- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

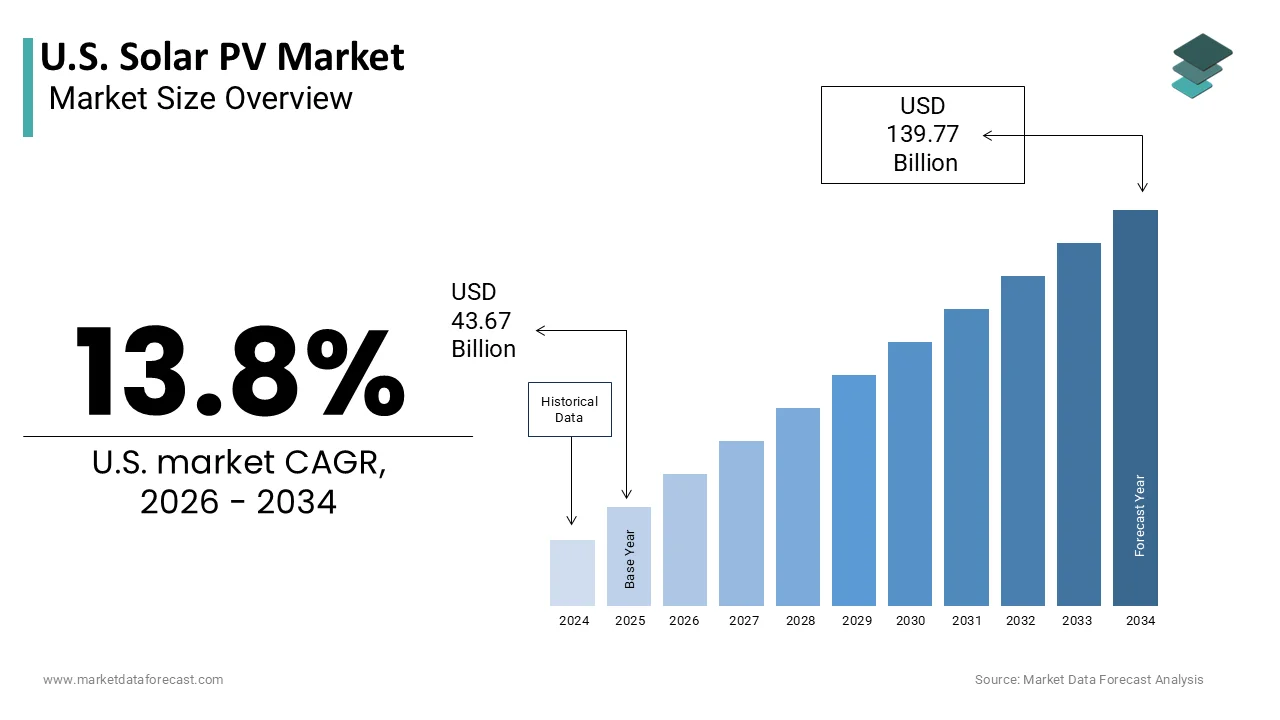

Market Size, 2025

$43.67 BnMarket Estimate, 2026

$49.69 BnMarket Forecast, 2034

$139.77 BnCAGR, 2026–2034

13.8%U.S. Solar PV Market Size

The U.S. Solar PV Market was valued at USD 43.67 billion in 2025, is estimated to reach USD 49.69 billion in 2026, and is projected to reach USD 139.77 billion by 2034, growing at a CAGR of 13.8% from 2026 to 2034.

Solar PV (photovoltaics) is a technology that converts sunlight directly into electricity using semiconductor materials, typically silicon, within solar panels. It acts as a clean, renewable energy source, harnessing light, not heat, to produce direct current (DC) electricity, which is then converted into alternating current (AC) for household or commercial use. This market includes residential rooftop installations, commercial and utility-scale systems, and utility-scale solar farms that feed power into the national grid. The market is characterized by rapid technological policy-driven significant policy driven growth aimed at decarbonizing the electricity sector. According to the US Energy Information Administration, solar photovoltaic capacity has grown exponentially, with solar accounting for a substantial portion of new electric generating capacity added in recent years. As per the Solar Energy Industries Association, the cumulative installed solar capacity in the United States has reached 279.2 gigawatts as of year-end 2025, demonstrating the technology's maturity and scalability. The industry operates within a complex regulatory framework involving state-level incentives, state-level renewable portfolio standards, and local interconnection rules. Consumer adoption is increasingly driven by economic factors such as falling equipment costs and rising electricity rates from traditional utilities. The integration of energy storage systems with solar installations is becoming standard practice to enhance reliability and grid stability. Supply chain dynamics for critical components like polysilicon and inverters remain central to market performance. The shift toward domestic manufacturing under federal legislation aims to reduce reliance on imports and strengthen energy security. This evolving landscape requires stakeholders to navigate technical, financial, and regulatory complexities while meeting growing demand for clean energy solutions.

MARKET DRIVERS

Federal Policy Incentives and Tax Credits

Federal policy incentives and tax credits serve as primary drivers for the United States solar photovoltaic market by significantly improving project economics and reducing payback periods for investors and consumers. The Inflation Reduction Act extended and expanded the Investment Tax Credit, allowing residential and commercial entities to claim a tax credit equal to 30 percent of the cost of installing qualified solar energy systems against their federal tax liability, provided labor requirements are met for larger commercial projects. According to the US Department of the Treasury, this long-term policy certainty has unlocked billions of dollars in private sector investment for solar projects across the country. As per the Solar Energy Industries Association, the clarity provided by federal legislation has accelerated project pipelines and encouraged manufacturers to establish domestic state-level facilities. State-level policies such as Renewable Portfolio Standards mandate that utilities source a specific percentage of their electricity from renewable sources, creating guaranteed demand for solar power. Net metering regulations in many states allow system owners to receive credit for excess electricity generated, further enhancing the financial return on investment. These legislative measures create a favorable environment that lowers barriers to entry and stimulates market growth. The combination of federal tax benefits and state mandates ensures that solar energy remains a competitive and attractive option for diverse consumer segments. This robust policy support underpins the sustained expansion of the solar photovoltaic market despite broader economic fluctuations.

Declining Levelized Cost of Energy

The declining levelized cost of energy for solar photovoltaic systems significantly drives the United States market by making solar power increasingly competitive with conventional fossil fuel sources. Technological advancements in panel efficiency, manufacturing scale, and installation processes have reduced the overall cost of solar energy generation over the past decade. According to the National Renewable Energy Laboratory, the levelized cost of energy for utility-scale solar has decreased by more than 70 percent since 2010, reaching parity or below with coal and natural gas in many regions. As per Lazard’s Levelized Cost of Energy Analysis, unsubsidized utility-scale solar is now one of the cheapest sources of new electricity generation in the United States. This cost competitiveness attracts corporate buyers seeking to lower operational expenses and meet sustainability goals through power purchase agreements. Residential consumers benefit from lower equipment prices and improved financing options, accelerating adoption in the housing sector. The economic advantage of solar is further enhanced by the volatility of fossil fuel prices, which makes renewable energy a stable and predictable alternative. Utilities are increasingly choosing solar for new capacity additions due to its favorable economics and minimal fuel costs. This financial viability ensures that photovoltaic systems are not only an environmental choice but also a sound economic investment, driving widespread market penetration.

MARKET RESTRAINTS

Interconnection Queue Delays and Grid Constraints

Interconnection queue delays and grid infrastructure constraints act as major restraints on the United States solar photovoltaic market by slowing the deployment of new projects and increasing development costs. The rapid increase in solar capacity additions has overwhelmed the existing transmission network and interconnection processes managed by regional transmission organizations. According to the Lawrence Berkeley National Laboratory, the average wait time for interconnection approval has increased substantially, with some projects facing delays of several years before achieving commercial operation. As per the Federal Energy Regulatory Commission, outdated interconnection procedures and insufficient transmission capacity create bottlenecks that prevent the timely commissioning of solar farms. Utility companies often require extensive studies and upgrades to handle the variable nature of solar power, adding costs and time to project development. The lack of coordinated planning for transmission expansion exacerbates congestion issues, particularly in high-potential solar regions. These administrative and physical barriers discourage investment and lead to the cancellation of viable projects. Developers must navigate complex regulatory requirements and negotiate with multiple stakeholders, increasing project risk. The inability to connect generated power to the grid efficiently limits the scalability of the photovoltaic sector. Addressing these infrastructure gaps requires significant capital investment and regulatory reform. Systemic issues must be resolved. Until then, they will continue to constrain market expansion and hinder the realization of renewable energy goals.

Supply Chain Vulnerabilities and Trade Policies

Supply chain vulnerabilities and trade policies present significant restraints on the United States solar photovoltaic market by causing material shortages and price volatility. The US solar industry relies heavily on imports for key components such as polysilicon, wafers, cells, and modules, primarily from Asian markets. According to the Solar Energy Industries Association (SEIA), investigations by the US Department of Commerce into trade practices and the imposition of tariffs on solar imports have created uncertainty and fluctuating prices for developers. As per the Solar Energy Industries Association, supply chain bottlenecks have led to significant project delays and increased balance of system costs, affecting overall profitability. Geopolitical tensions and trade restrictions further complicate the procurement process, forcing companies to seek alternative suppliers or hold larger inventories. The concentration of manufacturing capacity in specific regions creates vulnerabilities to logistical disruptions such as port congestion and shipping shortages. Domestic manufacturing capabilities are still scaling up and cannot yet meet the full demand for high-volume projects. These supply-side constraints limit the speed at which new capacity can be deployed, slowing market growth. Developers face challenges in securing reliable contracts for modules and inverters, leading to risk aversion in planning. Until domestic supply chains are fully established and diversified, the market will remain exposed to external shocks. This instability hinders the ability to meet aggressive installation targets and maintain consistent pricing.

MARKET OPPORTUNITIES

Integration of Energy Storage Systems

The integration of energy storage systems with solar photovoltaic installations presents a significant opportunity for the United States market by enhancing grid stability and energy reliability. Combining solar panels with battery storage allows for the capture of excess energy during peak production times for use during periods of low sunlight or high demand. According to the US Energy Information Administration, the pairing of solar and storage is becoming increasingly common, with hybrid projects accounting for a growing share of new capacity additions. As per research, the co-location of batteries reduces interconnection and balance-of-system costs by sharing infrastructure, but primarily improves economic value by enabling energy time-shifting and ITC qualification, while often constraining participation in ancillary service markets compared to standalone storage. Residential customers benefit from greater energy independence and backup power during outages, driving demand for home solar-plus-storage solutions. Commercial and industrial users leverage storage to manage peak demand charges and optimize energy usage. Policy incentives such as the standalone investment tax credit for storage further encourage adoption. The ability to provide dispatchable renewable energy addresses concerns regarding intermittency, making solar more attractive to utilities and grid operators. Advances in battery technology and declining costs enhance the feasibility of these integrated systems. This synergy between solar and storage opens new revenue streams and applications, expanding the market potential beyond traditional generation.

Expansion of Community Solar Programs

The expansion of community solar programs offers a lucrative opportunity for the United States solar photovoltaic market by increasing access to solar energy for renters and low-income households. Community solar allows multiple subscribers to share the benefits of a single off-site solar array, eliminating the need for individual rooftop installations. According to the National Renewable Energy Laboratory, community solar projects can reduce energy bills for participants by 10 to 15 percent, providing immediate financial relief. As per the Solar Energy Industries Association's Solar Market Insight Report, while some states have existing programs, recent legislative efforts have faced setbacks, with no new community solar markets emerging to replace saturated ones, creating a challenging rather than favorable regulatory environment marked by interconnection delays and policy hurdles. This model democratizes access to clean energy, allowing individuals who lack suitable roofs or capital to participate in the solar economy. Utilities and third-party developers collaborate to build and manage these projects, sharing revenues and risks. Corporate subscriptions to community solar help businesses meet sustainability goals without on-site infrastructure. The scalability of community solar enables rapid deployment in urban and suburban areas with high-density housing. Marketing efforts focused on inclusivity and affordability resonate with diverse consumer segments. By broadening the customer base, community solar expands the total addressable market for photovoltaic technology. This inclusive approach fosters social equity and accelerates the transition to renewable energy.

MARKET CHALLENGES

Workforce Shortages and Labor Constraints

Workforce shortages and labor constraints pose a major challenge to the United States solar photovoltaic market by limiting installation capacity and increasing operational costs. The rapid growth of the solar industry has outpaced the availability of skilled technicians, engineers, and construction workers needed to deploy projects. According to the Interstate Renewable Energy Council, the solar workforce needs to expand significantly to meet future installation targets, but recruitment and training pipelines remain insufficient. Data from the Bureau of Labor Statistics confirms that high demand for skilled labor is driving up wages, while the Associated General Contractors of America reports that these shortages are delaying project completion times. The lack of standardized training programs and certification requirements creates inconsistencies in workforce quality and safety practices. High turnover rates in the industry further exacerbate staffing challenges, requiring continuous investment in recruitment and retention. Small and medium-sized installers struggle to compete with larger firms for talent, limiting their growth potential. The shortage of qualified personnel delays permitting inspections and commissioning, affecting overall project efficiency. Addressing this gap requires collaboration between industry associations, educational institutions, and government agencies to develop comprehensive training initiatives. Without a robust and skilled workforce, the industry risks losing demand and maintaining quality standards. This human capital constraint remains a critical bottleneck for sustainable market expansion.

Regulatory Uncertainty and Net Metering Changes

Regulatory uncertainty and changes to net metering policies present a significant challenge to the United States solar photovoltaic market by impacting the financial viability of residential and commercial systems. Net metering allows solar owners to receive credit for excess electricity exported to the grid, but several states are revising these policies to reduce compensation rates. According to the Vote Solar organization, recent regulatory decisions in key markets such as California have significantly lowered the value of exported solar energy, affecting payback periods for customers. As per the Solar Energy Industries Association, inconsistent and unpredictable policy changes create hesitation among consumers and investors, slowing adoption rates. Utilities argue that net metering shifts costs to non-solar customers, leading to political and legal battles over rate design. The transition to time-of-use rates and fixed charges adds complexity to financial modeling for solar projects. Developers face difficulties in forecasting long-term revenues, increasing the perceived risk of investments. The lack of uniform national standards results in a fragmented market where rules vary by jurisdiction. This regulatory volatility undermines consumer confidence and disrupts market stability. Establishing clear and fair compensation mechanisms is essential to sustain growth. The market will face headwinds in customer acquisition and project development. This will continue until policy frameworks stabilize.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Mounting Structure, Connectivity, End Use, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | First Solar Inc., SunPower Corporation, Sunrun Inc., Tesla Inc., Suniva Inc., Auxin Solar Inc., Canadian Solar Inc., Sharp Corporation, Trinity Solar Inc., Momentum Solar, Sunlux Energy, Titan Solar Power |

SEGMENTAL ANALYSIS

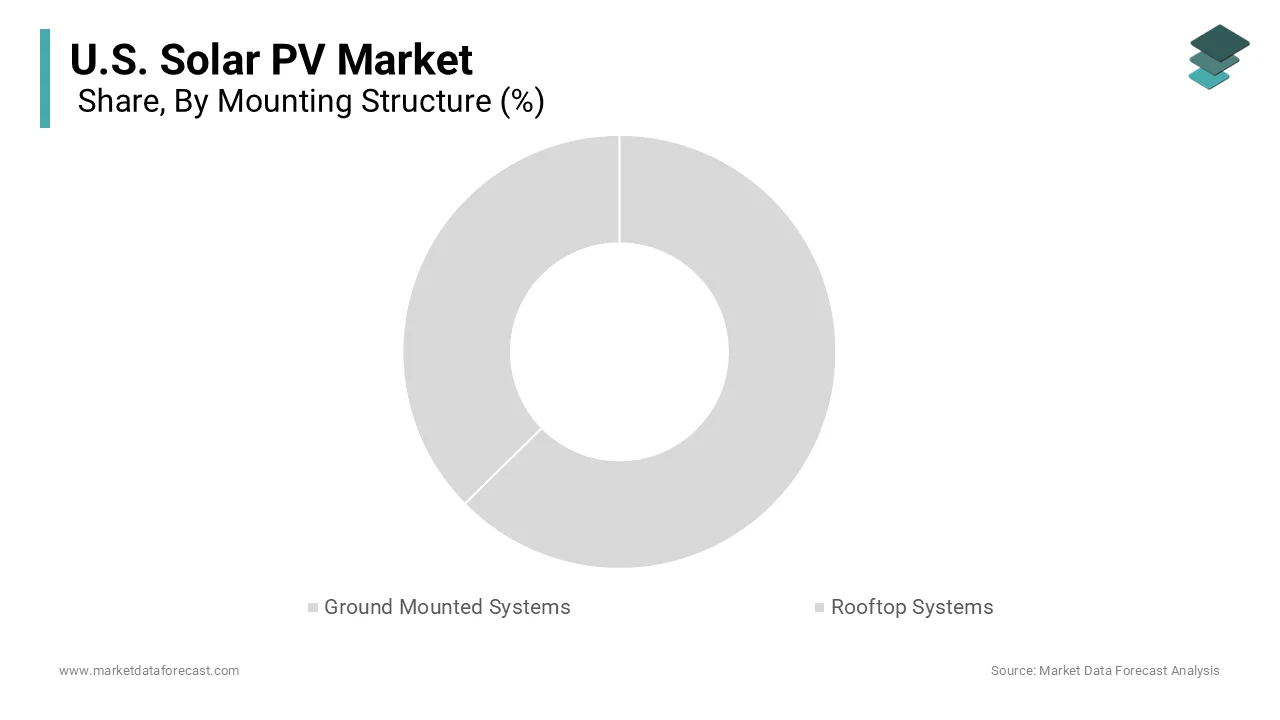

By Mounting Structure Insights

The ground-mounted systems segment was the largest segment in the United States solar PV market and occupied a 61.2% share in 2025. This prominence of the segment is supported by its extensive deployment in utility-scale projects, which account for the largest share of installed capacity. These installations are typically located on large tracts of land and are designed to feed electricity directly into the transmission grid, serving thousands of households and businesses. According to the US Energy Information Administration, utility-scale solar facilities represent the majority of new solar capacity additions annually, driven by the economies of scale that lower the levelized cost of energy. As per the Solar Energy Ground-Mounted Association, single-axis systems,ngle axis single-axisems which follow the sun’s path to maximize energy production by up to 25 percent compared to fixed tilt systems. This technological advantage makes ground-mount the preferred choice for independent power producers and utilities seeking to meet renewable portfolio standards efficiently. The ability to install massive arrays in optimal geographic locations with high solar irradiance further enhances their performance and financial viability. Land availability in states such as Texas, California, and Florida supports the continued expansion of these large-scale projects. The standardized engineering and procurement processes for ground-mounted systems reduce construction timelines and costs, reinforcing their market leadership. Long-term agreements that provide revenue stability, attracting significant institutional investment. The sheer volume of megawatts deployed in this category ensures that ground-mounted systems remain the dominant mounting structure in the national market. The cost efficiency and operational scalability of ground-mounted systems significantly contribute to their market domination by enabling the rapid deployment of large capacity assets. Ground-mounted installations benefit from streamlined logistics and easier access for maintenance crews compared to rooftop systems, which often require specialized equipment and safety protocols. According to the National Renewable Energy Laboratory, the balance of system costs for utility-scale ground-mounted installations are substantially lower per watt than distributed rooftop installations due to bulk purchasing and standardized components. As per Wood Mackenzie, the modular nature of ground-mounted arrays allows developers to phase construction and expand capacity incrementally, reducing initial capital outlay and financial risk. The use of automated cleaning and monitoring technologies is more feasible in open field environments, ensuring consistent performance and reduced operational expenditures. Land lease agreements with agricultural or private landowners provide a steady income stream for rural communities, fostering local support for solar development. The scalability of ground-mounted systems enables them to respond quickly to grid demand spikes, providing essential reliability services. Regulatory frameworks in many states prioritize large-scale renewable projects for interconnection queues, further accelerating their adoption. This combination of economic efficiency and operationalground-moundground-mountednsures that ground mounground-mountedintain their leading position in the solar photovoltaic market.

The rooftop systems segment is likely to experience the fastest CAGR of 6.5% from 2026 to 2034, owing to the rise of distributed energy resources and the increasing number of prosumers who generate their own electricity. Homeowners and businesses are installing solar panels on rooftops to reduce utility bills and gain energy independence, particularly in regions with high electricity rates. According to the Solar Energy Industries Association, residential solar installations declined by 2% in 2025 following a major 32% drop in 2024, with growth suppressed by high interest rates and shifts in state-level net metering. The integration of smart inverters and home energy management systems allows rooftop owners to optimize their energy usage and participate in virtual power plants. Urban densification and limited land availability for ground-mounted projects further drive the adoption of rooftop solutions in metropolitan areas. Corporate sustainability initiatives also encourage commercial buildings to utilize unused roof space for solar generation, enhancing brand image and reducing operational costs. The psychological appeal of owning a personal energy asset resonates with environmentally conscious consumers. This shift toward decentralized generation empowers individuals and reduces strain on the central grid. The continuous improvement in aesthetic designs and building-integrated photovoltaics further boosts consumer acceptance. These factors collectively ensure that the rooftop segment experiences the highest growth rate in the market. Technological advancements in installation methods and innovative financing models accelerate the growth of the rooftop solar segment. Streamlined installation techniques, pre-assembled systems, and pre assembled pre-assembledve reduced labor time and costs, making rooftop projects more profitable for installers. According to the Department of Energy, innovations in software tools for remote site assessment and design have shortened the sales cycle and improved accuracy in energy yield predictions. As per Sunrun and other major residential providers, the availability of solar leases and power purchase agreements allows customers to adopt solar with little to no upfront cost, removing financial barriers. Third-party ownership models transfer the maintenance and performance risk to the provider, increasing consumer confidence. The emergence of digital platforms that connect homeowners with certified installers enhances market transparency and competition. Insurance products tailored for rooftop solar systems mitigate risks associated with weather damage and liability. Local governments are simplifying permitting processes through online portals, reducing administrative delays. These improvements in technology and finance make rooftop solar a convenient and attractive option for a broad demographic. The ease of adoption and reduced friction in the customer journey ensure that the rooftop segment continues to expand rapidly.

By Connectivity Insights

The on-grid systems segment held the majority share of the US solar photovoltaic market in 2025. This supremacy of the segment is credited to its seamless integration with the existing electrical infrastructure and the financial benefits of net metering. Most residential, commercial, and utility-scale installations are connected to the public grid, allowing users to draw power when solar production is low and export excess energy when production is high. According to the Federal Energy Regulatory Commission, net metering policies in over 40 states enable system owners to receive credit for exported electricity, significantly improving the return on investment. As per the Solar Energy Industries Association, the vast majority of solar installations are grid-tied because they do not require expensive battery storage for basic operation, lowering initial costs. The reliability of the grid provides a backup power source, ensuring an uninterrupted electricity supply during periods of low sunlight or system maintenance. Utilities benefit from the additional capacity provided by distributed solar resources, which can help meet peak demand without building new power plants. Interconnection standards established by the Institute of Electrical and Electronics Engineers ensure safe and stable integration of solar inverters with the grid. The established regulatory framework on grid and non-grid systems, on grid system implementation complexity, and risk. This widespread compatibility and economic incentive structure solidifies on-grid systems as the dominant connectivity type in the market. Regulatory support and well-defined interconnection standards significantly drive the dominance of on-grid systems by providing a clear pathway for project approval and operation. State public utility commissions have developed streamlined procedures for connecting solar systems to the distribution network, reducing administrative burdens for developers and homeowners. According to the National Conference of State Legislatures, many states have adopted standardized interconnection agreements that clarify technical requirements and timelines for utility review. As per the North American Electric Reliability Corporation, grid operators have implemented guidelines to manage the variability of solar power, ensuring system stability and reliability. The existence of these frameworks encourages investment by reducing uncertainty regarding grid access and compensation mechanisms. Utilities are increasingly required to accommodate distributed generation through state mandates, fostering a cooperative environment for on-grid solar expansion. The ability to participate in community solar programs also relies on grid connectivity, expanding access to renters and those with unsuitable roofs. The maturity of grid integration technology, including advanced inverters with grid support functions, enhances the value proposition of on-grid robust regulatory and technical foundation ensures that on-grid connectivity remains the standard for solar deployment in the country.

The off-grid and hybrid systems segment is on the rise, fast-growing to be the fastest market by witnessing. 1% over the forecast period due to increasing demand for energy independence and resilience against grid outages. Extreme weather events and aging infrastructure have highlighted the vulnerabilities of the central grid, prompting consumers to seek self-sufficient power solutions. Rural properties without access to reliable grid service also contribute to the growth ofoff-gridd soof off-gridtiolithium-ionlining cost of lithium ion balithium-iones hybrid systems more economically viable, allowing users to store excess solar energy for nighttime use. Government incentives for standalone storage further encourage the adoption of hybrid configurations. The desire for energy security among critical facilities such as hospitals and data centers drives commercial interest in off-grid systems. This trend toward decentralization and off-grid systemsoff grid and hybrid systems is experiencing rapid growth. The ability to maintain power continuity during emergencies provides a compelling value proposition that transcends economic considerations. Technological advancements in energy storage and smart management systems drive off-grid and hybrid segments. Innovations in battery chemistry, such as lithium iron phosphate, offer higher safety, longer lifespan, and greater energy density, making them ideal for solar storage applications. These systems can automatically disconnect from the grid during outages and reconnect when stability is restensuring aing an power supply. The integration of artificial intelligence allows for predictive maintenance and load forecasting, enhancing system reliability. Modular battery designs enable users to scale storage capacity according to their needs, providing flexibility for future expansion. The interoperability of different components from various manufacturers is improving through standardization efforts, reducing installation complexity. These techno-off-grid enhancements and hybrid user-friendly, reliable, and attractive, attracting a broader customer base. The continuous innovation in storage and control technologies ensures that this segment remains at the forefront of market growth.

By End Use Insights

The residential segment led the United States solar PV market and captured a significant share in 2025. This leading position of the segment is attributed to high consumer adoption rates driven by substantial financial incentives and rising electricity costs. Homeowners are increasingly installing solar panels to reduce monthly utility bills and take advantage of the federal Investment Tax Credit. State-level rebates and property tax exemptions further enhance the affordability of residential systems, making them accessible to a broader demographic. Theof zero down financing options and solar leases allows households to install solar without significant upfront capital, lowering the barrier to entry. Community awareness and neighborhood effects, where seeing neighbors install solar influences others to follow suit, drive organic growth. The desire for energy independence and environmental stewardship motivates many homeowners to invest in clean energy. Retailers and installers have streamlined the sales and installation process, making it easier for consumers to switch to solar. This combination of economic benefits and social influence ensures that the residential seend-usemainsend-use remainsnd use segmeend-usehe distributed solar market. Technological accessibility and improvements in system aesthetics significantly contribute to the dominance of the residential solar sector. Modern solar panels are more efficient, durable, and visually appealing, addressing previous concerns about roof damage and appearance. The development of lightweight mounting systems reduces structural load concerns, making solar viable for older homes. Smart home integration allows residents to monitor and control their energy usage via mobile apps, providing real-time insights and convenience. The compatibility of solar systems with electric vehicle chargers and smart appliances creates a holistic home energy tech-savvy that appeals to tech savvy contech-savvystallers offer customized designs that optimize energy production based on roof orientation and shading, ensuring maximum efficiency. These technological and aesthetic enhancements make solar an attractive home improvement investment. The ease of use and visual integration ensure that residential solar continues to lead the market in terms of customer adoption and satisfaction.

The commercial and industrial segment is expected to exhibit a noteworthy CAGR of 11.5% between 2026 and 2034. This rapid acceleration of the segment is fuelled by corporate sustainability goals and environmental, social, and governance commitments. Businesses are increasingly investing in on-site solar installations to reduce their carbon footprint and meet renewable energy targets set by shareholders and regulators. Power purchase agreements allow businesses to lock in long-term, protective utility rates and enhance financial stability. Tax incentives such as accelerated depreciation and investment tax credits improve the return on investment for commercial solar assets. The visibility of solar installations on corporate campuses and retail stores serves as a marketing tool, demonstrating a commitment to sustainability to customers and employees. Industry collaborations and green building certifications such as LEED further encourage the adoption of solar technology. This strategic alignment with corporate values ensures that the commercial and industrial sector experiences rapid growth. The scale of these installations contributes significantly to overall market capacity expansion. Furthermore, the need for operational cost reduction and energy security accelerates the growth of the commercial and industrial solar segment. Manufacturing facilities, warehouses, and retail chains have large roof spaces and high energy consumption, making them ideal candidates for solar installations. The ability to generate power during peak demand periods helps companies avoid high demand charges imposed by utilities. Advanced energy management systems allow businesses to optimize their energy usage and participate in demand response programs, generating additional revenue streams. The modularity of commercial solar systems allows for phased implementation, minimizing disruption to business operations. Government grants and loans for energy efficiency projects further support the adoption of solar technology in the industrial sector. The tangible financial benefits and enhanced energy resilience make solar an attractive investment for commercial entities. This focus on cost efficiency and reliability ensures that the commercial and industrial segment continues to expand at a rapid pace.

COUNTRY LEVEL ANALYSIS

United States

The United States outperformed other countries in the North American solar PV market and accounted for a 85% share in 2025. Furthermore, it served as a global leader in innovation and policy development. Its market status is characterized by robust growth driven by federal incentives, state-level, and strong private sector investment. According to the Solar Energy Industries Association (SEIA), the United States is the second-largest solar market globally, with a cumulative capacity of 279.2 gigawatts (GW) as of early 2025 (reaching 236 GW by year-end 2024). As per the US Energy Information Administration, solar power is the fastest-growing electricity generation in the country, reflecting its critical role in the energy transition. The implementation of the Inflation Reduction Act has stimulated unprecedented investment in domestic manufacturing and project development, enhancing energy security and economic competitiveness. The market benefits from a diverse mix of utility-scale and residential installations, supported by a mature financing and regulatory framework. Technological leadership in cell efficiency and energy storage integration further strengthens the US position. Challenges such as supply chain dependencies and interconnection delays are being addressed through policy reforms and infrastructure upgrades. The commitment to achieving net zero emissions by 2050 drives long term long-termd strategic planning. This combination of policy support, technological innovation, and market scale ensures that the United States remains the central pillar of the North American solar industry.

COMPETITIVE LANDSCAPE

The competition in the United States solar photovoltaic market is intense and characterized by a mix of established domestic manufacturers internationa, international giants, and emerging technology startups. Major players compete based on cost structure, re supply chain, reliability and technol, and technological innovation to secure contracts with utilities and distributors. The market sees significant investment in domestic production facilities as companies strive to qualify for federal tax credits and meet local content requirements. International manufacturers face trade barriers and tariffs, which create opportunities for domestic firms to capture market share. Technological differentiation through advanced cell architecture,s such as heterojunction and tandem cells, ls drives competitive advantage. Service quality and warranty terms are critical factors influencing customer decisions in the residential and commercial segments. The rise of community solar and energy storage integration adds complexity to competitive dynamics, requiring holistic solution offerings. Regulatory compliance and interconnection expertise also distinguish leading firms from smaller competitors. Consolidation through mergers and acquisitions is common as companies seek to scale operations and diversify portfolios. This dynamic landscape requires continuous innovation and strategic agility to navigate policy shifts and maintain market relevance effectively.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. solar market include

- First Solar Inc.

- SunPower Corporation

- Sunrun Inc.

- Tesla Inc.

- Suniva Inc.

- Auxin Solar Inc.

- Canadian Solar Inc.

- Sharp Corporation

- Trinity Solar Inc.

- Momentum Solar

- Sunlux Energy

- Titan Solar Power

TOP LEADING PLAYERS IN THE MARKET

- First Solar Inc is a leading American manufacturer of thin film thin-filmaic modules and a key provider of utility-scale plants. The company distinguishes itself through its proprietary cadmium telluride technology, which offers superior performance in high temperaturhigh-temperatureFirst Solar has significantly expanded its manufacturing footprint in the United States to capitalize on federal incentives provided by the Inflation Reduction Act. Recent actions include the announcement of new production facilities in Alabama and Louisiana to increase domestic supply capacity. The company focuses on sustainable manufacturing practices and comprehensive recycling programs to minimize environmental impact. These initiatives strengthen its market position by ensuring supply chain resilience and meeting the growing demand for locally sourced solar components. First Solar continues to invest in research and development to enhance module efficiency and reduce production costs. By maintaining a vertically integrated business model the comp, any controls quality and delivery timelines effectively. This strategic approach solidifies its role as a dominant player in the global utility scale.

- JinkoSolar Holding Co Co., Ltd., one of the largest and most innovative solar module manufacturers in the world, has a presence in the United States market. The company produces high-efficiency silicon modules and provides comprehensive solar solutions for residential, commercial, nd utility sectors. JinkoSolar has established a robust global distribution network and manufacturing base to serve diverse customer needs. Recent actions involve expanding its production capacity in the United States to meet local content requirements and qualify for federal tax credits. The company invests heavily in research and development to advance cell technologies such as TOPCon and heterojunction structures. These efforts strengthen its market position by offering competitive products with higher energy yields and reliability. JinkoSolar also emphasizes sustainability by implementing green manufacturing processes and reducing carbon emissions. JinkoSolar leverages its scale and technological expertise. This strategy maintains its strong competitive edge in the international solar industry.

- Enphase Energy Inc is a global energy technology company that delivers smart, easy-to-use solar generation, storage,e and energy management. company is renowned for its microinverter technology, which optim,izes energy production at the individual panel level. Enphase has expanded its product portfolio to include battery storage systems and an electric vehicle charging ecosystem. Recent actions involve scaling up manufacturing operations in the United States and India to diversify supply chains and reduce reliance on single regions. The company leverages advanced software platforms to provide real time monreal-timend control for consumers and installers. These efforts strengthen its market position by enhancing user experience and system reliability. Enphase actively partners with leading solar installers and distributors to broaden its reach in residential and commercial sectors. Enphase focuses on innovation and customer-centric design. This approach allows them to maintain a competitive edge in the rapidly evolving distributed energy resource market.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States solar photovoltaic market employ several major strategies to maintain competitiveness and drive growth. Vertical integration is central to these efforts, with companies securing control over supply chains from raw materials to final installation to ensure stability and cost efficiency. Strategic partnerships with local manufacturers and developers help firms navigate regulatory requirements and access federal incentives under the Inflation Reduction Act. Investment in research and development focuses on enhancing module efficiency and developing advanced storage solutions to address intermittency issues. Expansion of domestic manufacturing capabilities allows companies to qualify for tax credits and reduce dependence on imports. Digitalization of customer experiences through online platforms and smart monitoring tools improves engagement and service delivery. Diversification into adjacent markets such as electric vehicle charging and energy management systems creates new revenue streams. These combined strategies enable participants to adapt to policy changes and sustain long term prolong-termy in a dynamic environment.

MARKET SEGMENTATION

This research report on the U.S solar pv market is segmented and sub-segmented into the following categories

By Mounting Structure

- Ground Mounted Systems

- Rooftop Systems

By Connectivity

- On-Grid Systems

- Off-Grid and Hybrid Systems

By End Use

- Residential

- Commercial and Industrial

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States