U.S. Insulation Market Size, Share, Trends & Growth Forecast Report Segmented By Disease Indication (Mineral Wools, Foamed Plastics, Cellulose, Aerogels, Others), End-User and Country – Industry Analysis From 2025 to 2033

U.S. Insulation Market Report Summary

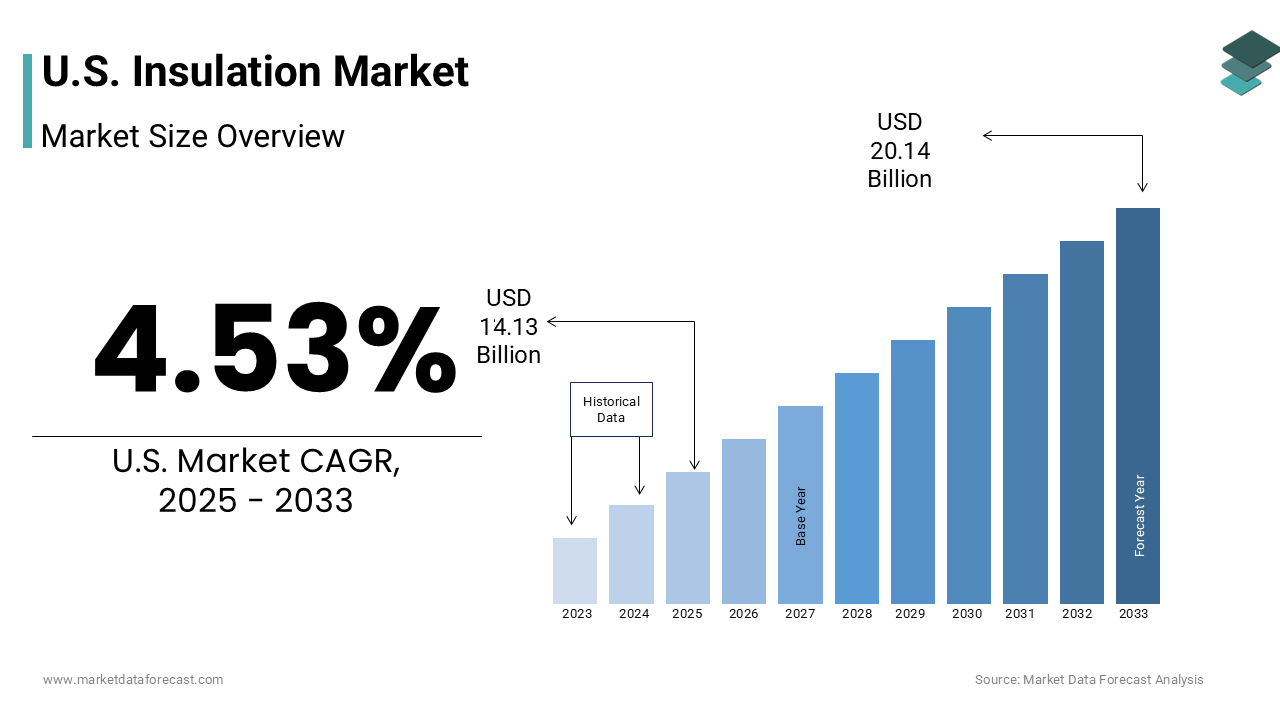

The U.S. insulation market was valued at USD 13.52 billion in 2024, is anticipated to reach USD 14.13 billion in 2025, and is projected to reach USD 20.14 billion by 2033, growing at a CAGR of 4.53% during the forecast period from 2025 to 2033. The growth of the U.S. insulation market is driven by the increasing adoption of energy-efficient construction materials, rising awareness regarding energy conservation, and stringent government building energy codes. The market also benefits from rapid urbanization, infrastructure upgrades, and the growing emphasis on sustainable and green building designs across residential, commercial, and industrial sectors.

Key Market Trends

- Rising demand for high-performance insulation materials driven by energy efficiency standards such as LEED and ENERGY STAR.

- Increasing adoption of eco-friendly and recyclable insulation materials, including glass wool and cellulose.

- Growth in retrofit and renovation projects, particularly in older residential and commercial buildings.

- Expanding usage of insulation in HVAC and industrial applications to improve thermal performance and reduce energy costs.

- Integration of smart insulation systems with IoT-enabled monitoring for industrial facilities.

Segmental Insights

- Based on material, the glass wool segment dominated the U.S. insulation market in 2024, accounting for 62.3% of the total market share. The segment’s dominance is attributed to its superior thermal efficiency, sound absorption properties, and cost-effectiveness, making it a preferred material for residential and commercial insulation applications.

- Based on application, the building and construction segment was the largest in 2024, holding a dominant share of the U.S. insulation market. The segment’s growth is supported by increased adoption of insulation in new housing developments, commercial spaces, and infrastructure projects aimed at reducing energy consumption and improving building sustainability.

Competitive Landscape

The U.S. insulation market is moderately consolidated, with major players focusing on expanding production capacity, introducing eco-friendly insulation materials, and leveraging advanced manufacturing technologies. Strategic mergers, acquisitions, and partnerships are enhancing product portfolios and market presence across key states. Some of the major companies operating in the U.S. insulation market include Owens Corning, Johns Manville, Knauf Insulation, Saint-Gobain, BASF SE, 3M Company, Huntsman Corporation, and Kingspan Group PLC.

U.S. Insulation Market Size

The United States insulation market size was valued at USD 14.13 billion in 2024 and is anticipated to reach USD 14.77 billion in 2025 from USD 21.05 billion by 2034, growing at a CAGR of 4.53% during the forecast period from 2026 to 2034.

The U.S. insulation market is likely to witness sustained development over the next few years, maintaining a robust expansion driven by building safety requirements and green energy initiatives. The U.S. market utilizes a variety of material types, including fiberglass, mineral wool, cellulose, foam plastics, and natural fibers, each offering distinct thermal resistance properties known as R values. As per the U.S. Census Bureau, there are approximately 145 million housing units in the U.S., with a significant portion requiring retrofitting or upgrades to meet modern energy standards. The construction sector consumes the majority of insulation products, driven by both new builds and renovation activities. According to the U.S. Department of Energy, buildings account for nearly 40% of total primary energy consumption in the nation, highlighting the critical importance of effective thermal envelopes. Regulatory frameworks, such as the International Energy Conservation Code, mandate minimum insulation levels for new constructions, influencing material selection and installation practices. The geographic distribution of demand varies significantly, with colder northern states prioritizing high R value materials for heating retention, while southern regions focus on reflective barriers for cooling efficiency. Environmental concerns are increasingly shaping product development, with a shift toward sustainable and recycled content materials. The interplay between building codes, energy prices, and consumer awareness defines the operational landscape of the insulation industry in the U.S.

MARKET DRIVERS

Stringent Building Energy Codes Mandate Higher Performance Standards

The implementation and continuous updating of stringent building energy codes is a primary driver for the U.S. insulation market by legally requiring higher thermal performance in new constructions and major renovations. Codes such as the International Energy Conservation Code, or IECC, set minimum R value requirements for walls, roofs, and floors, which vary by climate zone to ensure optimal energy efficiency. According to the U.S. Department of Energy, the implementation of the 2021 IECC provides a 9.4% site energy savings improvement for residential buildings, saving homeowners thousands of dollars over the life of a typical mortgage, which is driving compliance among builders and developers. State and local jurisdictions increasingly adopt these model codes or enact even stricter regulations to meet climate action goals. This regulatory pressure forces the construction industry to utilize higher quantities of insulation or more advanced materials, such as spray foam and rigid board, to achieve compliance. The enforcement of these codes through permitting and inspection processes ensures widespread adherence across the residential and commercial sectors. Builders must adapt their designs and material sourcing to meet these evolving standards, creating consistent demand for insulation products. The transition toward net zero energy buildings further amplifies this driver, as designers seek to minimize thermal bridging and air leakage. Consequently, regulatory mandates provide a stable and growing baseline for insulation consumption regardless of economic fluctuations.

Rising Residential Retrofit and Renovation Activities Boost Demand

The increasing volume of residential retrofit and renovation projects significantly drives demand for insulation materials, as homeowners seek to improve energy efficiency and reduce utility bills, which is further fuelling the U.S. insulation market expansion. A large portion of the existing U.S. housing stock was built before modern energy codes were established, resulting in inadequate insulation levels and significant energy waste. As per the Harvard Joint Center for Housing Studies, spending on home improvements and repairs in the U.S. reached over 600 billion dollars, with energy related improvements comprising a substantial share of these investments, totaling 139 billion dollars. Homeowners are motivated by rising energy prices and environmental awareness to upgrade attic, wall, and basement insulation. Government incentives, such as tax credits and rebates under the Inflation Reduction Act, further encourage these improvements by offsetting installation costs. The aging housing inventory, particularly in the Northeast and Midwest, requires extensive weatherization to maintain comfort and structural integrity. Professional contractors and DIY enthusiasts alike contribute to this demand, purchasing batts, blown in cellulose, and spray foam kits. The focus on indoor air quality and moisture control also drives the adoption of advanced insulation systems that provide air sealing benefits. This sustained activity in the retrofit sector ensures a robust market for insulation products beyond new construction cycles.

MARKET RESTRAINTS

Volatility in Raw Material Prices Impacts Production Costs

The volatility of raw material prices is a significant restraint for the U.S. insulation market growth, as many insulation products are derived from petroleum based chemicals or energy intensive minerals. Materials such as polyurethane spray foam, extruded polystyrene, and fiberglass rely heavily on inputs like crude oil, natural gas, and silica sand, whose prices fluctuate due to global supply chain dynamics and geopolitical events. As per the U.S. Bureau of Labor Statistics, producer price indices for plastic materials and resins have experienced double digit percentage increases, directly impacting manufacturing costs for foam insulation producers. These cost increases are often passed on to consumers, leading to higher project budgets and potential delays in construction schedules. Manufacturers struggle to maintain profit margins when input costs rise unpredictably, forcing them to adjust pricing strategies frequently. The reliance on fossil fuel derivatives makes the industry vulnerable to energy market shocks, which can disrupt production planning and inventory management. Alternative bio based materials face similar challenges regarding agricultural commodity prices and availability. The inability to fully hedge against raw material price risks limits the financial stability of smaller manufacturers. Consequently, price volatility acts as a persistent constraint on market growth, discouraging price sensitive customers from opting for premium insulation solutions.

Skilled Labor Shortages Hinder Installation Quality and Speed

The shortage of skilled labor in the construction industry poses a substantial restraint to the U.S. insulation market, as proper installation is critical for achieving desired thermal performance. Insulation materials require precise handling and application to avoid gaps, compression, or moisture trapping, which can significantly reduce effectiveness. As per the Associated General Contractors of America, approximately 82% of construction firms report difficulty in finding qualified workers to fill hourly craft positions, highlighting a deep workforce challenge that directly affects mechanical and general labor availability. This labor scarcity leads to project delays, increased labor costs, and potential quality issues that compromise energy efficiency goals. Improperly installed insulation can result in thermal bridging, air leaks, and mold growth, negating the benefits of high performance materials. The complexity of modern insulation systems, such as spray foam, requires specialized training and certification, which are not widely available in the workforce. Training programs take time to develop and scale, exacerbating the immediate shortage. The aging workforce and lack of interest among younger generations in trade careers further deepen the crisis. These operational challenges restrict the capacity of contractors to take on new projects and limit the overall throughput of the insulation market. Without a sufficient skilled workforce, the industry cannot fully capitalize on growing demand.

MARKET OPPORTUNITIES

Adoption of Sustainable and Bio Based Insulation Materials

The growing consumer preference for sustainable and environmentally friendly building materials is a significant opportunity for the U.S. insulation market to expand its product offerings. Bio based insulation materials, such as sheep wool, cotton, hemp, and cork, are gaining traction due to their renewable nature, low embodied carbon, and non-toxic properties. As per the Green Building Council, the demand for LEED certified buildings is increasing, driving specifiers to choose materials with Environmental Product Declarations and low volatile organic compound emissions. These natural alternatives appeal to health conscious homeowners and developers seeking to improve indoor air quality and reduce environmental impact. Manufacturers are investing in research and development to enhance the thermal performance and fire resistance of bio based options, making them competitive with traditional materials. Government incentives for green building practices further support the adoption of these sustainable solutions. The circular economy trend encourages the use of recycled content, such as denim or cellulose from newspaper, which reduces waste and resource extraction. Marketing strategies focused on sustainability and health benefits help differentiate these products in a crowded market. The alignment with corporate social responsibility goals attracts commercial clients committed to environmental stewardship. This shift toward eco-friendly materials opens new revenue streams and market segments for innovative insulation providers.

Integration of Smart Insulation Technologies in Buildings

The integration of smart technologies into insulation systems offers a promising opportunity for the U.S. market by enabling real time monitoring and optimization of building energy performance. Smart insulation materials embedded with sensors can detect temperature changes, moisture levels, and structural integrity, providing valuable data for building management systems. As per the National Institute of Standards and Technology, the adoption of Internet of Things devices in buildings is projected to grow significantly, enhancing the ability to manage energy usage efficiently. These advanced systems allow for predictive maintenance, identifying potential issues such as leaks or thermal breaches before they cause significant damage. The data collected helps optimize heating and cooling operations, reducing energy consumption and extending the lifespan of HVAC equipment. Developers of high performance and net zero buildings are increasingly interested in these intelligent solutions to verify performance claims and ensure compliance with strict energy standards. Partnerships between insulation manufacturers and technology firms facilitate the development of integrated products that offer both thermal resistance and digital connectivity. The ability to demonstrate tangible energy savings through data analytics enhances the value proposition for property owners. This technological convergence positions insulation as an active component of smart building infrastructure rather than a passive material.

MARKET CHALLENGES

Health and Safety Concerns Regarding Chemical Exposure

Health and safety concerns related to chemical exposure during the installation and lifecycle of certain insulation materials pose a major challenge for the U.S. market. Materials such as spray polyurethane foam and fiberglass can release volatile organic compounds, formaldehyde, or irritating particulates that pose risks to installers and occupants if not handled properly. As per the Occupational Safety and Health Administration, strict guidelines govern the use of personal protective equipment and ventilation during insulation installation to mitigate these risks. Negative public perception regarding potential health impacts can deter homeowners from choosing high performance options, despite their superior thermal properties. Litigation and regulatory scrutiny regarding chemical safety further complicate the market environment, requiring manufacturers to invest heavily in testing and compliance. The need for specialized training and certification for installers adds to the cost and complexity of projects. Any incidents of improper installation leading to indoor air quality issues can damage brand reputation and reduce consumer trust. Manufacturers are under pressure to develop safer formulations and transparent labeling to address these concerns. The balance between performance and safety remains a delicate issue that requires ongoing education and regulation. These health related challenges restrict market acceptance and necessitate rigorous quality control measures.

Competition from Alternative Energy Efficiency Measures

Competition from alternative energy efficiency technologies and measures presents a significant challenge to the U.S. insulation market, as building owners seek holistic solutions for energy reduction. Advances in high performance windows, smart thermostats, and efficient HVAC systems offer compelling returns on investment that may compete for the same capital budget as insulation upgrades. As per the American Council for an Energy Efficient Economy, other energy efficiency measures often provide immediate, visible benefits, such as improved comfort or convenience, which can overshadow the invisible benefits of insulation. Building designers and engineers may prioritize air sealing and mechanical system upgrades over adding bulk insulation, especially in space constrained retrofits. The diminishing returns of adding excessive insulation thickness compared to upgrading to a high efficiency heat pump can influence decision making. Consumers may perceive insulation as a onetime static improvement, whereas smart technologies offer ongoing optimization and control. The fragmentation of the home improvement market means that insulation providers must compete for attention and budget against a wide array of service providers. This competitive landscape requires insulation manufacturers to clearly articulate the foundational role of thermal envelopes in overall building performance. Failure to differentiate the unique value of insulation can lead to lost opportunities in comprehensive energy retrofit projects.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Material Type, Application and Region. |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Key Market Players | Owens Corning, Johns Manville, Knauf Insulation, Saint-Gobain, BASF SE, 3M Company, Huntsman Corporation, Kingspan Group PLC |

SEGMENTAL ANALYSIS

By Material Type Insights

The mineral wool segment dominated the market by accounting for the largest share of the U.S. market in 2025. The dominance of this segment in the U.S. market is primarily due to its non-combustible nature and superior fire resistance capabilities, which are increasingly mandated by building codes. Unlike organic foam plastics, mineral wool can withstand temperatures exceeding 1000 degrees Celsius without melting or releasing toxic fumes, making it a critical material for fire safety in commercial and high rise residential structures. As per the National Fire Protection Association, building fires cause billions of dollars in property damage annually, prompting stricter adherence to fire rated assembly requirements that favor mineral wool products. This material is extensively used in fire stops, curtain walls, and structural steel protection, ensuring compliance with International Building Code standards. The inherent durability of mineral wool also provides excellent acoustic insulation, reducing noise transmission in multi-family housing and office buildings. Its resistance to moisture and mold growth further enhances its appeal in humid climates, where organic materials may degrade. Manufacturers benefit from the abundance of raw materials, such as basalt and recycled slag, which are widely available across the U.S. The established production infrastructure and familiarity among contractors ensure consistent supply and reliable installation practices. These safety and performance attributes solidify mineral wool as the dominant choice for applications where fire protection is a primary concern.

However, the aerogels segment is a prominent segment and is estimated to witness the fastest CAGR in the U.S. insulation market during the forecast period owing to their exceptional thermal resistance per unit thickness, which addresses the need for high performance insulation in space constrained applications. With an R value significantly higher than traditional materials, aerogels allow for thinner insulation layers while achieving equivalent or superior energy efficiency. According to the National Aeronautics and Space Administration, aerogel technology, originally developed for space exploration, is increasingly adapted for commercial and industrial use due to its lightweight and highly porous structure. This material is particularly valuable in retrofit projects, where adding bulk insulation is not feasible due to architectural or spatial limitations. The oil and gas industry utilizes aerogel blankets for subsea pipelines and offshore platforms, where weight and space are critical factors. The automotive sector is also exploring aerogels for electric vehicle battery thermal management to enhance safety and range. Although the initial cost is higher, the long term energy savings and performance benefits justify the investment for high value applications. Advances in manufacturing processes are gradually reducing production costs, making aerogels more accessible to broader markets. The unique properties of aerogels position them as a premium solution for specialized insulation needs, driving rapid market expansion.

By Application Insights

The building and construction segment held the leading position in the U.S. insulation market in 2025 due to the continuous volume of new residential and commercial construction projects across the country. Insulation is a mandatory component in all new builds to meet energy code requirements, ensuring consistent demand regardless of economic fluctuations. As per the U.S. Census Bureau, hundreds of thousands of new housing units are authorized for construction annually, each requiring substantial amounts of insulation for walls, roofs, and foundations. The commercial sector, including offices, retail spaces, and warehouses, also contributes significantly to demand, due to larger floor areas and stringent energy performance standards. The geographic diversity of the U.S. necessitates varied insulation solutions tailored to different climate zones, from cold northern states to hot southern regions. The integration of insulation into building envelopes is critical for maintaining indoor comfort and reducing HVAC loads. Builders and developers prioritize insulation quality to enhance property value and attract energy conscious buyers. The established supply chains and distribution networks for construction materials facilitate efficient delivery to job sites. These factors collectively establish building and construction as the dominant application segment for insulation in the U.S.

On the other side, the transportation segment is anticipated to register promising growth during the forecast period in the U.S. market owing to the rapid expansion of the electric vehicle market and the critical need for battery thermal management. EV batteries require precise temperature control to ensure safety, performance, and longevity, necessitating advanced insulation materials that can withstand high voltages and thermal runaway conditions. As per the Alliance for Automotive Innovation, sales of electric vehicles in the U.S. have increased substantially, requiring specialized insulation solutions, such as aerogels and mica plates. These materials provide superior thermal protection and fire resistance, preventing heat propagation between battery cells. The lightweight nature of advanced insulation materials also contributes to overall vehicle efficiency by reducing mass. Automakers are investing heavily in research and development to integrate innovative insulation technologies into vehicle designs. The transition from internal combustion engines to electric powertrains creates new opportunities for insulation manufacturers to supply high value components. Regulatory safety standards for EVs mandate rigorous testing and certification of battery systems, further driving demand for reliable insulation. The growing production capacity of EV manufacturers in the U.S. ensures a robust pipeline for insulation demand. These factors position transportation as the fastest growing application segment in the U.S. insulation market.

COMPETITIVE LANDSCAPE

The competitive landscape of the U.S. insulation market is characterized by intense rivalry among established multinational corporations and regional manufacturers who strive to differentiate through product quality and sustainability credentials. Major competitors compete on factors such as thermal performance ease of installation and environmental impact rather than price alone due to the commoditized nature of basic insulation materials. The shift toward green building practices has intensified competition for eco-friendly products and certifications such as LEED and Energy Star. Firms are increasingly investing in research and development to create innovative materials like aerogels and bio based foams that offer superior efficiency. Regulatory frameworks regarding energy efficiency and fire safety shape competitive dynamics by favoring companies with robust compliance capabilities. Supply chain resilience has become a critical differentiator as disruptions highlight the importance of localized production and raw material sourcing. Collaborative efforts between manufacturers and construction stakeholders are becoming more common to drive innovation and secure long term contracts. This dynamic environment requires continuous adaptation and strategic investment to maintain relevance and profitability in a rapidly evolving market structure driven by sustainability mandates.

KEY MARKET PLAYERS

A few of the major companies in the U.S. Insulation Market include

- Owens Corning

- Johns Manville

- Knauf Insulation

- Saint-Gobain

- BASF SE

- 3M Company

- Huntsman Corporation

- Kingspan Group PLC

Top Market Players

Owens Corning

Owens Corning stands as a global leader in building materials with a dominant presence in the U.S. insulation market through its extensive portfolio of fiberglass and foam solutions. The company leverages its strong brand recognition and distribution network to serve residential and commercial sectors effectively. Recent actions include significant investments in manufacturing capacity expansion and the development of sustainable product lines such as EcoTouch insulation. Owens Corning focuses on digital transformation to enhance customer experience and supply chain efficiency. The company actively engages in sustainability initiatives aiming to reduce carbon footprint across its operations. Strategic partnerships with builders and contractors strengthen its market position by ensuring product availability and technical support. These efforts reinforce its leadership by delivering high performance energy efficient solutions that meet evolving regulatory standards and consumer preferences for green building materials.

Knauf Insulation

Knauf Insulation operates as a major participant in the U.S. market specializing in glass mineral wool and eco friendly insulation technologies. The company distinguishes itself through its commitment to sustainability by utilizing recycled materials and bio based binders in its production processes. Recent initiatives focus on expanding its ECOSE technology which eliminates formaldehyde and reduces embodied energy in insulation products. Knauf invests heavily in research and development to create innovative solutions for acoustic and thermal performance. The company strengthens its market position by collaborating with architects and engineers to promote sustainable building practices. Strategic expansions of production facilities ensure consistent supply to meet growing demand. By prioritizing environmental stewardship and product innovation Knauf builds strong relationships with customers who value health and sustainability. These actions enhance its competitive edge in the increasingly eco conscious construction industry.

Johns Manville

Johns Manville contributes significantly to the U.S. insulation market by offering a diverse range of premium insulation systems for commercial industrial and residential applications. The company is known for its high quality fiberglass mineral wool and foam products that deliver superior thermal and acoustic performance. Recent actions include the launch of advanced roofing and insulation integrated systems that enhance building envelope efficiency. Johns Manville focuses on digital tools and training programs to support contractors and distributors in proper installation techniques. The company invests in sustainable manufacturing practices to reduce waste and energy consumption. Strategic acquisitions and partnerships expand its product offerings and geographic reach. By emphasizing technical expertise and customer service Johns Manville maintains a strong reputation for reliability and innovation. These initiatives strengthen its market presence by addressing complex building challenges and supporting long term energy efficiency goals.

Top Strategies Used by Key Market Participants

Key players in the U.S. insulation market primarily employ strategies focused on product innovation and sustainability to maintain competitive advantages. Companies are increasingly investing in research and development to create eco friendly materials with lower embodied carbon and higher thermal performance. Strategic expansions of manufacturing facilities ensure consistent supply and reduce logistical costs for regional markets. Digitalization of sales channels and customer support platforms enhances user experience and streamlines procurement processes. Partnerships with construction firms and architects promote the adoption of advanced insulation systems in new projects. Compliance with stringent energy codes drives the development of high R value products. These strategic moves collectively strengthen market positions by addressing economic environmental and regulatory challenges inherent in the building materials industry landscape today.

MARKET SEGMENTATION

This research report on the U.S. insulation market has been segmented based on the following categories.

By Material

- Mineral Wools

- Glass Wool

- Stone Wool

- Foamed Plastics

- Expanded Polystyrene

- Extruded Polystyrene

- Polyurethane

- Polyisocyanurate

- Others

- Cellulose

- Aerogels

- Others

By Application

- HVAC & OEM

- Transportation

- Packaging

- Building & Construction

- Others

By Country

- California

- Washington

- Oregon

- New York

- Rest of the United States

Frequently Asked Questions

What is the U.S. insulation market?

The U.S. insulation market involves the production and sale of materials used to reduce heat, sound, or energy loss in residential, commercial, and industrial buildings.

What drives growth in the U.S. insulation market?

Growth is driven by increasing energy efficiency regulations, construction activities, and demand for sustainable buildings.

Who are the key players in the U.S. insulation market?

Owens Corning, Johns Manville, Knauf Insulation, Saint-Gobain, BASF SE, 3M Company, Huntsman Corporation, Kingspan Group PLC.

What trends are shaping the U.S. insulation market?

Green building trends, advanced materials like spray foam, and smart insulation solutions are key trends.

What challenges does the market face?

High raw material costs, volatile supply chains, and skilled labor shortages are common challenges.

What is the future outlook for the U.S. insulation market?

The market is expected to grow steadily due to sustainable building initiatives, regulatory support, and technological innovation.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com