U.S. Weight Loss Market Size, Share, Trends & Growth Forecast Report Segmented By Service Type (Digital Weight-Loss Programs, Fitness Centres & Health Clubs, Slimming / Commercial Weight-Loss Centres, Consulting & Coaching Services, Medical Weight-Loss Programs (non-surgical)), Delivery Mode and Country – Industry Analysis From 2026 to 2034

U.S. Weight Loss Market Report Summary

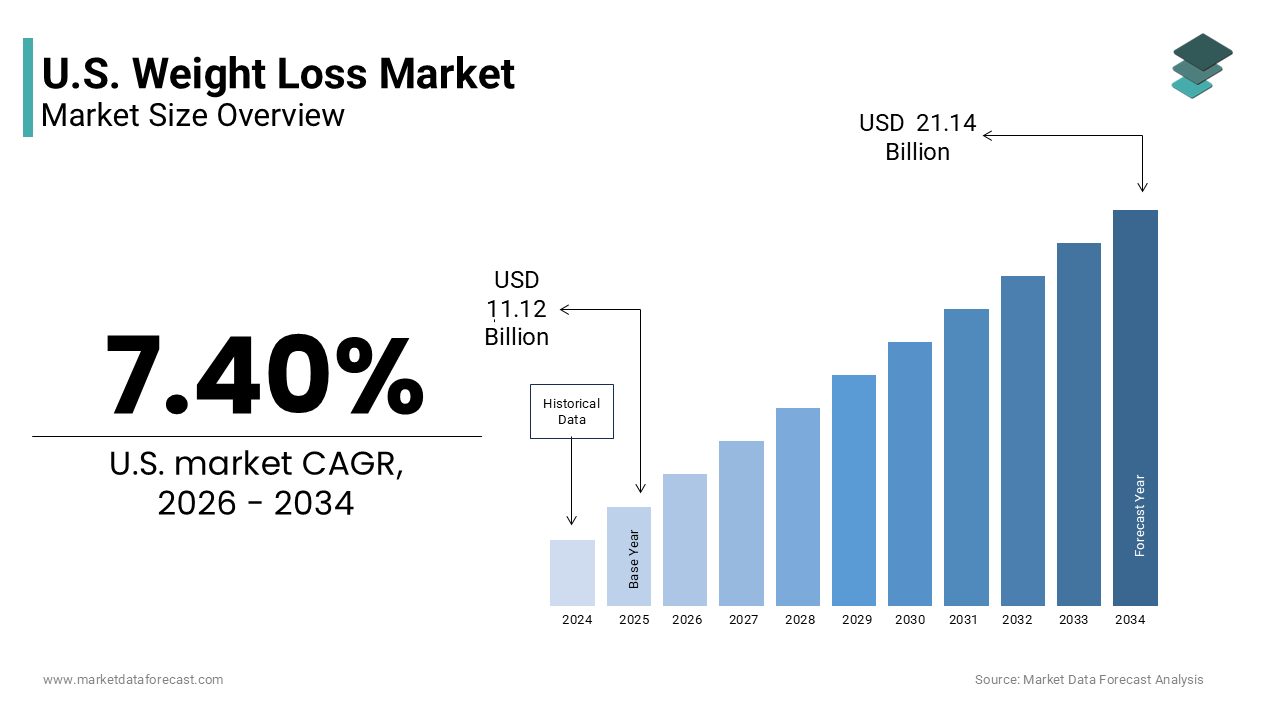

The U.S. weight loss market was valued at USD 11.12 billion in 2025, is estimated to reach USD 11.94 billion in 2026, and is projected to reach USD 21.14 billion by 2034, growing at a CAGR of 7.40% during the forecast period from 2026 to 2034. The growth of the U.S. weight loss market is driven by the rising prevalence of obesity and obesity-related health conditions, increasing consumer awareness regarding health and wellness, and growing adoption of medically supervised weight management programs. The increasing popularity of digital health platforms, fitness applications, and personalized nutrition programs is further accelerating market expansion. Additionally, advancements in anti-obesity medications, increasing employer-sponsored wellness initiatives, and rising demand for convenient and technology-driven weight management solutions are contributing to the growth of the market.

Key Market Trends

- Rising adoption of digital weight loss platforms, AI-powered health tracking applications, and virtual coaching services

- Increasing demand for GLP-1 receptor agonists and medically supervised weight management treatments

- Growing popularity of personalized nutrition plans, wearable fitness devices, and holistic wellness programs

- Strong focus on preventive healthcare and employer-sponsored corporate wellness initiatives

- Expansion of online and mobile app-based weight loss services offering flexible and accessible solutions

Segmental Insights

- Based on service type, the fitness centres and health clubs segment accounted for the largest share of the U.S. weight loss market in 2025. The segment’s dominance is attributed to the growing consumer preference for structured fitness environments, availability of certified trainers, and increasing integration of wellness services such as nutritional counseling and personalized exercise programs.

- The digital weight loss programs segment is anticipated to witness the fastest growth during the forecast period owing to the rising smartphone penetration, increasing use of wearable health devices, and growing demand for convenient and personalized virtual weight management solutions.

- Based on delivery mode, the on-site and in-person services segment dominated the U.S. weight loss market in 2025 due to the higher levels of accountability, personalized coaching, and strong social support associated with in-person weight management programs and fitness services.

- The online and mobile app-based services segment is projected to grow at a significant pace during the forecast period owing to the increasing adoption of telehealth, digital coaching platforms, AI-powered nutrition guidance, and flexible subscription-based wellness solutions.

Regional Insights

The U.S. weight loss market is witnessing strong growth across California, Washington, Oregon, New York, and the rest of the United States, supported by the high prevalence of obesity, increasing healthcare expenditure, rising awareness regarding preventive healthcare, and strong adoption of digital wellness technologies. California remains one of the major regional markets owing to its large health-conscious population, strong fitness culture, and high adoption of advanced wellness and digital health solutions.

Competitive Landscape

The U.S. weight loss market is highly competitive and characterized by the presence of pharmaceutical companies, digital health providers, fitness organizations, nutrition companies, and wellness coaching platforms competing through innovation, personalized services, and technology integration. Companies are increasingly focusing on AI-powered wellness platforms, advanced anti-obesity medications, personalized nutrition programs, hybrid coaching models, and strategic partnerships with healthcare providers and employers to strengthen their market position and improve customer engagement.Prominent players in the U.S. weight loss market include WW International Inc., Herbalife Nutrition Ltd., Nutrisystem Inc., Jenny Craig Inc., Medifast Inc., Noom Inc., Abbott Laboratories, Nestlé Health Science, Johnson & Johnson, Novo Nordisk, Eli Lilly and Company, and Atkins Nutritionals Inc.

U.S. Weight Loss Market Size

The U.S. weight loss market size was valued at USD 11.12 billion in 2025 and is anticipated to reach USD 11.94 billion in 2026 from USD 21.14 billion by 2034, growing at a CAGR of 7.40% during the forecast period from 2026 to 2034.

The prevalence of obesity serves as the foundational context for this market and as per the Centers for Disease Control and Prevention, the prevalence of U.S. adults age 20 and older with obesity was 40.3% between August 2021 and August 2023. This high incidence rate creates a sustained demand for effective weight management solutions across diverse demographic groups. Furthermore, according to the Centers for Disease Control and Prevention, another 31.7% of adults are classified as overweight, which indicates that approximately 72% of American adults are either overweight or obese. These health metrics drive both consumer initiated efforts and physician recommended treatments. The cultural emphasis on physical appearance and wellness further amplifies market activity, as individuals seek aesthetic improvements alongside health benefits. Technological advancements in digital health platforms have also transformed accessibility, allowing users to track progress and receive personalized guidance remotely. The integration of medical expertise with consumer friendly applications has expanded the reach of weight loss interventions. As healthcare costs associated with obesity related conditions rise, there is increasing pressure from insurers and employers to support preventive measures. This multifaceted environment defines the current state of the market, where medical necessity intersects with lifestyle aspirations. The convergence of clinical innovation and consumer demand shapes the trajectory of weight loss solutions in the U.S.

MARKET DRIVERS

Rising Prevalence of Obesity Related Comorbidities Drives Medical Intervention Demand

The escalating rates of obesity related health conditions are a key factor propelling the expansion of the U.S. weight loss market. Obesity is a significant risk factor for numerous chronic diseases, including type 2 diabetes, cardiovascular disease, and certain cancers. According to the Journal of Managed Care and Specialty Pharmacy, the annual medical costs of obesity in the U.S. were estimated at $260.50 billion in 2020. This financial impact motivates healthcare systems and insurers to prioritize weight management strategies that can mitigate long term health expenses. As per the American Diabetes Association, nearly 90% of people living with type-2-diabetes are overweight or have obesity. This strong correlation drives demand for weight loss medications and programs that offer clinically proven results. Physicians are increasingly prescribing anti-obesity medications as part of comprehensive treatment plans, recognizing their potential to improve metabolic health. According to a study published in the International Journal of Obesity, only about 1.1% of eligible adults are currently being prescribed anti-obesity medications and this suggests a vast untapped potential for market growth. As awareness of the health risks associated with excess weight grows, more individuals are seeking professional guidance and evidence based solutions. This shift toward medicalized weight loss enhances the credibility and adoption of pharmaceutical and clinical interventions, driving market expansion through increased patient engagement and healthcare provider endorsement.

Growing Consumer Awareness of Health and Wellness Fuels Proactive Weight Management

Increasing consumer awareness regarding health and wellness is a significant driver propelling the U.S. weight loss market expansion as individuals adopt proactive approaches to manage their weight and overall well-being. The modern consumer is more informed about the benefits of maintaining a healthy weight, driven by extensive access to health information through digital platforms and media. According to the International Food Information Council, 57% of Americans followed a specific eating pattern or diet in 2025. This trend is further amplified by the influence of social media and fitness influencers, who promote healthy lifestyles and weight loss journeys. As per a survey by the Pew Research Center, roughly 80% of internet users have searched for a health related topic online. The desire for improved mental health and self-esteem also motivates individuals to pursue weight loss, as studies link obesity with increased risks of depression and anxiety. The American Psychological Association notes that stress and emotional well-being are closely tied to eating habits, prompting many to seek structured weight management programs that address psychological factors. Additionally, the rise of wearable technology and health tracking apps empowers consumers to monitor their progress and stay accountability. These tools provide real time feedback and personalized insights, enhancing engagement and adherence to weight loss plans. The combination of health consciousness, digital empowerment, and psychological motivation creates a robust demand for diverse weight loss solutions, ranging from dietary supplements to fitness programs and coaching services.

MARKET RESTRAINTS

High Cost of Advanced Weight Loss Treatments Limits Accessibility for Many Consumers

The substantial cost associated with advanced weight loss treatments is impeding the weight loss market growth in the U.S. Prescription medications, bariatric surgery, and specialized meal replacement programs often come with high price tags that are not fully covered by insurance plans. According to the Kaiser Family Foundation, many private insurance plans exclude coverage for weight loss medications, leaving patients to bear the full out of pocket expense. For instance, popular GLP 1 receptor agonists can cost over 1,000 dollars per month without insurance, making them unaffordable for many individuals. This financial barrier prevents widespread adoption of effective medical interventions, particularly among lower income groups who are disproportionately affected by obesity. As per the Commonwealth Fund, 38% of adults reported skipping or delaying medical care in 2023 due to cost. Even when insurance coverage is available, high deductibles and copayments can deter patients from initiating or continuing treatment. The lack of standardized coverage policies across different insurers creates confusion and inconsistency in access. Furthermore, the long term nature of weight management requires sustained financial commitment, which can be burdensome for households facing economic pressures. As per the Bureau of Labor Statistics, rising inflation and stagnant wage growth have reduced disposable income, forcing consumers to prioritize essential expenses over optional health services. This economic constraint stifles market growth by restricting the pool of potential customers who can afford premium weight loss solutions, thereby limiting the overall penetration of advanced treatments.

Regulatory Scrutiny and Safety Concerns Hinder Product Approval and Consumer Trust

Stringent regulatory oversight and persistent safety concerns are further hindering the U.S. weight loss market expansion. The Food and Drug Administration maintains rigorous standards for the approval of weight loss medications and supplements, requiring extensive clinical trials to demonstrate efficacy and safety. According to the Federal Trade Commission, numerous weight loss products face legal action for making false or misleading claims, which undermines consumer trust in the industry. High profile recalls and safety warnings for certain dietary supplements have further eroded confidence, with the Centers for Disease Control and Prevention reporting thousands of emergency department visits annually due to adverse events from weight loss supplements. These incidents highlight the risks associated with unregulated or poorly tested products, causing consumers to be cautious about trying new interventions. The lengthy approval process for new drugs also delays market entry, limiting the availability of innovative treatments. As per the Pharmaceutical Research and Manufacturers of America, it takes an average of 10 to 12 years for a new medicine to make it from the initial discovery to the marketplace. Additionally, the stigma surrounding obesity and weight loss treatments can discourage individuals from seeking help, fearing judgment or skepticism from healthcare providers. The American Medical Association emphasizes the need for greater education among physicians to address bias and improve patient care. These regulatory and social barriers create a challenging environment for market participants, requiring them to navigate complex compliance landscapes and rebuild consumer trust through transparency and evidence based practices.

MARKET OPPORTUNITIES

Integration of Digital Health Technologies Offers Personalized Weight Management Solutions

The integration of digital health technologies is a significant opportunity for the U.S. weight loss market by enabling personalized and accessible weight management solutions. Mobile applications, wearable devices, and telehealth platforms allow users to track their dietary intake, physical activity, and progress in real time, fostering greater accountability and engagement. In the U.S., the proliferation of smartphones and internet connectivity facilitates the widespread use of these technologies, reaching diverse demographic groups. As per the Pew Research Center, 90% of Americans now own a smartphone. These tools leverage artificial intelligence and machine learning to provide customized recommendations based on individual preferences and behaviors, enhancing the effectiveness of weight loss efforts. Telehealth consultations have also become more common, allowing patients to access medical advice and prescription medications from the comfort of their homes. According to the American Telemedicine Association, telehealth services have stabilized at a rate significantly higher than pre pandemic levels. Furthermore, digital platforms can integrate with electronic health records, enabling seamless communication between patients and healthcare providers. This holistic approach supports continuous monitoring and adjustment of treatment plans, leading to better outcomes. By combining convenience with personalization, digital health technologies expand the reach and impact of weight loss interventions, creating new revenue streams and enhancing user satisfaction.

Expansion into Corporate Wellness Programs Drives Institutional Demand for Weight Loss Services

The expansion of corporate wellness programs offers a substantial opportunity for the U.S. weight loss market, as employers increasingly recognize the value of investing in employee health to reduce healthcare costs and improve productivity. Companies are implementing comprehensive wellness initiatives that include weight management components, such as nutrition counseling, fitness incentives, and access to weight loss programs. According to the Society for Human Resource Management, 81% of organizations indicated that wellness programs are a part of their benefit offerings. These programs often partner with weight loss providers to offer subsidized or free services to employees, creating a stable and scalable customer base for market participants. As per research published in the Journal of Health Economics, comprehensive workplace wellness programs have the potential to return significant savings over several years through reduced health risks and healthcare spending. The focus on preventive care aligns with broader trends in healthcare reform, encouraging employers to address chronic conditions like obesity before they lead to more serious health issues. Additionally, the rise of remote work has prompted companies to explore virtual wellness solutions, expanding the reach of digital weight loss services. The National Business Group on Health reports that 60% of employers plan to increase their investment in mental and physical health resources, including weight management. This institutional demand provides a consistent revenue stream for weight loss providers and enhances brand visibility through corporate partnerships. By targeting the workplace sector, the market can tap into a large and engaged audience, driving growth through structured and supported weight loss initiatives.

MARKET CHALLENGES

Sustainability of Weight Loss Results Remains a Persistent Challenge for Long Term Success

The difficulty in maintaining long term weight loss results is a significant challenge for the U.S. weight loss market, as many individuals experience weight regain after initial success. This phenomenon often referred to as the yo-yo effect and this undermines consumer confidence and reduces the perceived value of weight loss products and services. According to a review published in Medical Clinics of North America, the majority of people who lose a significant amount of weight will regain most of it within two to five years. Biological factors such as metabolic adaptation and hormonal changes contribute to weight regain, which is making it difficult for individuals to maintain their reduced weight without ongoing support. As per the data from the American Journal of Clinical Nutrition, resting metabolic rate decreases significantly after weight loss, requiring continued dietary restriction and physical activity to prevent regain. This physiological reality challenges the effectiveness of short term diets and quick fix solutions and this often fail to address underlying behavioural and metabolic issues. The lack of long term support structures in many weight loss programs exacerbates this problem, which is leaving individuals without guidance during the maintenance phase. Furthermore, psychological factors such as stress and emotional eating can trigger relapse, complicating efforts to sustain healthy habits. According to the American Psychological Association, stress management is crucial for long term weight control, yet many programs do not adequately address this component. This challenge requires a shift toward comprehensive, lifelong approaches to weight management that include ongoing coaching, behavioral therapy, and medical monitoring. Market participants must develop strategies to support customers beyond the initial weight loss phase to ensure lasting results and customer loyalty.

Social Stigma and Psychological Barriers Impede Open Discussion and Treatment Seeking

Social stigma and psychological barriers associated with obesity is also challenging the growth of the U.S. weight loss. Negative societal attitudes toward weight can lead to feelings of shame, guilt, and low self-esteem, which prevent many people from accessing available resources. According to the Rudd Center for Food Policy and Health, weight bias and discrimination have increased by 66% over the past decade. This stigma can result in delayed or avoided medical care, as patients fear judgment or discrimination from healthcare providers. As per the Obesity Action Coalition, many individuals report experiencing bias from healthcare professionals and this can lead to poorer health outcomes. The psychological impact of stigma can also lead to disordered eating patterns and avoidance of physical activity, counteracting weight loss efforts. The American Psychological Association emphasizes that internalized weight bias is associated with higher levels of depression and anxiety, which can undermine motivation and adherence to weight management plans. Additionally, the lack of inclusive marketing and representation in weight loss advertising can alienate potential customers who do not see themselves reflected in promotional materials. This exclusionary practice limits market reach and reinforces negative stereotypes. To overcome this challenge, the industry must promote body positivity and inclusive messaging that focuses on health and well-being rather than appearance alone. Creating supportive and non-judgmental environments is essential for encouraging individuals to seek help and engage effectively with weight loss solutions.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.40% |

| Segments Covered | By Service Type, Delivery Mode and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | California, Washington, Oregon, New York, and the rest of the United States. |

| Market Leader Profiled | WW International Inc., Herbalife Nutrition Ltd., Nutrisystem Inc., Jenny Craig Inc., Medifast Inc., Noom Inc., Abbott Laboratories, Nestlé Health Science, Johnson & Johnson, Novo Nordisk, Eli Lilly and Company, and Atkins Nutritionals Inc. |

SEGMENTAL ANALYSIS

By Service Type Insights

The fitness centres and health clubs segment captured the highest share of the U.S. weight loss market in 2025. The growth of the fitness centers and health clubs segment in the U.S. market can be credited to the consumer preference for structured exercise environments that foster accountability and community. According to the Health and Fitness Association, there are approximately 30,000 to 40,000 fitness clubs in the U.S., which is serving millions of members. This extensive network ensures widespread accessibility for consumers across urban and suburban areas. Furthermore, the integration of group fitness classes and personal training services enhances user engagement and retention. As per the Health and Fitness Association, clubs that successfully implement group exercise programs often see higher member retention rates compared to those that do not. The presence of certified trainers also provides a layer of safety and expertise, which is crucial for individuals with limited exercise experience or specific health conditions. According to the American Council on Exercise, millions of sessions are led by certified professionals annually to ensure safe and effective workouts. Additionally, modern health clubs are evolving into holistic wellness hubs by offering nutritional counseling and recovery services, thereby addressing multiple aspects of weight management. This multifaceted approach creates a sticky user experience that drives consistent revenue and market leadership. The tangible nature of physical facilities also builds trust among consumers who value visible and accessible resources for their health journeys.

However, the digital weight loss programs segment is estimated to register the fastest CAGR of 21.2% during the forecast period in the U.S. market owing to the increasing adoption of mobile technology and the demand for flexible, personalized weight management solutions and the convenience and accessibility offered by digital platforms, which allow users to manage their weight from anywhere at any time. According to the Pew Research Center, 90% of Americans own a smartphone, providing a ubiquitous platform for health applications and online coaching services. This high penetration rate enables digital providers to reach a broad demographic, including younger consumers who prefer tech driven solutions. Furthermore, the use of artificial intelligence and data analytics allows these programs to offer highly customized meal plans and workout routines, enhancing effectiveness and user satisfaction. The cost effectiveness of digital programs also attracts price sensitive consumers, as they often require lower subscription fees than traditional gym memberships or in person coaching. Additionally, the integration of wearable devices with digital apps provides real time feedback and progress tracking, which motivates users to stay engaged. These technological advancements and consumer preferences position digital programs as a dynamic and rapidly expanding component of the market.

By Delivery Mode Insights

The On-site and in person services segment was the popular segment and held the largest share of the U.S. weight loss market in 2025. The dominance of this segment in the U.S. market is primarily attributed to the perceived efficacy and accountability associated with physical presence. According to a study published in the Journal of Medical Internet Research, participants in in person weight loss programs often achieve greater weight reduction compared to those in online only programs due to higher levels of accountability. This evidence reinforces the value of direct supervision and immediate feedback in achieving health goals. Furthermore, the social aspect of in person interactions fosters a sense of community and shared purpose, which enhances motivation and reduces feelings of isolation. Data from the American Psychological Association indicates that social support is a critical predictor of long term weight loss success, with individuals in group settings showing higher adherence rates. The ability to build personal relationships with coaches and peers creates a supportive environment that encourages consistency and resilience. Additionally, in person services allow for precise monitoring of physical metrics and technique correction, which minimizes the risk of injury and maximizes results. As per the National Strength and Conditioning Association, proper form instruction is essential to reduce injury risk, a benefit that is best delivered through hands on guidance. These factors collectively sustain the leadership of on-site services, particularly among individuals seeking structured and intensive weight management interventions.

However, the online and mobile app based services segment is predicted to expand at a CAGR of 22.4% during the forecast period in the U.S. market owing to the flexibility and scalability of online platforms, which eliminate geographical and temporal barriers to access. According to the American Telemedicine Association, telehealth utilization remains at levels significantly higher than pre pandemic baselines, indicating a permanent shift in consumer behavior toward virtual care. This trend extends to weight management, where users appreciate the ability to consult with nutritionists and coaches via video calls or chat interfaces. Furthermore, the gamification features embedded in many weight loss apps enhance user engagement and motivation. These features make weight loss efforts feel less like a chore and more like an engaging activity. Additionally, the affordability of online services compared to in person alternatives appeals to a broader audience, particularly younger demographics who are digital natives. The continuous improvement of app functionalities, such as image recognition for food logging and automated progress reports, further enhances the user experience. These innovations drive rapid adoption and establish online and mobile app based services as a dominant force in the future of weight loss delivery.

COUNTRY ANALYSIS

The U.S. is anticipated to maintain its status as the most significant contributor to the global weight loss industry over the next few years. This dominant position is underpinned by high prevalence rates of obesity, substantial healthcare expenditure, and a strong cultural emphasis on physical fitness and appearance. The market status in the region is characterized by intense competition among diverse providers, ranging from pharmaceutical companies to digital health startups and traditional fitness chains. A primary driving factor for this robust market is the widespread availability of advanced medical treatments and technologies. According to the Centers for Disease Control and Prevention, the adult obesity rate in the U.S. was 40.3% in the 2021 to 2023 period, creating a vast addressable population for weight loss interventions. This high demand stimulates continuous innovation and investment in new products and services. Furthermore, the presence of major industry players and research institutions fosters a dynamic ecosystem of development and commercialization. As per the Pharmaceutical Research and Manufacturers of America, the U.S. biopharmaceutical industry is a global leader in research and development, with thousands of medicines in development. The high disposable income of American consumers also enables greater spending on premium weight loss solutions, including personalized coaching and specialized dietary programs. As per the Bureau of Labor Statistics, household expenditure on health and fitness services has shown an upward trend over the past decade, reflecting a willingness to invest in well being. Additionally, the integration of weight management into corporate wellness initiatives expands market reach through employer sponsored programs. These structural and behavioral factors solidify the U.S. as the central hub for weight loss market activity and innovation.

COMPETITIVE LANDSCAPE

The competition in the U.S. weight loss market is intense and multifaceted involving pharmaceutical giants digital health startups and traditional fitness organizations. Pharmaceutical companies compete on clinical efficacy and safety profiles of their medications while navigating complex regulatory landscapes and supply chain constraints. Digital health platforms differentiate themselves through user experience personalization and integration with wearable technology to drive engagement. Traditional fitness centers and weight loss clinics focus on community building and in person support to retain members amidst rising digital alternatives. Price sensitivity remains a critical factor as consumers compare costs of subscriptions medications and services. Strategic mergers and acquisitions are common as companies seek to consolidate offerings and achieve economies of scale. Innovation in treatment modalities such as gene therapy and microbiome based solutions adds further complexity to the competitive dynamics. Regulatory changes regarding insurance coverage also significantly impact market accessibility and competitive positioning. Ultimately success depends on the ability to deliver measurable results while maintaining affordability and user satisfaction in a crowded marketplace.

KEY MARKET PLAYERS

A few of the major companies in the U.S. weight loss market include

- WW International Inc.

- Herbalife Nutrition Ltd.

- Nutrisystem Inc.

- Jenny Craig Inc.

- Medifast Inc.

- Noom Inc.

- Abbott Laboratories

- Nestlé Health Science

- Johnson & Johnson

- Novo Nordisk

- Eli Lilly and Company

- Atkins Nutritionals Inc.

Top Players in the US Market

WW International Inc

WW International Inc maintains a prominent position in the U.S. weight loss market through its comprehensive digital and community based programs. The company has rebranded from Weight Watchers to emphasize holistic wellness beyond simple scale metrics. Recent actions include the expansion of its WW Studio concept which combines in person coaching with digital tracking tools. This hybrid approach aims to enhance user engagement and retention by offering personalized support. The company also integrates health coaching and mental well being resources into its platform to address behavioral aspects of weight management. By leveraging data analytics WW provides customized meal plans and activity recommendations that adapt to individual progress. These initiatives strengthen its market presence by catering to diverse consumer preferences for flexible and supportive weight loss solutions.

Novo Nordisk A/S

Novo Nordisk A/S significantly influences the U.S. weight loss market through its innovative pharmaceutical solutions for obesity management. The company manufactures GLP 1 receptor agonists that have demonstrated high efficacy in clinical trials for weight reduction. Recent actions include scaling up manufacturing capabilities to meet surging demand for its anti obesity medications. Novo Nordisk also engages in extensive educational campaigns to reduce stigma and increase awareness among healthcare providers and patients. The company collaborates with insurance providers to improve access and affordability of its treatments. By focusing on scientific rigor and medical endorsement Novo Nordisk establishes credibility and trust in the pharmacological approach to weight loss. These efforts solidify its role as a key driver of medicalized weight management in the U.S.

Eli Lilly and Company

Eli Lilly and Company plays a critical role in the U.S. weight loss market with its advanced portfolio of metabolic disease treatments. The company develops and distributes potent injectable therapies that target multiple hormonal pathways to regulate appetite and glucose levels. Recent actions involve investing billions in new production facilities to alleviate supply constraints and ensure consistent product availability. Eli Lilly also pursues strategic partnerships with digital health platforms to integrate its medications with comprehensive lifestyle support services. The company actively participates in policy discussions to advocate for broader insurance coverage of obesity treatments. By combining pharmaceutical innovation with accessible delivery models Eli Lilly enhances patient outcomes and strengthens its competitive position in the rapidly evolving weight loss landscape.

Top Strategies Used by Key Market Participants

Key players in the U.S. weight loss market primarily utilize product innovation and strategic partnerships to maintain competitive advantages. Companies invest heavily in research and development to create more effective and convenient weight loss solutions such as next generation medications and integrated digital platforms. Collaborations with healthcare providers and insurance companies help expand access and improve reimbursement rates for treatments. Marketing strategies focus on destigmatizing obesity and promoting holistic wellness to broaden consumer appeal. Additionally firms leverage data analytics to personalize user experiences and enhance engagement through tailored recommendations. Pricing models are adapted to offer flexible subscription options that cater to varying budget constraints. These multifaceted approaches enable participants to navigate regulatory challenges and meet evolving consumer demands effectively.

MARKET SEGMENTATION

This research report on the U.S. weight loss market has been segmented based on the following categories.

By Service Type

- Digital Weight-Loss Programs

- Fitness Centres & Health Clubs

- Slimming / Commercial Weight-Loss Centres

- Consulting & Coaching Services

- Medical Weight-Loss Programs (non-surgical)

By Delivery Mode

- On-site / In-Person

- Online / Mobile App

- Hybrid

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com