U.S. Tablet Market Size, Share, Trends & Growth Forecast Report By Distribution Channel, Type, Os, and Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Tablet Market Report Summary

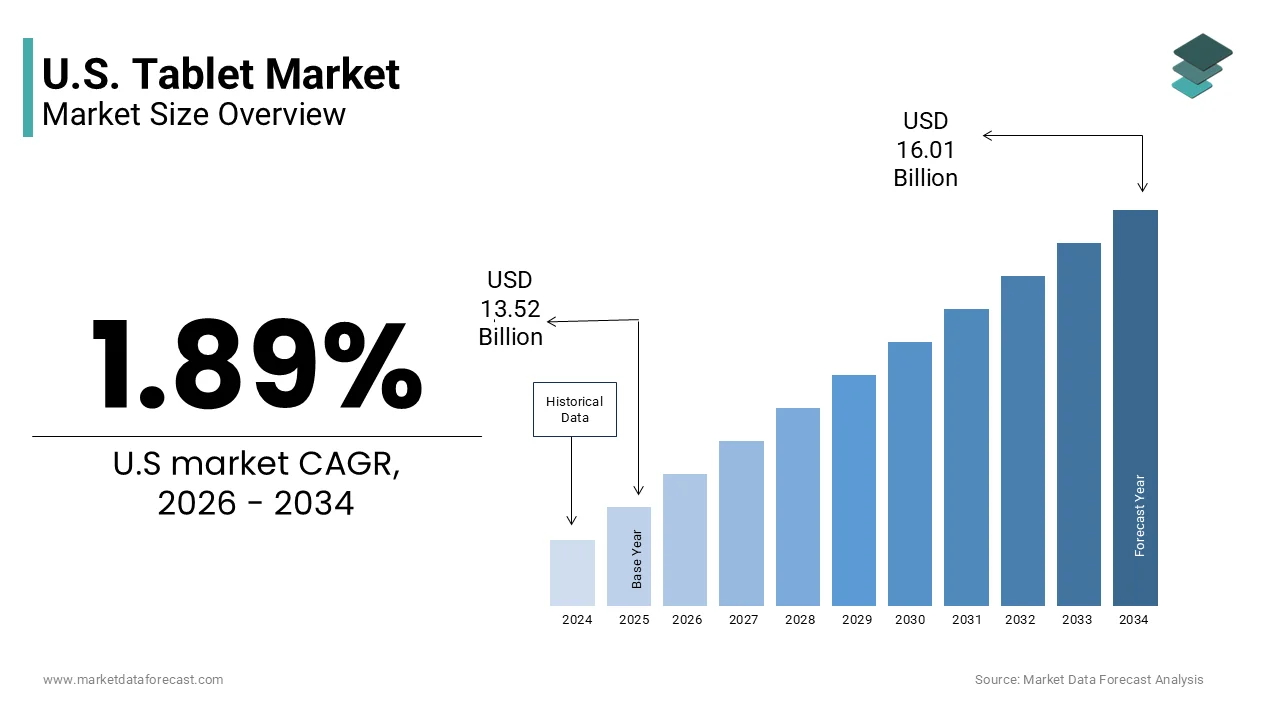

The U.S. tablet market was valued at USD 13.52 billion in 2025, is estimated to reach USD 13.78 billion in 2026, and is projected to reach USD 16.01 billion by 2034, growing at a CAGR of 1.89% during the forecast period. Market growth is driven by increasing demand for portable computing devices, expanding use of tablets in education and enterprise applications, and rising consumer preference for lightweight digital devices. Tablets continue to remain popular for entertainment, productivity, remote learning, and hybrid work environments due to their portability and multifunctionality. The growing integration of advanced processors, cloud connectivity, and AI powered features is further supporting market development across the United States.

Key Market Trends

- Rising demand for portable and multifunctional digital devices is driving market growth.

- Increasing adoption of tablets in education, enterprise, and remote work applications is boosting market expansion.

- Growing consumer preference for lightweight entertainment and productivity devices is supporting product demand.

- Expansion of hybrid work and digital learning environments is enhancing tablet usage.

- Innovation in AI features, cloud integration, and detachable keyboard compatibility is influencing market development.

Segmental Insights

- Based on distribution channel, the offline segment accounted for the dominant share of the U.S. tablet market in 2025. This dominance is attributed to the strong presence of electronics retailers, carrier stores, and large format retail outlets that provide hands on product experiences and immediate purchases.

- Based on type, the slate tablet segment held the leading share of the U.S. tablet market in 2025 and is expected to maintain its dominance during the forecast period due to its portability, ease of use, and broad consumer adoption.

Regional Insights

- The United States accounted for 31.3% of the North American tablet market share in 2025 and is expected to maintain its leadership position during the forecast period. Strong consumer electronics adoption, advanced digital infrastructure, and rising demand for connected devices continue to support market expansion across the country.

Competitive Landscape

The U.S. tablet market is highly competitive, with key players focusing on advanced display technologies, productivity features, and ecosystem integration to strengthen their market position. Companies are investing in AI enabled devices, premium hardware, and enterprise mobility solutions. Prominent players in the U.S. tablet market include Acer Inc., Amazon.com Inc., Apple Inc., Dell Technologies Inc., Google LLC, HP Inc., Lenovo Group Ltd., Microsoft Corp., Motorola Mobility LLC, OnePlus Technology Co. Ltd., Panasonic Holdings Corp., Razer Inc., Samsung Electronics Co. Ltd., TCL Industries Holdings Ltd., Xiaomi Inc., and Zebra Technologies Corp..

U.S. Tablet Market Size

The U.S. tablet market size was valued at USD 13.52 billion in 2025, is estimated to reach USD 13.78 billion in 2026, and is projected to reach USD 16.01 billion by 2034, growing at a CAGR of 1.89% from 2026 to 2034.

As digital integration deepens, tablets have become essential tools in education, healthcare, and enterprise environments. According to the National Center for Education Statistics, approximately 95% of schools in the U.S. provide access to digital devices, with tablets being a primary choice for K 12 students due to their durability and ease of use. The healthcare sector also relies heavily on these devices for patient monitoring and electronic health record management. According to the American Hospital Association, over 80% of hospitals utilize mobile devices, including tablets, for clinical workflows to enhance efficiency and accuracy. Furthermore, the aging population drives demand for user friendly interfaces that facilitate communication and health monitoring. As per the Pew Research Center, approximately 42% of adults aged 65 and older own a tablet, reflecting its role in bridging the digital divide. The convergence of high performance processors and lightweight designs enables seamless multitasking, which appeals to professionals requiring mobility. This technological sophistication ensures that tablets remain relevant despite the prevalence of other personal computing devices, serving as critical nodes in modern digital lifestyles.

MARKET DRIVERS

Expansion of Hybrid Work Models and Remote Learning Infrastructure

The widespread adoption of hybrid work models and remote learning infrastructure is a significant driver of the U.S. tablet market. Organizations and educational institutions increasingly recognize the need for flexible devices that support collaboration and accessibility outside traditional settings. According to the Bureau of Labor Statistics, approximately 22% of employed Americans continue to work from home at least part of the time, creating sustained demand for portable computing solutions. Tablets offer the mobility required for dynamic work environments, while providing sufficient processing power for video conferencing and document editing. In the education sector, the shift towards digital curricula necessitates reliable devices for student engagement. According to the National Center for Education Statistics, spending on educational technology has increased significantly, as schools integrate interactive learning platforms. Tablets facilitate this transition by supporting diverse applications and intuitive interfaces, suitable for various age groups. The ability to connect peripherals, such as keyboards and styluses, enhances their utility for professional and academic tasks. As per a survey by the Society for Human Resource Management, 60% of employers provide company owned devices to remote workers, with tablets being a popular choice for field staff. This institutional endorsement drives bulk purchases and long term replacement cycles. Furthermore, the compatibility of tablets with cloud based productivity suites ensures seamless integration into existing digital ecosystems. These factors collectively sustain robust demand across multiple sectors.

Growing Penetration of 5G Networks and Enhanced Connectivity

The rapid expansion of 5G networks and enhanced connectivity options primarily drives the U.S. tablet market by enabling faster data transmission and low latency experiences. Consumers and businesses increasingly rely on constant internet access for streaming, cloud computing, and real time collaboration. According to the Federal Communications Commission, 5G coverage reached 98% of the U.S. population by 2025, facilitating widespread adoption of connected devices. Tablets equipped with 5G capabilities allow users to maintain high speed connections without dependence on Wi Fi hotspots. This mobility is particularly valuable for professionals who travel or work in remote locations. According to the Consumer Technology Association, sales of 5G enabled tablets increased significantly as consumers seek future proof devices. The improved network infrastructure supports bandwidth intensive applications, such as augmented reality and high definition video conferencing. As per Verizon Communications, the average download speeds on 5G networks are ten times faster than 4G, enhancing the performance of cloud based services on tablets. This technological advancement encourages the development of more sophisticated applications that leverage real time data processing. Additionally, the Internet of Things ecosystem benefits from 5G connectivity that allow tablets to serve as central hubs for smart home and industrial devices. The reliability and speed of 5G networks thus transform tablets into powerful tools for both entertainment and professional productivity, driving consumer upgrades and new purchases.

MARKET RESTRAINTS

Market Saturation and Extended Device Replacement Cycles

Market saturation and extended device replacement cycles are major restraints for the U.S. tablet market, which is limiting growth potential in mature segments. Most consumers already own a tablet or smartphone that meets their basic needs, reducing the urgency for upgrades. According to the Pew Research Center, 90% of Americans own a smartphone, which often overlaps in functionality with entry level tablets, diminishing the perceived necessity of a separate device. The improved performance and larger screens of modern smartphones have cannibalized the lower end tablet market. According to the Consumer Electronics Association, the average replacement cycle for tablets has extended to 4 to 5 years, as devices become more durable and software support lasts longer. This longevity reduces the frequency of repeat purchases, impacting overall sales volume. Furthermore, the lack of significant innovation in recent generations fails to compel consumers to upgrade prematurely. According to a study by IDC, many users find their existing devices sufficient for media consumption and light productivity tasks. The economic uncertainty also prompts households to prioritize essential expenditures over discretionary electronics. Consequently, manufacturers face challenges in stimulating demand without compelling value propositions. The saturation in the consumer segment forces companies to focus on niche markets or enterprise solutions, where replacement cycles may be shorter due to heavy usage. These factors collectively constrain the expansion of the broader tablet market.

Competition from Large Screen Smartphones and Lightweight Laptops

Intense competition from large screen smartphones and lightweight laptops is further hampering the expansion potential of the U.S. tablet market. The boundary between device categories has blurred as phones grow larger and laptops become thinner and more versatile. According to the International Data Corporation, shipments of foldable and large screen smartphones have grown rapidly, providing users with ample display area for content consumption. This trend reduces the need for a secondary device for casual browsing and media viewing. Additionally, the rise of ultrabooks and convertible laptops with touch screens offers superior productivity features that tablets often lack. According to Gartner, laptop sales have remained stable as remote work drives demand for full featured computing devices with physical keyboards. These laptops provide better multitasking capabilities and software compatibility for professional applications. As per Apple Inc, the introduction of powerful M series chips in MacBooks has enhanced their appeal to creative professionals, who might otherwise consider high end tablets. The versatility of these alternatives makes them more attractive for users seeking a single device for work and play. Consequently, tablets struggle to justify their existence as standalone devices for many consumers. This competitive pressure forces tablet manufacturers to differentiate through specialized features or ecosystem integration, which may not appeal to the mass market.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Advanced Productivity Features

The integration of artificial intelligence and advanced productivity features is a significant opportunity for the U.S. tablet market, by transforming these devices into powerful creative and professional tools. Manufacturers are incorporating AI driven capabilities, such as voice recognition, image enhancement, and predictive text, to improve user experience and efficiency. According to the Consumer Technology Association, the adoption of AI enabled features in tablets has increased significantly, attracting professionals and creators. These technologies enable tasks such as real time language translation, automated note taking, and intelligent photo editing, which enhance the utility of tablets for work and study. According to Microsoft, the use of productivity apps on tablets has grown by 25%, as users leverage these devices for business tasks. The inclusion of neural processing units allows for faster and more efficient AI computations on device, ensuring privacy and speed. As per NVIDIA, the deployment of AI accelerators in mobile chips has improved performance significantly, enabling complex applications to run smoothly. This technological advancement opens new markets in graphic design, video production, and data analysis. Furthermore, AI powered accessibility features make tablets more inclusive for users with disabilities, expanding the potential customer base. By positioning tablets as essential tools for creativity and productivity, manufacturers can justify premium pricing and drive upgrades among professional users. This shift from consumption to creation devices creates a new growth avenue in the mature market.

Expansion in Healthcare and Industrial Enterprise Applications

The expansion of tablets in healthcare and industrial enterprise applications offers a promising opportunity for the U.S. market, by addressing specific operational needs in specialized sectors. Hospitals and manufacturing facilities increasingly deploy ruggedized and secure tablets for data collection, patient care, and inventory management. According to the American Hospital Association, over 80% of hospitals use mobile devices, including tablets, for clinical workflows to enhance efficiency. These devices enable real time access to electronic health records, improving patient safety and care coordination. According to the Manufacturing Institute, approximately 60% of industrial firms have adopted mobile technology for floor operations, to enhance efficiency and reduce errors. Rugged tablets withstand harsh environments and provide reliable connectivity for logistics and quality control tasks. As per Zebra Technologies, the demand for enterprise grade tablets has grown by 18% annually, driven by the need for durable and secure solutions. The integration of barcode scanners and sensors further enhances their functionality in supply chain management. Additionally, telemedicine initiatives rely on tablets for remote consultations, expanding access to healthcare services. These specialized applications require high performance and security features that standard consumer devices cannot provide. By targeting these high value sectors, manufacturers can achieve steady revenue streams and build long term partnerships. This diversification reduces reliance on the volatile consumer market and leverages the growing digitization of critical industries.

MARKET CHALLENGES

Supply Chain Volatility and Component Shortages

Supply chain volatility and component shortages are key challenges to the U.S. tablet market, which is affecting production timelines and product availability. The manufacturing of tablets relies on complex global supply chains for semiconductors, displays, and batteries, which are vulnerable to geopolitical tensions and logistical bottlenecks. According to the Semiconductor Industry Association, global semiconductor sales reached $526.8 billion in 2023, though lead times for critical microcontrollers remain a challenge for consumer electronics manufacturing. This scarcity forces companies to prioritize high margin models and delay launches of new products. According to the Institute for Supply Management, 60% of manufacturing firms experienced significant supply chain disruptions in the past year due to transport issues. The reliance on overseas production exposes manufacturers to trade policy changes and tariff fluctuations. As per the U.S. International Trade Commission, tariffs on imported electronics have increased costs by 10% for some manufacturers, affecting profit margins. These cost increases are often passed on to consumers, potentially dampening demand in price sensitive segments. Additionally, the shortage of rare earth materials used in batteries and screens complicates production planning. Small and medium sized brands are disproportionately affected, as they lack the bargaining power to secure supply allocations. Diversifying supply chains and nearshoring production are strategic responses, but require substantial investment and time. The unpredictability of global logistics complicates long term planning and inventory management. Ensuring consistent product availability while managing costs remains a critical operational challenge for industry leaders navigating this volatile environment.

Cybersecurity Vulnerabilities and Data Privacy Concerns

Cybersecurity vulnerabilities and data privacy concerns are further challenging the expansion of the U.S. tablet market, as these devices become increasingly integrated into professional and personal networks. Tablets store sensitive information and connect to various cloud services, making them attractive targets for cyberattacks. According to the Cybersecurity and Infrastructure Security Agency, approximately 15% of reported network breaches involved mobile devices, highlighting the risks associated with their connected use. Vulnerabilities in operating systems and third party applications can expose user data to theft or manipulation. According to the Ponemon Institute, 45% of organizations have experienced a security incident related to internet of things and mobile devices, emphasizing the need for robust security measures. Compliance with regulations, such as the California Consumer Privacy Act, requires manufacturers to implement strict data protection protocols. As per the Federal Trade Commission, companies failing to safeguard user privacy face significant fines and reputational damage. The complexity of securing diverse device models and ensuring timely software updates adds to the challenge. Many users neglect to install security patches, leaving devices exposed to known threats. This gap between manufacturer efforts and user behavior creates ongoing vulnerabilities. Additionally, the use of tablets in public networks increases the risk of interception. Addressing these risks requires continuous investment in security technologies and user education. However, the cost of implementing comprehensive security solutions can increase device prices, potentially deterring budget conscious buyers. Balancing security, usability, and affordability remains a complex challenge for market participants.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 1.89% |

| Segments Covered | By Distribution Channel, Type, Os, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | Acer Inc., Amazon.com Inc., Apple Inc., Dell Technologies Inc., Google LLC, HP Inc., Lenovo Group Ltd., Microsoft Corp., Motorola Mobility LLC, OnePlus Technology Co. Ltd., Panasonic Holdings Corp., Razer Inc., Samsung Electronics Co. Ltd., TCL Industries Holdings Ltd., Xiaomi Inc., and Zebra Technologies Corp |

SEGMENTAL ANALYSIS

By Distribution Channel Insights

The offline segment had the highest share of the U.S. tablet market in 2025 and is anticipated to maintain its leading market position during the forecast period due to the established presence of major electronics retailers, carrier stores, and big box outlets. This segment allows consumers to physically interact with devices, assessing screen quality, build, and ergonomics before making a purchase decision, which is crucial for high value electronics. Physical stores continue to optimize their interactive displays to maintain strong local consumer engagement. The rising consumer preference for hands on evaluation and immediate product availability is also propelling the expansion of the offline segment in the U.S. market. Tablets are tactile devices where display resolution, touch sensitivity, and weight significantly influence buying decisions. According to the National Retail Federation, approximately 60% of consumers prefer to test electronic devices in person before purchasing, to ensure they meet their specific needs. Major retailers, such as Best Buy and Walmart, provide dedicated experience zones where customers can compare different models side by side. According to the Consumer Electronics Association, 45% of tablet buyers visit physical stores to verify specifications and compatibility with existing accessories. The ability to take the product home immediately satisfies the demand for instant gratification, which online shipping cannot match. Furthermore, offline stores offer personalized assistance from knowledgeable staff, who can guide customers through technical features and setup processes. As per a survey by Deloitte, 55% of shoppers value the expert advice provided in store, which reduces the perceived risk of purchasing complex technology. Return policies are also perceived as more straightforward in physical locations, enhancing consumer confidence. These factors collectively reinforce the offline channel as the preferred route for many tablet purchasers, particularly for first time buyers and those seeking premium devices.

However, the online distribution channel segment is projected to experience rapid expansion over the coming years and register a CAGR of 12.1% during the forecast period owing to the convenience of home delivery, extensive product variety, and competitive pricing strategies employed by e commerce giants. Digital consumers increasingly prefer automated purchase paths and localized delivery options. The unparalleled convenience of shopping from home, and the ability to access a wider range of models and configurations than physical stores can stock is further boosting the tablet market expansion in the U.S. E commerce platforms offer detailed comparisons, user reviews, and competitive pricing, which appeal to tech savvy consumers. According to the U.S. Census Bureau, e commerce sales of electronics and appliances have shown continuous steady gains, reflecting a structural shift in consumer behavior. Online retailers frequently offer exclusive discounts, bundle deals, and trade in programs that lower the effective cost of tablets. Data from Statista shows that 70% of consumers check online prices before making an in store purchase, indicating the strong influence of digital channels on buying decisions. The integration of augmented reality tools allows users to visualize device sizes and features, enhancing the online shopping experience. As per Amazon.com, same day or next day delivery options have reduced the waiting time gap with offline retail, making online purchases more attractive. Additionally, online platforms provide access to niche brands and specialized models that may not be available locally. The ease of returning products through prepaid labels further mitigates purchase anxiety. These advantages drive the sustained growth of the online distribution channel, as consumers increasingly prioritize efficiency and value.

By Type Insights

The slate tablet segment dominated the market in 2025 and is expected to remain the highest share of the U.S. market throughout the forecast period due to its lightweight design, ease of use, and affordability, which is making it the preferred choice for media consumption, casual browsing, and educational purposes. Slate tablets lack attached keyboards, offering a pure touch screen experience that appeals to a broad demographic. Educational institutions and budget conscious households form the core baseline for this product form factor. The affordability and simplicity of slate segment that make it accessible to a wide range of consumers, including students, seniors, and casual users is further boosting the expansion of the slate tablet segment in the U.S. market. Slate tablets are generally less expensive than hybrid or convertible models, lowering the barrier to entry. According to the Pew Research Center, approximately 42% of adults aged 65 and older own a tablet, with slate models being the most popular due to their intuitive interface and portability. The education sector heavily relies on slate tablets for digital learning initiatives. According to the National Center for Education Statistics, a vast majority of K 12 schools use tablets for classroom activities, because they are durable and easy for young children to handle. The lightweight nature of slate devices makes them ideal for travel and leisure use. As per the Consumer Technology Association, slate tablets account for 65% of total tablet shipments in the U.S., reflecting their mass market appeal. The availability of budget friendly options from various manufacturers ensures that there is a slate tablet for every price point. Furthermore, the long battery life of these devices enhances their utility for all day use without frequent charging. These factors collectively establish the slate segment as the cornerstone of the tablet market, serving the fundamental needs of the majority of users.

However, the hybrid tablet segment is projected to grow at the fastest CAGR of 14.1% during the forecast period owing to the increasing demand for versatile devices that combine the portability of a tablet with the productivity of a laptop. Enterprise professionals and mobile creators are increasingly adopting these multi-functional architectures. The enduring trend of remote work and the need for versatile devices that support both mobility and productivity are primarily fuelling the growth of the hybrid tablet segment in the U.S. market. Hybrid tablets with detachable keyboards allow users to switch seamlessly between touch based interaction and traditional typing modes. According to the Bureau of Labor Statistics, approximately 22% of employed Americans work from home at least part of the time, creating a sustained demand for flexible computing solutions. Data from Microsoft indicates that sales of Surface Pro devices, which are leading hybrids, have shown strong annual gains, as professionals seek alternatives to bulky laptops. The ability to run full desktop applications on hybrid devices makes them suitable for business tasks, such as spreadsheet management and video conferencing. As per IDC, the adoption of hybrid tablets in the enterprise sector has grown by 15%, due to their compatibility with corporate software ecosystems. The inclusion of high performance processors and ample storage further enhances their appeal to creative professionals. Additionally, the rise of digital nomadism encourages the use of lightweight yet powerful devices for work on the go. These factors ensure that the hybrid segment continues to expand, as users prioritize versatility and efficiency in their personal and professional lives.

COUNTRY LEVEL ANALYSIS

The U.S. captured 31.3% of the North American market share in 2025 and is poised to strengthen its status as the world's most dominant and advanced tablet economy for the next several years. This leading position is supported by a robust economy, a large corporate sector, and high technological adoption rates. The dominant position of the U.S. in the global tablet market is supported by high levels of disposable income and a robust digital infrastructure that facilitates widespread device usage. Consumers in the US have the financial capacity to invest in premium tablets and accessories, driving revenue growth. According to the Bureau of Economic Analysis, real personal consumption expenditures on durable goods have remained highly resilient, indicating sustained purchasing power. The extensive coverage of high speed broadband and 5G networks enhances the utility of tablets for streaming and cloud computing. According to the Federal Communications Commission, 95% of Americans have access to broadband internet, enabling seamless connectivity for tablet users. The presence of major technology companies and a vibrant app ecosystem further stimulates demand. As per the Software Alliance, the U.S. is home to the largest number of mobile app developers, ensuring a constant stream of innovative content and services for tablet users. Educational and healthcare institutions also contribute significantly to demand through large scale procurement programs. The cultural emphasis on connectivity and digital literacy encourages regular upgrades and adoption of new technologies. These economic and structural advantages solidify the U.S. as the pivotal hub for the global tablet industry, driving global innovation.

COMPETITIVE LANDSCAPE

The competition in the U.S. tablet market is intense and characterized by a few dominant players leveraging ecosystem lock in and brand loyalty to maintain their positions. Apple leads with its premium iPad lineup while Samsung and Amazon compete strongly in the Android and budget segments respectively. The market is mature with slow unit growth prompting manufacturers to focus on increasing average selling prices through premium features and accessories. Differentiation is achieved via processor performance display quality and software capabilities such as artificial intelligence integration. Price competition remains fierce in the entry level segment where Amazon dominates with loss leading strategies to drive content sales. Enterprise and education sectors represent key battlegrounds where companies offer specialized devices and management tools. The rise of hybrid work has blurred lines between tablets and laptops forcing innovation in keyboard attachments and desktop class applications. Supply chain efficiency and component sourcing are critical for maintaining margins amidst global volatility. Regulatory scrutiny regarding app store practices and data privacy adds complexity to competitive strategies. Companies must continuously innovate and adapt to changing consumer preferences to retain relevance in this highly consolidated and dynamic market environment.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. tablet market are

- Acer Inc.

- Amazon.com Inc.

- Apple Inc.

- Dell Technologies Inc.

- Google LLC

- HP Inc.

- Lenovo Group Ltd.

- Microsoft Corp.

- Motorola Mobility LLC

- OnePlus Technology Co. Ltd.

- Panasonic Holdings Corp.

- Razer Inc.

- Samsung Electronics Co. Ltd.

- TCL Industries Holdings Ltd.

- Xiaomi Inc.

- Zebra Technologies Corp.

Top Players in the Market

- Apple Inc maintains a commanding presence in the U.S. tablet market through its iPad lineup which sets industry standards for performance and ecosystem integration. The company leverages its proprietary silicon chips to deliver superior processing power and energy efficiency. Recent actions include introducing advanced AI features in iPadOS to enhance productivity and creativity for professional users. Apple has also expanded its education initiatives by offering specialized discounts and curriculum resources to schools. The seamless connectivity with iPhones and Macs encourages brand loyalty and repeat purchases. By focusing on premium build quality and a robust app ecosystem Apple attracts high value customers. The company continues to innovate with accessories like the Apple Pencil and Magic Keyboard to transform tablets into laptop replacements. These strategic moves reinforce its leadership position by addressing diverse consumer needs from entertainment to professional workflows while maintaining strong profit margins.

- Samsung Electronics Co Ltd is a key competitor in the U.S. tablet market offering a diverse range of Android based devices that cater to various price points and user preferences. The company emphasizes display technology and multitasking capabilities in its Galaxy Tab series. Recent efforts include integrating advanced artificial intelligence tools into its software suite to improve user experience and productivity. Samsung has strengthened partnerships with major US carriers to ensure wide availability and promotional support. The introduction of S Pen functionality across more models enhances appeal for creative professionals and students. The company focuses on ecosystem synergy allowing seamless interaction with Galaxy smartphones and wearables. By offering flexible storage options and durable designs Samsung captures both consumer and enterprise segments. Its commitment to regular software updates and security patches builds trust among business users. These strategies enable Samsung to maintain a strong foothold in the competitive landscape by delivering versatile and high quality computing solutions.

- Amazon com Inc plays a significant role in the U.S. tablet market with its Fire tablet lineup which prioritizes affordability and content accessibility. The company targets budget conscious consumers and families by offering devices at competitive price points. Recent actions include enhancing parental control features and integrating deeper connections with Prime Video and Kindle services. Amazon has expanded its advertising supported models to lower entry costs further attracting price sensitive buyers. The inclusion of Alexa voice assistant capabilities adds value for smart home management and hands free usage. By leveraging its extensive digital content library Amazon creates a sticky ecosystem that encourages long term engagement. The company also focuses on durability for kids editions reducing replacement frequency for parents. These strategies allow Amazon to dominate the entry level segment and drive revenue through subscriptions and digital content sales rather than hardware profits alone ensuring sustained market relevance.

Top Strategies Used by Key Market Participants

Key players in the U.S. tablet market primarily employ ecosystem integration and product differentiation strategies to sustain competitiveness. Companies focus on creating seamless connectivity between tablets smartphones and laptops to enhance user stickiness and reduce churn. This approach encourages consumers to remain within a single brand environment for all their digital needs. Manufacturers also invest heavily in research and development to introduce unique features such as advanced stylus support and high refresh rate displays. Subscription based services including cloud storage and streaming platforms are bundled with hardware to generate recurring revenue streams. Strategic partnerships with educational institutions and enterprise clients help secure bulk orders and long term contracts. Marketing campaigns emphasize productivity and creativity to position tablets as essential work tools rather than just media consumption devices. Sustainability initiatives including recycled materials and trade in programs appeal to environmentally conscious buyers. Continuous software updates and security enhancements build trust and extend device lifespan. These multifaceted strategies enable companies to navigate market saturation and maintain growth in a mature industry.

MARKET SEGMENTATION

This research report on the U.S. tablet market is segmented and sub-segmented into the following categories.

By Distribution channel

- Offline

- Online

By Type

- Hybrid

- Convertible

- Slate

- Rugged

By Os

- iOS

- Android

- Windows

- Others

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

1.What is driving the growth of the U.S. tablet market?

The growth of the U.S. tablet market is driven by increasing demand for portable computing devices, rising adoption of digital learning, and growing usage of tablets for entertainment and remote work.

2.Which types of tablets are popular in the U.S. market?

Detachable tablets, slate tablets, and rugged tablets are among the most popular tablet types used across consumer and commercial applications in the United States.

3.How is remote work influencing the U.S. tablet market?

The rise of remote and hybrid work environments has increased demand for lightweight, high performance tablets that support productivity and mobile connectivity.

4.What role does the education sector play in the U.S. tablet market?

Educational institutions are increasingly adopting tablets for digital classrooms, online learning, and interactive educational content, contributing significantly to market growth.

5.Which operating systems are commonly used in tablets in the U.S.?

Android, iOS, and Windows are the most widely used operating systems in tablets across the U.S. market.

6.How are technological advancements impacting the tablet industry?

Advancements such as 5G connectivity, improved battery life, AI integration, enhanced displays, and stylus support are improving tablet functionality and user experience.

7.What are the major challenges faced by the U.S. tablet market?

High competition from laptops and smartphones, shorter replacement cycles, and pricing pressures are key challenges affecting the tablet market.

8.How is e commerce contributing to tablet sales in the United States?

E commerce platforms have expanded consumer access to tablets by offering competitive pricing, wider product selections, and convenient purchasing options.

9.Which sectors are major users of tablets in the U.S.?

Major sectors using tablets include education, healthcare, retail, enterprise, logistics, and entertainment industries.

10.Who are the key participants in the U.S. tablet market?

Major companies operating in the U.S. tablet market include Apple Inc., Samsung Electronics Co. Ltd., Lenovo Group Ltd., Microsoft Corp., and Amazon.com Inc.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com