U.S Dietary Supplement Market Size, Share, Trends & Growth Forecast Report - Segmented By Customer Orientation and Primary Ingredients, Form and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Dietary Supplements Market Report Summary

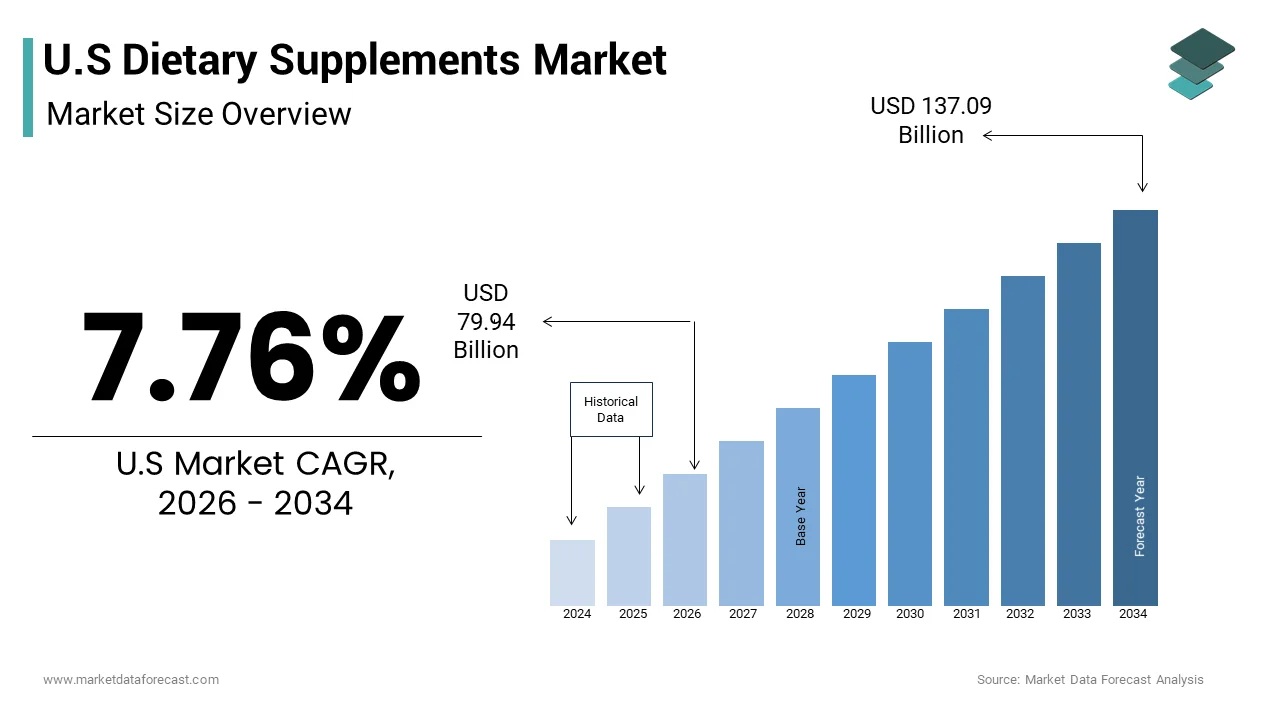

The U.S. dietary supplements market was valued at USD 74.18 billion in 2025, is estimated to reach USD 79.94 billion in 2026, and is projected to reach USD 137.09 billion by 2034, growing at a CAGR of 7.76% during the forecast period. The growth of the U.S. dietary supplements market is driven by rising consumer awareness regarding preventive healthcare, increasing focus on immunity and wellness, and growing demand for nutritional support products across all age groups. The increasing prevalence of lifestyle-related disorders, expanding fitness culture, and rising adoption of personalized nutrition solutions are further accelerating market growth in the United States. In addition, the growing popularity of plant-based, organic, and clean-label supplements is supporting product innovation and consumer adoption.

Key Market Trends

- Rising consumer demand for immunity-boosting supplements, vitamins, minerals, and herbal products to support overall health and wellness.

- Increasing adoption of personalized nutrition and customized dietary supplement solutions based on individual health needs and lifestyles.

- Growing popularity of plant-based, vegan, and clean-label supplements driven by changing consumer preferences toward natural ingredients.

- Expansion of e-commerce platforms and direct-to-consumer supplement brands improving accessibility and product availability.

- Increasing focus on sports nutrition, weight management, and healthy aging supplements among fitness-conscious and aging populations.

Segmental Insights

- Based on customer orientation, the women segment accounted for 36.4% of the United States dietary supplements market share in 2025. The segment’s dominance is attributed to rising awareness regarding women’s health, increasing demand for prenatal vitamins, beauty supplements, bone health products, and nutritional support for hormonal wellness.

- Based on form, the tablets and capsules segment captured 45.3% of the United States dietary supplements market share in 2025. The growth of this segment is driven by convenience, precise dosage formats, longer shelf life, and widespread consumer preference for easy-to-consume supplement products.

Regional Insights

The United States continues to represent one of the largest dietary supplements markets globally, supported by high consumer health awareness, strong retail distribution networks, and increasing investments in wellness and preventive healthcare products. Major metropolitan regions such as California, New York, Texas, and Florida are witnessing strong demand for dietary supplements due to rising health-conscious populations, expanding fitness trends, and increasing disposable incomes. The growing adoption of digital health platforms and online supplement purchasing channels is further strengthening market growth across the country.

Competitive Landscape

The U.S. dietary supplements market is highly competitive, with leading companies focusing on product innovation, clean-label formulations, strategic partnerships, and digital marketing initiatives to strengthen their market presence. Manufacturers are increasingly investing in research and development, personalized nutrition technologies, and sustainable ingredient sourcing to meet evolving consumer preferences. The growing demand for immunity support, sports nutrition, and holistic wellness products is further intensifying competition within the market.

Prominent players in the U.S. dietary supplements market include Bayer, Sanofi, Nestlé Health Science, Glanbia, Amway, Herbalife, NOW Foods, Pharmavite, and Unilever.

U.S Dietary Supplement Market Size

The U.S dietary supplements market size was valued at USD 74.18 billion in 2025 and is anticipated to reach USD 79.94 billion in 2026 to reach USD 137.09 billion by 2034, growing at a CAGR of 7.76% during the forecast period.

Current Market Overview and Definition

The dietary supplement are products including vitamins, minerals, herbs, amino acids, and enzymes intended to augment the daily diet. These products are regulated under the Dietary Supplement Health and Education Act of 1994, which defines them as a category distinct from conventional food and pharmaceutical drugs. Consumers utilize these supplements to address nutritional gaps support specific health goals or manage chronic conditions without medical intervention. As per the Council for Responsible Nutrition, approximately 75% of US adults report using dietary supplements indicating a deep integration into daily lifestyle routines. This widespread adoption is fueled by an aging population and increasing health consciousness across demographic segments. The regulatory framework allows for rapid innovation, while maintaining safety standards through post market surveillance. Manufacturers must ensure that their products do not contain adulterants and that label claims are substantiated by scientific evidence. Retail channels have expanded beyond traditional pharmacies to include online platforms and specialty health stores reflecting changing purchasing behaviors. The definition extends to include sports nutrition and weight management products which cater to specific fitness oriented demographics.

MARKET DRIVERS

Rising Prevalence of Chronic Diseases Drives Supplement Adoption

The escalating incidence of chronic conditions, such as diabetes cardiovascular diseases and osteoporosis is ascribed in boosting the growth of the United States dietary supplements market. Individuals diagnosed with these conditions often turn to dietary supplements to manage symptoms and improve quality of life alongside conventional medical treatments. This substantial burden of illness creates a sustained demand for nutrients that support metabolic health and immune function. For instance, patients with osteoporosis frequently consume calcium and vitamin D supplements to maintain bone density and reduce fracture risk. Similarly, individuals with cardiovascular issues may use omega three fatty acids to support heart health. The aging population exacerbates this trend as older adults are more susceptible to chronic ailments and nutrient deficiencies. The National Institute on Aging states that by 2060 the number of Americans aged 65 and older is projected to reach 95 million. This shift ensures a growing base of consumers who rely on supplements for long term health management. Healthcare providers increasingly recognize the role of nutrition in disease prevention leading to more frequent recommendations for specific supplements. This medical endorsement validates consumer choices and encourages regular usage.

Increasing Health Consciousness and Preventive Care Focus

A profound shift in consumer mindset towards preventive healthcare is accelerating the growth of the United States dietary supplements market. Modern consumers are more informed and proactive about their health seeking ways to optimize wellness rather than merely treating illness. This trend is particularly evident among millennials and Generation Z, who prioritize fitness mental clarity and immune support. As per the International Food Information Council, 52% of Americans follow a specific eating pattern or diet many of which involve supplementation to ensure adequate nutrient intake. The rise of social media and digital health platforms has amplified awareness about the benefits of various nutrients leading to increased experimentation with new products. Consumers are increasingly interested in personalized nutrition, where supplements are tailored to individual genetic profiles and lifestyle needs. This demand for customization drives innovation in product formulation and delivery methods. The concept of biohacking, which involves using science and technology to optimize human performance has gained traction further boosting sales of nootropics and energy enhancing supplements. Retailers respond to this consciousness by offering transparent labeling and third party testing certifications to build trust. The emphasis on preventive care reduces long term healthcare costs for individuals making supplement investment appear economically rational.

MARKET RESTRAINTS

Regulatory Ambiguity and Lack of Pre Market Approval

The regulatory framework governing dietary supplements due to the absence of mandatory approval by the Food and Drug Administration is hindering the growth of the United States dietary supplement market. Unlike pharmaceutical, drugs supplements do not require rigorous clinical trials to prove efficacy or safety before reaching consumers. This regulatory gap leads to market saturation with products of varying quality and potency by causing consumer awareness. As per the Government Accountability Office, the FDA faces challenges in monitoring the vast number of supplement products and identifying adulterated or misbranded items efficiently. The lack of standardized testing requirements allows some manufacturers to make unsubstantiated health claims misleading consumers about product benefits. This ambiguity erodes trust in the industry as high profile cases of contamination or ineffective products receive media attention. Consumers may hesitate to purchase supplements fearing potential health risks or financial loss from ineffective purchases. The burden of proof lies with the FDA to demonstrate that a product is unsafe after it has entered the market which is a resource intensive and time-consuming process. This reactive approach fails to prevent harmful products from reaching shelves initially.

Product Adulteration and Quality Consistency Issues

The concerns regarding product adulteration and inconsistent quality is declining the growth of the United States dietary supplement market. Instances, where supplements contain undeclared ingredients such as prescription drugs or heavy metals have raised serious safety alarms among consumers and healthcare professionals. As per the United States Pharmacopeia, thousands of supplement products fail to meet quality standards for identity purity and strength during independent testing. These failures highlight inconsistencies in manufacturing practices and supply chain oversight within the industry. Adulteration is particularly prevalent in categories such as weight loss and sexual enhancement where consumers seek rapid results. The presence of hidden pharmaceutical compounds can lead to adverse health effects and dangerous interactions with other medications. Such incidents damage the reputation of the entire industry making consumers wary of trying new brands or products. The lack of uniform Good Manufacturing Practice enforcement across all facilities contributes to variability in product quality. Small and medium sized manufacturers may lack resources for comprehensive testing leading to higher risks of contamination. Consumer reports of ineffective products further diminish confidence in supplement efficacy. The fear of consuming contaminated or substandard products drives some individuals to avoid supplements altogether.

MARKET OPPORTUNITIES

Integration of Digital Health and Personalized Nutrition

The convergence of digital health technologies and personalized nutrition is lucratively to create new opportunities for the growth of the United States dietary supplement market. Advances in genetic testing microbiome analysis and artificial intelligence enable the creation of highly customized supplement regimens tailored to individual biological needs. The demand for personalized nutrition solutions is growing rapidly as consumers seek more effective and targeted health interventions. Companies leverage data from wearable devices and health apps to recommend specific nutrients based on real time physiological metrics. This approach enhances product efficacy and consumer satisfaction by addressing unique health concerns rather than offering one size fits all solutions. Subscription based models facilitate continuous engagement and allow for adjustments in formulations as health status changes. The integration of telehealth platforms enables direct consultation with nutritionists who can prescribe supplements alongside lifestyle advice. This holistic service model adds value beyond the product itself fostering brand loyalty. Digital tools also improve adherence by sending reminders and tracking progress towards health goals. The ability to demonstrate tangible results through data visualization strengthens consumer trust in supplement benefits. Innovations in packaging, such as single serve packets labeled with user names further enhance convenience and personalization.

Expansion into Functional Foods and Beverage Formats

The transformation of dietary supplements into functional foods and beverages by appealing to consumers seeking convenience and enjoyment is another factor to leverage the growth of the United States dietary supplement market in coming years. Traditional pill and capsule formats are being supplemented by gummies powders bars and fortified drinks that integrate nutrients into daily meals and snacks. Launches of functional food and beverage products with health claims have increased substantially reflecting consumer preference for edible wellness solutions. This format innovation lowers the barrier to entry for younger people, who may dislike swallowing pills. Functional beverages such as vitamin enriched waters and adaptogenic teas offer hydration along with health benefits aligning with busy lifestyles. Gummy vitamins have gained immense popularity among children and adults due to their palatable taste and ease of consumption. The fusion of supplements with popular food items allows for seamless integration into existing dietary habits without requiring additional routine steps. Manufacturers collaborate with food companies to develop innovative products that combine taste with nutritional value. This trend also extends to snack bars infused with protein fiber or probiotics catering to health conscious on the go consumers. The versatility of functional formats enables brands to reach new retail channels such as grocery stores and convenience outlets.

MARKET CHALLENGES

Supply Chain Volatility and Raw Material Sourcing

The volatility in the global supply chain and challenges in sourcing high quality raw materials is one of the challenges for the growth of the United States dietary supplement market. Many key ingredients, such as botanicals, vitamins, and minerals are sourced from international countries, particularly Asia and Europe making them susceptible to geopolitical tensions and trade disruptions. As per the American Botanical Council fluctuations in the availability of certain herbs due to climate change and overharvesting have led to price instability and scarcity. Dependence on foreign suppliers exposes manufacturers to risks related to quality control and regulatory compliance in source countries. Contamination issues at the source can compromise entire batches of products leading to recalls and financial losses. Transportation bottlenecks and increased freight costs further exacerbate supply chain inefficiencies affecting profit margins. The lack of transparency in multi-tier supply chains makes it difficult to trace the origin and handling of raw materials. Manufacturers must invest heavily in supplier audits and testing protocols to ensure ingredient integrity. Climate change impacts agricultural yields of key crops such as turmeric and ashwagandha creating uncertainty in long term supply. These logistical and environmental challenges require companies to diversify sourcing strategies and invest in domestic production capabilities.

Consumer awareness and misinformation proliferation

The pervasive consumer awareness fueled by the spread of misinformation on digital platforms is also to impede the growth of the United States dietary supplement market. The internet abounds with conflicting advice and unverified claims about supplement efficacy leading to confusion and distrust among consumers. A substantial portion of adults encounter health misinformation online, which influences their perceptions of supplement safety and benefits. Social media algorithms often amplify anecdotal evidence over scientific consensus creating echo chambers that promote ineffective or dangerous products. This information overload makes it difficult for consumers to distinguish between credible brands and fraudulent operators. High profile scandals involving celebrity endorsed supplements that failed to deliver promised results further erode public trust. Skepticism is particularly high among educated consumers who demand rigorous scientific backing for health claims. The lack of standardized education about nutrition and supplements leaves many individuals vulnerable to misleading marketing tactics. Healthcare providers often struggle to counteract misinformation due to limited consultation time and varying levels of nutritional training. This environment of doubt hinders market growth as potential users hesitate to invest in products they perceive as risky or ineffective. Brands must invest in educational initiatives and transparent communication to rebuild trust and establish credibility in a saturated and noisy marketplace.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.76% |

| Segments Covered | By Customer Orientation and Primary Ingredients, Form, and By Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

| Regions Covered | California, Washington, Oregon, New York & Rest of the United States |

| Market Leaders Profiled | Bayer AG, Sanofi SA, Nestlé Health Science, Glanbia plc, Amway, Herbalife, NOW Foods, Pharmavite, Unilever |

SEGMENTAL ANALYSIS

By Customer Orientation Insights

Women segment was accounted in holding 36.4% of the United States dietary supplement market share in 2025 driven by specific physiological needs and higher health engagement levels. This demographic actively seeks solutions for bone health iron deficiency and hormonal balance throughout various life stages including pregnancy and menopause. As per the Council for Responsible Nutrition, women are significantly more likely than men to use dietary supplements with approximately 80% of adult women reporting regular usage compared to 70% of men. This disparity stems from a greater propensity among women to consult healthcare providers and adhere to medical recommendations regarding nutrition. The focus on preventive care is particularly strong among women, who often manage family health decisions influencing household purchasing patterns. Prenatal vitamins represent a critical subcategory where compliance is high due to medical necessity and widespread insurance coverage. Postmenopausal women drive demand for calcium and vitamin D formulations to mitigate osteoporosis risks, which affect one in two women over age 50, as stated by the National Osteoporosis Foundation. The beauty from within trend further amplifies consumption of collagen and biotin supplements among younger women seeking skin and hair benefits. Marketing strategies tailored to female wellness narratives resonate deeply fostering brand loyalty. Retailers prioritize shelf space for women centric products recognizing their higher purchase frequency and basket size.

The senior citizen segment is lucratively to witness a fastest CAGR of 7.6% from 2026 to 2034 with the rapid demographic aging and increasing health awareness among older adults. This cohort is expanding swiftly as baby boomers reach retirement age bringing with them a strong emphasis on active aging and longevity. As per the United States Census Bureau, the population aged 65 and older is projected to grow from 56 million in 2020 to 95 million by 2060 representing a significant expansion of the potential consumer base. Seniors are increasingly proactive about managing age related conditions such as cognitive decline joint pain and vision loss through targeted supplementation. The demand for omega three fatty acids coenzyme Q10 and lutein is rising sharply within this group due to their perceived benefits for heart brain and eye health. Medicare Advantage plans and private insurers are beginning to recognize the value of preventive nutrition potentially improving access to high quality supplements. Older consumers also exhibit higher brand loyalty and willingness to pay premium prices for products with clinical backing. The shift towards home based care and telehealth has facilitated easier access to nutritional counseling for seniors who may have mobility limitations. Digital literacy among older adults is improving enabling them to research and purchase supplements online.

Leading Segment Analysis: Vitamins in Primary Ingredients

The vitamins segment was the largest by holding 55.4% of the United States dietary supplement market share in 2025 due to their foundational role in general health maintenance and widespread consumer familiarity. Multivitamins remain the most commonly used supplement category serving as an insurance policy against dietary gaps for millions of Americans. Vitamin D and vitamin C have seen surged popularity, particularly following the global pandemic as consumers sought to bolster immune defenses. The Endocrine Society notes that nearly 40% of the US population has vitamin D deficiency driving consistent demand for supplementation especially in northern latitudes with limited sunlight exposure. Vitamin B complex formulations are widely consumed for stress management and energy support appealing to busy professionals and students. The ease of understanding vitamin benefits compared to more complex botanicals or amino acids lowers the barrier to entry for new users. Retailers allocate prominent shelf space to vitamin products ensuring high visibility and accessibility. Private label brands compete aggressively in this category offering affordable options that maintain volume sales.

The prebiotics and probiotics constitute segment is esteemed to grow at a fastest CAGR of 8.1% during the forecast period with the expanding scientific understanding of the gut microbiome. Consumers are increasingly aware of the link between gut health and overall wellness, including mental health immune function and weight management. The proliferation of research linking gut bacteria to conditions, such as irritable bowel syndrome, anxiety, and obesity is fuelling the growth if the segment. Strain specific formulations are gaining traction as consumers seek targeted solutions for digestive issues rather than generic blends. The American Gastroenterological Association acknowledges the growing evidence supporting the use of probiotics for certain gastrointestinal disorders lending credibility to consumer choices. Yogurt and fermented food trends have paved the way for supplement adoption among health-conscious individuals. Innovations in shelf stable technologies allow for more potent and convenient products that do not require refrigeration. Personalized probiotic services using stool analysis are emerging as premium offerings attracting early adopters. The integration of prebiotics fibers that feed beneficial bacteria enhances product efficacy and appeal.

By Form Insights

The tablets and capsules segment was the largest by capturing 45.3% of the United States dietary supplements market share in 2025 due to their cost efficiency stability and precise dosing capabilities. This traditional format allows for high concentrations of active ingredients in a compact size making it ideal for multivitamins and mineral supplements. The production process for these forms is well established and scalable resulting lower manufacturing costs compared to gummies or liquids. This economic advantage translates to competitive retail pricing which appeals to budget conscious shoppers and bulk buyers. Tablets offer extended release options that enhance absorption and efficacy for certain nutrients such as calcium and iron. Capsules are preferred for herbal extracts and oils as they mask unpleasant tastes and odors effectively. The familiarity of swallowing pills among older demographics ensures steady demand despite the rise of alternative formats. Pharmacists and healthcare providers often recommend tablets and capsules for their reliability and standardized potency. Retailers benefit from longer shelf lives and reduced packaging waste associated with these forms. The ability to combine multiple ingredients in a single tablet supports the popularity of comprehensive multivitamin formulations.

The gummies and chews segment is expected to grow at a fastest CAGR of 9.2% during the forecast period with their palatability convenience and appeal to younger people. This format transforms supplement intake into an enjoyable experience overcoming the aversion many consumers feel towards swallowing pills. Children and adults alike prefer the taste and texture of gummies making adherence to daily regimens easier. The success of gummy vitamins has expanded into other categories including sleep aids stress relief and beauty supplements. Major confectionery and pharmaceutical companies have entered this space leveraging their expertise in flavor profiling and manufacturing. Sugar free and vegan options are emerging to address health concerns associated with traditional gummies. The visual appeal of gummies makes them highly shareable on social media platforms driving organic marketing and brand awareness. Retailers place gummies at eye level and near checkout counters capitalizing on impulse purchases.

COMPETITIVE LANDSCAPE

The competition in the United States dietary supplement market is intense and characterized by a fragmented landscape with numerous established pharmaceutical companies alongside emerging niche brands. Major corporations leverage their extensive distribution networks and strong brand recognition to dominate shelf space in retail outlets and online platforms. Smaller entities compete by offering specialized formulations and unique ingredient combinations that appeal to specific health concerns such as gut health or cognitive support. Innovation plays a pivotal role as companies strive to differentiate their products through novel delivery methods like gummies and effervescent tablets. Price competition is fierce particularly in the multivitamin segment where private label brands offer affordable alternatives to premium products. Regulatory compliance and quality assurance serve as key differentiators with third party certifications becoming essential for building consumer trust. Digital presence is crucial as brands invest heavily in e commerce capabilities and direct to consumer models to bypass traditional retail channels. Marketing strategies focus heavily on influencer partnerships and educational content to engage informed consumers.

KEY MARKET PLAYERS

A few of the market players that are dominating the U.S dietary supplements market are

- Bayer AG

- Sanofi SA

- Nestlé Health Science

- Glanbia plc

- Amway

- Herbalife

- NOW Foods

- Pharmavite

- Unilever

Top Players In The Market

- Bayer AG maintains a robust presence in the European dietary supplement sector through its Consumer Health division which offers a wide portfolio of trusted brands. The company focuses on science backed nutrition solutions that address specific health needs such as immune support and bone health. Recent actions include strategic investments in digital health platforms to enhance consumer engagement and personalized nutrition services. Bayer actively collaborates with healthcare professionals to promote evidence based supplement usage ensuring high credibility among consumers. The company continues to expand its product range with innovative formulations that cater to evolving lifestyle demands across various European markets. Its commitment to sustainability and transparent sourcing strengthens brand loyalty and trust. Bayer leverages its extensive distribution network to ensure widespread availability of its products in pharmacies and retail outlets. These efforts reinforce its position as a leading provider of high quality dietary supplements in the region.

- Sanofi SA contributes significantly to the European dietary supplement market by leveraging its pharmaceutical expertise to develop high efficacy nutritional products. The company focuses on preventive health solutions that complement medical treatments and support overall wellness. Recent initiatives include the launch of specialized supplement lines targeting gut health and immune resilience driven by advanced research and development. Sanofi engages in strategic partnerships with local distributors to enhance market penetration in key European countries. The company emphasizes clinical validation of its products to differentiate itself in a competitive landscape. Sanofi also invests in consumer education campaigns to raise awareness about the benefits of targeted nutrition. Its strong regulatory compliance framework ensures product safety and quality consistency.

- Glanbia plc is a prominent player in the European dietary supplement market known for its extensive portfolio of sports nutrition and wellness brands. The company specializes in high quality protein powders vitamins and mineral supplements that cater to active lifestyles and general health maintenance. Recent actions include the expansion of its manufacturing facilities to increase production capacity and meet growing demand. Glanbia focuses on innovation by developing clean label products that appeal to health conscious consumers seeking natural ingredients. The company strengthens its market position through strategic acquisitions of niche brands that offer specialized nutritional solutions. Glanbia also enhances its direct to consumer capabilities through e commerce platforms providing personalized shopping experiences. Its commitment to sustainability and ethical sourcing resonates with environmentally aware customers.

Top Strategies Used By Key Market Participants

Key players in the United States dietary supplement market primarily employ product innovation and strategic partnerships to maintain competitive advantage. Companies focus heavily on developing personalized nutrition solutions using digital health technologies to tailor products to individual consumer needs. This approach enhances customer loyalty and drives repeat purchases. Mergers and acquisitions are frequently utilized to expand product portfolios and enter new demographic segments efficiently. Brands invest significantly in clinical research to substantiate health claims and build consumer trust in product efficacy. Digital marketing and social media engagement serve as critical tools for reaching younger demographics and educating consumers about benefits. Expansion into functional food and beverage formats allows companies to integrate supplements into daily diets seamlessly. Supply chain transparency and sustainable sourcing practices are increasingly adopted to appeal to environmentally conscious shoppers.

MARKET SEGMENTATION

This research report on the U.S dietary supplements market is segmented and sub-segmented into the following categories.

By Customer Orientation

- Women

- Men

- Senior Citizen

- Toddlers/Kids

By Primary Ingredients

- Vitamins

- Minerals

- Omega 3

- Botanicals Herbs or Compounds

- Prebiotics & Probiotics

- Collagen

- Amino Acid

- Enzymes

- Protein (Whey, Casein)

By Form

- Tablets & Capsules

- Gummies & Chews

- Powder

- Soft Gel

- Liquid

- Others (Lollipops, hard boiled candies)

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

What is the U.S. dietary supplements market?

The U.S. dietary supplements market includes vitamins, minerals, herbal products, and nutritional supplements used to support health and wellness.

Why is the U.S. dietary supplements market growing rapidly?

The market is growing due to rising health awareness and increasing consumer focus on preventive healthcare.

What types of dietary supplements are most popular in the U.S.?

Popular supplements include vitamins, protein powders, probiotics, omega-3 products, and herbal supplements.

Which dietary supplement segment leads the U.S. market?

Vitamin supplements lead the market due to strong consumer demand for daily nutritional support.

Who are the primary consumers in the U.S. dietary supplements market?

Fitness enthusiasts, aging populations, athletes, and health-conscious consumers are the major users.

How is e-commerce influencing the U.S. dietary supplements market?

Online platforms are increasing product accessibility and supporting direct-to-consumer supplement sales.

Why are plant-based dietary supplements gaining popularity in the U.S.?

Consumers are increasingly choosing plant-based products for natural and clean-label health solutions.

What challenges does the U.S. dietary supplements market face?

Regulatory concerns, misleading product claims, and quality control issues can affect market growth.

How is innovation impacting the dietary supplements industry?

Personalized nutrition and functional ingredient development are driving new product innovation.

What is the future outlook for the U.S. dietary supplements market?

The market is expected to grow steadily with increasing focus on wellness, immunity, and preventive nutrition.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com