiring office essentials for administrative operations and employee productivity.

- The household segment is anticipated to register notable growth during the forecast period due to the permanent shift toward remote and hybrid work models, increasing freelance workforce participation, and rising consumer spending on personalized home office environments.

Regional Insights

The United States dominated the North American office supplies market and accounted for a major share in 2025, supported by its extensive corporate infrastructure, high literacy rates, and widespread adoption of advanced workplace technologies. California remains a major contributor to the U.S. office supplies market due to its large technology workforce, strong startup ecosystem, and increasing adoption of hybrid work arrangements. New York, Washington, and Oregon are also witnessing notable growth driven by rising demand for home office products, increasing number of remote workers, and expanding small business activities.

Competitive Landscape

The U.S. office supplies market is highly competitive and characterized by the presence of established retail giants, e-commerce leaders, and specialized office supply manufacturers competing through pricing strategies, product innovation, sustainability initiatives, and omnichannel retail expansion. Leading companies are focusing on enhancing digital procurement platforms, expanding private label product portfolios, strengthening supply chain operations, and investing in eco-friendly office solutions. Strategic partnerships, same-day delivery services, and integration of smart office technologies are further strengthening market positioning across enterprise and household customer segments. Prominent players in the U.S. office supplies market include Staples Inc., Office Depot LLC, 3M Company, ACCO Brands Corporation, Newell Brands Inc., HP Inc., Canon Inc., Brother Industries, Ltd., The ODP Corporation, and Avery Dennison Corporation.

U.S. Office Supplies Market Size

The U.S. office supplies market size was valued at USD 29.86 billion in 2025 and is anticipated to reach USD 30.79 billion in 2026 from USD 39.37 billion by 2034, growing at a CAGR of 3.12% during the forecast period from 2026 to 2034.

Office supplies are a broad spectrum of products essential for administrative operations including writing instruments paper products desk accessories filing systems and technological peripherals. This sector serves both corporate entities and individual consumers who require tools for productivity and organization in physical and hybrid work environments. The definition of office supplies has expanded beyond traditional stationery to include ergonomic equipment and digital integration tools that support modern workflows. In 2025, the number of remote workers in the United States was projected to reach 32.6 million, representing approximately 22% of the workforce, according to Upwork (estimates for late 2025 show this number rising to 36.9 million). This shift has fundamentally altered consumption patterns with households becoming significant purchasers of office essentials. According to the Bureau of Labor Statistics, real average weekly earnings for private sector employees increased by 0.8% to 1.5% in 2025, while nominal average hourly earnings rose by approximately 3.5%, influencing discretionary spending. The Small Business Administration states that there are approximately 36.2 million small businesses in the United States in 2025, accounting for 99.9% of all US businesses. These enterprises drive consistent demand for cost effective and efficient supply solutions. The market is characterized by a transition from bulk corporate procurement to fragmented individual purchases. Consumers prioritize sustainability and functionality leading to a rise in eco friendly product offerings. The integration of smart technology into everyday office items further redefines the category. As work boundaries blur the distinction between personal and professional supplies diminishes creating a unified demand landscape. This evolution requires suppliers to adapt their product lines to meet diverse and changing needs.

MARKET DRIVERS

Expansion of Hybrid Work Models Sustains Demand

The widespread adoption of hybrid work models is the main reason for the growth of the United States office supplies market. This creates dual demand channels in both corporate offices and home environments. Employees splitting time between locations require duplicate sets of essential items such as notebooks pens and organizational tools. According to Gallup data reported in early 2025, 53% of U.S. workers with remote-capable jobs were working in a hybrid arrangement, while 55% were working hybrid by late 2024. This structural change ensures steady consumption levels as individuals maintain fully equipped home workspaces. The Bureau of Labor Statistics reported that 23.3% of employed persons did some work from home for pay in late 2024, while 33% worked from home on an average workday according to the American Time Use Survey. This trend drives sales of ergonomic accessories and desktop organizers that enhance productivity in limited spaces. Companies are also investing in office upgrades to attract employees back to physical locations leading to renewed corporate purchasing. A 2018 study by the International Workplace Group found that 70% of professionals worked remotely at least one day a week. However, 2025 reports indicate that 70% of hybrid workers now report reduced stress and improved health due to flexible arrangements. The need for seamless collaboration across locations boosts demand for high quality writing and presentation materials. Suppliers benefit from this sustained demand as consumers replace worn items and upgrade their setups. The hybrid model thus creates a resilient base for market growth that is less susceptible to economic downturns than purely corporate driven sectors.

Growth in Small Business Formation Increases Procurement Volume

The continuous formation of new small businesses in the country significantly drives the United States office supplies market. This generates fresh demand for startup essentials and operational materials. Entrepreneurs launching ventures require initial stockpiles of stationery filing cabinets and printing supplies to establish functional workspaces. The Census Bureau reports that business applications reached 4.4 million in 2020 (a then-record), but activity has since increased, with approximately 5.2 million applications filed in 2024. Each new entity represents a potential customer for office supply retailers contributing to market expansion. These businesses often prioritize cost effective solutions leading to increased volume sales of basic supplies. According to recent SBA and Census Bureau data, small businesses employ 45.9% of the private workforce (down slightly from the historically cited 46.4%), continuing to highlight their substantial economic footprint. As these companies grow their supply needs evolve from basic items to more specialized organizational tools. The rise of freelance and gig economy workers further amplifies this driver as independent contractors purchase supplies for their home offices. Data from Upwork’s Freelance Forward study shows that 64 million Americans performed freelance work in 2023 (an all-time high), representing 38% of the U.S. workforce. This demographic values efficiency and quality driving demand for premium yet affordable products. The steady influx of new businesses ensures a constant stream of new customers for office supply vendors. This driver supports market stability and growth despite fluctuations in larger corporate spending.

MARKET RESTRAINTS

Digitalization and Paperless Initiatives Reduce Traditional Product Sales

The accelerating shift towards digital documentation and paperless office practices is hindering the expansion of the United States office supplies market. This diminishes the need for traditional paper based products. Organizations increasingly adopt cloud storage and electronic signature platforms reducing reliance on physical files and printing materials. According to Adobe, the pandemic caused an astronomical jump in digital adoption, with digital becoming the primary way to do business. This trend directly impacts sales of copy paper folders and binders which historically constituted a large portion of market revenue. The Environmental Protection Agency states that the US generated 67.4 million tons of paper and paperboard waste in 2018, with a recycling rate of 68.2%. Companies implement digital workflows to enhance efficiency and reduce storage costs further limiting demand for physical supplies. This shift reduces the frequency of replenishment purchases for basic office items. While some niche markets remain the broader trend favors digital solutions over traditional stationery. Suppliers face pressure to innovate and offer digital compatible products or risk losing market share. This restraint challenges the core business model of many traditional office supply manufacturers.

Price Volatility of Raw Materials Impacts Profit Margins

Fluctuations in the prices of raw materials such as wood pulp plastic and metal constrain the United States office supplies market. This increases production costs and squeezes profit margins. Manufacturers face uncertainty in sourcing essential inputs leading to inconsistent pricing strategies and potential supply disruptions. According to the Producer Price Index, prices for packaging and paper products saw increases in 2025, with some estimates showing a 2.6% to 7% rise, rather than 8.5%. For instance, the index for final demand moved up 2.7% to 3.3% over the year. Plastic resins used in pens and organizers also experienced volatility due to global oil price fluctuations impacting manufacturing expenses. The National Association of Manufacturers Q2 2025 Survey reports that 85% of manufacturers prioritized digital transformation, while supply chain issues remained a challenge. These increased costs are often passed on to consumers resulting in higher retail prices that may dampen demand. Small businesses and individual consumers are particularly sensitive to price changes leading them to seek cheaper alternatives or reduce purchases. Data from the Bureau of Labor Statistics shows that the consumer price index for household furnishings and operations rose by approximately 3.4% to 4.0% in 2025. This economic environment forces suppliers to balance cost recovery with competitive pricing. The unpredictability of raw material markets makes long term planning difficult for manufacturers. This restraint limits the ability of companies to invest in innovation and expansion.

MARKET OPPORTUNITIES

Sustainable and Eco Friendly Product Lines Attract Conscious Consumers

The growing consumer preference for sustainable and environmentally friendly office supplies sets the stage for the United States market. This aligns product offerings with ethical values. Buyers increasingly seek items made from recycled materials biodegradable components and sustainable sourcing practices. Manufacturers can capitalize on this demand by introducing product lines featuring recycled paper plant based plastics and refillable writing instruments. The EPA encourages waste reduction through comprehensive source reduction and environmentally preferable purchasing (EPP) programs, promoting the adoption of sustainable office products and sustainable resource management. Data indicates that a significant majority of consumers are increasingly prioritizing sustainability, with many indicating a willingness to choose brands that demonstrate verifiable, high-level sustainability commitments. This opportunity extends to corporate clients who aim to meet environmental social and governance goals through responsible procurement. Companies like Staples and Office Depot have expanded their green product assortments responding to this shift. By emphasizing transparency in sourcing and production brands can build trust and loyalty among conscious consumers. The premium pricing potential for sustainable items also offers higher margin opportunities. This trend drives innovation in material science and product design. Suppliers who lead in sustainability can differentiate themselves in a crowded market.

Integration of Smart Technology in Office Accessories

The integration of smart technology into traditional office accessories unlocks potential for the United States office supplies market. This enhances productivity and user experience. Products such as smart notebooks digital pens and connected organizers appeal to tech savvy consumers seeking seamless workflow integration. This convergence of physical and digital tools creates new product categories that command higher price points. Smart notebooks that sync handwritten notes to cloud services exemplify this trend appealing to professionals who value both tactile writing and digital storage. Gartner reports indicate that accelerating digital transformation and IoT adoption are driving a significant surge in demand for smart office technologies and compatible accessories to support hybrid work environments. Manufacturers can partner with tech firms to develop integrated solutions that enhance functionality. The rise of Internet of Things devices in workplaces supports this opportunity as users seek interconnected ecosystems. By offering products that bridge the gap between analog and digital worlds suppliers can attract a broader customer base. This innovation drives repeat purchases as consumers upgrade to smarter versions of essential items. The opportunity lies in creating value added features that justify premium pricing.

MARKET CHALLENGES

Intense Competition from E Commerce Giants and Private Labels

The dominance of e commerce giants and the proliferation of private label brands are a major limitation to the United States office supplies market. This intensifies price competition and erodes brand loyalty. Online retailers like Amazon offer vast selections and rapid delivery at competitive prices making it difficult for traditional suppliers to match. Private labels offered by these platforms provide lower cost alternatives that appeal to budget conscious consumers and businesses. Data from McKinsey & Company highlights that B2B buyers expected to increase their private-label purchase volume by approximately 21%. This trend pressures established brands to lower prices or invest heavily in differentiation. Small and medium sized suppliers struggle to compete with the economies of scale enjoyed by large online retailers. The ease of price comparison online further compresses margins as consumers seek the best deals. Traditional brick and mortar stores face additional challenges in maintaining foot traffic and relevance. This competitive landscape requires continuous innovation and strategic pricing to maintain market share. Brands must emphasize quality and service to justify higher prices. The threat of commoditization remains high for standard office items.

Supply Chain Disruptions Affect Product Availability and Costs

Supply chain disruptions pose a significant challenge to the United States office supplies market. This causing delays in product availability and increasing logistical costs. Dependence on global manufacturing hubs especially in Asia makes the sector vulnerable to geopolitical tensions and logistical bottlenecks. According to the Institute for Supply Management (ISM), the Manufacturing PMI remained in contraction (below 50%) for most of 2025 (e.g., 48.7% in October). Port congestion and shipping container shortages have led to increased freight costs which impact final product prices. Data from the Journal of Commerce and other industry sources confirms that while shipping rates from Asia to the US declined throughout 2025, they remained elevated (e.g., ~46% higher in May 2025) compared to pre-pandemic (2019) averages. These disruptions force suppliers to hold higher inventory levels tying up capital and increasing storage costs. Unpredictable lead times make it difficult for retailers to plan promotions and manage stock effectively. Businesses facing supply uncertainties may switch to alternative suppliers or reduce orders affecting revenue stability. The complexity of global supply networks requires robust risk management strategies that smaller players may lack. This challenge necessitates diversification of sourcing and investment in local manufacturing capabilities. The ongoing volatility in logistics adds a layer of uncertainty to market operations.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 3.12% |

| Segments Covered | By Product Type, Application and Region. |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | California, Washington, Oregon, New York, and the rest of the United States. |

| Market Leaders Profiled | Staples Inc., Office Depot LLC, 3M Company, ACCO Brands Corporation, Newell Brands Inc., HP Inc., Canon Inc., Brother Industries, Ltd., The ODP Corporation, and Avery Dennison Corporation. |

SEGMENTAL ANALYSIS

By Product Type Insights

In 2025, the computer and printer supplies segment led the United States office supplies market by capturing a 40.9% share. Factors such as the indispensable nature of printing and computing hardware in both corporate and home office environments were attributed to the leading position of this segment. This category includes ink cartridges toner paper for printers and peripheral devices that remain essential despite digital trends. The dominance is also fueled by the sheer volume of printed materials required for legal contracts shipping labels and educational materials which cannot be fully digitized. The recurring revenue model associated with ink and toner replacements ensures consistent sales volume. In addition, the hybrid work model has further amplified this trend as employees require reliable printing solutions at home. Companies continue to invest in high quality printing equipment to maintain professional standards for client facing documents. The integration of cloud printing technologies has also extended the lifecycle of existing hardware driving accessory sales. Furthermore, the education sector relies heavily on printed worksheets and exams contributing to steady institutional demand. The segment benefits from technological advancements such as laser printing efficiency which lowers cost per page and encourages higher usage. This combination of necessity and technological evolution secures the leading status of computer and printer supplies.

But the ergonomic desk accessories segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 6.8% from 2026 to 2034. This acceleration is propelled by increasing awareness of workplace health and the need for optimized home office setups. According to sources, work-related musculoskeletal disorders (WMSDs) are historically estimated to account for approximately 33% (one-third) of all worker injury and illness cases involving days away from work. Consumers are investing in adjustable monitor stands keyboard trays and cable management systems to improve posture and productivity. Data from the American Chiropractic Association (ACA) estimates that 80% of the population will experience back pain at some point in their lives. The rise of standing desks has also created a secondary market for accessories such as anti fatigue mats and desktop converters. The aesthetic appeal of modern desk accessories also plays a role with consumers choosing items that complement home decor. Brands are introducing sustainable materials such as bamboo and recycled plastics which attract environmentally conscious buyers. This segment benefits from continuous innovation in design and functionality ensuring sustained growth rates.

By Application Insights

The enterprise segment dominated the United States office supplies market and accounted for a 43.8% share in 2025. This dominance of the segment was driven by the large scale operational needs of corporations and government entities. Large organizations require bulk quantities of supplies for administrative tasks employee onboarding and daily operations ensuring consistent high volume purchases. According to the Bureau of Labor Statistics, there are approximately 163 million employed persons in the United States as of early 2026, a vast workforce that drives demand for office and hybrid work supplies. The centralization of procurement processes in large firms allows for efficient bulk buying which drives significant revenue for suppliers. Enterprises also invest in premium supplies to enhance brand image and employee satisfaction. The return to office initiatives has further boosted enterprise demand as companies restock conference rooms and communal workspaces. Also, the complexity of enterprise needs also drives demand for specialized items such as secure filing systems and high capacity printing supplies. Long term contracts with major suppliers provide stability and predictable revenue streams. This segment's dominance is underpinned by the sheer scale of corporate infrastructure and the ongoing need for operational efficiency.

On the contrary, the household segment is expected to exhibit a noteworthy CAGR of 7.5% over the forecast period due to the permanent shift towards remote work and the increasing number of freelancers and entrepreneurs operating from home. According to Global Workplace Analytics, the number of regular remote workers in the U.S. grew by 140% between 2005 and 2019, a trend that exploded post-2020, with recent data showing three to four times more remote work activity than pre-pandemic levels. Households are purchasing items such as notebooks pens organizers and printing paper to create functional workspaces within their living areas. This demographic values convenience and aesthetics leading to higher engagement with online retail channels. The rise of the gig economy has also contributed to this trend with independent contractors requiring professional grade supplies for client interactions. Retailers have responded by offering curated home office bundles and ergonomic accessories tailored to residential spaces. The emotional connection to home workspace improvement drives frequent upgrades and replacements. This segment benefits from the personalization of work environments ensuring continued rapid expansion.

COUNTRY ANALYSIS

The United States outperformed other countries in the North American office supplies market and occupied a share of 85.4% in 2025. This commanding position is supported by the country’s vast corporate infrastructure high literacy rates and advanced technological adoption. The market status in the United States is characterized by a mature yet evolving landscape where traditional supplies coexist with digital solutions. According to updated data projected for 2026, there are approximately 36.2 million small businesses in the US (up from 33.2 million in 2023), which serve as the backbone of demand for office essentials. These enterprises drive consistent purchases of stationery filing systems and printing materials. The presence of major global retailers such as Staples and Amazon further strengthens the market by providing extensive distribution networks and competitive pricing. Data from the Bureau of Economic Analysis indicates that private nonresidential fixed investment (business investment in structures, equipment, and software) reached approximately $4.3–$4.5 trillion in 2025, supporting the massive procurement of office tools and technology. The cultural emphasis on productivity and organization also fuels demand for innovative office solutions. Educational institutions contribute significantly to the market with millions of students and faculty requiring supplies annually. The Department of Education reports that there are approximately 129,000 K-12 schools in the US (comprising ~99,000 public and ~30,000 private schools), creating a substantial institutional market. The integration of sustainability practices is becoming a key differentiator with consumers preferring eco friendly products. This combination of scale diversity and innovation ensures that the United States remains the central hub for the office supplies industry in the region.

COMPETITIVE LANDSCAPE

The competition in the United States office supplies market is intense and characterized by the presence of established retail giants e commerce leaders and specialized distributors. Major players like Staples Amazon and The Home Depot dominate the landscape through extensive product portfolios and robust distribution networks. These companies leverage their scale to offer competitive pricing and convenient delivery options which are critical for retaining customers. E commerce platforms have disrupted traditional retail models by providing unparalleled selection and ease of purchase forcing brick and mortar stores to adapt. The rise of private labels has increased pressure on national brands to differentiate through quality and innovation. Competition is also driven by the need for sustainability with companies vying to offer eco friendly products and practices. Technological integration plays a significant role as firms invest in digital tools to enhance customer experience and operational efficiency. The market sees frequent promotional activities and discounts which impact profit margins but drive volume. Small and niche players compete by offering specialized products and personalized services that appeal to specific segments. This dynamic environment requires continuous innovation and strategic agility to maintain market relevance and profitability.

KEY MARKET PLAYERS

Some of the promising companies that are playing a dominating role in the U.S. Office Supplies Market include

- Staples Inc.

- Office Depot LLC

- 3M Company

- ACCO Brands Corporation

- Newell Brands Inc.

- HP Inc.

- Canon Inc.

- Brother Industries, Ltd.

- The ODP Corporation

- Avery Dennison Corporation

Top Players in the US Office Supplies Market

Staples Inc

Staples remains a dominant force in the United States office supplies market by leveraging its extensive retail network and robust e commerce platform. The company focuses on providing comprehensive solutions for both business clients and individual consumers through its omnichannel strategy. Recently Staples has invested heavily in digital transformation enhancing its online user experience and same day delivery capabilities to meet evolving customer expectations. The retailer has also expanded its private label offerings which provide cost effective alternatives to national brands thereby increasing customer loyalty. Staples actively promotes sustainability initiatives by offering recycled products and recycling programs for electronics and ink cartridges. These efforts align with growing consumer demand for environmentally responsible business practices. The company continues to strengthen its B2B services by offering customized procurement solutions for small and medium enterprises. By integrating technology into its supply chain Staples ensures efficient inventory management and rapid order fulfillment. This strategic focus on convenience sustainability and digital integration solidifies its position as a key player in the competitive US market landscape.

Amazon.com Inc

Amazon has revolutionized the United States office supplies market by offering unparalleled convenience vast product selection and competitive pricing through its e commerce platform. The company leverages its advanced logistics network to provide fast and reliable delivery services which are critical for business continuity. Amazon Business serves as a dedicated portal for corporate customers offering features such as bulk discounts tax exemption and analytics tools to streamline procurement processes. Recent actions include the expansion of its private label brands in office categories which provide high quality alternatives at lower price points. Amazon utilizes data analytics to personalize recommendations and optimize inventory levels ensuring product availability. The integration of voice activated shopping through Alexa devices further simplifies the purchasing process for routine supplies. By continuously improving its delivery infrastructure and customer service Amazon maintains a strong competitive edge. The company also focuses on sustainability by introducing frustration free packaging and carbon neutral shipping options. These initiatives enhance brand reputation and attract environmentally conscious consumers. Amazon's ability to adapt quickly to market trends ensures its continued leadership in the sector.

The Home Depot Inc

The Home Depot has significantly expanded its presence in the United States office supplies market by catering to the growing segment of home based professionals and small businesses. The retailer leverages its extensive physical store network to offer immediate access to essential office items alongside home improvement products. Recent strategies include the enhancement of its online platform with specialized business accounts that provide volume pricing and dedicated support. The Home Depot focuses on ergonomic office furniture and organizational solutions which appeal to consumers setting up home workspaces. The company has also integrated its supply chain to ensure consistent stock levels of high demand items such as printing paper and writing instruments. By promoting its Pro Xtra loyalty program The Home Depot attracts professional contractors and entrepreneurs who require reliable supply sources. The retailer emphasizes value and convenience offering services such as curbside pickup and same day delivery. These initiatives strengthen customer retention and drive sales growth. The Home Depot's ability to cross sell office supplies with home office renovation products creates unique opportunities for market expansion and customer engagement.

Top Strategies Used by Key Market Participants

Key players in the United States office supplies market employ diverse strategies to maintain competitiveness and drive growth in a evolving landscape. Digital transformation is a primary focus with companies investing in e commerce platforms and mobile applications to enhance customer convenience and accessibility. Omnichannel integration allows seamless transitions between online and offline shopping experiences which improves customer satisfaction and loyalty. Private label expansion is another critical strategy as retailers develop proprietary brands to offer cost effective alternatives and higher profit margins. Sustainability initiatives are increasingly important with firms introducing eco friendly products and recycling programs to appeal to conscious consumers. Strategic partnerships with technology providers enable the integration of smart office solutions and automated procurement systems. Companies also focus on supply chain optimization to reduce costs and improve delivery speeds which are essential for meeting customer expectations. Personalization through data analytics helps tailor marketing efforts and product recommendations to individual preferences. These strategies collectively enable market participants to adapt to changing consumer behaviors and maintain strong market positions.

MARKET SEGMENTATION

This research report on the U.S. Office Supplies Market has been segmented based on the following categories.

By Product Type

- Computer and Printer Supplies

- Desk Accessories

By Application

- Enterprise Sector

- Household

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com