U.S. Rebar Market Size, Share, Trends & Growth Forecast Report Segmented By Type (Mild, Deformed), End Use and Country – Industry Analysis From 2026 to 2034

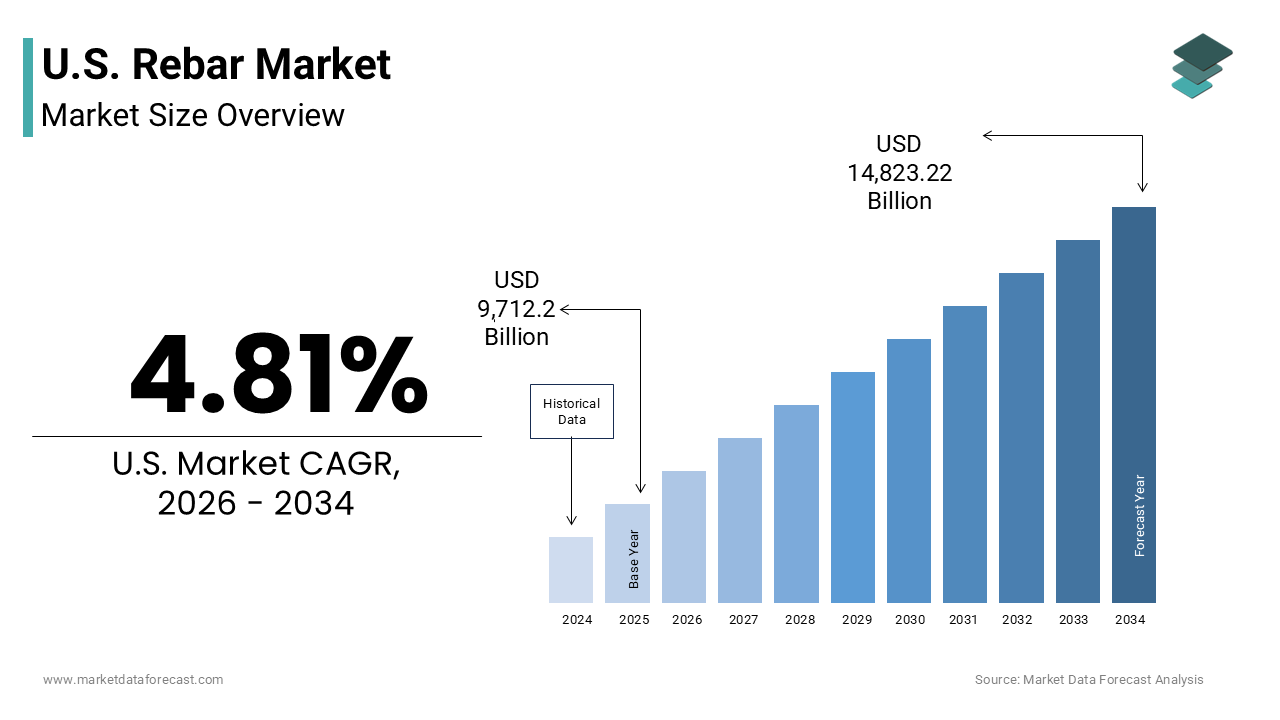

Market Size, 2025

$9,712.21 MnMarket Estimate, 2026

$10,179.37 MnMarket Forecast, 2034

$14,823.22 MnCAGR, 2026–2034

4.81%U.S. Rebar Market Report Summary

The U.S. rebar market was valued at USD 9,712.21 million in 2025 and is anticipated to reach USD 10,179.37 million in 2026 from USD 14,823.22 million by 2034, growing at a CAGR of 4.81% during the forecast period from 2026 to 2034. The growth of the U.S. rebar market is driven by increasing federal infrastructure investments, rising urban construction activities, and growing demand for reinforced concrete structures across residential, commercial, and civil engineering applications. Expanding adoption of corrosion-resistant rebar products, increasing investments in transportation and utility infrastructure, and rising focus on sustainable construction materials are further accelerating market growth. Moreover, advancements in digital fabrication technologies, expansion of smart construction practices, and increasing use of high-performance reinforcement solutions are supporting the expansion of the U.S. rebar market.

Key Market Trends

- Rising adoption of corrosion-resistant epoxy-coated and galvanized rebar for infrastructure projects in harsh environments.

- Increasing implementation of digital fabrication and Building Information Modeling (BIM) technologies in reinforcement planning and production.

- Growing demand for sustainable steel reinforcement products manufactured using recycled scrap metal.

- Strong focus on resilient infrastructure development capable of withstanding extreme weather and seismic conditions.

- Expansion of automated cutting, bending, and fabrication technologies improving productivity and reducing material waste.

Segmental Insights

- Based on type, the deformed rebar segment dominated the U.S. rebar market and held the largest share in 2025. The segment’s dominance is attributed to superior bonding characteristics with concrete, higher tensile strength, widespread compliance with construction standards, and extensive utilization across infrastructure, residential, and commercial projects.

- The mild rebar segment is projected to witness the fastest CAGR during the forecast period owing to increasing demand for decorative concrete applications, growing residential landscaping projects, rising restoration activities for historic structures, and ease of fabrication for customized designs.

- Based on end-use, the infrastructure segment accounted for the leading share of the U.S. rebar market in 2025. The dominance of this segment is driven by extensive government investments in roads, bridges, tunnels, water systems, and public transportation infrastructure under large-scale federal development programs.

- The residential segment is anticipated to register the fastest CAGR during the forecast period due to increasing housing construction activities, growing suburban development, rising renovation projects, and expanding adoption of reinforced concrete foundations in residential buildings.

Regional Insights

The United States maintained a strong position in the global rebar market in 2025, supported by large-scale infrastructure modernization programs, robust construction activity, and strong domestic steel manufacturing capabilities. California remains a major contributor to the U.S. rebar market due to extensive transportation infrastructure projects, earthquake-resistant construction requirements, and large-scale urban development activities. New York, Washington, and Oregon are also witnessing notable growth driven by bridge rehabilitation projects, commercial construction investments, and increasing focus on sustainable infrastructure development.

Competitive Landscape

The U.S. rebar market is highly competitive and characterized by the presence of integrated steel manufacturers, regional steel fabricators, and specialty reinforcement suppliers competing through production efficiency, product quality, and supply chain reliability. Leading companies are focusing on expanding manufacturing capacities, investing in automation technologies, strengthening sustainable steel production practices, and developing high-performance reinforcement products. Strategic partnerships with contractors, fabricators, and infrastructure developers are further strengthening market positioning across residential, commercial, and infrastructure construction applications. Prominent players in the U.S. rebar market include Nucor Corporation, Commercial Metals Company (CMC), Steel Dynamics, Inc., Gerdau S.A., EVRAZ North America, ArcelorMittal, Liberty Steel Group, Celsa Group, Outokumpu Oyj, Schnitzer Steel Industries, Inc., Byer Steel Group, Inc., and Cascade Steel Rolling Mills, Inc.

U.S. Rebar Market Size

The U.S. rebar market size was valued at USD 9,712.21 million in 2025 and is anticipated to reach USD 10,179.37 million in 2026 from USD 14,823.22 million by 2034, growing at a CAGR of 4.81% during the forecast period from 2026 to 2034.

The rebar is the national construction infrastructure, where steel reinforcement bars essential for concrete strengthening in residential, commercial, and civil engineering projects. Rebar serves as the tensile backbone of reinforced concrete structures by ensuring durability and resistance to structural stress in buildings, bridges, highways, and dams. According to the Census Bureau, there are approximately 140 million housing units in the United States, with a significant portion requiring ongoing maintenance and structural upgrades that utilize rebar. Geographic demand patterns are heavily influenced by regional construction activity, with substantial consumption in urban centers undergoing vertical expansion and coastal regions investing in resilient infrastructure. The sector is increasingly focused on sustainability, leveraging the recyclability of steel to meet green building certification requirements. Technological advancements in epoxy coating and galvanization have expanded application possibilities in corrosive environments, enhancing product longevity. Supply chain dynamics are shaped by the availability of ferrous scrap and energy costs by influencing production efficiency and pricing stability for end users in the construction sector.

MARKET DRIVERS

Federal Infrastructure Investment Catalyzes Civil Engineering Demand

The enactment of comprehensive federal legislation by institutionalizing long term demand through substantial capital allocation for public works is fuelling the growth of the United States rebar market. The Infrastructure Investment and Jobs Act authorizes new spending with a significant portion dedicated to the rehabilitation of roads, bridges, and transit systems that rely heavily on reinforced concrete. According to the American Society of Civil Engineers, the nation faces a 259 billion dollar backlog in bridge repair needs, necessitating extensive use of rebar for structural retrofitting and new construction. This legislative framework prioritizes the modernization of critical infrastructure, creating a predictable consumption trajectory for domestic steel producers. As per the Federal Highway Administration, over 45,000 bridges are classified as structurally deficient, requiring immediate attention that involves the replacement of deteriorated reinforcement systems. The mandate for using American made iron and steel in federally funded projects further secures market share for domestic rebar manufacturers, shielding them from international competition. These buy America provisions ensure that public funds circulate within the national economy, reinforcing industrial stability and encouraging capacity expansion. The focus on resilient infrastructure design also drives demand for higher grade rebar capable of withstanding extreme weather events and seismic activities. Construction spending on public infrastructure has shown consistent growth, reflecting the tangible implementation of these federal commitments. Manufacturers are scaling production capacities to meet the anticipated surge in orders, leading to higher employment rates in steel producing regions. This sustained government backing provides a buffer against cyclical downturns in private sector construction, ensuring steady revenue streams for industry participants.

Urban Vertical Expansion Drives High Rise Construction Activity

The continued trend of urbanization and land scarcity in major metropolitan areas is driving the adoption of reinforced concrete for high rise residential and commercial developments, directly boosting rebar consumption. The urban vertical expansion is also propelling the growth of the Steel reinforcement is essential for the structural integrity of tall buildings, providing the necessary tensile strength to support heavy loads and resist lateral forces from wind and seismic activity. According to the Council on Tall Buildings and Urban Habitat, there were 45 skyscrapers completed in the United States in 2025, with reinforced concrete structures accounting for a significant majority of these projects. Cities like New York, Chicago, and Miami continue to see dense vertical growth as populations concentrate in urban cores, creating demand for luxury apartments and office towers that utilize extensive rebar frameworks. As per construction industry data, the average high rise building requires thousands of tons of reinforcement steel, with density varying based on design complexity and height. The ability of reinforced concrete to offer fire resistance and acoustic insulation further enhances its appeal for multi-family housing projects. Developers value the predictability of concrete construction schedules, which helps in managing financing costs and leasing timelines. Additionally, the retrofitting of existing urban infrastructure often involves concrete additions or reinforcements, further expanding the market scope. The aesthetic appeal of exposed concrete elements in contemporary architecture also contributes to its popularity among designers seeking industrial chic aesthetics. This urban density dynamic ensures a consistent demand for high grade rebar in major economic hubs, supporting sustained production levels for domestic manufacturers.

MARKET RESTRAINTS

Volatility in Raw Material Costs Disrupts Production Economics

The fluctuations in the prices of ferrous scrap and energy inputs, where the profitability and operational stability of rebar manufacturers, which is limiting the growth of the United States rebar market. The cost structure of rebar production is heavily dependent on global commodity markets, which are subject to geopolitical tensions and supply chain disruptions. According to Trading Economics, the price of heavy melting steel scrap experienced a variance of over 20% in 2025, imposing severe pressure on electric arc furnace operators who rely on recycled metal as their primary feedstock. These elevated input costs often cannot be fully passed on to customers due to fixed price contracts and competitive bidding processes in the construction sector. As per the World Steel Association, global steelmaking capacity reached 2.55 billion metric tons by the end of 2025, creating an oversupply environment that limits pricing power for producers. The volatility in energy costs, particularly electricity and natural gas, further exacerbates production expenses, as steel manufacturing is an energy intensive process. Manufacturers face challenges in forecasting accurate profit margins when input prices swing unpredictably within short timeframes. This uncertainty discourages long term capital investment in new facilities or technology upgrades, potentially hindering innovation and efficiency gains. Smaller producers are disproportionately affected as they lack the financial reserves to absorb sudden cost spikes compared to integrated multinational corporations. The reliance on imported scrap materials for certain regions also exposes manufacturers to currency exchange risks and trade barriers. Consequently, companies must implement sophisticated hedging strategies and inventory management systems to mitigate financial exposure, adding complexity to their operational frameworks.

Stringent Environmental Regulations Increase Compliance Burdens

The imposition of rigorous environmental standards by federal agencies presents a substantial operational challenge for rebar manufacturers, which is additionally hindering the growth of the United States rebar market. The Environmental Protection Agency has implemented stricter limits on hazardous air pollutants emitted from iron and steel manufacturing facilities, compelling companies to upgrade their emission control systems. As per the Federal Register, compliance deadlines for these new standards were set for April 2027, requiring firms to invest millions of dollars in retrofitting existing plants to meet permissible emission levels. These regulatory mandates increase the overall cost of production, reducing competitiveness against imports from countries with less stringent environmental oversight. The transition towards low carbon manufacturing processes also demands substantial research and development investments, diverting resources from other strategic initiatives. Manufacturers must navigate a complex web of state and federal regulations that often vary by jurisdiction, creating administrative burdens and legal uncertainties. Non-compliance risks severe penalties and operational shutdowns, forcing companies to prioritize regulatory adherence over production optimization. The push for decarbonization also requires shifts in energy sourcing, such as adopting renewable energy or hydrogen-based reduction techniques, which are currently more expensive than traditional methods. The cost of installing carbon capture and storage systems can significantly impact project economics, delaying expansion plans. Furthermore, environmental advocacy groups frequently challenge permits for new facilities, leading to prolonged litigation and project delays. This regulatory landscape creates an unpredictable business environment where long term planning is difficult, discouraging new entrants and consolidating market power among larger firms with greater compliance capabilities.

MARKET OPPORTUNITIES

Adoption of Corrosion Resistant Coatings Expands Application Scope

The advancements in protective coating technologies to expand into harsh operating environments, such as coastal infrastructure and chemical processing facilities which is setting up new opportunities for the growth of the United States rebar market. Epoxy coated and galvanized rebar offer superior resistance to chloride induced corrosion, extending the service life of concrete structures in marine and de icing salt exposed areas. The economic burden drives demand for premium rebar products that reduce long term maintenance and replacement costs. The bridge projects in coastal states increasingly mandate the use of corrosion resistant reinforcement to meet durability standards and extend asset lifecycles. Manufacturers investing in advanced coating lines can access niche markets with higher profit margins and less competition. The growing emphasis on sustainable infrastructure also favors durable materials that minimize resource consumption over the structure's lifespan. The expansion of offshore wind energy projects further amplifies demand for specialized rebar capable of withstanding saline environments. Companies that secure certifications for these specialized applications can establish long term contracts with government agencies and energy corporations, ensuring stable order books. The ability to customize coating thickness and composition for specific project requirements also strengthens customer relationships and fosters collaborative engineering partnerships.

Integration of Digital Fabrication Technologies Enhances Efficiency

The integration of digital fabrication and Building Information Modeling technologies to improve design accuracy and operational efficiency, which is also to escalate the growth of the United States rebar market. Automated bending and cutting machines guided by digital models allow for precise production of complex rebar shapes, reducing material waste and labor requirements on construction sites. This technology enables seamless collaboration between engineers, fabricators, and contractors, ensuring that reinforcement details are translated accurately into buildable components. The ability to optimize rebar usage through algorithmic design reduces material waste and lowers overall project costs, enhancing the competitiveness of reinforced concrete against alternative structural systems. Digital twins also facilitate ongoing maintenance by providing owners with detailed data on structural health and reinforcement layout, extending the lifecycle of the asset. This technological advancement positions rebar as a smart, data rich building material, attracting tech savvy developers and institutional investors. The transition towards digital fabrication workflows allows for greater customization and complexity in architectural designs, opening new markets for high end commercial and cultural projects.

MARKET CHALLENGES

Supply Chain Fragility Impacts Timely Material Availability

The persistent vulnerabilities in the global and domestic supply chains by affecting the timely availability of raw materials and finished products is certainly one of the major challenges for the growth of the United States rebar market. Disruptions in logistics networks, rail capacity constraints, and port congestion can delay the delivery of scrap metal and finished rebar, causing costly setbacks for construction projects operating on tight schedules. According to the Logistics Management Institute, lead times for steel deliveries extended by an average of four weeks in 2025 compared to historical norms, due to bottlenecks in transportation and inventory management. This unpredictability forces contractors to hold larger inventories, tying up capital and increasing storage costs. As per industry feedback, just in time delivery models, which are for urban construction sites with limited storage space, have become increasingly difficult to maintain. Dependence on specific mills for specialized rebar grades creates single points of failure, where any production issue at one facility can ripple through the entire supply network. Geopolitical tensions and trade policies further complicate sourcing strategies, limiting options for alternative suppliers. The lack of transparency in tier two supply chains makes it difficult to anticipate disruptions caused by raw material shortages or energy outages. These logistical challenges undermine the reliability of rebar as a construction material, prompting some developers to consider alternative structural systems with more predictable supply lines. Mitigating these risks requires significant investment in supply chain diversification and digital tracking tools, adding to operational complexities.

Skilled Labor Shortages Hinder Production and Installation Capacity

The scarcity of skilled workers in steel fabrication and concrete reinforcement installation to meet growing demand efficiently is also to impede the growth of the United States rebar market. An aging workforce and insufficient vocational training programs have created a gap in the availability of qualified personnel needed to operate advanced bending machinery and install complex rebar cages. According to the Associated General Contractors of America, 70% of construction firms reported difficulty in filling craft worker positions in 2025, with steel fixing being among the hardest roles to staff. This labor deficit leads to extended project timelines and increased labor costs as companies compete for a limited pool of qualified personnel. As per workforce analysis, the average age of a certified steelworker in the United States is now over 45, indicating an impending retirement wave that will exacerbate the shortage in the coming decade. Training new workers requires significant time and resources, and the complexity of modern reinforcement designs demands higher levels of technical proficiency than in the past. Delays in fabrication and installation due to labor shortages can cascade into broader construction schedules, causing penalties and strained client relationships. The inability to scale up production quickly in response to surge demand limits revenue potential for fabricators. Furthermore, safety concerns arise when less experienced workers are pressed into service, potentially leading to accidents and regulatory scrutiny.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.81% |

| Segments Covered | By Type, End-Use and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Nucor Corporation, Commercial Metals Company (CMC), Steel Dynamics, Inc., Gerdau S.A., EVRAZ North America, ArcelorMittal, Liberty Steel Group, Celsa Group, Outokumpu Oyj, Schnitzer Steel Industries, Inc., Byer Steel Group, Inc., and Cascade Steel Rolling Mills, Inc. |

SEGMENTAL ANALYSIS

By Type Insights

The deformed rebar segment was accounted in holding a significant share of the United States rebar market in 2025 with its superior bonding capabilities with concrete, which are essential for structural integrity. The mandatory use of deformed bars in almost all modern reinforced concrete construction, including high rise buildings, bridges, and highways, where load transfer between steel and concrete is critical. The deformed bars provide significantly higher tensile strength and slip resistance compared to plain mild steel by making them the standard specification for structural applications under building codes such as ACI 318. The widespread adoption of deformed rebar is further reinforced by federal infrastructure projects that require materials capable of withstanding seismic activities and heavy dynamic loads. The manufacturing process for deformed rebar has become highly efficient, with domestic mills producing consistent quality products that meet ASTM A615 standards. This reliability ensures that engineers and architects prefer deformed bars for critical structural elements. The versatility of deformed rebar allows it to be used in various diameters and lengths, catering to diverse construction needs. Additionally, the integration of deformed rebar into prefabricated concrete components has streamlined construction processes by reducing on site labor and enhancing project timelines.

The mild rebar segment is likely to grow at a fastest CAGR of 3.2% from 2026 to 2034 with its specific applications in non-structural and decorative concrete works. The primary growth driver is the increasing demand for architectural concrete finishes and lightweight reinforcement in residential landscaping and interior design projects. The trend towards customized home features has increased the use of mild rebar for decorative elements such as garden walls, pathways, and ornamental structures where high tensile strength is not required. The mild rebar is preferred for these applications due to its ease of bending and shaping, allowing for intricate designs that deformed bars cannot easily achieve. The cost effectiveness of mild rebar also makes it an attractive option for small scale DIY projects and minor repairs, contributing to its steady demand in the retail sector. Furthermore, the restoration of historic structures often requires the use of plain bars to match original construction methods, supporting a specialized market segment. Manufacturers are responding to this demand by offering pre cut and pre bent mild rebar products that cater to the convenience needs of homeowners and small contractors.

By End Use Insights

The infrastructure segment held 45.3% of the United States rebar market share in 2025 with the extensive public investment in transportation and utility networks. The implementation of the Infrastructure Investment and Jobs Act, which allocates billions of dollars for the repair and expansion of roads, bridges, tunnels, and water systems is also boosting the growth of the segment. According to the study, the nation requires significant rehabilitation of its aging bridge inventory, with over 45,000 structures classified as structurally deficient, necessitating large volumes of rebar for reconstruction efforts. As per the American Society of Civil Engineers, the backlog in infrastructure maintenance creates a sustained demand for reinforcement steel that is less susceptible to economic cycles than private construction. The complexity of modern infrastructure projects, such as high speed rail systems and seismic retrofits, requires high grade deformed rebar that meets stringent safety standards. Government contracts often prioritize domestic steel production, ensuring a stable market for local manufacturers. The long duration of infrastructure projects also provides predictable demand patterns, allowing producers to plan capacity effectively.

The residential segment is the anticipated to grow at a fastest CAGR of 4.5% from 2026 to 2034 owing to the ongoing housing shortage and the shift towards single family home construction. The primary growth driver is the need for new housing units to accommodate population growth and household formation, particularly in suburban and exurban areas. According to the Census Bureau, housing starts reached 1.4 million units in 2025, with single family homes accounting for the majority of new construction activity. As per the National Association of Home Builders, the average size of new homes has increased, leading to larger foundations and structural elements that require more rebar. The trend towards basements and multi-story homes in regions with limited land availability further amplifies rebar consumption. Additionally, the renovation and expansion of existing homes, driven by remote work needs and lifestyle changes, contribute to steady demand for reinforcement materials. The use of insulated concrete forms in energy efficient home construction also boosts rebar usage, as these systems require dense reinforcement grids. Manufacturers are adapting to this growth by offering smaller diameter rebar packages tailored for residential contractors and DIY enthusiasts. The geographic shift in population towards the Sun Belt states, where concrete slab foundations are common, further supports regional growth in residential rebar consumption.

COMPETITIVE LANDSCAPE

The competition in the United States rebar market is characterized by a mix of large integrated producers and specialized regional fabricators vying for dominance in diverse construction segments. Intense rivalry exists due to the commoditized nature of standard reinforcement bars, prompting firms to differentiate through service quality, delivery speed, and technical support. Major players leverage economies of scale to offer competitive pricing while investing in advanced manufacturing technologies to improve product consistency and reduce lead times. The features moderate barriers to entry due to high capital requirements for milling equipment and stringent quality certifications, which protect established incumbents from new competitors. Price volatility in raw materials adds complexity to competitive dynamics, forcing companies to adopt sophisticated hedging strategies to maintain margins. Customer loyalty plays a crucial role as builders prioritize reliability and consistent supply over minor price differences. Innovation in sustainable production methods provides avenues for differentiation beyond traditional metrics.

KEY MARKET PLAYERS

Some of the promising companies that are playing a dominating role in the U.S. Rebar Market include

- Nucor Corporation

- Commercial Metals Company (CMC)

- Steel Dynamics, Inc.

- Gerdau S.A.

- EVRAZ North America

- ArcelorMittal

- Liberty Steel Group

- Celsa Group

- Outokumpu Oyj

- Schnitzer Steel Industries, Inc.

- Byer Steel Group, Inc.

- Cascade Steel Rolling Mills, Inc.

Top Players in the US Rebar Market

Nucor Corporation

Nucor Corporation stands as a leading force in the United States rebar market by leveraging its extensive network of electric arc furnace facilities to produce high quality reinforcement steel. The company focuses on sustainable manufacturing practices, utilizing recycled scrap metal to reduce environmental impact while maintaining cost efficiency. Recent investments in advanced rolling mills have enhanced its ability to produce specialized rebar grades required for large scale infrastructure projects. Nucor actively collaborates with fabricators to ensure timely delivery of materials, strengthening supply chain reliability for critical construction timelines. The firm’s commitment to innovation includes adopting digital technologies for quality control and production optimization.

Steel Dynamics Inc

Steel Dynamics Inc contributes significantly to the rebar sector through its integrated approach to steel production and fabrication services. The company operates state of the art facilities that produce a diverse range of reinforcement bars tailored for bridge, building, and industrial applications. Recent expansions in its Texas and Alabama plants have increased capacity for heavy structural sections, allowing it to meet growing demand from infrastructure projects. Steel Dynamics emphasizes rapid turnaround times and precise engineering support, which appeals to contractors managing tight schedules. The firm also invests in research and development to create high strength low alloy steels that offer superior performance in extreme conditions.

Gerdau S.A.

Gerdau S.A. maintains a strong presence in the United States rebar market by providing a comprehensive portfolio of long steel products including various grades of reinforcement bars. The company leverages its global expertise and local manufacturing capabilities to serve diverse sectors such as energy, transportation, and commercial construction. Recent initiatives include upgrading its micro mill technology to enhance production flexibility and reduce carbon emissions, aligning with sustainability goals of modern developers. Gerdau focuses on building long term relationships with distributors and fabricators to ensure seamless material flow to job sites. The firm also offers technical assistance and value added services that help clients optimize steel usage and reduce waste. Through strategic investments in automation and customer service infrastructure, Gerdau continues to deliver high quality structural solutions that meet the rigorous demands of the United States construction industry.

Top Strategies Used by Key Market Participants

Key players in the United States rebar market primarily employ vertical integration strategies to control production costs and ensure consistent material availability for clients. Companies invest heavily in technological advancements, such as automated rolling mills and digital quality control systems to enhance product precision and operational efficiency. Strategic expansion of manufacturing facilities in high growth regions allows firms to reduce logistics costs and improve delivery speeds for local projects. Participants also focus on sustainability initiatives by adopting electric arc furnace technologies and recycling programs to meet environmental regulations and appeal to green building standards. Long term partnerships with major construction firms and fabricators help secure stable demand and mitigate market volatility risks. Additionally, manufacturers prioritize product differentiation by developing high strength alloys and customized sections that address specific engineering challenges.

MARKET SEGMENTATION

This research report on the U.S. Rebar Market has been segmented based on the following categories.

By Type

- Mild

- Deformed

By End-Use

- Infrastructure

- Residential

- Commercial

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com