Global Urinary Catheters Market Size, Share, Trends & Growth Forecast Report By Product Type (Intermittent, Foley/Indwelling, External), Application (Urinary Incontinence, Benign Prostate Hyperplasia & Prostate Surgeries, Spinal Cord Injury, Others), Catheter Coating Type (Coated, Uncoated), Gender (Male, Female), End-User (Hospitals, Clinics, Long-Term Care Facilities, Others), and Region (North America, Europe, Asia Pacific, Latin America, Middle East and Africa) – Industry Analysis, 2026 to 2034

Market Size, 2025

$3.41 BnMarket Estimate, 2026

$3.64 BnMarket Forecast, 2034

$6.11 BnCAGR, 2026–2034

6.7%Global Urinary Catheters Market Report Summary

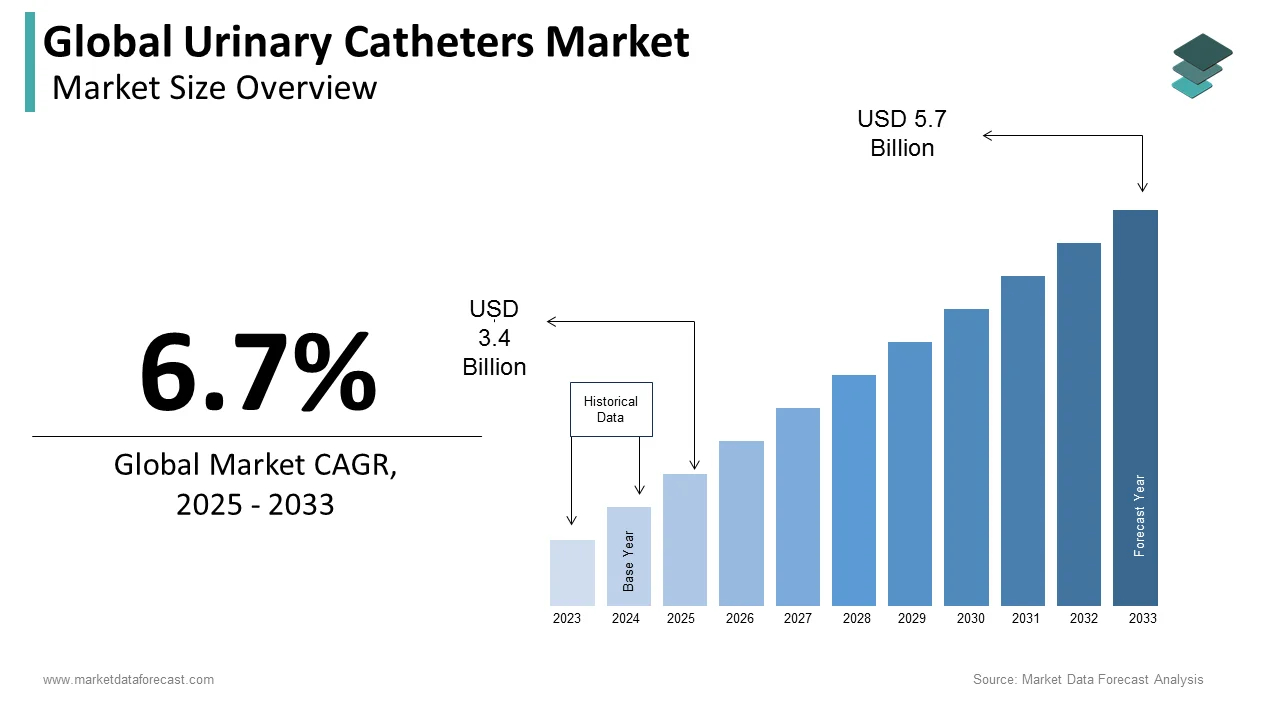

The global urinary catheters market was valued at USD 3.41 billion in 2025 and is projected to grow from USD 3.64 billion in 2026 to USD 6.11 billion by 2034, registering a CAGR of 6.7% from 2026 to 2034. Market growth is driven by the rising prevalence of urinary incontinence, increasing incidence of urological disorders, and growing demand for long-term patient care solutions. Expanding geriatric populations, rising surgical procedures, and increasing awareness regarding infection prevention and patient comfort are further supporting market expansion. Advancements in catheter materials, antimicrobial coatings, and minimally invasive urinary management technologies are also contributing to market growth globally.

Key Market Trends

- Increasing adoption of coated and antimicrobial urinary catheters to reduce catheter-associated infections.

- Rising demand for intermittent catheterization due to improved patient comfort and lower infection risks.

- Growing prevalence of urological disorders and urinary incontinence worldwide.

- Expansion of home healthcare and long-term care services.

- Continuous advancements in biocompatible materials and catheter design technologies.

Segmental Insights

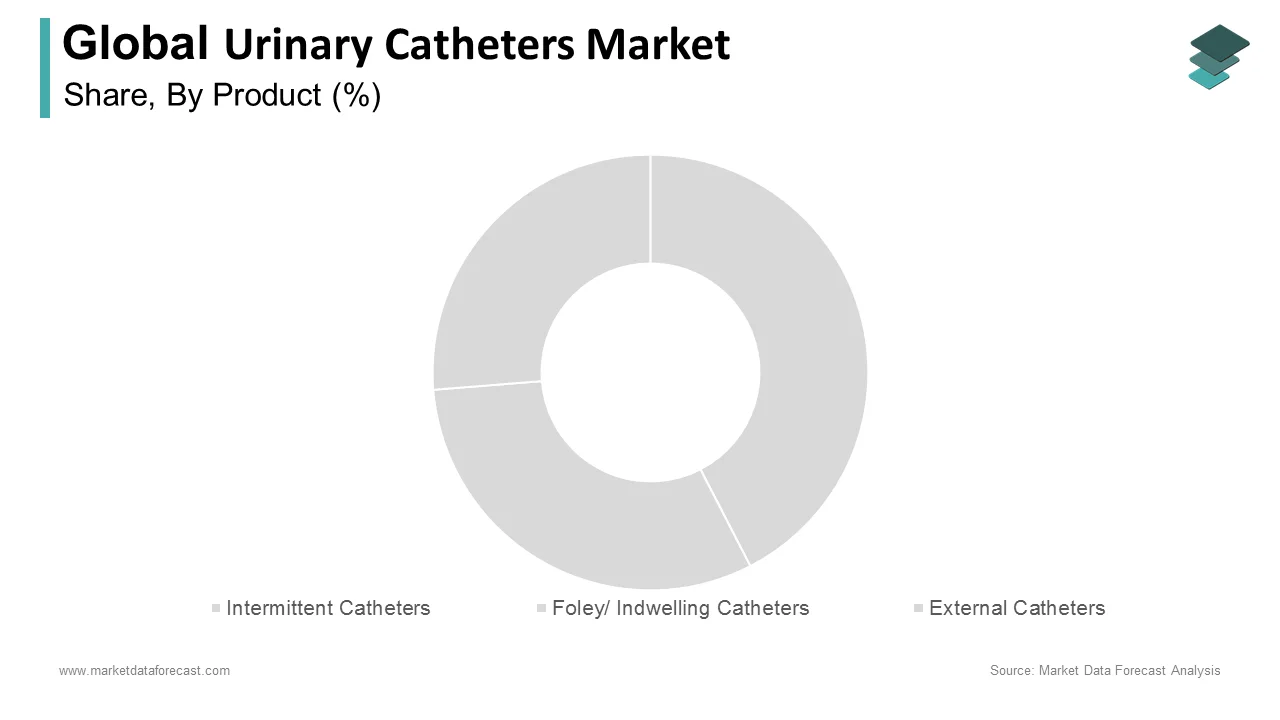

- Based on product type, the intermittent catheters segment dominated the global urinary catheters market in 2025 by accounting for 52.8% market share, driven by lower infection risk, ease of use, and increasing patient preference for self-catheterization.

- Based on application, the urinary incontinence segment led the market by capturing 26.8% share in 2025, supported by rising prevalence of bladder dysfunction and age-related urinary disorders.

- Based on catheter coating type, the coated catheters segment held the majority share of 60.4% in 2025, driven by increasing adoption of antimicrobial and hydrophilic coatings to improve patient safety and comfort.

- Based on gender, the male segment was the largest in 2025, occupying 54.3% market share, supported by higher prevalence of prostate-related urinary conditions and urological procedures.

- Based on end user, the hospitals segment remained the leading category by accounting for 44.2% share in 2025, driven by high patient admissions, surgical procedures, and acute care requirements.

Regional Insights

The global urinary catheters market is witnessing steady growth across major regions, supported by rising healthcare investments, increasing chronic disease burden, and improving healthcare access.

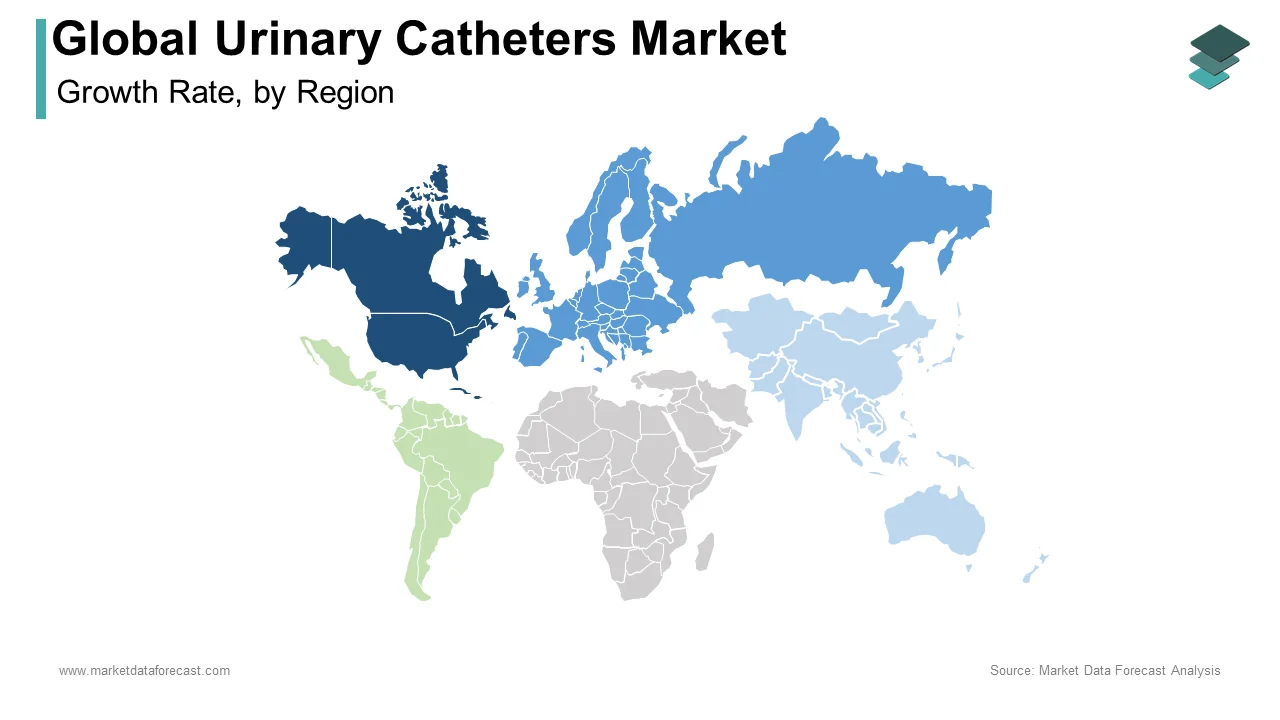

- North America dominated the global market in 2025 with 39.1% share, driven by advanced healthcare infrastructure, high adoption of advanced catheter technologies, and strong reimbursement systems.

- Europe held the second-largest position with 28.4% share in 2025, supported by increasing elderly populations and strong healthcare regulatory frameworks.

- Asia-Pacific remains a key growth region, driven by rising healthcare expenditure, expanding medical infrastructure, and increasing access to advanced urinary management solutions across emerging economies.

Competitive Landscape

The global urinary catheters market is characterized by strong competition among medical device manufacturers and urology care providers focusing on product innovation, patient safety, and infection prevention technologies. Market players are emphasizing development of coated catheters, expansion of product portfolios, and integration of advanced biocompatible materials to strengthen market positioning. Strategic collaborations, acquisitions, and investments in home healthcare solutions are shaping competitive dynamics across the market.

Prominent companies operating in the global urinary catheters market include Medtronic, J and M Urinary Catheters LLC, Teleflex Inc., C.R. Bard, Inc., Cook Medical, Medline Industries, Inc., B. Braun Melsungen AG, Boston Scientific Corporation, Coloplast, and Hollister Incorporated.

Global Urinary Catheters Market Size

The size of the global urinary catheters market was valued at USD 3.41 billion in 2025. This market is expected to grow at a CAGR of 6.7% from 2026 to 2034 and be worth USD 6.11 billion by 2034 from USD 3.64 billion in 2026.

A urinary catheter is a thin, flexible tube inserted into the bladder to drain and collect urine. These devices include indwelling catheters, intermittent catheters, and external collection systems, each tailored to specific clinical indications and patient capabilities. Urinary incontinence affects between 10% and 20% of individuals across European populations according to epidemiological surveys. The aging demographic trajectory intensifies clinical demand, as 22% of the European Union population was aged 65 years and over on 1 January 2025, according to Eurostat data. Clinical surveillance data indicate that urinary tract infections represent approximately 19% of all healthcare-acquired infections, with between 43% and 56% of these specific infections linked to urethral catheter utilization. In the Netherlands, population-based cohort research shows that the number of indwelling catheter users increased by 44.6% (from 41,619 to 60,172 individuals) between 2012 and 2021. Reflecting demographic shifts that directly influence urological care requirements, the median age of the European Union population reached 44.7 years in 2024 and rose to 44.9 years by 1 January 2025, according to Eurostat. Healthcare systems across Europe continue refining protocols for catheter management, emphasizing evidence-based practices to minimize complications while preserving patient dignity and comfort in bladder care delivery.

MARKET DRIVERS

Rising Prevalence of Age-Related Urological Conditions

The escalating incidence of benign prostatic hyperplasia and age-related urinary dysfunction drives the demand for these devices and the growth of the urinary catheters market. The estimated prevalence of lower urinary tract symptoms related to benign prostatic hyperplasia in men over 50 years of age reaches approximately 30% according to European urological research. Eastern Europe exhibited the highest age-standardized incidence rate for benign prostatic hyperplasia at 661.12 per 100000 persons in 2021, as per the global burden of disease analysis. This clinical reality translates into substantial catheter utilization. Longitudinal Dutch population studies reveal that between 2012 and 2021, the overall number of clean intermittent catheter users increased by 27.3%, driven primarily by escalating demand among male populations over 65 years of age. Demographic pressures continue to expand this market, with the European Union population aged 65 and over now representing 22.0% of total inhabitants. Healthcare providers increasingly recognize that timely catheter intervention prevents complications such as renal deterioration and urinary sepsis in elderly patients with compromised bladder function. Clinical guidelines from the European Association of Urology emphasize appropriate catheter selection based on patient capability and underlying pathology, further standardizing utilization patterns across member states. The convergence of aging demographics, rising urological disease prevalence, and evidence-based clinical protocols creates sustained demand for advanced catheter technologies that balance efficacy with patient safety and comfort in European care settings.

Expanding Clinical Applications in Neurological Care Pathways

Neurological disorders requiring bladder management represent a significant and growing segment that fuels urinary catheter adoption throughout regional healthcare networks, which propels the expansion of the urinary catheter market. While neurogenic bladder dysfunction cannot be entirely reversed, neurological urology research emphasizes that up to 90% of patients can successfully protect their long-term renal health and mitigate severe complications through timely clinical intervention. Spinal cord injury patients frequently require intermittent catheterization as the recommended urinary management method because it addresses multiple lower urinary tract conditions while supporting long-term renal health. According to rehabilitation studies, approximately 58.8% of spinal cord injury patients who are unable to volitionally void possess adequate upper extremity function to independently perform clean intermittent catheterization. The European healthcare infrastructure increasingly integrates specialized urological care for neurological populations, with guidelines emphasizing harmonized clinical practice across member states. Multiple sclerosis, Parkinson's disease, and stroke survivors often experience neurogenic bladder dysfunction necessitating structured catheterization protocols. Healthcare systems recognize that appropriate catheter selection reduces hospital readmissions and improves the quality of life for neurological patients managing chronic bladder dysfunction. The expansion of home-based care models further amplifies demand for user-friendly catheter systems that empower patient independence while maintaining clinical safety standards. As neurological care pathways evolve toward personalized medicine approaches, catheter technologies accommodating diverse patient capabilities and preferences gain strategic importance within European urological service delivery frameworks.

MARKET RESTRAINTS

Infection Control Concerns and Catheter-Associated Complications

Catheter-associated urinary tract infections are a formidable barrier to the urinary catheter market expansion. This is due to clinical risks and healthcare cost implications. The mean catheter-associated urinary tract infection incidence rate reached 6.99 per 1000 patient days according to intensive care unit surveillance data. Between 15% and 25% of hospitalized patients receive urinary catheters, yet approximately 75% of hospital-acquired urinary tract infections are associated with catheter use as per infection control research. These statistics underscore the clinical dilemma facing healthcare providers who must balance necessary bladder drainage against infection risks. European healthcare systems implement stringent catheter utilization protocols to minimize unnecessary device placement, potentially limiting market volume growth. The European Centre for Disease Prevention and Control emphasizes evidence-based guidelines for preventing catheter-associated infections, encouraging healthcare facilities to adopt restrictive catheterization policies. Clinical awareness of complications such as urethral trauma, bladder spasms, and antimicrobial resistance further constrains indiscriminate catheter adoption. Healthcare economics research indicates that infection prevention initiatives may reduce catheter utilization in settings where alternative bladder management strategies prove viable. Patient safety priorities increasingly favor intermittent catheterization over indwelling devices when clinically appropriate, reshaping product preference patterns. These infection control imperatives create market headwinds that manufacturers must address through innovative antimicrobial technologies and enhanced clinical education programs supporting appropriate catheter selection.

Regulatory Complexity and Reimbursement Variability Across European Markets

Divergent regulatory frameworks and inconsistent reimbursement policies across the nations in the region constrain the accessibility and commercial predictability of the urinary catheter market. European healthcare systems operate under varied national procurement protocols, creating fragmented market entry pathways for catheter manufacturers. Reimbursement structures for incontinence materials and catheter devices differ substantially between member states, influencing patient access and provider prescribing patterns. Some European healthcare systems do not fully reimburse incontinence materials, creating financial incentives for patients to opt for reimbursed indwelling catheters despite higher complication risks, according to health economics analysis. This reimbursement variability complicates market forecasting and strategic planning for manufacturers seeking pan-European commercial strategies. Regulatory requirements for medical device certification under European Union frameworks demand substantial investment in clinical evidence generation and quality management systems. Healthcare technology assessment processes vary between nations, affecting market access timelines and pricing negotiations. The complexity of navigating multiple national formularies and procurement channels increases commercial overhead for catheter suppliers. These regulatory and reimbursement challenges disproportionately impact smaller manufacturers lacking resources for multi-jurisdictional market development. Market participants must invest significantly in health economics research and regulatory affairs capabilities to achieve sustainable European market penetration, creating barriers to entry that restrain overall market dynamism and innovation diffusion.

MARKET OPPORTUNITIES

Technological Innovation in Antimicrobial and Smart Catheter Systems

Advanced catheter technologies incorporating antimicrobial coatings and digital monitoring capabilities offer substantial growth opportunities within the European urinary catheters market. Life-cycle research indicates that advanced recycling of non-infectious or decontaminated clinical waste generates a lower carbon footprint than incineration, establishing clear environmental incentives for sustainable, circular catheter design. Manufacturers developing catheters with silver alloy or antibiotic-impregnated surfaces address infection prevention priorities while differentiating products in competitive tender processes. Smart catheter systems integrating flow sensors and bladder volume monitoring enable personalized care protocols that reduce unnecessary catheter duration and associated complications. European healthcare systems increasingly value technologies supporting antimicrobial stewardship initiatives, creating favorable adoption pathways for innovative catheter platforms. The European IMAGINE project demonstrated that targeted interventions reduced urinary tract infections by 27% in long-term care facilities, validating the commercial potential of technology-enabled infection prevention strategies. Digital health integration opportunities allow catheter manufacturers to develop companion applications supporting patient education and adherence monitoring. Healthcare providers seek solutions that reduce nursing workload while improving patient outcomes, positioning technologically advanced catheters as strategic investments rather than commodity purchases. Regulatory pathways for software as a medical device create additional innovation avenues for manufacturers willing to invest in digital health capabilities. These technological opportunities enable premium pricing strategies and strengthen manufacturer relationships with healthcare systems pursuing quality improvement and cost containment objectives simultaneously.

Expansion of Home-Based Care and Patient Empowerment Models

The transition toward community-based urological care creates promising prospects for manufacturers within the urinary catheter market. These manufacturers are serving the regional home care landscapes. Many seniors continue living independently at home for longer periods due to limited nursing home capacity, increasing demand for user-friendly catheter systems suitable for self-management, according to demographic care studies. Clean intermittent catheterization enables greater patient independence and mobility while reducing infection risks compared to indwelling devices, according to clinical guidelines. Manufacturers developing ergonomic catheter designs with simplified insertion mechanisms address the needs of elderly patients and informal caregivers managing bladder care at home. European healthcare policies increasingly support discharge to home settings, accelerating the adoption of catheter products compatible with community care workflows. Patient education platforms and telehealth support services represent value-added opportunities for manufacturers seeking to differentiate beyond product features alone. The growing prevalence of urinary incontinence among middle-aged women, affecting up to 35% of this demographic according to European surveys, substantially expands the addressable market for discreet, comfortable, and independent catheter solutions. Home care providers seek reliable supply chains and comprehensive training resources, creating partnership opportunities for manufacturers willing to invest in service infrastructure. These home care expansion trends align with European healthcare sustainability goals by reducing institutional care costs while maintaining patient quality of life. Manufacturers positioned to support the home care ecosystem through integrated product and service offerings capture strategic advantages in evolving European urological care delivery models.

MARKET CHALLENGES

Healthcare Workforce Constraints and Training Deficits

Shortages of trained healthcare professionals capable of managing complex catheterization protocols challenge optimal utilization of these devices across the regional healthcare systems, which slows down the growth of the Urinary catheters market. Specialized nursing expertise in urological care remains unevenly distributed, with rural and resource-constrained settings facing particular challenges in accessing trained personnel. The European Association of Urology Nurses emphasizes evidence-based guidelines for best practice in catheterization, yet implementation varies substantially between institutions. Inadequate training increases complication risks, including catheter-associated infections and urethral trauma, undermining patient outcomes and increasing healthcare costs. Healthcare workforce pressures intensify as aging populations require more urological care, while staff recruitment and retention challenges persist across European nations. Manufacturers investing in comprehensive education programs and simulation-based training tools address this challenge while building brand loyalty among healthcare providers. However, scaling training initiatives across diverse European healthcare systems requires substantial investment and cultural adaptation. Language barriers, varying clinical protocols, and differing regulatory requirements complicate standardized training delivery. The economic burden of urinary incontinence in the European Union reached approximately 69.2 billion euros, highlighting the stakes associated with effective catheter management. Healthcare systems seeking cost containment may limit investment in specialized training, creating tension between quality improvement aspirations and budget realities. Manufacturers must navigate these workforce dynamics through flexible education strategies that accommodate varying resource levels while maintaining clinical excellence standards essential for safe catheter utilization.

Environmental Sustainability Pressures and Waste Management Imperatives

Growing environmental consciousness across the healthcare systems in the region creates obstacles for manufacturers within the urinary catheters market. These manufacturers are reliant on single-use disposable products. Incontinence pad waste disposal represents a significant environmental consideration, with recycling alternatives preventing substantial carbon dioxide equivalent emissions compared to incineration, according to sustainability research. European Union waste management regulations increasingly restrict landfill disposal of medical products, compelling manufacturers to develop recyclable or biodegradable catheter materials. The environmental impact of clinical waste streams receives heightened scrutiny as healthcare systems pursue carbon neutrality commitments. Manufacturers face technical and economic challenges in developing sustainable catheter alternatives that maintain clinical performance while reducing ecological footprint. Supply chain transparency requirements demand comprehensive lifecycle assessments that many manufacturers struggle to deliver consistently. Patient preferences increasingly favor environmentally responsible products, yet clinical efficacy remains the paramount selection criterion, creating complex value proposition challenges. Healthcare procurement policies incorporating environmental criteria add complexity to tender processes and product development roadmaps. The tension between infection control requirements favoring single-use devices and sustainability goals promoting reusable alternatives creates strategic uncertainty for market participants. Manufacturers investing in circular economy innovations and sustainable material science gain competitive advantages, yet these investments require long-term commitment amid evolving regulatory landscapes. Balancing clinical safety, patient comfort, environmental responsibility, and commercial viability represents a multifaceted challenge shaping the future trajectory of the European urinary catheters market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Application, Catheter Coating Type, Gender, End-User, and Region.. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa |

| Market Leaders Profiled | Medtronic, J and M Urinary Catheters LLC, Teleflex Inc., C.R.Bard, Inc., Cook Medical, Medline Industries, Inc., B. Braun Melsungen AG, Boston Scientific Corporation, Coloplast, and Hollister Incorporated, and Others. |

SEGMENTAL ANALYSIS

By Product Insights

The intermittent catheters segment dominated the urinary catheters market and accounted for a 52.8% in 2025. This dominance of the segment was driven by the growing preference for self-catheterization among patients with neurogenic bladder dysfunction and spinal cord injuries. Clean intermittent catheterization reduces infection risks compared to indwelling devices while promoting patient independence and mobility, according to clinical guidelines. Rehabilitation studies demonstrate product market viability by showing that approximately 58.8% of spinal cord injury patients unable to volitionally void possess adequate upper extremity function to perform intermittent catheterization independently. "Providing a strong demand baseline for this product type, Netherlands population-based research documented a 27.3% overall expansion in clean intermittent catheter users between 2012 and 2021, heavily driven by aging male demographics. Healthcare systems increasingly favor intermittent protocols for chronic bladder management due to lower complication rates and improved quality of life outcomes. Patient education programs and home care expansion further amplify adoption as individuals seek discreet and comfortable bladder management solutions. Manufacturers respond with ergonomic designs and hydrophilic coatings that simplify insertion and enhance user experience. These converging clinical and lifestyle factors sustain intermittent catheters as the preferred choice across diverse patient populations and care settings.

However, the external catheters segment is expected to exhibit a noteworthy CAGR of 8.2% from 2026 to 2034 due to rising adoption of non-invasive urinary management solutions for male incontinence and post-operative care. According to manufacturer disclosures from BD's Official PureWick Data, the PureWick external catheter system has been utilized in over 50 million applications for female patients and 5 million for male patients across combined acute care and home care settings. External catheters minimize urethral trauma and catheter-associated infection risks while preserving patient dignity, according to clinical evidence. Long-term care facilities increasingly integrate external systems to reduce nursing workload and improve resident comfort during continence management. The aging demographic trajectory intensifies demand as elderly patients benefit from non-invasive alternatives that support independent living. Technological innovations, including portable collection units and enhanced suction mechanisms, expand clinical applicability across home and institutional environments. Healthcare economics research demonstrates cost savings through reduced infection treatment expenses and shorter hospital stays. These advantages position external catheters as a high-growth opportunity within the evolving urinary management landscape.

By Application Insights

The urinary incontinence segment led the global market and captured a 26.8% share in 2025. This leading position of the segment was attributed to the substantial prevalence of incontinence. It affects between 10% and 20% of the European population according to epidemiological surveys. Reflecting a highly scalable addressable market, European health surveys indicate that up to 35% of middle-aged women experience some form of urinary incontinence. The economic burden of urinary incontinence in the European Union reached approximately 69.2 billion euros, highlighting the scale of clinical need. Healthcare systems prioritize effective bladder management solutions to reduce social isolation and improve the quality of life for affected individuals. Intermittent and external catheter options enable discreet management that supports continued participation in daily activities. Clinical guidelines emphasize personalized treatment approaches based on incontinence type severity and patient capability. The growing awareness of incontinence as a treatable condition rather than an inevitable aging consequence drives earlier intervention and sustained product utilization. Manufacturers develop user-friendly designs and educational resources to empower patient self-management. These factors collectively sustain urinary incontinence as the primary application driver for urinary catheter demand across global markets.

On the other hand, the spinal cord injury segment is predicted to witness the highest CAGR of 9.1% over the forecast period, owing to improved survival rates and specialized rehabilitation protocols that extend life expectancy for spinal cord injury patients. While neurogenic bladder dysfunction cannot be reversed, neurological urology research emphasizes that up to 90% of patients successfully protect their long-term renal health and mitigate severe complications through timely clinical management. Clean intermittent catheterization remains the recommended urinary management method for spinal cord injury patients because it addresses multiple lower urinary tract conditions while supporting long-term renal health. According to rehabilitation studies, approximately 58.8% of spinal cord injury patients who are unable to volitionally void possess adequate upper extremity function to independently perform clean intermittent catheterization. Specialized care centers increasingly integrate comprehensive urological management into rehabilitation pathways, improving outcomes and reducing complications. Patient advocacy organizations promote awareness of bladder management options, empowering individuals to access appropriate catheter technologies. Technological innovations, including hydrophilic coatings and compact designs, enhance usability for patients with limited dexterity. These converging clinical and technological factors position spinal cord injury as a high-growth application segment within the urinary catheters market.

By Catheter Coating Type Insights

The coated catheters segment held the majority share of 60.4% of the urinary catheters market in 2025 because of clinical preference for hydrophilic and antimicrobial coatings that reduce insertion trauma and infection risks. Antimicrobial catheters with silver antibiotic and hydrophilic coatings have demonstrated 30% to 50% decreases in bacterial colonization and catheter-associated urinary tract infections according to clinical research. Validating the clinical impact of technology-enabled infection prevention, the European IMAGINE project demonstrated that targeted, structured institutional interventions reduced urinary tract infections by 27% in long-term care facilities. Healthcare providers increasingly specify coated products for patients at elevated infection risk, including elderly individuals and those with compromised immune function. Patient comfort considerations also favor coated catheters, which require less lubrication and minimize urethral irritation during insertion. Manufacturing advances enable consistent coating application and extended shelf life, supporting broader clinical adoption. Regulatory frameworks in Europe and North America encourage the use of infection prevention technologies, creating favorable reimbursement pathways. These clinical, economic, and regulatory factors sustain coated catheters as the preferred choice across diverse care settings and patient populations.

On the contrary, the coated catheters segment is also estimated to register the fastest CAGR of 8.4% from 2026 to 2034. This swift expansion is propelled by an intensifying focus on infection prevention and antimicrobial stewardship within healthcare systems globally. Clinical guidelines from the European Centre for Disease Prevention and Control emphasize evidence-based strategies for preventing catheter-associated infections, encouraging adoption of advanced coating technologies. Hospital procurement policies increasingly incorporate infection reduction metrics, creating competitive advantages for manufacturers offering coated solutions. Patient awareness of infection risks drives preference for products with demonstrated safety profiles. Research and development investments focus on next-generation coatings with enhanced durability and broader antimicrobial spectra. These converging clinical, regulatory, and commercial factors position coated catheters for sustained high growth within the evolving urinary catheters market landscape.

By Gender Insights

The male segment was the largest by occupying a 54.3% share of the urinary catheters market in 2025. This prominence of the segment was supported by a higher prevalence of benign prostatic hyperplasia and prostate-related urinary dysfunction among aging male populations. The estimated prevalence of lower urinary tract symptoms related to benign prostatic hyperplasia in men over 50 years of age reaches approximately 30% according to European urological research. Eastern Europe exhibited the highest age-standardized incidence rate for benign prostatic hyperplasia at 661.12 per 100000 persons in 2021, as per the global burden of disease analysis. Male patients frequently require catheterization following prostate surgery or for management of urinary retention associated with prostate enlargement. Clinical protocols for male catheterization are well established, supporting consistent product utilization across healthcare settings. Manufacturers develop anatomically optimized designs that accommodate male urethral anatomy and improve insertion comfort. Patient education initiatives promote appropriate catheter selection and self-management techniques for chronic conditions. These clinical demographic and product development factors sustain male patients as the primary user group within the urinary catheters market.

But the female segment is anticipated to witness the fastest CAGR of 7.8% over the forecast period. This rapid growth of the segment is fuelled by rising awareness and treatment of urinary incontinence among women, particularly following childbirth and during menopause. Reflecting a highly scalable addressable market, European health surveys indicate that up to 35% of middle-aged women experience some form of urinary incontinence. Female intermittent catheter users more than doubled from 91 to 201 per 100000 insured persons in longitudinal studies documenting utilization trends. Healthcare providers increasingly recognize gender specific anatomical considerations in catheter design, leading to the development of female-optimized products. Demonstrating high clinical and market acceptance, manufacturer disclosures confirm that the PureWick female external catheter system has been utilized in over 50 million applications across combined acute care and home care settings. Patient advocacy organizations promote awareness of treatable incontinence conditions, reducing stigma and encouraging earlier intervention. Manufacturers invest in discreet, comfortable designs that support continued participation in daily activities. These converging clinical, social, and product innovation factors position female patients as the highest growth demographic within the urinary catheters market.

By End User Insights

The hospitals segment remained the top performer in the urinary catheter market and accounted for a 44.2% share in 2025. This dominance of the segment was driven by the central role of acute care facilities in managing complex urological conditions and post-surgical recovery. Between 15% and 25% of hospitalized patients receive urinary catheters during their stay, according to infection control research. The mean catheter-associated urinary tract infection incidence rate reached 6.99 per 1000 patient days in intensive care units according to surveillance data. Hospitals require reliable supply chains and comprehensive product portfolios to address diverse clinical scenarios from emergency retention to post-operative drainage. Clinical protocols emphasize appropriate catheter selection based on patient condition and anticipated duration of use. Infection prevention initiatives drive adoption of coated and antimicrobial catheter technologies within hospital formularies. Staff training programs ensure proper insertion techniques and maintenance procedures to minimize complications. These operational, clinical, and quality improvement factors sustain hospitals as the primary procurement channel for urinary catheters across global healthcare systems.

On the contrary, the long-term care facilities segment is likely to experience the fastest CAGR of 8.9% during the forecast period. This quick surge of the segment is supported by the aging demographic trajectory and increasing prevalence of chronic bladder dysfunction among elderly residents. Demographic pressures continue to impact long-term care end users, as exactly 22.0% of the European Union population was aged 65 years and over on 1 January 2025, according to Eurostat data. Use of indwelling catheters in nursing home residents tended to increase from 15.0% in men treated with 0 to 4 medications to 32.1% in men treated with multiple drugs, according to clinical research. Long-term care providers increasingly integrate structured bladder management protocols to preserve resident dignity and reduce infection risks. Staff training initiatives promote appropriate catheter utilization and timely removal to minimize complications. External catheter systems gain adoption as non-invasive alternatives that support resident comfort and reduce nursing workload. Regulatory frameworks emphasize quality metrics related to infection prevention and resident quality of life. These demographic, clinical, and operational factors position long-term care facilities as the highest growth procurement channel within the urinary catheters market.

REGIONAL ANALYSIS

North America Urinary Catheters Market Analysis

North America outperformed other regions in the global urinary catheters market and captured a 39.1% share in 2025. This leading position of the regional market was propelled by advanced healthcare infrastructure, high treatment spending, and robust reimbursement frameworks that support access to innovative catheter technologies. Healthcare systems prioritize infection prevention, creating favorable demand for coated and antimicrobial catheter solutions. Patient awareness programs and clinical guidelines promote appropriate catheter utilization across acute and long-term care settings. Manufacturers invest in research and development to introduce next-generation products addressing unmet clinical needs. Regulatory pathways through the Food and Drug Administration support timely market access for innovative technologies. These converging clinical, economic, and regulatory factors sustain North America as the primary revenue generator within the global urinary catheters market landscape.

Europe Urinary Catheters Market Analysis

Europe was positioned second in the global market and occupied a 28.4% share in 2025. Demographic aging intensifies clinical demand, as exactly 22.0% of the European Union population was aged 65 years and over on 1 January 2025, according to Eurostat data. Healthcare systems across member states implement evidence-based guidelines for catheter management, emphasizing infection prevention and patient-centered care. The European Centre for Disease Prevention and Control promotes standardized protocols for preventing catheter-associated infections, encouraging adoption of advanced technologies. Reimbursement frameworks vary between nations, creating diverse market access pathways for manufacturers. Patient advocacy organizations raise awareness of treatable urological conditions, supporting earlier intervention and sustained product utilization. Manufacturers adapt product portfolios to accommodate varying clinical practices and regulatory requirements across European markets. These demographic, clinical, and policy factors position Europe as a stable, high-value market within the global urinary catheters landscape.

Asia Pacific Urinary Catheters Market Analysis

Asia Pacific is another key player in the urinary catheters market. Rising healthcare expenditure and improving medical infrastructure across emerging economies support increased access to advanced catheter technologies. Urbanization and changing lifestyle patterns contribute to the rising prevalence of urological conditions, including benign prostatic hyperplasia and urinary incontinence. Government initiatives to expand healthcare coverage increase patient access to catheter-based treatments across public and private facilities. Local manufacturers develop cost-effective products addressing price-sensitive markets while global players introduce premium technologies through strategic partnerships. Clinical education programs promote appropriate catheter utilization and infection prevention practices among healthcare providers. These economic, demographic, and policy factors position the Asia Pacific as the highest growth regional market within the global urinary catheters landscape.

Latin America Urinary Catheters Market Analysis

Latin America grew steadily in the global market. Healthcare infrastructure development and rising awareness of urological conditions support gradual market expansion across the region. Public health initiatives increasingly address chronic disease management, including bladder dysfunction among aging populations. Private healthcare facilities in major urban centers adopt advanced catheter technologies, aligning with global clinical standards. Reimbursement frameworks remain evolving, creating opportunities for manufacturers offering cost-effective solutions with demonstrated clinical value. Patient education efforts promote awareness of treatable incontinence conditions, reducing stigma and encouraging earlier intervention. Local distribution partnerships enable global manufacturers to navigate diverse regulatory environments and procurement practices. Clinical training programs support appropriate catheter selection and utilization among healthcare providers across public and private settings. Economic growth in select markets supports increased healthcare spending and access to innovative medical devices. These converging clinical, economic, and policy factors position Latin America as an emerging growth market within the global urinary catheters landscape with potential for accelerated expansion as healthcare systems mature.

Middle East and Africa Urinary Catheters Market AnalysisThe

Middle East and Africa region is predicted to hold a notable share of the urinary catheters market during the forecast period. Healthcare infrastructure development and rising medical tourism support gradual market expansion across select markets within the region. Gulf Cooperation Council nations invest in advanced healthcare facilities, adopting global clinical standards for urological care. Public health initiatives increasingly address chronic disease management, including bladder dysfunction among aging populations. Private healthcare facilities in major urban centers adopt advanced catheter technologies, aligning with international best practices. Reimbursement frameworks remain evolving, creating opportunities for manufacturers offering cost-effective solutions with demonstrated clinical value. Patient education efforts promote awareness of treatable incontinence conditions, reducing stigma and encouraging earlier intervention. Strategic partnerships with local distributors enable global manufacturers to navigate diverse regulatory environments and procurement practices. Clinical training programs support appropriate catheter selection and utilization among healthcare providers across public and private settings. These converging clinical, economic, and policy factors position the Middle East and Africa as an emerging growth market within the global urinary catheters landscape, with potential for accelerated expansion as healthcare systems mature and investment increases.

COMPETITIVE LANDSCAPE

The urinary catheters market features intense competition among established medical device manufacturers and emerging innovators pursuing technological differentiation. Market leaders leverage extensive distribution networks, clinical relationships, and regulatory expertise to maintain share while investing in next-generation catheter technologies. Competition centers on infection prevention capabilities, patient comfort features, and ease of use attributes that influence provider preference and patient adherence. Price pressure from group purchasing organizations and public procurement systems creates margin challenges, particularly in mature markets. Manufacturers respond through value-based offerings demonstrating clinical outcomes and cost savings associated with advanced catheter solutions. Emerging players focus on niche applications, including pediatric catheterization and home care, and optimized designs to gain footholds against established competitors. Intellectual property protection around coating technologies and device architectures creates barriers to entry while encouraging continued research and development investment. Regulatory complexity across global markets favors companies with robust quality systems and market access capabilities. Patient-centered design and sustainability considerations increasingly influence purchasing decisions, creating opportunities for differentiation beyond traditional clinical specifications. These dynamics shape a competitive landscape where innovation execution and clinical evidence determine long-term market success.

KEY MARKET PARTICIPANTS

Some of the companies that are playing a dominating role in the global urinary catheters market include

- Medtronic

- J and M Urinary Catheters LLC

- Teleflex Inc.

- C.R. Bard, Inc.

- Cook Medical

- Medline Industries, Inc.

- B. Braun Melsungen AG

- Boston Scientific Corporation

- Coloplast

- Hollister Incorporated

TOP PLAYERS IN THE MARKET

- Coloplast A S maintains a prominent position in the urinary catheters market through continuous innovation in patient-centered catheter solutions. The company focuses on developing hydrophilic-coated intermittent catheters that enhance user comfort and reduce insertion trauma. Coloplast invests in sustainable packaging initiatives, responding to regulatory and payer preferences for environmentally responsible medical devices. The company expanded its portfolio through strategic acquisitions, including IntegraMedical to strengthen urological and wound care capabilities. Coloplast emphasizes direct patient engagement and education programs supporting self-management and adherence to catheterization protocols. Recent organizational restructuring created dedicated business units to accelerate the execution of growth strategies in catheter markets. The company collaborates with healthcare providers to implement evidence-based practices that improve clinical outcomes and reduce complications. Coloplast maintains manufacturing facilities across multiple regions, ensuring reliable supply chains and rapid response to market demands. These strategic initiatives reinforce Coloplast as a leading innovator committed to improving the quality of life for individuals requiring urinary catheterization.

- Becton Dickinson and Company strengthens its urinary catheters market position through the PureWick external catheter portfolio and advanced indwelling catheter technologies. BD expanded the PureWick portfolio with next-generation female external catheters featuring enhanced comfort and reliability. The company integrates digital health capabilities supporting remote monitoring and personalized care protocols for catheter users. BD leverages its global distribution network to ensure broad market access across acute care, long-term care, and home settings. The recent corporate strategy includes the separation of business segments to enhance focus on high-growth medical technology areas, including urology. BD invests in clinical research demonstrating infection reduction and cost savings associated with advanced catheter technologies. The company collaborates with healthcare systems to implement standardized protocols for appropriate catheter selection and utilization. These initiatives position BD as a technology leader committed to advancing urinary management solutions that improve patient outcomes and operational efficiency.

- Teleflex Incorporated advances its urinary catheters market presence through focused innovation in urology device portfolios and strategic acquisitions. Teleflex develops advanced Foley balloon catheters and intermittent catheter systems featuring hydrophilic coatings that reduce insertion friction and patient discomfort. The company emphasizes patient-centric design principles, creating ergonomic products that support self-catheterization and independence. Teleflex maintains strong relationships with healthcare providers through clinical education programs and evidence generation supporting appropriate catheter utilization. Recent corporate development activities include portfolio optimization to focus resources on high-growth urology and vascular intervention segments. The company invests in manufacturing excellence, ensuring consistent product quality and reliable supply across global markets. Teleflex collaborates with clinical experts to refine catheter technologies addressing unmet needs in neurogenic bladder and post-operative care. These strategic initiatives reinforce Teleflex as a committed partner in advancing urinary catheter solutions that enhance patient care and clinical efficiency.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the urinary catheters market employ multiple strategic approaches to strengthen their competitive position and drive sustainable growth. Product innovation remains central with manufacturers investing in hydrophilic coatings, antimicrobial technologies, and ergonomic designs that enhance patient comfort and reduce complications. Strategic acquisitions enable rapid portfolio expansion and access to novel technologies, as demonstrated by recent transactions in urology device segments. Geographic expansion focuses on high-growth emerging markets where healthcare infrastructure development creates new opportunities for advanced catheter adoption. Partnerships with healthcare providers support clinical education and evidence generation, promoting appropriate catheter selection and utilization protocols. Digital health integration creates value-added services, including remote monitoring and patient adherence support, that differentiate product offerings. Sustainable manufacturing and packaging initiatives respond to regulatory and payer preferences for environmentally responsible medical devices. Direct patient engagement programs build brand loyalty and support self-management among chronic catheter users. These converging strategies enable market participants to address evolving clinical needs while capturing growth opportunities across diverse global healthcare settings.

MARKET SEGMENTATION

This research report on the global urinary catheters market has been segmented and sub-segmented based on the product type, application, catheter coating type, gender, end-User, and region.

By Product Type

- Intermittent Catheters

- Foley/Indwelling Catheters

- External Catheters

By Application

- Urinary Incontinence

- Benign Prostate Hyperplasia & Prostate Surgeries

- Spinal Cord Injury

- Others

By Catheter Coating Type

- Coated Catheters

- Uncoated Catheters

By Gender

- Male

- Female

By End-User

- Hospitals

- Clinics

- Long-Term Care Facilities

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. Which countries dominate the europe urinary catheters market?

Germany, France, and the UK lead the europe urinary catheters market, driven by aging populations and advanced healthcare infrastructure

2. What are the main types of urinary catheters used in europe?

Intermittent, Foley/indwelling, and external catheters are the main types in the europe urinary catheters market, with intermittent leading in revenue

3. How does aging population affect the europe urinary catheters market?

Rising elderly population with urinary issues increases demand for catheters in the europe urinary catheters market

4. What applications drive the europe urinary catheters market?

Urinary incontinence, benign prostatic hyperplasia, surgeries, and other urological conditions boost the europe urinary catheters market

5. What is the impact of antimicrobial catheters in europe market?

Growing adoption of antimicrobial-coated catheters reduces infection risks, positively impacting the europe urinary catheters market

6. How do hospitals contribute to the europe urinary catheters market?

Hospitals are major end-users with rising surgeries and hospital stays driving demand in the europe urinary catheters market

7. What innovations are shaping the europe urinary catheters market?

Material innovations, antimicrobial coatings, and design improvements shape growth in the europe urinary catheters market

8. What challenges does the europe urinary catheters market face?

Challenges include strict regulations, reimbursement issues, and infection control concerns in the europe urinary catheters market

9. How does reimbursement influence the europe urinary catheters market?

Reimbursement policies affect product adoption and pricing in the europe urinary catheters market

10. What role do ambulatory care settings play in europe urinary catheters market?

Growing home care and outpatient catheterization contribute to the europe urinary catheters market expansion

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com