U.S. Reusable Launch Vehicle Market Size, Share, Trends & Growth Forecast Report By Type, By Orbit Type, By Vehicle Capacity, and By Country (California, Texas, Florida, Virginia & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

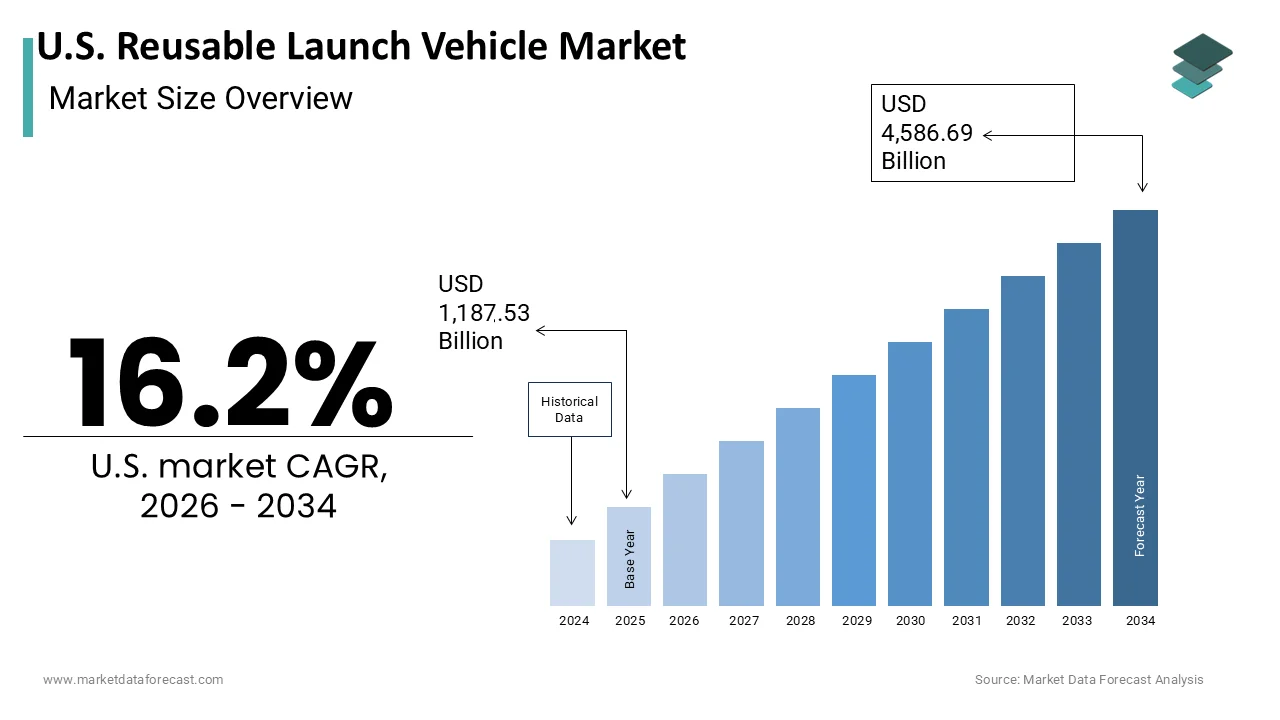

Market Size, 2025

$1.19 BnMarket Estimate, 2026

$1.38 BnMarket Forecast, 2034

$4.59 BnCAGR, 2026–2034

16.2%U.S. Reusable Launch Vehicle Market Size

The U.S. Reusable Launch Vehicle Market is projected to grow from USD 1,187.53 million in 2025 to USD 1,379.91 million in 2026 and reach USD 4,586.69 million by 2034, registering a CAGR of 16.2% during the forecast period from 2026 to 2034.

A Reusable Launch Vehicle (RLV) is a space vehicle designed to recover and reuse its components (like rocket stages or winged re-entry bodies) after launch, rather than discarding them. This paradigm shift from expendable architectures aims to drastically reduce the cost per kilogram to low Earth orbit by amortizing manufacturing expenses across multiple missions. The sector is pivotal to the national space strategy, enabling frequent and affordable access to space for commercial satellite deployment,t scientific exploration, and national security payloads. According to commercial spaceflight logs tracked alongside the Federal Aviation Administration (FAA), the United States conducted 116 orbital launch attempts in 2023, with a substantial majority utilizing partially reusable rocket systems like the Falcon 9. This high launch cadence underscores the operational maturity of current reusable platforms. According to the National Aeronautics and Space Administration, the Artemis program relies heavily on reusable technologies such as the SpaceX Starship to sustain long-term lunar presence and eventual Mars missions. The integration of advanced materials like carbon composites and thermal protection systems allows these vehicles to withstand the extreme heat of atmospheric reentry. Tracking data from registries like the Union of Concerned Scientists Satellite Database reflects that the overwhelming majority of active payloads in low-Earth orbit are deployed by partially reusable launch systems, highlighting a structural shift in global space access. This dominance shows the market's transition away from legacy expendable models. The regulatory framework managed by the Office of Commercial Space Transportation continues to evolve to support rapid innovation while ensuring public safety and environmental compliance.

MARKET DRIVERS

Significant Reduction in Launch Costs Through Amortization

A significant reduction in launch costs through amortization fuels the growth of the United States reusable launch vehicle market. Traditional expendable launch systems require the construction of a new rocket for every mission, resulting in prohibitive costs that limit access to space. Reusable architectures allow operators to fly the same hardware multiple times, spreading the initial manufacturing investment over numerous payloads. Aerospace industry economic analyses show that the introduction of reusable booster technology has driven commercial launch costs to low Earth orbit down from historic expendable baselines to under $2,700 per kilogram on the Falcon 9 platform. This economic efficiency enables smaller commercial entities and research institutions to afford space access. As per the Center for Strategic and International Studies, the marginal cost of a reused booster is significantly lower than building a new one, primarily involving inspection and refueling expenses. The ability to offer competitive pricing has allowed US providers to capture a dominant share of the global commercial launch market. Government agencies also benefit from these savings,s allowing them to allocate budgets to payload development rather than transportation. The financial viability of large constellation deployments such as Starlink depends entirely on the low-cost structure provided by reusability. This economic model drives continuous investment in recovery and refurbishment technologies. The proven track record of cost savings ensures that new entrants prioritize reusability in their design philosophies. Therefore, the market sees sustained growth as more customers seek affordable and frequent launch opportunities.

Increased Launch Cadence and Operational Frequency

Increased launch cadence and operational frequency significantly propel the expansion of the United States reusable launch vehicle market. This demonstrates reliability and responsiveness. Reusable systems are designed for rapid turnaround times, allowing for a higher number of launches per year compared to expendable counterparts. According to the Federal Aviation Administration, in the United States, a record-breaking launch rate was achieved in 2023 with an average of nearly one launch every three days, largely driven by reusable fleets. This high tempo is essential for deploying and maintaining large satellite constellations that require regular replenishment and upgrades. The ability to launch on demand enhances national security capabilities by providing responsive access to space for critical defense payloads. Commercial customers value the predictability and schedule certainty offered by established reusable providers. The accumulation of flight data from repeated missions improves safety margins and operational efficiency over time. High launch frequency also fosters a robust ecosystem of ground support services and supply chain partners. This operational rhythm creates a barrier to entry for competitors who cannot match the pace. The demonstrated reliability of frequent flights builds customer confidence and encourages long-term contracting. Thus, the capacity for high cadence operations remains a key driver of market expansion.

MARKET RESTRAINTS

Complex Refurbishment Processes and Maintenance Costs

Complex refurbishment processes and maintenance costs greatly limit the profitability and scalability of the United States reusable launch vehicle market. While reusability reduces manufacturing costs, it introduces substantial expenses related to inspection, repair,r and recertification of flown hardware. Each returning stage undergoes rigorous testing to identify fatigue cracks, KS thermal damage, and component wear, which can be time-consuming and expensive. As per the Government Accountability Office, unexpected maintenance issues can delay launch schedules and increase operational overhead,s affecting customer satisfaction. The need for specialized facilities and skilled technicians further adds to the logistical burden. Thermal protection systems often require extensive replacement or repair after each reentry due to extreme heat exposure. The complexity of integrating new components with aged structures poses engineering challenges that must be carefully managed. These maintenance requirements can erode the cost advantages of reusability if not optimized effectively. Smaller launch providers may struggle to bear these upfront infrastructure costs, limiting their ability to compete. The unpredictability of refurbishment timelines creates scheduling uncertainties that can deter risk-averse customers. Until automated inspection and repair technologies mature, the high labor and material costs associated with refurbishment will remain a significant constraint. This operational complexity necessitates continuous innovation to streamline processes and reduce downtime.

Regulatory Hurdles and Environmental Compliance Requirements

Regulatory hurdles and environmental compliance requirements are significant constraints to the rapid expansion of the United States reusable launch vehicle market. The Federal Aviation Administration and other agencies enforce strict safety and environmental standards that govern launch operations and reentry procedures. Obtaining licenses for new reusable vehicles involves lengthy review processes that can delay deployment and increase development costs. According to the Office of Commercial Space Transportation, the licensing timeline for novel launch systems can extend beyond 12 months due to comprehensive safety assessments. The deposition of black carbon and alumina particles in the upper atmosphere from frequent rocket burns is subject to growing scientific scrutiny and potential regulation. Noise pollution and sonic booms from returning boosters also face local community opposition, leading to restrictions on landing zones. Compliance with these evolving regulations requires significant legal and technical resources from launch providers. The lack of standardized international norms for reusable spaceflight complicates cross-border order operations and partnerships. Uncertainty regarding future environmental laws creates investment risks for manufacturers planning long-term fleets. The balance between fostering innovation and ensuring public safety remains a delicate regulatory challenge. These bureaucratic and environmental constraints can slow the pace of technological adoption and market growth. Providers must navigate this complex landscape to maintain operational continuity and public license to operate.

MARKET OPPORTUNITIES

Expansion of Satellite Constellations and Broadband Services

Expansion of satellite constellations and broadband services offers a substantial opportunity for the United States reusable launch vehicle market. This creates sustained demand for frequent and reliable launches. Companies like SpaceX Amazon, and OneWeb are deploying thousands of satellites to provide global internet coverag,e requiring regular replenishment and upgrades. Comprehensive database tracking shows that there are over 10,000 active satellites currently in orbit, with the overwhelming majority deployed in Low Earth Orbit (LEO) telecommunications mega-constellations. This massive deployment cycle ensures a steady stream of launch contracts for reusable providers. As per the Federal Communications Commission, the approval of new spectrum allocations for broadband services encourages further investment in satellite infrastructure. Reusable rockets offer the necessary cost efficiency and launch frequency to support these ambitious projects. The ability to launch multiple satellites per mission maximizes payload utilization and reduces per-unit costs. The growing demand for connectivity in remote areas and maritime environments drives the expansion of these networks. Manufacturers are developing dedicated rideshare programs to accommodate smaller payloads alongside major constellation deployments. This diversification of revenue streams enhances market stability. The synergy between satellite manufacturing and launch services creates a vertically integrated ecosystem that benefits from economies of scale. As constellation sizes grow, the reliance on reusable launch vehicles will intensify. This trend provides a robust foundation for long-term market growth and innovation in launch technologies.

Development of Heavy Lift and Fully Reusable Systems

Development of the heavy lift and fully reusable systems provides a promising prospect for the United States reusable launch vehicle market. This enables ambitious deep space missions and large-scale infrastructure projects. Next-generation vehicles such as the SpaceX Starship are designed to be fully reusable and capable of carrying over 100 metric tons to low Earth orbit. According to the National Aeronautics and Space Administration, these capabilities are essential for the Artemis program,m which aims to establish a sustainable human presence on the Moon. As per the Department of Defense,se heavy lift vehicles provide the capacity to launch large national security payloads, space-based sensors, in a single mission. The economic potential of fully reusable systems lies in their ability to achieve airline-like operational efficiency with minimal turnaround time. The use of methane fuel and stainless steel construction reduces material costs and simplifies manufacturing. These vehicles can also support point-to-point Earth transportation, reducing travel time between distant locations. The technology developed for these systems has broader applications in aerospace and materials science. Investment in heavy lift capabilities attracts government funding and private capital, all driving technological advancement. The ability to deploy large space stations and industrial facilities opens new commercial frontiers. This strategic focus on heavy lift and full reusability positions the United States at the forefront of the next space age.

MARKET CHALLENGES

Technical Risks Associated with Reentry and Landing

Technical risks associated with re-entry and landing are severe challenges to the reliability and safety of the United States reusable launch vehicle market. The process of returning a rocket stage from orbital velocities involves extreme thermal and mechanical stresses that can lead to catastrophic failure. The complexity of controlling a large vehicle through supersonic speeds and landing precisely on a drone ship or pad requires sophisticated software and hardware integration. Any malfunction in the grid fins, engines, or landing legs can compromise the mission. The high-energy environment of reentry limits the margin for error in material performance. Developing robust systems that can withstand repeated cycles of stress without degradation is an ongoing engineering challenge. The potential for debris from failed landings to endanger populated areas or shipping lanes adds to the operational risk. Insurance costs for reusable launches remain high due to these inherent uncertainties. Continuous testing and iterative design improvements are necessary to mitigate these risks. The market must balance the drive for rapid innovation with the need for proven reliability. Ensuring consistent, safe landings is critical for maintaining customer trust and regulatory approval.

Supply Chain Constraints and Material Availability

Supply chain constraints and material availability are significant obstacles to the production and scaling of these vehicles, which negatively impact the expansion of the United States reusable launch vehicle market. The manufacturing of advanced rockets requires specialized materials such as carbon fiber composites, high-strength aluminum, lithium alloys, and heat-resistant ceramics. According to the Aerospace Industries Association, disruptions in the global supply chain have led to delays in the delivery of critical components. As per the Bureau of Labor Statistics,s the shortage of skilled workers in aerospace manufacturing further exacerbates production bottlenecks. The reliance on single-source suppliers for certain proprietary technologies increases vulnerability to disruptions. Geopolitical tensions and trade restrictions can limit access to rare earth elements and other essential raw materials. The rapid scaling of production to meet high launch cadences strains existing manufacturing capacities. Quality control issues arising from rushed production can lead to defects and increased scrap rates. The cost of raw materials has also fluctuated due to inflation and energy price hikes, affecting overall project budgets. Establishing resilient and diversified supply chains is a complex and costly endeavor. Manufacturers must invest in vertical integration or long-term contracts to secure material flows. The inability to consistently source high-quality materials can delay launch schedules and increase costs. Addressing these supply chain vulnerabilities is crucial for sustaining market growth and competitiveness.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Orbit Type, Vehicle Capacity, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Texas, Florida, New York, and the rest of the United States |

| Market Leaders Profiled | SpaceX, Blue Origin, Rocket Lab USA, Inc., Northrop Grumman Corporation, Lockheed Martin Corporation, Boeing Company, Sierra Space Corporation, Relativity Space, Inc., Firefly Aerospace, Inc., Astra Space, Inc., Virgin Galactic Holdings, Inc., Dynetics, Inc. |

SEGMENTAL ANALYSIS

By Type Insights

The partially reusable launch vehicles segment held the majority share of the United States reusable launch vehicle market in 2025. Proven operational reliability and flight heritage drive the domination of partially reusable launch vehicles. This segment includes systems where only the first stage booster is recovered and reused while the upper stage remains expendable. The operational maturity and proven reliability of these systems drive their widespread adoption across commercial and government sectors. Systems such as the Falcon 9 have demonstrated consistent success over hundreds of missions, establishing a track record that builds customer confidence. This extensive flight history reduces perceived risk for satellite operators who require guaranteed delivery of their payloads. Insurance premiums for missions on proven partially reusable rockets are lower compared to new unproven fully reusable designs. The established infrastructure for handling and refurbishing these boosters further supports their dominance. Government agencies like NASA and the Department of Defense prefer these vehicles for critical national security and scientific missions due to their reliability. The accumulation of data from repeated flights allows for continuous improvement in maintenance and operations. This robust ecosystem ensures that partially reusable vehicles remain the backbone of the US launch industry. The trust earned through consistent performance sustains their leading market position.

In addition, cost efficiency through booster refurbishment significantly contributes to the leading status of partially reusable launch vehicles in the United States market. Recovering and reusing the most expensive component of the rocket, the first stage booster, allows providers to offer competitive pricing. This economic advantage makes space access affordable for a broader range of commercial entities, es including small satellite developers and research institutions. The streamlined refurbishment process, ess which involves inspection and minor repairs rather than complete reconstruction, minimizes turnaround time and labor costs. Launch providers can pass these savings to customers, securing long-term contracts and high launch volumes. The financial model of partial reusability has been validated by the profitability of major launch providers. This cost structure creates a barrier to entry for competitors using expendable systems. The ability to offer frequent and affordable launches drives the deployment of large satellite constellations. Consequently, the economic benefits of booster reuse ensure the continued dominance of this segment in the market.

However, the fully reusable launch vehicles segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 28.5% from 2026 to 2034. Potential for airline-like operational efficiency drives the rapid growth of these vehicles. This segment covers systems where both the first and second stages are recovered and reused, aiming for airline-like operational efficiency. Although currently in development and early testing phases, this segment represents the future of space transportation. These systems aim to eliminate the need for extensive refurbishment between flights,s enabling rapid turnaround and high launch frequency. The capability promises to reduce launch costs by an order of magnitude, making space access vastly more affordable. Also, the ability to launch daily or even hourly opens up new markets such as point-to-point Earth transportation and large-scale space infrastructure construction. The elimination of hardware loss per mission maximizes asset utilization and return on investment. Investors and government agencies are heavily funding these developments due to their transformative potential. The prospect of routine and cheap space travel attracts commercial interest in space tourism and manufacturing. This operational paradigm shift drives intense innovation and competition in the sector. As technology matures, fully reusable vehicles are expected to capture a significant share of the market. The promise of unprecedented efficiency fuels the rapid growth of this segment.

Moreover, the enablement of deep space exploration and heavy lift missions accelerates the adoption of fully reusable launch vehicles in the United States market. These vehicles are designed with large payload capacities and in-orbit refueling capabilities essential for missions to the Moon, Mars,s and beyond. The ability to refuel in orbit allows these vehicles to carry heavier payloads further into the solar system than traditional rockets. This strategic capability enhances national security and scientific exploration potential. The versatility of these systems supports a wide range of missions from satellite deployment to interplanetary travel. Government funding and partnerships drive the development of these advanced capabilities. The potential to establish a sustainable presence on other celestial bodies motivates significant investment. The technological advancements required for full reusability also benefit other aerospace applications. This strategic importance ensures sustained growth and development in the segment. The alignment with national space goals positions fully reusable vehicles as a key driver of future space activities.

By Orbit Type Insights

The Low Earth Orbit segment led the United States reusable launch vehicle market and captured a significant share in 2025. Deployment of large satellite constellations fuels the domination of this segment. This orbit ranges from 160 to 2000 kilometers above the Earth and is preferred for satellite constellations, earth observation,n and human spaceflight. The high demand for LEO deployments drives the dominance of this segment. Companies like SpaceX, Amazon, and OneWeb are launching thousands of satellites to provide global broadband internet coverage. The massive deployment requires frequent and affordable launch services, which reusable vehicles provide. Reusable rockets enable the rapid replenishment and expansion of these networks at a fraction of the cost of expendable systems. The ability to launch multiple satellites per mission maximizes efficiency and reduces per-unit costs. The growing demand for connectivity in remote areas and maritime environments sustains this trend. The infrastructure for LEO operations is well established, supporting high launch cadences. The economic viability of these constellations depends entirely on low-cost access to LEO. This dependency ensures that LEO remains the primary destination for reusable launch vehicles. The continuous expansion of these networks drives sustained market growth. The scale of these projects solidifies the leading position of the LEO segment.

In addition, human spaceflight and International Space Station missions significantly contribute to the leading status of Low Earth Orbit in the United States reusable launch vehicle market. NASA and private companies regularly conduct crewed and cargo missions to the ISS, which resides in LEO. These missions require high reliability and safety standards, which partially reusable systems have demonstrated. The consistency of launch schedules ensures the continuous presence and operation of the station. The success of commercial crew programs has increased the frequency of human spaceflight activities. Tourism flights to LEO are also emerging as a new market segment driven by reusable technologies. The established infrastructure for human spaceflight in LEO supports these operations. The strategic importance of maintaining a human presence in space drives ongoing investment. This consistent demand for crew and cargo transport sustains the dominance of the LEO segment. The reliability of reusable vehicles is critical for these high-stakes missions.

But the Geosynchronous Transfer Orbit (GTO) segment is expected to exhibit a noteworthy CAGR of 12.5% over the forecast period, owing to demand for high-capacity communication satellites. This orbit is used for communication,s weather, and navigation satellites that require a fixed position relative to the Earth. Advances in reusable vehicle performance are enabling more efficient GTO missions. These satellites provide broadband broadcasting and military communications services requiring precise placement in geostationary orbit. Reusable launch vehicles are now capable of delivering these heavy payloads to GTO efficiently. The ability to launch larger satellites reduces the number of missions required to build out communication networks. Government and commercial operators rely on these satellites for secure and reliable connectivity. The economic benefits of reusability make GTO launches more affordable,e encouraging new deployments. The strategic value of GEO satellites for national security and commerce drives investment. The improved payload capacity of reusable vehicles supports the next generation of large communication platforms. This trend ensures steady growth in the GTO segment. The critical role of these satellites in global infrastructure sustains demand. The advancement of reusable technology expands access to this valuable orbit.

Furthermore, the enhanced payload capacity of reusable upper stages accelerates the adoption of Geosynchronous Transfer Orbit in the United States market. Innovations in engine design and fuel efficiency allow reusable rockets to deliver heavier payloads to higher orbits. These advancements make it feasible to launch multiple large satellites or single very heavy payloads to GTO. The ability to perform direct to GEO injections reduces satellite fuel requirements and extends operational life. This efficiency gain makes reusable launches attractive for high-value GTO missions. The competition among providers to offer superior GTO performance drives technological innovation. The growing size and complexity of communication satellites require these enhanced capabilities. The strategic advantage of placing large assets in GEO supports national and commercial interests. This technological progress drives the rapid growth of the GTO segment. The ability to efficiently access high orbits expands the utility of reusable launch vehicles.

By Vehicle Capacity Insights

The above 3000 Kg capacity segment was the largest by occupying a substantial share of the United States reusable launch vehicle market in 2025. Launch of large satellite constellations and heavy payloads supports the prominence of this segment. This segment includes medium to heavy-lift vehicles capable of carrying large satellites and multiple payloads. Modern communication and earth observation satellites are becoming larger and more complex, requiring significant lift capacity. The ability to consolidate multiple payloads into a single launch reduces costs and simplifies logistics. Government agencies also use these vehicles for launching large national security and scientific instruments. The economic efficiency of heavy lift reusable rockets makes them the preferred choice for bulk deployments. The growing size of satellite buses and propulsion systems further increases demand for high-capacity launchers. This trend ensures that the above 3000 kg segment remains the largest by mass. The scalability of these vehicles supports the expanding space economy. The capacity to deliver substantial mass reliably sustains market leadership.

Moreover, cost-effectiveness for bulk deployments significantly contributes to the leading status of the Above 3000 Kg capacity segment in the United States market. Reusable heavy lift vehicles offer the lowest cost per kilogram to orbit, making them ideal for launching large masses. This financial advantage encourages satellite operators to bundle their launches or design larger satellites. The ability to amortize launch costs over a larger payload mass improves return on investment. Commercial constellations rely on this cost structure to achieve profitability. The affordability of heavy lift launches enables new business models and services. The competitive pricing of these vehicles drives high launch volumes. The efficiency of bulk deployments supports the rapid expansion of space infrastructure. This economic benefit ensures the continued dominance of the high-capacity segment. The value proposition of low cost per kilogram sustains market preference.

On the contrary, the 1000 Kg to 3000 Kg capacity segment is predicted to witness the highest CAGR of 15.25 between 2026 and 2034. Increasing demand for dedicated mid-sized launches fuels this growth. This segment covers medium lift vehicles suitable for single large satellites or small rideshare missions. Satellite operators increasingly prefer dedicated launches to control timing and orbit placement rather than relying on rideshares. Reusable vehicles offering this capacity provide a flexible and cost-effective solution. Government and commercial users value the autonomy and flexibility of dedicated missions. The development of new reusable medium lift vehicles supports this trend. The growing complexity of satellite missions requires precise insertion, which dedicated launches provide. This preference for control and customization drives segment growth. The availability of reliable mid-sized reusable options expands market opportunities. The balance between cost and capability makes this segment attractive. The increasing number of mid-sized satellite projects sustains growth.

In addition, expansion of rideshare opportunities for medium payloads accelerates the adoption of the 1000 Kg to 3000 Kg capacity segment in the United States market. Reusable vehicles can accommodate multiple medium-sized payloads on a single mission, sharing costs among customers. The flexibility of reusable vehicles allows for efficient integration of diverse payloads. The growing ecosystem of rideshare brokers and integrators supports this market. The demand for flexible and affordable launch options drives segment expansion. The efficiency of combining multiple medium payloads maximizes vehicle utilization. This collaborative model fosters innovation and participation in the space economy. The availability of rideshare options sustains the rapid growth of this segment. The economic benefits of shared launches attract new customers.

COUNTRY LEVEL ANALYSIS

United States Reusable Launch Vehicle Market Analysis

The United States dominated the North American reusable launch vehicle market and accounted for a significant share in 2025. It serves as the global leader in technology and operational capacity. The nation’s market profile benefits from a thriving private space economy, proactive state backing, and state-of-the-art production capabilities. The presence of major providers like SpaceX and Blue Origin drives innovation and dominance. Commercial enterprise and government funding jointly propel the U.S. reusable launch sector to global leadership. The synergy between private companies and federal agencies has created a dynamic ecosystem for development and deployment. According to the Federal Aviation Administration, the US conducts the majority of global orbital launches with reusable vehicles leading the way. As per the National Aeronautics and Space Administration, partnerships with commercial providers have reduced launch costs and increased access to space. The regulatory framework supports rapid innovation while ensuring safety and compliance. The investment in research and development by both sectors drives technological advancements. The United States benefits from a skilled workforce and an established supply chain. The strategic focus on maintaining space leadership motivates continued investment. The success of commercial reusable programs has set a global standard. The ability to launch frequently and affordably strengthens national security and economic competitiveness. This combination of public and private strength ensures market dominance. The continuous innovation in reusable technologies maintains the competitive edge. The United States remains the primary driver of global reusable launch trends. The strategic importance of space access reinforces this leading position.

COMPETITIVE LANDSCAPE

The competition in the United States reusable launch vehicle market is characterized by intense rivalry among established industry leaders and emerging innovators striving to achieve superior reusability and cost efficiency. Major players compete based on launch frequency,ency payload capacity, and the degree of reusability achieved in their systems. The market features a dominant incumbent with proven operational history while new entrants develop next-generation vehicles to capture share. Companies differentiate themselves through unique technological approaches such as methane-fueled engines or carbon composite structures. Strategic alliances with government entities provide critical funding and mission opportunities that reinforce market positions. The barrier to entry remains high due to substantial capital requirements and complex regulatory hurdles. However, the potential for transformative cost reductions attracts significant private investment. Intellectual property related to propulsion and guidance systems serves as a key competitive asset. The race to achieve full and rapid reusability drives continuous innovation and testing. This dynamic environment fosters rapid technological advancement,t benefiting customers with lower prices and increased access. The ability to demonstrate reliable and frequent launches determines long-term success in this high-stakes sector.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. Reusable Launch Vehicle Market include

- SpaceX

- Blue Origin

- Rocket Lab USA, Inc.

- Northrop Grumman Corporation

- Lockheed Martin Corporation

- Boeing Company

- Sierra Space Corporation

- Relativity Space, Inc.

- Firefly Aerospace, Inc.

- Astra Space, Inc.

- Virgin Galactic Holdings, Inc.

- Dynetics, Inc.

TOP LEADING PLAYERS IN THE MARKET

- Space Exploration Technologies Corp dominates the United States reusable launch vehicle market through its Falcon 9 and Falcon Heavy rockets. The company has revolutionized space access by achieving routine booster recovery and reflights, significantly reducing launch costs. Recent actions include the continued development and testing of the Starship system, which aims for full reusability and super-heavy lift capabilities. SpaceX actively collaborates with NASA for crewed missions to the International Space Station and lunar exploration programs. The firm maintains a high launch cadence supporting commercial satellite constellations and national security payloads. By iterating rapidly on design and manufacturing processes, SpaceX ensures continuous improvement in reliability and performance. Their vertical integration strategy allows for tight control over production timelines and costs. These efforts solidify its position as the primary provider of orbital launch services in the United States. The company's focus on making life multiplanetary drives long-term innovation and market leadership.

- Blue Origin LLC contributes significantly to the market by developing the New Glenn orbital launch vehicle designed for partial reusability. The company focuses on building a road to space with lower costs and greater access through its reusable booster technology. Recent developments involve the final stages of preparation for the inaugural launch of New Glenn, which features a recoverable first stage. Blue Origin also operates the New Shepard suborbital vehicle, which has demonstrated successful repeated landings and reuse. The firm partners with various government agencies and commercial entities to provide payload delivery services. Blue Origin emphasizes sustainable space exploration and manufactures advanced rocket engines for its own vehicles and others. Their investment in large-scale manufacturing facilities supports the production of multiple launch systems. These initiatives enhance its competitive standing in the emerging reusable launch sector. The company's commitment to incremental innovation ensures steady progress toward operational orbital flights.

- Rocket Lab USA Inc is expanding its presence in the reusable launch vehicle market with the development of the Neutron rocket. This medium lift vehicle is designed with reusability in mind, featuring a carbon composite structure and a recoverable first stage. Recent actions include the construction of dedicated launch and manufacturing facilities to support Neutron production and operations. Rocket Lab leverages its experience from the Electron small launch vehicle to inform the design of its larger reusable system. The company secures contracts for national security and commercial satellite deployments, demonstrating growing customer confidence. Rocket Lab integrates vertical manufacturing capabilities to streamline production and reduce costs. Their focus on frequent and responsive launch services appeals to constellation operators and government clients. By entering the medium lift segment with a reusable architecture,e Rocket Lab diversifies its offerings. This strategic expansion positions the company as a key competitor in the reusable launch landscape. The anticipation of Neutron flights drives significant interest and investment in the firm.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the United States reusable launch vehicle market primarily employ strategies focused on vertical integration and rapid iterative development to maintain a competitive advantage. Companies invest heavily in proprietary manufacturing techniques such as advanced composite materials and automated assembly lines to reduce production costs and timelines. Strategic partnerships with government agencies like NASA and the Department of Defense secure stable revenue streams and validate technological capabilities. Firms prioritize the development of fully reusable architectures to achieve airline-like operational efficiency and minimize marginal launch costs. Investment in ground infrastructure, including autonomous landing platforms and refurbishment facilities,s enhances turnaround speed. Manufacturers also focus on diversifying their customer base by serving commercial satellite operators, research and scientific missions,ons and national security requirements. Continuous testing and data collection from flight campaigns drive improvements in reliability and safety. These strategic initiatives enable firms to lower barriers to space access and respond effectively to the growing demand for frequent and affordable launch services in the dynamic aerospace sector.

U.S. REUSABLE LAUNCH VEHICLE MARKET NEWS

- In March 2024, Space Exploration Technologies Corp conducted another successful integrated flight test of its Starship vehicle to advance full reusability goals. This test is anticipated to allow SpaceX to refine landing procedures and strengthen the US reusable launch vehicle market presence.

- In June 2023, Blue Origin LLC completed major structural testing of the New Glenn first stage booster to prepare for the inaugural orbital launch. This completion is anticipated to allow Blue Origin to demonstrate orbital capabilities and strengthen the US reusable launch vehicle market presence.

- In January 2024, Space Exploration Technologies Corp launched additional Starlink satellites using a reused Falcon 9 booster, achieving a new reflight record. This launch is anticipated to allow SpaceX to prove operational reliability and strengthen the US reusable launch vehicle market presence.

MARKET SEGMENTATION

This research report on the U.S. reusable launch vehicle market is segmented and sub-segmented into the following categories.

By Type

- Partially Reusable Launch Vehicles

- Fully Reusable Launch Vehicles

By Orbit Type

- Low Earth Orbit (LEO)

- Medium Earth Orbit (MEO)

- Geosynchronous Transfer Orbit (GTO)

- Geostationary Orbit (GEO)

- Beyond Earth Orbit (BEO)

By Vehicle Capacity

- Below 1000 Kg

- 1000 Kg to 3000 Kg

- Above 3000 Kg

By Country

- California

- Texas

- Florida

- Virginia

- Rest of the United States

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com