U.S. Timber Market Size, Share, Trends & Growth Forecast Report Segmented By Type (Industrial round wood, Fuel woods, Others), and Region (New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado), Industry Forecast From 2025 to 2033

U.S. Timber Market Size

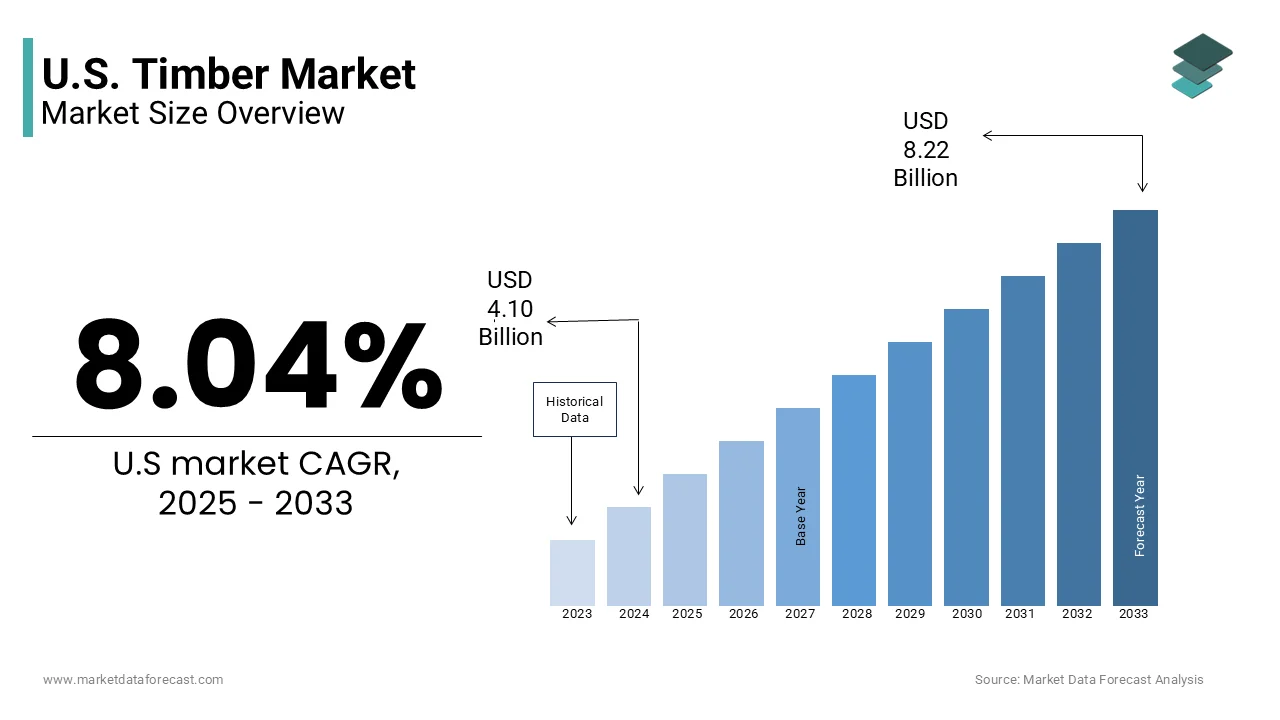

The U.S. timber market size was valued at USD 4.10 billion in 2024, and the market size is expected to be worth USD 8.22 billion by 2033 from USD 4.43 billion by 2025. The market is growing at a CAGR of 8.04% during the forecast period.

The timber is a living infrastructure shaped by ecological boundaries, cultural building traditions, and the slow rhythm of forest regeneration. The average mature tree in the Pacific Northwest reaches 80–120 years before harvest, embedding time itself into the material’s value. Timber from these forests fuels everything from rural homes to urban mass-timber skyscrapers, with each cubic foot carrying the legacy of watershed protection, wildlife corridors, and Indigenous stewardship practices that predate colonial logging.

MARKET DRIVERS

Mass Timber Construction and Urban Density Policies

The rise of engineered wood products such as cross-laminated timber (CLT) has redefined architectural possibilities in high-density urban environments, which is levelling up the growth of U.S. timber market. Cities like Portland, Seattle, and Boston now mandate or incentivize timber use in structures up to 18 stories under updated building codes, recognizing its lower embodied carbon compared to steel and concrete. This regulatory momentum, paired with public appetite for biophilic design, has shifted timber from a rural commodity to a symbol of sustainable urbanism.

Rural Housing Demand and Infrastructure Resilience Post-Disaster

The rebuilding efforts in vulnerable regions have intensified demand for locally sourced, durable timber is also escalating the growth of U.S. timber market. As per the Federal Emergency Management Agency, over 1.3 million residential units were damaged or destroyed between 2020 and 2023 due to extreme weather events, triggering emergency procurement programs that prioritize domestic wood over imported alternatives. Simultaneously, the Census Bureau reports a 19% increase in single-family housing permits in non-metro counties between 2021 and 2023, driven by remote work trends and affordability pressures.

MARKET RESTRAINTS

Forest Health Decline Due to Bark Beetle Infestations and Drought

The integrity of the U.S. timber resource base is being eroded by cascading ecological stressors, which is particularly bark beetle outbreaks fueled by prolonged drought and warmer winters. In 2023, the Forest Service estimated that 28% of commercially viable timber in the Southern Rockies was already compromised rendering it unsuitable for structural applications due to internal decay and reduced strength.

Regulatory Delays and Permitting Bottlenecks in Federal Land Harvesting

Complex environmental reviews under the National Environmental Policy Act, coupled with litigation from advocacy groups, delay or cancel nearly 30% of proposed timber sales annually is limiting the growth of U.S. timber market. These delays create instability for regional mills dependent on consistent feedstock; in Oregon, seven small sawmills closed between 2020 and 2023 because they could no longer secure long-term supply agreements.

MARKET OPPORTUNITIES

Carbon Sequestration Credits and Timber as a Climate Asset

The increasing recognized not as a harvested product but as a stored carbon asset, which is unlocking new revenue streams is likely to create new opportunities for the growth of U.S. timber market. Companies like Weyerhaeuser and Rayonier now bundle timber harvests with verified carbon sequestration contracts by allowing developers to offset emissions from new construction while maintaining harvest yields.

Domestic Substitution of Imported Softwood Lumber

The persistent trade disruptions and geopolitical volatility have reignited efforts to replace Canadian softwood imports, which historically supplied 60% of U.S. framing lumber is creating new opportunities for the growth of U.S. timber market. States like Georgia and Alabama expanded plantation forestry by 1.1 million acres between 2021 and 2023, primarily using fast-growing loblolly pine.

MARKET CHALLENGES

Labor Scarcity in Forestry and Mill Operations

The deepening crisis of workforce attrition, with the median age of loggers and mill operators reaching 54.6 years is likely to hinder the growth of U.S. timber market. Fewer than 15 vocational schools nationwide offer accredited training in sustainable forestry or heavy equipment operation, and rural recruitment remains stagnant despite wage premiums averaging 22% above national averages. The consequence is operational inefficiency: in Maine, delayed harvest schedules due to understaffing caused 18% of scheduled timber volumes to rot before extraction in 2023, according to the Maine Forest Service.

Fragmentation of Private Forest Ownership and Lack of Coordinated Management

The fragmentation impedes large-scale, ecologically sound management with only 12% of these small holdings have formal forest management plans, which is degrading the growth of U.S. timber market. In the Southeast, where 40% of national timber production occurs, this disorganization has contributed to a 17% decline in average stumpage prices since 2019, as smaller landowners compete for spot-market buyers rather than securing long-term contracts.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 8.04% |

| Segments Covered | By Type, and Region |

| Various Analyses Covered | Global, Regional, and Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | New York, Massachusetts, Pennsylvania, Illinois, Ohio, Michigan, Texas, Florida, Georgia, California, Washington, Colorado |

| Market Leaders Profiled | Weyerhaeuser Company, UFP Industries Inc., Sierra Pacific Industries, PotlatchDeltic Corporation, Rayonier, Boise Cascade Company, West Fraser Timber Co. Ltd., and Louisiana-Pacific Corporation (LP). |

SEGMENTAL ANALYSIS

By Type Insights

The industrial roundwood segment was the largest and held a dominant share of the U.S. timber market in 2024 with its irreplaceable role as the foundational feedstock for structural lumber, engineered wood products, and millwork materials essential to residential, commercial, and institutional construction.

The fuelwood segment is estimated to witness a CAGR of 6.9% throughout the forecast period with two converging trends like rural energy resilience and the expansion of biomass power generation. The USDA Forest Service reports that 42 million dry tons of low-value forest residues previously left to decay or burn are now being collected annually for fuel, thanks to improved chipping technology and regional logistics hubs.

REGIONAL ANALYSIS

Washington State timber market growth is likely to wotness a significant CAGR during the forecast period with primary supplier of premium structural timber for high-rise and seismic-sensitive construction. Washington produces 35% of all CLT-grade lumber in the country, with mills like Weyerhaeuser’s Longview facility certified under strict structural grading protocols required for tall wood buildings. The state’s aggressive forest stewardship policies, including mandatory riparian buffers and reforestation mandates, have preserved timber quality despite decades of harvest, earning it recognition from the Forest Stewardship Council for sustainable yield practices.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

A few of the dominating players in the U.S. timber market include

- Weyerhaeuser Company

- UFP Industries, Inc.

- Sierra Pacific Industries

- PotlatchDeltic Corporation

- Rayonier

- Boise Cascade Company

- West Fraser Timber Co. Ltd.

- Louisiana-Pacific Corporation (LP)

MARKET SEGMENTATION

This research report on the U.S. timber market is segmented and sub-segmented into the following categories.

By Type

- Industrial round wood

- Fuel woods

- Others

By Region

- New York

- Massachusetts

- Pennsylvania

- Illinois

- Ohio

- Michigan

- Texas

- Florida

- Georgia

- California

- Washington

- Colorado

Frequently Asked Questions

1. What is the U.S. Timber Market?

The U.S. Timber Market includes the production, trade, and utilization of timber and wood products across construction, manufacturing, and forestry sectors.

2. What is the future outlook for the U.S. Timber Market?

The market is expected to grow steadily, driven by sustainable forestry, increasing demand for wood-based construction, and ongoing investments in engineered timber products.

3. What are the major segments of the U.S. timber market?

Key segments include timber construction, hardwood lumber, softwood lumber, timberland ownership, and imports/exports of timber products.

4. Who are the key players in the U.S. Timber Market?

Major players include Weyerhaeuser Company, UFP Industries Inc., Sierra Pacific Industries, PotlatchDeltic Corporation, Rayonier, Boise Cascade Company, West Fraser Timber Co. Ltd., and Louisiana-Pacific Corporation (LP).

5. Which regions dominate timber production in the U.S.?

The U.S. South and Pacific Northwest are the largest timber-producing regions, with extensive softwood and hardwood forests.

6. What drives the growth of the U.S. Timber Market?

Growth is driven by increasing construction activities, rising demand for sustainable wood products, residential and commercial infrastructure development, and adoption of engineered wood products.

7. What is the role of timberland ownership in the U.S.?

Timberland ownership involves managing forested land for lumber production, investment, and sustainable forestry practices. Large companies like Rayonier and PotlatchDeltic own millions of acres of timberland.

8. What are the major challenges facing the U.S. Timber Market?

Challenges include fluctuating timber prices, environmental regulations, climate change impacts, wildfires, and competition from alternative building materials.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1200

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com