U.S. Flooring Market Size, Share, Trends And Growth Forecasts Research Report, Segmented By Material, Application, End-User & Country, Industry Analysis (2026 to 2034)

U.S. Flooring Market Report Summary

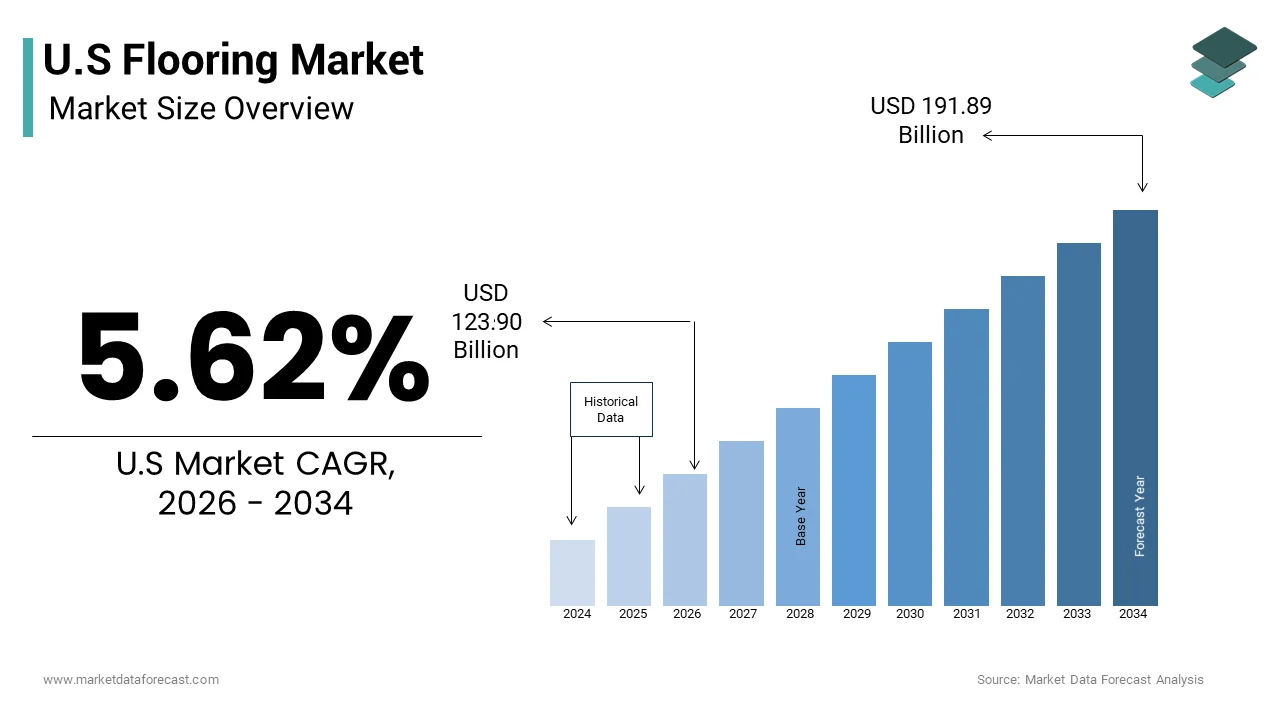

The U.S. flooring market was valued at USD 117.31 billion in 2025, is estimated to reach USD 123.90 billion in 2026, and is projected to reach USD 191.89 billion by 2034, growing at a CAGR of 5.62% from 2026 to 2034. The growth of the U.S. flooring market is driven by rising residential and commercial construction activities, increasing demand for durable and aesthetic flooring materials, and expanding renovation and remodeling projects across the country. Additionally, technological advancements in flooring designs, materials, and installation techniques are enhancing product appeal and performance, contributing to sustained market growth.

Key Market Trends

- Growing adoption of luxury vinyl tiles (LVT) and resilient flooring for their durability, water resistance, and easy maintenance.

- Rising focus on eco-friendly and sustainable flooring materials such as bamboo, cork, and recycled wood.

- Expanding demand for digitally printed and customizable flooring designs in both residential and commercial spaces.

- Increasing renovation and remodeling activities are fueled by changing interior design preferences.

- Continuous innovations in flooring adhesives and installation systems for improved efficiency and longevity.

Segmental Insights

- Based on material, the vinyl segment held 34.2% of the U.S. flooring market share in 2024, driven by its affordability, design versatility, and superior resistance to moisture and wear, making it popular in both residential and commercial settings.

- Based on application, the residential sector segment was the largest, capturing 61.2% of the U.S. flooring market share in 2024, supported by the growing housing demand, home improvement trends, and preference for stylish yet low-maintenance flooring solutions.

- Based on end-user, the renovation segment accounted for 52.3% of the U.S. flooring market share in 2024, reflecting the strong demand for remodeling projects in existing homes and commercial buildings aimed at modernizing interiors and enhancing property value.

Regional Insights

- The U.S. flooring market demonstrates significant regional diversity influenced by construction trends, consumer preferences, and climate factors.

- The South region dominates the market, driven by large-scale residential construction, infrastructure development, and population growth.

- The Midwest shows steady demand supported by renovation activities and the prevalence of cost-effective flooring options.

- The Northeast experiences strong growth in commercial and institutional flooring demand, particularly from offices, hospitals, and educational facilities.

- The Western region, led by California and Nevada, is witnessing rising adoption of sustainable and luxury flooring solutions across residential and hospitality sectors.

Competitive Landscape

- The U.S. flooring market is highly competitive, with leading manufacturers focusing on innovation, sustainable production, and expansion of product portfolios to meet evolving customer needs.

- Companies are investing in digital printing technologies, eco-friendly materials, and strategic distribution networks to strengthen their market presence.

- Prominent players in the U.S. flooring market include Mohawk Industries, Inc., Tarkett S.A., AFI Licensing, Shaw Industries, Inc., Interface, Inc., Gerflor, Mannington Mills, Inc., Polyflor, and LG Hausys Ltd.

- These players are emphasizing product diversification, sustainable flooring solutions, and strategic partnerships to enhance competitiveness and cater to the growing demand across residential, commercial, and industrial applications.

U.S Flooring Market Size

The U.S flooring market size was valued at USD 117.31 billion in 2025 and is anticipated to reach USD 123.90 billion in 2026 to reach USD 191.89 billion by 2034, growing at a CAGR of 5.62% during the forecast period from 2026 to 2034.

MARKET OVERVIEW

The flooring is surface covering materials, including hardwood, laminate, vinyl, carpet, and ceramic tile used in residential, commercial, and institutional settings. This sector serves as a critical component of the broader construction and home improvement industries, reflecting consumer preferences for aesthetics, durability, and functionality. According to the United States Census Bureau, approximately 1.45 million housing starts were recorded in early 2026, providing a steady pipeline for new flooring installations in newly constructed residences. The Joint Center for Housing Studies at Harvard University indicates that annual spending on home improvements and repairs exceeded 485 billion dollars in 2025. Regulatory frameworks, such as the FloorScore certification program influence product development by setting strict standards for indoor air quality and volatile organic compound emissions. The Environmental Protection Agency continues to monitor formaldehyde levels in composite wood products by impacting the manufacturing processes of laminate and engineered hardwood. Consumer trends increasingly favor sustainable materials, with the Forest Stewardship Council reporting a rise in certified wood flooring sales. The aging housing stock, with median ages exceeding 40 years in many regions, drives continuous remodeling activity.

MARKET DRIVERS

Robust Activity in Home Renovation and Remodeling

The home renovation and remodeling activities are fueled by an aging housing inventory and changing consumer lifestyles, which is a major factor propelling the growth of the United States flooring market. Many homeowners opt to upgrade existing properties rather than relocate, driven by high mortgage rates and limited availability of existing homes for sale. According to the Joint Center for Housing Studies at Harvard University, expenditures on home improvements and repairs reached approximately 485 billion dollars in 2025, with flooring replacements constituting a significant portion of these investments. Older homes often feature outdated or worn flooring materials that require substitution to enhance aesthetic appeal and property value. The National Association of the Remodeling Industry reports that kitchen and bathroom remodels, which frequently involve flooring updates, remain among the most popular projects. Consumers are increasingly selecting durable and low maintenance options, such as luxury vinyl plank and engineered hardwood to withstand daily wear and tear. The rise of remote work has also prompted homeowners to create dedicated office spaces, driving demand for comfortable and acoustically sound flooring solutions. DIY trends have further accelerated market growth, with retail sales of flooring materials remaining strong as individuals undertake smaller scale projects.

Expansion of Commercial Construction and Infrastructure Projects

The expansion of commercial construction and infrastructure projects, particularly in the hospitality, healthcare, and retail sectors is another factor escalating the growth of the United States flooring market. As economic activity rebounds, businesses are investing in new facilities and renovating existing spaces to attract customers and improve operational efficiency. According to the American Institute of Architects, billings for commercial construction projects increased by 8% in 2025, signaling heightened demand for interior finishes including flooring. Healthcare facilities prioritize hygienic and durable flooring options such as sheet vinyl and rubber to meet stringent sanitation standards and withstand heavy foot traffic. The hospitality industry focuses on aesthetic appeal and comfort, driving adoption of carpet tiles and luxury vinyl in hotels and restaurants. Retailers are redesigning stores to enhance customer experience, often incorporating unique flooring designs to define zones and guide movement. Government infrastructure initiatives, including the modernization of airports and transit hubs, also contribute to demand for high performance flooring materials capable of enduring extreme usage conditions. The trend towards open plan offices and collaborative workspaces favors modular flooring systems that allow for easy reconfiguration and maintenance. These diverse commercial applications create a broad and stable demand base, supporting the growth of specialized flooring segments and encouraging innovation in material performance and design.

MARKET RESTRAINTS

Volatility in Raw Material Prices and Supply Chain Disruptions

The volatility in raw material prices and supply chain disruptions by affecting production costs and availability is restricting the growth of the United States flooring market. Key materials such as wood, petroleum-based resins, and ceramics are subject to global market fluctuations influenced by geopolitical tensions, trade policies, and natural disasters. According to the Producer Price Index, prices for softwood lumber experienced swings of up to 20% in 2025, directly impacting the cost of hardwood and engineered flooring products. Petroleum price instability affects the production of vinyl and carpet fibers, leading to unpredictable manufacturing expenses. Supply chain bottlenecks, particularly in shipping and logistics, have resulted in delayed deliveries and increased freight costs. The American Trucking Associations report that freight rates for building materials remained elevated due to driver shortages and capacity constraints. These disruptions force manufacturers to adjust pricing frequently, creating uncertainty for contractors and consumers who may postpone projects due to budget concerns. Small and mid-sized retailers face particular challenges in maintaining inventory levels, leading to lost sales opportunities. The inability to secure consistent supplies of high quality raw materials also compromises product consistency and lead times. This environment of instability discourages long term planning and investment, constraining market growth and forcing companies to prioritize resilience over expansion.

Stringent Environmental Regulations and Compliance Costs

The stringent environmental regulations and compliance costs by imposing additional burdens on manufacturers and suppliers is limiting growth of the United States flooring market. Regulatory bodies such as the Environmental Protection Agency enforce strict limits on volatile organic compound emissions from flooring materials to protect indoor air quality. Compliance with standards, such as California Air Resources Board Section 01350 requires rigorous testing and certification processes, increasing operational expenses. The manufacturers must invest significantly in reformulating products to meet evolving emission standards for adhesives and backing materials. The Toxic Substances Control Act also restricts the use of certain chemicals in flooring production, necessitating the development of alternative formulations that may be more costly or less effective. State level regulations often exceed federal requirements by creating a fragmented regulatory landscape that complicates national distribution strategies. Small manufacturers face disproportionate challenges in absorbing these compliance costs, potentially leading to market consolidation. Additionally, consumers are increasingly aware of environmental impacts, demanding transparency and sustainability credentials that require extensive documentation and verification. Failure to comply with regulations can result in hefty fines and reputational damage, discouraging innovation and new product launches. The tension between regulatory compliance and economic feasibility remains a central challenge, requiring careful navigation to maintain competitiveness while adhering to legal mandates.

MARKET OPPORTUNITIES

Growth in Sustainable and Eco Friendly Flooring Solutions

The growing emphasis on sustainability and eco-friendly practices, particularly in the realm of recycled and renewable materials is certainly to fuel the growth of the United States flooring market. Consumers are increasingly prioritizing products with minimal environmental impact, driving demand for flooring made from reclaimed wood, bamboo, cork, and recycled content. Manufacturers can capitalize on this trend by developing products with low carbon footprints and biodegradable components. The Leadership in Energy and Environmental Design certification system rewards the use of sustainable materials in commercial construction by creating incentives for architects and developers to specify eco-friendly flooring. Recycling programs for old carpet and vinyl are also gaining traction by allowing companies to recover valuable materials and reduce waste. The introduction of bio-based plastics in vinyl production further enhances the sustainability profile of resilient flooring. Brands that transparently communicate their environmental commitments through certifications and labeling can differentiate themselves in a crowded market. Additionally, government incentives for green building practices support the adoption of sustainable flooring options. Embracing these eco-friendly innovations allows firms to align with broader corporate social responsibility goals and appeal to environmentally conscious demographics.

Advancements in Digital Printing and Customization Technologies

The advancements in digital printing and customization technologies by enabling the creation of highly realistic and personalized designs is additionally to surge the growth of the United States flooring market. Digital printing allows manufacturers to reproduce intricate patterns and textures of natural materials such as stone, wood, and concrete with exceptional accuracy on vinyl and laminate surfaces. The digital printing capabilities have expanded the design possibilities for resilient flooring by attracting consumers seeking unique aesthetic solutions without the high cost of natural materials. Customization services enable homeowners and designers to create bespoke flooring patterns, colors, and layouts, by enhancing the emotional connection to the product. The ability to produce small batch runs economically allows manufacturers to respond quickly to trending styles and niche market demands. Augmented reality tools further enhance the shopping experience by allowing customers to visualize flooring options in their own spaces before purchase. This technological integration reduces return rates and increases customer satisfaction. Manufacturers who invest in digital infrastructure can offer greater variety and flexibility, distinguishing themselves from competitors relying on traditional mass production methods. The convergence of technology and design creates compelling value propositions that drive premium pricing and brand differentiation.

MARKET CHALLENGES

Labor Shortages in Installation and Construction Sectors

The labor shortages in the installation and construction sectors by affecting project timelines and quality is a huge challenge for the growth of the United States flooring market. The demand for skilled flooring installers exceeds the available workforce by leading to delays and increased labor costs. According to the National Association of Home Builders, nearly 80% of construction firms report difficulty in finding qualified tradespeople, including floor layers. This scarcity drives up wages and training expenses, squeezing profit margins for contractors and retailers. The aging workforce and insufficient pipeline of young entrants into trades contribute to this ongoing crisis, requiring industry wide initiatives to promote vocational training and apprenticeships. Inexperienced installers may deliver subpar results by leading to customer dissatisfaction and warranty claims that damage brand reputations. The complexity of installing advanced flooring systems such as luxury vinyl plank and engineered hardwood requires specialized skills that are in short supply. Delays in installation can disrupt entire construction schedules, causing friction between contractors and clients.

Intense Competition from Substitute Materials

The intense competition from substitute materials for traditional segments, such as carpet and solid hardwood is also to hinder the growth of the United States flooring market. Alternative flooring options, such as luxury vinyl tile, laminate, and polished concrete offer comparable aesthetics and durability at lower price points by attracting budget conscious consumers. The perception of vinyl and laminate as high quality alternatives has improved with technological advancements by eroding the competitive advantage of traditional materials. Solid hardwood faces pressure from engineered wood products that offer greater stability and lower costs. Retailers and manufacturers must continuously innovate to differentiate their products and justify premium pricing. The proliferation of private label brands in big box stores further intensifies price competition by reducing margins for established brands. Consumers are increasingly informed and willing to switch brands based on value and performance, reducing brand loyalty. This dynamic environment requires constant adaptation and marketing efforts to maintain relevance. Failure to address the threat of substitutes can result in declining sales volumes and diminished market presence.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.62% |

| Segments Covered | By Material, Application, End-User, and Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

| Regions Covered | US, Canada, and the Rest of North America |

| Market Leaders Profiled | Mohawk Industries, Inc., Tarkett, S.A., AFI Licensing, Shaw Industries, Inc., Interface, Inc., Gerflor, Mannington Mills, Inc., Polyflor, LG Hausys Ltd. |

SEGMENT ANALYSIS

By Material Insights

The vinyl flooring segment was accounted in holding 54.3% of the United States flooring market with its versatility, durability, and cost effectiveness, which have gained immense popularity due to their ability to mimic natural materials like wood and stone, while offering superior water resistance. The dominance of vinyl is reinforced by its suitability for both residential and commercial applications, where moisture protection and ease of maintenance are important. Advances in printing technology have enhanced the aesthetic appeal of vinyl by making it a preferred choice for designers and homeowners alike. The material's resilience against scratches and stains further contributes to its widespread adoption in high traffic areas. As consumer preferences shift towards low maintenance and long-lasting solutions, vinyl continues to capture significant market share from traditional materials, such as carpet and laminate.

The wood flooring segment is lucratively growing at an anticipated CAGR of 4.2% from 2026 to 2034 owing to increasing consumer preference for natural and sustainable materials in home design. Hardwood and engineered wood floors are perceived as premium products that enhance property value and aesthetic appeal. The trend towards open concept living spaces has amplified the demand for continuous wood flooring that creates a seamless flow throughout the home. Additionally, advancements in finishing technologies have improved the durability and moisture resistance of wood products, addressing previous limitations. The rise of eco conscious consumers who prioritize responsibly sourced timber further supports this growth. As disposable incomes rise and housing markets stabilize, investment in high quality wood flooring continues to accelerate, outpacing other material categories.

By Application Insights

The residential application segment was the dominant by capturing 32.1% of the United States flooring market share in 2025 with the vast number of housing units, including single family homes, apartments, and condominiums, that require flooring installations. The personal nature of residential spaces encourages frequent updates and renovations, leading to higher consumption volumes compared to commercial sectors. Homeowners prioritize comfort, aesthetics, and durability, influencing the selection of diverse flooring materials. The strong correlation between housing market activity and flooring sales ensures a steady baseline demand. The high volume of housing starts and the extensive existing housing stock are primary drivers of the residential segment's dominance. According to the United States Census Bureau, approximately 1.45 million housing starts were recorded in early 2026, each requiring substantial flooring installations for new constructions. This continuous influx of new homes creates a consistent demand for flooring materials across all price points. Furthermore, the United States has an existing housing stock of over 140 million units, many of which undergo periodic renovations and upgrades. The Joint Center for Housing Studies at Harvard University reports that older homes, particularly those built before 1980, are prime candidates for flooring replacements due to wear and tear or outdated styles. The sheer scale of the residential market ensures that even small%ages of renovation activity translate into significant sales volumes. Regional variations in housing density and construction rates further diversify demand, preventing reliance on single markets.

The commercial application segment is projected to witness a fastest CAGR of 3.8% from 2026 to 2034 with the recovery and expansion of the hospitality, healthcare, and retail sectors. Businesses are investing in facility upgrades to improve customer experience and employee productivity. The demand for durable, low maintenance, and hygienic flooring solutions in high traffic areas is accelerating. Corporate sustainability goals are also influencing procurement decisions, favoring eco friendly commercial flooring options. The recovery and expansion of hospitality and retail sectors are propelling the growth of the segment. Retailers are redesigning stores to create immersive experiences, often utilizing distinctive flooring to define zones and guide customer flow. The emphasis on hygiene and durability in these high traffic environments drives demand for resilient materials such as luxury vinyl tile and commercial grade carpet. New restaurant openings and franchise expansions further contribute to flooring consumption. The need for quick installation and minimal downtime favors modular flooring systems that allow for efficient renovations.

By End Use Insights

The renovation segment was the largest by occupying 55.4% of the United States flooring market share in 2025 with the aging housing stock and the tendency of homeowners to improve rather than move. Renovation projects include full room makeovers, floor replacements, and minor repairs, generating consistent demand for flooring materials. The flexibility of renovation timelines allows consumers to respond to market conditions and personal finances, sustaining activity levels. The prevalence of DIY renovations further amplifies this segment, as individuals undertake smaller projects that cumulatively contribute significant volume. The aging housing stock is fuelling the growth of the segment. Older flooring materials often suffer from wear, damage, or outdated styles, prompting homeowners to replace them. As homes age, structural issues, such as subfloor damage may also necessitate flooring replacement, adding to the volume. The continuous cycle of maintenance and improvement ensures that renovation remains a stable and large source of demand.

The new construction segment is projected to register a fastest CAGR of 4.5% from 2026 to 2034 with the recovery in housing starts and the construction of new commercial facilities. Builders are incorporating modern flooring trends into new designs to appeal to buyers and tenants. The efficiency of installing flooring in new builds that allows for bulk purchasing and standardized processes, driving volume. Each new home requires complete flooring installation by creating immediate and substantial demand for materials. Builders are responding to buyer preferences by including upgraded flooring options as standard features or incentives, boosting volume and value. The construction of multifamily apartments and condominiums also contributes to this growth, as these projects often utilize durable and cost effective flooring solutions. The geographic distribution of new construction in high growth regions further amplifies demand.

COMPETITIVE LANDSCAPE

The competition in the United States flooring market is intense and characterized by the presence of large multinational corporations alongside numerous regional manufacturers. Market leaders compete primarily on product innovation price quality and sustainability credentials. The market exhibits moderate barriers to entry due to significant capital requirements for manufacturing facilities and distribution networks. However, niche players can enter specific segments, such as handmade tiles or custom hardwoods with lower initial investment. Competitive dynamics are driven by the rapid pace of technological advancements in digital printing and material science. Companies strive to differentiate their offerings through unique designs durability and environmental benefits. Price competition remains relevant in commodity segments such as standard carpet and laminate where consumers seek value. Premium segments focus on aesthetics and brand reputation to justify higher price points. Retail partnerships and online presence play crucial roles in determining market visibility and sales volume. Brand loyalty is strong but can be eroded by negative experiences or superior competitor offerings. The threat of substitution among different flooring types such as vinyl replacing carpet is high.

KEY MARKET PLAYERS

A few of the market players in the U.S flooring market include

- Mohawk Industries,

- Inc. Tarkett, S.A.

- AFI Licensing

- Armstrong World Industries Inc

- Shaw Industries, Inc.

- Interface, Inc.

- Gerflor

- Mannington Mills, Inc.

- Polyflor

- LG Hausys Ltd.

Top Players In The Market

- Mohawk Industries Inc stands as a leading global flooring manufacturer with a substantial presence in the United States market. The company offers a comprehensive portfolio including carpet, rugs, ceramic tile, laminate, wood, and luxury vinyl flooring. Mohawk has recently focused on vertical integration to control costs and ensure supply chain stability. The company invested heavily in recycling technologies to produce sustainable flooring materials from post consumer waste. Recent actions include expanding its production capacity for luxury vinyl tile to meet growing consumer demand. Mohawk also launched new digital tools to help customers visualize flooring options in their homes. These initiatives enhance customer experience and drive sales growth. The company continues to prioritize environmental sustainability through reduced water usage and energy efficient manufacturing processes.

- Shaw Industries Group Inc is a major participant in the United States flooring market known for its extensive carpet and hard surface offerings. As a subsidiary of Berkshire-Hathaway, the company benefits from strong financial backing and operational stability. Shaw has recently emphasized sustainable manufacturing practices by increasing the use of recycled materials in its products. The company launched new collections featuring bio-based materials and low volatile organic compound emissions. Shaw expanded its commercial flooring division to serve healthcare and education sectors with durable and hygienic solutions. The company also invested in advanced printing technologies to enhance the aesthetic appeal of its luxury vinyl products. Strategic partnerships with retailers and designers have strengthened its market reach. Shaw focuses on providing high quality products that meet rigorous performance standards. These efforts reinforce its position as a trusted supplier in both residential and commercial segments.

- Armstrong World Industries Inc is a prominent player in the United States flooring market specializing in resilient and mineral fiber ceiling solutions. The company is renowned for its luxury vinyl tile and sheet flooring products used in commercial and institutional settings. Armstrong has recently focused on developing health focused flooring solutions that improve indoor air quality and acoustic comfort. The company introduced new product lines with enhanced durability and ease of maintenance for high traffic areas. Armstrong invested in digital platforms to streamline specification and procurement processes for architects and contractors. The company also expanded its manufacturing capabilities to reduce lead times and improve supply chain reliability. Armstrong prioritizes sustainability by offering products with high recycled content and certified environmental profiles. These strategic moves enhance its value proposition in the commercial sector.

Top Strategies Used By Key Market Participants

Key players in the United States flooring market employ several strategic initiatives to maintain competitiveness and drive growth. Product innovation remains central as companies develop sustainable and high performance flooring solutions to meet evolving consumer preferences. Manufacturers invest heavily in research and development to create eco friendly materials such as recycled vinyl and bio based carpets. Vertical integration is a common strategy where firms control raw material sourcing and production to optimize costs and ensure supply stability. Expansion into digital sales channels and virtual design tools enhances customer engagement and simplifies the selection process. Companies focus on sustainability by obtaining environmental certifications and reducing carbon footprints to appeal to green building projects. Strategic acquisitions allow firms to diversify product portfolios and enter new market segments efficiently. Partnerships with architects and designers help influence specification decisions in commercial projects. Cost management through automation and efficient logistics further supports profitability.

MARKET SEGMENTATION

This research report on the U.S flooring market is segmented and sub-segmented into the following categories.

By Material Type

- Wood

- Vinyl

- Carpet

- Tile

By Application Type

- Residential

- Commercial

By End Use Type

- New Construction

- Renovation

- Maintenance

By Country

- USA

- Canada

- Mexico

Frequently Asked Questions

Why is luxury vinyl flooring so popular right now?

It’s waterproof, scratch-resistant, affordable, and mimics real wood or stone—making it ideal for pets, kids, and high-moisture areas like basements and kitchens.

Is hardwood flooring still in demand?

Yes—especially in high-end renovations and resale upgrades. Consumers value authenticity, but many opt for engineered hardwood for better stability and lower cost.

How are sustainability concerns changing flooring choices?

Buyers and builders now prioritize low-VOC emissions, recycled content, and third-party certifications like FloorScore® or Declare labels—especially in schools and healthcare.

Are carpet sales declining?

In new homes, yes—due to allergy and maintenance concerns. But carpet remains strong in apartments, hotels, and senior living for comfort and noise reduction.

What’s driving the shift to domestic flooring production?

Tariffs on Chinese LVT and supply chain risks have pushed brands to manufacture in the U.S. or nearshore in Mexico—though costs remain higher than pre-2020.

How is the labor shortage affecting flooring projects?

With fewer certified installers, contractors favor click-lock, loose-lay, or pre-glued products that cut installation time—delaying custom or glue-down jobs.

Which regions prefer which flooring types?

Sun Belt states lean toward waterproof LVT for humidity; the Northeast favors hardwood; the West Coast prioritizes eco-friendly and fire-resistant materials.

Is e-commerce replacing physical flooring stores?

Not yet—while online sampling is growing, most buyers still visit showrooms to test texture, color, and durability under real lighting before deciding.

What innovations are emerging in 2025?

Bio-based vinyl (from corn or algae), antimicrobial finishes, and modular tiles with built-in acoustic padding are gaining traction in both residential and commercial spaces.

What’s the biggest challenge for flooring retailers today?

Balancing inventory of fast-moving LVT styles while managing margin pressure from big-box stores—and educating customers on quality differences beyond price.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com