U.S. Telecom Market Size, Share, Trends & Growth Forecast Report By End User, By Type, By Application, By Technology, and By Country (California, Washington, Oregon, New York & Rest of the United States) – Industry Analysis and Forecast, 2026 to 2034

U.S. Telecom Market Size

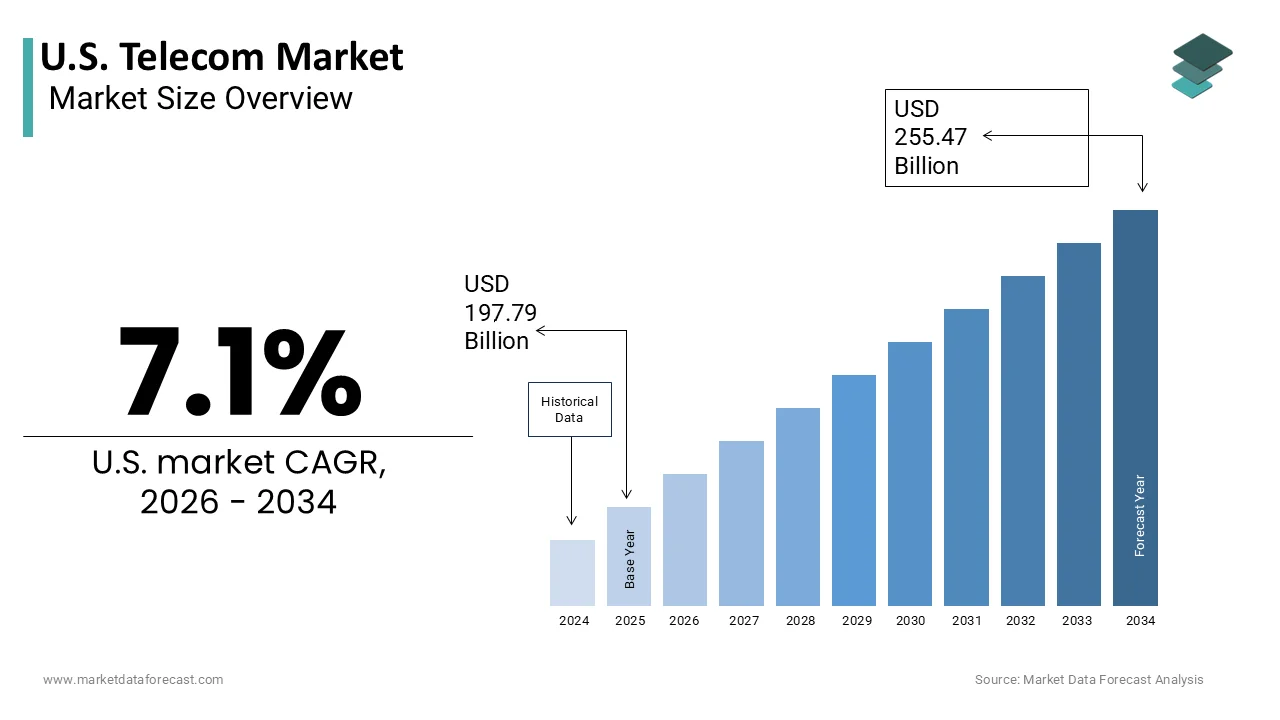

The U.S. Telecom Market was valued at USD 197.79 billion in 2025, is estimated to reach USD 147.58 billion in 2026, and is projected to reach USD 255.47 billion by 2034, growing at a CAGR of 7.1% from 2026 to 2034.

The United States is likely to maintain its position as a global leader in digital infrastructure over the next few years, as providers accelerate the transition from legacy copper to advanced fiber and 5G networks. As per data from the Federal Communications Commission, approximately 95% of Americans have access to fixed broadband services at speeds of at least 25 Mbps download and 3 Mbps upload, reflecting significant progress in infrastructure deployment. The proliferation of mobile devices has further intensified demand, with the Pew Research Center noting that 90% of American adults own a smartphone, which serves as the primary interface for digital engagement. The transition from legacy copper networks to fiber optic and fifth-generation wireless technologies defines the current operational paradigm. According to the Bureau of Labor Statistics, the number of telecommunications equipment installers and repairers is projected to decline 4% through 2033, yet the sector evolves towards specialized technical roles requiring advanced skills in network architecture and cybersecurity. The integration of Internet of Things devices into homes and industries adds complexity to network management, requiring robust and scalable solutions. This market is not merely a utility provider, but a strategic enabler of digital transformation, influencing productivity, innovation, and social connectivity across the nation.

MARKET DRIVERS

Rapid Deployment of Fifth-Generation Wireless Networks

The rapid deployment of fifth-generation wireless networks that offer significantly higher speeds, lower latency, and greater capacity than previous generations is primarily driving the expansion of the U.S. telecom market. This technological leap enables new applications, such as autonomous vehicles, remote surgery, and immersive augmented reality experiences that require real-time data transmission. According to the CTIA, the wireless industry invested $42.1 billion in network infrastructure in 2023 alone, with a substantial portion dedicated to fifth-generation rollout. According to the data from the Federal Communications Commission, fifth-generation coverage now reaches over 90% of the U.S. population, driving adoption among consumers and enterprises. The ability of these networks to support massive machine-type communications facilitates the expansion of the Internet of Things ecosystem, where billions of devices connect simultaneously. Telecommunications providers are leveraging this technology to offer fixed wireless access as an alternative to traditional broadband, particularly in rural areas where fiber deployment is costly. The competitive landscape among major carriers accelerates investment and innovation, ensuring continuous improvement in service quality. This infrastructure upgrade also supports industrial automation and smart city initiatives, creating new revenue streams beyond consumer subscriptions. The strategic importance of fifth-generation technology for national competitiveness further motivates regulatory support and private sector investment. This widespread adoption sustains growth and modernization within the telecom sector.

Surging Demand for High Bandwidth Content and Cloud Services

The U.S. telecommunications sector is likely to see an unprecedented rise in data traffic over the next few years, driven by the expansion of 4K and 8K streaming and sophisticated cloud-based AI tools. Consumers are increasingly consuming ultra-high-definition video streaming, online gaming, and virtual reality content, which requires substantial data throughput and low latency. According to the Nielsen Company, streaming reached a record-breaking 40.3% of total TV usage in the U.S. in June 2024, with video accounting for the majority of traffic. Data from Sandvine indicates that video services constitute over 60% of downstream internet traffic in North America, placing immense pressure on network capacity. Enterprises are also migrating workloads to cloud platforms, requiring reliable and secure connectivity for mission-critical applications. The shift towards remote work and hybrid models has further amplified the need for high-quality home broadband connections. Telecommunications providers are responding by upgrading their networks with fiber optic technology and advanced compression techniques to handle this load efficiently. The integration of content delivery networks closer to end users reduces latency and improves user experience. This trend drives continuous capital expenditure on network enhancements and expansion. The reliance on digital services for entertainment, education, and work ensures sustained demand for high-performance telecommunications infrastructure. This consumption pattern underpins the economic viability of network investments.

MARKET RESTRAINTS

High Capital Expenditure Requirements for Infrastructure Upgrades

The high capital expenditure required for infrastructure upgrades that strain financial resources and impact profitability is a key impediment to the U.S. telecom market growth. Deploying fiber optic networks and fifth-generation wireless infrastructure involves significant costs related to equipment, labor, and right-of-way acquisitions. According to the USTelecom Industry Broadband Scorecard, the industry has invested more than $2.2 trillion in communications networks since 1996, with annual investments reaching record levels. Data from the Federal Reserve Bank of St. Louis indicates that interest rate increases have raised the cost of borrowing for telecommunications companies, making large-scale investments more expensive. The long payback period for these investments creates financial pressure, particularly for smaller providers and rural cooperatives. Regulatory requirements, such as environmental assessments and permitting processes, further delay projects and increase costs. The need to maintain legacy systems while building new networks adds to the operational burden. Competition among providers often leads to price wars, which compress margins and limit funds available for reinvestment. The financial risk associated with unproven technologies or uncertain demand can deter investment in innovative solutions. These economic constraints slow down the pace of modernization and limit the reach of advanced services to underserved areas. Balancing investment needs with financial sustainability remains a critical challenge for the industry.

Regulatory Complexity and Permitting Bottlenecks

The growth of the U.S. telecom market is further restrained by regulatory complexity and permitting bottlenecks that delay infrastructure deployment and increase operational costs. Telecommunications providers must navigate a patchwork of federal, state, and local regulations governing zoning, environmental protection, and historic preservation. According to the Government Accountability Office, it can take two years or more for some broadband providers to obtain federal authorizations to deploy on federal lands, due to inconsistent local rules. As per the data from the Federal Communications Commission, streamlined permitting guidelines have been issued,d but implementation varies widely across municipalities. The lack of standardized procedures creates uncertainty and inefficiency for providers planning nationwide rollouts. Legal challenges and community opposition to new towers or fiber lines further complicate project timelines. Compliance with diverse safety and aesthetic standards requires additional engineering and administrative resources. The fragmentation of regulatory authority means that providers must engage with thousands of local governments, each with unique requirements. This administrative burden diverts resources from network construction and maintenance. Delays in permitting slow down the introduction of new services and hinder competition. Until regulatory frameworks are harmonized and streamlined, these bureaucratic hurdles will continue to impede the efficient expansion of telecommunications infrastructure.

MARKET OPPORTUNITIES

Expansion of Fixed Wireless Access in Rural Areas

The expansion of fixed wireless access in rural areas is a potential opportunity for the U.S. telecom market. Fifth-generation technology offers a viable alternative for delivering high-speed broadband to underserved communities without the need for extensive trenching and cabling. According to the Federal Communications Commission, approximately 14% of people in rural areas lack access to terrestrial fixed broadband at speeds of 100/20 Mbps, making it an attractive solution for rural connectivity. Data from the Rural Utilities Service indicates that millions of households in rural America lack access to adequate broadband, creating a substantial market potential. Telecommunications providers are leveraging their existing wireless infrastructure to offer home internet services, targeting these unserved and underserved populations. Government subsidies and grant programs, such as the Broadband Equity Access and Deployment program, provide financial incentives for expanding rural coverage. The ability to rapidly deploy fixed wireless solutions allows providers to capture market share quickly and generate recurring revenue. This approach also supports digital inclusion initiatives by connecting schools, libraries, and healthcare facilities in remote areas. The growing acceptance of wireless technology as a reliable broadband option enhances its appeal to consumers. By addressing the rural digital divide, telecommunications companies can unlock new growth avenues and contribute to national connectivity goals.

Integration of Internet of Things and Smart City Solutions

The integration of the Internet of Things and smart city solutions that create new revenue streams beyond traditional connectivity services is another promising opportunity for the U.S. telecom market. Telecommunications providers are positioning themselves as key enablers of smart infrastructure by offering managed services for connected devices and data analytics. According to the International Data Corporation, global spending on the Internet of Things is expected to reach $1.1 trillion by 2028, with the U.S. being a major contributor to this growth. Data from the National League of Cities shows that municipalities are increasingly investing in smart technologies for traffic management, public safety, and energy efficiency. Telecommunications companies can partner with local governments to deploy sensor networks and communication platforms that support these initiatives. The ability to provide end-to-end solutions, including device management, security, and data processing, adds value for enterprise and government clients. The emergence of private fifth-generation networks for industrial applications offers further opportunities for customization and premium services. By leveraging their network expertise and customer relationships, providers can diversify their business models. This strategic shift towards solution provision enhances customer stickiness and opens up high-margin service categories. The convergence of connectivity and digital services positions telecommunications firms as central players in the digital economy.

MARKET CHALLENGES

Cybersecurity Threats and Network Vulnerabilities

The U.S. telecom market is likely to face more aggressive cyber-attacks over the next few years, necessitating a shift toward zero-trust architectures and AI-driven threat detection. A major challenge confronting the U.S. telecom market is the increasing frequency and sophistication of cybersecurity threats, which pose risks to network integrity and customer data. Telecommunications infrastructure is a critical target for cybercriminals and state-sponsored actors seeking to disrupt services or steal sensitive information. According to the Federal Bureau of Investigation, recorded ransomware attacks in the U.S. increased by 18% in 2023, with telecommunications being a key sector at risk. Data from the Cybersecurity and Infrastructure Security Agency highlights that supply chain vulnerabilities in network equipment can expose providers to significant security risks. The transition to software-defined networks and cloud-based architectures expands the attack surface, requiring robust security measures. Protecting against distributed denial-of-service attacks and data breaches requires continuous investment in advanced security technologies and personnel. The interconnected nature of telecom networks means that a breach in one area can have cascading effects across the system. Compliance with evolving security regulations adds complexity and cost to operations. Customer trust is paramount, and any security incident can damage reputation and lead to churn. The need to balance openness and innovation with security and resilience is a persistent operational challenge. Providers must adopt a proactive security posture to mitigate these risks effectively.

Workforce Shortages and Skills Gap

The U.S. telecom market faces significant challenges due to workforce shortages and a skills gap, which hinder the deployment and maintenance of advanced networks. The rapid evolution of technology requires workers with specialized skills in fiber optics, fifth-generation technology, and network security, which are in short supply. According to the Bureau of Labor Statistics, employment in the telecommunications industry is projected to decline slightly, yet the industry faces difficulties in recruiting qualified technicians and engineers despite competitive wages. Data from the Information Technology Industry Council indicates that the skills gap is widening, as educational institutions struggle to keep pace with technological advancements. The aging workforce in the sector exacerbates the issue, as experienced professionals retire without adequate replacements. Training new employees takes time and resources, delaying project timelines and increasing costs. The competition for talent with other technology sectors further intensifies the recruitment challenge. The lack of skilled labor can compromise the quality of network installations and maintenance, leading to service disruptions. Addressing this shortage requires collaboration between industry, educators, and policymakers to develop targeted training programs. Apprenticeships and vocational training initiatives are essential for building a sustainable pipeline of workers. Until the workforce crisis is resolved, it will remain a bottleneck for industry growth and innovation.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By End User, Type, Application, Technology, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, United States |

| Market Leaders Profiled | AT&T Inc., Verizon Communications Inc., T-Mobile US, Inc., Comcast Corporation, Charter Communications, Inc., Lumen Technologies, Inc., Cox Communications, Inc., Altice USA, Inc., Frontier Communications Parent, Inc., Dish Network Corporation, Cisco Systems, Inc., Nokia Corporation |

SEGMENTAL ANALYSIS

By End User Insights

The consumer segment dominated the market by holding the largest share of the U.S. telecom market in 2025. The dominance of the consumer segment in the U.S. market is driven by the ubiquitous penetration of mobile devices and the insatiable demand for data consumption among individuals. Smartphones have become essential tools for communication, entertainment, and daily life management, resulting in a vast subscriber base. According to the Pew Research Center, approximately 90% of American adults own a smartphone, which serves as the primary access point for telecommunications services. This high level of device ownership translates directly into sustained demand for wireless voice and data plans. Data from the CTIA indicates that there were 558 million wireless subscriber connections in the U.S. in 2023, which exceeds the total population due to multiple device ownership per person. Consumers are increasingly consuming high-bandwidth content, such as streaming video and online gaming, which requires robust and unlimited data packages. The average monthly data usage per smartphone user has grown exponentially, forcing carriers to continuously upgrade network capacity. The reliance on mobile connectivity for social interaction and information access ensures that consumer spending remains the largest component of telecom revenue. The competitive landscape among carriers focuses heavily on attracting and retaining individual subscribers through bundled services and promotional offers. This mass market appeal and constant need for connectivity solidify the dominance of the consumer segment.

On the other hand, the business segment is anticipated to showcase the fastest CAGR in the U.S. market during the forecast period, due to the accelerated digital transformation and the widespread adoption of cloud computing solutions across enterprises. Companies are migrating critical applications and data storage to cloud platforms, requiring secure, high-speed, and low-latency connectivity. According to the International Data Corporation, global spending on digital transformation is forecast to reach $3.9 trillion by 2027, as businesses prioritize operational efficiency. Data from Flexera indicates that 89% of organizations have a multi-cloud strategy, necessitating a robust telecommunications infrastructure to support these workflows. Telecom providers are responding by offering specialized enterprise-grade services, such as software-defined wide area networks and dedicated fiber connections. These solutions ensure reliable performance for mission-critical applications and real-time collaboration tools. The shift towards remote and hybrid work models has further increased the demand for secure corporate networks that connect distributed teams. Businesses are investing in advanced cybersecurity measures integrated with their telecom services to protect sensitive data. The need for scalable and flexible connectivity solutions drives continuous upgrades and expansions. This strategic reliance on digital infrastructure positions the business segment as a key growth engine for the telecom industry.

By Type Insights

The wireless segment led the market by capturing the leading share of the U.S. telecom market in 2025. The growth of the wireless segment in the U.S. market is attributed to the pervasive mobile-first behavior of consumers who prioritize convenience and connectivity on the go. Smartphones have replaced landlines as the primary communication device for most Americans, enabling seamless access to voice and data services anywhere. According to the National Center for Health Statistics, 77.6% of adults lived in wireless-only households as of late 2023, reflecting the decline of wired voice services. Data from the Federal Communications Commission shows that wireless subscriptions significantly outnumber wireline connections, highlighting the preference for mobile connectivity. The ability to access internet services, social media, and entertainment applications from mobile devices drives continuous usage and data consumption. Wireless networks have evolved to offer speeds comparable to fixed broadband, making them a viable primary internet source for many users. The proliferation of mobile apps for banking, shopping, and communication reinforces the reliance on wireless infrastructure. Carriers invest heavily in network expansion and enhancement to meet this demand, ensuring broad coverage and high performance. The flexibility and mobility offered by wireless services align with modern lifestyles characterized by movement and multitasking. This consumer preference ensures that wireless remains the dominant type of telecommunications service.

On the other side, the wireline segment is experiencing rapid growth and is predicted to showcase a promising CAGR in the U.S. market during the forecast period, owing to the increasing demand for high-capacity fiber optic infrastructure to support bandwidth-intensive applications. Fiber optic technology offers superior speed, reliability, and symmetry compared to copper-based connections, making it ideal for modern digital needs. According to the Fiber Broadband Association, fiber providers in the U.S. passed a record 9 million new homes in 2023, as providers expand their footprints. Data from the American Community Survey shows that fiber availability is increasing in both urban and rural areas, bridging the digital divide. Consumers and businesses are seeking fiber connections to support activities such as 4K video streaming, large file transfers, and video conferencing, which require stable and high-speed connections. Telecommunications companies are investing heavily in fiber-to-the-home projects to replace aging copper infrastructure and meet future demand. Government initiatives and funding programs are also accelerating fiber deployment in underserved communities. The longevity and scalability of fiber networks make them a preferred investment for long-term infrastructure development. As data consumption continues to rise, the need for robust wireline connections ensures sustained growth in this segment.

By Application Insights

The residential segment held the highest share of the U.S. telecom market in 2025. The growth of the residential segment in the U.S. market can be credited to the high household penetration of broadband services and the essential nature of internet connectivity for daily life. Almost every household in the U.S. requires internet access for education, work, entertainment, and communication. According to the Pew Research Center, 80% of American adults have high-speed broadband service at home, indicating widespread adoption. Data from the Federal Communications Commission shows that broadband subscription rates remain high across various demographic groups, reflecting its status as a basic utility. The reliance on internet-connected devices, such as smart TVs, gaming consoles, and home security systems, drives continuous demand for residential broadband. Families require reliable connections to support multiple users and devices simultaneously, increasing the need for higher-speed plans. The shift towards remote learning and telehealth has further cemented the importance of home internet access. Telecom providers focus on capturing residential customers through competitive pricing and bundled offerings. The large number of households in the U.S. provides a substantial base for residential telecom services. This universal need for connectivity ensures that the residential segment remains the largest application area.

However, the commercial segment is the fastest-growing area in the U.S. telecom market due to the widespread adoption of software-defined wide area networks by businesses. SD-WAN technology allows organizations to manage and optimize their network connections more efficiently and cost-effectively than traditional methods. According to Gartner, by 2026, 60% of new SD-WAN purchases will be part of a single-vendor secure access service edge (SASE) offering to support their digital transformation initiatives. Data from IDC shows that spending on SD-WAN infrastructure is growing rapidly, as businesses seek to improve application performance and security. This technology enables companies to use multiple types of connections, including broadband and wireless, to create a resilient and flexible network. Telecom providers are offering managed SD-WAN services to help businesses navigate the complexity of implementation and maintenance. The ability to prioritize critical applications and ensure secure access to cloud resources drives adoption. The shift towards cloud-based operations requires dynamic network management, which SD-WAN provides. This technological advancement creates new opportunities for telecom operators to offer value-added services to commercial clients. The efficiency and scalability of SD-WAN solutions ensure sustained growth in the commercial segment.

By Technology Insights

The fourth-generation LTE technology segment accounted for the major share of the U.S. telecom market in 2025 due to its established infrastructure and widespread coverage availability across the country. LTE networks have been deployed for over a decade, providing reliable and high-speed connectivity for the majority of mobile users. According to the CTIA, 4G LTE networks cover 99% of the U.S. population, ensuring consistent access to voice and data services. Data from Opensignal shows that LTE remains the most widely used technology for mobile internet access, despite the rollout of fifth-generation networks. The maturity of LTE technology means that devices and network equipment are widely available and cost-effective. Most smartphones and mobile devices are optimized for LTE performance, ensuring a smooth user experience. The extensive coverage of LTE makes it the backbone of current mobile communications, supporting billions of data transactions daily. Telecom providers continue to maintain and optimize their LTE networks to ensure reliability and capacity. The widespread adoption of LTE-based applications and services reinforces its dominance. Until fifth-generation coverage becomes equally ubiquitous, LTE will remain the primary technology for mobile connectivity.

The fifth-generation technology segment is anticipated to register the fastest CAGR in the U.S. market during the forecast period, owing to its superior speed and low-latency capabilities that enable new applications and experiences. Fifth-generation networks offer data speeds up to 100 times faster than fourth-generation LTE and latency as low as one millisecond. According to the Federal Communications Commission, 5G technology is a key component of the American economy, expected to contribute $1.5 trillion to U.S. GDP. Data from Speedtest by Ookla shows that fifth-generation download speeds are significantly higher than LTE averages, enhancing user satisfaction. These performance improvements attract early adopters and tech-savvy consumers who demand the best possible connectivity. The ability to handle massive amounts of data simultaneously supports the growth of the Internet of Things and smart cities. Telecom providers are marketing fifth-generation as a premium service, differentiating themselves in a competitive market. The technology enables new business models and services that were not possible with previous generations. The continuous expansion of fifth-generation coverage and device availability drives rapid adoption. The transformative potential of fifth-generation technology ensures its status as the fastest-growing segment.

COUNTRY LEVEL ANALYSIS

U.S. Telecom Market Analysis

The United States is likely to maintain its position as the world's most innovative telecom market over the next few years, as it leads the global push toward Open RAN and 6G research. The U.S. stands as the largest and most advanced telecommunications market in North America, accounting for the majority of regional revenue and innovation. The country serves as a global leader in network technology deployment and digital service adoption, influencing trends worldwide. According to the World Bank, 92% of the U.S. population used the internet as of 2022, reflecting its mature digital ecosystem. The market status is characterized by intense competition among major carriers and continuous investment in next-generation infrastructure. The presence of leading technology companies and telecom operators drives rapid innovation and service improvement. Data from the International Telecommunication Union indicates that the U.S. ranks highly in global connectivity indices, demonstrating its robust telecommunications framework. The mature nature of the market means that growth is driven by technology upgrades and value-added services, rather than simple subscriber additions. The U.S. also leads in the development of fifth-generation standards and applications, setting benchmarks for other nations. This leadership position ensures that the U.S. market remains the primary focus for strategic investments and product launches. The stability and size of the market provide a foundation for long-term industry resilience and global influence.

COMPETITIVE LANDSCAPE

The competition in the U.S. telecom market is intense and characterized by three major national carriers vying for dominance through network quality and service innovation. Verizon, AT&, and T-Mobile lead the sector while smaller regional providers and cable companies compete in specific niches. Price competition is fierce with carriers offering promotional deals and bundled services to attract and retain subscribers. Network performance serves as a primary differentiator as companies invest billions in fifth-generation infrastructure to offer superior speed and latency. The rise of fixed wireless access has introduced new competitive dynamics, allowing wireless providers to challenge traditional cable broadband monopolies. Customer service quality and digital engagement platforms are critical for building brand loyalty in a saturated market. Regulatory policies regarding spectrum allocation and net neutrality influence competitive strategies and market entry barriers. Mergers and acquisitions have consolidated the industry, leaving fewer but larger players with significant resources. Innovation in enterprise solutions and Internet of Things connectivity offers new revenue streams beyond consumer subscriptions. This dynamic environment requires continuous investment and strategic agility to sustain market position and achieve long-term profitability.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the U.S. telecom market include

- AT&T Inc.

- Verizon Communications Inc.

- T-Mobile US, Inc.

- Comcast Corporation

- Charter Communications, Inc.

- Lumen Technologies, Inc.

- Cox Communications, Inc.

- Altice USA, Inc.

- Frontier Communications Parent, Inc.

- Dish Network Corporation

- Cisco Systems, Inc.

- Nokia Corporation

TOP LEADING PLAYERS IN THE MARKET

- Verizon Communications maintains a leading position in the U.S. telecom market through its extensive wireless network and fiber optic infrastructure. The company focuses on delivering high-speed connectivity and reliable service to consumer and business segments. Recent strategic actions include aggressive expansion of its fifth-generation ultra-wideband network to cover more urban and suburban areas. Verizon has invested heavily in spectrum acquisitions to enhance network capacity and performance. The company also promotes its fixed wireless access service as a competitive alternative to traditional broadband. By integrating advanced technologies like edge computing, Verizon supports enterprise digital transformation initiatives. These efforts reinforce its reputation for network quality and reliability. Verizon continues to prioritize customer experience through digital tools and personalized service offerings. This consistent focus on infrastructure excellence strengthens its market presence.

- AT&T Inc contributes significantly to the U.S. telecom landscape by providing comprehensive wireless and fiber-based communication services. The company leverages its vast network assets to offer bundled solutions for residential and commercial clients. Recent initiatives involve accelerating the deployment of fiber to the home premises across multiple states to increase broadband availability. AT&T has streamlined its portfolio to focus on core connectivity businesses after divesting media assets. The company is enhancing its fifth-generation network with mid-band spectrum to improve speed and coverage. AT&T also emphasizes network security and managed services for enterprise customers. By investing in network modernization and customer-centric innovations, AT&T aims to drive growth. These strategic moves ensure it remains a key player in the evolving telecommunications industry.

- T-Mobile U.S. plays a vital role in the U.S. telecom sector by challenging established competitors with innovative pricing and network expansion. The company has grown its subscriber base through aggressive marketing and superior customer service initiatives. Recent actions include the continued integration of Sprint network assets to enhance coverage and capacity. T-Mobile is expanding its fifth-generation network reach to rural areas through government-funded programs. The company offers unique perks such as streaming service bundles to attract and retain customers. T-Mobile also focuses on enterprise solutions, including Internet of Things connectivity. By leveraging its merged network capabilities, T T-Mobile delivers improved performance and value. This strategy has strengthened its competitive position and brand loyalty among diverse consumer segments nationwide.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS IN THE MARKET

Key players in the U.S. telecom market primarily focus on expanding fifth-generation network coverage to enhance speed and reliability for users. Companies are investing heavily in spectrum acquisitions to secure the necessary bandwidth for future growth. Strategic bundling of wireless and fiber services helps increase customer retention and average revenue per user. Partnerships with technology firms enable the development of innovative enterprise solutions and Internet of Things applications. Emphasis on customer experience through digital platforms and personalized support drives brand loyalty. Cost optimization measures, including network automation and operational efficiency improvement,s protect margins. Expansion into fixed wireless access provides an alternative to traditional broadband in underserved areas. These strategies enable firms to maintain competitiveness and drive sustainable growth in a dynamic industry landscape.

MARKET SEGMENTATION

This research report on the U.S. telecom market is segmented and sub-segmented into the following categories.

By End User

- Consumer

- Business

By Type

- Wireless

- Wireline

By Application

- Residential

- Commercial

By Technology

- Fourth Generation LTE (4G LTE)

- Fifth Generation (5G)

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com