U.S. Perforating Gun Market Size, Share, Trends, and Growth Analysis Report, Segmented by Carrier Type, Explosive Type, Well Type, and Country – Industry Forecast From 2026 to 2034

Market Size, 2025

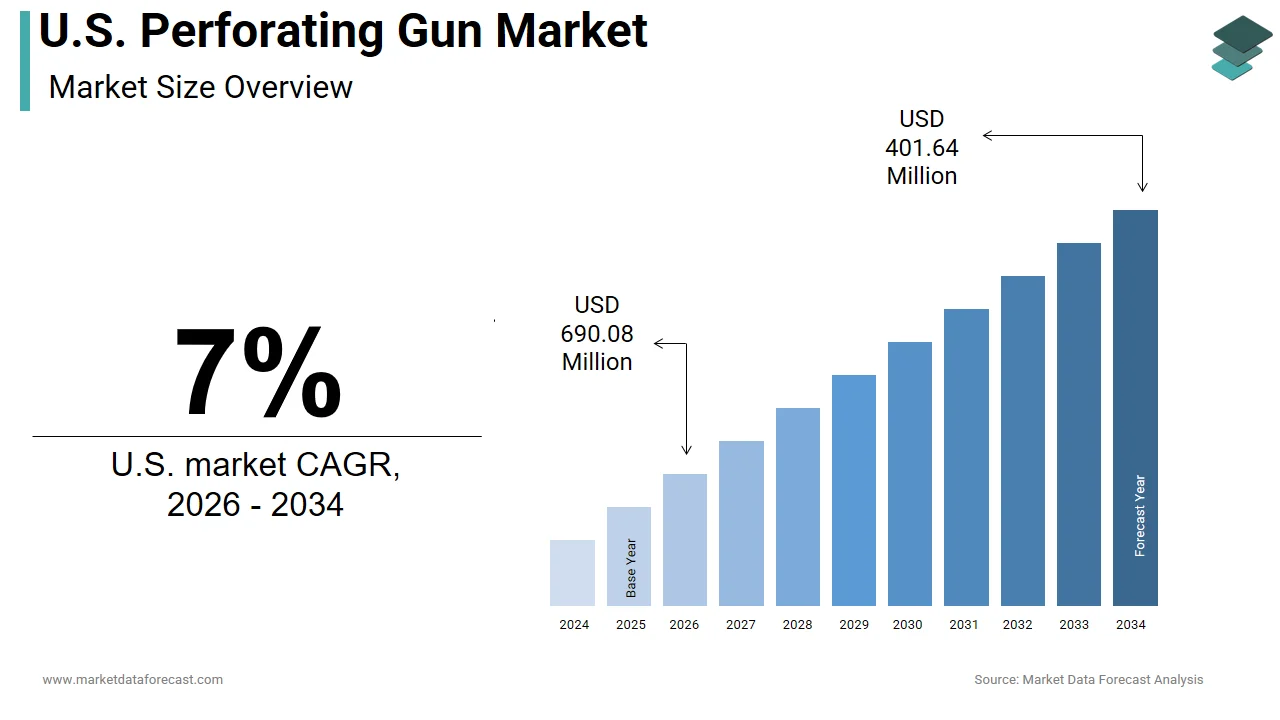

$375.36 MnMarket Estimate, 2026

$401.64 MnMarket Forecast, 2034

$690.08 MnCAGR, 2026–2034

7%U.S. Perforating Gun Market Report Summary

The U.S. perforating gun market was valued at USD 375.36 million in 2025 and is projected to grow from USD 401.64 million in 2026 to USD 690.08 million by 2034, registering a CAGR of 7% from 2026 to 2034. Market growth is driven by increasing oil and gas exploration activities, rising shale production, and growing demand for efficient well completion technologies across the United States. Perforating guns play a crucial role in establishing communication between the wellbore and hydrocarbon-bearing formations, enhancing production efficiency and reservoir recovery. Advancements in horizontal drilling, hydraulic fracturing technologies, and high-performance explosive systems are further supporting market expansion.

Key Market Trends

- Rising adoption of advanced well completion and hydraulic fracturing technologies.

- Increasing demand for high-performance perforating systems in unconventional oil and gas extraction.

- Growing investments in shale gas and tight oil exploration activities.

- Expansion of horizontal and directional drilling operations across major U.S. basins.

- Continuous advancements in explosive technologies and precision perforation systems.

Segmental Insights

- Based on carrier type, the hollow carrier segment dominated the U.S. perforating gun market in 2025 by accounting for a substantial share, driven by its durability, pressure resistance, and widespread usage in high-pressure well environments.

- Based on explosive type, the RDX segment held the majority share in 2025, supported by its high detonation performance, reliability, and effectiveness in deep well perforation applications.

Regional Insights

- The United States maintained a dominant position in the global perforating gun market in 2025 by capturing 39.7% share, driven by extensive shale reserves, advanced drilling infrastructure, and strong investments in upstream oil and gas activities. Increasing exploration and production activities across major regions such as the Permian Basin, Eagle Ford, and Bakken formations continue to support market growth.

Competitive Landscape

The U.S. perforating gun market is characterized by strong competition among oilfield service providers and well completion technology companies focusing on operational efficiency, safety, and advanced perforation solutions. Market participants are emphasizing the development of high-performance explosive systems, customized perforating technologies, and integrated well completion services to strengthen market positioning. Strategic partnerships, technological advancements, and investments in unconventional resource extraction are shaping competitive dynamics across the market.

Prominent companies operating in the U.S. perforating gun market include Baker Hughes Company, Schlumberger Limited, Weatherford International plc, NOV Inc., and Halliburton Company.

U.S. Perforating Gun Market Size

The size of the U.S. perforating gun market was worth USD 375.36 million in 2025. The market is anticipated to grow at a CAGR of 7% from 2026 to 2034 and be worth USD 690.08 million by 2034 from USD 401.64 million in 2026.

A perforating gun is a specialized tool used in the oil and gas industry during well completion. These tools are not ancillary but foundational to well productivity, serving as the critical interface between the engineered wellbore and the natural reservoir. According to data tracked by the U.S. Energy Information Administration (EIA) and industry engineering benchmarks, the vast majority of all newly completed onshore wells in the U.S. are horizontal, with modern multi-stage completions scaling drastically to utilize between 200 and 500+ individual perforation clusters per well to maximize reservoir contact. The technology has evolved from rudimentary bullet-based systems to sophisticated shaped charge arrays capable of penetrating casing under extreme downhole pressures exceeding twenty thousand pounds per square inch. According to the U.S. Energy Information Administration (EIA) and the American Petroleum Institute (API), the average lateral length of horizontal wells in major tight oil basins has climbed to over 10,000 feet, directly corresponding to an increased number of fracturing stages and perforation intervals per well. Operational precision is nonnegotiable. According to completion diagnostic studies published by the Society of Petroleum Engineers (SPE), uneven fluid distribution, misperforation, or cluster dominance can cause a significant portion of planned clusters to underperform, resulting in structural reservoir bypass and making downhole execution consistency paramount for initial production rates. Deployment is concentrated in the major unconventional basins, including the Permian, Eagle Ford, and Bakken, where multistage fracturing is standard practice. The market is shaped not by consumer trends but by geomechanical necessity, reservoir physics, and the relentless pursuit of recovery efficiency in mature and emerging plays.

MARKET DRIVERS

Escalating Multi-Stage Fracturing Activity in Unconventional Basins Is Driving Demand for High-Density Perforating Systems

The relentless expansion of multistage hydraulic fracturing operations across major U.S. shale plays is the principal force propelling growth in the United States perforating gun market. Consequently, there is a growing need for advanced, high-density perforating gun systems capable of delivering precision under extreme conditions. According to tight oil completion trend reviews, the average horizontal well drilled in the Permian Basin features an increasing stage density with operators compressing cluster spacing down to 30–50 feet to optimize fracture network surface areas and enhance oil recovery. According to the Society of Petroleum Engineers, operators in the Eagle Ford and Bakken plays now routinely deploy over fifty clusters per lateral in pursuit of enhanced reservoir contact and improved estimated ultimate recovery. This intensification is not optional but economically mandated. According to completion diagnostic studies, wells designed with tighter cluster spacing and optimized perforation designs can significantly increase initial production rates by maximizing the total fracture surface area in contact with the reservoir. Equipment specifications have evolved accordingly. As per SLB Perforating System Technical Specifications, modern high-density perforating guns routinely house up to 6 to 12 shaped charges per foot and are engineered to reliably withstand harsh downhole environment differential pressures up to 15,000 to 20,000 psi. The logistical scale is immense. According to field operations benchmarks from major oilfield service providers like Halliburton and SLB, a single modern extended-reach horizontal well with 40 to 60 fracturing stages can require between 1,500 and 4,000+ individual shaped charges. This operational complexity and volume intensity ensure sustained, noncyclical demand for next-generation perforating systems.

Regulatory Emphasis on Well Integrity and Zonal Isolation Is Forcing Adoption of Precision Engineered Perforating Tools

Operators are abandoning legacy perforation methods due to heightened federal and state regulatory scrutiny over wellbore integrity and groundwater protection, which further propels the expansion of the United States perforating gun market. To comply, they are turning to precision-engineered systems that guarantee zonal isolation and minimize casing damage. State regulatory frameworks and the EPA emphasize strict well-construction standards, requiring multiple layers of steel casing and robust cement isolation specifically to prevent any migration of fluids into shallow freshwater aquifers. In response, states such as Colorado, Pennsylvania, and New Mexico have enacted stringent well construction rules mandating third-party verification of perforation quality and cement bond logs before fracturing. The technical threshold is exacting. According to API Recommended Practice 19B, well perforating systems must undergo rigorous, standardized testing protocols to objectively measure penetration depth, core flow efficiency, and casing impact characteristics under strict quality controls. Failure carries severe penalties. Under Statewide Rule 13 of the Railroad Commission of Texas, operators must maintain rigorous casing and cementing integrity protocols; non-compliant operators face formal enforcement actions, including statutory financial penalties and the potential suspension of operating certificates. This regulatory architecture has transformed perforating guns from commodity consumables into engineered safety systems, where certification, traceability, and performance validation are now contractual prerequisites rather than optional upgrades.

MARKET RESTRAINTS

High Operational Failure Rates in Extreme Pressure Environments Are Constraining Equipment Reliability and Increasing Non-Productive Time

The persistent occurrence of perforating gun misfires, partial detonations, and mechanical failures under ultra-high-pressure downhole conditions remains a critical operational constraint, slowing the growth of the United States perforating gun market. This directly inflates completion costs and delays first production timelines across major U.S. basins. In high-pressure, high-temperature (HPHT) environments exceeding 15,000 psi, operators face significantly elevated risk profiles for mechanical and electrical downhole misfires, requiring advanced pressure-rated gun systems to prevent fluid ingress and preserve the ballistic sequence. According to completion operations engineering reviews, downhole perforation failures introduce significant Non-Productive Time (NPT) due to the need to safely pull out of the hole (POOH) and re-run tool strings, accumulating tens of thousands of dollars in daily spread-cost overruns. The root cause is multifactorial. According to petroleum mechanical specifications, extreme hydrostatic differential pressures can compromise and collapse low-tier gun carriers, while ambient downhole temperatures exceeding 300°F cause rapid thermal degradation of standard RDX explosives, requiring transition to premium thermal stabilizers like HMX or HNS. The financial impact is systemic. Operational overruns stemming from completion delays and equipment failures significantly impact operator capital efficiency in tight oil plays, making tool reliability a primary metric for corporate cost control. Mitigation efforts are costly. Field completion models prove that the upfront cost of deploying high-strength alloy carriers and premium redundant addressable switches is heavily offset by avoiding the catastrophic costs of deep-well remedial fishing operations. Reliability remains the dominant bottleneck in operational efficiency. This will remain true until materials science and detonation physics overcome the current environmental thresholds.

Supply Chain Fragmentation for Specialty Explosives Is Disrupting Manufacturing Consistency and Field Deployment Schedules

The highly fragmented and heavily regulated supply chain for military-grade explosives and detonation components used in these guns is systematically undermining manufacturing predictability and field-level availability across the United States, perforating the gun market. Due to the hazardous nature of manufacturing premium oilfield energetics, production is concentrated among a small group of specialized chemical defense and oilfield service providers subject to heavy oversight under Federal Explosives Laws. Commercial shaped-charge manufacturers rely on highly controlled, fresh industrial chemical supply pipelines to ensure that powder grain distribution and liner geometries match strict quality tolerances for precise downhole penetration. This dependency introduces severe volatility. Broad global manufacturing disruptions and logistics logjams have driven up supply lead times for critical oilfield components across the sector, prompting major service providers to optimize their local inventory footprints. Field operations are directly impacted. Supply chain constraints in oilfield equipment sectors disproportionately impact small-to-mid-cap operators who lack the multi-year volume purchase agreements maintained by major multinational operators. Regulatory compliance compounds the bottleneck. Under PHMSA hazardous materials regulations, the commercial transport of loaded perforating guns requires adherence to pre-established hazardous material trucking routes and strict placarding laws to ensure public safety without requiring individual load-by-load routing approvals. Supply fragility will remain a structural impediment to market scalability. This will persist until domestic explosive manufacturing capacity expands under civilian oversight.

MARKET OPPORTUNITIES

Advancements in Fiber Optic-Enabled Real-Time Perforation Diagnostics Are Unlocking Precision Completion Optimization

The integration of distributed fiber optic sensing with perforating gun systems is creating unprecedented opportunities for real-time, downhole verification of charge performance and fracture initiation, which is likely to boost the growth of the United States perforating gun market. This enables operators to dynamically adjust completion designs and maximize reservoir contact. According to tight-oil completion benchmarks, permanent or carbon-rod deployed fiber optic lines run outside the casing utilize Distributed Acoustic Sensing (DAS) to analyze fluid distribution and cluster efficiency, rather than measuring the active ballistic sequence within the perforating gun. Field validation data from oilfield service leaders proves that interpreting real-time DAS fiber data allows completion engineers to modify fracture treatment designs dynamically, optimizing cluster efficiency and fluid allocation across underperforming zones. The economic value is quantifiable. Case studies archived by the Society of Petroleum Engineers (SPE) indicate that leveraging fiber-optic diagnostic insights helps operators eliminate non-performing clusters, leading to long-term improvements in wellbore production and capital efficiency. Deployment is accelerating. The technology also satisfies regulatory mandates. State regulatory frameworks like those managed by the Colorado ECMC require standard acoustic cement bond logging to strictly verify well integrity and protect local aquifers prior to any high-pressure stimulation. This convergence of diagnostics, compliance, and performance optimization is transforming perforating guns from passive tools into intelligent, data-generating systems that actively enhance recovery economics.

Expansion into Geothermal and Carbon Storage Applications Is Opening New Revenue Channels Beyond Hydrocarbons

The adaptation of oilfield perforating gun technology for engineered geothermal systems and carbon dioxide sequestration wells is driving a new industrial shift, which is predicted to fuel the expansion of the United States perforating gun market. It is creating a structurally distinct and rapidly expanding market segment that remains uncorrelated with oil price volatility. According to the U.S. Department of Energy (DOE), Enhanced Geothermal Systems (EGS) increasingly adapt conventional petroleum perforating and fracturing equipment to create artificial permeability pathways within deep, low-permeability crystalline granite structures. Mechanical assessments show that perforating hard granite formations for geothermal circulation loops requires specialized, deep-penetrating shaped charges designed to withstand high rock compressive strengths without using extreme shot densities that compromise the wellbore shell. Carbon storage presents even greater scale. Data from the Global CCS Institute highlights that while hundreds of Class VI carbon disposal well applications are under review, the actual pace of formal permit issuance by regulatory agencies remains a key bottleneck for carbon capture deployment. The technical requirements are stringent. Under the U.S. Environmental Protection Agency (EPA) UIC program, Class VI operators must demonstrate long-term wellbore integrity and zone containment through robust mechanical integrity testing (MIT) to ensure the stored carbon dioxide remains permanently isolated. Equipment manufacturers are responding. Corporate financial disclosures from major energy service providers like SLB highlight expanding capital commitments toward new energy horizons, adapting traditional wellbore logging, completion, and perforating technologies for carbon capture and geothermal markets. This diversification not only diversifies revenue streams but also aligns product development with federal decarbonization mandates, ensuring long-term market relevance beyond fossil fuels.

MARKET CHALLENGES

Material Science Limitations in Gun Carrier Design Are Impeding Performance in Ultra-Deep and High-Temperature Wells

Conventional steel alloy gun carriers struggle to withstand the combined stresses of extreme heat, ultra-high pressure, and corrosive fluids, which challenge the growth of the United States perforating gun market. This failure severely limits perforation efficiency in next-generation deep basin and geothermal applications. In ultra-deep wells exceeding 20,000 feet, downhole tools face extreme hydrostatic pressures that can cause plastic deformation or collapse in standard-tier steel gun carriers, requiring operators to transition to high-strength, low-alloy carbon steels with minimum yield strengths exceeding 125,000 psi to maintain tool alignment. Technical case studies archived by the Society of Petroleum Engineers (SPE) note that excessive external pressure in deep shale plays can compress or crush perforation gun tubes prior to firing, creating mechanical misruns that disrupt the ballistic chain and require specialized pressure-rated engineering solutions. Temperature exacerbates the problem. Metallurgical data shows that while prolonged exposure to ultra-high temperatures weakens downhole equipment, the immediate operational constraint at 400°F is the thermal destabilisation of standard ballistic explosives, which mandates the use of premium heat-stabilized explosive compounds like HMX or HNS. Corrosive environments compound degradation. In highly sour environments containing hydrogen sulfide (H2S), carbon steel downhole tools are highly vulnerable to Sulfide Stress Cracking (SSC) and hydrogen embrittlement, requiring adherence to strict material hardness limits (such as a maximum of 22 HRC) per NACE MR0175/ISO 15156 standards. To combat corrosive sour gas and high-pressure downhole environments cost-effectively, the oilfield services sector relies on specialized heat-treated carbon steel alloys optimized for hardness and tensile performance, avoiding the prohibitive manufacturing costs associated with exotic metals. Performance ceilings will persist in the most technically demanding wells. This will remain the case until cost-effective, high-strength composite or functionally graded materials achieve commercial readiness.

Lack of Standardized Performance Metrics and Field Validation Protocols Is Undermining Operator Confidence and Procurement Consistency

The absence of universally accepted performance benchmarks and independent field validation protocols for perforating gun systems is eroding operator confidence, which inhibits the expansion of the United States perforating gun market. Consequently, this inflates procurement risk and fragments vendor selection criteria. Operator engineering teams select ballistic perforating tools based on standardized performance testing protocols overseen by industry standard bodies, ensuring that charge penetration values conform to independent design baselines. According to testing data from Core Laboratories' Energetics Division, shaped-charge ballistic profiles are engineered to deliver highly uniform penetration and consistent entry-hole diameters, allowing operators to minimize formation tortuosity and accurately model downstream hydraulic fracturing friction. Field outcomes vary dramatically. The financial consequence is severe. Downhole execution failures and sub-optimal perforation cluster efficiency negatively impact localized well productivity and capital returns, prompting operators to prioritize strict completion quality control. Regulatory bodies are beginning to respond. Procurement remains a high-risk, low-transparency exercise that suppresses innovation and inflates operational uncertainty. This will continue until industry-wide standards are codified and enforced.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Carrier Type, Explosive Type, Well Type, and Country. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Baker Hughes Company, Schlumberger Limited, Weatherford International plc, NOV Inc., Halliburton Company, and Others |

SEGMENTAL ANALYSIS

By Carrier Type Insights

The Hollow Carrier segment dominated the United States perforating gun market, accounting for a substantial share in 2025. This dominance of the segment was driven by its operational versatility, cost efficiency, and compatibility with the vast majority of conventional and unconventional well completions across major basins. In major tight-oil plays like the Permian and Eagle Ford basins, hollow carrier gun systems are the primary completion tool chosen by operators because their sealed design keeps wellbore fluids away from explosives and contains explosive debris to prevent the tool string from sticking downhole. The economic calculus is decisive. Standard hollow carrier systems provide a highly predictable and cost-effective completion methodology, delivering consistent entrance-hole diameters across a broad spectrum of rock compressive strengths. Deployment logistics further entrench this preference. Perforation gun strings built from hollow carriers rely on rigid, pre-assembled mechanical configurations, which eliminate mechanical moving parts and minimize the risk of structural tool failure as the string is conveyed downhole. Regulatory acceptance also plays a role. Evaluation and certification protocols for commercial oilfield perforating gun systems are strictly governed by API Recommended Practice 19B, which provides operators with standardized performance baselines across the industry. This trifecta of cost, reliability, and standardization ensures continued market hegemony despite technological alternatives.

On the other hand, the Expandable Shaped Charge Gun segment is predicted to witness the highest CAGR of 18.9% from 2026 to 2034 due to its unique ability to maintain charge standoff and alignment in highly deviated and extended reach laterals where casing eccentricity renders conventional carriers ineffective. The technology is becoming indispensable in next-generation completions. To maximize cluster efficiency and bypass placement deviations in extended-reach laterals exceeding 15,000 feet, operators rely on advanced wireline tractoring and specialized decentralized hollow carriers to ensure a consistent casing clearance during detonation. Performance in extreme environments further fuels adoption. Ultra-deep and geothermal reservoir applications demanding performance under high hydrostatic pressures require premium high-strength low-alloy steel carriers rated for extreme environments, rather than expandable alloy structures. Field economics are improving. Industry efforts to lower well-completion costs focus heavily on automating the assembly of conventional, modular hollow carrier gun systems to reduce manual handling risks and optimize field-deployment timelines. This convergence of technical necessity and cost reduction is unlocking rapid adoption in the most demanding well architectures.

By Explosive Type Insights

The RDX segment held the majority share of the United States perforating gun market in 2025. This supremacy of the segment was credited to its optimal balance of detonation velocity, cost efficiency, and regulatory accessibility for commercial oilfield use. The Cyclotrimethylene Trinitramine is commonly known as RDX. Under federal explosives regulations enforced by the ATF, RDX, HMX, and HNS are subjected to identical storage, tracking, and permit requirements, with RDX serving as the standard industry baseline due to its widespread commercial synthesis and manufacturing availability. Performance characteristics further cement its leadership. According to energetic material specifications, RDX-based shaped charges provide high detonation velocities that generate hyper-velocity metallic jets, which are structurally optimized to pierce standard cased-hole configurations under conventional downhole pressures. Cost differentials are decisive. Commercial procurement models show that RDX remains the most economical explosive choice for standard well completions, whereas specialized high-temperature stabilizers are reserved for deep wells due to their higher raw chemical manufacturing costs. Supply chain resilience also favors RDX. This combination of regulatory permissibility, adequate performance, and economic scalability ensures RDX will remain the backbone of the market despite the emergence of higher energy alternatives.

But the Hexanitrostilbene, or HNS, segment is estimated to register the fastest CAGR of 24.3% over the forecast period, owing to its unparalleled thermal stability and reliability in ultra-high temperature wells where conventional explosives decompose or misfire. High-temperature wellbore profiles show that while standard RDX decomposes near 400°F, HMX provides stable downhole operations up to 500°F, and premium HNS is deployed for extreme-temperature environments due to its ability to resist thermal runaway up to 540°F. This makes HNS the only viable option for deep gas plays such as the Haynesville and emerging geothermal wells in Nevada and Utah, where bottom hole temperatures routinely exceed four hundred degrees. Regulatory mandates are accelerating adoption. Field validation confirms performance. Field performance data from oilfield service providers indicates that substituting HNS for HMX in environments nearing 500°F dramatically minimizes the risk of thermal misruns, ensuring a reliable ballistic sequence across deep, high-temperature completion zones. Collaborative developments between chemical manufacturers and oilfield suppliers focus on stabilizing the availability of premium energetic compounds, ensuring cost-effective deployment options for ultra-deep and geothermal exploration initiatives. This niche but nonsubstitutable role ensures explosive growth in the most technically extreme wells.

COUNTRY ANALYSIS

The United States led the global perforating gun market and captured a 39.7% share in 2025. It serves as the primary innovation hub and largest consumption base for advanced downhole perforation systems. This top position is also supported by decades of unconventional resource development, regulatory codification, and private sector investment in extreme environment tool reliability. According to global oilfield service benchmarks, completion methodologies optimized within the high-volume shale plays of the United States serve as a leading operational blueprint for international operators seeking to maximize reservoir drainage across unconventional reservoirs. Domestic manufacturers dominate global supply chains. According to global oilfield logistics tracking, specialized ballistic perforating guns, custom charge carriers, and high-performance energetics engineered in the United States are heavily exported to active drilling hubs, such as Canada, Saudi Arabia, and Argentina, to handle complex horizontal downhole environments. Regulatory frameworks developed in Texas and Colorado have been adopted internationally. Technical standards developed by the American Petroleum Institute (API), specifically testing certifications governed under API RP 19B, are voluntarily integrated into company-specific engineering manuals and field safety guides by major global operators to harmonize completion performance parameters. Research and development intensity remains unmatched. Global patent data indicates that major multi-national oilfield service providers based in the United States drive a high percentage of technical innovations regarding real-time downhole monitoring, debris-free gun geometries, and high-temperature ballistic execution. This convergence of market scale, regulatory influence, and technological innovation ensures the United States will remain the gravitational center of perforating gun advancement and deployment for the foreseeable future.

COMPETITIVE LANDSCAPE

Competition in the United States perforating gun market is defined by technological precision, operational reliability, and regulatory compliance rather than price alone. The market is dominated by integrated oilfield service giants possessing in-house explosive manufacturing, metallurgical engineering, and field deployment capabilities. These players compete on penetration consistency, debris management, and survival under extreme pressure rather than cost per foot. Differentiation is achieved through proprietary charge formulations, real-time diagnostics, and digital integration with completion management software. Smaller niche manufacturers compete by specializing in ultra-high temperature or corrosion-resistant applications where performance justifies premium pricing. Regulatory frameworks act as both barrier and enabler, with compliance to API and state mandates determining vendor eligibility. Supply chain control is a critical battleground, as access to certified explosives and pressure-rated alloys dictates delivery timelines. Collaboration with national laboratories and universities is common to validate performance claims. International expansion is pursued not through volume but through technology transfer, positioning U.S. systems as the global standard for extreme environment completions. Innovation cycles are rapid, driven by operator demands for higher stage counts and tighter cluster spacing. This environment rewards engineering excellence, field validation, and regulatory fluency above all else.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. perforating gun market include

- Baker Hughes Company

- Schlumberger Limited

- Weatherford International plc

- NOV Inc.

- Halliburton Company

TOP PLAYERS IN THE MARKET

- Schlumberger Limited maintains a commanding presence in the United States perforating gun market through its integrated well construction and intervention portfolio. The company engineers proprietary shaped charge systems optimized for extreme pressure and high temperature environments, particularly in the Permian and Haynesville basins. In early 2024, Schlumberger launched its latest generation Quantum XP perforating platform featuring real-time downhole diagnostics and automated charge alignment. It also expanded its Texas-based explosive component manufacturing facility to ensure domestic supply chain resilience. Globally, Schlumberger’s systems are deployed in deepwater Gulf of Mexico, Middle Eastern carbonate reservoirs, and geothermal projects in Southeast Asia, exporting U.S. engineered reliability to international high-stress applications.

- Halliburton Company leverages its extensive North America field network and decades of perforation engineering to deliver application-specific gun systems tailored to regional geologies. The company emphasizes operational efficiency through modular gun designs that reduce rig time and minimize non-productive events. In late 2023, Halliburton introduced its DuraCluster perforating system with enhanced debris containment and thermally stable charges for extended laterals. It also partnered with U.S. national laboratories to validate performance under ultra-high differential pressures. Internationally, Halliburton supplies perforating tools for high-pressure wells in Argentina’s Vaca Muerta and Saudi Arabia’s unconventional plays, transferring U.S. multistage expertise to emerging shale markets while adapting to local regulatory frameworks.

- Baker Hughes Company differentiates itself through advanced materials science and digital integration in its perforating gun offerings. Its systems incorporate corrosion-resistant alloys and fiber optic-enabled diagnostics to verify charge performance before fracturing initiation. In mid-2024, Baker Hughes unveiled its SpectraGun XP platform featuring machine learning-driven cluster optimization based on real-time rock mechanics data. The company also established a dedicated high-temperature explosive testing facility in Oklahoma to accelerate product validation. Globally, Baker Hughes deploys its U.S.-developed systems in geothermal wells in Italy and carbon storage projects in Norway, extending the application of American perforation technology beyond hydrocarbons into energy transition infrastructure.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Leading participants in the United States perforating gun market pursue a tightly integrated set of strategies to maintain technological leadership and operational dominance. First, they invest heavily in materials science to enhance gun carrier integrity under extreme downhole conditions. Second, they embed real-time diagnostics into tool strings to provide verification of charge performance prior to fracturing. Third, they vertically integrate explosive component manufacturing to ensure supply chain security and regulatory compliance. Fourth, they tailor charge density and penetration profiles to specific basin geologies through extensive laboratory and field testing. Fifth, they partner with national laboratories and universities to validate performance under simulated ultra-high pressure environments. Sixth, they develop modular and reusable gun systems to reduce rig time and operational cost. Seventh, they expand into non-hydrocarbon applications such as geothermal and carbon storage to diversify revenue. Eighth, they train field crews extensively to minimize deployment errors and non-productive time. Ninth, they align product development with evolving state and federal well construction regulations. Tenth, they export U.S.-engineered systems globally to set international performance benchmarks.

U.S. PERFORATING GUN MARKET NEWS

- In February 2024, Schlumberger Limited inaugurated its expanded shaped charge manufacturing line in Houston, Texas, to increase domestic production capacity and reduce lead times for high-demand perforating systems in the United States perforating gun market.

- In November 2023, Halliburton Company launched its DuraCluster perforating system with integrated debris containment and thermally stable charges designed for extended laterals in the Permian Basin, strengthening its position in the United States perforating gun market.

- In May 2024, Baker Hughes Company opened its high-temperature explosive validation facility in Tulsa, Oklahoma, to accelerate testing and certification of perforating tools for deep gas and geothermal applications in the United States perforating gun market.

- In August 2023, Schlumberger Limited partnered with Sandia National Laboratories to co-develop next-generation gun carrier materials capable of withstanding pressures exceeding twenty-eight thousand pounds per square inch in the United States perforating gun market.

- In January 2024, Halliburton Company signed a long-term supply agreement with a major independent operator in the Eagle Ford Shale to provide customized perforating solutions for high-pressure intervals, reinforcing its footprint in the United States perforating gun market.

MARKET SEGMENTATION

This research report on the U.S. perforating gun market has been segmented and sub-segmented into the following categories.

By Carrier Type

- Hollow Carrier

- Expandable Shaped-Charged Gun

- Other Carrier Types

By Explosive Type

- Cyclotrimethylene Trinitramine (RDX)

- Cyclotetramethylene Trinitramine (HMX)

- Hexanitrosilbene (HNS)

By Well Type

- Horizontal and Deviated Well

- Vertical Well

By Country

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

What is the U.S. perforating gun market?

The U.S. perforating gun market supplies downhole tools that create openings in well casing and formation rock to improve oil and gas flow.

How does the U.S. perforating gun market function?

The U.S. perforating gun market works by deploying shaped charges into wells through wireline or tubing-conveyed systems for controlled perforation.

What drives growth in the U.S. perforating gun market?

The U.S. perforating gun market grows from shale drilling, unconventional resource development, and higher upstream spending.

Which segments lead the U.S. perforating gun market?

Conventional perforating guns lead the U.S. perforating gun market, while intelligent guns are gaining traction for advanced well operations.

What role do shaped charges play in the U.S. perforating gun market?

Shaped charges are the core of the U.S. perforating gun market because they penetrate casing and rock to create flow channels.

How important is wireline deployment in the U.S. perforating gun market?

Wireline deployment is important in the U.S. perforating gun market for accurate positioning and efficient perforation in cased wells.

What is tubing conveyed perforating in the U.S. perforating gun market?

Tubing conveyed perforating is a method in the U.S. perforating gun market that allows guns to be run into wells through tubing strings.

What trends shape the U.S. perforating gun market?

The U.S. perforating gun market is shaped by automation, deeper wells, precision completion tools, and demand for faster well readiness.

What challenges face the U.S. perforating gun market?

The U.S. perforating gun market faces safety concerns, tool reliability requirements, and pressure from volatile drilling activity.

How does shale activity affect the U.S. perforating gun market?

Shale activity supports the U.S. perforating gun market by increasing demand for well completion and reservoir access tools.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com