Global Van Market Size Share, Trends, and Growth Analysis Report, Segmented By Toonage Capacity, Propulsion, End-User & Region (North America, Europe, Latin America, Asia Pacific, Middle East & Africa), Industry Forecast From 2026 to 2034

Global Van Market Size

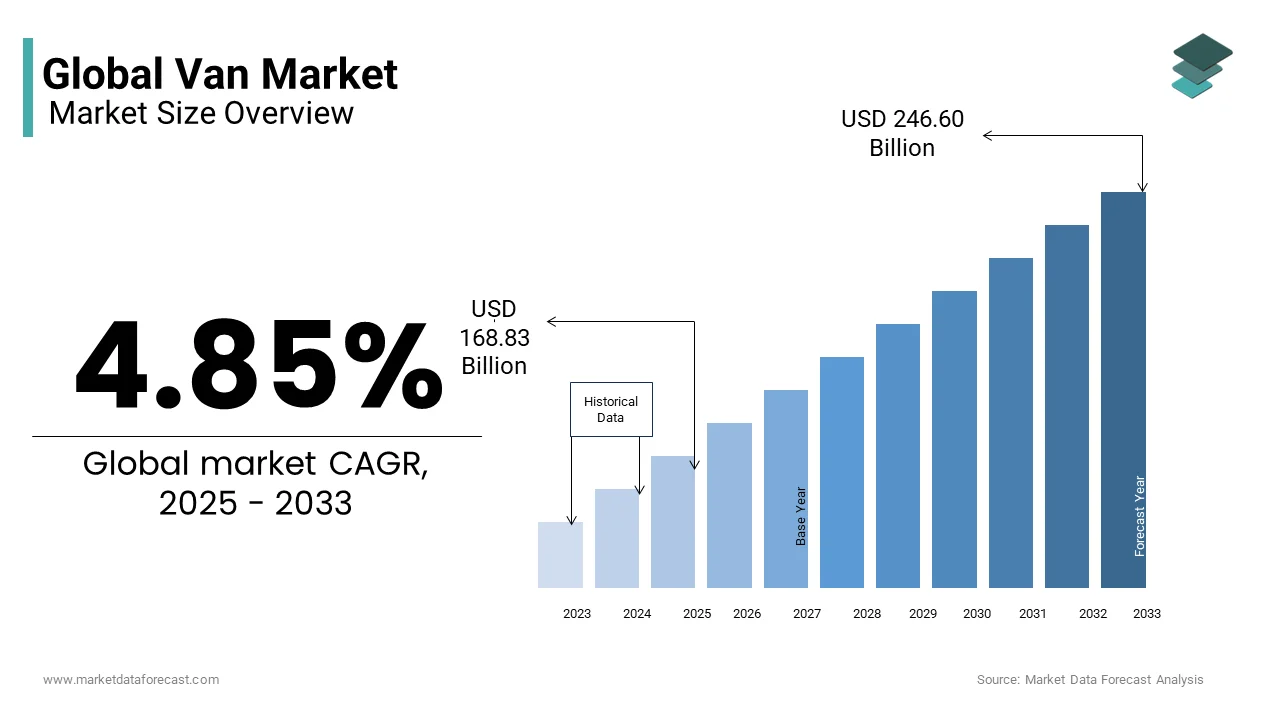

The global van market size was valued at USD 168.83 billion in 2025 and is anticipated to reach USD 177.02 billion in 2026 to reach USD 258.56 billion by 2034, growing at a CAGR of 4.85% during the forecast period from 2026 to 2034.

The van market covers light commercial vehicles (LCVs) designed for passenger transport, urban logistics, last-mile delivery, and mobile service operations. These vehicles serve as critical enablers of urban mobility and commercial efficiency, supporting sectors ranging from e-commerce and healthcare to construction and emergency services. Moreover, vans account for a notable share of all road freight movements in urban areas across OECD countries, despite representing only a small portion of the total vehicle fleet. Like, a large number of medical vans are deployed globally for mobile clinics and vaccination campaigns, particularly in rural and underserved regions. Similarly, rapid urbanization has intensified demand for compact, maneuverable vans capable of navigating dense city environments, with over 56% of the world’s population now residing in urban centers. The integration of digital dispatch systems and telematics has further elevated the operational sophistication of van fleets, transforming them into dynamic nodes within smart city ecosystems.

MARKET DRIVERS

Surge in Urban Last-Mile Delivery Demand

The exponential growth of online retail has dramatically increased the need for agile, high-utilization vans capable of executing rapid urban deliveries. According to the U.S. Department of Commerce, e-commerce sales in the United States reached $1.1 trillion in 2023, necessitating a corresponding expansion in delivery fleets. In Europe, the European Environment Agency confirms that van kilometers traveled for freight increased by 29% between 2015 and 2022, primarily due to parcel delivery services. Amazon alone operates over 20,000 custom electric delivery vans in Europe and North America, with plans to scale to 100,000 globally by 2025, as reported in its Climate Pledge Progress Update. Municipalities in Seoul, London, and Toronto are establishing urban consolidation centers, where large trucks offload cargo to smaller electric vans for final distribution, reducing congestion and emissions while increasing van utilization rates.

Expansion of Mobile Service and On-Demand Economies

The proliferation of mobile service platforms, spanning healthcare, food delivery, home repairs, and financial services, has elevated the van from a utility vehicle to a mobile operational unit. According to the International Labour Organization, over 150 million workers globally are engaged in platform-based gig economy jobs, many of which rely on vans for mobility and storage. Globally, DoorDash drivers completed over 2.16 billion food deliveries in 2023. Mobile medical clinics, often van-based, serve some of the primary healthcare needs in sub-Saharan Africa, where fixed clinics are scarce. These shifts are driving demand for customized interiors, refrigerated compartments, and integrated power systems, reinforcing the van’s role as a versatile service delivery platform.

MARKET RESTRAINTS

Limited Charging Infrastructure for Electric Vans in Emerging Markets

The transition to electric vans is hindered by inadequate charging networks, particularly in developing economies where grid reliability and urban planning constraints persist. Also, only a limited number of public charging stations in Latin America are compatible with commercial vehicles, compared to those in Western Europe. In India, despite government incentives under the FAME-II scheme, there are fewer units of fast-charging points dedicated to commercial EVs across the entire country. Nigeria’s power grid supplies electricity for only 8–10 hours per day in major cities, making overnight charging unreliable for fleet operators, according to the Nigerian Electricity Regulatory Commission. Additionally, the high upfront cost of depot-based charging systems deters small logistics firms from electrifying their fleets. These limitations delay adoption, particularly in regions where van-based delivery is expanding fastest.

Rising Insurance and Maintenance Costs for Advanced Van Fleets

Modern vans equipped with driver-assistance systems, telematics, and alternative powertrains face escalating insurance premiums and repair expenses, dampening fleet renewal cycles. Also, comprehensive insurance for a new electric cargo van in the U.S. is higher than for its internal combustion counterpart due to expensive battery and sensor replacements. In the UK, repair costs for vans with adaptive cruise control and lane-keeping systems are higher on average, driven by the complexity of recalibrating cameras and radar units after minor collisions. These financial pressures are particularly acute for small businesses, which constitute a significant share of van owners in Southeast Asia, limiting their ability to upgrade to newer, safer, or more efficient models.

MARKET OPPORTUNITY

Integration of Vans into Micro-Mobility and Urban Logistics Hubs

Cities are increasingly adopting integrated urban freight strategies that position vans as central nodes in consolidated delivery networks. According to the C40 Cities Climate Leadership Group, over 60 global cities have established low-emission urban consolidation centers where large trucks transfer cargo to electric vans for final distribution. Paris operates many such hubs, reducing last-mile delivery emissions. In Singapore, all new commercial vans will be zero-emission by 2040, accelerating the adoption of compact electric models. The World Economic Forum estimates that micro-consolidation models could reduce urban van traffic by 15–20% while increasing delivery efficiency. These developments are prompting OEMs to design modular, lightweight vans optimized for frequent stop-start cycles and tight turning radii, aligning vehicle capabilities with smart city logistics frameworks.

Customization and Fleet Digitization for Specialized Applications

The demand for purpose-built vans tailored to specific industries is driving innovation in modular interiors, connectivity, and lifecycle management. A significant share of fleet operators now require integrated telematics, real-time tracking, and predictive maintenance systems in their van procurement. In Germany, Mercedes-Benz Vans reports that many of its Sprinter sales were for customized configurations, including refrigerated units for pharma logistics, mobile workshops for utilities, and secure cash-in-transit variants. US deploys a large number of modified vans as mobile clinics, equipped with telemedicine systems and climate-controlled medical storage. Additionally, the rise of subscription-based fleet models, offered by companies, allows businesses to access up-to-date, software-enabled vans without capital investment, fostering faster adoption of digital and electric platforms in both developed and emerging markets.

MARKET CHALLENGES

Regulatory Fragmentation in Urban Access and Emission Zones

Van operators face a complex and inconsistent landscape of low-emission zones (LEZs), curbside regulations, and vehicle classification rules that vary by city and country, complicating fleet planning and compliance. As per the International Association of Public Transport, over 350 LEZs are now active in Europe, with differing standards for particulate matter, nitrogen oxides, and zero-emission requirements. In 2023, London expanded its Ultra Low Emission Zone (ULEZ) to cover all 32 boroughs, imposing daily charges on non-compliant vans, affecting a large number of vehicles. China enforces real-time emissions monitoring, requiring GPS-linked OBD systems in all commercial vans. The lack of harmonization across jurisdictions increases administrative burden and necessitates multi-fleet configurations, particularly for logistics companies operating across national borders. This regulatory patchwork raises operational costs and delays the retirement of older, polluting vehicles.

Intensifying Competition from Alternative Urban Mobility Solutions

Vans are increasingly competing with compact electric cargo bikes, drones, and autonomous delivery robots for last-mile dominance in dense urban environments. In Europe, cargo e-bikes are used for a portion of urban deliveries in Amsterdam, Berlin, and Copenhagen, with an increase in fleet deployments since 2020. In New York City, the number of delivery e-bikes surged to over 65,000 in 2023, many operating in areas where vans face parking restrictions, as reported by the NYC Department of Transportation. Amazon has completed a hundred commercial deliveries in California and Texas. These alternatives offer lower operating costs, reduced congestion, and easier curb access, challenging the van’s traditional role. While vans retain advantages in payload and range, their economic and spatial efficiency is being re-evaluated in cities prioritizing decarbonization and traffic decongestion.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.85% |

| Segments Covered | By Toonage Capacity, Propulsion, End-User, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Ford Motor Company, Mercedes-Benz Group AG, Volkswagen Group, Renault Group, TOYOTA MOTOR CORPORATION, Nissan Motor Co., Ltd., Hyundai Motor Company, MITSUBISHI MOTORS CORPORATION, ISUZU MOTORS LIMITED, Stellantis NV. |

SEGMENT ANALYSIS

By Tonnage Capacity Insights

The Up To 2 Tons segment dominated the global landscape by capturing 57.4% of total van sales in 2025. This segment’s dominance is primarily driven by its suitability for urban logistics, last-mile delivery, and small business operations in densely populated areas. In Europe, a large number of parcel deliveries in major cities are executed using sub-2-ton vans due to their maneuverability and compliance with low-emission zone (LEZ) access rules. In India, a significant number of new commercial van registrations in 2023 fell within the Up To 2 Tons category. These compact vans, including models like the Renault Kangoo and Toyota HiAce, are optimized for frequent stop-start cycles and offer lower acquisition and insurance costs, making them the preferred choice for gig economy fleets and urban service operators.

The 3 to 5.5 segment is the fastest-growing in the van market, projected to expand at a CAGR of 9.6% from 2023 to 2030, as per the U.S. Department of Energy’s Vehicle Technologies Office. This growth is fueled by the increasing demand for higher-payload vehicles in construction, municipal services, and inter-district logistics, where larger cargo volumes are required. Also, many of the utility and telecom service vans in the U.S. exceed 3 tons GVW to accommodate specialized equipment, aerial lifts, and mobile workshops. In Australia, there has been an increase in registrations of 4–5.5-ton vans in recent years, driven by mining support, emergency response, and regional freight needs. Additionally, the rise of mobile medical units and modular disaster relief vehicles, many based on 5-ton platforms like the Mercedes-Benz Sprinter 516, has expanded the functional scope of this segment. The integration of advanced chassis systems and extended-range electric drivetrains is further enhancing their operational viability in remote and off-road environments.

By Propulsion Insights

The Internal Combustion Engine (ICE) segment remained the prominent propulsion in the market by accounting for a substantial share of global van sales in 2024. This lead position is sustained by the extensive availability of fueling infrastructure, lower upfront costs, and proven reliability in diverse operating conditions. Moreover, the majority of commercial vans in operation across Latin America and Africa are powered by diesel or gasoline engines due to limited access to charging networks and grid instability. In Southeast Asia, ICE vans continue to dominate because of their ability to operate in high-temperature, high-humidity environments. Additionally, in regions like Eastern Europe and Central Asia, where average fleet turnover exceeds 12 years, the durability and ease of repair of ICE powertrains make them economically preferable. The widespread availability of spare parts and trained mechanics further entrenches ICE vans as the default choice for small and medium enterprises across emerging markets.

The Electric propulsion segment is growing at the fastest pace, with a projected CAGR of 28.4% from 2025 to 2033. This acceleration is driven by tightening urban emission regulations, corporate sustainability mandates, and declining battery costs. Also, numerous cities in the EU will ban non-zero-emission vans from city centers, compelling logistics firms to electrify their fleets. In the UK, the number of electric vans on the road surpassed 100,000 in 2023, representing a 47% year-on-year increase, as reported by the Society of Motor Manufacturers and Traders. In the U.S., electric van adoption among federal and municipal fleets grew notably in recent years, supported by the Inflation Reduction Act’s tax credits. Companies like Amazon and UPS have placed orders for over 50,000 electric delivery vans from Rivian and BrightDrop. Additionally, the total cost of ownership for electric vans is now 20–30% lower than ICE equivalents over five years, as verified by the National Renewable Energy Laboratory, making electrification increasingly economical even without subsidies.

By End-use Insights

The Commercial segment was the commanding end-use category in the market by representing a substantial share of global van demand in 2024. This dominance is rooted in the vehicle’s critical role in urban freight, service delivery, and enterprise mobility. Moreover, millions of small and medium enterprises (SMEs) worldwide rely on vans for daily operations, including retail distribution, plumbing, electrical services, and mobile healthcare. In 2023, China registered over 4 million commercial vehicles, serving e-commerce, delivery, and construction sectors. The rise of gig economy platforms like Uber, DoorDash, and Lalamove has further institutionalized van usage for income-generating activities. Municipal governments also deploy large fleets for waste collection, road maintenance, and emergency response. The integration of telematics and route optimization software has elevated vans from utility vehicles to data-driven operational assets, reinforcing their indispensability in modern economic ecosystems.

The Personal use segment is experiencing the fastest growth and is projected to expand at a CAGR of 8.9% during the forecast period. This surge is driven by shifting lifestyle preferences, remote work adoption, and the rise of recreational van living. The “workation” trend, where individuals combine remote work with travel, has boosted demand for self-contained van setups equipped with solar panels, sleeping quarters, and Wi-Fi connectivity. In Europe, private van registrations for leisure use rose in the past few years, particularly among millennials and digital nomads. Additionally, in countries like New Zealand and Canada, vans are increasingly used for outdoor recreation, including ski trips, camping, and fishing expeditions. The availability of factory-upfitted models from manufacturers like Mercedes-Benz (V-Class) and Ford (Transit Custom Nugget) has lowered entry barriers, making personalized van living more accessible and mainstream.

REGIONAL ANALYSIS

Europe Market Analysis

Europe holds a significant share of the global van market in 2024 and is positioned as a leader in vehicle safety, emissions regulation, and electrification adoption. Germany is a significant market, with 2,844,609 new registrations in 2023, according to the Federal Motor Transport Authority (KBA). The country hosts major OEMs such as Mercedes-Benz Vans, Volkswagen Commercial Vehicles, and Ford Otomotiv, which collectively dominate the mid- and high-end segments. France and the UK are among the key players in electric van deployment, with approximately 91,000 for the entire EU zero-emission vans registered in 2023, supported by national subsidies and urban access incentives. The European Union’s CO₂ emission standards for vans, mandating a 55% reduction by 2030 compared to 2021 levels, are accelerating the shift toward electrified platforms. Additionally, the proliferation of last-mile delivery hubs in cities like Amsterdam and Copenhagen is driving demand for compact, agile models tailored to dense urban environments.

Asia Pacific Market Analysis

Asia Pacific commands the largest regional share at 36.1% in 2024, which is driven by rapid urbanization, expanding e-commerce, and robust domestic manufacturing. China operates the world’s largest van fleet, with millions of units in commercial service. The country sold over 4 million new vans in 2023, led by brands like Maxus, Foton, and Wuling, which dominate the sub-2-ton delivery segment. India’s van landscape grew considerably year-on-year, fueled by the expansion of quick-commerce platforms, which require high-frequency, short-distance delivery fleets. Japan maintains a mature market with high penetration of kei vans, compact, tax-advantaged vehicles that account for a notable share of light commercial vehicle sales. South Korea is investing in hydrogen-powered delivery vans, with Hyundai deploying its XCIENT Fuel Cell models in urban logistics pilots, signaling a long-term shift toward alternative fuels.

North America Market Analysis

North America accounts for a notable share of the global van market, with the United States serving as the primary driver of innovation and fleet modernization. The U.S. operates a vast number of commercial vans, with Class 1 and 2 vans (up to 10,000 lbs GVW) comprising most of the new registrations. The rise of Amazon Logistics, UPS, and FedEx Ground has created sustained demand for durable, high-utilization delivery vans. California's Advanced Clean Fleets (ACF) rule mandates zero-emission vehicle (ZEV) purchases with the requirement for 50% ZEVs by 2026. However, it applies only to government fleets. Canada’s van market is closely aligned with U.S. trends, with cross-border logistics and last-mile delivery driving growth. Also, telematics adoption in Canadian van fleets has increased significantly since 2020, enhancing route efficiency and driver safety across urban and rural operations.

Latin America Market Analysis

Latin America holds a decent share of the global van market, with Brazil and Mexico emerging as key commercial and logistical hubs, as per the Inter-American Development Bank. As of 2025, Brazil’s van fleet has a substantial number of units, with Fiat Ducato dominating the urban delivery and service sectors. The country’s vast agricultural exports require extensive regional distribution networks, increasing demand for 3–5.5-ton vans capable of navigating rural roads. Mexico’s proximity to the U.S. has made it a critical node in nearshoring supply chains, with van traffic at border crossings rising. However, fuel theft, road degradation, and inconsistent enforcement of emission standards limit fleet modernization. Despite these challenges, the adoption of Euro 5 and ProCONVE L7 regulations is driving gradual upgrades in vehicle efficiency and safety across major metropolitan areas.

Middle East and Africa Market Analysis

Middle East & Africa collectively account for a small share of the global van market, with the Gulf Cooperation Council (GCC) states leading in fleet modernization and logistics infrastructure, as per the Gulf Organization for Industrial Consulting. The UAE operates over4o0,000 commercial vans, with Dubai registering an annual increase in delivery and service vans in recent years. Saudi Arabia’s Vision 2030 includes a $13 billion investment in logistics, aiming to increase non-oil GDP contribution and position the country as a regional freight hub. In South Africa, the van market is shaped by informal trade and minibus taxis, with a large number of repurposed vans serving as public transport. The African Development Bank reports that e-commerce growth in Nigeria and Kenya is driving demand for last-mile delivery vans, though fuel price volatility and import tariffs constrain widespread adoption. Nevertheless, pilot programs for electric vans in Dubai and Cape Town signal a growing commitment to sustainable urban mobility.

COMPETITIVE LANDSCAPE

The van market is characterized by intense competition shaped by technological disruption, regulatory divergence, and evolving urban logistics demands. Traditional OEMs face increasing pressure from new entrants specializing in electric and connected commercial vehicles, compelling legacy players to accelerate innovation cycles. Competition extends beyond vehicle performance to include total cost of ownership, software integration, and after-sales support networks. European and Japanese manufacturers lead in safety and efficiency, while Chinese firms are gaining traction through aggressive pricing and rapid electrification. In the Asia Pacific, localized production, service accessibility, and fleet customization are key differentiators. The rise of digital freight platforms and subscription-based mobility models is redefining ownership paradigms, intensifying the race for ecosystem dominance in this capital-intensive, application-driven sector.

KEY MARKET PLAYERS

These are the market players that are dominating the global van market.

- Ford Motor Company

- Mercedes-Benz Group AG

- Volkswagen Group

- Renault Group

- TOYOTA MOTOR CORPORATION

- Nissan Motor Co., Ltd.

- Hyundai Motor Company

- MITSUBISHI MOTORS CORPORATION

- ISUZU MOTORS LIMITED

- Stellantis NV.

Top Players In The Market

- Mercedes-Benz Vans has solidified its influence in the Asia Pacific van market through a strategic focus on premium commercial mobility, electrification, and localized innovation. The company has expanded its presence in China, India, and Southeast Asia by introducing the eSprinter and eVito electric models tailored for urban logistics and last-mile delivery. It also established a regional innovation hub in Shanghai to co-develop smart fleet management solutions with Chinese logistics firms. The integration of MBUX Pro Connect telematics into its Asia Pacific fleet offerings enables real-time monitoring of energy consumption, driver behavior, and predictive maintenance. Additionally, the company’s collaboration with DHL and Amazon on zero-emission delivery pilots in Tokyo and Sydney reinforces its leadership in sustainable urban freight ecosystems.

- Toyota Motor Corporation maintains a dominant footprint in the Asia Pacific van sector through its HiAce, Dyna, and Proace models, which are widely used in passenger transport, cargo delivery, and mobile services. The company has strengthened its regional position by localizing production in Thailand, Indonesia, and India, ensuring cost efficiency and supply chain resilience. It also partnered with Japan Post to deploy hybrid-powered delivery vans across rural prefectures, reducing fuel consumption compared to conventional models. The company’s investment in hydrogen fuel-cell technology, demonstrated through the Sora fuel-cell van trials in Tokyo, positions it at the forefront of alternative propulsion development in the region.

- Ford Motor Company has reinforced its relevance in the Asia Pacific van market by leveraging the global reputation of the Transit series while adapting to regional logistical demands. The company has intensified its focus on digital integration and electrification, launching the all-electric E-Transit in Thailand, New Zealand, and Australia in 2023. In India, Ford has partnered with startups in the quick-commerce space to offer customized Transit-based delivery solutions for 10-minute grocery services. The company’s SYNC 4A connected vehicle platform now supports multilingual voice commands and route optimization for drivers in Indonesia and the Philippines. Additionally, Ford’s investment in battery-as-a-service (BaaS) models in partnership with energy firms in Singapore is reducing upfront costs for fleet operators, accelerating the adoption of electric vans across the region.

Top Strategies Used by Key Market Participants

Key players in the van market are deploying a multi-pronged strategy centered on electrification, digital integration, regional localization, and ecosystem partnerships. Companies are accelerating the rollout of battery-electric models to comply with urban emission regulations and meet corporate sustainability targets. Expansion of charging infrastructure and battery leasing programs is reducing adoption barriers for small and medium enterprises. OEMs are integrating advanced telematics, AI-driven diagnostics, and over-the-air updates to enhance fleet efficiency and reduce downtime. Strategic collaborations with logistics platforms, e-commerce firms, and municipal agencies are enabling tailored vehicle configurations for last-mile delivery, mobile healthcare, and emergency response. Additionally, manufacturers are investing in modular platforms that allow rapid reconfiguration for diverse applications, from refrigerated transport to mobile workshops, ensuring versatility and faster time-to-market in an increasingly dynamic commercial landscape.

RECENT MARKET NEWS

In February 2024, Toyota introduced a hydrogen-powered prototype of the HiAce at the Tokyo Motor Show, marking a strategic move toward zero-emission long-range vans and positioning the company for future adoption in regions with developing hydrogen infrastructure.

MARKET SEGMENTATION

This research report on the global van market is segmented and sub-segmented into the following categories.

By Tonnage Capacity

- Up to 2 Tons

- 2 to 3 Tons

- 3 to 5.5 Tons

By Propulsion

- Internal Combustion Engine (ICE)

- Electric

- Hybrid

- Others

By End-use

- Commercial

- Personal

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East And Africa

Frequently Asked Questions

What is the Global Van Market?

It refers to the worldwide production, sale, and use of light commercial vans used for delivery, transport, and passenger services.

What’s driving the growth of the van market?

Rising e-commerce means more last-mile delivery needs, pushing companies to buy delivery vans.

Which regions lead in van sales?

Europe dominates due to strict emissions rules and high cargo van usage in cities.

How are electric vans shaping the market?

EV vans like the Ford E-Transit and Mercedes eSprinter are helping fleets cut emissions and fuel costs.

What types of vans are most popular?

Compact and mid-size cargo vans lead in commercial use for deliveries and services.

Who are the major van manufacturers globally?

Companies like Mercedes-Benz, Ford, Renault, Toyota, and Fiat are key players.

How has the pandemic affected the van market?

Lockdowns boosted online shopping, increasing demand for delivery vans.

Are used vans in high demand?

Yes, especially in developing countries where affordability matters.

What challenges do van makers face?

Supply chain issues and semiconductor shortages have slowed production.

What’s the future of the global van market?

Electric and connected vans will grow as cities push for cleaner transport.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com