U.S. Soybean Market Size, Share, Trends & Growth Forecast Report Segmented By Nature (GMO, Non-GMO), Form, End-Use, and Country, Industry Forecast From 2025 to 2033

U.S. Soybean Market Report Summary

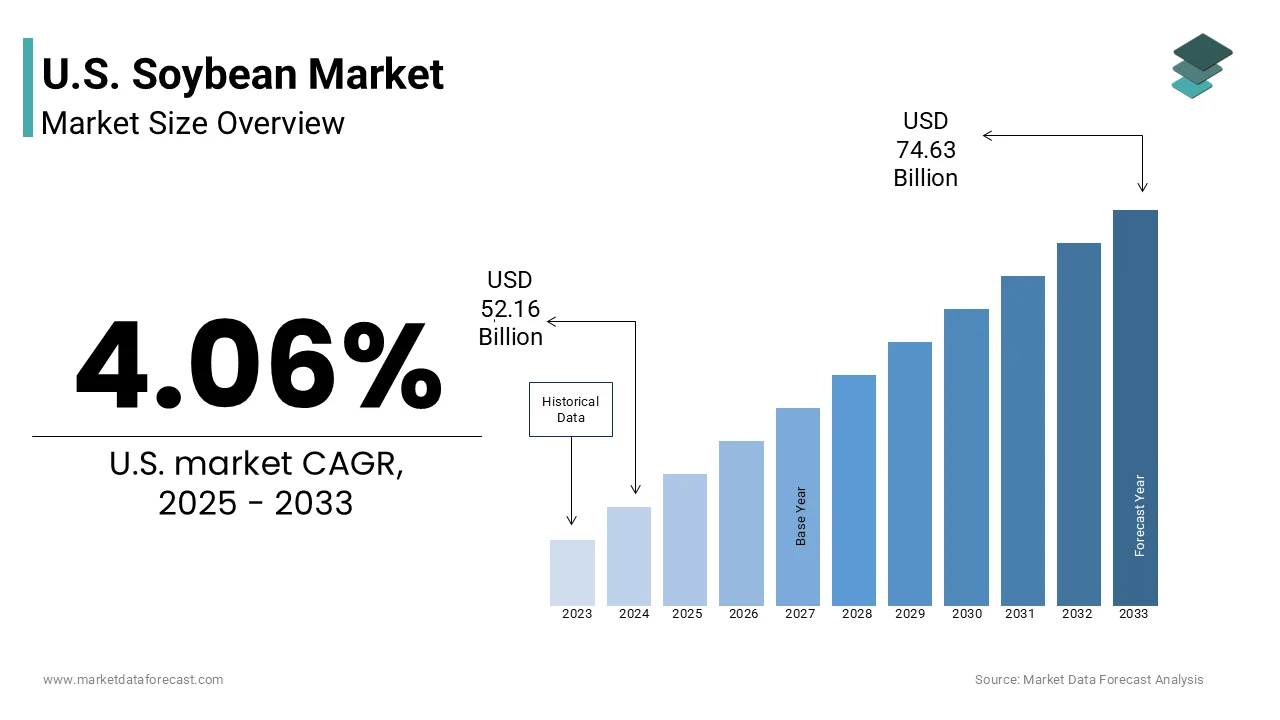

The U.S. soybean market was valued at USD 52.16 billion in 2024, is anticipated to reach USD 54.28 billion in 2025, and is projected to reach USD 74.63 billion by 2033, growing at a CAGR of 4.06% during the forecast period. The growth of the U.S. soybean market is driven by rising global demand for plant-based protein, expanding use of soy in biofuel production, and increasing adoption of genetically modified (GM) soybean varieties that offer higher yields, pest resistance, and environmental sustainability. Moreover, favorable trade dynamics and advancements in agricultural biotechnology continue to strengthen the country’s position as one of the world’s largest soybean producers and exporters.

Key Market Trends

- Rising global demand for soy-based products, including soy protein, tofu, and soy milk, fueled by the shift toward plant-based diets.

- Expanding use of soybean oil in biodiesel production, supporting both agricultural and energy markets.

- Increasing adoption of precision agriculture technologies to improve crop yield and reduce resource usage.

- Continued innovation in genetically modified seed varieties offering improved drought tolerance and disease resistance.

- Strategic export partnerships with key international markets such as China, Mexico, and the European Union driving long-term market stability.

Segmental Insights

- Based on nature, the genetically modified organisms (GMO) segment dominated the U.S. soybean market in 2024 by capturing a significant share. The widespread adoption of GM soybean seeds is driven by their superior productivity, pest resistance, and lower input costs, making them the preferred choice among U.S. farmers for large-scale cultivation.

Competitive Landscape

The U.S. soybean market is moderately consolidated, with key players emphasizing supply chain efficiency, export capacity, and seed innovation. Companies are investing in R&D for high-protein soybean strains, sustainable farming partnerships, and biodiesel supply integration to strengthen market positioning. Major players dominating the U.S. soybean market include Archer Daniels Midland (ADM), Cargill, CHS Inc., Louis Dreyfus Company (LDC), SunOpta, Corteva Agriscience (Pioneer®), Bayer CropScience (Monsanto), and Syngenta.

U.S. Soybean Market Size

The U.S. soybean market size was valued at USD 52.16 billion in 2024, and the market size is expected to be worth USD 74.63 billion by 2033 from USD 54.28 billion by 2025. The market is growing at a CAGR of 4.06% during the forecast period.

The soybean is the integrated system of cultivation, crushing, processing, and distribution of Glycine max across domestic food, feed, fuel, and industrial channels.

MARKET DRIVERS

The structural expansion of U.S. meat production, which anchors domestic demand for soybean meal as the primary protein source in livestock rations, is driving the growth of the U.S. soybean market. Tyson Foods, as disclosed in its 2023 sustainability report, sources 100% of its poultry feed soy from U.S.-grown, deforestation-free verified supply chains, which have a procurement standard now adopted by 80% of top meat processors, according to the North American Meat Institute’s 2024 supply chain survey.

The accelerating adoption of renewable diesel, which utilizes soybean oil as a primary feedstock under federal clean fuel mandates, is accelerating the growth of the U.S. soybean market.

MARKET RESTRAINTS

The intensifying competition for arable land from corn and cotton strains soybean acreage expansion despite rising global protein and oil demand, which is hampering the growth of the U.S. soybean market. The prevented planting claims for soybeans totaled 1.8 million acres in 2023 due to persistent spring rainfall in the Eastern Corn Belt, with a climatic pattern NOAA attributes to intensified La Niña oscillations.

The tightening federal regulations on neonicotinoid seed treatments, which protect early-season soybean stands from bean leaf beetles and soybean aphids, which is restricting the growth of the U.S. soybean market. As per the Environmental Protection Agency’s 2023 interim decision, three major neonicotinoid compounds used on 89% of U.S. soybean acres face use restrictions or label modifications by 2026.

MARKET OPPORTUNITIES

The commercialization of high-oleic soybean varieties, which offer oxidative stability for foodservice frying and industrial lubricants without hydrogenation, is creating new opportunities fof the growth ofthe US soybean market.

The integration of soybean cultivation with carbon credit programs under emerging regenerative agriculture frameworks is expected to bolster the growth of the US soybean market. Bayer’s Carbon Initiative, as detailed in its 2023 sustainability report, compensates farmers $3 per acre for adopting no-till and cover cropping practices shown by USDA-ARS trials to increase soil organic carbon by 0.4 tons per hectare annually.

MARKET CHALLENGES

The accelerating degradation of herbicide efficacy due to evolved weed resistance is quite challenging for the growth of the US soybean market. University of Arkansas field trials in 2023 demonstrated that resistant weed infestations reduce soybean yields by 54% if uncontrolled, with a loss equivalent to 22 bushels per acre.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 4.06% |

| Segments Covered | By Nature, Form, End-Use, and Region |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado |

| Market Leaders Profiled | Archer Daniels Midland (ADM), Cargill, CHS Inc., Louis Dreyfus Company (LDC), SunOpta, Corteva Agriscience (Pioneer®), Bayer CropScience (Monsanto), and Syngenta |

SEGMENTAL ANALYSIS

By Nature Insights

The genetically modified organisms segment was the largest by capturing a significant share of the US soybean market in 2024, with agronomic resilience and yield optimization under industrial-scale farming systems. Monsanto-Bayer’s Intacta RR2 PRO soybeans, deployed across 58 million acres in 2023, deliver dual herbicide tolerance and lepidopteran insect resistance.

The non-GMO segment is likely to grow wita h 12.3% CAGR during the forecast period, with the premium export contracts and clean-label food manufacturing mandates.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

A few of the dominating players in the U.S. soybean market include

-

Archer Daniels Midland (ADM)

-

Cargill

-

CHS Inc.

-

Louis Dreyfus Company (LDC)

-

SunOpta

-

Corteva Agriscience (Pioneer®)

-

Bayer CropScience (Monsanto)

-

Syngenta

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

Key players deploy farmer-aligned sustainability premiums, invest in port and crush infrastructure resilience, and vertically integrate into high-margin specialty ingredients. They secure long-term offtake contracts with biofuel and plant-based protein manufacturers to de-risk commodity exposure. Digital traceability platforms authenticate non-GMO and regenerative claims for export compliance. Strategic retrofits enable segregated processing for identity-preserved streams. Partnerships with agtech firms optimize planting and logistics using predictive analytics.

COMPETITION OVERVIEW

Competition in the U.S. soybean sector is less about price and more about control of logistics, processing differentiation, and sustainability verification. Regional cooperatives challenge through localized premium programs and direct export channels. Competition intensifies around carbon credit integration, non-GMO segregation, and feedstock contracts for renewable diesel.

TOP PLAYERS IN THE MARKET

- Archer Daniels Midland operates as a linchpin in global soybean value chains, transforming U.S.-grown beans into protein meals, lecithin, and industrial oils. The company secured long-term offtake agreements with European plant-based food manufacturers for non-GMO isolates. Its investment in traceability blockchain for soy shipments to Asia reinforces premium positioning.

- Cargill anchors its soybean leadership through integrated origination, processing, and risk management across 40 U.S. states. The company retrofitted three Gulf Coast export terminals to handle high-oleic and identity-preserved soy streams. Cargill’s joint venture with NatureWorks to produce bio-based polymers from soy oil diversifies end-use exposure.

MARKET SEGMENTATION

This research report on the U.S. soybean market is segmented and sub-segmented into the following categories.

By Nature

-

GMO

-

Non-GMO

By Form

-

Raw

-

Processed

By End-Use

-

Food & Beverages

-

Animal Feed

-

Industrial Use

-

Others

By Region

-

New York

-

Massachusetts

-

Pennsylvania

-

Illinois

-

Ohio

-

Michigan

-

Texas

-

Florida

-

Georgia

-

California

-

Washington

-

Colorado

Frequently Asked Questions

1. Which factors are driving growth in the U.S. soybean market?

Key drivers include rising demand for plant-based proteins, increasing use in animal feed and industrial products, and growing biofuel consumption.

2. What are the main uses of soybeans in the U.S.?

Soybeans are primarily used for soybean oil, soybean meal, animal feed, food products, and biofuel production.

3. Which states are the top producers of soybeans in the U.S.?

The leading soybean-producing states are Illinois, Iowa, Minnesota, Indiana, and Nebraska, contributing significantly to total national output.

4. What are the challenges faced by the U.S. soybean market?

Challenges include price volatility, trade tensions (especially with China), climate change impacts, and competition from other global producers like Brazil.

5. How is soybean oil demand affecting the market?

Over half of soybean oil production in the U.S. is used for biofuel, which has driven domestic demand to record levels.

6. What are the emerging trends in the U.S. soybean market?

Emerging trends include increased use in plant-based foods, sustainable farming practices, technological adoption in farming, and biofuel expansion.

7. How do trade policies affect the U.S. soybean market?

Trade policies, tariffs, and export regulations directly influence soybean prices, export volumes, and market stability.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com