U.S Ventilator Market Size, Share, Trends & Growth Forecast Report Segmented By Type (Adult, Paediatric & Neonatal), Interface, End User, And Country (California, Washington, Oregon, New York & Rest Of The United States) – Industry Analysis And Forecast, 2026 To 2034

U.S. Ventilator Market Report Summary

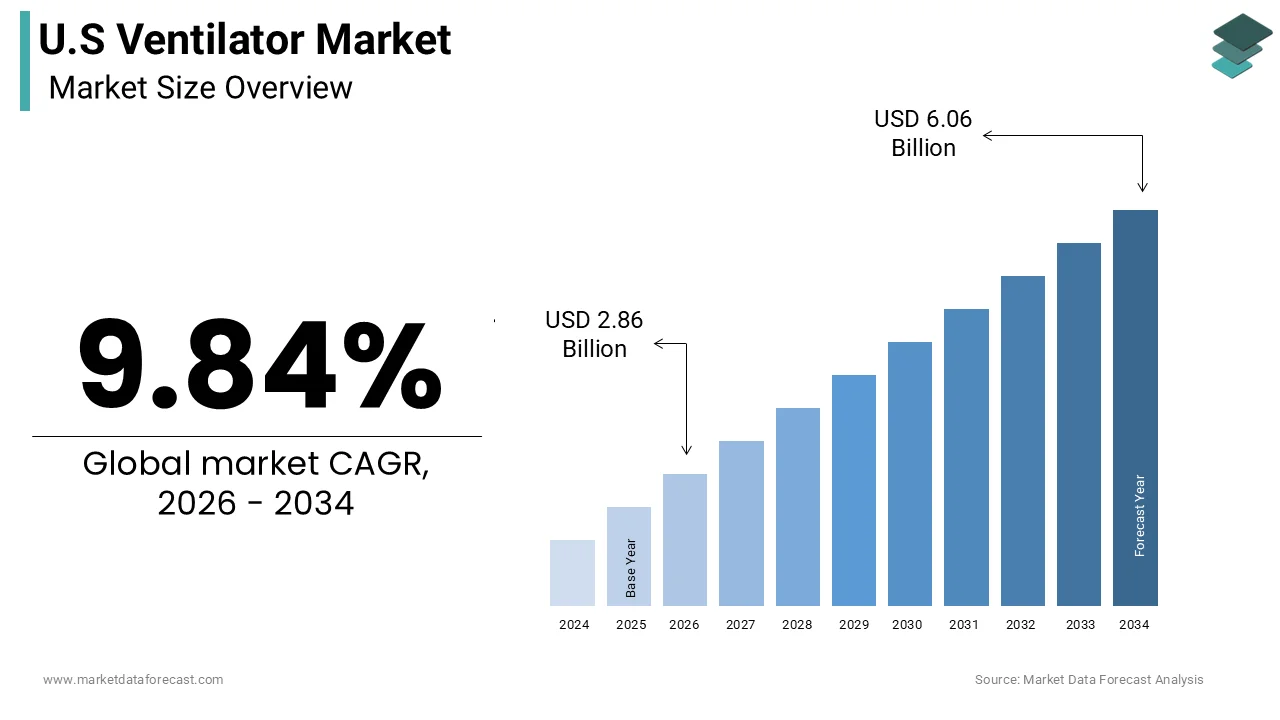

The United States ventilator market was valued at USD 2.60 billion in 2025 and is projected to reach USD 6.06 billion by 2034, growing from USD 2.86 billion in 2026 at a CAGR of 9.84% during the forecast period. Market growth is driven by the increasing prevalence of respiratory disorders, rising demand for critical care infrastructure, and advancements in respiratory support technologies. The growing aging population, expansion of intensive care facilities, and increasing adoption of portable ventilators are further supporting the growth of the U.S. ventilator market.

Key Market Trends

- Rising prevalence of chronic respiratory diseases and sleep apnea

- Increasing demand for portable and home-care ventilators

- Growth in ICU and emergency care infrastructure

- Expansion of AI-enabled and smart ventilator technologies

- Increasing focus on non-invasive respiratory support solutions

Segmental Insights

- Based on type, the adult ventilators segment dominated the U.S. ventilator market in 2025 by accounting for 71.7% of the market share, driven by high hospitalization rates among the adult and elderly population

- Based on interface, the invasive ventilation segment held the leading share in 2025 due to its extensive use in intensive care units and critical respiratory treatment

- Based on end user, the hospitals segment occupied the major share of the market in 2025, supported by growing ICU admissions and advanced healthcare infrastructure

Regional Insights

- United States is expected to maintain a dominant position in the global respiratory care market due to advanced healthcare systems, strong medical device adoption, and increasing investments in critical care technologies

Competitive Landscape

- The U.S. ventilator market is highly competitive, with companies focusing on advanced respiratory technologies, portability, and smart monitoring systems. Market players are investing in AI-based ventilation support, remote patient monitoring, and compact ventilator designs to strengthen their market presence.

- Prominent players in the U.S. ventilator market include Medtronic, GE HealthCare, Philips Healthcare, ResMed, Dräger, Hamilton Medical, Vyaire Medical, Getinge, Smiths Medical, Airon Corporation, Allied Healthcare Products, Becton Dickinson, Fisher & Paykel Healthcare, Zoll Medical, and Mindray.

U.S Ventilator Market Size

The U.S. ventilator market was valued at USD 2.60 billion in 2025, is estimated to reach USD 2.86 billion in 2026, and is projected to reach USD 6.06 billion by 2034, growing at a CAGR of 9.84% from 2026 to 2034.

According to the Centers for Disease Control and Prevention, chronic lower respiratory diseases remain the fifth leading cause of death in the United States, highlighting the persistent burden of pulmonary conditions. As per the American Lung Association, approximately 16 million adults have been diagnosed with chronic obstructive pulmonary disease, creating a substantial base for long-term ventilation needs. The Food and Drug Administration regulates ventilators as Class II medical devices, ensuring strict adherence to safety and performance standards through premarket notification processes. Technological advancements, such as adaptive support ventilation and integrated monitoring systems, have enhanced clinical outcomes by minimizing ventilator-induced lung injury. The National Institutes of Health emphasizes the importance of precise tidal volume delivery and pressure support in managing acute respiratory distress syndrome. This market is characterized by a shift toward portable and home-based solutions, driven by the aging population and the prevalence of neuromuscular disorders. The integration of telemedicine capabilities allows for remote patient monitoring, improving management of chronic respiratory conditions outside hospital settings. This landscape is defined by the critical need for reliable respiratory support across acute and post-acute care environments.

MARKET DRIVERS

Rising Prevalence of Chronic Respiratory Diseases and Aging Population

The escalating incidence of chronic respiratory conditions, combined with demographic shifts toward an older population, is one of the major factors propelling the growth of the U.S. ventilator market. According to the Centers for Disease Control and Prevention, chronic lower respiratory diseases affect millions of Americans, with chronic obstructive pulmonary disease accounting for a significant portion of these cases. As per the American Lung Association, approximately 6.5% of adults in the United States have been diagnosed with COPD, reflecting the widespread nature of this debilitating condition. The U.S. Census Bureau projects that the population aged sixty-five and older will reach ninety-five million by 2060, nearly doubling from 2016 levels. Older adults are disproportionately affected by respiratory decline due to reduced lung elasticity and increased susceptibility to infections. Furthermore, the prevalence of comorbidities, such as heart failure and diabetes, exacerbates respiratory complications requiring mechanical support. According to the National Institute on Aging, age-related changes in respiratory muscle strength necessitate intervention during acute exacerbations. The increasing incidence of asthma and interstitial lung disease further expands the patient pool requiring ventilation therapy. This demographic reality ensures a consistent and growing base of patients needing both acute and long-term ventilatory assistance. Healthcare providers must invest in diverse ventilator types to manage the complexity of care for multimorbid patients. Consequently, the structural growth of the elderly population creates a robust and enduring demand trajectory for ventilator technologies.

Increased Incidence of Acute Respiratory Distress Syndrome and Critical Care Needs

The high incidence of acute respiratory failures and the critical need for intensive care support significantly propel the adoption of advanced ventilator systems, which further contribute to the U.S. market expansion. According to the Society of Critical Care Medicine, acute respiratory distress syndrome affects approximately two hundred thousand adults annually in the United States, with mortality rates remaining significant despite advances in care. As per clinical data, severe pneumonia, sepsis, and trauma are leading causes of ARDS, requiring immediate mechanical ventilation to maintain oxygenation. The COVID-19 pandemic highlighted the essential role of ventilators in managing viral pneumonias, leading to increased stockpiling and infrastructure investment in hospitals. The Centers for Medicare and Medicaid Services reports that intensive care unit admissions for respiratory failures have risen, prompting facilities to upgrade their ventilator fleets. Furthermore, advancements in lung protective ventilation strategies have improved survival rates, encouraging earlier and more aggressive intervention. According to the American Thoracic Society, guidelines emphasize the use of low tidal volume ventilation to prevent ventilator-induced lung injury, driving the adoption of sophisticated modes. Hospitals are increasingly investing in high-end critical care ventilators, with advanced monitoring capabilities, to meet these clinical standards. The need for rapid response in emergency departments and operating rooms also drives demand for portable and transport ventilators. This clinical urgency, combined with evolving treatment protocols, ensures sustained procurement of ventilator systems across acute care settings.

MARKET RESTRAINTS

High Cost of Advanced Ventilators and Reimbursement Constraints

The substantial capital expenditure required for acquiring advanced ventilator systems, combined with restrictive reimbursement policies, is primarily hampering the U.S. market expansion. According to hospital industry data, the average cost of an ICU ventilator ranges between $10,000 and $50,000, while specialized neonatal units can cost significantly more. As per the Centers for Medicare and Medicaid Services, reimbursement rates for mechanical ventilation services have remained stagnant or declined in real terms, despite rising operational costs. Healthcare providers face pressure to justify large equipment purchases through volume and efficiency, which is challenging in value-based care models. Private insurers often impose prior authorization requirements for home ventilation equipment, limiting patient access and creating administrative burdens. According to the Medical Group Management Association, many smaller community hospitals operate on thin margins, making it difficult to fund capital upgrades without incurring significant debt. Furthermore, the total cost of ownership includes maintenance contracts, disposable circuits, and specialized training, which adds to the financial burden. These economic constraints force providers to delay replacements or opt for refurbished equipment, slowing the adoption of new technologies. According to industry analyses, rural hospitals are particularly vulnerable to these financial pressures, limiting their ability to provide comprehensive respiratory care. Consequently, high upfront costs and uncertain reimbursement landscapes act as persistent restraints on market expansion, particularly for resource-constrained facilities.

Shortage of Respiratory Therapists and Clinical Staff

The persistent shortage of qualified respiratory therapists and critical care nurses poses a significant barrier to the effective utilization of ventilator systems, which is further impeding the U.S. ventilator market growth. According to the American Association for Respiratory Care, over 92,000 respiratory therapists are projected to leave the profession by 2030, due to an aging workforce and insufficient training pipeline capacity. As per the Bureau of Labor Statistics, employment of respiratory therapists is projected to grow, but supply remains insufficient to meet rising demand, particularly in rural and underserved areas. The operation of advanced ventilators requires specialized knowledge of pulmonary physiology and device mechanics, which takes years to develop. Without skilled staff, the risk of ventilator-associated complications, such as pneumonia and barotrauma, increases significantly. The Society of Critical Care Medicine notes that nurse-to-patient ratios in intensive care units impact the quality of ventilator management and patient outcomes. Furthermore, the high-stress environment of critical care leads to burnout and turnover, exacerbating staffing challenges. According to industry surveys, many healthcare facilities report difficulties in recruiting and retaining experienced staff, leading to increased overtime costs and reliance on temporary agencies. This labor constraint limits the effective utilization of installed base equipment and hinders the adoption of complex new technologies. Consequently, the workforce shortage acts as a persistent restraint on market growth and operational efficiency.

MARKET OPPORTUNITIES

Expansion of Home Non-Invasive Ventilation and Telehealth Integration

The growing adoption of home non-invasive ventilation and the integration of telehealth technologies offer a substantial opportunity for market expansion. According to the American Lung Association, the number of patients requiring long-term ventilation at home is increasing due to the prevalence of neuromuscular diseases and severe COPD. As per industry developments, manufacturers are developing portable and user-friendly non-invasive ventilators that enhance patient comfort and compliance. The integration of wireless connectivity allows for remote monitoring of ventilation parameters, enabling clinicians to adjust settings without in-person visits. The Centers for Medicare and Medicaid Services has expanded reimbursement for remote patient monitoring services, encouraging the use of connected devices. According to the National Institutes of Health, telehealth interventions reduce hospital readmissions and improve the quality of life for patients with chronic respiratory failure. Furthermore, the rise of direct-to-consumer health services facilitates access to home ventilation equipment and supplies. According to market analyses, the home care segment is expected to grow at a faster rate than the hospital segment, due to these trends. Manufacturers focusing on compact designs and intuitive interfaces can capture this growing market niche. This shift toward decentralized care creates new revenue streams and improves patient autonomy. Consequently, the convergence of technology and home care models positions non-invasive ventilation as a key growth area.

Technological Advancements in Smart Ventilation and AI

The incorporation of artificial intelligence and smart ventilation algorithms offers significant potential for enhancing clinical outcomes and operational efficiency, which is another promising opportunity for the U.S. market. According to the Society of Critical Care Medicine, AI-driven ventilators can automatically adjust support levels based on real-time patient effort and lung mechanics, reducing the workload on clinicians. As per industry developments, manufacturers are embedding machine learning models into ventilator software to predict weaning readiness and detect adverse events early. The Food and Drug Administration has cleared several intelligent ventilation modes, fostering innovation and clinical adoption. According to research published in the Journal of Critical Care, AI-assisted ventilation reduces the duration of mechanical ventilation and length of stay in intensive care units. Furthermore, the integration of electronic health records allows for seamless data transfer and comprehensive patient monitoring. The American Thoracic Society highlights that personalized ventilation strategies improve survival rates and reduce complications. Manufacturers leveraging these technologies can differentiate their products and offer value-added solutions that enhance clinical workflow. This technological convergence transforms ventilators from passive support devices into intelligent therapeutic partners. By providing predictive insights and automated adjustments, smart ventilators address the staffing shortage challenge. Consequently, the adoption of AI-driven systems creates robust growth opportunities for innovative manufacturers.

MARKET CHALLENGES

Risk of Ventilator-Associated Pneumonia and Complications

The potential for ventilator-associated pneumonia and other complications is a significant clinical and financial challenge to the U.S. market. According to the Centers for Disease Control and Prevention, ventilator-associated pneumonia affects between 5% and 40% of patients receiving invasive mechanical ventilation for more than two days, leading to prolonged hospital stays and increased mortality. As per the Society for Healthcare Epidemiology of America, VAP is one of the most common healthcare-associated infections in intensive care units, resulting in substantial additional costs. The complexity of preventing VAP requires strict adherence to bundles of care, including head of bed elevation and oral hygiene, which can be difficult to maintain consistently. Furthermore, prolonged mechanical ventilation can lead to diaphragm dysfunction and muscle weakness, complicating the weaning process. According to the American Journal of Respiratory and Critical Care Medicine, ventilator-induced lung injury remains a concern despite protective strategies. Manufacturers must invest in features, such as heated humidification and closed suction systems, to mitigate these risks. However, the implementation of these technologies adds to the cost and complexity of care. According to industry analyses, hospitals face penalties for high rates of healthcare-associated infections, creating financial pressure. Consequently, managing complications and ensuring patient safety remain critical challenges for the ventilator market, affecting both clinical practice and economic outcomes.

Supply Chain Vulnerabilities and Component Shortages

Global supply chain disruptions and shortages of critical components pose significant challenges to the expansion of the U.S. ventilator market. According to the U.S. Department of Commerce, the medical device industry relies heavily on global suppliers for semiconductors, sensors, and specialized plastics, which are subject to geopolitical tensions and logistical bottlenecks. As per the Semiconductor Industry Association, the ongoing chip shortage has impacted the production of sophisticated ventilators, leading to extended lead times. The concentration of manufacturing in specific regions increases exposure to natural disasters and trade restrictions. According to the Bureau of Labor Statistics, inflationary pressures on raw materials and transportation costs have elevated production expenses, squeezing profit margins for manufacturers. These cost increases are often passed on to healthcare providers, potentially dampening demand. Furthermore, the lack of domestic manufacturing capacity for certain critical components creates dependencies that compromise supply security. According to the Advanced Medical Technology Association, diversifying supply chains requires significant capital investment and time, which many companies find challenging. The unpredictability of supply availability complicates inventory management and planning, affecting the ability to meet sudden spikes in demand during health crises. Consequently, supply chain instability remains a persistent challenge, affecting market consistency and accessibility.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 9.84% |

| Segments Covered | By Type, Interface, End User, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado. |

| Market Leaders Profiled | Medtronic, GE HealthCare, Philips Healthcare, ResMed, Dräger, Hamilton Medical, Vyaire Medical, Getinge, Smiths Medical, Airon Corporation, Allied Healthcare Products, Becton, Dickinson and Company (BD), Fisher & Paykel Healthcare, Zoll Medical, Mindray |

SEGMENTAL ANALYSIS

By Type Insights

The adult ventilators segment dominated the market by capturing the highest share of 71.7% of the U.S. market in 2025. The dominance of the adult ventilator segment in the U.S. market is mainly driven by the substantial burden of chronic respiratory diseases among the adult population. According to the Centers for Disease Control and Prevention, chronic lower respiratory diseases were the fifth leading cause of death in the United States in 2024, affecting millions of adults annually. As per the American Lung Association, approximately sixteen million adults have been diagnosed with chronic obstructive pulmonary disease, which frequently progresses to require mechanical ventilation during exacerbations. The aging demographic further amplifies this demand, with the U.S. Census Bureau projecting that individuals aged sixty-five and older will comprise 21% of the population by 2040. Older adults are more susceptible to pneumonia and acute respiratory distress syndrome, necessitating intensive care intervention. According to the Society of Critical Care Medicine, adult intensive care units account for the majority of ventilator days in hospitals, due to the complexity of comorbidities such as heart failure and diabetes. Furthermore, the rising incidence of obesity related hypoventilation syndrome contributes to the need for long-term ventilatory support. This convergence of high disease prevalence, demographic shifts, and clinical necessity ensures that adult ventilators remain the primary revenue driver in the market. Healthcare providers must maintain robust fleets of adult ventilators to manage the consistent volume of respiratory failures.

However, the paediatric and neonatal ventilators segment is estimated to showcase a CAGR of 9.2% during the forecast period in the U.S. market, owing to the advancements in neonatal care and increasing survival rates of premature infants. The improving survival rates of premature infants and advancements in neonatal intensive care significantly drive expansion in this segment. According to the Centers for Disease Control and Prevention, approximately 10.41% of babies were born preterm in the United States in 2025, requiring specialized respiratory support. As per the March of Dimes, preterm birth complications are the leading cause of death in children under five years old, necessitating immediate ventilation in many cases. Modern neonatal ventilators offer gentle ventilation modes, such as high-frequency oscillatory ventilation, which minimizes lung injury in fragile infants. The National Institutes of Health highlights that technological innovations in non-invasive support have improved outcomes for infants with respiratory distress syndrome. Furthermore, the increasing use of surfactant therapy, combined with precise ventilator management, has enhanced survival rates for extremely low birth weight infants. According to the American Academy of Pediatrics, specialized neonatal intensive care units are expanding capacity to meet the needs of high-risk pregnancies. This clinical progress drives hospitals to invest in state-of-the-art neonatal ventilators. The focus on minimizing long-term developmental impacts also encourages the adoption of sophisticated monitoring features. Consequently, the emphasis on neonatal survival and quality of life positions this segment for rapid growth.

By Interface Insights

The invasive ventilation segment led the market by holding the leading share of the U.S. market in 2025. The growth of the invasive ventilation segment in the U.S. market is attributed to the insertion of an endotracheal tube or tracheostomy to deliver air directly into the lungs. The critical nature of acute respiratory failure and the need for secure airway management significantly sustain the dominance of invasive ventilation. According to the Society of Critical Care Medicine, at least 25% of people in a hospital setting require mechanical ventilation due to conditions like acute respiratory distress syndrome. As per clinical guidelines, invasive ventilation provides superior control over tidal volume and pressure compared to non-invasive methods in unstable patients. According to the Centers for Disease Control and Prevention, invasive mechanical ventilation is essential for patients with compromised consciousness or the inability to protect their airway. Furthermore, surgical procedures requiring general anesthesia necessitate invasive ventilation to maintain respiratory function during the operation. According to the American Society of Anesthesiologists, millions of surgeries annually rely on endotracheal intubation for safe anaesthetic delivery. In trauma cases, invasive ventilation allows for suctioning of secretions and prevention of aspiration, which is critical for patient survival. For instance, intensive care units prioritize invasive ventilators for their reliability and versatility in managing complex cases. This clinical necessity for secure and controlled respiratory support ensures that invasive ventilation remains the standard of care for critically ill patients.

On the other hand, the non-invasive ventilation segment is estimated to showcase the fastest CAGR of 11.4% during the forecast period in the U.S. market, owing to the shift toward home care and avoidance of intubation risks. The increasing preference for home-based care and the desire to avoid complications associated with intubation further significantly drive expansion in this segment in the U.S. market. According to the American Lung Association, non-invasive ventilation is increasingly used for managing chronic obstructive pulmonary disease and sleep apnea in home settings. As per clinical studies, non-invasive ventilation reduces the risk of ventilator-associated pneumonia and shortens hospital stays, compared to invasive methods. The Centers for Medicare and Medicaid Services has expanded coverage for home non-invasive devices, encouraging patient adoption. Furthermore, the comfort and convenience of mask-based interfaces improve patient compliance and quality of life. According to the National Sleep Foundation, nearly 38% of adults in the United States are at an increased risk for sleep apnea, driving consistent demand for non-invasive devices. The portability of modern non-invasive ventilators allows patients to maintain active lifestyles while receiving therapy. According to market analyses, the rise of telehealth enables remote monitoring of home users, enhancing safety and efficacy. This shift toward decentralized and patient-centric care positions non-invasive ventilation as the fastest-growing segment in the U.S. market.

By End User Insights

The hospitals segment occupied the major share of the U.S. ventilator market in 2025. The high volume of critically ill patients and extensive critical care infrastructure in hospitals is contributing to the dominance of the hospital segment in the U.S. market. According to the American Hospital Association, U.S. hospitals operate over eighty thousand intensive care beds, requiring a vast array of ventilator systems. As per the Society of Critical Care Medicine, hospitals manage the majority of acute respiratory failure cases requiring immediate and complex ventilatory support. The presence of emergency departments and operating rooms further drives demand for both critical care and anaesthesia ventilators. The Centers for Medicare and Medicaid Services reimburses hospitals for critical care services, ensuring financial viability for maintaining large fleets. Furthermore, hospitals serve as trauma centers and referral hubs for complex cases, necessitating advanced ventilator capabilities. According to industry analyses, the capital budget of hospitals supports regular upgrades and expansion of respiratory care units. The concentration of specialized staff, such as pulmonologists and respiratory therapists, facilitates efficient utilization of equipment. This institutional scale and clinical complexity ensure that hospitals remain the primary consumers of ventilator technology.

On the other hand, the specialty clinics segment is predicted to showcase the fastest CAGR of 10.4% during the forecast period in the U.S. market, owing to the shift toward outpatient respiratory care and sleep centers. The proliferation of sleep disorder centers and outpatient respiratory clinics significantly drives expansion in this segment. According to the American Academy of Sleep Medicine, the number of accredited sleep centers has increased significantly to address the rising prevalence of sleep apnea. As per industry data, these clinics primarily utilize non-invasive ventilators for diagnosis and treatment, driving consistent equipment sales. The Centers for Disease Control and Prevention notes that outpatient care is becoming preferred for managing chronic respiratory conditions, due to cost efficiency. Specialty clinics offer focused expertise and personalized care, attracting patients seeking alternatives to hospital visits. According to market analyses, the convenience of local clinics reduces travel burden for patients requiring regular therapy adjustments. Furthermore, the integration of pulmonary rehabilitation programs in specialty clinics increases the utilization of ventilatory support devices. The ability to provide comprehensive care, including testing, fitting, and follow-up in one location, enhances patient satisfaction. This focus on specialized and accessible care positions specialty clinics as a high-growth segment.

REGIONAL ANALYSIS

The United States is expected to maintain its leadership in the global respiratory care market through the next few years by holding the highest share of the U.S. market in 2025 due to the convergence of advanced healthcare infrastructure, high healthcare expenditure, and a strong culture of critical care innovation. According to the American Hospital Association, the U.S. has the highest number of intensive care beds per capita globally, ensuring broad access to mechanical ventilation. As per the Centers for Medicare and Medicaid Services, the U.S. spends more on healthcare per capita than any other nation, enabling widespread adoption of advanced ventilator technologies. The presence of leading medical device manufacturers and research institutions fosters a dynamic innovation ecosystem. The Food and Drug Administration maintains a rigorous yet efficient regulatory pathway that encourages the launch of new ventilator models. According to the National Institutes of Health, federal funding for respiratory research supports the development of novel ventilation strategies. Furthermore, the fee-for-service payment model historically incentivized the adoption of high-technology equipment, although this is shifting toward value-based care. The combination of financial capacity, regulatory clarity, and industrial strength ensures that the United States remains the largest and most influential market for ventilators globally.

COMPETITION OVERVIEW

The United States ventilator market features intense competition among global medical technology corporations and specialized device manufacturers. Established players leverage extensive distribution networks, brand recognition, and clinical expertise to maintain leadership, while emerging companies differentiate through innovative portable technologies and artificial intelligence integration. Competition centers on precision and ease of use, with companies investing billions in research to develop adaptive ventilation modes and automated weaning tools. Pricing strategies vary significantly, with premium brands emphasizing comprehensive feature sets and value-oriented competitors focusing on affordability and durability. The shift toward home-based respiratory care drives demand for compact and connected devices, creating new competitive dynamics. Patent protection and intellectual property rights remain critical battlegrounds as firms seek to protect proprietary algorithms and sensor designs. Strategic collaborations with software developers and telehealth platforms accelerate product enhancement and market entry. Regulatory compliance and cybersecurity standards serve as key differentiators, ensuring patient safety and data privacy. This dynamic environment fosters continuous innovation, improving clinical outcomes while companies strive for sustainable growth and market relevance in a highly regulated sector.

KEY MARKET PLAYERS

A few major players of the U.S ventilator market include

- Medtronic

- GE HealthCare

- Philips Healthcare

- ResMed

- Dräger

- Hamilton Medical

- Vyaire Medical

- Getinge

- Smiths Medical

- Airon Corporation

- Allied Healthcare Products

- Becton

- Dickinson and Company (BD)

- Fisher & Paykel Healthcare

- Zoll Medical

- Mindray

Leading Players in the U.S. Ventilator Market

- Medtronic plc maintains a prominent position in the United States ventilator market through its comprehensive portfolio of critical care and respiratory care solutions. The company leverages advanced technology to deliver precise ventilation support for neonatal, pediatric, and adult patients. Medtronic recently strengthened its market position by enhancing its Puritan Bennett ventilator series with improved connectivity and data integration capabilities. The company actively collaborates with healthcare providers to optimize clinical workflows and patient outcomes. Medtronic also invests heavily in research and development to advance non-invasive ventilation technologies. These initiatives reinforce its commitment to innovation while addressing diverse respiratory needs across hospitals and home care settings in the U.S. healthcare system.

- Getinge AB contributes significantly to the U.S. ventilator market with its Servo line of intensive care ventilators, known for precision and reliability. The company utilizes proprietary lung protective ventilation strategies to minimize ventilator-induced lung injury and improve patient safety. Getinge recently expanded its digital health offerings by integrating artificial intelligence-driven monitoring tools into its ventilator platforms. The company strengthens its position by partnering with academic institutions to validate clinical efficacy and support education. Furthermore, Getinge focuses on sustainability in its manufacturing processes and supply chain operations. These efforts demonstrate its dedication to advancing critical care standards while maintaining a strong presence in acute care environments across the United States.

- Hamilton Medical AG plays a pivotal role in the U.S. ventilator market with its intelligent ventilation systems designed for automated respiratory support. The company is renowned for its ASV adaptive support ventilation mod,e which personalizes therapy based on patient physiology. Hamilton Medical recently announced significant investments in expanding its service network and training programs for U.S. healthcare professionals. The company actively pursues collaborations with telehealth providers to enhance remote patient monitoring capabilities. Hamilton Medical also emphasizes user-friendly interfaces and robust durability in its device design. Through sustained innovation and strategic expansion, the company reinforces its leadership in providing smart and efficient ventilation solutions that address critical respiratory challenges in the United States.

Top Strategies Used by Key Market Participants

Key players in the United States ventilator market employ strategic approaches to maintain competitive advantages and drive growth. Companies prioritize technological innovation by integrating artificial intelligence and machine learning into ventilation algorithms for enhanced patient safety. Strategic partnerships with healthcare providers facilitate the adoption of smart ventilation systems in diverse clinical settings. Manufacturers invest heavily in research and development to create portable and non-invasive devices that expand access to care. Regulatory compliance and quality assurance initiatives ensure the safety and efficacy of new products. Digital transformation efforts focus on cloud connectivity and data analytics to improve workflow efficiency. Market participants also emphasize education and training programs to support clinicians. These coordinated strategies enable companies to navigate complex regulatory environments while delivering high-value respiratory solutions to diverse healthcare sectors effectively.

MARKET SEGMENTATION

This research report on the US ventilator market has been segmented and sub-segmented based on type, interface, end user & region.

By Type

- Adult

- Paediatric & Neonatal

By Interface

- Invasive

- Non-invasive

By End User

- Hospitals

- Specialty Clinics

- Others

By Region

- New York

- Texas

- Florida

- Georgia

- California

- Rest of U.S.

Frequently Asked Questions

1. What factors are driving the growth of the U.S. ventilator market?

Key growth drivers include the increasing prevalence of chronic respiratory diseases, aging population, technological advancements, and higher demand for emergency and intensive care services.

2. Which types of ventilators are most commonly used in the United States?

Critical care ventilators, portable ventilators, neonatal ventilators, and transport ventilators are among the most commonly used types in the U.S. healthcare system.

3. What are the major applications of ventilators in healthcare settings?

Ventilators are widely used in intensive care units (ICUs), emergency departments, operating rooms, ambulatory care centers, and home healthcare environments.

4. Which end users dominate the U.S. ventilator market?

Hospitals and critical care centers are the leading end users due to the high number of respiratory emergency cases and surgical procedures.

5. What technological advancements are shaping the ventilator market?

Innovations such as AI-assisted monitoring, touchscreen interfaces, wireless connectivity, and smart alarm systems are improving ventilator efficiency and patient care.

6. What challenges are affecting the U.S. ventilator market?

High equipment costs, strict regulatory requirements, supply chain disruptions, and maintenance complexities are major challenges faced by manufacturers and healthcare providers.

7. Which companies are leading the U.S. ventilator market?

Major companies include Medtronic, GE HealthCare, Philips Healthcare, ResMed, Dräger, Hamilton Medical, and Vyaire Medical.

8. What role does home healthcare play in ventilator market growth?

Home healthcare is becoming increasingly important as more patients with chronic respiratory conditions prefer long-term treatment at home using portable ventilation devices.

9. How is artificial intelligence being integrated into ventilator systems?

AI technologies help optimize airflow settings, monitor patient conditions in real time, and improve clinical decision-making for better treatment outcomes.

10. What is the future outlook for the U.S. ventilator market?

The market is expected to grow steadily in the coming years due to increasing respiratory heal

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com