U.S. Reading Glasses Market Size, Share, Trends & Growth Forecast Report - Segmented By Age Group, Corrective Strength, and Type, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Reading Glasses Market Size

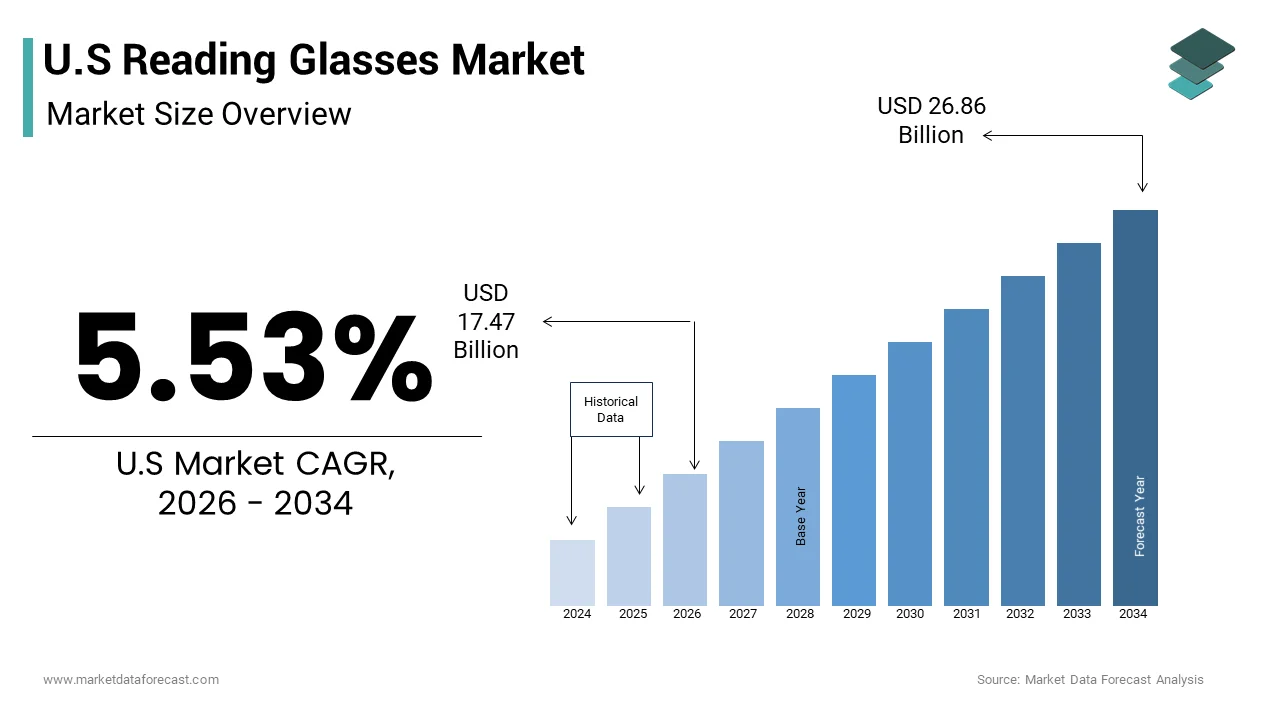

The U.S reading glassed market size was valued at USD 16.55 billion in 2025 and is anticipated to reach USD 17.47 billion in 2026 to reach USD 26.86 billion by 2034, growing at a CAGR of 5.53% during the forecast period from 2026 to 2034.

According to the National Eye Institute, approximately 128 million people in the U.S. will have presbyopia by 2050, reflecting the inevitable demographic shift toward an aging population. As per the American Optometric Association, nearly 75% of adults between the ages of 45 and 64 experience some degree of difficulty with near vision tasks. The proliferation of digital devices has also expanded the market scope, with consumers seeking specialized lenses to mitigate computer vision syndrome. According to recent surveys by Harmony Healthcare IT, Americans spend an average of over 5 hours per day looking at their phone screens alone, which exacerbates eye fatigue and drives demand for blue light filtering reading glasses. These socioeconomic and health related factors underscore the transition of reading glasses from medical necessities to essential daily wear items. The market is increasingly influenced by consumer preferences for style, comfort, and technological integration, such as anti-reflective coatings and lightweight materials. This evolution reflects a broader trend where visual health intersects with personal aesthetics and digital wellness, creating a dynamic and resilient industry landscape.

MARKET DRIVERS

Aging Population and Increasing Prevalence of Presbyopia

The demographic shift toward an older population is one of the key factors propelling the growth of the U.S. reading glasses market. Presbyopia is a universal condition that typically manifests after the age of 40, affecting nearly everyone as they age. According to the U.S. Census Bureau, the number of Americans aged 65 and older is projected to reach 95 million by 2060, representing a significant increase from current levels. This growing cohort requires visual assistance for daily activities, such as reading, cooking, and using smartphones. According to the National Institutes of Health, the prevalence of presbyopia increases sharply after age 45, with over 90% of individuals affected by age 60. The sheer volume of potential users ensures a consistent and expanding customer base for reading glasses manufacturers and retailers. Additionally, the increasing life expectancy means that individuals will require visual correction for a longer period of their lives. As per the Centers for Disease Control and Prevention, approximately 1 in 28 Americans aged older than 40 years is affected by low vision or blindness. This demographic inevitability creates a stable demand floor that is resistant to economic fluctuations. Manufacturers are responding by offering a wider range of magnification strengths and multifocal options to cater to varying degrees of vision loss. The sustained growth of the senior demographic ensures that the reading glasses market remains robust and continues to expand in tandem with population trends.

Proliferation of Digital Devices and Screen Time

The ubiquitous presence of digital devices and the resulting increase in screen time have significantly accelerated the demand for reading glasses in the U.S., which is further boosting the U.S. market expansion. Modern lifestyles involve extensive use of smartphones, tablets, and computers for work, education, and entertainment, which is leading to increased eye strain and fatigue. According to the Pew Research Center, 90% of Americans own a smartphone, and nearly all adults use the internet regularly, exposing them to prolonged periods of near focus. This behavior exacerbates presbyopic symptoms and leads to a condition known as digital eye strain or computer vision syndrome. According to the American Optometric Association, common symptoms associated with digital eye strain include blurred vision, headaches, and dry eyes. To mitigate these effects, consumers are increasingly purchasing reading glasses with blue light filtering coatings and anti-reflective treatments. The rise of remote work has further intensified this trend, as employees spend more hours in front of screens without the natural breaks associated with office commutes. As per a survey by the Vision Council, 70% of adults report that they use digital devices for more than six hours a day. This high level of exposure drives the need for specialized eyewear that enhances visual comfort and clarity. Manufacturers are innovating with lens technologies that reduce glare and improve contrast, making reading glasses an essential tool for digital natives. The intersection of technology usage and visual health ensures sustained growth in this segment.

MARKET RESTRAINTS

Availability of Low Cost Over-The-Counter Alternatives

The widespread availability of low cost over the counter reading glasses is primarily hindering the U.S. reading glasses market expansion. Ready-made readers are sold in pharmacies, supermarkets, and online retailers at prices ranging from 5 to 20 dollars, making them an attractive option for budget conscious consumers. According to the Federal Trade Commission, these inexpensive alternatives are easily accessible and do not require a prescription or professional consultation. This convenience undermines the value proposition of higher priced custom glasses, which can cost hundreds of dollars. Data from consumer surveys indicates that over 60% of presbyopic individuals initially try over the counter readers before seeking professional care. The perception that reading glasses are a commodity rather than a medical device leads many consumers to prioritize price over quality and fit. As per the Federal Trade Commission, the Eyeglass Rule requires that optometrists and ophthalmologists provide patients a copy of their prescription after an exam without extra cost, which allows consumers to buy from various sellers. Furthermore, the lack of regulation for over the counter readers means that quality and accuracy can vary, leading to potential dissatisfaction but also reinforcing the idea that expensive options are unnecessary. This price sensitivity limits the ability of premium brands to differentiate themselves based solely on optical quality. The ubiquity of low cost options creates a ceiling for market growth in the higher end segments as consumers remain reluctant to upgrade unless medically necessary. This restraint challenges manufacturers to justify higher price points through added features, such as style, durability, or advanced lens coatings.

Lack of Awareness Regarding Professional Eye Examinations

A significant portion of the population lacks awareness regarding the importance of regular professional eye examinations, which is leading to self-diagnosis and improper use of reading glasses and this is further hampering the reading glasses market growth in the U.S. Many individuals assume that blurry near vision is solely due to aging and purchase over the counter readers without ruling out other underlying eye conditions. According to the American Academy of Ophthalmology, adults should get an eye disease screening by age 40, yet many people wait until they experience significant vision problems. This lack of professional guidance can result in the use of incorrect magnification strengths, which may cause headaches, eye strain, and further vision deterioration. According to the National Eye Institute, common conditions, such as glaucoma and diabetic retinopathy, are expected to affect over 6 million and 14 million people respectively by 2050. The misconception that reading glasses are a one size fits all solution discourages consumers from seeking personalized care. As per healthcare statistics, only 30% of adults between the ages of 45 and 64 have had a comprehensive dilated eye exam in the past year. This gap in preventive care limits the market for custom prescribed glasses and reduces opportunities for optometrists to recommend advanced lens solutions. The reliance on trial and error purchasing methods perpetuates a cycle of suboptimal visual health. Educating consumers about the benefits of professional fittings and the risks of untreated eye diseases is crucial, but remains a challenging endeavor for the industry. This awareness gap restricts the conversion of casual users into loyal customers of premium optical services.

MARKET OPPORTUNITIES

Integration of Blue Light Filtering and Anti-Fatigue Technologies

The integration of blue light filtering and anti-fatigue technologies offers a potential opportunity for the reading glasses market in the U.S., as consumers seek protection from digital eye strain. With the increasing amount of time spent on screens, there is a growing demand for lenses that block harmful high energy visible light. According to the Vision Council, sales of blue light blocking lenses have increased by 20% annually as awareness of their benefits grows. Manufacturers can capitalize on this trend by incorporating these features into both prescription and over the counter reading glasses. According to the American Optometric Association, blue light filtering can reduce eye strain and discomfort associated with prolonged screen use. This health benefit appeals to a broad demographic, including younger adults who are beginning to experience early signs of presbyopia. As per market research, 65% of consumers are willing to pay a premium for lenses that offer additional protective features. The opportunity extends to marketing these glasses as wellness tools rather than just vision correctors. Brands can collaborate with tech companies and health organizations to validate claims and build trust. The development of stylish frames that appeal to younger demographics further expands the addressable market. By positioning reading glasses as essential accessories for digital life, companies can drive higher average transaction values. This technological differentiation allows manufacturers to escape the commodity trap of basic readers and create a niche for high value functional eyewear.

Expansion into Fashion Forward and Customizable Designs

The transformation of reading glasses into fashion accessories offers a significant opportunity for market growth through style driven differentiation. Consumers increasingly view eyewear as an extension of their personal identity and are willing to invest in designs that complement their attire. The eyewear market is heavily influenced by consumer trends where aesthetics play a vital role in purchase decisions. Manufacturers can leverage this by collaborating with designers and launching limited edition collections that appeal to style conscious buyers. Data from retail reports shows that fashionable frames command higher margins and foster brand loyalty among younger presbyopic users. The rise of direct to consumer brands has facilitated customization options, allowing customers to choose frame colors, materials, and shapes online. As per consumer surveys, 50% of women consider the style of their reading glasses as important as their functionality. This shift encourages repeat purchases as users buy multiple pairs for different occasions. The opportunity also lies in marketing reading glasses as jewelry or statement pieces rather than medical devices. Social media platforms play a crucial role in showcasing these designs and influencing purchasing decisions. By focusing on aesthetics and personalization, companies can attract a broader audience, including those who previously resisted wearing readers due to stigma. This strategic pivot towards fashion enhances the emotional appeal of the product and drives volume growth.

MARKET CHALLENGES

Regulatory Scrutiny and Quality Control Standards

The increasing regulatory scrutiny regarding the quality and accuracy of over the counter products is a significant challenge to the U.S. reading glasses market growth. While ready-made readers are generally exempt from strict medical device regulations, there are growing concerns about inconsistent magnification levels and optical clarity. According to the Food and Drug Administration, reading glasses are regulated as Class I medical devices and must meet specific standards for safety and labeling. Recent initiatives by consumer advocacy groups have called for stricter standards to ensure that all reading glasses meet minimum optical performance criteria. Data from testing reports shows that variations in diopter strength can occur in low cost readers, which may cause eye strain for the user. This variability undermines consumer trust and exposes brands to liability risks. As per industry reports, the focus on stricter quality control have led to increased operational costs for manufacturers. Compliance with evolving standards requires investment in quality control processes and third party certifications, which increase production costs. Small manufacturers may struggle to meet these requirements, leading to market consolidation. The challenge also extends to online retailers who must verify the accuracy of product descriptions and specifications. Failure to adhere to quality standards can result in recalls and reputational damage. Navigating this complex regulatory landscape requires constant vigilance and adaptation. Companies must balance affordability with compliance to maintain consumer confidence. This challenge necessitates a proactive approach to quality assurance and transparency in manufacturing practices.

Stigma Associated With Aging and Visual Impairment

Despite the universality of presbyopia, a persistent stigma associated with aging and visual impairment continues to hinder the adoption of reading glasses among certain demographics, which is further challenging the U.S. market expansion. Many individuals perceive the need for readers as a sign of declining vitality and youthfulness, leading to resistance and delay in purchasing. According to psychological studies on body image, a significant portion of adults in their 40s and 50s avoid wearing reading glasses in public due to fear of appearing old. This social anxiety limits the frequency of use and encourages reliance on less effective coping mechanisms, such as holding devices further away. Data from market research indicates that 30% of presbyopic individuals admit to hiding their need for readers from colleagues and friends. This stigma particularly affects men, who are statistically less likely to seek visual correction than women. As per industry observations, the reluctance to embrace reading glasses results in lost sales opportunities for premium and fashionable options. Manufacturers face the challenge of rebranding reading glasses as symbols of sophistication and intelligence rather than decline. Marketing campaigns that feature vibrant and active older adults can help shift perceptions but require significant investment. The cultural narrative around aging is slowly changing but remains a barrier to full market penetration. Overcoming this psychological hurdle requires nuanced messaging that emphasizes empowerment and style. Until the stigma is fully dismantled, it will continue to suppress demand and limit the potential of the reading glasses market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.53% |

| Segments Covered | By Age Group, Corrective Strength, and Type, By Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

| Regions Covered | California, Washington, Oregon, New York & Rest of the United States |

| Market Leaders Profiled | EssilorLuxottica (France), ZEISS International (Germany), Warby Parker Inc, Zenni Optical Inc, SAFILO GROUP S.P.A. (Italy), HOYA Corporation (Japan), Hilco Vision (U.S.), ThinOptics, Inc. (U.S.), ZENNI OPTICAL, INC. (U.S.), GUNNAR Optiks (U.S.), Pixel Eyewear (U.S.), Swanwick (U.S.) |

SEGMENTAL ANALYSIS

By Age Group Insights

The 18 to 64 years age group dominated the market by holding the highest share of the U.S. market in 2025. The dominance of 18 to 64 years segment in the U.S. market can be credited to the early onset of presbyopia and the high prevalence of digital eye strain among working adults. This demographic encompasses individuals who are actively engaged in the workforce and daily activities that require sustained near vision. The physiological reality that presbyopia typically begins to affect individuals in their early to mid-forties that falls squarely within this age bracket is further boosting the expansion of this segment in the U.S. market. According to the American Optometric Association, presbyopia usually becomes noticeable in the mid 40s and continues to worsen until around age 65. According to the U.S. Bureau of Labor Statistics, there are millions of people in the labor force with a large concentration in the 45 to 64 age range. These individuals rely heavily on clear near vision for tasks, such as reading documents, using smartphones, and operating computers. According to the National Eye Institute, the number of people with presbyopia in the U.S. is projected to reach 128 million by 2050, with the majority of this growth occurring within the working age population. As professionals continue their careers, they cannot afford visual impairment that hinders productivity. Consequently, this group represents the largest volume of consumers seeking both over the counter and prescription reading solutions. The necessity to maintain professional competence and daily functionality ensures that this age group remains the primary consumer base for reading glasses, sustaining its leadership position in the market.

On the other hand, the 65 years and older segment is growing at the fastest and is estimated to grow at a CAGR of 5.03% during the forecast period owing to the rapid expansion of the senior population and the increasing severity of vision issues associated with advanced age. As life expectancy increases and the baby boomer generation ages, the number of individuals requiring strong visual correction is rising significantly. According to the U.S. Census Bureau, the population aged 65 and older is projected to grow to 95 million by 2060. This substantial increase expands the total addressable market for reading glasses. According to the National Institutes of Health, nearly 100% of individuals over the age of 65 experience some form of presbyopia, often requiring higher magnification strengths. Unlike younger users, who may only need readers for specific tasks, seniors often require them for most daily activities, including reading medication labels, cooking, and hobbies. The sheer volume of new entrants into this age group drives consistent demand for replacement and multiple pairs of glasses. As per healthcare demographics, the senior cohort is also more likely to have disposable income and insurance coverage for vision care, facilitating purchases. This demographic inevitability ensures that the 65 and older segment will experience the highest growth rate in the coming years. The structural expansion of this population base provides a robust foundation for market growth.

By Corrective Strength Insights

The +0.25 to +2 corrective strength segment held the major share of the U.S. reading glasses market in 2025. The growth of the +0.25 to +2 segment in the U.S. market is majorly attributed to the initial and most common stage of presbyopia that affects the widest demographic. Most individuals begin to experience difficulty with near vision in their early forties, requiring low magnification powers. According to the American Optometric Association, the onset of presbyopia typically starts around age 40 with mild symptoms that progress gradually. According to the National Eye Institute, the majority of first time reading glass users falls within the lower magnification ranges. This large influx of new users creates a substantial volume of sales for lower strength lenses. As per industry retail standards, over the counter readers are most commonly stocked in these strengths because they meet the needs of the broadest audience. The gradual nature of vision loss means that individuals spend several years in this low strength range before progressing to higher powers. This extended duration of use ensures consistent demand for replacements and backups. Furthermore, many consumers in this stage prefer affordable over the counter options, which are predominantly available in these strengths. The sheer number of people entering this phase of visual aging sustains the leadership of the +0.25 to +2 segment. The widespread availability and affordability of these strengths further reinforce their market dominance.

However, the greater than +3 corrective strength segment is the fastest growing category in the U.S. reading glasses market and is expected to exhibit a CAGR of 5.4% during the forecast period. The natural progression of presbyopia in the aging population is one of the major factors propelling the growth of this segment in the U.S. market. As individuals age, the lens of the eye continues to lose flexibility, requiring stronger magnification to focus on near objects. According to the National Institutes of Health, by age 65, most individuals require significant magnification strength to perform near vision tasks. According to the U.S. Census Bureau, the fastest growing age group is those over 75, who are most likely to need high strength readers. This demographic shift ensures a steady increase in the number of consumers requiring powerful lenses. As per clinical data, the demand for high magnification glasses increases significantly among the elderly population. Individuals in this stage often struggle with standard over the counter options and seek specialized high power readers. The necessity for clear vision in daily tasks, such as reading fine print and managing health conditions, drives consistent purchases. The lack of alternative solutions for severe presbyopia makes high strength glasses essential. This physiological inevitability, combined with the expanding senior population, drives the rapid growth of the greater than +3 segment.

By Type Insights

The over-the-counter (OTC) segment led the market by capturing the largest share of the U.S. market in 2025. The growth of the OTC segment in the U.S. market is driven by its affordability, accessibility, and convenience for consumers with mild to moderate presbyopia. These ready-made glasses are widely available in pharmacies, supermarkets, and online. Unlike prescription glasses, which require professional exams and custom fabrication, OTC readers are mass produced and sold at low prices. According to the Federal Trade Commission, OTC readers can be purchased for as little as 5 to 20 dollars, making them an economical choice for many consumers. Data from retail reports indicates that a high percentage of reading glasses sold in the U.S. are over the counter products. The presence of these items in high traffic locations, such as drugstores, grocery stores, and convenience stores, ensures easy access. As per consumer behavior studies, the impulse buy nature of OTC readers contributes significantly to sales volume. Individuals often purchase them when they first notice vision changes without seeking professional care. The convenience of immediate availability without waiting for lab processing appeals to busy consumers. Furthermore, the variety of styles and strengths available off the shelf allows for quick selection. The low financial risk encourages experimentation with different pairs. This combination of low cost and ubiquitous presence sustains the leadership of the OTC segment in the market.

However, the prescription segment is anticipated to register a CAGR of 4.4% during the forecast period in the U.S. market owing to the increasing complexity of vision needs among consumers, particularly the prevalence of astigmatism and other refractive errors. Many individuals with presbyopia also suffer from astigmatism, which requires cylindrical correction that OTC readers cannot provide. According to the National Eye Institute, millions of adults in the US have astigmatism, necessitating custom lenses. Data from optical associations shows that as people age, the likelihood of having multiple vision issues increases. This complexity drives consumers to seek professional eye exams and prescribed glasses. The inability of OTC readers to correct astigmatism leads to eye strain and headaches, prompting upgrades to prescription options. According to the American Academy of Ophthalmology, regular eye exams are vital for detecting age related eye diseases, leading to more prescriptions. The demand for progressive lenses, which correct near, intermediate, and distance vision in one pair, is also rising. These specialized products offer superior visual quality and convenience. The growing awareness of the limitations of OTC readers encourages shifts to prescription solutions. This medical necessity drives the steady growth of the prescription segment.

COUNTRY ANALYSIS

U.S. Market Analysis

The United States is likely to maintain its dominant position in the reading glasses market for the next few years due to a large and rapidly aging population combined with high spending on vision care. The U.S. maintains its dominance due to a large and rapidly aging population combined with high healthcare spending on vision care. The prevalence of presbyopia is universal among older adults, creating a vast consumer base. According to the U.S. Census Bureau, the population aged 65 and older is projected to reach 95 million by 2060, driving sustained demand for visual aids. According to the Centers for Medicare and Medicaid Services, national health expenditure per capita is among the highest in the world, facilitating access to eye care services. The widespread availability of vision insurance and flexible spending accounts encourages consumers to purchase high quality prescription reading glasses. As per the Federal Trade Commission, the Eyeglass Rule allows patients to obtain their prescriptions and shop at different providers, which promotes competition in the market. The strong regulatory framework ensures product safety and quality, building consumer trust. The cultural emphasis on maintaining productivity and independence in old age further supports market growth. With increasing life expectancy and digital device usage, the U.S. remains the premier market for reading glasses, setting global trends for innovation and consumption.

COMPETITIVE LANDSCAPE

The competition in the U.S. reading glasses market is intense and characterized by a mix of established optical giants and agile direct to consumer startups. Large companies leverage their extensive resources to dominate through broad distribution networks and heavy marketing spending. They continuously innovate to maintain relevance and protect their market positions against newer entrants. Independent brands often differentiate themselves by focusing on niche segments such as affordable fashion or specialized lens technologies. These smaller entities utilize digital channels to build direct relationships with consumers and foster community loyalty. The barrier to entry has lowered due to the rise of e commerce platforms allowing new players to launch with minimal overhead. This dynamic environment forces all participants to prioritize speed and agility in product development. Price competition is prevalent in the mass market segment while premium brands compete on brand heritage and technological superiority. Retailers play a crucial role by curating assortments that balance popular staples with emerging trends. Private label offerings from major retailers further intensify pressure on branded manufacturers. Consumer loyalty is increasingly fluid as shoppers experiment with new products influenced by social media trends. Companies must therefore maintain constant engagement through educational content and transparent communication. The ability to adapt quickly to regulatory changes and shifting consumer values determines long term survival. Strategic partnerships and collaborations are common as firms seek to expand their reach and capabilities. Overall the market remains highly fragmented with no single entity holding absolute dominance across all categories.

KEY MARKET PLAYERS

A few of the market players that are dominating the U.S reading glasses market are

- EssilorLuxottica (France)

- ZEISS International (Germany)

- Warby Parker Inc

- Zenni Optical Inc

- SAFILO GROUP S.P.A. (Italy)

- HOYA Corporation (Japan)

- Hilco Vision (U.S.)

- ThinOptics, Inc. (U.S.)

- ZENNI OPTICAL, INC. (U.S.)

- GUNNAR Optiks (U.S.)

- Pixel Eyewear (U.S.)

- Swanwick (U.S.)

Top Three Key Players In The Market

- EssilorLuxottica SA stands as a global leader in the U.S. reading glasses market through its extensive portfolio of brands including Ray Ban Oakley and LensCrafters. The company integrates manufacturing and retail operations to control the entire value chain from lens production to final consumer sale. Recent strategic initiatives include the expansion of its digital health offerings with smart glasses that incorporate audio and visual assistance features. EssilorLuxottica has invested heavily in teleoptometry services allowing customers to obtain prescriptions remotely which strengthens its direct to consumer capabilities. The corporation focuses on sustainability by introducing eco friendly frame materials and recycling programs. Its robust distribution network ensures widespread availability in both independent optical stores and large retail chains. By leveraging advanced lens technologies such as blue light filtering and anti fatigue coatings the company addresses modern visual needs. These efforts reinforce its position as a premium provider of vision care solutions.

- Warby Parker Inc has disrupted the U.S. reading glasses market by offering stylish and affordable eyewear through a direct to consumer model. The company is renowned for its Home Try On program which allows customers to test frames before purchasing. Recent actions to strengthen its market position include the expansion of its physical retail footprint with new stores in key urban markets. Warby Parker has enhanced its digital platform with virtual try on technology using augmented reality to improve online shopping experiences. The corporation emphasizes social responsibility through its Buy a Pair Give a Pair initiative which builds brand loyalty and positive public perception. It offers a wide range of ready made readers and custom prescription options at competitive prices. By focusing on transparency and customer convenience Warby Parker appeals to younger demographics who value aesthetics and ethics. Its integrated approach to design manufacturing and sales ensures high quality control and rapid innovation.

- Zenni Optical Inc holds a significant position in the U.S. reading glasses market by providing low cost eyewear exclusively through its online platform. The company leverages vertical integration to minimize costs and offer competitive pricing for both prescription and over the counter readers. Recent strategies to strengthen its market presence include the introduction of advanced lens coatings such as blue light blocking and anti reflective treatments at no extra cost. Zenni has expanded its product line to include fashionable frames and collaborations with designers to attract style conscious consumers. The corporation invests in user friendly website features including virtual face shape analysis and detailed sizing guides. Its efficient supply chain enables fast delivery times despite the direct to consumer model. Zenni actively engages with customers through social media and community forums to build brand advocacy. By prioritizing affordability and accessibility Zenni captures a large segment of budget aware buyers. Its focus on technological innovation in lens manufacturing ensures consistent quality and customer satisfaction.

Top Strategies Used By Key Market Participants

Key players in the U.S. reading glasses market employ several strategic initiatives to maintain competitiveness and drive growth. Product innovation remains a primary strategy with companies investing heavily in research and development to create advanced lens technologies such as blue light filtering and anti fatigue coatings. Brands frequently introduce stylish frames and customizable options to meet evolving consumer preferences for aesthetics and functionality. Digital transformation is another critical approach as firms enhance their online presence through e commerce platforms and virtual try on tools. Companies utilize data analytics to offer personalized recommendations and improve customer experiences. Strategic partnerships with healthcare providers and insurance companies help build credibility and reach targeted audiences effectively. Sustainability initiatives are increasingly prominent with firms adopting eco friendly materials and ethical sourcing practices to appeal to environmentally conscious buyers. Direct to consumer models allow brands to control distribution and increase margins while offering competitive pricing. These multifaceted strategies enable market participants to adapt to changing trends and sustain long term success in the dynamic industry landscape.

MARKET SEGMENTATION

This research report on the U.S reading glasses market is segmented and sub-segmented into the following categories.

By Age Group

- Less than 18 Years

- 18 to 64 Years

- 65 Years and Older

By Corrective Strength

- 0.25 to +2

- +2.25 to +3

- Greater than +3

By Type

- Prescription

- Over-the-Counter (OTC)

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

What is driving the growth of the U.S. reading glasses market?

An aging population, increasing vision-related issues, and growing awareness of eye health are driving market growth.

What does the U.S. reading glasses market include?

The market includes prescription reading glasses, over-the-counter reading glasses, blue-light reading glasses, and specialty eyewear products.

Which product category holds the largest share of the U.S. reading glasses market?

Over-the-counter reading glasses hold the largest share due to their affordability and easy accessibility.

Why are reading glasses becoming increasingly popular in the United States?

Rising cases of age-related vision changes and increased screen exposure are boosting demand for reading glasses.

Who are the primary consumers in the U.S. reading glasses market?

Older adults, working professionals, students, and individuals experiencing near-vision difficulties are the primary consumers.

How are consumer preferences influencing the U.S. reading glasses market?

Consumers are increasingly seeking lightweight, stylish, and comfortable eyewear with enhanced visual performance.

What factors are increasing demand for blue-light reading glasses in the U.S.?

Growing digital device usage and concerns about eye strain are driving demand for blue-light filtering lenses.

What challenges are impacting the U.S. reading glasses market?

Price competition, counterfeit products, and changing consumer purchasing behaviors can affect market growth.

How is innovation shaping the U.S. reading glasses industry?

Advanced lens technologies, customizable frames, and online eyewear retail platforms are transforming the market.

What is the future outlook for the U.S. reading glasses market?

The market is expected to grow steadily with increasing vision care awareness and continued demand for convenient eyewear solutions.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com