U.S. Intraoperative Neuromonitoring (IONM) Market Size, Share, Trends & Growth Forecast Report Segmented By Product & Service (Systems, Services, Accessories & Consumables),Source Type, Monitoring Modality, and Country – Industry Analysis From 2025 to 2033

U.S. Intraoperative Neuromonitoring (IONM) Market Size

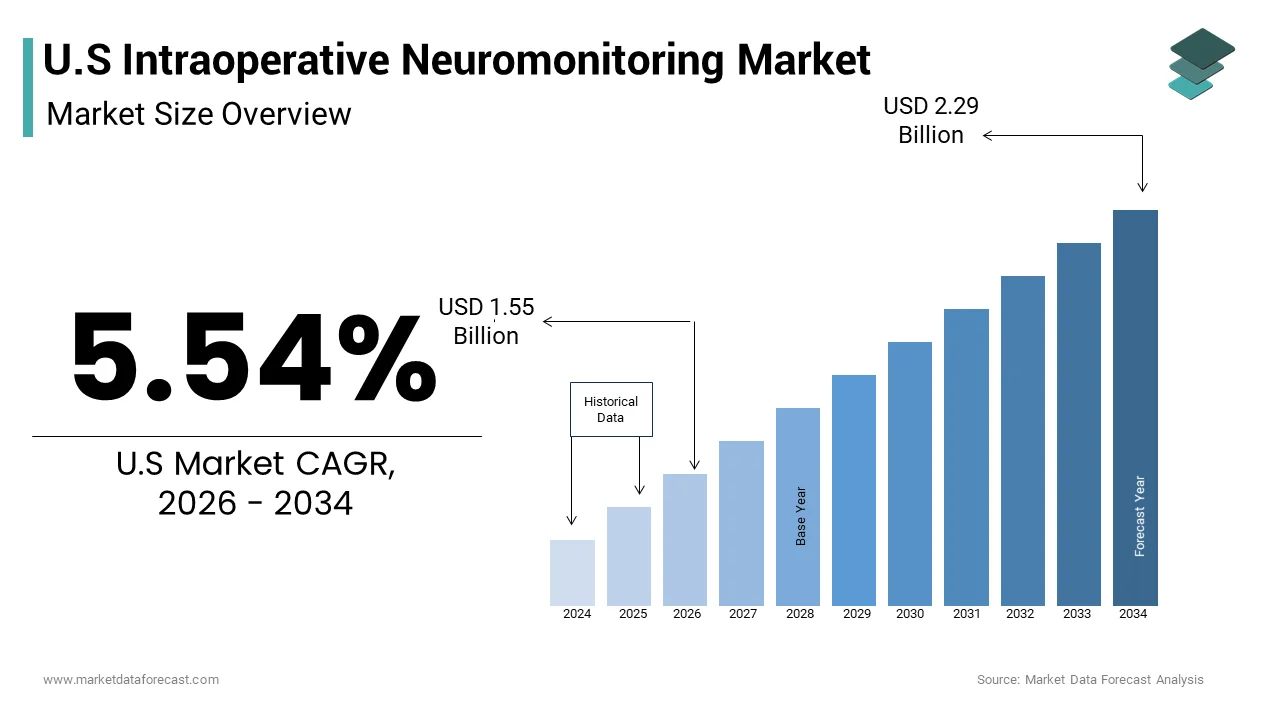

The U.S. intraoperative neuromonitoring (IONM) market size was valued at USD 4.12 billion in 2024 and is anticipated to reach USD 4.36 billion in 2025 from USD 6.82 billion by 2033, growing at a CAGR of 5.75% during the forecast period from 2025 to 2033.

Intraoperative neuromonitoring (IONM) is a safeguard woven into the fabric of high-risk neurosurgical and spinal interventions, where milliseconds of delayed signal detection can mean the difference between paralysis and preservation of function.

MARKET DRIVERS

Surgeon-Led Adoption Driven by Malpractice Risk Mitigation and Surgical Precision Demands

The escalation in neurological injury-related malpractice claims is propelling the growth of U.S. intraoperative neuromonitoring (IONM) market. According to the National Practitioner Data Bank, surgical negligence claims involving permanent nerve damage increased by 43% between 2018 and 2023. In response, hospital risk management teams now require IONM protocols as mandatory pre-authorization for high-risk cases, especially in states like California and New York, where jury awards for sensory or motor deficits are among the nation’s highest.

Proliferation of Minimally Invasive and Robotic-Assisted Neurosurgical Procedures

The penetration of minimally invasive and robotic assisted neurosurgical procedures are bolstering the growth of U.S. intraoperative neuromonitoring (IONM) market. The FDA cleared 14 new robotic-assisted spine systems between 2020 and 2023, including the Mazor X and Globus ExcelsiusGPS platforms, all of which integrate IONM alerts directly into their guidance interfaces.

MARKET DRIVERS

Workforce Shortages in Certified Neurophysiologists and Technical Staff

The U.S. faces a shortage of qualified neurophysiologists trained to interpret IONM signals in real time, which is degrading the growth of U.S. intraoperative neuromonitoring (IONM) market. Training programs produce fewer than 150 new specialists annually, while the number of complex surgeries requiring IONM has risen by 29% since 2020, according to the Centers for Medicare & Medicaid Services.

Reimbursement Ambiguity and Insurance Denial Patterns

The inconsistent and often adversarial reimbursement from private insurers and even Medicare is also hindering the growth of U.S. intraoperative neuromonitoring (IONM) market. Insurers frequently challenge billing when multiple modalities are used simultaneously even though guidelines from the American Clinical Neurophysiology Society endorse multimodal monitoring for high-risk cases. Hospitals report spending up to $180,000 annually on appeals and legal fees to recover denied payments, diverting resources from staffing and equipment upgrades.

MARKET OPPORTUNITIES

Integration of AI-Powered Real-Time Signal Interpretation and Anomaly Detection

The integration of AI-powered real time signal interpretation and anomaly detection is creating new opportunities for the growth of U.S. intraoperative neuromonitoring (IONM) market. These systems reduce false negatives by 47% and decrease cognitive load on technologists, allowing one specialist to monitor up to four simultaneous cases safely. The FDA has granted Breakthrough Device designation to three AI-enhanced IONM platforms, including Medtronic’s NeuroGuard AI and Natus’ IntelliMonitor Pro, paving the way for regulatory approval as adjunctive decision-support tools.

Expansion into Non-Traditional Surgical Environments and Outpatient Settings

The ambulatory surgery centers (ASCs) and outpatient spine clinics performing high-volume cervical and lumbar fusions are also to show up new opportunities for the growth of U.S. intraoperative neuromonitoring (IONM) market. Portable, wireless IONM systems with cloud-based telemetry enable real-time monitoring in decentralized settings, which is reducing patient transport risks and lowering overall costs.

MARKET CHALLENGES

Fragmentation of Standards and Lack of Universal Protocol Alignment

Fragmentation of standards and lack of universal protocol alignment are sophistically leveraging the growth of U.S. intraoperative neuromonitoring (IONM) market. As per 2022 multi-institutional audit by the Joint Commission, 56% of facilities lacked standardized documentation templates for IONM events, and 31% did not have written escalation protocols for signal loss. This inconsistency undermines research validity, complicates training, and exposes institutions to liability if outcomes vary due to procedural divergence rather than surgical skill.

Technological Obsolescence Due to Rapid Innovation Cycles and Vendor Lock-In

The IONM systems are highly specialized, proprietary ecosystems dominated by a handful of manufacturers such as Natus, Medtronic, and Cadwell. A 2023 survey by Health Affairs revealed that 41% of rural hospitals continue using IONM systems over eight years old, lacking the capital to upgrade despite declining reliability and increased false alarms

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Product & Service, Source Type, Monitoring Modality and Region. |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East, and Africa |

| Key Market Players | Natus Medical Incorporated, Medtronic plc, NuVasive, Inc., SpecialtyCare, Nihon Kohden Corporation, IntraNerve Neuroscience Holdings, Accurate Monitoring, Neural Monitoring Associates, Procirca, and Moberg Research, Inc. |

SEGMENTAL ANALYSIS

By Product & Services Insights

The services segment was the largest and held a dominant share of U.S. intraoperative neuromonitoring (IONM) market in 2024. This dominance arises not from equipment cost but from the irreplaceable human expertise required to interpret complex neurophysiological signals in real time during high-stakes procedures.

The systems segment is projected to expand at a CAGR of 11.8% in coming years with the integration of AI-enhanced hardware platforms, wireless sensor arrays, and automated signal processing tools that reduce dependence on manual interpretation. Companies like Natus Medical and Medtronic have launched next-generation IONM consoles with embedded machine learning algorithms that flag early amplitude decay or latency shifts before human technologists detect them byreducing false negatives by up to 47%. These systems also feature modular, interoperable components allowing hospitals to scale incrementally without full-suite overhauls.

By Source Type Insights

The Outsource Monitoring segment held a significant share of the U.S. intraoperative neuromonitoring (IONM) market in 2024 with the acute shortage of certified neurophysiologists and the prohibitive cost of maintaining in-house teams capable of 24/7 coverage across multiple operating rooms. In rural and community hospitals, outsourcing eliminates the need for $500,000+ capital expenditures on equipment and training while ensuring compliance with Joint Commission standards.

The insource monitoring segment is likely to grow with an expected CAGR of 14.9% during the forecast period. Newer systems now feature one-touch setup, automated baseline generation, and color-coded alert thresholds that allow anesthesiologists or perioperative nurses to initiate basic monitoring with minimal training. Medicare’s 2023 update to CPT code 95940 now permits “incident-to” billing when services are rendered under physician supervision, making it financially viable for ASCs and small hospitals to invest in their own systems.

By Monitoring Modality Insights

The Somatosensory Evoked Potentials (SSEP) segment is attributed in holding a significant share of U.S. intraoperative neuromonitoring (IONM) market in 2024. Its non-invasive nature, low susceptibility to anesthesia interference, and well-established normative data make it the universal starting point for any procedure involving the spinal axis.

The Motor Evoked Potentials (MEP) segment is likely to grow with an expected CAGR of 16.3% during the forecast period with the increasing prevalence of anterior spinal approaches, robotic-assisted fusion, and awake craniotomies procedures where motor pathway preservation is paramount and SSEP alone is insufficient. MEP directly assesses corticospinal tract function, detecting impending paralysis before irreversible damage occurs, with sensitivity exceeding 90% in lumbar decompression cases, per a 2023 meta-analysis in Neurosurgery. Additionally, new integrated systems from Medtronic and Natus now synchronize MEP with navigation software, triggering automatic alerts when trajectory deviations threaten motor tracts.

REGIONAL ANALYSIS

New York Intraoperative Neuromonitoring (IONM) Market Analysis

New York held 16.3% of U.S. intraoperative neuromonitoring (IONM) market share in 2024 with its position as the epicenter of academic neurosurgery and high-volume tertiary care drives unmatched demand for advanced, multimodal IONM. The state’s stringent malpractice environment mandates IONM for nearly all spinal fusions, and its Medicaid program explicitly reimburses for comprehensive monitoring protocols.

California Intraoperative Neuromonitoring (IONM) Market Analysis

California was positioned second by holding 14.3% of share in 2024. Home to Silicon Valley’s medtech innovation ecosystem, California leads in adopting AI-enhanced IONM platforms and wireless telemetry systems that enable remote expert oversight across geographically dispersed hospitals. UC San Francisco pioneered the use of real-time IONM data dashboards integrated into EHRs, allowing surgical teams to review trends retrospectively for quality improvement.

KEY MARKET PLAYERS

A few of the major companies in the U.S. intraoperative neuromonitoring (IONM) market include

- Natus Medical Incorporated

- Medtronic plc

- NuVasive, Inc.

- SpecialtyCare

- Nihon Kohden Corporation

- IntraNerve Neuroscience Holdings

- Accurate Monitoring

- Neural Monitoring Associates

- Procirca

- Moberg Research, Inc.

MARKET SEGMENTATION

This research report on the U.S. intraoperative neuromonitoring (IONM) market has been segmented based on following categories.

By Product & Service

- Systems

- Services

- Accessories & Consumables

By Source Type

- Insourced Monitoring

- Outsourced Monitoring

By Monitoring Modality

- Somatosensory Evoked Potentials (SSEPs)

- Motor Evoked Potentials (MEPs)

- Electroencephalography (EEG)

- Electromyography (EMG)

- Auditory & Visual Evoked Potentials (BAEPs, VEPs)

By Surgical Application

- Spinal Surgery

- Neurosurgery

- Orthopedic Surgery

- ENT & Thyroid Surgery

- Vascular & Cardiovascular Surgery

- Other Complex Procedures

Frequently Asked Questions

What is driving the growth of the U.S. IONM market?

The market is driven by the increasing number of complex surgeries, rising awareness about patient safety, technological advancements in monitoring systems, and a growing preference for outsourced IONM services.

What are the main components of IONM systems?

The key components include monitoring systems, electrodes, software, and accessories used to record and interpret electrical signals from the nervous system.

What are the major challenges in the IONM market?

Challenges include a shortage of trained professionals, high service costs, and reimbursement limitations in certain regions.

What is the forecast outlook for the U.S. IONM market?

The market is expected to grow steadily over the next decade due to increased adoption of neuromonitoring across surgical disciplines and continuous technological innovation.

What are the trends shaping the future of the IONM market?

Trends include AI integration in monitoring software, remote neuromonitoring, cloud-based data analysis, and partnerships between device manufacturers and service providers.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com