U.S Elevator Market Size, Share, Trends And Growth Forecasts Research Report, Segmented By Type, Business, Application and Country - Industry Analysis (2026 to 2034)

Market Size, 2025

$30.54 BnMarket Estimate, 2026

$32.43 BnMarket Forecast, 2034

$52.39 BnCAGR, 2026–2034

6.18%U.S. Elevator Market Summary

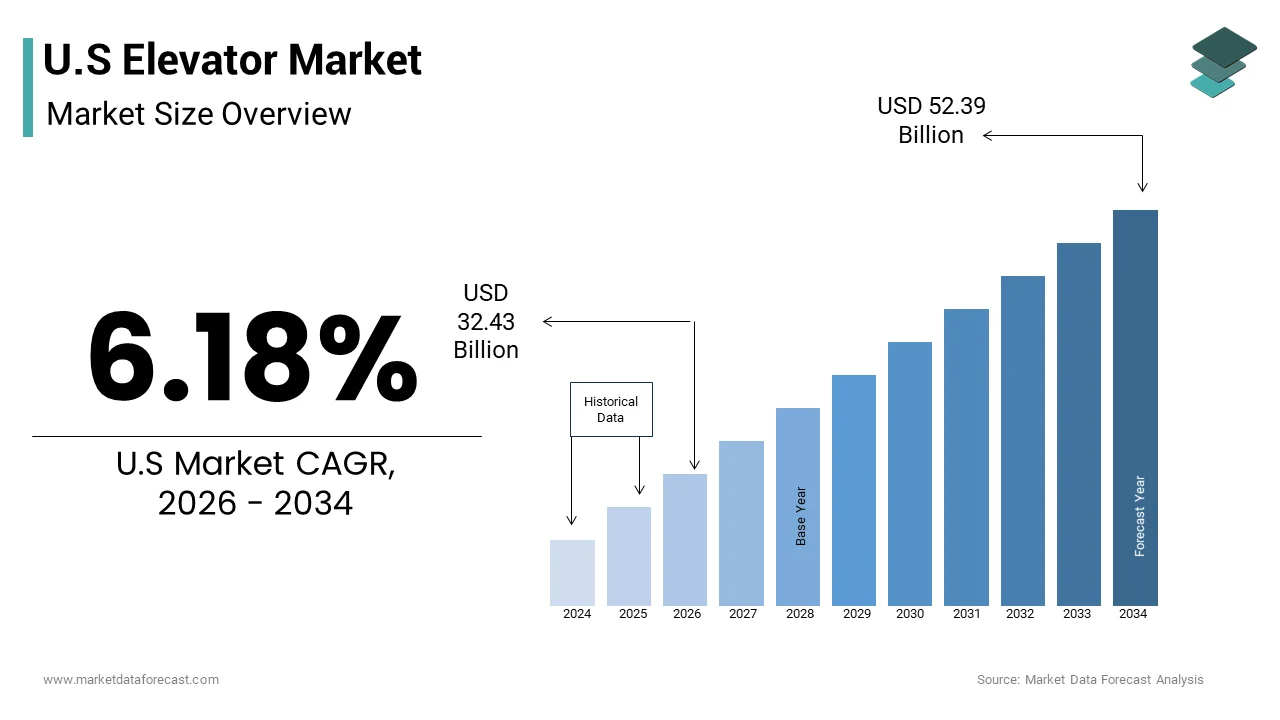

The U.S. elevator market was valued at USD 30.54 billion in 2025, is estimated to reach USD 32.43 billion in 2026, and is projected to reach USD 52.39 billion by 2034, growing at a CAGR of 6.18% from 2026 to 2034. The growth of the U.S. elevator market is driven by increasing construction of high-rise buildings, modernization of aging infrastructure, rising demand for smart and energy-efficient elevators, and expanding urbanization. In addition, advancements in IoT-based maintenance systems and automation technologies are further enhancing elevator safety, performance, and user experience across the country.

Key Market Trends

- Rising adoption of smart elevators integrated with IoT and AI for predictive maintenance and real-time monitoring.

- Growing demand for energy-efficient and regenerative drive systems to reduce power consumption and operational costs.

- Increasing modernization of aging elevator systems in commercial and residential buildings.

- Expansion of urban infrastructure projects and mixed-use developments boosting elevator installations.

- Advancements in touchless and destination control technologies improving safety and passenger convenience post-pandemic.

Segmental Insights

- Based on Type: The traction elevators segment held a significant share of the U.S. elevator market in 2025, driven by its higher energy efficiency, smoother ride experience, and suitability for high-rise and commercial structures. Growing adoption in both new installations and modernization projects continues to reinforce the segment’s dominance.

- Based on Business: The maintenance services segment held 54.3% of the U.S. elevator market share in 2025, supported by the need for regular inspections, repair, and upgrades to ensure safety compliance and performance reliability. The rising demand for service contracts and preventive maintenance solutions is boosting the growth of this segment.

- Based on Application: The commercial segment was the largest in 2024, capturing 67.3% of the market share, primarily driven by installations across office buildings, shopping malls, airports, and hospitality sectors. Increasing commercial infrastructure investments and smart building projects are further supporting market expansion in this category.

Regional Insights

- The U.S. elevator market demonstrates robust growth across metropolitan and developing regions due to infrastructure advancements and vertical construction trends.

- The Northeast region continues to lead in modernization projects, particularly in New York and Boston, where aging high-rise structures are being upgraded with smart elevators.

- The South region is experiencing rapid installation growth driven by expanding urban centers, new commercial complexes, and real estate development in cities like Atlanta, Dallas, and Miami.

- The Midwest region shows steady demand from industrial facilities, healthcare institutions, and educational buildings emphasizing energy-efficient systems.

- The West region, especially California, is witnessing growing adoption of advanced, eco-friendly elevators integrated with smart control systems in tech hubs and residential towers.

Competitive Landscape

- The U.S. elevator market is highly competitive, with companies focusing on product innovation, digitalization, and service expansion to strengthen market presence.

- Leading players are integrating IoT-based monitoring platforms, sustainable materials, and AI-enabled predictive analytics to enhance customer experience and operational efficiency.

- Prominent companies operating in the U.S. elevator market include TK Elevator, Schindler, Otis Worldwide Corporation, KONE Corporation, Hitachi Ltd., HYUNDAI ELEVATOR CO., LTD., Mitsubishi Electric Corporation, Toshiba Group, FUJITEC CO., LTD., Aritco Lift AB, EMAK, Sigma Elevator Company, Schumacher Elevator Company, ESCON Elevators Pvt Limited, Electra Elevators, and CANNY ELEVATOR CO., LTD.

- These players are emphasizing strategic partnerships, digital transformation, and long-term maintenance contracts to expand their footprint and cater to the evolving demand for intelligent and sustainable elevator solutions in the U.S.

U.S Elevator Market Size

The U.S elevator Market size was valued at USD 30.54 billion in 2025 and is anticipated to reach USD 32.43 billion in 2026 to reach USD 52.39 billion by 2034, growing at a CAGR of 6.18% during the forecast period from 2026 to 2034.

According to the U.S. Department of Transportation, there are approximately 1 million elevators and escalators in operation across the country, serving billions of passengers daily. The regulatory landscape is governed by strict safety codes, such as ASME A17.1, which mandates regular inspections and compliance standards. As per the National Elevator Industry Inc, the typical lifespan of an elevator system is 20 to 30 years on average, creating a substantial demand for modernization and retrofitting services. Urbanization trends continue to drive the construction of taller buildings, which require advanced high-speed and double-deck elevator systems. The market definition extends to smart elevator technologies that integrate Internet of Things sensors for predictive maintenance and energy efficiency. Stakeholders are increasingly focusing on sustainability and accessibility to meet evolving building codes and consumer expectations. The interplay between new construction activity, aging infrastructure, and technological innovation defines the current operational environment. Manufacturers are investing in digital solutions to enhance user experience and operational reliability.

MARKET DRIVERS

Rapid Urbanization and High Rise Construction Activity

Rapid urbanization and the consequent surge in high-rise construction activity are propelling the expansion of the U.S. elevator market. As populations concentrate in metropolitan areas, the vertical expansion of cities becomes necessary to optimize land use and accommodate housing and commercial needs. According to the Council on Tall Buildings and Urban Habitat, the U.S. remains a global leader in high-rise architecture, with prominent supertall projects, such as Central Park Tower in New York City, reaching heights of 472 meters. These structures require sophisticated vertical transportation systems capable of handling high traffic volumes and speeds. The growth of mixed-use developments, which combine residential, office, and retail spaces, further amplifies the demand for diverse elevator configurations. As per the U.S. Census Bureau, urban population growth continues to drive the need for denser housing solutions that rely heavily on elevator access. The construction of luxury condominiums and premium office towers often includes multiple elevator banks and destination control systems to enhance convenience and prestige. Developers prioritize advanced elevator technologies to differentiate their properties and attract tenants. The integration of elevators into building design is critical for maximizing usable floor space and ensuring efficient vertical circulation. This sustained construction momentum ensures a steady pipeline for new elevator installations. The complexity of modern high-rises drives innovation in rope-less and multi-directional elevator systems.

Aging Infrastructure and Modernization Requirements

The aging infrastructure of existing buildings and the resulting need for modernization are further boosting the growth of the U.S. elevator market. A large proportion of elevators installed in the mid-to-late 20th century have reached the end of their useful life, or no longer meet current safety and efficiency standards. According to the National Elevator Industry Inc, modernization is recommended for most units once they reach 20 to 25 years of age to upgrade major components and ensure compliance with updated codes, such as the Americans with Disabilities Act. Building owners are increasingly investing in modernization projects to improve reliability, reduce energy consumption, and enhance passenger experience. As per the American Society of Mechanical Engineers, modernization can extend the lifespan of an elevator by 20 years or more, while significantly lowering maintenance costs. The replacement of obsolete control systems with microprocessor-based technology allows for smarter traffic management and predictive maintenance capabilities. Energy-efficient motors and regenerative drives are popular upgrades that align with sustainability goals and reduce operational expenses. The regulatory pressure to ensure accessibility for individuals with disabilities also mandates modifications to existing units. The steady stream of modernization projects provides a stable revenue source for manufacturers and service providers, independent of new construction cycles. This segment benefits from the critical nature of vertical transportation in maintaining building functionality and value.

MARKET RESTRAINTS

High Installation and Maintenance Costs

High installation and maintenance costs are significantly hampering the expansion of the U.S. elevator market. The initial capital expenditure for installing elevators, particularly in retrofits, can be prohibitive due to structural modifications and specialized labor requirements. According to the Bureau of Labor Statistics, employment costs for construction workers climbed 24% between 2020 and 2025, impacting the overall budget for vertical transportation projects. The complexity of installing high-speed elevators in existing shafts often requires extensive engineering and customization, which drives up prices. As per the Bureau of Labor Statistics, the median annual wage for elevator and escalator installers and repairers reached $106,580 in 2024, reflecting the high cost of skilled technical labor. Regular maintenance contracts are mandatory for safety compliance, adding to the long-term operational expenses for property managers. Small and medium-sized building owners may delay necessary upgrades or replacements due to financial constraints, leading to potential safety risks and inefficiencies. The high cost of spare parts for older models further exacerbates maintenance burdens. Economic uncertainty can cause developers to scale back on premium elevator features, opting for basic models instead. This price sensitivity limits the adoption of advanced technologies and slows the pace of modernization. Until cost-effective solutions become more widely available, financial barriers will remain a persistent challenge.

Regulatory Compliance and Safety Standards Complexity

Regulatory compliance and the complexity of safety standards are further impeding the U.S. market growth. Elevator installations and modifications must adhere to a patchwork of federal, state, and local codes, which can vary significantly across jurisdictions. According to the National Association of Home Builders, navigating these diverse regulatory frameworks requires specialized knowledge and often leads to delays in permitting and inspection processes. The American Society of Mechanical Engineers regularly updates safety codes, such as ASME A17.1, requiring manufacturers and contractors to continuously adapt their practices and designs. As per the Occupational Safety and Health Administration, strict safety protocols for installation and maintenance work increase labor hours and costs. Non-compliance can result in hefty fines and legal liabilities, discouraging some building owners from undertaking necessary upgrades. The rigorous inspection requirements for new installations can prolong project completion times, affecting overall construction schedules. The need for certified inspectors and specialized testing equipment adds to the operational complexity. Inconsistent enforcement of codes across different regions creates uncertainty for national developers and manufacturers. The administrative overhead associated with compliance diverts resources from innovation and expansion. These regulatory hurdles act as a brake on market growth by increasing the time and cost required to bring new systems online.

MARKET OPPORTUNITIES

Integration of Smart Technologies and IoT Solutions

The integration of smart technologies, and Internet of Things solutions is a significant opportunity for the U.S. elevator market to enhance efficiency and user experience. Smart elevators, equipped with sensors and connectivity features, enable real-time monitoring, predictive maintenance, and optimized traffic flow. According to industry reports, the adoption of IoT-enabled systems can significantly reduce downtime through early detection of potential issues. Building managers can leverage data analytics to optimize energy usage and improve passenger wait times, enhancing overall satisfaction. As per the Smart Buildings Center, the integration of elevator systems with building management platforms allows for seamless coordination of vertical and horizontal transportation. Destination control systems, that assign passengers to specific cars based on their floor requests, improve efficiency in high-traffic environments. The ability to remotely diagnose and repair issues reduces the need for on-site visits, lowering maintenance costs. Mobile apps, that allow users to call elevators from their smartphones, offer a contactless and convenient experience. Manufacturers are developing AI-driven algorithms that learn traffic patterns and adjust operations accordingly. The shift towards smart cities and connected buildings creates a favorable environment for these innovations. By offering value-added services through digital platforms, companies can differentiate their offerings and capture new revenue streams.

Expansion of Accessibility and Inclusive Design Features

The expansion of accessibility and inclusive design features offers a noteworthy opportunity for the U.S. elevator market to meet growing demographic needs and regulatory requirements. An aging population, and increased awareness of disability rights, drive the demand for elevators that accommodate individuals with limited mobility and sensory impairments. According to the U.S. Census Bureau, the number of Americans aged 65 and older is projected to reach 95 million by 2060, increasing the need for accessible vertical transportation. The Americans with Disabilities Act mandates specific design criteria for elevators, including braille buttons, audible signals, and adequate cabin dimensions. As per the Access Board, updates to accessibility guidelines encourage the adoption of features such as low-force doors and tactile indicators. Manufacturers are developing customizable cabins that cater to diverse user needs, including wheelchair-accessible layouts and voice-activated controls. The renovation of older buildings to meet current accessibility standards creates a robust market for retrofitting services. Healthcare facilities and senior living communities are prioritizing inclusive design to enhance patient and resident comfort. The focus on universal design principles extends beyond compliance to create welcoming environments for all users. Companies that specialize in accessible solutions can tap into a growing niche market. This trend aligns with broader societal values of equity and inclusion, driving long-term demand.

MARKET CHALLENGES

Skilled Labor Shortage and Technical Expertise Gap

Skilled labor shortage and the technical expertise gap are challenging the U.S. elevator market growth. The U.S. market faces a declining number of trained elevator mechanics and technicians due to an aging workforce and insufficient recruitment of new talent. According to the Bureau of Labor Statistics, there were approximately 24,200 elevator installer and repairer jobs in 2024, with a projected 5% growth rate through 2034. The complexity of modern elevator systems, requiring knowledge of electronics, software, and mechanics, raises the barrier to entry for new workers. As per the Bureau of Labor Statistics, the demand for skilled tradespeople outpaces the supply, leading to wage inflation and project delays. The lack of qualified personnel can result in improper installations and inadequate maintenance, compromising safety and performance. Training programs are often lengthy and expensive, discouraging potential entrants from pursuing careers in the field. The reliance on a small pool of experts increases vulnerability to labor disruptions and strikes. Manufacturers struggle to provide timely support and service due to staffing constraints. The technical expertise gap hinders the adoption of advanced technologies that require specialized skills for implementation. Until the industry addresses the workforce crisis through enhanced training and recruitment initiatives, the challenge of labor scarcity will persist.

Supply Chain Disruptions and Material Cost Volatility

Supply chain disruptions and material cost volatility are further challenging the expansion of the U.S. elevator market. The U.S. elevator market relies on global supplies of steel, copper, electronics, and specialized components, which are subject to price fluctuations and availability issues. According to the Institute for Supply Management, manufacturing indices have indicated persistent bottlenecks in sourcing critical parts, affecting lead times for elevator production. The volatility in raw material prices, particularly for steel and copper, increases manufacturing costs, which are often passed on to customers. As per the Bureau of Labor Statistics, prices of material inputs to new residential construction rose 42% between 2020 and 2025. These disruptions force manufacturers to hold higher inventory levels, tying up capital and increasing storage costs. Project timelines are extended due to delayed equipment deliveries, causing dissatisfaction among developers and building owners. The unpredictability of supply chains complicates long-term planning and contract negotiations. Small manufacturers are particularly vulnerable, as they lack the bargaining power to secure favorable terms. The reliance on single-source suppliers for specialized technologies increases risk exposure. Until supply chains stabilize and diversify, the industry will face ongoing operational inefficiencies and cost pressures.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.18% |

| Segments Covered | By Type, Business, Application, and Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

| Regions Covered | US, Canada, and the Rest of North America |

| Market Leaders Profiled | TK Elevator, Schindler, KONE Corporation, Hitachi Ltd., HYUNDAIELEVATOR CO., LTD., Mitsubishi Electric Corporation, Toshiba Group, FUJITEC CO., LTD., Aritco Lift AB, EMAK, Sigma Elevator Company, Schumacher Elevator Company, ESCON Elevators Pvt Limited, Electra Elevators, CANNY ELEVATOR CO, LTD. |

SEGMENT ANALYSIS

By Type Insights

The traction elevators segment accounted for the major share of the U.S. elevator market in 2025. The domination of this segment in the U.S. market is driven by the extensive presence of high-rise commercial and residential structures in major urban centers, which require reliable and fast vertical transportation. According to the Council on Tall Buildings and Urban Habitat, the U.S. features numerous buildings exceeding 150 meters in height, all of which rely on traction systems for efficient operation. Traction elevators use a counterweight system that reduces the energy required to move the cab, making them more cost-effective to operate over the long term compared to hydraulic systems. As per the American Society of Mechanical Engineers, traction systems are capable of speeds exceeding 1,000 feet per minute, which is essential for minimizing wait times in busy skyscrapers. The durability of traction components, such as steel ropes and sheaves, ensures a longer service life, reducing the frequency of major replacements. Modern gearless traction motors offer near-silent operation and precise leveling, which enhances passenger comfort in luxury hotels and office towers. The widespread adoption of regenerative drives in traction systems further aligns with green building standards, such as LEED certification. This technological advantage ensures that traction elevators remain the preferred choice for new construction projects in dense metropolitan areas. The established manufacturing base and technical expertise for traction systems in the U.S. is supporting their continued market leadership and contributing to the dominating position of this segment in the U.S. market.

However, the machine room-less traction segment is estimated to record a CAGR of 7.4% during the forecast period in the U.S. elevator market owing to the space-saving design and energy efficiency of MRL systems, which appeal to developers maximizing usable floor area. According to the National Elevator Industry Inc, MRL elevators eliminate the need for a separate machine room by housing the motor within the hoistway, thereby freeing up valuable real estate for rentable space. This feature is particularly attractive in urban infill projects where land costs are high and building footprints are constrained. As per the General Services Administration, modernization criteria often include reducing energy use by 30%, which is a target MRL systems help achieve compared to traditional units. The compact design also simplifies installation and reduces construction time, allowing for faster project completion. Advances in permanent magnet motor technology have enabled MRL systems to serve mid-rise buildings with speeds and capacities comparable to conventional traction elevators. The retrofitting of older buildings with MRL units is gaining traction, as owners seek to modernize without structural modifications. The versatility of MRL systems in both commercial and residential applications drives their rapid adoption. Regulatory updates, supporting energy-efficient technologies, further encourage the shift towards MRL solutions. These factors collectively propel the MRL segment at a faster pace than traditional types.

By Business Insights

The maintenance services segment held the leading position in the U.S. elevator market in 2025. The growth of the maintenance services segment in the U.S. market is driven by the large installed base of elevators, mandatory safety regulations requiring regular upkeep and the critical need to ensure passenger safety and system reliability in millions of existing units across the country. According to the National Elevator Industry Inc, there are approximately 1 million elevators and escalators in the U.S., each requiring routine inspections and preventive maintenance. State and local laws mandate frequent safety checks, which create a recurring revenue stream for service providers regardless of new construction activity. As per the Occupational Safety and Health Administration, failure to maintain elevators can result in severe penalties and liability issues, prompting building owners to prioritize service contracts. The aging infrastructure in many cities means that older units require more frequent repairs and parts replacement, further boosting maintenance demand. Service contracts often include emergency response and modernization consultations, which deepen customer relationships and ensure long-term retention. The complexity of modern elevator systems, with integrated software and sensors, requires specialized technicians whose expertise is in high demand. The stability of the maintenance segment provides a buffer against cyclical fluctuations in new equipment sales. This segment benefits from the essential nature of vertical transportation in maintaining building functionality and value. The consistent cash flow from maintenance supports ongoing investment in training and technology.

On the other end, the modernization segment is experiencing the fastest growth and is estimated to record a CAGR of 8.1% during the forecast period in the U.S. market owing to the fact that a significant portion of the US elevator inventory was installed decades ago, and no longer meets contemporary performance expectations. According to the National Elevator Industry Inc., elevators reaching 20 to 25 years of age are primary candidates for modernization to improve reliability and energy efficiency. Building owners are increasingly investing in upgrades, such as new control systems, motors, and doors, to reduce downtime and operating costs. As per the Government Accountability Office, energy-efficient building criteria emphasize reducing energy use by 30%, which can be addressed through modernization. The implementation of the Americans with Disabilities Act requirements also drives modernization, as older units must be updated to ensure accessibility for individuals with disabilities. Smart technology integration during modernization allows for predictive maintenance and enhanced user experience, which adds value to properties. The cost of modernization is significantly lower than full replacement, making it an attractive option for budget-conscious property managers. The shortage of new construction sites in dense urban areas shifts focus towards improving existing assets. These factors collectively ensure that the modernization segment expands rapidly as the installed base continues to age.

By Application Insights

The commercial segment led the market by holding the highest share of the U.S. elevator market in 2025. The growth of the commercial segment in the U.S. market is driven by the high density of office buildings, retail centers, and hospitality establishments in urban areas. The dominance of this segment is fueled by the continuous demand for efficient vertical transportation in high-traffic environments where reliability and speed are paramount. According to the U.S. Census Bureau, nonresidential construction spending reached a seasonally adjusted annual rate of $728.2 billion in January 2026, supporting the installation of new elevators. Office towers and shopping malls require multiple elevator banks to manage peak hour traffic efficiently, driving the adoption of advanced destination control systems. As per the International Council of Shopping Centers, the expansion and renovation of retail spaces often involve elevator upgrades to enhance customer experience and accessibility. The hospitality industry relies heavily on elevators for guest convenience and luggage transport, necessitating high-capacity and quiet operating systems. Commercial building owners prioritize aesthetic customization and smart features to differentiate their properties and attract tenants. The strict safety and maintenance regulations for public access buildings ensure a steady demand for service and modernization. The concentration of commercial activity in major metropolitan hubs creates a robust market for high-performance elevator solutions. This segment benefits from the economic vitality of the service sector, which drives ongoing investment in facility improvements. The scale of commercial projects ensures that this application remains the primary driver of elevator demand.

On the other side, the residential segment is anticipated to experience a CAGR of 6.3% during the forecast period in the U.S. market owing to the increasing preference for apartment living among millennials and baby boomers, who seek low-maintenance lifestyles in city centers. According to the Joint Center for Housing Studies of Harvard University, developers started 416,000 multifamily units in 2025, reflecting a construction environment that remains elevated by historical standards. These buildings require reliable and safe elevators to serve multiple floors and residents, creating a steady pipeline for new installations. As per the National Association of Home Builders, the inclusion of elevators in mid-rise residential projects has become standard to comply with accessibility codes and enhance property value. The trend towards luxury amenities in residential complexes often includes high-speed elevators with smart features, such as keyless entry and mobile app integration. The renovation of older residential buildings to add elevators is also gaining momentum, as owners seek to improve accessibility for aging residents. Government incentives for affordable housing development further support the construction of multi-story residential units. The shift towards vertical living in urban areas ensures that the residential segment continues to expand. The focus on resident comfort and security drives the adoption of advanced elevator technologies in this sector.

COUNTRY ANALYSIS

The U.S. held the leading position in the global market in 2025 and is anticipated to maintain its leadership as the most influential and technologically advanced national market for elevators in North America over the coming years. According to the National Elevator Industry Inc, the U.S. is home to approximately 1 million elevators and escalators, creating a substantial service and modernization market. The domestic industry is supported by major global manufacturers who maintain significant production and research facilities within the country. As per the Bureau of Labor Statistics, the median annual wage for elevator installers and repairers was $106,580 in 2024, reflecting the consistent demand for highly skilled maintenance services. The regulatory environment is stringent, with rigorous safety codes enforced at state and local levels, ensuring high standards for equipment and operations. Consumer preference for energy-efficient and smart building technologies influences product development and adoption rates. The integration of digital solutions, such as IoT-enabled monitoring, positions the U.S. as a leader in elevator innovation. The market is resilient to economic downturns due to the essential nature of maintenance and safety compliance. The presence of a skilled workforce and robust supply chain networks supports efficient service delivery. The U.S. continues to drive global trends in elevator technology and sustainability practices. The combination of infrastructure age and new construction activity ensures sustained market growth.

COMPETITIVE LANDSCAPE

The competition in the U.S. elevator market is characterized by intense rivalry among global giants who compete on technology service quality and brand reputation. The market structure is highly consolidated with a few key players dominating the new equipment and maintenance segments. Competitive intensity is driven by the need to differentiate through digital innovations such as smart dispatching and predictive analytics. Regulatory compliance regarding safety and accessibility serves as a standard requirement but excellence in service delivery becomes a key differentiator. Established players leverage their extensive installed bases to secure long term maintenance contracts which provide stable recurring revenue. Price competition is moderate in the new equipment segment but fierce in the modernization and repair sectors. Customer loyalty is maintained through reliable performance and rapid response times for emergencies. The focus on sustainability and energy efficiency is becoming increasingly important for winning bids in commercial projects. Overall the competitive landscape requires continuous investment in research and development to stay ahead in technological advancements and service excellence.

KEY MARKET PLAYERS

A Few of the market players in the U.S elevator market include

- TK Elevator

- Schindler

- Otis Worldwide Corporation

- KONE Corporation

- Hitachi Ltd.

- HYUNDAIELEVATOR CO., LTD.

- Mitsubishi Electric Corporation

- Toshiba Group

- FUJITEC CO., LTD.

- Aritco Lift AB

- EMAK

- Sigma Elevator Company

- Schumacher Elevator Company

- ESCON Elevators Pvt Limited

- Electra Elevators

- CANNY ELEVATOR CO, LTD.

Top Players In The Market

- Otis Worldwide Corporation is a pioneering leader in the U.S. elevator market with a vast installed base and comprehensive service network. The company provides innovative vertical transportation solutions for residential commercial and infrastructure projects across the nation. Otis strengthens its market position through the deployment of its digital platform Otis ONE which enables real time monitoring and predictive maintenance. The company recently launched the Gen360 elevator featuring advanced connectivity and energy efficient designs to meet modern building standards. Otis focuses on sustainability by introducing carbon neutral operations and eco friendly materials in manufacturing. Its strong brand recognition and extensive dealer network ensure reliable service delivery. These initiatives reinforce its reputation for safety and innovation while addressing the evolving needs of urban mobility and smart building integration.

- KONE Corporation is a major player in the US elevator industry known for its people flow solutions and sustainable technology offerings. The company serves a diverse range of sectors including high rise offices hospitals and residential complexes with a focus on user experience. KONE strengthens its market position through its 24/7 connected services platform which utilizes artificial intelligence to optimize elevator performance and reduce downtime. The company recently expanded its production capabilities in the U.S. to support growing demand for machine room less elevators. KONE prioritizes eco efficiency by developing energy saving drives and regenerative systems that lower operational costs. Its commitment to collaboration and open innovation allows for seamless integration with building management systems. These efforts enable KONE to deliver reliable and future proof vertical transportation solutions.

- Schindler Group is a prominent manufacturer in the U.S. elevator market offering a wide portfolio of elevators escalators and moving walks. The company leverages digital technologies to enhance mobility and safety in urban environments through its Schindler Ahead platform. Schindler strengthens its market position by investing in research and development for autonomous dispatching and touchless interface solutions. The company recently introduced new modular elevator systems that reduce installation time and construction waste. Schindler focuses on circular economy principles by refurbishing components and minimizing environmental impact throughout the product lifecycle. Its robust service network ensures timely maintenance and support for customers across the country. These strategic actions demonstrate Schindlers dedication to improving urban mobility while maintaining high standards of quality and reliability in the competitive US market.

Top Strategies Used by Key Market Participants

Key players in the U.S. elevator market primarily employ strategies such as digitalization service expansion and sustainability initiatives to strengthen their market position. Companies frequently invest in Internet of Things platforms to enable predictive maintenance and real time monitoring which reduces downtime and enhances customer satisfaction. This approach allows them to transition from product sales to recurring service revenue models. Strategic acquisitions of local service providers help firms expand their geographic reach and consolidate market presence. By focusing on energy efficient technologies companies align with green building standards and regulatory requirements. Additionally manufacturers develop modular and machine room less designs to reduce installation costs and save space. Product customization is another key strategy as companies tailor solutions to specific architectural needs. These combined strategies enable market participants to maintain competitiveness and drive growth in a mature industry landscape.

MARKET SEGMENTATION

This research report on the U.S elevator market is segmented and sub-segmented into the following categories.

By Type

- Hydraulic

- Traction

- Machine Room-Less Traction

- Others

By Business

- New Equipment

- Maintenance

- Modernization

By Application

- Residential

- Commercial

- Industrial

By Country

- USA

- Canada

- Mexico

Frequently Asked Questions

Why is elevator modernization booming in the U.S.?

Most elevators are over 20 years old; building owners are upgrading for safety, ADA compliance, energy efficiency, and to avoid costly emergency repairs

Are new elevator installations growing?

Modestly—driven by multi-family housing in the Sun Belt and mixed-use towers, but outpaced by modernization due to limited high-rise construction in many regions.

How is technology changing elevators today?

IoT sensors enable predictive maintenance, touchless calls via apps or voice, and real-time performance tracking—reducing downtime and improving user experience.

What’s causing delays in elevator service?

A nationwide shortage of certified elevator mechanics—exacerbated by retirements and slow apprenticeship pipelines—is straining response times for repairs and inspections.

Are green elevators a real trend?

Yes—regenerative drives, LED lighting, and machine-room-less (MRL) designs cut energy use by 30–70%, helping buildings meet local climate laws like NYC’s Local Law 97.

How do rising steel prices affect the market?

They increase costs for new cabs and guide rails, but since most revenue comes from service/modernization (not new builds), the overall impact is muted.

Which states have the highest elevator demand?

New York, California, Texas, Florida, and Illinois lead—due to dense urban centers, aging infrastructure, and strong multifamily construction.

Is residential elevator adoption rising?

Yes—especially in luxury homes and aging-in-place renovations, with compact, hydraulic, and gearless models gaining traction outside traditional commercial use.

How are safety regulations evolving?

ASME A17.1 updates now emphasize cybersecurity for connected elevators, emergency comms reliability, and stricter seismic requirements on the West Coast.

What’s the biggest challenge for elevator companies in 2025?

Balancing technician recruitment with digital transformation—while managing customer expectations for faster, smarter, and more sustainable vertical transport.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com