U.S. Parental Control Software Market Size, Share, Trends & Growth Forecast Report By Operating System (Windows, Android, iOS & OS X, and Cross-Platform & Others), Deployment, Application, and Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

Market Size, 2025

$241.96 MnMarket Estimate, 2026

$265.75 MnMarket Forecast, 2034

$562.65 MnCAGR, 2026–2034

9.83%U.S. Parental Control Software Market Report Summary

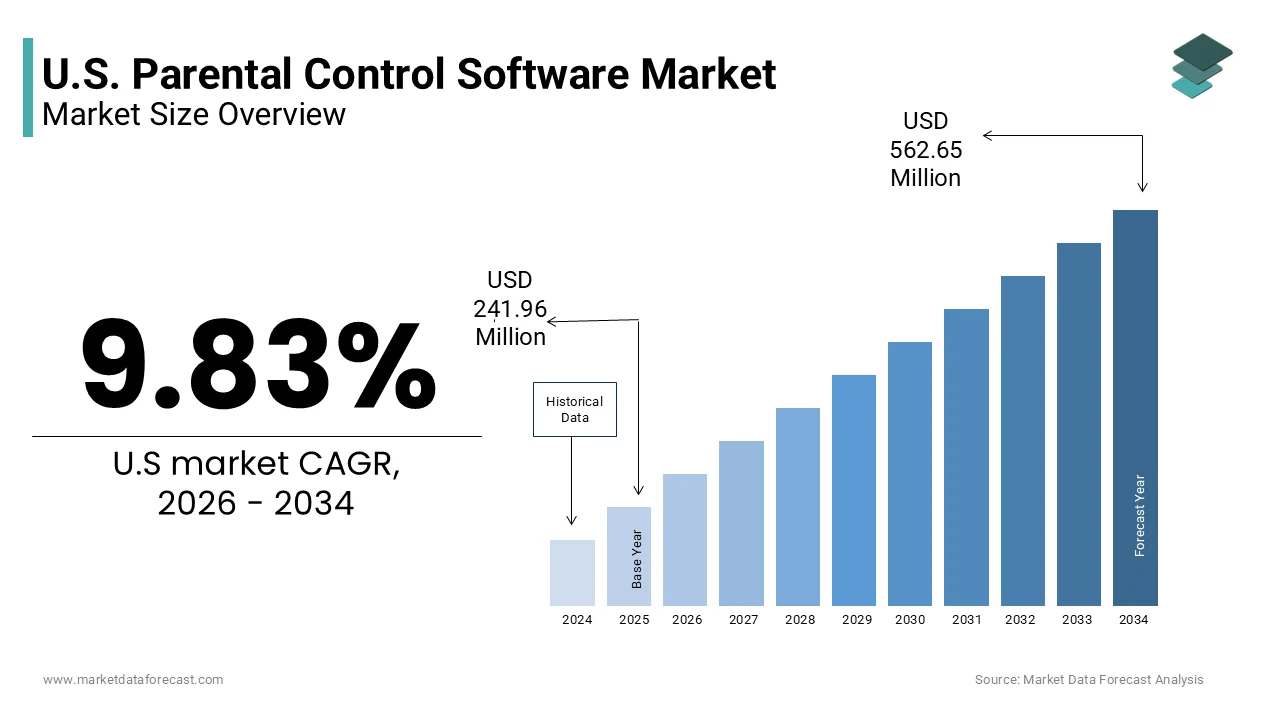

The U.S. parental control software market was valued at USD 241.96 million in 2025, is estimated to reach USD 265.75 million in 2026, and is projected to reach USD 562.65 million by 2034, growing at a CAGR of 9.83% during the forecast period. Market growth is driven by increasing concerns regarding child online safety, rising digital device usage among children, and growing awareness regarding screen time management solutions. Parental control software has become increasingly important for monitoring online activity, content filtering, and managing digital behavior across connected devices. Rising adoption of cloud technologies and growing focus on cyber safety are further supporting market expansion across the United States.

Key Market Trends

- Growing concerns regarding child online safety are driving market growth.

- Increasing smartphone and digital device adoption among children is boosting software demand.

- Rising awareness regarding screen time management and digital wellbeing is supporting market expansion.

- Expansion of cloud based monitoring technologies is enhancing software accessibility and scalability.

- Innovation in AI powered monitoring, content filtering, and cyber protection tools is influencing market development.

Segmental Insights

- Based on operating system, the Android segment accounted for 44.9% of the U.S. parental control software market share in 2025. This dominance is attributed to broad Android device adoption and strong mobile ecosystem penetration.

- Based on deployment, the cloud based deployment segment held 84.4% of the U.S. parental control software market share in 2025, supported by scalability, remote accessibility, and easier software management capabilities.

- Based on application, the residential segment accounted for 88.4% of the U.S. parental control software market share in 2025, driven by increasing household adoption of child safety and monitoring solutions.

Regional Insights

- The United States held the dominant position in the North American parental control software market in 2025. Rising internet penetration, increasing child digital engagement, and growing cybersecurity awareness continue to strengthen market development.

Competitive Landscape

The U.S. parental control software market is highly competitive, with companies focusing on AI enabled monitoring solutions, content filtering technologies, and cloud platform enhancements to strengthen their market position. Software providers continue investing in privacy protection capabilities and digital safety innovation. Prominent players in the U.S. parental control software market include Gen Digital Inc., Alphabet Inc., Microsoft Corporation, McAfee, LLC, AT&T Inc., Smith Micro Software, Inc., SafeDNS, Inc., Mobicip LLC, Qustodio, and Bark.

U.S. Parental Control Software Market Size

The U.S. parental control software market size was valued at USD 241.96 million in 2025, is estimated to reach USD 265.75 million in 2026, and is projected to reach USD 562.65 million by 2034, growing at a CAGR of 9.83%.

The U.S. parental control software market has evolved from simple website filters to comprehensive family safety ecosystems integrating artificial intelligence for behavioural analysis. According to the Pew Research Center, 95% of teens have access to a smartphone and 45% say they are online almost constantly, highlighting the ubiquity of digital connectivity among youth. This pervasive access necessitates robust oversight mechanisms for guardians. According to the Centers for Disease Control and Prevention, suicide rates among adolescents have risen significantly with cyberbullying identified as a contributing factor driving demand for monitoring tools. According to the Federal Bureau of Investigation, thousands of complaints annually regard online enticement of children, which is further emphasizing the need for protective software. Operating systems such as iOS and Android have integrated basic controls, yet third party applications offer granular customization and cross platform compatibility. The market is influenced by increasing awareness of digital wellbeing and mental health impacts of excessive screen time. Regulatory frameworks like the Childrens Online Privacy Protection Act shape data handling practices within these applications. Parents seek balanced solutions that protect without infringing excessively on privacy, fostering trust and open communication within families. This dynamic landscape drives innovation in user friendly interfaces and real time alert systems.

MARKET DRIVERS

Rising Prevalence of Cyberbullying and Online Predatory Behavior

The growing prevalence of cyberbullying and online predatory behavior is primarily fuelling the adoption of parental control software in the U.S. and is a key market driver. The anonymity and reach of digital platforms have exacerbated harassment and exploitation risks for minors. According to the Pew Research Center, 46% of teens aged 13 to 17 have experienced at least one form of cyberbullying, including offensive name calling and spreading of false rumors. This alarming statistic prompts parents to seek proactive monitoring solutions to identify and mitigate harmful interactions. As per the National Center for Missing and Exploited Children, the number of reported online enticement cases has increased substantially with over 28 million reports filed in recent years. Parental control software offers features such as keyword alerts and social media monitoring that enable guardians to detect suspicious conversations and intervene promptly. The psychological impact of online harassment on adolescent mental health drives the urgency for protective measures. Schools and community organizations increasingly advocate for digital safety tools to complement educational efforts. Parents perceive these software solutions as essential safeguards against invisible threats that traditional supervision cannot address. The ability to track location and monitor app usage provides a sense of security in an unpredictable digital environment. Consequently, the fear of victimization sustains robust demand for advanced monitoring capabilities. This driver underscores the critical role of technology in ensuring child safety online.

Increasing Awareness of Digital Wellbeing and Screen Time Management

The rising awareness of digital wellbeing and screen time management is further boosting the expansion of the U.S. parental control software market. Excessive screen time is linked to sleep deprivation, attention deficits, and sedentary lifestyles among children. According to the American Academy of Pediatrics, children aged 8 to 12 spend an average of 4 to 6 hours daily on screens while teenagers may spend up to 9 hours. This extensive exposure raises concerns about developmental impacts and physical health. As per the Common Sense Media census, nearly 70% of parents worry about their childrens screen time habits and seek tools to enforce limits. Parental control software enables users to set daily usage caps, schedule device free periods, and block distracting applications during study hours. These features promote healthier digital habits and encourage offline activities. The integration of detailed reporting allows parents to understand usage patterns and adjust rules accordingly. Educational initiatives by health organizations emphasize the importance of balanced technology use. Parents view these tools as instrumental in fostering self-regulation and responsible digital citizenship. The shift from restrictive blocking to constructive management reflects evolving parenting strategies. Software providers respond by offering intuitive dashboards and flexible scheduling options. This focus on holistic wellbeing drives adoption beyond mere content filtering. Thus, the prioritization of mental and physical health sustains market growth.

MARKET RESTRAINTS

Privacy Concerns and Data Security Risks

Privacy concerns and data security risks significantly hampering the growth of the U.S. parental control software market. These applications require extensive permissions to monitor device activity, raising fears about data misuse and unauthorized access. According to the Electronic Frontier Foundation, many parental control apps collect sensitive information, including location history and communication logs, which may be vulnerable to breaches. As per a study by the University of Michigan, several popular parental control applications exhibited security vulnerabilities that could allow hackers to intercept data or take control of the device. Parents are increasingly cautious about granting third party companies access to their childrens private interactions. The lack of transparency in data handling practices exacerbates these concerns. High profile incidents of data leaks have heightened awareness of digital privacy rights. Regulatory scrutiny under laws such as the California Consumer Privacy Act imposes strict compliance requirements on developers. Some families opt for built in operating system controls rather than third party software to minimize data exposure. The perception that monitoring infringes on childrens right to privacy also creates ethical dilemmas. Trust deficits hinder widespread adoption, particularly among tech savvy demographics. Developers must invest heavily in encryption and transparent privacy policies to mitigate these risks. Until security standards improve and trust is restored, these concerns will limit market penetration.

Technical Limitations and Evasion by Tech Savvy Minors

Technical limitations and evasion by tech savvy minors are further impeding the growth of the U.S. market. Children and teenagers often possess advanced digital literacy, enabling them to bypass restrictions using virtual private networks, proxy servers, or alternative devices. According to a survey by Bark Technologies, 60% of teens admit to using methods to circumvent parental controls, including deleting browsing history or using incognito modes. As per the Family Online Safety Institute, older children frequently exploit loopholes in software algorithms to access blocked content or extend screen time unnoticed. The constant evolution of mobile operating systems and applications requires frequent updates to maintain efficacy, which some providers fail to deliver promptly. Incompatibility with certain devices or platforms further reduces coverage. Parents may experience frustration when software fails to detect new threats or allows unrestricted access to harmful content. The cat and mouse dynamic between developers and users undermines confidence in these tools. Some families abandon subscription services due to perceived ineffectiveness. The resource intensive nature of maintaining robust evasion protection increases operational costs for vendors. These technical shortcomings limit the reliability of parental control solutions. Consequently, the ability of minors to outsmart software acts as a persistent restraint on market satisfaction and retention.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence for Behavioural Analysis

The integration of artificial intelligence for behavioural analysis presents a substantial opportunity for the U.S. parental control software market. AI driven tools can detect subtle changes in online behavior that may indicate distress, bullying, or mental health issues. According to the Journal of Medical Internet Research, machine learning algorithms can identify patterns associated with depression and anxiety with high accuracy by analysing language and usage metrics. As per data on algorithmic tracking deployments, security frameworks incorporating advanced analytics are increasingly shaping modern consumer safety applications. Parental control software leveraging AI can provide contextual insights rather than simple keyword matching, reducing false positives. These systems can alert parents to potential self-harm or suicidal ideation based on search queries and social media posts. The ability to differentiate between harmless teen slang and genuine threats enhances utility. Personalized recommendations for digital wellbeing interventions add value beyond monitoring. Parents appreciate proactive alerts that facilitate timely conversations with their children. Vendors can differentiate their offerings by emphasizing emotional intelligence and predictive capabilities. The growing acceptance of AI in healthcare and education supports adoption in family safety. This technological advancement transforms parental controls from reactive blockers to proactive wellness partners. Consequently, AI integration opens new revenue streams and enhances customer loyalty.

Expansion into Smart Home and Internet of Things Ecosystems

The expansion into smart home and Internet of Things ecosystems offers a promising avenue for growth in the U.S. parental control software market. Connected devices such as smart speakers, cameras, and gaming consoles present new avenues for online interaction and risk. According to industry tracking surveys, the number of connected household devices in the US has passed hundreds of millions of units, creating a complex digital environment for families. As per the Consumer Technology Association, parents seek unified solutions that manage safety across all connected endpoints rather than isolated device controls. Parental control software integrating with smart home hubs can enforce rules across smartphones, tablets, and IoT devices seamlessly. Features such as voice activity monitoring on smart speakers and content filtering on connected TVs enhance comprehensive protection. The ability to manage screen time and access permissions from a single dashboard simplifies user experience. Partnerships with hardware manufacturers enable pre installation of safety software on new devices. This ecosystem approach addresses the fragmented nature of modern digital consumption. Parents value the convenience and thoroughness of holistic management solutions. The rise of remote learning and telehealth further increases reliance on connected devices. By expanding beyond mobile phones, vendors can capture a larger share of household safety spending. This diversification strengthens market position and drives long term growth.

MARKET CHALLENGES

Balancing Surveillance with Trust and Autonomy

Balancing surveillance with trust and autonomy is a major challenge to the U.S. parental control software market by creating familial tension. Excessive monitoring can undermine the parent child relationship, leading to resentment and secretive behavior. According to the American Psychological Association, adolescents require increasing levels of privacy and autonomy to develop healthy identity and decision making skills. As per a study published in Computers in Human Behavior, intrusive parental monitoring is associated with higher levels of anxiety and lower self esteem in teenagers. Parents struggle to find the right balance between protection and respect for privacy. Over reliance on software may hinder open communication about digital safety. Children may perceive monitoring as a lack of trust, damaging emotional bonds. Ethical considerations regarding the extent of surveillance vary widely among families and cultures. Software providers face difficulty in designing features that empower rather than oppress. The challenge lies in creating tools that facilitate dialogue rather than replace it. Some experts advocate for collaborative rule setting over unilateral restriction. The stigma associated with spying tools limits broader acceptance. Vendors must educate users on responsible usage and emphasize transparency. Failure to address these relational dynamics can lead to churn and negative reviews. Thus, the psychological impact of surveillance remains a critical hurdle.

Fragmentation of Devices and Operating Systems

Fragmentation of devices and operating systems poses significant technical challenges to the U.S. parental control software market by complicating compatibility and coverage. Families typically own multiple devices running different operating systems such as iOS, Android, Windows, and macOS. According to data from international tracking groups, the diversity of mobile devices and tablet models creates a fragmented landscape for software developers. As per Apple, strict privacy policies and sandboxing restrictions in iOS limit the depth of monitoring capabilities compared to Android systems. This inconsistency results in uneven protection levels across devices. Parents may find that features available on one platform are unavailable on another, leading to frustration. Maintaining compatibility with frequent operating system updates requires substantial development resources. New device categories such as wearables and gaming consoles add further complexity. Cross platform synchronization issues can lead to gaps in monitoring coverage. The inability to provide a uniform experience diminishes product value. Users may switch to native operating system controls that offer better integration albeit with fewer features. Developers must navigate varying app store guidelines and technical constraints. This fragmentation increases costs and slows innovation. Until standardization improves or cross platform solutions mature, this challenge will persist. It limits the effectiveness and appeal of comprehensive parental control suites.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 9.83% |

| Segments Covered | By Operating System, Deployment, Application, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Gen Digital Inc. (NortonLifeLock Inc.) (U.S. & Czech Republic), Alphabet Inc. (Google LLC) (U.S.), Microsoft Corporation (U.S.), McAfee, LLC (U.S.), AT&T Inc. (U.S.), Smith Micro Software, Inc. (U.S.), SafeDNS, Inc. (U.S.), Mobicip LLC (U.S.), Qustodio (Spain), and Bark (U.S.) |

SEGMENTAL ANALYSIS

By Operating System Insights

The android segment occupied the largest share of 44.9% of the U.S. market in 2025. This dominance is driven by the open nature of the operating system, which allows for deeper integration of monitoring tools, and the widespread adoption of Android devices among younger demographics due to affordability. Open architecture enabling deep monitoring capabilities drives the domination of Android in the U.S. parental control software market. Unlike closed ecosystems, Android permits third party applications to access extensive system permissions, including call logs, SMS messages, app usage, and location history. According to Google, Android powers a massive percentage of mobile devices, providing a vast install base for developers. As per Statista, Android holds a significant share of the US tablet market, which is heavily used by children for entertainment and education. The ability to overlay screens, block specific apps at the system level, and monitor background activities provides parents with comprehensive control. Developers can utilize accessibility services to detect screen content and enforce time limits more effectively than on restricted platforms. This technical flexibility allows for feature rich applications that offer granular management of device functions. Parents prefer Android devices for children because they can install robust safety solutions without jailbreaking or complex workarounds. The availability of diverse hardware options at various price points further increases penetration. The ecosystem supports a wide range of parental control apps, from free basic tools to premium suites. Consequently, the technical openness of Android sustains its leadership in the market. The ease of deployment and management ensures high user satisfaction and retention.

On the other side, the cross-platform solutions segment is estimated to showcase a promising CAGR of 14.4% during the forecast period owing to the increasing number of connected devices per household and the need for unified management. Proliferation of multi device households drives the rapid growth of Cross-Platform solutions in the U.S. parental control software market. Modern families own a mix of smartphones, tablets, laptops, and gaming consoles running different operating systems. According to Deloitte, the typical U.S. household operates an average of 21 connected devices, creating a complex digital environment. As per Parks Associates, over 80% of broadband homes have at least one smart speaker and multiple streaming devices requiring centralized management. Parents struggle to monitor activity across fragmented ecosystems using separate tools for each device type. Cross-platform solutions offer a unified interface to set rules, view reports, and manage screen time for all devices simultaneously. This convenience reduces administrative burden and ensures consistent safety policies. The ability to synchronize settings across iOS, Android, and Windows devices enhances user experience. Families value the holistic view of their childrens digital footprint regardless of the hardware used. The rise of remote learning has further increased the number of devices used for education at home. Cross-platform tools enable parents to balance educational and recreational usage effectively. This demand for simplicity and comprehensiveness accelerates adoption. The trend towards interconnected smart homes supports the expansion of these solutions. Consequently, the need for unified control sustains rapid growth.

By Deployment Insights

The cloud-based deployment segment accounted for the leading share of 84.4% of the U.S. market in 2025. This model involves hosting software and data on remote servers accessed via the internet. Its dominance is driven by ease of access, real time updates, and remote management capabilities. Accessibility and real time remote management drive the domination of Cloud Based deployment in the U.S. parental control software market. Parents can monitor and adjust settings from anywhere using any internet connected device. According to digital infrastructure tracking reports, global data networks continue to grow, supporting the reliability of cloud services. As per corporate software assessments, approximately 90% of buyers say ease of use is as important as product functionality, highlighting the value of accessible interfaces. Cloud based solutions allow parents to receive instant alerts about suspicious activity or location changes regardless of their physical presence. The ability to block websites or pause internet access remotely provides immediate intervention capabilities. This flexibility is crucial for working parents who need to manage digital safety while away from home. Cloud infrastructure ensures that data is backed up and secure, reducing the risk of loss. Automatic synchronization across devices ensures that rules are consistently applied. The elimination of local server maintenance reduces technical barriers for users. Parents appreciate the convenience of managing family safety through simple mobile apps. The scalability of cloud platforms supports growing numbers of devices and users. Consequently, the ease of access and control sustains cloud dominance. The alignment with modern mobile lifestyles ensures continued preference for cloud solutions.

On the other hand, the hybrid deployment segment is estimated to register a promising CAGR of 12.2% during the forecast period in the U.S. market. This model combines local device processing with cloud based management. The rising need for offline functionality and enhanced privacy control are boosting the expansion of the U.S. parental control software market growth. Need for offline functionality and local processing drives the rapid growth of Hybrid Deployment in the U.S. parental control software market. Pure cloud solutions rely on internet connectivity, which may be intermittent or unavailable. According to the Federal Communications Commission, rural areas in the US still face broadband gaps, making offline capabilities valuable. As per tracking assessments from industrial tech analysts, hybrid models allow for local enforcement of rules even when the device is disconnected from the internet. This ensures that screen time limits and app blocks remain active during travel or in areas with poor coverage. Local processing reduces latency for immediate actions such as blocking inappropriate content. Parents value the reliability of hybrid systems that do not fail due to network issues. The ability to store some data locally enhances performance and reduces bandwidth usage. Hybrid solutions offer a balance between cloud convenience and local resilience. This redundancy provides peace of mind for parents who depend on consistent protection. The technical advantage of offline operation appeals to users in diverse geographic locations. The growing expectation for uninterrupted service drives adoption. Consequently, the reliability of hybrid deployment sustains its growth. The combination of local and cloud benefits ensures robust performance.

By Application Insights

The residential segment led the market by accounting for 88.4% of the U.S. market share in 2025. The dominance of residential segment in the U.S. market is majorly driven by high consumer awareness and direct parental responsibility. High parental awareness and direct responsibility drive the domination of Residential application in the U.S. parental control software market. Parents are the primary decision makers for family digital safety and are increasingly educated about online risks. According to the American Academy of Pediatrics, parents are encouraged to create family media plans and use monitoring tools. As per Common Sense Media, over 70% of parents use some form of parental control to manage their childrens device usage. The emotional investment in child safety motivates purchases of premium software solutions. Parents seek tools that align with their specific values and parenting styles. The direct relationship between parent and child facilitates personalized rule setting and monitoring. Residential users are willing to pay for features that provide peace of mind and detailed insights. The widespread availability of consumer focused marketing campaigns raises awareness of available products. Social networks and community groups share recommendations and reviews, influencing purchasing decisions. The immediacy of residential needs drives quick adoption of new technologies. Parents act swiftly to address emerging threats, such as new social media trends. Consequently, the proactive stance of parents sustains market leadership. The personal nature of family safety ensures consistent demand.

On the other side, the educational institutes segment is estimated to showcase a CAGR of 15.1% during the forecast period owing to the integration of technology in schools and the need for compliant, safe learning environments. Mandates for safe digital learning environments drive the rapid growth of Educational Institutes in the U.S. parental control software market. Schools are required to filter harmful content to comply with federal regulations such as the Childrens Internet Protection Act. According to the Federal Communications Commission, schools must implement technology protection measures to receive E-rate funding. As per the National Center for Education Statistics, nearly all public schools have access to internet connected devices, necessitating robust management tools. Educational institutions adopt parental control software to ensure students access only appropriate educational resources. The shift to digital textbooks and online assignments increases reliance on filtered networks. Schools need to block distractions such as gaming and social media during class hours. Compliance with legal requirements drives institutional purchases of enterprise grade solutions. Administrators seek tools that provide detailed reporting and centralized management for thousands of devices. The responsibility to protect students from cyberbullying and inappropriate content motivates investment. The integration of these tools with learning management systems enhances functionality. Consequently, regulatory and ethical obligations sustain growth. The focus on safe education ensures long term demand.

COUNTRY LEVEL ANALYSIS

The U.S. held the largest share of the North American parental control software market in 2025. Over the next few years, the U.S. is likely to maintain absolute dominance across North American territories as domestic software vendors scale regional AI-driven features. The country's market status is characterized by high internet penetration, strong consumer spending on child safety, and advanced technological infrastructure. The prevalence of digital devices among youth drives significant demand for monitoring solutions. Dominance driven by high digital penetration and safety concerns defines the U.S. parental control software market. The widespread availability of high speed internet and smart devices creates a large addressable audience. According to the Pew Research Center, 95% of teens have access to a smartphone, creating an urgent need for oversight. As per the Centers for Disease Control and Prevention, rising rates of cyberbullying and mental health issues among adolescents motivate parents to seek protective tools. The cultural emphasis on child safety and well-being drives proactive adoption of monitoring software. The robust legal framework, including CIPA and COPPA, supports the development of compliant solutions. The presence of major technology companies fosters innovation in AI driven safety features. High disposable income allows families to invest in premium subscription services. The awareness of online predators and data privacy risks further stimulates demand. Educational initiatives in schools reinforce the importance of digital citizenship and safety. This combination of technological access and social concern ensures US leadership. The continuous evolution of online threats sustains market dynamism. The strategic focus on family safety reinforces this dominant position. The U.S. sets global trends in parental control technology and usage.

COMPETITIVE LANDSCAPE

The competition in the U.S. parental control software market is characterized by intense rivalry among specialized startups and established cybersecurity giants striving to offer superior protection and ease of use. Major players compete based on the accuracy of content filtering breadth of platform support and depth of monitoring insights. The market features a mix of subscription based services and one time purchase options catering to diverse budget preferences. Companies differentiate themselves through unique features such as AI driven sentiment analysis and real time alert systems. Strategic collaborations with educational institutions and child safety organizations help firms build credibility and reach target audiences. Price competitiveness remains a key factor particularly in the entry level segment where free or low cost alternatives exist. Innovation in user experience and dashboard design drives customer acquisition and retention. The rise of built in operating system controls poses a threat to third party providers requiring them to offer added value. Intellectual property related to detection algorithms serves as a competitive barrier. This dynamic environment fosters continuous improvement and innovation benefiting families with diverse and effective tools. The ability to adapt to new digital trends determines long term success.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. parental control software market are

- Gen Digital Inc. (NortonLifeLock Inc.) (U.S. & Czech Republic)

- Alphabet Inc. (Google LLC) (U.S.)

- Microsoft Corporation (U.S.)

- McAfee, LLC (U.S.)

- AT&T Inc. (U.S.)

- Smith Micro Software, Inc. (U.S.)

- SafeDNS, Inc. (U.S.)

- Mobicip.LLC (U.S.)

- Qustodio (Spain)

- Bark (U.S.)

Top Players in the Market

- Qustodio LLC is a leading provider of comprehensive parental control solutions in the U.S. market. The company offers robust features including screen time management app blocking and location tracking across multiple devices. Recent actions involve the integration of advanced artificial intelligence to detect cyberbullying and inappropriate content in real time. Qustodio has expanded its compatibility with various operating systems ensuring seamless protection for smartphones tablets and computers. The firm focuses on user friendly interfaces that empower parents to manage digital wellbeing effectively. By introducing detailed activity reports and instant alerts Qustodio enhances parental awareness and control. These innovations strengthen its reputation for reliability and ease of use. The company continues to invest in research and development to address emerging online threats. This commitment to safety and technology solidifies its position as a trusted partner for families seeking digital protection.

- Bark Technologies Inc contributes significantly to the market by specializing in monitoring social media and text messages for potential risks. The company uses sophisticated algorithms to identify signs of cyberbullying depression and online predation. Recent developments include the launch of Bark Phone a dedicated device with built in safety features. Bark has expanded its monitoring capabilities to cover more platforms and applications used by teenagers. The firm emphasizes privacy conscious monitoring that alerts parents only to serious issues. This approach balances safety with trust respecting adolescent autonomy. Bark actively collaborates with mental health experts to refine its detection models. The company also provides resources and support for families dealing with digital challenges. These efforts enhance its value proposition beyond simple restriction. By focusing on emotional wellbeing Bark distinguishes itself in the competitive landscape. This strategic focus drives customer loyalty and market growth.

- NortonLifeLock Inc plays a vital role in the U.S. parental control market through its Norton Family suite. The company integrates parental controls with comprehensive cybersecurity and identity protection services. Recent actions include enhancing web supervision features to block inappropriate sites and monitor search terms. Norton has improved its time management tools allowing parents to set specific schedules for device usage. The firm leverages its global security expertise to protect families from online threats and malware. Norton Family offers cross platform support ensuring consistent protection across all connected devices. The company focuses on providing actionable insights through detailed reporting dashboards. By bundling parental controls with antivirus software Norton offers a holistic safety solution. This integration appeals to parents seeking all in one protection for their digital lives. The brand recognition and trust in Norton security products drive adoption. These strategies reinforce its strong presence in the family safety sector.

Top Strategies Used by Key Market Participants

Key players in the U.S. parental control software market primarily employ strategies focused on artificial intelligence integration and cross platform compatibility to maintain competitive advantage. Companies invest heavily in machine learning algorithms to enhance content filtering and behavioral analysis capabilities. Strategic partnerships with device manufacturers enable pre installation of safety software on new hardware. Firms prioritize user friendly interfaces and mobile accessibility to improve parent engagement and ease of use. Expansion into mental health monitoring and cyberbullying detection addresses growing consumer concerns about emotional wellbeing. Providers also focus on transparent data privacy practices to build trust with privacy conscious users. Continuous updates to keep pace with evolving social media platforms and apps are essential for relevance. Marketing efforts emphasize education and resources for digital parenting to foster community loyalty. These strategic initiatives enable firms to differentiate their offerings and respond effectively to changing family needs in the dynamic digital safety sector.

MARKET SEGMENTATION

This research report on the U.S. parental control software market is segmented and sub-segmented into the following categories.

By Operating System

- Windows

- Android

- iOS & OS X

- Cross Platform & Others

By Deployment

- On premise

- Cloud

By Application

- Residential

- Educational Institutes

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

1.What is parental control software?

Parental control software helps parents monitor, manage, and restrict children's online activities across devices and digital platforms.

2.What factors are driving the growth of the U.S. parental control software market?

Growing concerns about online safety, increasing screen time among children, and rising awareness of digital parenting tools are driving market growth.

3.What devices commonly use parental control software?

Parental control software is widely used across smartphones, tablets, desktops, laptops, and gaming devices.

4.What features are commonly available in parental control software?

Common features include screen time management, website filtering, app blocking, location tracking, and online activity monitoring.

5.Which operating systems support parental control software?

Most solutions support Windows, Android, iOS, OS X, and cross platform operating systems.

6.What is cloud based parental control software?

Cloud based parental control software allows parents to remotely monitor and manage device usage through internet connected platforms.

7.Who are the major end users of parental control software?

Residential users and educational institutions are among the primary users of parental control software.

8.Why is parental control software becoming increasingly important in the U.S.?

Growing internet usage among children and concerns regarding harmful content exposure are increasing software adoption.

9.How do educational institutions benefit from parental control software?

Educational institutions use parental control tools to improve digital safety and manage internet access within learning environments.

10.What challenges impact the U.S. parental control software market?

Privacy concerns, compatibility limitations, and evolving cyber threats can affect market expansion.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com