U.S. Probiotics Market Size, Share, Trends And Growth Forecasts Research Report, Segmented By Product, Distribution Channel & Country - Industry Analysis (2026 to 2034)

U.S. Probiotics Market Report Summary

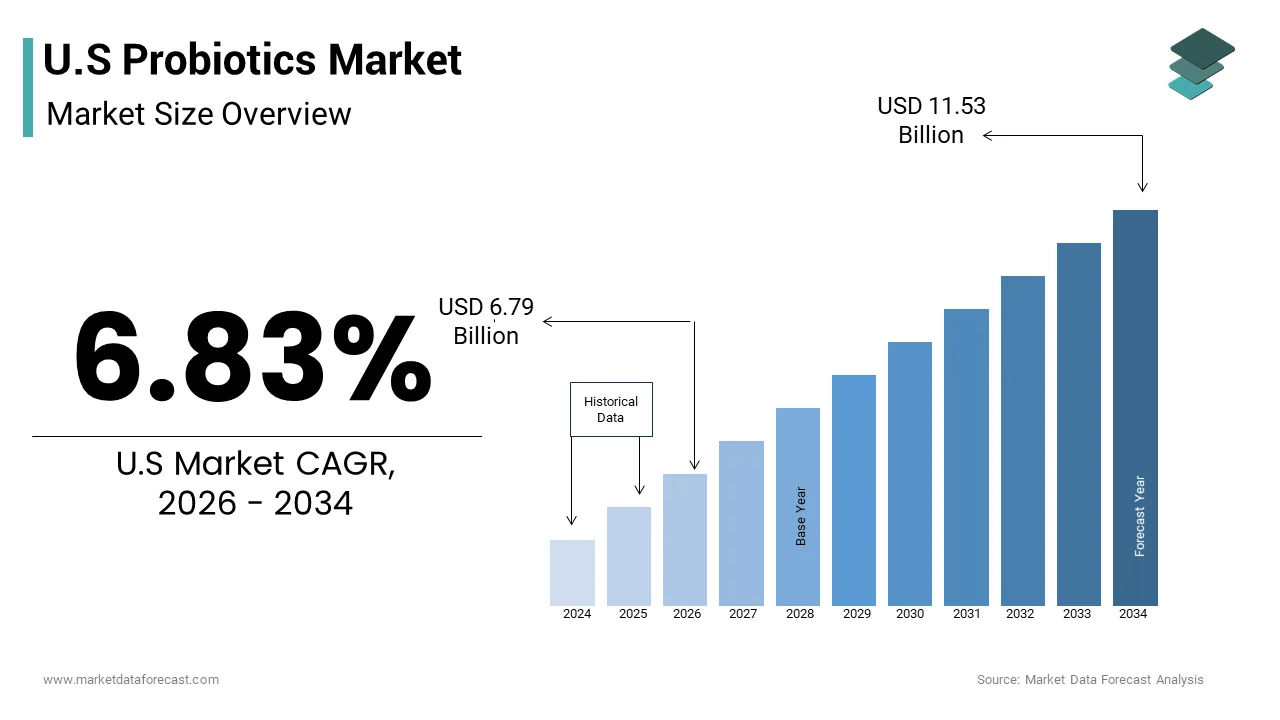

The U.S. probiotics market was valued at USD 6.36 billion in 2025, is estimated to reach USD 6.79 billion in 2026, and is projected to reach USD 11.53 billion by 2034, growing at a CAGR of 6.83% from 2026 to 2034. The growth of the U.S. probiotics market is driven by increasing consumer awareness of gut health, the rising prevalence of digestive disorders, and growing demand for functional foods and beverages. Additionally, the adoption of probiotics in dietary supplements, skincare products, and animal nutrition, along with innovations in formulation and delivery methods, is further propelling market expansion.

Key Market Trends

- Rising consumer focus on gut microbiome health and its link to immunity and mental well-being.

- Expanding availability of probiotic-infused foods and beverages, including yogurts, juices, and snacks.

- The increasing popularity of vegan and plant-based probiotic products among health-conscious consumers.

- Growing integration of probiotics in dietary supplements and nutraceuticals for preventive healthcare.

- Advancements in microencapsulation and strain-specific research to improve probiotic stability and efficacy.

Segmental Insights

- Based on distribution channel, the supermarkets and hypermarkets segment held 47.4% of the U.S. probiotics market share in 2025, driven by widespread product accessibility, strong brand visibility, and increasing consumer preference for purchasing probiotic-rich foods and beverages through organized retail outlets.

Competitive Landscape

- The U.S. probiotics market is highly competitive, with companies focusing on product innovation, clean-label formulations, and strategic distribution partnerships.

- Manufacturers are investing in R&D for strain differentiation, product diversification, and advanced delivery technologies to enhance consumer benefits.

- Prominent players in the U.S. probiotics market include Danone SA, Chobani LLC, General Mills Inc., PepsiCo Inc. (KeVita), Now Foods, Yakult Honsha, BioGaia AB, Lifeway Foods, Inc., Nestlé SA, Procter & Gamble Company, i-Health (Culturelle), Suja Life, Wren Laboratories Ltd., Groupe Lactalis S.A., Seven Turns Private Limited (The Good Bug), Culture Pop, Nature’s Garden, Nutritionalab Private Limited, Vlado Sky Enterprise Pvt Ltd, and Hero Group.

- These companies are emphasizing product innovation, consumer education, and expansion into plant-based and personalized probiotic solutions to strengthen their market presence and cater to evolving health and wellness trends in the U.S.

U.S Probiotics Market Size

The U.S probiotics market size was valued at USD 6.36 billion in 2025 and is anticipated to reach USD 6.79 billion in 2026 to reach USD 11.3 billion by 2034, growing at a CAGR of 6.83% during the forecast period from 2026 to 2034.

According to the National Center for Complementary and Integrative Health, approximately 4 million U.S. adults used probiotics or prebiotics within a 30 day period, representing 1.6% of the adult population. As per the National Institute of Diabetes and Digestive and Kidney Diseases, digestive diseases affect 60 to 70 million individuals across the United States, creating substantial underlying demand for microbiome focused interventions. According to a 2024 survey from Danone North America, 84% of Americans have become more interested in foods or products that support gut health in recent years. As per an Ipsos poll conducted for MDVIP, 85% of Americans received a failing grade on a quiz assessing microbiome knowledge, indicating significant educational gaps. The Food and Drug Administration regulates probiotics through multiple pathways including dietary supplements, foods, and drugs, depending on intended use and claimed benefits. According to a systematic review and meta-analysis published in BMJ Open, clinical evidence supports probiotic efficacy for specific indications such as antibiotic associated diarrhoea where pooled analyses demonstrate that co-administration reduces the risk by 37% when probiotics accompany antibiotic therapy. This complex interplay of consumer interest, clinical validation, and regulatory oversight defines the contemporary U.S. probiotics landscape.

MARKET DRIVERS

Rising Prevalence of Digestive Disorders Fuels Probiotic Adoption

The escalating burden of gastrointestinal conditions across the United States majorly drives the U.S. probiotics market expansion. As per the National Institute of Diabetes and Digestive and Kidney Diseases, digestive diseases impact between 60 and 70 million Americans, generating substantial demand for supportive interventions. According to research published in Clinical Gastroenterology and Hepatology, more than 40% of adults reported one or more digestive symptoms monthly, including abdominal pain or discomfort, bloating, and diarrhea. As per a claims based analysis of U.S. insurance data, digestive disease prevalence reached 33.2% among privately insured individuals and 51.5% among Medicaid beneficiaries, highlighting widespread clinical need. Antibiotic associated diarrhea represents another significant driver with incidence rates ranging from 5% to 35% among patients receiving antibiotic therapy according to epidemiological surveys. According to meta-analyses of clinical trials, probiotic co-administration reduces antibiotic associated diarrhea likelihood by approximately 50%, providing compelling evidence for preventive use. Consumer behavior data reinforces this trend as 46% of Americans report using over the counter digestive products including fiber supplements and laxatives while 41% have taken probiotics specifically for gut health management according to market intelligence. The convergence of high symptom prevalence, documented clinical benefits, and proactive consumer self-care behaviors creates sustained demand momentum for probiotic formulations targeting digestive wellness.

Growing Consumer Awareness of Microbiome Health Drives Market Penetration

Expanding public understanding of the gut microbiome and its systemic health implications significantly propels probiotic market growth in the United States. According to a late 2024 Danone North America survey, 88% of Americans are now familiar with probiotics, representing a 4 percentage point increase from 2021. As per the same research, 76% of consumers recognize prebiotics and 60% acknowledge postbiotics, which is indicating broadening awareness of the complete biotics ecosystem. Despite knowledge gaps, an Ipsos poll revealed that 68% of Americans correctly identify stress as influencing gut bacterial balance while 67% understand sleep impacts microbiome composition. Consumer interest translates directly to purchasing behavior as 51% of Americans incorporate probiotics into their diets specifically to promote gut health and 33% utilize them to bolster immune function according to market intelligence data. The connection between gut health and broader wellness priorities strengthens adoption with research showing that 82% of U.S. consumers believe digestive health greatly influences overall physical well being. Social media engagement and digital health content amplify awareness as Google searches for gut health related terms have more than doubled over a three year period. This expanding knowledge base combined with increasing health consciousness creates a receptive consumer environment that supports continued probiotic market expansion across multiple product categories and distribution channels.

MARKET RESTRAINTS

Regulatory Complexity Creates Product Development Uncertainty

The fragmented regulatory framework governing probiotics in the United States presents a significant restraint on the U.S. probiotics market growth. According to the Centers for Disease Control and Prevention, probiotic products may be regulated as dietary supplements, foods, or drugs, depending on intended use, creating compliance ambiguity for manufacturers. As per the Food and Drug Administration, dietary supplements do not require premarket approval, yet manufacturers bear responsibility for substantiating safety and structure function claims without standardized efficacy verification protocols. This regulatory variability increases development costs and timelines as companies must navigate distinct requirements for each product category while managing potential enforcement actions for non-compliant labeling. According to the National Center for Complementary and Integrative Health, probiotics marketed as drugs must undergo rigorous clinical trials and FDA approval processes similar to pharmaceutical products, creating substantial barriers for therapeutic applications. Furthermore the absence of a unified definition for probiotics within U.S. regulatory statutes complicates product classification and claim substantiation according to industry analyses. Recent FDA warning letters regarding probiotic use in neonatal intensive care units demonstrate enforcement risks that may deter investment in certain clinical applications. This regulatory uncertainty discourages smaller innovators from entering the market and limits the translation of emerging clinical research into commercially available products, ultimately constraining category evolution and consumer access to evidence based formulations.

Limited Strain Specific Clinical Evidence Restricts Consumer Confidence

The insufficient availability of strain specific clinical data for many probiotic products undermines consumer trust and limits market expansion potential. According to research published in Clinical Infectious Diseases, strong evidence supports the hypothesis that probiotic efficacy is both strain specific and disease specific, yet many commercial products lack rigorous validation for their particular formulations. As per a systematic review analyzing 228 clinical trials, only a subset of probiotic strains demonstrated statistically significant benefits for defined health outcomes, creating confusion among consumers seeking evidence based options. According to the National Institutes of Health Office of Dietary Supplements, researchers have not yet determined which specific probiotics are helpful for most health conditions, what dosages are effective, or which populations would benefit most. This evidence gap is particularly pronounced in the United States where a PubMed analysis revealed that only 3 of 27 human probiotic studies published in a nine month period were conducted domestically, limiting locally relevant clinical data. According to Danone research, consumer surveys reflect this uncertainty as 41% of Americans remain unaware of the gut microbiome concept and 50% do not recognize its impact on gut health. Without clear strain outcome correlations consumers struggle to differentiate products leading to purchase hesitation and brand switching behavior. This evidence deficit also complicates healthcare provider recommendations reducing clinical endorsement opportunities that could accelerate mainstream adoption across diverse patient populations.

MARKET OPPORTUNITIES

Personalized Probiotic Formulations Present Significant Growth Potential

The emergence of microbiome testing and personalized nutrition creates substantial opportunity for targeted probiotic product development in the United States. According to clinical research published in Frontiers in Microbiology, the majority of probiotic studies registered on ClinicalTrials.gov originate from the United States or Europe, representing 56% of global trials, indicating robust research infrastructure to support innovation. As per advances in genomic sequencing and bioinformatics companies can now analyze individual microbiome profiles to recommend strain specific probiotic interventions tailored to unique physiological needs. Consumer interest in personalization is substantial with survey data showing that 64% of Americans consider clinically supported health claims on packaging highly important when selecting probiotic products. The integration of artificial intelligence and machine learning further enhances formulation precision enabling developers to match probiotic strains with specific health outcomes based on large scale clinical datasets. Direct to consumer microbiome testing services have expanded access to personalized insights with companies offering at home stool analysis kits that generate customized probiotic recommendations. This convergence of advanced diagnostics, data analytics, and consumer demand for individualized health solutions positions personalized probiotics as a high growth segment capable of commanding premium pricing and fostering brand loyalty through demonstrable efficacy.

Expansion into Non Digestive Health Applications Broadens Market Scope

Probiotic applications extending beyond gastrointestinal wellness represent a compelling opportunity for the U.S. probiotics market. According to the National Center for Complementary and Integrative Health, probiotics have shown promise for preventing necrotizing enterocolitis in premature infants, treating infant colic, and supporting remission in ulcerative colitis, indicating therapeutic potential across multiple clinical domains. As per emerging research probiotics may influence immune function, mental well-being, and metabolic health, with studies demonstrating associations between probiotic consumption and elevated enterolignan concentrations linked to reduced disease risk. Consumer awareness of these broader benefits is growing as survey data reveals that Americans increasingly recognize connections between gut health and immune support, mental well-being, healthy aging, and sleep quality. The immune health segment shows particular promise with 33% of Americans using probiotics specifically to bolster immune function according to market intelligence reports. Clinical trial activity reflects this diversification with research exploring probiotic applications in rheumatoid arthritis, dermatological conditions, and respiratory health, indicating expanding scientific validation. This application broadening enables manufacturers to target new consumer segments, develop innovative product formats, and establish differentiated brand positions beyond traditional digestive health positioning, ultimately driving category expansion and long term market sustainability.

MARKET CHALLENGES

Product Quality and Viability Concerns Undermine Consumer Trust

Maintaining probiotic viability and ensuring consistent product quality throughout the supply chain is challenging the U.S. probiotics market growth. According to research published in Nutrients, consumers encounter difficulties assessing the authenticity of probiotic health claims, making informed purchasing decisions challenging amid variable product quality. As per stability studies, many probiotic formulations experience significant reductions in viable colony forming units during storage, transportation, and retail display, potentially delivering subtherapeutic doses to end users. The absence of mandatory third party verification for live microorganism counts on product labels creates transparency gaps that erode consumer confidence according to industry analyses. Temperature sensitivity further complicates distribution as many probiotic strains require refrigeration to maintain potency yet cold chain integrity cannot be guaranteed across all retail environments. A study examining commercial probiotic products found substantial discrepancies between labeled and actual microbial counts with some formulations containing less than 50% of advertised viable organisms. This quality inconsistency leads to variable clinical outcomes that may discourage repeat purchases and generate negative word of mouth. Manufacturers face elevated production costs to implement advanced encapsulation technologies and stability testing protocols while competing against lower priced alternatives that may compromise quality. Without standardized industry wide quality benchmarks and independent verification mechanisms this challenge will continue to impede consumer trust and limit market maturation.

Scientific Communication Gaps Hinder Evidence Based Adoption

The disconnect between emerging probiotic research and accessible consumer education is further challenging the growth of the U.S. probiotics market. According to an Ipsos poll conducted for MDVIP, 85% of Americans received a failing grade on a microbiome knowledge assessment, indicating profound educational deficits despite growing product interest. As per the Danone North America survey, 41% of consumers remain unaware of the gut microbiome concept while 50% do not recognize its impact on gut health, highlighting critical communication gaps. Healthcare providers face similar challenges as many lack updated training on probiotic strain specificity, appropriate indications, and dosing protocols, according to clinical education assessments. The complexity of translating peer reviewed research into actionable consumer guidance is compounded by conflicting media reports and marketing claims that oversimplify scientific findings. Social media amplification of anecdotal experiences further muddies the information landscape making it difficult for consumers to distinguish evidence based recommendations from unsubstantiated assertions. This communication deficit leads to suboptimal product selection, inappropriate usage patterns, and unrealistic efficacy expectations that may result in perceived product failure. Addressing this challenge requires coordinated efforts among researchers, clinicians, manufacturers, and public health agencies to develop clear, consistent, and accessible educational resources that empower informed decision making and maximize the public health potential of probiotic interventions.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.83% |

| Segments Covered | By Product, Distribution Channel, and Country |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities. |

| Regions Covered | US, Canada, and the Rest of North America |

| Market Leaders Profiled | Danone SA, Chobani LLC, General Mills Inc., PepsiCo Inc. (KeVita), Now Foods, Yakult Honsha, BioGaia AB, Lifeway Foods, Inc., Nestlé SA, Procter & Gamble Company, i-Health (Culturelle), Suja Life, Wren Laboratories Ltd, Groupe Lactalis S.A, Seven Turns Private Limited (The Good Bug), Culture Pop, Nature's Garden, Nutritionalab Private Limited, Vlado Sky Enterprise Pvt Ltd, Hero Group.p |

SEGMENT ANALYSIS

By Product Insights

The probiotic food and beverages segment commanded the dominant position in the U.S. probiotics market with 70.7% of the market share in 2025. The seamless incorporation of probiotics into familiar food formats represents a key factor for the dominance of this segment in the U.S. market. According to Danone North America research, 88% of Americans recognize probiotics and actively seek them within food products rather than isolated supplement formats. As per market intelligence, probiotic sales now represent 9% of all vitamin sales in the United States with food based formats capturing the majority of consumer transactions. The convenience factor significantly influences purchasing behavior as 68% of shoppers discover new probiotic products while browsing grocery aisles according to Food Marketing Institute data. Product innovation further strengthens adoption with manufacturers launching lactose free, plant based, and low sugar probiotic options that align with contemporary dietary preferences. Retailers have responded by dedicating expanded shelf space to microbiome friendly products with Whole Foods Market identifying gut health as its top trend for 2024. This convergence of accessibility, taste appeal, and wellness positioning creates sustained demand momentum that reinforces the food and beverage segment market leadership.

On the other side, the probiotic dietary supplements segment is predicted to expand at a CAGR of 9.2% during the forecast period in the U.S. market owing to the increasing consumer demand for targeted probiotic interventions. According to research published in Clinical Infectious Diseases, probiotic efficacy is both strain specific and condition specific, prompting health conscious consumers to seek supplements with documented clinical validation. As per the National Institutes of Health Office of Dietary Supplements, consumers are becoming more discerning about colony forming unit counts, strain identification, and third party verification when selecting probiotic supplements. Market intelligence indicates that supplement formats enable precise dosing and strain combinations that food matrices cannot reliably deliver, supporting therapeutic applications beyond general wellness. The rise of personalized nutrition platforms further accelerates adoption as companies offer microbiome testing coupled with customized supplement regimens. According to a 2024 consumer survey, 64% of Americans consider clinically supported health claims on packaging highly important when selecting probiotic products. This evidence based purchasing behavior combined with the flexibility of supplement formats creates robust growth momentum for the dietary supplements segment.

By Distribution Channel Insights

The supermarkets and hypermarkets segment led the market by holding 46.7% of the U.S. market share in 2025. The growth of the supermarkets and hypermarkets segment in the U.S. market is attributed to the strategic positioning of probiotic products within high volume retail environments. According to the Food Marketing Institute, 68% of shoppers discover new probiotic products while browsing grocery aisles rather than conducting targeted online searches. As per retail analytics, probiotic yogurt and fermented beverage categories benefit from placement adjacent to complementary wellness products including organic foods, vitamins, and natural snacks. This category adjacency creates cross purchasing opportunities that amplify basket size and brand visibility. Retailers further enhance engagement through end cap displays, promotional bundling, and in store sampling programs that drive trial and repeat purchase behavior. According to a 2024 survey from the International Food Information Council, 51% of Americans prefer purchasing probiotics during routine grocery shopping, citing convenience and immediate product access as primary motivators. The integration of digital tools such as mobile scanning and loyalty program personalization strengthens this channel by connecting physical browsing with digital research. This convergence of accessibility, discovery, and convenience creates sustained distribution momentum that reinforces the supermarket and hypermarket segment market leadership.

However, the online retail stores segment is expected to exhibit the fastest CAGR of 24.1% during the forecast period in the U.S. market due to the capacity for tailored product recommendations and educational content. According to Shopify commerce data, direct to consumer probiotic brands experienced 89% year over year sales growth by leveraging intake quizzes and personalized recommendation engines. As per Jungle Scout analytics, Amazon Subscribe and Save program increased probiotic repurchase rates by 57% in 2023, demonstrating the power of automated replenishment models. The digital environment enables brands to deliver strain specific education, dosage guidance, and usage protocols that enhance consumer understanding and product satisfaction. According to a 2024 consumer survey, 64% of Americans consider clinically supported health claims on packaging highly important when selecting probiotic products and online platforms excel at communicating this information. Telehealth integration further strengthens this channel as healthcare providers increasingly recommend specific supplement brands during virtual consultations. This convergence of personalization, education, and convenience creates a powerful growth engine for the online retail segment.

UNITED STATES COUNTRY ANALYSIS

The United States is projected to experience sustained expansion for the next few years and accounted for 21.3% of the global market share in 2025. This market leadership reflects the convergence of advanced healthcare infrastructure, robust consumer health awareness, and innovative product development capabilities that distinguish the United States from regional peers. The systematic incorporation of probiotics within clinical care pathways and preventive health framework represents a primary factor for United States market dominance. According to the Society of Hospital Medicine, 41% of acute care institutions now stock medical grade probiotics for inpatients receiving broad spectrum antibiotics. As per Medicare Advantage program data, post discharge nutrition counseling increasingly includes probiotic recommendations for high risk senior populations, creating institutional demand that stabilizes market growth. The United States healthcare system unique emphasis on preventive care and value based reimbursement models further strengthens probiotic adoption across diverse patient populations. According to the National Center for Complementary and Integrative Health, clinical evidence supports probiotic efficacy for specific indications such as antibiotic associated diarrhea where meta-analyses demonstrate approximately 50% risk reduction. This evidence based integration combined with consumer preference for proactive health management creates sustained demand momentum that reinforces United States market leadership.

COMPETITIVE LANDSCAPE

The United States probiotics market features intense competition among multinational corporations specialized supplement brands and emerging biotech innovators. Established players leverage brand recognition retail relationships and scientific resources to maintain shelf space and consumer trust while agile newcomers differentiate through novel strains personalized formulations and digital engagement. Competition centers on clinical validation as companies invest in human trials to substantiate health claims and secure regulatory approvals that build credibility with healthcare professionals and informed consumers. Product innovation focuses on strain stability targeted delivery systems and multi benefit formulations that address digestive immune mental and metabolic health simultaneously. Price competition remains moderate as consumers prioritize efficacy and quality over cost for probiotic purchases yet private label offerings from major retailers exert downward pressure on premium brands. Marketing strategies emphasize education and transparency as brands work to close consumer knowledge gaps regarding strain specificity dosage and storage requirements. The competitive landscape continues evolving through mergers acquisitions and strategic partnerships that consolidate expertise accelerate innovation and expand geographic reach across diverse distribution channels.

KEY MARKET PLAYERS

A few of the market players in the U.S probiotics market include

- Danone SA

- Chobani LLC

- General Mills Inc.

- PepsiCo Inc. (KeVita)

- Garden of Life A Nestlé Health Science Brand

- Now Foods

- Yakult Honsha

- BioGaia AB

- Lifeway Foods, Inc.

- Nestlé SA

- Procter & Gamble Company

- i-Health (Culturelle)

- Suja Life

- Wren Laboratories Ltd.

- Groupe Lactalis S.A.

- Seven Turns Private Limited (The Good Bug)

- Culture Pop

- Nature's Garden

- Nutritionalab Private Limited

- Vlado Sky Enterprise Pvt Ltd

- Hero Group

Top Players In The Market

- Danone North America maintains a prominent position in the United States probiotics market through its diversified portfolio of fermented dairy and plant based products. The company leverages scientific research to validate probiotic benefits and recently strengthened its gut health leadership by acquiring The Akkermansia Company in June 2025 to advance next generation biotic innovation. Danone North America also supports academic research through its annual Gut Microbiome Fellowship Grant which awarded fifty thousand dollars to graduate students studying microbiome health in January 2025. The company integrates probiotic strains into recognizable brands like Activia and DanActive while pursuing Certified B Corporation status to align with consumer values around sustainability and transparency.

- Garden of Life operates as a leading probiotic brand within the United States market offering clinically studied formulations across capsules powders and gummies. As part of Nestlé Health Science the brand benefits from global research infrastructure while maintaining its commitment to organic and Non GMO Project Verified ingredients. Garden of Life expanded its European distribution in February 2025 introducing high potency probiotic products containing up to 50 billion CFU per serving to international consumers. The brand strengthens market position through strategic retail partnerships including Costco placements and USATF sponsorship which enhances visibility among health conscious athletes and active lifestyle consumers.

- Yakult Honsha contributes significantly to the United States probiotics market through its signature fermented milk beverage containing the proprietary Lactobacillus casei Shirota strain. The company announced a three hundred five million dollar investment in July 2024 to construct a second United States production facility in Bartow County Georgia which will expand manufacturing capacity and create over 90 new jobs. Yakult targets millennial and Gen Z consumers through updated marketing campaigns launched in September 2024 that emphasize immune support and digestive wellness. The company leverages its century long scientific heritage to differentiate its single strain formulation while expanding distribution through convenience channels and e commerce platforms.

Top Strategies Used by Key Market Participants

Key players in the United States probiotics market employ several strategic approaches to strengthen competitive positioning. Companies invest heavily in clinical research to validate strain specific health claims and secure qualified health authorizations from regulatory bodies. Strategic acquisitions enable rapid access to novel probiotic strains and proprietary delivery technologies that enhance product efficacy. Brands pursue omnichannel distribution expansion by integrating traditional retail presence with direct to consumer e commerce platforms and subscription models. Personalization strategies leverage microbiome testing and artificial intelligence to recommend tailored probiotic regimens that increase consumer engagement and loyalty. Sustainability commitments including regenerative agriculture sourcing and B Corporation certification resonate with values driven consumers and differentiate brands in crowded marketplaces. Collaborative partnerships with healthcare providers academic institutions and sports organizations extend brand credibility and reach new consumer segments.

MARKET SEGMENTATION

This research report on the U.S probiotics market size is segmented and sub-segmented into the following categories.

By Product Type

- Probiotic Foods

- Yogurt

- Bakery/Breakfast Cereals

- Baby Food and Infant Formula

- Other Probiotic Foods

- Probiotic Drinks

- Dairy-based Drinks

- Fruit/Plant-based Drinks

- Others (Kombucha and Fermented Tea)

- Dietary Supplements

- Capsules

- Tablets

- Powders

- Gummies

- Others

By Distribution Channel Type

- Supermarkets/Hypermarkets

- Pharmacies/Health Stores

- Convenience Stores

- Online Retail Stores

- Other Distribution Channels

By Country

- USA

- Canada

- Mexico

Frequently Asked Questions

What’s driving the growth of the probiotics market in the U.S.?

Rising consumer focus on gut health, immunity, and preventive wellness—amplified by post-pandemic health awareness—is fueling demand across supplements, functional foods, and beverages

Which product formats are most popular among U.S. consumers?

Dietary supplements (capsules, tablets) lead in sales, but probiotic-fortified yogurts, kombucha, kefir, and gummies are gaining rapid traction, especially among younger, health-conscious shoppers.

How does scientific research influence market credibility?

Clinically studied strains (e.g., Lactobacillus rhamnosus GG, Bifidobacterium lactis) and transparent labeling of CFUs (colony-forming units) build trust, with brands increasingly investing in human trials to substantiate health claims.

Are regulatory standards strict for probiotics in the U.S.?

Probiotics are regulated as dietary supplements (under DSHEA) or foods by the FDA—meaning pre-market approval isn’t required, but manufacturers must ensure safety and avoid unapproved disease claims.

Which demographics are adopting probiotics most actively?

Millennials and Gen Z drive functional food trends, while aging adults prioritize digestive and immune support—making probiotics a cross-generational wellness staple.

Who are the leading brands in the U.S. market?

Key players include Culturelle (i-Health), Garden of Life, Renew Life (Bayer), Danone (Activia, Align), and emerging brands like Seed and Pendulum—blending science, clean labels, and targeted formulations.

How is personalization shaping product development?

Companies are launching strain-specific probiotics for women’s health, mental wellness (psychobiotics), skin health, and metabolic support—moving beyond “one-size-fits-all” to precision microbiome solutions.

Are clean-label and sustainable practices important to buyers?

Yes—consumers increasingly seek non-GMO, dairy-free, vegan, and plastic-neutral probiotic options, pushing brands toward transparent sourcing and eco-friendly packaging.

What challenges does the market face?

Strain viability during shelf life, inconsistent regulatory enforcement, and consumer confusion over efficacy claims can undermine trust and hinder mainstream adoption

What’s the market outlook for 2025–2030?

The U.S. probiotics market is projected to grow steadily, driven by microbiome science advances, functional food innovation, and expanding retail and e-commerce access—solidifying its role in everyday preventive health.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com