U.S. Residential Solar Market Size, Share, Trends & Growth Forecast Report By Technology, Type, Connectivity, and Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

Market Size, 2025

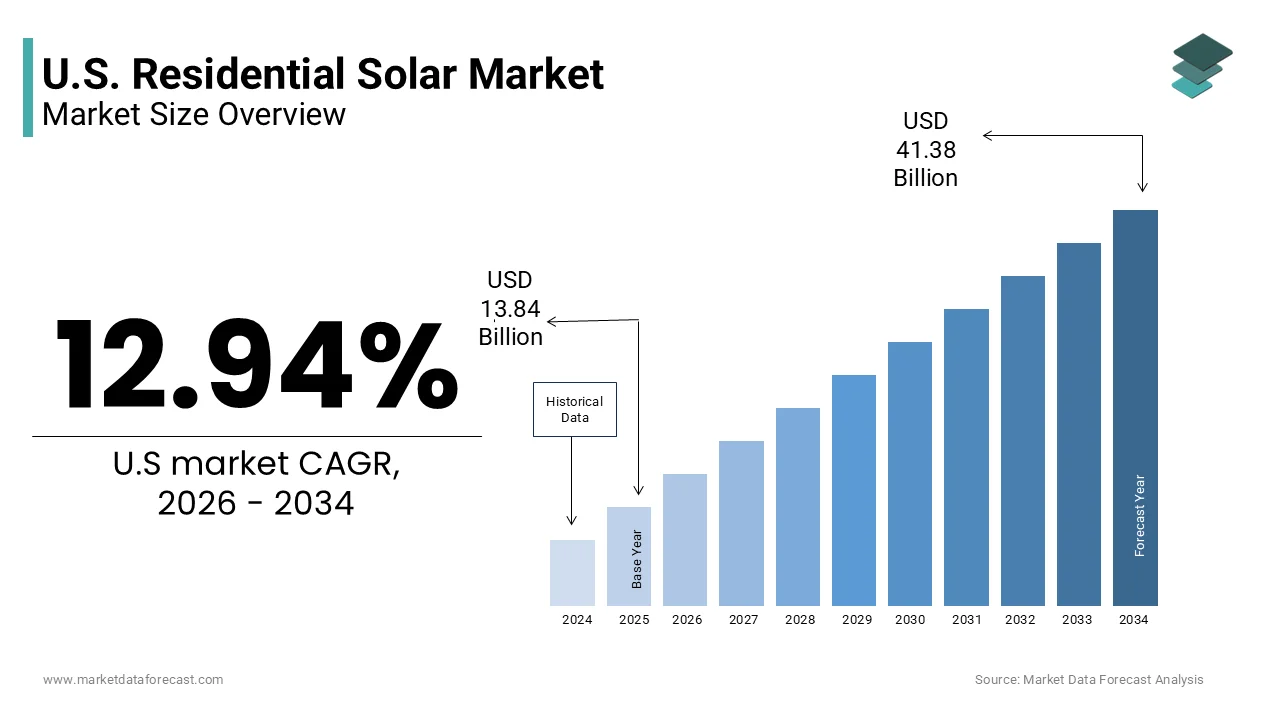

$13.84 BnMarket Estimate, 2026

$15.63 BnMarket Forecast, 2034

$41.38 BnCAGR, 2026–2034

12.94%U.S. Residential Solar Market Report Summary

The U.S. residential solar market was valued at USD 13.84 billion in 2025, is estimated to reach USD 15.63 billion in 2026, and is projected to reach USD 41.38 billion by 2034, growing at a CAGR of 12.94% during the forecast period. Market growth is driven by increasing adoption of renewable energy solutions, rising electricity costs, supportive government incentives, and growing consumer awareness regarding energy independence. Advancements in solar panel efficiency, battery storage technologies, and smart energy management systems are further accelerating residential solar installations across the United States.

Key Market Trends

- Increasing consumer demand for clean and renewable energy is driving market growth.

- Rising electricity prices are encouraging homeowners to adopt solar power systems.

- Growing integration of battery energy storage solutions is supporting market expansion.

- Expansion of federal and state level incentives is enhancing residential solar adoption.

- Innovation in solar panel efficiency and smart energy management technologies is influencing market development.

Regional Insights

- The United States accounted for 80.5% of the North American residential solar market share in 2025 and maintained its dominant regional position. Strong policy support, increasing residential solar installations, and growing investments in renewable energy infrastructure continue to support market growth.

Competitive Landscape

The U.S. residential solar market is highly competitive, with companies focusing on solar panel innovation, integrated energy storage solutions, financing programs, and installation services to strengthen their market position. Market participants continue investing in technology advancements and customer focused energy solutions. Key companies operating in the U.S. residential solar market include Canadian Solar Inc., Elevation Capital, Enphase Energy Inc., Freedom Forever LLC, Lumos Solar, Generac Power Systems Inc., Hanwha Q Cells America Inc., JinkoSolar Holding Co. Ltd., Mission Solar Energy, Momentum Solar, Palmetto Clean Technology Inc, Powur PBC, REC Solar Holdings AS, Silfab Solar Inc., Solar Optimum Inc., SolarEdge Technologies Inc., Sunnova Energy International, SunPower Corp., Sunrun Inc., and Tesla Inc..

U.S. Residential solar Market Size

The U.S. residential solar market size was valued at USD 13.84 billion in 2025, and is projected to reach USD 41.38 billion by 2034 from USD 15.63 billion in 2026, growing at a CAGR of 12.94%.

Residential solar refers to solar power systems installed on or around private homes to generate electricity for household use. These systems capture sunlight and convert it into usable energy to power lights, fans, and appliances, effectively lowering or eliminating your utility bills. This market represents a critical component of the national transition toward decentralized renewable energy infrastructure driven by technological advancements and policy incentives. The market is defined by the integration of solar panels inverters and increasingly battery storage systems that empower homeowners to reduce reliance on traditional utility grids. As per data from the US Energy Information Administration residential sector electricity consumption accounted for approximately 38 percent of total US electricity sales in 2023 highlighting the substantial potential for rooftop solar adoption . The proliferation of net metering policies and federal tax credits has further catalyzed consumer interest in energy independence. According to the Solar Energy Industries Association the number of US homes with solar installations surpassed 4 million in 2023 demonstrating significant penetration across diverse geographic regions . This growth is supported by declining hardware costs and improved financing options such as power purchase agreements and solar leases. The market dynamics are also influenced by state level mandates and renewable portfolio standards that encourage distributed generation. Homeowners are increasingly viewing solar assets as long term investments that enhance property value and provide protection against volatile utility rates. The definition of the market has expanded to include smart energy management solutions that optimize consumption and storage. As per market observations the average age of installed systems is decreasing due to rapid technological iteration. This evolving landscape reflects a shift from niche adoption to mainstream acceptance as solar energy becomes a standard feature in modern home construction and retrofitting projects.

MARKET DRIVERS

Federal Incentives and Policy Support Mechanisms

Federal incentives and policy support mechanisms are the primary driver propelling the United States residential solar market. They make solar energy much more affordable for homeowners by drastically lowering initial installation costs. The Inflation Reduction Act of 2022 originally extended a 30% tax credit for home solar energy systems through 2032. However, recent law changes ended the residential clean energy credit on December 31, 2025. The federal solar tax credit allows qualified taxpayers to subtract 30% of solar installation costs from what they owe in federal taxes, which directly cuts down the break-even payback period. This policy stability has created a favorable environment for consumer confidence and long term planning. Additionally many states offer complementary rebates and performance based incentives that further enhance the economic viability of residential solar. For instance programs in California New York and Massachusetts provide additional cash back or tax exemptions that stack with federal benefits. Studies show that regions with robust state-level incentives and favorable utility policies experience solar adoption rates up to five times higher than areas lacking local financial support. The clarity and longevity of these policies encourage manufacturers and installers to invest in capacity expansion and workforce training. Furthermore local governments are implementing property tax exemptions for solar additions ensuring that increased home values do not result in higher tax burdens. These layered financial supports make solar energy accessible to a broader demographic including middle income households. The consistent policy backdrop thus serves as a foundational pillar for sustained market growth and widespread adoption.

Rising Electricity Rates and Desire for Energy Independence

Persistent rise in electricity rates across the country coupled with a growing consumer desire for energy independence and resilience further boosts the growth of the United States residential solar market. Utility prices have increased significantly in recent years due to aging infrastructure fuel cost volatility and transmission upgrades. Data from the U.S. Energy Information Administration (EIA) shows that average residential electricity prices rose rapidly after 2022, climbing nearly 10 to 13 percent over multi-year margins and hitting historic highs in several states. This trend motivates homeowners to seek alternative energy sources that offer predictable and lower long term costs. Solar energy provides a hedge against fluctuating utility rates allowing consumers to lock in a fixed cost for electricity generation over the lifespan of the system. The concept of energy independence has gained traction particularly in regions prone to grid instability and extreme weather events. Homeowners are increasingly interested in pairing solar panels with battery storage to ensure power availability during outages. Surveys indicate that approximately 60% of potential solar buyers cite energy reliability and emergency backup power as core reasons for wanting a solar system. This shift in consumer mindset transforms solar from a purely economic choice to a security imperative. The ability to generate and store own electricity reduces dependence on centralized utilities and enhances household resilience. As per industry reports the demand for off grid capable systems is rising in rural and suburban areas where grid service is less reliable. This dual motivation of cost savings and energy security drives robust demand for residential solar solutions. The tangible benefits of reduced monthly bills and increased self sufficiency ensure that this driver remains potent and influential in shaping market dynamics.

MARKET RESTRAINTS

High Upfront Costs and Financing Barriers

The high upfront capital required for system installation, despite the availability of incentives, is a significant restraint impacting the United States residential solar market. The average cost of a residential solar panel system ranges from 15000 to 25000 dollars before tax credits which remains a substantial financial barrier for many households. Studies show that most homeowners do not purchase solar energy systems upfront with cash, choosing instead to use loans, leases, or third-party power purchase agreements (PPAs). These financing options often involve interest rates and fees that can erode the long term savings potential of solar energy. Credit constraints and strict lending criteria exclude lower income families from accessing affordable solar financing. The complexity of navigating various loan products and understanding terms such as annual percentage rates and lien positions confuses many potential buyers. Furthermore the appraisal process for homes with solar loans can be cumbersome affecting mortgage approvals and refinancing opportunities. Financial comparisons show that specialized solar loans often feature more flexible qualification parameters than traditional home equity loans, focusing primarily on credit scores and project-driven utility savings. This limits the pool of eligible candidates and slows down adoption rates among middle and lower income demographics. The lack of standardized financing products across different lenders also creates market fragmentation and inefficiency. Homeowners may face hidden costs such as roof repairs or electrical upgrades that are not covered by initial quotes leading to budget overruns. These financial hurdles deter risk averse consumers who prefer the certainty of fixed utility bills over the variable costs of ownership. Thus, the high initial investment and complex financing landscape act as a substantial brake on market expansion.

Interconnection Delays and Grid Capacity Constraints

The increasing prevalence of interconnection delays is also a major impediment to the United States residential solar market. These grid capacity constraints hinder the timely installation and activation of residential solar systems. As the number of solar installations grows many utility grids are reaching their capacity limits for accepting distributed energy resources. As per regulatory filings wait times for interconnection approval have doubled in some states extending from a few weeks to several months . Utilities are implementing stricter review processes and requiring additional equipment such as smart inverters to manage voltage fluctuations and ensure grid stability. These requirements add to the cost and complexity of installations causing project delays and customer frustration. In certain high penetration areas utilities have paused new interconnection applications entirely until grid upgrades are completed. This moratorium effectively halts market growth in specific regions regardless of consumer demand. The lack of uniform interconnection standards across different utility jurisdictions creates uncertainty for installers and homeowners. Research reveals that 40% of solar installers cite local permitting and regulatory delays as the single greatest challenge to keeping their project completion timelines on track. These delays increase soft costs such as labor and administrative expenses which are passed on to consumers. The uncertainty surrounding approval timelines also discourages potential adopters who seek immediate benefits from their investment. Furthermore the need for costly grid upgrades to accommodate higher solar penetration is often funded by ratepayers leading to political and regulatory pushback. This infrastructure bottleneck represents a critical structural restraint that requires coordinated investment and policy reform to resolve. Solar adoption is outpacing grid modernization. Until the grid catches up, these constraints will continue to impede market fluidity.

MARKET OPPORTUNITIES

Integration of Battery Storage and Smart Energy Management

The integration of battery storage systems and smart energy management technologies provides a prominent opportunity for the United States residential solar market. As battery costs decline and efficiency improves more homeowners are opting to add storage to their solar installations to maximize self consumption and provide backup power. Various sources show that the battery attachment rate for new solar installations has skyrocketed, reaching between 70% and 95% in primary solar markets like California and Hawaii. This trend is driven by the desire for energy resilience during power outages and the ability to store excess energy for use during peak pricing periods. Smart energy management systems allow homeowners to optimize energy usage by automatically shifting loads to times when solar production is highest or electricity rates are lowest. These technologies enhance the value proposition of solar by providing greater control and visibility over energy consumption. The integration of electric vehicle chargers with home solar and storage systems creates a holistic energy ecosystem that appeals to tech savvy consumers. As per studies, the combined market for solar and storage is expected to grow at a faster rate than solar alone due to these synergies. Manufacturers are developing user friendly apps that simplify monitoring and control making these systems accessible to non technical users. The potential for virtual power plants where aggregated home batteries support grid stability offers additional revenue streams for homeowners. This convergence of technologies positions residential solar as a central node in the future smart grid. By offering comprehensive energy solutions companies can differentiate themselves and capture higher value customers. This opportunity enables the market to evolve beyond simple generation into intelligent energy management.

Expansion into Underserved and Low Income Communities

The expansion of residential solar access into underserved and low-income communities through innovative business models and community solar programs offers a promising prospect for the growth of the United States residential solar market. Historically these demographics have been excluded from the solar boom due to credit barriers and rental housing status. Community solar allows multiple subscribers to share the benefits of a single off site solar array without installing panels on their own roofs. As per policy updates several states have expanded community solar legislation enabling renters and homeowners with unsuitable roofs to participate in renewable energy initiatives . This model lowers entry barriers by eliminating upfront costs and allowing subscribers to receive credits on their utility bills. Non profit organizations and government agencies are partnering with developers to create targeted programs that provide affordable solar access to low income households. These initiatives often include job training and local hiring components which stimulate economic development in disadvantaged areas. As per social impact studies expanding solar access can reduce energy burden which is disproportionately high for low income families who spend a larger share of their income on utilities. The federal government has allocated funds specifically for equitable clean energy deployment encouraging private sector participation. By tapping into this large untapped market segment companies can drive volume growth while fulfilling corporate social responsibility goals. The scalability of community solar projects allows for efficient deployment and management. This opportunity not only broadens the customer base but also fosters inclusive growth in the renewable energy sector. It aligns with broader societal goals of equity and environmental justice ensuring that the benefits of solar energy are shared widely.

MARKET CHALLENGES

Supply Chain Volatility and Trade Policy Uncertainty

Persistent volatility in the global supply chain and uncertainty surrounding trade policies are major hurdles for the United States residential solar market. The US solar industry relies heavily on imported components particularly polysilicon wafers and cells from Asia. Trade tariffs and import restrictions such as the Uyghur Forced Labor Prevention Act have disrupted supply flows and increased costs. The U.S. Department of Commerce's anti-circumvention investigation into solar imports from Southeast Asia (Cambodia, Malaysia, Thailand, and Vietnam) did freeze the market, prompting President Biden to issue a two-year moratorium on new tariffs in June 2022 to bridge the supply gap. While the moratorium temporarily shielded importers, the investigation itself caused months of severe supply chain delays and cancellation risks for developers. This unpredictability makes it difficult for companies to plan inventory and pricing strategies leading to project delays and cancellations. The concentration of manufacturing capacity in a few countries exposes the US market to geopolitical risks and logistical bottlenecks. Shipping delays and port congestion further exacerbate supply shortages causing installation timelines to extend. The lack of domestic manufacturing scale means that the US cannot quickly pivot to local sources when international supplies are constrained. While efforts to build domestic capacity are underway they will take years to reach meaningful scale. In the interim homeowners face higher prices and limited availability of preferred equipment. The complexity of complying with varying trade regulations adds administrative burdens and legal risks for businesses. This challenge underscores the vulnerability of the residential solar market to external global factors. Companies must navigate this complex landscape by diversifying suppliers and maintaining flexible procurement strategies. Until domestic production ramps up supply chain instability will remain a critical hurdle.

Labor Shortages and Workforce Development Gaps

The acute shortage of skilled labor is a significant limitation to the United States residential solar market. These workforce development gaps constrain the market's ability to meet growing demand. The rapid expansion of the residential solar market has outpaced the supply of qualified installers electricians and sales professionals. This shortage leads to increased labor costs and longer wait times for customers seeking installations. Many existing workers lack specialized training in newer technologies such as battery storage and smart inverters limiting the quality and efficiency of installations. The transient nature of construction work and competition from other trades such as HVAC and general electrical work further complicate recruitment and retention. Training programs and apprenticeships are often insufficient in scale and scope to address the widening gap. This labor constraint limits the capacity of installers to take on new projects and expand into new markets. The lack of standardized certification and licensing requirements across states adds to the complexity of workforce mobility. Companies must invest heavily in internal training and recruitment efforts which increases operational expenses. The shortage also impacts safety standards as inexperienced workers may be deployed to meet deadlines. Addressing this challenge requires coordinated efforts between industry associations educational institutions and policymakers to create robust pipeline programs. The residential solar market faces strong consumer demand. However, it risks stagnation without a sufficiently skilled workforce.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 12.94% |

| Segments Covered | By Technology, Type, Connectivity, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Canadian Solar Inc., Elevation Capital, Enphase Energy Inc., Freedom Forever LLC, Lumos Solar, Generac Power Systems Inc., Hanwha Q Cells America Inc., JinkoSolar Holding Co. Ltd., Mission Solar Energy, Momentum Solar, Palmetto Clean Technology Inc., Powur PBC, REC Solar Holdings AS, Silfab Solar Inc., Solar Optimum Inc., SolarEdge Technologies Inc., Sunnova Energy International, SunPower Corp., Sunrun Inc., and Tesla Inc. |

COUNTRY LEVEL ANALYSIS

The United States outperformed other countries in the North American residential solar market and accounted for an 80.5% share in 2025. This growth of the US market was driven by its favorable policy environment and large consumer base . The country serves as the primary engine for solar growth in the region driven by a combination of federal incentives state level mandates and declining technology costs. The market is characterized by a diverse landscape of installation models including third party ownership direct sales and community solar programs which cater to varying consumer preferences. The presence of a robust manufacturing and supply chain ecosystem although still reliant on imports supports the scalability of residential projects. State level policies such as net metering and renewable portfolio standards play a crucial role in shaping market dynamics with states like California Texas and Florida leading in total installations. The decentralized nature of the US electricity grid encourages distributed generation making residential solar a key component of energy strategy. As per energy forecasts the residential sector is expected to contribute significantly to national renewable energy targets in the coming decades. The strong cultural emphasis on home ownership and property improvement further drives adoption as homeowners view solar as a valuable investment. The United States thus remains the central hub for residential solar innovation and deployment in North America setting trends that influence neighboring markets. The ongoing evolution of policy and technology ensures that the country maintains its leadership position in the global solar landscape.

COMPETITIVE LANDSCAPE

The competition in the United States residential solar market is intense and fragmented characterized by a mix of national integrators regional installers and local contractors. National players leverage economies of scale branding and financing capabilities to capture significant volume while local installers compete on personalized service and community trust. The market sees aggressive pricing strategies as companies vie for customer acquisition in saturated regions like California and Arizona. Differentiation increasingly relies on technology integration such as battery storage and smart home connectivity rather than just panel efficiency. High customer acquisition costs remain a critical challenge prompting firms to invest heavily in digital marketing and referral programs. Regulatory variability across states creates uneven playing fields requiring companies to adapt strategies locally. Supply chain constraints and labor shortages further intensify competition for resources and skilled workers. Consolidation trends are emerging as larger firms acquire smaller installers to expand footprint and eliminate rivals. Consumer awareness and education play pivotal roles as buyers compare complex financing options and long term value propositions. Reputation and review scores significantly influence purchasing decisions making customer satisfaction a key competitive metric. The entry of tech giants and utility backed programs adds another layer of complexity disrupting traditional business models. Overall the market demands continuous innovation in service delivery product offerings and operational efficiency to maintain competitive advantage. Success depends on balancing cost effectiveness with high quality customer experiences and reliable long term performance.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. residential solar market are

- Canadian Solar Inc.

- Elevation Capital

- Enphase Energy Inc.

- Freedom Forever LLC

- Lumos Solar

- Generac Power Systems Inc.

- Hanwha Q Cells America Inc.

- JinkoSolar Holding Co. Ltd.

- Mission Solar Energy

- Momentum Solar

- Palmetto Clean Technology Inc

- Powur PBC

- REC Solar Holdings AS

- Silfab Solar Inc.

- Solar Optimum Inc.

- SolarEdge Technologies Inc.

- Sunnova Energy International

- SunPower Corp.

- Sunrun Inc.

- Tesla Inc.

Top Players in the Market

- Sunrun Inc stands as a pioneering force in the United States residential solar market specializing in distributed energy services and battery storage solutions. The company operates primarily through a direct to consumer model offering solar leases power purchase agreements and cash sales to homeowners. Recent strategic initiatives focus heavily on integrating home battery systems with solar installations to enhance grid resilience and energy independence for customers. Sunrun has expanded its virtual power plant programs allowing aggregated home batteries to support grid stability during peak demand periods. The company actively partners with utilities and technology providers to streamline interconnection processes and improve customer experience. By emphasizing long term service contracts and maintenance Sunrun ensures consistent revenue streams while building brand loyalty. Its robust financing platform enables accessible solar adoption for diverse income groups. Sunrun continues to invest in digital tools that simplify energy management for users. These efforts solidify its reputation as a comprehensive energy service provider rather than just an equipment installer. The company remains committed to accelerating the transition to clean energy through innovative business models and customer centric solutions.

- Tesla Inc significantly influences the United States residential solar market through its integrated approach combining solar roof tiles photovoltaic panels and Powerwall battery storage systems. The company leverages its strong brand recognition and technological expertise to offer sleek aesthetically pleasing energy solutions that appeal to modern homeowners. Tesla recently streamlined its installation process by utilizing proprietary software and standardized hardware components to reduce deployment time and costs. The integration of solar products with its electric vehicle ecosystem creates a compelling value proposition for consumers seeking holistic energy independence. Tesla actively promotes its solar roof as a premium alternative to traditional roofing materials enhancing curb appeal while generating electricity. The company utilizes its extensive supercharger network and retail presence to market residential energy products effectively. Tesla continues to innovate in battery chemistry and energy density improving the performance and longevity of its storage solutions. By controlling the entire value chain from manufacturing to installation Tesla maintains high quality standards and competitive pricing. This vertical integration allows for rapid iteration and improvement of products. Tesla remains a key driver of consumer interest in residential renewable energy through its disruptive marketing and technological advancements.

- SunPower Corporation contributes to the United States residential solar market by focusing on high efficiency solar panels and premium installation services for residential customers. The company distinguishes itself through superior panel technology that generates more electricity per square foot making it ideal for homes with limited roof space. SunPower recently shifted its business model to a dealer network structure allowing local installers to leverage its brand and technology while maintaining operational flexibility. This strategy expands its geographic reach and enhances customer service quality through localized support. The company emphasizes durability and long term performance offering industry leading warranties that build consumer trust. SunPower actively integrates smart home energy management systems enabling users to monitor and optimize their energy consumption in real time. The firm collaborates with home builders to incorporate solar solutions into new construction projects ensuring seamless integration. SunPower prioritizes sustainability in its manufacturing processes appealing to environmentally conscious consumers. By focusing on premium segments and technological excellence SunPower maintains a strong competitive position. The company continues to invest in research and development to enhance panel efficiency and reduce degradation rates. This commitment to quality and innovation sustains its relevance in the evolving residential solar landscape.

Top Strategies Used by Key Market Participants

Key players in the United States residential solar market primarily employ vertical integration and technological innovation to enhance competitiveness and customer value. Companies increasingly bundle solar panels with battery storage systems to offer comprehensive energy independence solutions that appeal to resilience focused consumers. Strategic partnerships with utilities enable the creation of virtual power plants which provide additional revenue streams and grid support services. Dealership and installer network expansions allow firms to scale operations rapidly while maintaining localized customer service quality. Digital transformation initiatives streamline sales permitting and installation processes reducing soft costs and improving turnaround times. Financing innovations such as low interest loans and flexible lease terms lower entry barriers for middle income households. Brand differentiation through aesthetic design and high efficiency modules attracts premium segment buyers willing to pay for quality. Regulatory advocacy efforts ensure favorable policy environments including net metering and tax credit extensions. Customer retention strategies involve long term maintenance contracts and monitoring services that foster loyalty. Supply chain diversification mitigates risks associated with trade policies and material shortages. These multifaceted strategies enable participants to navigate market complexities and sustain growth amidst evolving consumer preferences and regulatory landscapes.

MARKET SEGMENTATION

This research report on the U.S. residential solar market is segmented and sub-segmented into the following categories.

By Technology

- Crystalline silicon

- Thin-film

By Type

- Rooftop solar systems

- Ground-mounted solar systems

By Connectivity

- On-grid solar systems

- Off-grid solar systems

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

1. What is the U.S. residential solar market?

The U.S. residential solar market consists of solar energy systems installed on homes to generate electricity and reduce dependence on traditional utility power.

2. What is driving the growth of the U.S. residential solar market?

Growth is driven by rising electricity costs, government incentives, increasing environmental awareness, and advancements in solar technology.

3. How do residential solar panels work?

Solar panels capture sunlight and convert it into electricity through photovoltaic cells, providing power for household energy needs.

4. What are the benefits of installing residential solar systems?

Key benefits include lower electricity bills, reduced carbon emissions, increased energy independence, and potential increases in property value.

5. Are government incentives available for residential solar installations?

Yes. Federal tax credits and various state level incentive programs help reduce the upfront cost of residential solar systems.

6. How long do residential solar panels typically last?

Most residential solar panels have a lifespan of 25 to 30 years and continue producing electricity efficiently with proper maintenance.

7. What role do battery storage systems play in residential solar energy?

Battery storage systems allow homeowners to store excess solar energy for use during nighttime, power outages, or periods of high electricity demand.

8. What opportunities exist in the U.S. residential solar market?

Opportunities include growth in battery storage, smart home integration, community solar programs, energy management solutions, and increased adoption of renewable energy technologies.

9. How is technology influencing the residential solar market?

Technological advancements are improving panel efficiency, battery performance, system monitoring, and overall energy management capabilities.

10. What challenges does the U.S. residential solar market face?

Challenges include high initial installation costs, permitting requirements, grid integration issues, and changing regulatory policies.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com