U.S Outsourcing Market Size, Share, Trends & Growth Forecast Report Segmented By Service Type (Application Outsourcing, Infrastructure Outsourcing, Others), Enterprise Size, End User Industry, And Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis And Forecast, 2026 To 2034

U.S Outsourcing Market Size

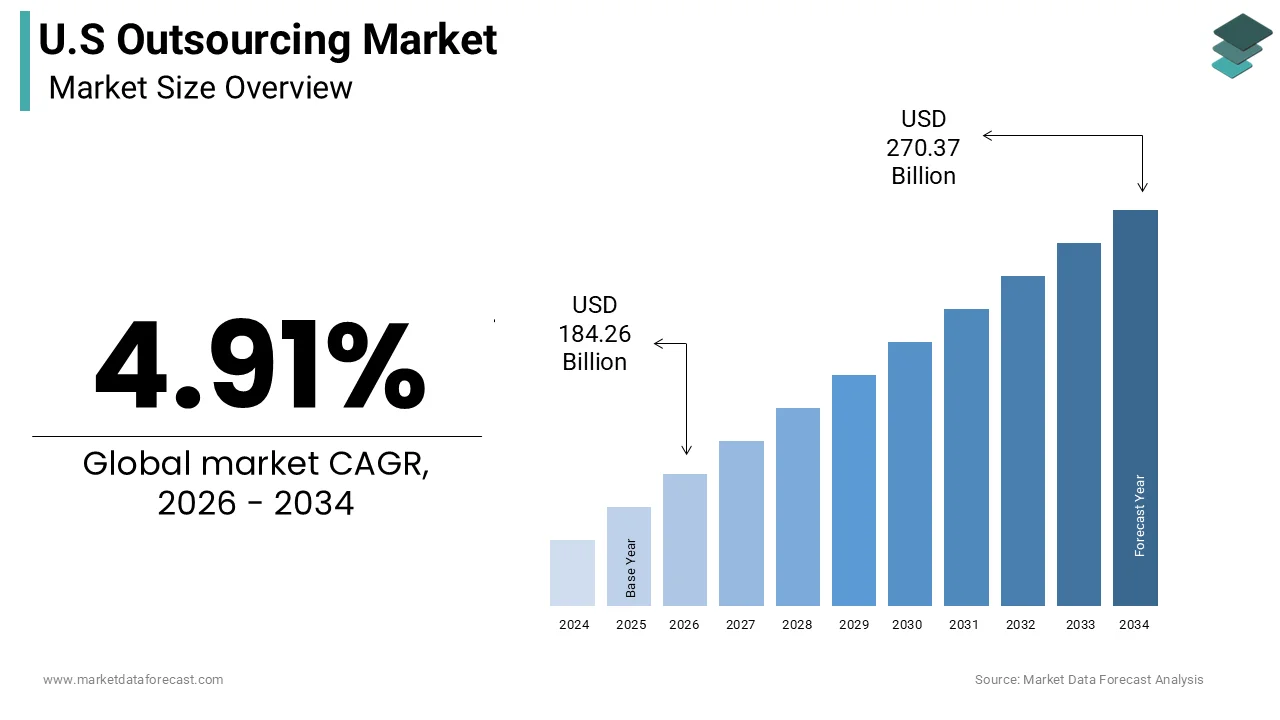

The U.S. outsourcing market size was calculated to be USD 175.64 billion in 2025 and is anticipated to be worth USD 270. 37 billion by 2034, from USD 184.26 billion in 2026, growing at a CAGR of 4.91% during the forecast period.

The outsourcing organizations contract third-party providers to handle specific operations or services that were traditionally performed in-house. As per the Bureau of Labor Statistics, the service sector accounts for approximately 80% of US employment, highlighting the significant role of external service providers in the national economy. According to the Deloitte Global Outsourcing Survey, nearly 70% of US executives view outsourcing as a key element of their overall business strategy rather than just a cost-cutting measure. This shift reflects a mature market where quality innovation and scalability are prioritized over mere expense reduction. The regulatory environment in the United States emphasizes data security and compliance, which shapes how outsourcing contracts are structured and managed. The integration of artificial intelligence and automation into outsourced services is redefining service delivery models.

MARKET DRIVERS

Accelerated Digital Transformation and Cloud Adoption

The rapid pace of digital transformation, as companies seek external expertise to navigate complex technological issues, is majorly fuelling the growth of the United States outsourcing market. Organizations are increasingly relying on outsourcing partners to implement cloud computing solutions, manage cybersecurity threats, and integrate artificial intelligence into their operations. According to the International Data Corporation, spending on digital transformation technologies and services in the United States is projected to reach 3.4 trillion dollars by 2026. This talent gap forces companies to look outward for qualified personnel who can deliver high-quality technical services. Outsourcing providers offer access to global talent pools with expertise in emerging technologies, such as blockchain, machine learning, and data analytics. The ability to scale technical teams quickly allows businesses to respond to market changes and consumer demands efficiently. Furthermore, outsourcing partners often possess established infrastructure and proprietary tools that reduce the time and cost associated with developing these capabilities in-house. The complexity of managing hybrid cloud environments also drives demand for managed service providers who can ensure seamless integration and performance.

Focus on Core Competencies and Operational Efficiency

The strategic imperative to focus on core competencies, while enhancing operational efficiency, is another major driver fueling the growth of the US outsourcing market. Companies are increasingly recognizing that non-core functions, such as payroll processing, customer service, and back office support, can be handled more effectively by specialized providers. This approach allows management to dedicate resources and attention to innovation, product development, and customer engagement, which are critical for competitive advantage. As per the Society for Human Resource Management, the average cost per hire in the United States has risen to over 4000 dollars, making internal expansion of support teams financially prohibitive for many firms. Outsourcing converts fixed labor costs into variable costs, providing greater financial flexibility and predictability. Service providers achieve economies of scale by serving multiple clients, which translates into lower costs and higher service quality for individual companies. The standardization of processes by outsourcing partners also leads to improved compliance and reduced error rates. Additionally, the ability to access 24/7 support services through global delivery models enhances customer satisfaction and responsiveness. This operational agility is particularly valuable in industries with fluctuating demand cycles.

MARKET RESTRAINTS

Data Security Risks and Privacy Concerns

The heightened concern over data security and privacy risks associated with sharing sensitive information with third-party providers is limiting the growth of the United States outsourcing market. As organizations outsource functions, they expose themselves to potential cyber threats and data breaches that can have severe financial and reputational consequences. The substantial financial risk makes companies hesitant to outsource processes involving confidential customer data or intellectual property. Companies can be held liable for the security failures of their vendors, which adds a layer of legal complexity to outsourcing arrangements. The varying regulatory landscapes across different countries further complicate compliance efforts, particularly regarding data sovereignty and protection laws such as the General Data Protection Regulation. Ensuring that outsourcing partners adhere to strict security standards requires continuous monitoring and auditing, which increases operational overhead. The fear of insider threats and unauthorized access also deters some organizations from fully embracing outsourcing models. High-profile security incidents involving major service providers have eroded trust and made businesses more cautious. The need for robust encryption, secure communication channels, and comprehensive insurance coverage adds to the cost of outsourcing. These security challenges create a barrier to adoption, particularly for highly regulated industries, such as healthcare and finance.

Quality Control and Communication Barriers

The challenge of maintaining consistent quality control and overcoming communication barriers when working with remote outsourcing partners is also hindering the growth of the United States outsourcing market. Differences in time zones, cultural norms, and language proficiency can lead to misunderstandings and delays in project execution. This lack of seamless interaction can result in deliverables that do not meet the expected standards, requiring additional time and resources for corrections. Monitoring performance and ensuring adherence to quality metrics is more difficult when teams are geographically dispersed. The reliance on digital communication tools often fails to capture nuances, leading to misinterpretation of requirements. Cultural differences in work ethics and problem-solving approaches can also create friction between client and provider teams. The inability to conduct face-to-face meetings limits the ability to build strong relationships and trust. These issues are particularly pronounced in knowledge process outsourcing, where complex decision-making is required. Companies often find themselves investing heavily in management oversight to bridge these gaps, which diminishes the cost benefits of outsourcing.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Automation

The integration of artificial intelligence and automation into service delivery models is likely to propel significant growth opportunities for the growth of the United States outsourcing market in the coming years. Outsourcing providers are increasingly adopting robotic process automation and machine learning algorithms to enhance efficiency and accuracy in tasks, such as data entry, customer support, and financial analysis. The automation technologies have the potential to automate 45% of current work activities, saving the global economy up to 2 trillion dollars annually. This technological evolution allows outsourcing firms to offer higher-value services at lower costs, creating a compelling value proposition for US clients. This shift enables providers to focus human talent on complex problem-solving and strategic advisory roles. The use of predictive analytics allows for proactive issue resolution and personalized customer experiences. US companies can leverage these advanced capabilities without making significant upfront investments in technology infrastructure. The scalability of automated solutions allows businesses to handle fluctuating volumes efficiently. Furthermore, the data generated by automated systems provides valuable insights for process optimization and decision-making. This transition from labor arbitrage to technology-enabled services opens new revenue streams for outsourcing providers.

Expansion into Knowledge Process Outsourcing

The expansion into knowledge process outsourcing (KPO), which involves high-value-added tasks requiring specialized expertise and analytical skills, is also to boost the growth of the United States outsourcing market. Unlike traditional business process outsourcing, KPO focuses on areas such as research and development, legal services, medical consulting, and financial modeling. The law firms are increasingly outsourcing legal research and document review to specialized providers to reduce costs and improve efficiency. The growing complexity of regulatory environments and business operations creates a demand for expert analysis and insights. US companies benefit from accessing global talent pools with advanced degrees and industry-specific experience. The ability to tap into specialized knowledge centers allows for faster innovation and better decision-making. KPO providers are also integrating advanced analytics and visualization tools to deliver actionable insights. It allows US firms to remain agile and competitive in knowledge-intensive industries.

MARKET CHALLENGES

Geopolitical Instability and Supply Chain Disruptions

The impact of geopolitical instability and supply chain disruptions on global service delivery is certainly a major factor impeding the growth of the United States outsourcing market. Political tensions, trade wars, and regional conflicts can disrupt operations and create uncertainty for businesses relying on international providers. These uncertainties can lead to sudden changes in regulations, tariffs, or restrictions on data flows, which impact outsourcing arrangements. Companies may face unexpected costs or delays due to political interventions or sanctions. The reliance on single-source providers in politically volatile regions increases vulnerability to disruptions. Diversifying sourcing strategies to mitigate these risks often involves higher costs and complexity. The unpredictability of international relations makes long-term planning difficult for both clients and providers. Cyber warfare and state-sponsored hacking also pose threats to the integrity of outsourced services. These geopolitical factors require companies to constantly reassess their risk exposure and contingency plans.

Talent Shortage and Skill Gap in Specialized Roles

The ongoing talent shortage and skill gap in specialized roles within the outsourcing industry will also hinder the growth of the United States outsourcing market. While outsourcing provides access to global talent, the demand for highly skilled professionals in areas such as cybersecurity, data science, and cloud architecture exceeds supply. Outsourcing providers struggle to recruit and retain qualified individuals who can meet the sophisticated requirements of US clients. The rapid pace of technological change means that skills become obsolete quickly, requiring continuous training and upskilling. This investment in human capital increases operational costs for providers. The high turnover rates in the outsourcing industry further exacerbate the problem, leading to inconsistency in service quality. Clients often face delays and disruptions when key personnel leave projects. The lack of standardized certification and training programs across different regions complicates the assessment of candidate qualifications. This skill gap limits the ability of outsourcing firms to deliver high-value services consistently. It forces companies to invest more in vendor management and quality assurance.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.91% |

| Segments Covered | By Service Type, Enterprise Size, End User Industry, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Accenture, IBM, Cognizant, Infosys, Tata Consultancy Services (TCS), Wipro, Capgemini, HCLTech, Genpact, Concentrix, Teleperformance, Alorica, ADP, Xerox, Sutherland Global Services |

SEGMENTAL ANALYSIS

By Service Type Insights

The application segment was the largest by occupying 59.1% of the United States outsourcing market share in 2025, with the need for continuous software development, maintenance, and modernization. The escalating demand for custom software development and the modernization of legacy systems is also propelling the growth of the segment. According to the International Data Corporation, global spending on digital transformation technologies and services, which heavily includes application development, is projected to reach 3.4 trillion dollars by 2026. US enterprises are increasingly moving away from off-the-shelf solutions to bespoke applications that address specific operational needs and customer preferences. Many large organizations have at least one legacy modernization initiative underway, escalating the urgent need to update outdated systems. Outsourcing partners provide access to specialized developers proficient in modern programming languages and frameworks, such as Python, Java, and React. This expertise allows companies to accelerate development cycles and reduce time to market. The complexity of integrating new applications with existing enterprise resource planning systems also necessitates external support. Outsourcing firms offer scalable teams that can handle peak development loads without the long-term commitment of hiring full-time employees. This flexibility is crucial for agile development methodologies that require rapid iteration. The cost efficiency of accessing global talent pools further enhances the appeal of application outsourcing. Companies can achieve high-quality outputs at competitive rates while focusing internal resources on strategic planning.

The infrastructure segment is likely to witness the fastest CAGR of 8.5% from 2026 to 2034. The rapid growth of the infrastructure outsourcing segment is primarily driven by the complex migration to hybrid and multi-cloud environments. Managing these diverse environments requires specialized expertise in network configuration, security, and performance optimization. Spending on cloud infrastructure services is growing at twice the rate of traditional IT infrastructure spending, as per a study. Outsourcing providers offer managed services that ensure seamless integration and operation across different cloud platforms. This capability allows US companies to avoid vendor lock-in and optimize costs by selecting the best services from various providers. The complexity of managing data gravity and latency issues in distributed environments further necessitates external support. Outsourcing firms provide 24/7 monitoring and management, ensuring high availability and reliability. The ability to scale infrastructure resources dynamically based on demand is a key benefit of outsourced management. This flexibility supports business continuity and disaster recovery efforts. The strategic advantage of leveraging expert knowledge in cloud architecture drives adoption.

By Enterprise Size Insights

The large enterprises segment held a dominant share of the US outsourcing market in 2025, owing to the sheer scale of their operations, which necessitates extensive outsourcing to achieve cost optimization. Managing these operations internally is often inefficient and costly, prompting these organizations to outsource non-core functions. The ability to standardize processes across global units further enhances efficiency. Outsourcing allows large enterprises to convert fixed costs into variable costs, providing greater financial flexibility. This model supports agility in responding to market changes and economic fluctuations. The complexity of managing global supply chains and customer bases also drives outsourcing adoption. Large firms benefit from the specialized expertise and infrastructure of service providers. This strategic alignment enables them to maintain competitiveness while optimizing resource allocation. The consistent demand from large enterprises sustains the leadership of this segment.

The small and medium enterprises (SMEs) segment is growing at an anticipated CAGR of 9.2% from 2026 to 2034 with the democratization of cloud-based services, which lowers the barriers to entry. Cloud computing allows SMEs to access enterprise-grade tools and infrastructure at affordable prices. Outsourcing providers offer managed cloud services that simplify implementation and maintenance for SMEs. This accessibility allows small firms to leverage advanced technologies without significant upfront investments. The scalability of cloud solutions supports business growth and expansion. SMEs can adjust their outsourcing needs based on current demand, ensuring cost efficiency. The availability of subscription-based models further reduces financial risks. This technological empowerment drives SMEs to outsource IT functions such as data storage and application hosting. The ability to focus on core business activities while relying on experts for technical support enhances productivity. This trend accelerates the adoption of outsourcing among smaller entities. The growing confidence in cloud security and reliability further supports this shift. SMEs are increasingly recognizing the strategic value of outsourcing.

By End User Industry Insights

The BFSI sector accounted in holding 43.2% of the US outsourcing market share in 2025, owing to the stringent regulatory environment that requires rigorous compliance and risk management. Meeting these requirements involves extensive reporting, auditing, and monitoring, which are resource-intensive. Outsourcing providers offer specialized services that ensure compliance with evolving regulations. These services include anti-money laundering checks, know your customer verification, and transaction monitoring. The expertise of outsourcing partners reduces the risk of non-compliance and associated penalties. The complexity of global financial regulations necessitates external support for multinational institutions. Outsourcing allows banks to stay updated with regulatory changes without diverting internal resources. The ability to leverage advanced analytics for risk assessment enhances decision-making. This strategic support is critical for maintaining trust and stability in the financial system. The consistent demand for compliance services sustains the leadership of the BFSI sector.

The healthcare and life sciences sector is projected to witness the fastest CAGR of 10.5% during the forecast period, with the mandatory adoption of electronic health records (EHR) and the need for data interoperability. Managing and integrating these vast amounts of data requires specialized technical support. As per the Healthcare Information and Management Systems Society, interoperability remains a significant challenge, with many systems unable to share data seamlessly. Outsourcing providers offer solutions that facilitate data exchange and integration across different platforms. These services improve patient care coordination and reduce administrative burdens. The complexity of EHR systems necessitates ongoing maintenance and updates. Outsourcing partners provide the expertise needed to optimize system performance and usability. Outsourcing enables healthcare providers to leverage data for improved outcomes. The regulatory push for interoperability through laws such as the 21st Century Cures Act accelerates adoption. Healthcare organizations rely on external partners to navigate these technical challenges.

KEY MARKET PLAYERS

A few major players of the U.S. outstanding market include

- Accenture

- IBM

- Cognizant

- Infosys

- Tata Consultancy Services (TCS)

- Wipro

- Capgemini

- HCLTech

- Genpact

- Concentrix

- Teleperformance

- Alorica

- ADP

- Xerox

- Sutherland Global Services

Top Strategies Used by Key Market Participants in the US Outsourcing Market

The competition in the United States outsourcing market is intense and characterized by a mix of global giants and specialized niche players. Large multinational corporations dominate the landscape by leveraging extensive resources and diverse service portfolios to offer end-to-end solutions. These established firms compete fiercely on technological innovation, scalability, and global delivery capabilities to retain large enterprise clients. Smaller boutique providers differentiate themselves by offering specialized expertise in areas such as cybersecurity, artificial intelligence, and industry-specific processes. The barrier to entry is moderate, but scaling requires significant investment in technology and talent acquisition. Competition is further exacerbated by the increasing demand for transparent pricing and measurable business outcomes from clients. Firms are increasingly investing in automation and artificial intelligence to reduce costs and improve service quality. The war for skilled talent is another critical aspect, with providers competing to attract and retain professionals with advanced digital skills. Strategic partnerships and alliances are common as companies seek to expand their capabilities and reach new markets. Ultimately, success depends on the ability to deliver consistent value and adapt to rapid technological changes. Trust and reliability are the primary differentiators in this mature market. Companies must continuously innovate to stay ahead of competitors and meet evolving client needs.

Leading Players in the Europe Outsourcing Market

- Accenture is a global professional services company with a significant presence in the European outsourcing market. The firm provides comprehensive solutions, including digital transformation, cloud services, and intelligent automation to clients across various industries. Recently, Accenture has strengthened its position by investing heavily in artificial intelligence and data analytics capabilities to enhance service delivery. The company has expanded its network of innovation hubs across Europe to foster collaboration with local startups and tech firms. The firm continues to acquire specialized boutique firms to bolster its expertise in niche areas such as cybersecurity and blockchain. These strategic moves demonstrate its commitment to delivering high value and innovative solutions. Accenture remains a key player by leveraging its extensive talent pool and technological prowess. Its ability to integrate advanced technologies into traditional outsourcing models sets it apart. The company actively partners with European governments to support digital infrastructure projects. This deep engagement ensures its continued relevance and leadership in the evolving market landscape.

- Capgemini is a leading French multinational information technology services and consulting corporation with a strong foothold in the European outsourcing sector. The company offers a wide range of services, including application development, infrastructure management, and business process outsourcing. Recently, Capgemini has reinforced its market position by accelerating its cloud-first strategy and expanding its partnerships with major cloud providers. The firm has invested significantly in upskilling its workforce to meet the demand for digital skills across Europe. The company focuses on creating sustainable and inclusive digital transformations for its clients. Capgemini actively engages in strategic acquisitions to expand its geographic reach and service offerings. These initiatives highlight its dedication to innovation and customer centricity. The firm leverages its deep industry knowledge to provide tailored solutions that drive business growth. Capgemini remains a dominant force by combining technical expertise with strategic insights. Its strong presence in key European markets ensures robust client relationships. The company continues to adapt to changing market dynamics through continuous innovation.

- Tata Consultancy Services is a major Indian IT services and consulting company with a substantial presence in the European outsourcing market. The firm provides comprehensive IT solutions, including software development, system integration, and business process services. Recently, TCS has strengthened its position by expanding its delivery centers in Europe to better align with client needs. The company has invested in artificial intelligence and automation technologies to enhance operational efficiency for its clients. The firm actively collaborates with local universities and training institutions to develop a skilled workforce. TCS emphasizes sustainability and corporate social responsibility in its operations across Europe. These efforts enhance its reputation and appeal to socially conscious clients. The company continues to innovate through its research and development initiatives. TCS remains a key contributor by delivering high-quality and cost-effective services. Its global expertise combined with local insights enables effective problem-solving. The firm strengthens its market position through strategic partnerships and customer-focused innovations.

MARKET SEGMENTATION

This research report on the US outsourcing market has been segmented and sub-segmented based on service type, enterprise size, end user industry & region.

By Service Type

- Application Outsourcing

- Infrastructure Outsourcing

- Others

By Enterprise Size

- Small and Medium Enterprises

- Large Enterprises

By End user

- BFSI

- IT and Telecom

- Government and Public Sector

- Retail and E-Commerce

- Others

By Region

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

1. What are the major drivers of growth in the U.S. outsourcing market?

Growing adoption of cloud computing, rising labor costs, increasing focus on core business functions, and demand for IT and customer support services are major growth drivers.

2. Which outsourcing service segment holds the largest market share in the United States?

The IT outsourcing segment holds the largest market share due to high demand for software development, cloud services, cybersecurity, and infrastructure management.

3. What is the projected CAGR of the U.S. outsourcing market during the forecast period?

The market is expected to register steady CAGR growth during the forecast period owing to increasing digitalization and automation across enterprises.

4. How is digital transformation influencing the U.S. outsourcing industry?

Digital transformation is encouraging companies to outsource advanced technologies such as AI, cloud migration, data analytics, and automation services to specialized providers.

5. What role does cloud computing play in the U.S. outsourcing market?

Cloud computing enables businesses to improve scalability, reduce infrastructure costs, and enhance remote operations, thereby increasing demand for outsourced cloud services.

6. How is artificial intelligence impacting outsourcing services in the United States?

Artificial intelligence is improving automation, customer service efficiency, predictive analytics, and operational productivity in outsourcing operations.

7. What are the key challenges faced by outsourcing service providers in the U.S.?

Data security concerns, regulatory compliance issues, communication barriers, and rising competition are key challenges in the outsourcing market.

8. What are the emerging trends in the United States outsourcing market?

Automation, AI integration, robotic process automation (RPA), remote workforce solutions, and cloud-based outsourcing are major emerging trends.

9. How are cybersecurity concerns affecting the outsourcing market in the United States?

Businesses are demanding stronger cybersecurity measures and compliance standards from outsourcing providers to protect sensitive enterprise data.

10 . What opportunities are expected to drive future growth in the U.S. outsourcing market?

Increasing adoption of AI-driven services, digital customer support, cloud migration, and business process automation are expected to create significant future opportunities.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com