U.S. Pet Care Market Size, Share, Trends & Growth Forecast Report By Product, By Pet Type, By Distribution Channel, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Pet Care Market Size

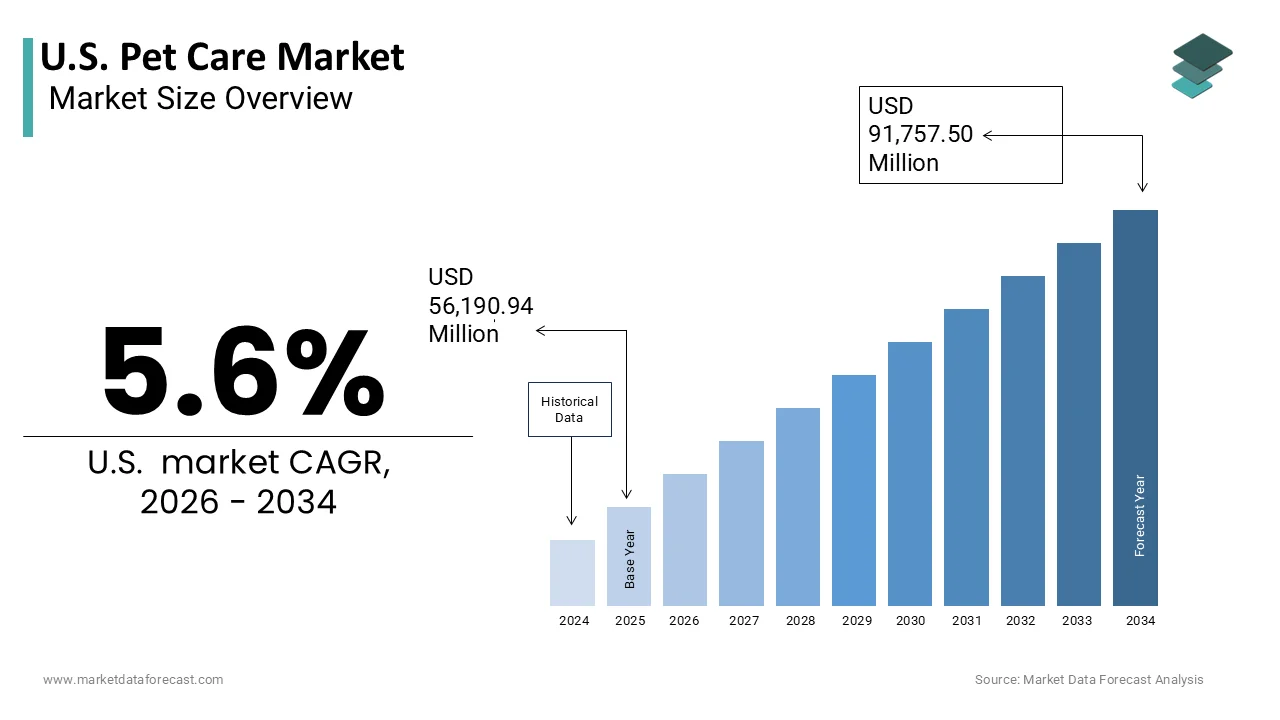

The United States Pet Care Market was valued at USD 56,190.94 million in 2025, is estimated to reach USD 59,337.64 million in 2026, and is projected to reach USD 91,757.50 million by 2034, growing at a CAGR of 5.6% from 2026 to 2034.

The pet care is to support the health, wellness, and overall quality of life for companion animals, primarily dogs and cats. The significant component of the consumer economy is riven by the humanization of pets, where animals are increasingly viewed as family members. As per the American Veterinary Medical Association, approximately 66% of US households own at least one pet, indicating a vast and engaged consumer base. Furthermore, spending on veterinary services and pet products has consistently outpaced general inflation rates in recent years,s demonstrating the resilience and priority of this expenditure category. The proliferation of dual-income households and delayed parenthood has further intensified this trend as individuals seek companionship and emotional support from animals. Regulatory frameworks regarding animal welfare and food safety also ensure high standards for product quality and service delivery. The integration of digital technologies such as telemedicine and automated feeding devices is transforming traditional care models.

MARKET DRIVERS

Humanization of Pets and Premiumization of Products

The profound humanization of pets by shifting consumer behavior toward purchasing premium and specialized products that mirror human lifestyle choices is propelling the growth of the United States pet care market. Owners increasingly view their pets as integral family members, leading to a willingness to spend on high-quality organic foods, luxury accessories, and advanced healthcare services. As per the Packaged Facts survey, over 70% of pet owners consider their pets to be part of the family, which directly influences their purchasing decisions toward higher-end brands. This emotional connection drives demand for grain-free raw and limited-ingredient diets that cater to specific health needs and dietary preferences. The trend extends to grooming and wellness, where spa-like treatments and natural skincare products are gaining popularity. Consumers are also investing in smart technology, such as GPS trackers and health monitoring devices, to ensure the safety and well-being of their companions. The premiumization trend is evident in the retail sector,r where specialty pet stores and boutique brands thrive alongside traditional supermarkets. This shift is supported by marketing strategies that emphasize emotional bonding and holistic health. Consequently, the desire to provide the best possible life for pets fuels continuous innovation and expansion in the market, et ensuring robust demand for high-value products and services that enhance the human animal relationship.

Increasing Focus on Preventive Healthcare and Wellness

The growing emphasis on preventive healthcare and wellness by encouraging regular veterinary visits and the adoption of health monitoring tools is another attribute fuelling the growth of the United States pet care market. Pet owners are becoming more proactive in managing their animals' health,h seeking early detection of diseases and maintaining optimal physical condition through balanced nutrition and exercise. Spending on veterinary care and product sales has risen steadily, with preventive services, such as vaccinations, dental cleanings, and annual checkups, which are becoming standard practices. The increased awareness of the benefits of early intervention can reduce long-term medical costs and extend the lifespan of pets. The rise of pet insurance further supports this trend by making preventive care more affordable and accessible to a broader demographic. Wellness products, including supplements, probiotics, and joint support formulas,s are increasingly integrated into daily routines to address age-related issues and maintain vitality. Digital health platforms and telemedicine services offer convenient access to professional advice, enabling owners to monitor symptoms and receive guidance without immediate clinic visits. This holistic approach to pet health fosters a culture of responsibility and care, driving consistent demand for veterinary services and wellness products.

MARKET RESTRAINTS

High Cost of Veterinary Care and Insurance Premiums

The high cost of veterinary care and insurance premiums, by limiting access to essential services for budget-conscious owners, is hindering the growth of the United States pet care market. Advanced medical procedures,s diagnostic tests, ts and emergency treatments can incur substantial expenses that are often not covered by basic insurance plans. As per the North American Pet Health Insurance Association, the average annual premium for pet insurance has increased significantly, reaching over 500 dollars for dogs and 300 dollars for cats in recent years. This financial burden forces many owners to delay or forego necessary medical attention, leading to poorer health outcomes and higher long-term costs. The complexity of insurance policies with varying deductibles, coverage limits, and exclusions further complicates decision-making for consumers. Additionally, the shortage of veterinary professionals in certain regions drives up service prices due to limited supply and high demand. Economic uncertainty and inflation exacerbate these challenges as households prioritize essential human needs over pet care expenditures. The lack of standardized pricing for veterinary services creates transparency issues, making it difficult for owners to budget effectively. Consequently, the high financial barrier to comprehensive healthcare restricts market growth among lower-income demographics and limits the adoption of premium services. Addressing affordability remains a critical challenge for the industry to ensure equitable access to quality care.

Supply Chain Disruptions and Ingredient Sourcing Challenges

The supply chain disruptions and ingredient sourcing challenges, by affecting the availability and cost of raw materials for pet food and products, are also hampering the growth of the United States pet care market. The reliance on global supply chains for key ingredients, such as meat, grains, and specialized additives, makes the industry vulnerable to geopolitical tensions, climate change,e and logistical hurdles. The fluctuations in agricultural production and trade policies have led to volatility in commodity prices, impacting manufacturing costs for pet food producers. These disruptions can result in product shortages, delayed deliveries, and increased prices for consumers,s undermining brand loyalty and trust. The demand for sustainable and ethically sourced ingredients further complicates sourcing efforts as suppliers must adhere to strict environmental and welfare standards. Limited availability of high-quality proteins and novel ingredients restricts product innovation and formulation flexibility. Additionally, transportation costs and labor shortages in the logistics sector contribute to operational inefficiencies and margin compression for manufacturers. The unpredictability of supply chains requires companies to maintain larger inventories and diversify suppliers, which increases working capital requirements.

MARKET OPPORTUNITIES

Expansion of E-Commerce and Direct-to-Consumer Models

The expansion of e-commerce and direct-to-consumer models by offering convenience, personalization, and broader product accessibility is certainly contributing to bolster new opportunities for the growth of the United States pet care market. Online platforms enable owners to purchase food supplies and accessories from the comfort of their homes with subscription services by ensuring the timely replenishment of essential items. The e-commerce sales in the retail sector have grown substantially, with pet products representing a rapidly expanding category driven by the ease of home delivery. Direct-to-consumer brands leverage data analytics to customize offerings based on individual pet profiles, such as breed, age,e and health conditions, by enhancing customer satisfaction and loyalty. Social media and digital marketing allow niche brands to reach targeted audiences effectively, fostering community engagement and brand advocacy. The ability to offer exclusive online bundles and promotional deals attracts price-sensitive consumers while maintaining premium positioning. Additionally, the rise of telehealth services integrated with e-commerce platforms provides holistic care solutions combining medical advice with product recommendations.

Innovation in Sustainable and Eco-Friendly Products

The innovation in sustainable and eco-friendly products by aligning with the growing environmental consciousness of modern consumers is another attribute to enhance the growth of the United States pet care market. Pet owners are increasingly seeking products that minimize ecological impact, such as biodegradable waste bags, recyclable packaging, and sustainably sourced food ingredients. A significant majority of consumers prefer brands that demonstrate commitment to sustainability, influencing their purchasing decisions in the pet care sector. Companies can capitalize on this trend by developing plant-based protein alternatives and upcycled ingredients that reduce carbon footprints and resource consumption. Eco-friendly grooming products using natural and non-toxic formulations appeal to health-conscious owners, who prioritize safety for their pets and the environment. The use of renewable materials in toy beds and accessories further enhances brand appeal and differentiation. Certification programs and transparent labeling help build trust and credibility with environmentally aware customers. Partnerships with conservation organizations and initiatives to support animal welfare resonate strongly with this demographic, fostering brand loyalty. The shift toward circular economy principles, such as take-back programs for used products, creates additional value propositions.

MARKET CHALLENGES

Regulatory Compliance and Safety Standards

The regulatory compliance and safety standards, imposed by imposing stringent requirements on product formulation, labeling, and manufacturing processes, are one of the major challenges for the growth of the United States pet care market. Agencies, such as the Food and Drug Administration and the Association of American Feed Control Officials, that enforce rigorous guidelines to ensure the safety and efficacy of pet foods and treats. The misleading claims or inadequate labeling can result in severe penalties,s recalls, and reputational damage for manufacturers. The complexity of navigating federal, state, and local regulations increases operational costs and requires dedicated legal and quality assurance resources. Recent incidents of contamination and adulteration in pet food have heightened scrutiny, leading to more frequent inspections and testing protocols. Compliance with evolving standards for novel ingredients and supplements adds further complexity,y requiring extensive research and validation. The global nature of supply chains necessitates adherence to international regulations, which may differ significantly from domestic requirements. Failure to meet these standards can disrupt production and distribution, causing financial losses and consumer distrust. Additionally, the rapid pace of innovation in pet health products often outpaces the regulatory framework,s creating uncertainty for developers. Balancing innovation with compliance requires careful planning and investment in robust quality control systems.

Fragmentation of the Market and Private Label Competition

The intense competition from private label brands by compressing margins and diluting brand loyalty is acting as a major barrier for the growth of the United States pet care market. The low barriers to entry for certain product categories have led to a proliferation of niche brands and store-owned labels that offer comparable quality at lower prices. The private label pet food and supply sales have grown significantly, capturing market share from established national brands. Retailers leverage their distribution networks and customer data to promote exclusive products, often undercutting branded competitors on price. This competitive pressure forces mainstream brands to increase marketing spend and offer discounts, eroding profitability. The abundance of choices can overwhelm consumers,s making it difficult for new or smaller brands to gain visibility and traction. Differentiation becomes challenging as many products claim similar benefits, such as natural ingredients or health improvements. Consolidation among large retailers further strengthens their bargaining power by allowing them to dictate terms to suppliers. The need to continuously innovate and maintain distinct brand identities requires substantial investment in research and development.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Pet Type, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Mars, Incorporated, Nestlé Purina PetCare Company, Hill’s Pet Nutrition, Inc., The J.M. Smucker Company, Blue Buffalo Co., Ltd. (General Mills, Inc.), Colgate-Palmolive Company, Spectrum Brands Holdings, Inc., Central Garden & Pet Company, Freshpet, Inc., Chewy, Inc., Petco Health and Wellness Company, Inc., PetSmart LLC |

SEGMENTAL ANALYSIS

By Product Insights

The pet food products segment accounted in holding 45.3% of the United States pet care market share in 2025, with the fundamental and recurring necessity of nutrition for companion animals. Unlike discretionary services or accessories,s food represents a non-negotiable daily expense that ensures consistent revenue generation for manufacturers and retailers. The increasing premiumization of diets, where owners see high-quality, natural, and specialized formulations to support pet health and longevity, is also propelling the growth of the segment. Consumers are willing to pay higher prices for grain-free organic and raw options that align with human dietary trends. The sheer volume of consumption,n given the large population of dogs and cats in the United States, creates a massive baseline demand. Additionally, the emotional bond between owners and pets leads to careful selection of brands that promise superior ingredients and transparency. The stability of this segment is further reinforced by subscription models and auto-replenishment services that ensure continuous purchase cycles. Innovation in functional foods that address specific health issues, such as weight management or joint health,h also drives growth within this category.

The veterinary care segment is likely to witness the fastest CAGR of 9.3% during the forecast period, with the rising emphasis on preventive health and advanced medical treatments. Pet owners are increasingly investing in regular checkups, vaccinations,s and diagnostic services to ensure early detection of diseases and overall well-being. The veterinary service costs have risen significantly, reflecting the adoption of sophisticated medical technologies and specialized care similar to human healthcare. The aging pet population contributes to this growth as older animals require more frequent medical attention and chronic disease management. Advances in veterinary medicine,e including oncology,gy cardiology, and orthopedic surgery,y have expanded the range of available treatments, ts encouraging owners to pursue life-extending interventions. The expansion of pet insurance coverage further facilitates access to these expensive services by reducing out-of-pocket expenses for consumers. Additionally, the shortage of veterinary professionals has led to higher service fees but also increased investment in clinic infrastructure and technology. The shift toward holistic and integrative medicine, including acupuncture and physical therapy, adds new revenue streams.

By Pet Type Insights

The dog segment accounted in holding 34.8% of the United States pet care market share in 2025, with the high population of canine companions and the extensive range of products and services tailored to their needs. Dogs typically require more frequent grooming, training, and outdoor activities, which translates into higher spending on accessories, supplies, es and professional services. The social nature of dogs encourages owners to invest in interactive toys, boarding facilities,s and daycare services to manage their energy and socialization needs. Furthermore, the diversity of dog breeds results in varied requirements for food, grooming, and healthcare, driving a broad spectrum of product innovations. Large breed dogs often need specialized joint support supplements and larger quantities of food, while small breeds may require dental care and specific kibble sizes. The strong emotional connection owners feel with dogs often leads to indulgence in premium products and experiences. Marketing efforts frequently target dog owners through community events and social media, fostering brand loyalty. The prevalence of dog-friendly policies in public spaces and workplaces also supports the integration of dogs into daily life, increasing visibility and spending.

The cat segment is projected to witness the fastest CAGR of 7.3% from 2026 to 2034, with the changing lifestyle preferences and urbanization trends. Cats are increasingly preferred by younger demographics and urban dwellers, who value their independence and lower maintenance requirements compared to dogs. The ownership of cats has risen steadily among millennials and Gen Z consumers, who often live in apartments with limited space. The perception of cats as low-maintenance companions appeals to busy professionals who seek affection without the time commitment required for dog walking and training. Additionally, the rise of indoor-only cats has increased spending on environmental enrichment products to ensure mental and physical stimulation. Premium cat food formulations focusing on urinary health, hairball control,l and weight management are gaining popularity as owners become more aware ofeline-specific health issues. Social media platforms have also played a role in popularizing cat content, influencing purchasing decisions and brand engagement.

By Distribution Channel Insights

The offline distribution channel segment held a significant share of the United States pet care market in 2025, with the immediate availability of products and the trust associated with physical retail interactions. Brick and mortar stores,s including specialty pet shops, supermarkets, etc., and veterinary clinics allow consumers to inspect products personally and receive immediate expert advice. Despite the rise of e-commerce, a significant majority of pet supply purchases still occur in physical stores,tores particularly for bulk items like litter and large bags of food. The tactile experience of evaluating product quality, texture, and packaging influences buying decisions, especially for new or hesitant customers. Specialty stores offer curated selections and personalized service that build strong community connections and customer loyalty. The ability to take products home immediately satisfies urgent needs such as running out of food or requiring emergency supplies. Additionally, many consumers prefer the convenience of combining pet shopping with other household errands at supermarkets and big box retailers. Promotional displays and in-store demonstrations effectively capture impulse buys and introduce new products.

The online distribution channel is growing at a rate of 9.1% from 2026 to 2034 with the convenience, variety,y and competitive pricing. E-commerce platforms enable consumers to browse extensive product catalogs, gs compare prices, and read reviews from the comfort of their homes. The online pet supply sales have surged, as consumers embrace subscription services for automatic delivery of recurring items like food and litter. The ability to access niche and specialized products that may not be available locally expands consumer choice and drives adoption of online shopping. Mobile applications and user-friendly websites enhance the shopping experience with features such as personalized recommendations and easy reordering. The integration of telehealth services with online pharmacies allows for seamless procurement of prescription medications following virtual consultations. Competitive pricing and frequent discounts on digital platforms attract budget-conscious shoppers seeking value. The logistics infrastructure has improved significantly, ensuring fast and reliable delivery even for heavy or bulky items. Social media marketing and influencer partnerships drive traffic to online stores,s creating a seamless path from discovery to purchase. The shift toward digital-first strategies by major retailers further accelerates this growth.

COMPETITIVE LANDSCAPE

The competition in the United States pet care market is intense and characterized by a mix of global conglomerates, specialized niche brands,s and private label retailers vying for consumer attention and spending. Major players leverage their extensive distribution networks and brand recognition to dominate shelf space in both physical and online stores. Differentiation is achieved through product innovation in sugrain-free formulas, functional treats, and sustainable packaging that appeal to health-conscious and environmentally aware pet owners. Price competition is significant in the mass market segment, while premium brands compete on quality and specialized benefits. Veterinary channels remain critical for prescription diets and professional recommendations,s creating a barrier to entry for on-endorsed products. Consolidation through mergers and acquisitions is common as companies seek to expand their portfolios and achieve economies of scale. Customer loyalty is driven by trust in brand safety and efficacy, making reputation management crucial.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. pet care market include

- Mars, Incorporated

- Nestlé Purina PetCare Company

- Hill’s Pet Nutrition, Inc.

- The J.M. Smucker Company

- Blue Buffalo Co., Ltd. (General Mills, Inc.)

- Colgate-Palmolive Company

- Spectrum Brands Holdings, Inc.

- Central Garden & Pet Company

- Freshpet, Inc.

- Chewy, Inc.

- Petco Health and Wellness Company, Inc.

- PetSmart LLC

TOP LEADING PLAYERS IN THE MARKET

- Mars Incorporated is a dominant force in the United States pet care market through its extensive portfolio of premium and mass market brands, including Royal Canin, Pedigree, ee, and Banfield Pet Hospital. The company leverages its vertical integration to control quality from ingredient sourcing to retail distribution, ensuring consistent product availability. Recent actions include significant investments in veterinary services and digital health platforms to create a holistic ecosystem for pet owners. Mars has expanded its specialized nutrition lines, focusing on breed-specific and health condition-based diets to meet evolving consumer demands. The acquisition of independent veterinary practices strengthens its service network and enhances customer loyalty. These strategic initiatives reinforce its position as a leader in both product innovation and comprehensive pet healthcare services across the nation.

- Nestle SA contributes significantly to the United States pet care market through its Purina division, which offers a wide range of trusted brands such as Pro Plan, Fancy Feast, and Tidy Cats. The company focuses on scientific research and development to create nutritionally balanced products that address the specific health needs of pets. Recent actions include the expansion of its fresh food offerings and sustainable packaging initiatives to align with environmental consciousness among consumers. Nestle has invested heavily in digital marketing and e-commerce partnerships to enhance direct-to-consumer engagement and accessibility. The launch of personalized nutrition plans using artificial intelligence helps owners tailor diets to their pets' unique requirements.

- Central Garden and Pet Company plays a pivotal role in the United States pet care market by distributing a diverse array of products through its owned brands and third-party partnerships. The company operates major retail chains and supplies independent pet specialty stores, ensuring a broad market reach. Recent actions include strategic acquisitions of niche brands in the natural and organic segments to cater to growing demand for premium options. Central Garden and Pet has enhanced its supply chain efficiency to improve product availability and reduce costs. The company focuses on expanding its private label offerings, which provide higher margins and exclusivity for retailers. Investments in employee training and customer service excellence strengthen relationships with retail partners and end consumers.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States pet care market primarily focus on product premiumization by introducing natural, organic, ic, and specialized formulations to meet rising consumer demand for high-quality nutrition. Companies are increasingly investing in veterinary services and digital health platforms to create integrated care ecosystems that enhance customer loyalty. Strategic acquisitions of niche brands allow firms to expand their portfolios and enter emerging segments such as raw food and eco-friendly supplies. Expansion of e-commerce capabilities and direct-to-consumer channels improves accessibility and convenience for pet owners. Sustainability initiatives, including recyclable packaging and ethical sourcing, are prioritized to align with environmental values. Personalization through data analytics enables tailored recommendations for diet and care, improving pet health outcomes. Partnerships with influencers and veterinarians build trust and brand credibility. These strategies collectively drive growth and competitiveness in the dynamic pet care landscape by addressing evolving consumer preferences and technological advancements.

MARKET SEGMENTATION

This research report on the U.S. pet care market is segmented and sub-segmented into the following categories.

By Product

- Pet Food Products

- Veterinary Care

- Pet Grooming

- Pet Accessories

- Pet Insurance

- Others

By Pet Type

- Dogs

- Cats

- Birds

- Fish

- Others

By Distribution Channel

- Offline

- Online

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com