Global Vacuum Valve Market Size, Share, Trends, & Growth Forecast Report, Segmented By Valve Type (Pressure Control Valves, Isolation Valves, Transfer Valves, Air Admittance Valves, Check Valves), Pressure Range (Low-to-Medium Vacuum (>10-3 torr), High Vacuum (<10-3->10-8 torr), Very High Vacuum (<10-8 torr)), Industry (Analytical Instruments, Chemicals, Flat-panel Display Manufacturing, Food & Beverages, Paper & Pulp, Pharmaceuticals, Semiconductor, Thin-film Coating, Others), Operation (Manual, Actuated and Others), Material (Stainless Steel, Aluminum, Glass, Polyvinyl Chloride (PVC), and Others) & Region, Industry Forecast From 2026 to 2034

Market Size, 2025

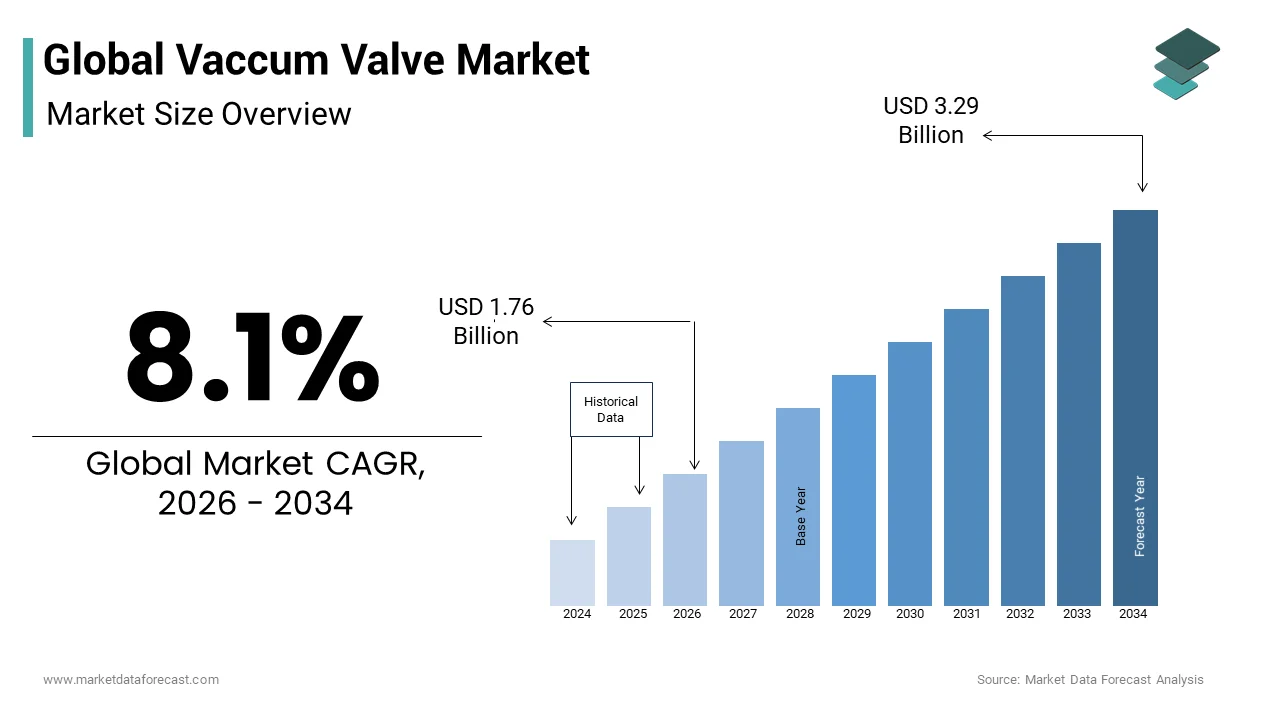

$1.63 BnMarket Estimate, 2026

$1.76 BnMarket Forecast, 2034

$3.29 BnCAGR, 2026–2034

8.1%Global Vacuum Valve Market Size

The global vacuum valve market size was valued at USD 1.63 billion in 2025 and is anticipated to reach USD 1.76 billion in 2025 to USD 3.29 billion by 2034, growing at a CAGR of 8.1% during the forecast period from 2026 to 2034.

Global Vacuum Valve Market Scenario

Vacuum valves are used to maintain a vacuum in the closed system. Vacuum valves are used for diverse applications such as isolation, ventilation, conduction, and gas flow in chambers. A series of pressure switches is also set up in most lines with vacuum valves (other than manual valves) to control the flow and convert the internal furnace pressure as demanded through the method being run.

The increasing demand for consumer devices such as smartphones, TVs, tablets, and laptops, coupled with the adoption of AI and deployment of 5G cellular networks, is expected to drive the growth of the vacuum valve market during the forecast period. For instance, according to secondary sources, by 2025, the number of 5G subscriptions across the globe is expected to reach 3 billion. These developments require advanced semiconductor components and devices. Thus, processes in the semiconductor manufacturing industry must be upgraded to meet the needs for higher memory output and better performance, thus producing IC chips of the highest quality. The IC chips require higher vacuum purity and, accordingly, need to be manufactured under vacuum. The demand for vacuum valves in the semiconductor industry is specifically driven by the reduction in semiconductor node sizes to get greater processing power into a smaller space. As node sizes shrink and chip architectures change, the need for purer vacuums and the wide variety of process steps under vacuum also increases, therefore producing demand for vacuum valves.

MARKET DRIVERS

The semiconductor industry is one of the fastest-growing industries globally. Semiconductors, such as memory chips and transistors, are an integral part of existing and emerging technologies.

Some of the key factors fueling the long-term demand for the chip industry include the Internet of Things (IoT), wireless communications, automotive electronics, artificial intelligence (AI), cloud computing, machine learning, consumer electronics, and data storage. The increasing demand for consumer electronics, such as smartphones, TVs, tablets, and laptops, coupled with the adoption of AI and deployment of 5G cellular networks, would require advanced semiconductor components and devices. Thus, processes in the semiconductor manufacturing industry must be upgraded to meet the needs for higher memory output and better performance, thus producing IC chips of the highest quality.

Semiconductor chips are used to power technologies that enable electronics products to work effectively and help run businesses with high productivity. These chips require higher vacuum purity and thus need to be manufactured under vacuum. The demand for vacuum valves in the semiconductor industry is mainly driven by the reduction in semiconductor node sizes to get more processing power into a smaller space. As node sizes shrink and chip architectures change, the need for purer vacuums and the number of process steps under vacuum also increase, thus generating demand for vacuum valves.

With the increasing competition, businesses are making significant R&D investments to boost their business growth by developing new products and services. R&D activities involve product R&D to create new products and improve the existing ones.

The leading companies in the vacuum valve market, such as VAT Group, Pfeiffer Vacuum, Agilent Technologies, and MKS Instruments, are focusing considerably on R&D activities and can be seen increasing their R&D investments year-on-year to gain or maintain their leading position. These investments are expected to help manufacturers with innovations in vacuum valves, thus enabling them to enhance business with existing customers and expand into adjacent markets. Such research initiatives and the development of new, enhanced products and technologies by the industrial players are expected to boost the vacuum valve market growth during the forecast period.

MARKET RESTRAINTS

The manufacturers of vacuum valves need to adhere to certain norms and regulations, which may hinder the global valve market share during the forecast period. Different regions have different certifications and policies concerning valves. This factor creates diversity in demand due to the wide applicability of valves in various industries, such as semiconductors, analytical instruments, chemicals, flat-panel display manufacturing, food & beverages, paper & pulp, and pharmaceuticals. However, this diversity is hindering the growth of the valves market, as industry players have to amend the same product according to the regional policies, which makes it difficult for them to achieve an ideal cost of installation. To resolve this issue, they have to invest their resources in setting up manufacturing facilities worldwide, which requires additional capital.

The efficient working of vacuum systems depends on suction load, temperature, leakage rate, and other process parameters such as the composition of suction gas. Malfunction of valves or failure of vacuum systems can result in extended downtime or shutdown of processes, resulting in high costs for emergency repair, wastage of materials, and disrupted production. Vacuum system failure can occur due to several factors, such as leakage, vacuum surges, vacuum hose failure, variation in seal water temperature, and vibration-related issues, among others. The requirement of a large space for assembly, starting, and maintenance of valves, and increasing susceptibility to leakage when operated at higher temperatures due to periodical fluctuations are some other disadvantages associated with vacuum valves, which can limit their adoption, and in turn, hamper market revenue growth to a certain extent over the forecast period.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 8.1% |

| Segments Covered | By Valve Type, Pressure Range, Industry, Operation, Material, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | MKS Instruments, VAT Group AG, V-TEX Corporation, CKD Corporation, SMC Corporation, ULVAC, KITZ SCT Corporation, HVA LLC, Agilent Technologies, Inc., Pfeiffer Vacuum GmbH, and Others. |

SEGMENTAL ANALYSIS

By Valve Insights

Over the forecast period, the isolation valves segment is expected to account for the largest global vacuum valve market size, owing to the increasing adoption of isolation valves in fluid handling systems such as chemical plants, oil production plants, pipeline safety systems, and firewater control, among others. They are also used to direct water for testing flow performance, for diverting process media, facilitating maintenance, and removing equipment. Isolation valves control flow without contaminating media such as blood, reagents, or medications in a variety of medical devices and analytical equipment. Isolation valves are perfectly suited for various medical applications like those that necessitate precise and repeated dispensing of media in diagnostic, analytical, and therapeutic equipment.

By Pressure Range Insights

The high vacuum segment is expected to register robust revenue CAGR over the forecast period in the vacuum value industry, owing to increasing demand for valves of high vacuum pressure range from various end-use industries such as semiconductors, lighting, and flat-panel display manufacturing, among others. High vacuum valves provide isolation for high vacuum pumps such as ion pumps or turbo pumps, and are used in systems where high vacuum pressure needs to be maintained in a closed vacuum processing system and in extreme pressure systems to control fluid flow dynamics. High-pressure range valves are designed to function under extreme pressure and temperatures, and are widely used in oil and natural gas upstream and downstream applications.

By Industry Insights

The semiconductor segment is expected to dominate other end-use segments in terms of revenue share, which is attributable to rising demand for vacuum valves for semiconductor manufacturing and fabrication processes. Semiconductor manufacturing requires high-precision and controlled conditions to prevent damage to wafers and chips, and this has boosted demand for advanced vacuum valves.

By Operation Insights

The manual operation segment is expected to register a considerably rapid revenue growth rate over the forecast period, attributable to increasing use of manually operated valves across various industrial sectors for a wide range of applications, such as clamping or closing safety doors and others. Manually operated valves are durable, reliable, and lightweight, and small and compact, thereby making them highly suitable for various pneumatic applications. The valves can be easily installed and have a plastic or metal housing that makes them sturdy.

By Material Insights

The stainless steel segment is expected to register a significantly faster revenue growth rate over the forecast period, attributable to increasing durability and reliability of stainless steel vacuum valves, high-pressure resistance, and decreased risk of corrosion. In addition, stainless steel valves do not leak under extreme temperature or pressure conditions, and ensure good joint integrity.

REGIONAL ANALYSIS

Based on regional analysis, North America is expected to register significantly larger revenue share over the forecast period, which is attributable to increasing demand for semiconductors due to rising need for more advanced consumer electronics, technological advancements in manufacturing processes, availability of advanced medical equipment that require medical isolation valves, and presence of major players in countries in the region.

The Asia Pacific region is expected to grow at the highest CAGR during the forecast period, owing to the growing demand for vacuum systems for the production of semiconductors and flat-panel displays, the rapid growth of the semiconductor industry in China and India due to growing demand for consumer electronics.

KEY MARKET PLAYERS

These are the market players that are dominating the global vacuum valves market.

- MKS Instruments

- VAT Group AG

- V-TEX Corporation

- CKD Corporation

- SMC Corporation

- ULVAC

- KITZ SCT Corporation

- HVA LLC

- Agilent Technologies,

- Pfeiffer Vacuum GmbH

RECENT MARKET NEWS

-

Hyperloop Transportation Technologies (USA) and GNB KL Group will collaborate in March 2021. (USA) Safety isolation valves were created by Hyperloop Transportation Technologies (USA) and GNB KL Group (USA) in March 2021, and are designed to isolate parts of the Hyperloop system tubes for emergency or maintenance pressurisation. The valves are the world's largest and most powerful, capable of withstanding stresses of up to 288,000 pounds.

-

Atlas Copco (Sweden) purchased HHV Pumps Pvt Ltd (India) in November 2021. The company designs and manufactures vacuum pumps and systems for a variety of industries. This acquisition will boost the company's market position and provide local manufacturing capabilities.

MARKET SEGMENTATION

This research report on the global vacuum values market is segmented and sub-segmented into the following categories.

By Valve Type

- Pressure Control Valves

- Isolation Valves

- Transfer Valves

- Air Admittance Valves

- Check Valves

By Pressure Range

- Low-to-Medium Vacuum (>10-3 torr)

- High Vacuum (<10-3->10-8 torr)

- Very High Vacuum (<10-8 torr)

By Industry

- Analytical Instruments

- Chemicals

- Flat-panel Display Manufacturing

- Food & Beverages

- Paper & Pulp

- Pharmaceuticals

- Semiconductor

- Thin-film Coating

- Others

By Operation

- Manual

- Actuated

- Others

By Material

- Stainless Steel

- Aluminum

- Glass

- Polyvinyl Chloride (PVC)

- Others

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

What is the vacuum valve market?

The vacuum valve market includes valves used to control and regulate vacuum flow in industrial and scientific applications.

What is driving the growth of the vacuum valve market?

The market is growing due to increasing demand from semiconductor, pharmaceutical, and industrial manufacturing sectors.

What types of vacuum valves are commonly used?

Common types include gate valves, angle valves, butterfly valves, and isolation vacuum valves.

Which segment dominates the vacuum valve market?

Gate vacuum valves dominate the market due to their strong sealing performance and wide industrial usage.

Who are the primary users of vacuum valves?

Semiconductor manufacturers, research laboratories, pharmaceutical companies, and industrial facilities are the main users.

How do vacuum valves improve industrial processes?

They help maintain controlled vacuum environments for accurate and efficient production operations.

Which regions lead the vacuum valve market?

Asia-Pacific leads the market due to strong semiconductor manufacturing and industrial expansion.

How is technology influencing the vacuum valve market?

Advancements in automation and precision engineering are improving valve efficiency and reliability.

What challenges does the vacuum valve market face?

High manufacturing costs and complex maintenance requirements can impact market growth.

What is the future outlook for the vacuum valve market?

The market is expected to grow steadily with rising demand for advanced vacuum systems and industrial automation.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com