U.S. Rainscreen Cladding Market Size, Share, Trends & Growth Forecast Report By Material, By End Use, and By Country (California, Texas, Florida, New York, Illinois & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

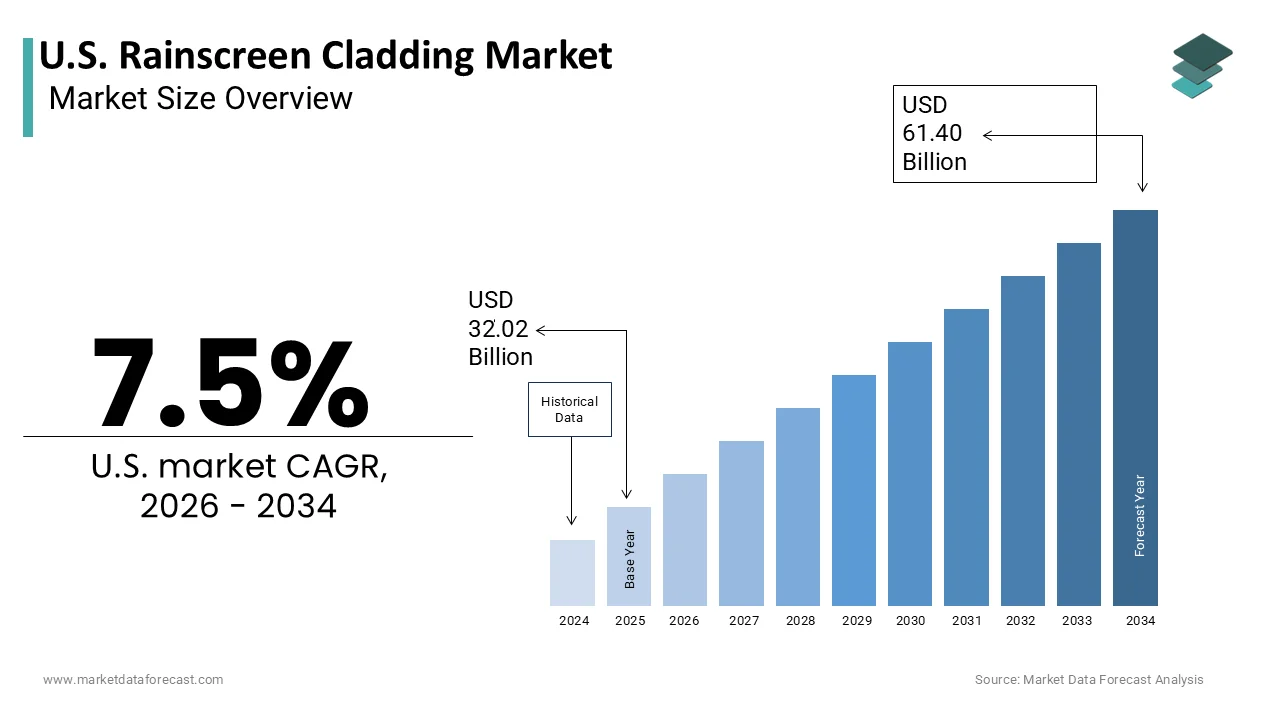

Market Size, 2025

$32.02 BnMarket Estimate, 2026

$34.43 BnMarket Forecast, 2034

$61.40 BnCAGR, 2026–2034

7.5%U.S. Rainscreen Cladding Market Size

The U.S. Rainscreen Cladding Market is projected to grow from USD 32.02 billion in 2025 to USD 34.43 billion in 2026 and reach USD 61.40 billion by 2034, registering a CAGR of 7.5% during the forecast period from 2026 to 2034.

The rainscreen cladding is an exterior building envelope system designed to manage moisture intrusion and enhance thermal performance through a ventilated cavity between the cladding and the structural wall. These systems function on the principle of pressure equalization and drainage, significantly reducing the risk of water damage, mold growth, and material degradation in building façades. As per the National Institute of Building Sciences, over 70% of building envelope failures in the United States are attributable to moisture-related issues, underscoring the functional necessity of rainscreen assemblies in modern construction. The adoption of such systems has been accelerated by evolving building science standards and climate resilience imperatives, particularly in regions prone to heavy precipitation or high humidity. While not yet universally mandated, rainscreen principles are increasingly embedded in state and municipal codes, especially in coastal and northern climates.

MARKET DRIVERS

Stringent Building Energy Codes and Moisture Management Mandates Drive Adoption

Regulatory frameworks that emphasize building envelope performance have become a primary catalyst for rainscreen cladding deployment, propelling growth in the United States rainscreen cladding market. The International Energy Conservation Code has been adopted in all fifty states, with many jurisdictions implementing stricter amendments that require continuous insulation and reduced thermal bridging, where conditions are effectively addressed by ventilated rainscreen systems. According to the US Department of Energy, buildings constructed to the 2021 IECC standard achieve up to 23% greater energy efficiency than those built to the 2015 version by incentivizing advanced façade solutions. Simultaneously, moisture control provisions in the International Building Code now explicitly reference drainage planes and air barriers for structures in Climate Zones 4 through 8, which encompass major metropolitan areas from Chicago to Seattle. The Federal Emergency Management Agency notes that water intrusion remains the leading cause of property insurance claims in commercial real estate, with annual losses exceeding 14 billion dollars as per the Insurance Institute for Business and Home Safety. In response, cities like Boston and Portland have updated façade inspection ordinances requiring moisture mitigation strategies for buildings over six stories. These overlapping regulatory and risk management pressures compel architects and developers to specify rainscreen cladding not as an aesthetic luxury but as a code-aligned necessity for long-term asset protection and operational efficiency.

Growing Emphasis on Climate Resilience and Extreme Weather Adaptation

The increasing frequency and intensity of extreme weather events have elevated rainscreen cladding from a performance enhancement to a resilience measure. The growing emphasis on climate resilience is another factor promoting the growth of the United States rainscreen cladding market. According to the National Oceanic and Atmospheric Administration, the continental United States experienced 28 weather and climate disaster events with losses exceeding one billion dollars each in 2023 alone, many involving wind-driven rain and prolonged humidity. Rainscreen systems mitigate these risks by decoupling the exterior finish from the structural wall, allowing trapped moisture to drain and evaporate rather than penetrate. Furthermore, the Biden Administration’s National Climate Resilience Framework directs federal infrastructure funding toward projects incorporating adaptive building technologies, indirectly promoting rainscreen adoption in publicly funded developments.

MARKET RESTRAINTS

High Initial Installation Costs and Skilled Labor Shortages Limit Widespread Use

The elevated upfront costs and a shortage of qualified installers are hampering the growth of the United States rainscreen cladding market. This cost premium is particularly prohibitive in cost-sensitive segments, such as multifamily housing and public schools, where budgets are tightly controlled. Improperly executed rainscreen assemblies can compromise performance by resulting in condensation buildup or air leakage that negates intended benefits. Moreover, the absence of standardized training programs for rainscreen installation means that even experienced contractors may lack familiarity with system-specific requirements.

Fragmented Building Codes and Lack of Uniform National Standards

The absence of a cohesive national regulatory framework creates uncertainty and inconsistency in its specification and approval, which is also impeding the growth of the United States rainscreen cladding market. While the International Building Code provides general guidance on drainage planes, it does not mandate specific rainscreen configurations, leaving interpretation to state and local authorities. Many states have modified the base code with varying requirements for air barrier, s drainage g,aps, and fire performance, complicating compliance for national developers and manufacturers. This regulatory patchwork increases design complexity and approval timelines for firms operating in multiple jurisdictions. Additionally, fire safety concerns following incidents like the Grenfell Tower tragedy have prompted ad hoc restrictions on combustible components in some cities, even though US rainscreen systems predominantly use non-combustible materials.

MARKET OPPORTUNITIES

Integration with Mass Timber and Sustainable Construction Trends

The convergence of rainscreen cladding with the rising use of mass timber in the construction sector is likely to amplify the growth of the United States rainscreen cladding market in the coming years. Mass timber structures, including cross-laminated timber and glued-laminated timber, are gaining traction due to their carbon sequestration benefits and prefabrication efficiency. However, these wood-based systems are highly sensitive to moisture exposure during and after construction. According to the Softwood Lumber Board, mass timber projects in the United States grew by 34% in 2023, with over 1200 buildings either completed or in design. Rainscreen cladding serves as a protective envelope that shields the structural timber from rain and humidity, while allowing vapor to escape, preserving material integrity and fire performance. The US Forest Service emphasizes that proper moisture management is essential to realizing the full lifecycle benefits of mass timber, including a 25 to 30% reduction in embodied carbon compared to steel or concrete. Developers of high-profile projects, such as the Ascent Tower in Milwaukee and the Carbon12 building in Portland, have paired mass timber frames with aluminum or terracotta rainscreens to meet both aesthetic and performance goals. As building codes increasingly recognize mass timber for mid-rise construction, the symbiotic relationship between timber structures and ventilated facades will drive co-adoption and open new avenues for integrated building system design.

Expansion into Retrofit and Façade Rehabilitation Projects

The growing stock of aging commercial and institutional buildings through retrofit applications is another factor to boost the growth of the United States rainscreen cladding market. The US Census Bureau estimates that nearly 40% of non-residential buildings were constructed before 1980, many featuring outdated cladding systems prone to moisture infiltration and poor insulation. Rainscreen retrofits provide a cost-effective solution to extend building life,e improve energy efficiency,y and enhance curb appeal without a full structural overhaul. The Department of Energy’s Better Buildings Initiative reports that façade upgrades incorporating ventilated cladding can reduce heating and cooling energy use by up to 18% in older structures. Cities like New York and Chicago have launched building performance mandates requiring energy benchmarking and envelope improvements, indirectly stimulating demand for rainscreen systems.

MARKET CHALLENGES

Supply Chain Volatility for Specialty Cladding Materials

The supply chain instability affecting key materials, such as aluminum composite panels, terracotta tiles, and high-pressure laminates, is inhibiting the growth of the United States rainscreen cladding market. Geopolitical disruptions and domestic manufacturing constraints have led to extended lead times and price fluctuations. These hurdles force project teams to substitute materials or delay construction, undermining design intent and budget predictability. The situation is exacerbated by just-in-time inventory practices common in the construction sector, which leave little buffer for supply shocks. While some firms are exploring localized sourcing or alternative composites, the lack of standardized performance equivalency complicates approval processes.

Complexity in Fire Safety Compliance for Composite Systems

The fire performance requirements for advanced systems that incorporate combustible components, particularly in mid and high-rise buildings, are also expected to decline the growth of the United States rainscreen cladding market. Although the United States does not use the same combustible cladding materials implicated in the Grenfell Tower fire, certain composite panels with polyethylene cores remain in use and face increasing scrutiny. The International Building Code mandates NFPA 285 testing for wall assemblies in Type I through III construction above 40 feet, where a costly and time-consuming process that many small manufacturers cannot afford. Architects often default to non-combustible materials like metal or fiber cement to avoid compliance risks by limiting innovation in lighter or more sustainable composites. This regulatory caution, while safety justified, constrains material choice and increases system costs by slowing the adoption of next-generation rainscreen products that balance performance, aesthetics, and environmental impact.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Material, End Use, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Texas, Florida, New York, and the rest of the United States |

| Market Leaders Profiled | Kingspan Group plc, Rockwool International A/S, Saint-Gobain S.A., Etex Group, Sika AG, Trespa International B.V., James Hardie Industries plc, Nichiha Corporation, Boral Limited, Arconic Corporation, Fiberon LLC, Swisspearl Group AG |

SEGMENTAL ANALYSIS

By Material Insights

The metal cladding segment was accounted in holding 36.4% of the United States rainscreen cladding market share in 2025, with the metal’s exceptional performance in fire resistance, durability,y and design adaptability, which align closely with the demands of modern high-performance facades. Aluminum and zinc alloys dominate due to their lightweight properties, corrosion resistance, and recyclability. Furthermore, metal systems integrate seamlessly with prefabricated construction methods,s which are gaining traction as the industry grapples with persistent labor shortages. Municipal building codes in states like California and New York increasingly favor non-combustible materials for buildings over four stories, reinforcing metal’s regulatory advantage. The material’s compatibility with digital fabrication also enables complex geometries and custom finishes that appeal to architects seeking both aesthetic distinction and technical reliability in ventilated wall assemblies.

The high-pressure laminate segment is swiftly emerging at an anticipated CAGR of 9.1% from 2026 to 20,,34 with its unique ability to deliver the visual richness of natural materials such as wood or stone while offering superior resistance to UV fading, moisture, re and impact. Unlike traditional organic claddings, high-pressure laminate requires minimal maintenance and does not warp, crack, or require sealing, making it ideal for mid-rise multifamily and mixed-use developments. Recent advancements have also addressed historical fire performance concerns with new phenolic core variants achieving compliance with NFPA 285 testing requirements for buildings up to 75 feet tall, as confirmed by the International Code Council. Urban infill projects in cities like Denver and Austin are increasingly specifying these panels to achieve distinctive street-level aesthetics without compromising durability or sustainability goals.

By End Use Insights

The commercial sector was the dominant segment by capturing 54.3% of the US rainscreen cladding market share in 2025, with the extensive deployment of rainscreen systems in office towers,s retail centers, and hospitality buildings, where energy efficiency,ency moisture control,ntrol and architectural identity are critical. The US Energy Information Administration states that commercial buildings consume nearly 18% of the nation’s total energy, with heating and cooling accounting for over 40% of that usage, prompting developers to adopt high-performance envelopes that reduce thermal bridging. Additionally, municipal mandates in coastal and high precipitation regions such as Seattle and Miami now require drainage planes and ventilated cavities in new commercial construction to mitigate long-term moisture damage. Corporate sustainability commitments, including science-based decarbonization targets by firms like Microsoft and JPMorgan Chase, further incentivize facade solutions that enhance building longevity and reduce operational carbon over the asset lifecycle.

The institutional segment is projected to grow at a CAGR of 8.5% throughout the forecast period with the unprecedented federal and state investment in public infrastructure, particularly in education and healthcare facilities, where building performance directly impacts occupant health and safety. The Bipartisan Infrastructure Law allocated 122 billion dollars for school modernization, and the US Department of Education estimates that over half of the nation’s 130000 public school buildings were constructed before 1990, many lacking adequate moisture management. Rainscreen cladding’s ability to prevent mold growth and interior condensation aligns precisely with these health-centric mandates. Furthermore, state-level green building policies, such as California’s requirement for all new public buildings to achieve LEED Silver certification, favor ventilated facades for their contribution to indoor environmental quality and thermal comfort, making institutional projects a high-growth frontier for rainscreen technology.

COMPETITIVE LANDSCAPE

The US rainscreen cladding market features a competitive landscape defined by a mix of large multinational building product manufacturers and specialized regional fabricators. Competition is not primarily price-driven but centers on technical performance of compliance with evolving building codes nd aesthetic customization. Major players differentiate through proprietary system engineerin, fire-testedd assemblies, and digital design support tools that streamline specification and installation. The market is further shaped by stringent local regulations, particularly in coastal and high seismic zones, which favor companies with proven track records in code-compliant solutions. New entrants face high barriers, including NFPA 285 certification costs and the need for established contractor networks. At the same time, demand for sustainable materials is encouraging innovation in recycled content and low embodied carbon cladding. This dynamic environment rewards firms that combine engineering rigor with agile manufacturing and strong architectural relationships for fostering continuous advancement in facade technology and performance standards across the sector.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. Rainscreen Cladding Market include

- Kingspan Group plc

- Rockwool International A/S

- Saint-Gobain S.A.

- Etex Group

- Sika AG

- Trespa International B.V.

- James Hardie Industries plc

- Nichiha Corporation

- Boral Limited

- Arconic Corporation

- Fiberon LLC

- Swisspearl Group AG

TOP LEADING PLAYERS IN THE MARKET

- Kawneer is a leading manufacturer of architectural aluminum systems in the United States, offering a comprehensive portfolio of rainscreen cladding solutions for commercial and institutional buildings. The company is recognized globally for its engineering precision and integration of thermal break technology that enhances building envelope performance. Kawneer has strengthened its position by launching next-generation pressure equalized rainscreen systems compliant with stringent fire and wind load standards. Recently, the company expanded its digital design support tool,s enabling architects to model façade performance in real time. Its collaboration with sustainability certification bodies ensures its products contribute to LEED and WELL building credits, reinforcing its role in advancing hhigh-performancefaçades worldwide.

- TerraCORE Panels specializes in terracotta rainscreen systems combining aesthetic versatility with exceptional durability and thermal mass benefits. The company supplies custom-fabricated terracotta panels to high-profile projects across North America and exports to Europe and the Middle East. TerraCORE has enhanced its market presence through investments in robotic fabrication technology that reduces lead times and improves dimensional accuracy. In recent years, it introduced a line of low-carbon terracotta made with recycled content and solar-fired kilns, aligning with global decarbonization goals. Its participation in international building expos and façade research consortia underscores its commitment to advancing ceramic cladding innovation beyond US borders.

- Centria, a part of Nucor Building Systems, ms is a major provider of metal composite and insulated metal panel rainscreen systems widely used in airports, hospitals,t malls, and corporate campuses. The company contributes to the global market through its proprietary thermal and moisture management technologies integrated into panelized facade solutions. Centria has recently upgraded its manufacturing facilities to incorporate closed-loop water recycling and energy-efficient curing processes. It also launched a digital twin platform for façade performance simulation, allowing clients to assess energy and condensation risks during design. These initiatives reinforce its reputation for delivering code-compliant high-performance cladding systems that meet international building standards.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the US rainscreen cladding market prioritize vertical integration to control material quality and delivery timelines while reducing dependency on external suppliers. They invest heavily in research and development to enhance the fire resistance, thermal performance, and moisture management capabilities of their systems. Strategic partnerships with architects , ts engin e, rs and sustainability consultants ensure early specification in high-value projects. Companies also expand digital capabilities, including BIM libraries and performance simulation tools to support design integration. Additionally, they pursue environmental certification and low-carbon manufacturing processes to align with green building mandates and corporate ESG goals, driving adoption in both public and private sectors.

MARKET SEGMENTATION

This research report on the U.S. rainscreen cladding market is segmented and sub-segmented into the following categories.

By Material

- Metal Cladding

- High-Pressure Laminate (HPL)

- Fiber Cement

- Composite Material

- Terracotta

- Wood

- Others

By End Use

- Commercial

- Institutional

- Residential

- Industrial

By Country

- California

- Texas

- Florida

- New York

- Illinois

- Rest of the United States

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com