Global Waste Management Market Size, Share, Trends & Growth Forecast Report – Segmented By Waste Type (Municipal solid waste (MSW), Industrial Waste, Hazardous Waste, Medical Waste, and Others), Service Type, Recycling Type, End User Type, and Region (North America, Latin America, Europe, Asia-Pacific, Middle East & Africa) - Industry Forecast (2026 to 2034)

Market Size, 2025

$1528 BnMarket Estimate, 2026

$1593 BnMarket Forecast, 2034

$2226 BnCAGR, 2026–2034

4.27%Global Waste Management Market Report Summary

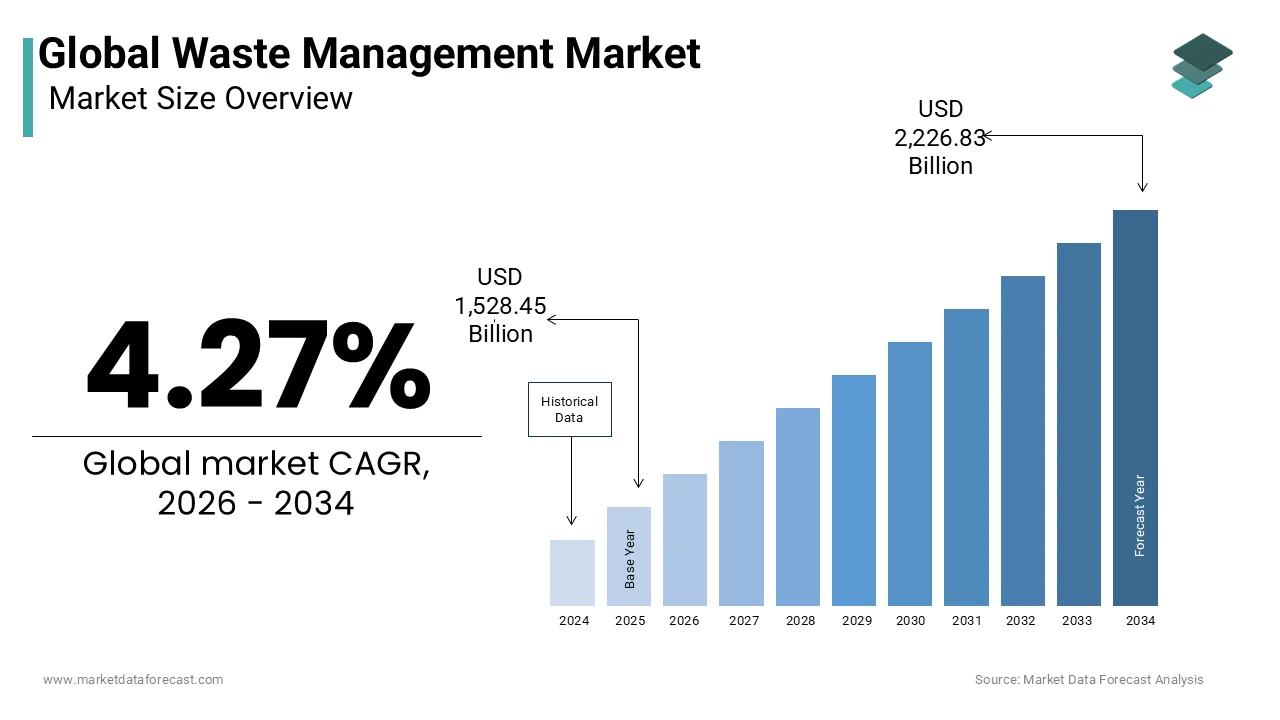

The global waste management market was valued at USD 1,528.45 billion in 2025, is estimated to reach USD 1,593.72 billion in 2026, and is projected to reach USD 2,226.83 billion by 2034, growing at a CAGR of 4.27% during the forecast period. Market growth is driven by increasing urbanization, rising waste generation, and growing environmental regulations across regions. Waste management plays a critical role in ensuring sustainable disposal, recycling, and resource recovery. The expansion of circular economy practices, along with advancements in waste processing technologies, is further supporting steady global market growth.

Key Market Trends

- Rising urbanization and population growth are driving waste generation and market demand.

- Increasing environmental regulations and sustainability initiatives are boosting market growth.

- Growing adoption of recycling and resource recovery practices is supporting market expansion.

- Expansion of waste to energy technologies is enhancing market development.

- Technological advancements in waste collection and processing are improving efficiency.

Segmental Insights

- Based on waste type, the municipal solid waste segment held 44.75% of the global waste management market share in 2025. This dominance is attributed to high volumes generated from households and urban areas.

- Based on service, the collection segment accounted for 41.1% of the global waste management market share in 2025, driven by the essential need for efficient waste gathering and transportation.

- Based on end user, the residential segment dominated with 47.4% of the global waste management market share in 2025, supported by increasing household waste generation.

Regional Insights

- The global waste management market is experiencing steady growth across regions, supported by rising waste volumes and regulatory frameworks.

- Asia Pacific was the largest contributor in 2025 and is expected to continue leading the market, driven by rapid urbanization, industrial expansion, and increasing focus on sustainable waste management solutions.

Competitive Landscape

The global waste management market is highly competitive, with key players focusing on service expansion, technological innovation, and sustainability initiatives to strengthen their market position. Companies are investing in advanced recycling technologies, waste to energy solutions, and digital waste management systems. Prominent players in the global waste management market include Waste Management Inc, Republic Services Inc, Veolia Environment S A, Suez Environment S A, Clean Harbors Inc, Stericycle Inc, Waste Connections Inc, Covanta Holding Corporation, Advanced Disposal Services Inc, and Biffa Group Holdings Ltd.

Global Waste Management Market Size

The global waste management market size was valued at USD 1,528.45 billion in 2025 and is projected to reach USD 2,226.83 billion by 2034 from USD 1,593.72 billion in 2026, growing at a CAGR of 4.27%.

Waste management encompasses the comprehensive spectrum of activities involved in the collection, transport, treatment, recycling, and disposal of waste materials generated by residential, commercial, industrial, and institutional sources. This sector is pivotal in maintaining public health, environmental sustainability, and resource efficiency within modern societies. The industry has evolved from simple landfilling to complex integrated systems that prioritize waste reduction, recovery, and energy generation. According to the World Bank, global waste generation is projected to reach 3.88 billion tonnes annually by 2050, reflecting the urgent need for robust management infrastructure. Urbanization and population growth are primary contributors to this increasing volume necessitating scalable solutions. As per the United Nations Environment Programme, the global recycling rate for plastic waste is approximately 9%, which is indicating significant gaps in current systems. Regulatory frameworks such as the European Union Circular Economy Action Plan are driving shifts towards sustainable practices. Technological advancements in sorting automation and waste to energy conversion are transforming operational efficiencies. The market is characterized by a mix of public municipal services and private sector operators striving to meet stringent environmental standards. Climate change mitigation efforts further emphasize the role of waste management in reducing greenhouse gas emissions from decomposing organic matter. Stakeholders are increasingly focusing on circular economy principles to minimize waste and maximize resource value. This dynamic landscape requires continuous innovation and investment to address the growing complexities of waste streams globally.

MARKET DRIVERS

Stringent Environmental Regulations and Government Mandates Drive Adoption of Sustainable Waste Practices

Governments worldwide are implementing rigorous environmental regulations and mandates that compel municipalities and industries to adopt sustainable waste management practices, which is a significant factor propelling the growth of the global waste management market. These policies aim to reduce landfill dependency, minimize pollution, and promote recycling and recovery rates. According to the European Commission, the EU Waste Framework Directive requires member states to recycle at least 55% of municipal waste by 2025, increasing to 60% by 2030. Such targets force significant investments in infrastructure and technology to achieve compliance. In the United States, the Environmental Protection Agency enforces strict guidelines on hazardous waste handling and landfill operations under the Resource Conservation and Recovery Act. These regulations ensure that waste is managed in a manner that protects human health and the environment. As per the Organisation for Economic Co-operation and Development, the number of extended producer responsibility policies has grown to over 400 globally, shifting the financial burden of waste management to manufacturers. This legislative pressure drives innovation in product design for recyclability and encourages the development of advanced sorting facilities. Non-compliance results in substantial fines and legal repercussions motivating organizations to prioritize waste management efficiency. Public awareness campaigns supported by government initiatives further reinforce the importance of proper waste segregation and disposal. The alignment of national policies with international climate goals such as the Paris Agreement amplifies the urgency for effective waste management. Consequently, regulatory frameworks serve as a powerful catalyst for market growth and technological advancement.

Rapid Urbanization and Population Growth Increase Waste Generation Volumes Requiring Expanded Infrastructure

The accelerating pace of urbanization and global population growth significantly increases the volume of waste generated, which is demanding for the expansion of waste management infrastructure and further propelling the global market expansion. As more people migrate to cities, the density of waste production rises, placing immense pressure on existing collection and disposal systems. According to the United Nations Department of Economic and Social Affairs, 68% of the world population is projected to live in urban areas by 2050, up from 55% in 2018. This demographic shift leads to higher consumption levels and, consequently, greater waste generation per capita. In developing regions, rapid urban expansion often outpaces the development of adequate waste management services, leading to environmental and health hazards. As per the World Bank, high-income countries generate approximately 1.58 kilograms of waste per person per day, while low-income countries generate 0.11 kilograms. The disparity highlights the need for tailored solutions across different economic contexts. Municipalities are investing in automated collection systems, larger transfer stations, and advanced processing facilities to handle the increasing load. The complexity of urban waste streams, which include diverse materials such as plastics, metals, organics, and e-waste, requires sophisticated sorting technologies. Smart city initiatives integrate digital solutions for efficient route optimization and real-time monitoring of waste bins. The sheer scale of waste produced in megacities demands innovative and scalable management strategies. Failure to expand infrastructure adequately results in overflowing landfills and increased pollution. Thus, urbanization acts as a primary driver for market expansion and modernization.

MARKET RESTRAINTS

High Capital Expenditure and Operational Costs Restrict Market Entry and Expansion

The high capital expenditure and operational costs associated with establishing and maintaining waste management facilities are impeding the expansion of the global waste management market. Building modern recycling plants, waste to energy facilities, and sanitary landfills requires substantial upfront investment, which can be prohibitive for smaller municipalities and private operators. According to the International Solid Waste Association, waste management costs can range from 20% to 50% of municipal budgets in some developing countries, depending on location and technology. These high initial costs limit the ability of many regions to adopt advanced waste management solutions. Operational expenses, including labor, fuel, maintenance, and regulatory compliance, which is further strain budgets. As per the Bureau of Labor Statistics, employment of refuse and recyclable material collectors is projected to grow by 3% through 2032, requiring competitive wages amidst labor shortages. The volatility of energy prices also impacts the profitability of waste to energy operations. Financial constraints often lead to deferred maintenance and outdated equipment, reducing efficiency and increasing environmental risks. In developing countries, limited access to financing and credit exacerbates the challenge of building adequate infrastructure. Governments may struggle to allocate sufficient funds for waste management amidst competing public service needs. The high cost barrier discourages new entrants and slows the adoption of innovative technologies. Without adequate financial support or public-private partnerships, many regions remain reliant on inefficient and environmentally harmful disposal methods. This economic restraint hinders the overall growth and modernization of the sector.

Inadequate Infrastructure and Logistical Challenges in Developing Regions Hinder Efficient Waste Collection

Inadequate infrastructure and logistical challenges in developing regions severely hinder the efficient collection and management of waste, which is posing a major restraint to the global market. Many low and middle income countries lack the necessary road networks, collection vehicles, and processing facilities to manage waste effectively. According to the World Health Organization, approximately 2.7 billion people globally lack access to waste collection services, leading to open dumping and burning. These practices cause severe environmental pollution and health issues, including respiratory diseases and water contamination. The absence of formal waste management systems forces reliance on informal sectors, which often operate under unsafe conditions. As per the United Nations Human Settlements Programme, narrow streets and unplanned urban settlements in many developing cities make it difficult for large collection vehicles to access residential areas. This logistical barrier results in irregular collection schedules and accumulated waste piles. The lack of segregated collection systems at the source complicates recycling efforts and reduces the quality of recoverable materials. Poor storage facilities lead to leakage of leachate and attraction of pests. Investment in infrastructure is often delayed due to bureaucratic hurdles and limited technical expertise. The fragmented nature of waste management services in these regions prevents economies of scale. Addressing these infrastructural deficits requires coordinated efforts between governments, international agencies, and private stakeholders. Until these foundational issues are resolved, efficient waste management will remain elusive in many parts of the world.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Robotics in Waste Sorting Enhances Efficiency and Recovery Rates

The integration of artificial intelligence (AI) and robotics in waste sorting is a significant opportunity for the waste management market by enhancing efficiency and material recovery rates. Traditional manual sorting is labor intensive, slow, and prone to errors, whereas AI-powered systems can identify and separate materials with high precision and speed. According to the McKinsey Global Institute, the circular economy supported by AI could reduce global greenhouse gas emissions by 3.6 billion tonnes per year by 2030, significantly improving the quality of recycled outputs. Robotics equipped with computer vision and machine learning algorithms can distinguish between different types of plastics, metals, and papers, even when they are contaminated or mixed. As per the Ellen MacArthur Foundation, improved sorting technologies are essential for achieving circular economy goals by ensuring that materials remain in use for longer periods. These technologies reduce operational costs by minimizing labor requirements and increasing throughput. Facilities adopting AI-driven sorting systems report higher purity levels in recycled bales, making them more valuable in secondary markets. The data generated by these systems provides insights into waste composition trends, enabling better planning and resource allocation. Investors are increasingly funding startups developing smart waste solutions, recognizing their potential to transform the industry. The scalability of AI technologies allows for deployment in various facility sizes, from small local centers to large regional hubs. This technological advancement not only improves economic viability but also supports environmental sustainability by maximizing resource recovery.

Expansion of Waste to Energy Technologies Offers Sustainable Alternatives to Landfilling

The expansion of waste to energy (WtE) technologies offers a lucrative opportunity for the waste management market by providing sustainable alternatives to landfilling and generating renewable energy. WtE facilities convert non-recyclable waste into electricity, heat, or fuel through processes such as incineration, gasification, and anaerobic digestion. According to the International Energy Agency, energy from waste (incineration and biogas) accounted for about 0.5% of total global electricity generation in recent years, reducing reliance on fossil fuels. This dual benefit of waste reduction and energy production aligns with global sustainability goals. As per the European Waste to Energy Association, modern WtE plants operate with high efficiency and strict emission controls, minimizing environmental impact. The technology is particularly effective for managing municipal solid waste that cannot be recycled. Governments are offering incentives and subsidies for WtE projects to encourage their development. In Asia, countries like Japan and South Korea have heavily invested in WtE infrastructure to address land scarcity and high waste volumes. The production of biogas from organic waste through anaerobic digestion is another growing segment contributing to renewable energy targets. Advances in emission control technologies have addressed previous concerns about air pollution, making WtE more socially acceptable. The ability to recover metals and other materials from bottom ash further enhances resource efficiency. As energy prices rise and landfill space diminishes, WtE becomes an increasingly attractive solution for integrated waste management strategies.

MARKET CHALLENGES

Fluctuating Commodity Prices for Recycled Materials Impact Economic Viability of Recycling Programs

The fluctuating commodity prices for recycled materials are majorly challenging the expansion of the global market. The profitability of recycling facilities depends heavily on the market demand and price for secondary raw materials such as paper, plastic, and metals. According to the Bureau of Labor Statistics, the Producer Price Index for recyclable material wholesalers fluctuated significantly between 2021 and 2024, affecting revenue streams for waste management companies. When prices for virgin materials drop due to low oil prices or oversupply, recycled materials become less competitive. As per the Institute of Scrap Recycling Industries, global trade tensions and tariffs have disrupted supply chains, leading to volatile pricing for scrap commodities. This uncertainty makes it difficult for recyclers to plan investments and maintain consistent operations. During periods of low prices, many recycling programs become financially unsustainable, leading to reduced collection services or increased fees for consumers. The lack of stable end markets for certain recycled plastics further exacerbates the issue. Manufacturers may prefer virgin materials due to consistent quality and lower costs. The volatility discourages long term contracts and investment in recycling infrastructure. To mitigate this challenge, the industry is seeking ways to create stable demand through mandated recycled content requirements in products. However, until market stability is achieved, financial risks remain a persistent challenge for waste management operators.

Public Resistance and NIMBY Syndrome Delay Construction of Waste Management Facilities

Public resistance and the "Not In My Back Yard" (NIMBY) syndrome significantly delay the construction and expansion of waste management facilities, which is posing a persistent challenge to the waste management market. Local communities often oppose the establishment of landfills, incinerators, or transfer stations near their residences due to concerns about odor, noise, traffic, and potential health risks. According to the Environmental Protection Agency, the development of a new waste facility typically involves public comment periods and hearings that can significantly extend the timeline of a project. This delays critical infrastructure projects and increases costs for developers. As per the National League of Cities, municipal leaders frequently face intense pressure from constituents to relocate proposed waste sites to other areas. The lack of trust in regulatory oversight and operator competence fuels opposition. Negative perceptions of waste facilities are often exacerbated by past incidents of pollution or mismanagement. Community engagement and transparency are essential but often insufficient to overcome deep-seated resistance. The resulting delays force municipalities to rely on distant facilities, increasing transportation costs and carbon emissions. In some cases, projects are cancelled entirely, leaving regions without adequate waste management capacity. The NIMBY phenomenon is particularly pronounced in densely populated urban areas where land is scarce and property values are high. Overcoming this challenge requires comprehensive education campaigns, community benefits agreements, and demonstrable commitment to environmental safety. Without public acceptance, the expansion of necessary waste infrastructure remains stalled.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.27% |

| Segments Covered | By Waste Type, Service Type, Recycling Type, End-User Type, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa. |

| Market Leaders Profiled | Waste Management, Inc., Republic Services, Inc., Veolia Environment S.A., Suez Environment S.A., Clean Harbors, Inc., Stericycle, Inc., Waste Connections, Inc., Covanta Holding Corporation, Advanced Disposal Services, Inc., Biffa Group Holdings Ltd., and Others. |

SEGMENTAL ANALYSIS

By Waste Type Insights

The municipal solid waste segment held the leading position in the global waste management market by holding 44.75 of the global market share in 2025. This segment dominates due to the continuous generation of waste from residential households, commercial establishments, and institutions, which forms the bulk of daily waste streams. The primary driver is the relentless pace of global urbanization, which concentrates population density and amplifies per capita waste production. According to the World Bank, global waste generation is expected to increase by 70% from 2016 levels to 3.40 billion tonnes by 2050. This volume necessitates robust collection and disposal infrastructure, making municipal waste the most visible and managed category. As per the United Nations Human Settlements Programme, cities are responsible for producing 70% of global waste, yet all regions face mounting pressure to manage these streams effectively. The composition of municipal waste, including packaging, food scraps, and disposable goods, reflects modern consumption patterns that prioritize convenience. Governments mandate regular collection services to maintain public health and sanitation standards, ensuring steady demand for waste management operators. The sheer consistency of this waste stream provides a stable revenue base for service providers. Regulatory frameworks increasingly target municipal waste for recycling and diversion from landfills, further driving investment in this segment. The universal nature of household waste generation ensures that this segment remains the cornerstone of the industry regardless of economic fluctuations.

However, the hazardous waste segment is the fastest growing segment in the global waste management market and is estimated to record a CAGR of 7.4% over the forecast period owing to the stricter environmental regulations governing the handling, treatment, and disposal of toxic and dangerous materials. Industries such as chemical manufacturing, pharmaceuticals, and electronics generate significant volumes of hazardous byproducts that require specialized management to prevent environmental contamination. According to the Environmental Protection Agency, under the Resource Conservation and Recovery Act, approximately 35 million tons of hazardous waste are generated annually in the United States alone. As per the Occupational Safety and Health Administration, workplace safety standards compel companies to invest in proper hazardous waste removal to avoid legal liabilities and health risks. The rising complexity of industrial processes introduces new types of hazardous substances that demand advanced treatment technologies such as incineration and chemical stabilization. Growing awareness of the long term health impacts of exposure to heavy metals and volatile organic compounds further drives demand for professional management services. Companies are increasingly outsourcing hazardous waste management to specialized firms to ensure compliance and reduce operational risks. The expansion of the pharmaceutical and semiconductor industries in emerging markets also contributes to the surge in hazardous waste volumes. These factors collectively position hazardous waste management as a high growth area within the broader industry.

By Service Insights

The collection segment led the market with 41.1% of the global market share in 2025. This dominance is primarily driven by the fundamental necessity of removing waste from generation points to prevent health hazards and environmental degradation. Collection services are typically mandated by local governments and form the first critical step in the waste management hierarchy. According to the World Bank, waste collection rates vary widely by income level, with high-income countries collecting nearly 100% of waste in cities while low-income countries collect about 48%. Efficient collection systems are the backbone of any successful waste management strategy, particularly in urban environments where waste accumulation poses immediate risks. The extensive logistical networks required for daily or weekly pickups involve significant investment in vehicles, personnel, and route optimization software. As per the Bureau of Labor Statistics, the number of employees in the waste collection industry has remained over 300,000 in the U.S. in recent years, reflecting the labor intensive nature of this service. The recurring nature of collection contracts provides waste management companies with predictable cash flows and long term customer relationships. Technological advancements such as smart bins and GPS tracking are enhancing the efficiency of collection operations, reducing fuel costs and improving service reliability. Collection acts as the gateway for subsequent services such as recycling and disposal, making it indispensable to the entire value chain.

On the other end, the energy recovery segment is on the rise and is predicted to expand at a CAGR of 8.1% over the forecast period due to the dual benefits of generating renewable energy and reducing the volume of waste sent to landfills. Waste to energy facilities convert non-recyclable municipal and industrial waste into electricity, heat, or fuel through processes like incineration and anaerobic digestion. According to the International Energy Agency, the global capacity for energy recovery from waste has grown as countries prioritize renewable energy targets and landfill diversion goals. As per the European Commission, the EU Waste Framework Directive establishes a waste hierarchy that places energy recovery above disposal, encouraging member states to invest in these facilities. The rising cost of fossil fuels and the urgency of climate change mitigation make energy from waste an attractive alternative for power generation. Governments offer subsidies and tax incentives for renewable energy projects, including waste to energy plants, enhancing their economic viability. Advances in emission control technologies have addressed environmental concerns, making these facilities more acceptable to communities. The ability to handle large volumes of mixed waste without extensive pre-sorting simplifies operations compared to recycling. Energy recovery aligns with corporate sustainability goals and national energy security strategies, driving sustained investment and growth in this segment.

By End User Insights

The residential segment accounted for 47.4% of the global market share in 2025. The growth of residential segment in the global market is attributed to the vast number of households globally and the consistent generation of municipal solid waste from daily activities. Residential waste includes packaging, food waste, plastics, and paper, which require regular collection and processing. According to the United Nations Department of Economic and Social Affairs, the world's population is expected to increase by nearly 2 billion persons in the next 30 years. As per the Environmental Protection Agency, food and paper/paperboard make up about 45% of total municipal solid waste in the U.S., much of which originates from residential sources. Local municipalities typically bear the responsibility for organizing residential waste services, ensuring widespread coverage and compliance with sanitation laws. The visibility of residential waste management issues, such as littering and illegal dumping, prompts continuous public and political attention. Consumer awareness campaigns regarding recycling and composting are primarily targeted at residential users, influencing behavior and participation rates. The decentralized nature of residential waste generation requires extensive logistical coordination but ensures a stable and predictable demand for services. Housing developments and urban expansion projects directly correlate with increased demand for waste management infrastructure. The residential sector's influence on policy and public opinion makes it a central focus for waste management initiatives and innovations.

However, the industrial segment is anticipated to register a CAGR of 6.6% over the forecast period in the global market owing to the increasing regulatory pressures on industries to manage their waste responsibly and adopt sustainable manufacturing practices. Industrial waste streams are diverse and often include hazardous materials requiring specialized treatment and disposal solutions. According to the Organisation for Economic Co-operation and Development, industrial sectors generate billions of tonnes of waste annually, prompting a global expansion of extended producer responsibility laws. As per the International Labour Organization, proper industrial waste management is vital to maintaining occupational health and safety standards for millions of workers. The rise of green manufacturing initiatives encourages industries to minimize waste generation and maximize recycling rates. Large corporations are setting ambitious sustainability targets that include zero-waste-to-landfill goals, driving demand for advanced waste management services. The growth of emerging economies has led to increased industrial activity, resulting in higher waste volumes that require professional management. Outsourcing waste management allows industrial firms to focus on core competencies while ensuring compliance with complex environmental laws. The integration of circular economy principles in industrial design further stimulates the demand for innovative waste recovery and recycling services.

REGIONAL ANALYSIS

Asia Pacific Waste Management Market Analysis

The Asia Pacific led the market globally in 2025 and this region is expected to lead the global market in waste management expansion for the next several years as it navigates the challenges of rapid industrialization and high-density urban waste generation. China and India are the primary contributors due to their massive populations and expanding manufacturing sectors. According to the World Bank, East Asia and Pacific region waste generation is expected to reach 602 million tonnes annually by 2030, a significant increase that outpaces many other regions. Governments are implementing stricter waste management regulations to address environmental pollution and public health concerns. As per the Ministry of Ecology and Environment in China, the nation has implemented the "zero waste city" pilot program in dozens of cities to promote resource recycling and reduce landfill usage. The region faces challenges with informal waste picking sectors but is gradually formalizing these operations. Investment in waste to energy facilities is increasing, particularly in Japan, South Korea, and China, to reduce landfill dependency. The presence of numerous multinational waste management companies facilitates technology transfer and best practices. Rapid urban expansion requires scalable solutions for municipal solid waste management. The region's commitment to sustainable development goals supports market growth.

Europe Waste Management Market Analysis

European countries are anticipated to further refine their circular economy models over the next few years, maintaining high recycling benchmarks through strict legislative targets and advanced sorting technology. The European market is defined by advanced regulatory frameworks and a strong commitment to circular economy principles. According to Eurostat, the EU recycling rate of municipal waste reached 49.1% in 2022, reflecting effective policy implementation. Countries like Germany, Sweden, and the Netherlands are pioneers in waste to energy and high efficiency recycling technologies. As per the European Environment Agency, landfilling of municipal waste in the EU has decreased by 53% since 1995. Strict environmental standards enforce proper handling of hazardous and electronic waste. Public awareness and participation in waste separation programs are high across the region. Investment in innovative sorting technologies and biological treatment facilities continues to grow. The region focuses on reducing plastic waste and promoting sustainable packaging solutions. Government subsidies support the development of green waste management infrastructure. Europe serves as a model for sustainable waste management practices worldwide.

North America Waste Management Market Analysis

North American nations are likely to accelerate their adoption of smart waste technologies and landfill diversion strategies over the next few years to address stagnant recycling rates and rising operational costs. The market in North America is characterized by a mix of advanced infrastructure and evolving regulatory landscapes across the United States and Canada. According to the Environmental Protection Agency, the U.S. generated about 292.4 million tons of municipal solid waste in a single recent reporting year. As per the National League of Cities, an increasing number of municipal leaders are prioritizing sustainable waste management to achieve climate and environmental goals. Private sector participation is strong, with major companies providing comprehensive waste services. The region is seeing increased investment in waste to energy projects, particularly in states with renewable portfolio standards. Canada focuses heavily on organic waste composting and extended producer responsibility programs. Technological innovation in sorting and processing is prevalent, driven by private investment. The market is shifting towards sustainable practices influenced by consumer demand and corporate sustainability commitments.

Latin America Waste Management Market Analysis

Latin American regions are expected to make strides in formalizing waste collection and expanding sanitary landfill infrastructure over the next few years to bridge the gap between urban centers and rural areas. Brazil, Mexico, and Chile are the leading markets due to their larger economies and urban populations. According to the Pan American Health Organization, waste collection coverage in Latin America and the Caribbean reaches about 90% in urban areas but falls significantly in rural regions. As per the World Bank, the region is expected to see a 25% increase in waste generation by 2050, necessitating urgent infrastructure improvements. The region faces challenges with open dumping, but governments are increasingly investing in modern waste treatment facilities. Efforts to integrate informal waste pickers into the formal economy are gaining momentum in several countries. The expansion of private sector involvement through concessions and partnerships is helping to improve service efficiency. Regulatory reforms aimed at promoting recycling and reducing environmental impact are becoming more common. Despite economic fluctuations, the region presents opportunities for waste-to-energy and resource recovery projects. The focus on improving public health and environmental quality drives the demand for professional waste management services.

COMPETITIVE LANDSCAPE

The competition in the Waste Management Market is characterized by a mix of large multinational corporations regional providers and specialized niche operators vying for market dominance. Major players leverage their extensive infrastructure and financial resources to offer integrated services including collection recycling and disposal. Regional competitors often differentiate themselves through localized knowledge and personalized customer service. The market sees intense rivalry in securing municipal contracts and commercial accounts which provide stable recurring revenue. Technological innovation serves as a key differentiator with companies investing in smart waste solutions and automated sorting systems. Regulatory compliance and environmental sustainability are critical factors influencing competitive advantage. Companies with strong environmental social and governance profiles attract environmentally conscious clients and investors. Price competition remains significant in commoditized services like landfill disposal prompting firms to optimize operational efficiency. The rise of circular economy principles encourages collaboration between waste managers and manufacturers to close material loops. Strategic acquisitions allow larger firms to enter new geographic markets or service segments. The competitive landscape requires continuous adaptation to regulatory changes and technological advancements to maintain relevance and profitability in this essential service sector.

Key Market Players

The major key players in the global waste management market are

- Waste Management, Inc.

- Republic Services, Inc.

- Veolia Environment S.A.

- Suez Environment S.A.

- Clean Harbors, Inc.

- Stericycle, Inc.

- Waste Connections, Inc.

- Covanta Holding Corporation

- Advanced Disposal Services, Inc.

- Biffa Group Holdings Ltd.

Top Players in the Market

- Waste Management Inc is a leading provider of comprehensive waste management environmental services in North America. The company contributes to the global market by operating an extensive network of landfills transfer stations and recycling facilities. It recently strengthened its market position by investing heavily in renewable natural gas projects which convert landfill methane into clean energy. In March 2023 the company expanded its recycling capabilities through advanced sorting technologies to improve material recovery rates. Waste Management Inc focuses on sustainability goals by reducing greenhouse gas emissions and enhancing circular economy practices. The organization leverages digital tools for route optimization and customer service efficiency. Its robust infrastructure and strategic acquisitions enable it to serve residential commercial and industrial clients effectively. These initiatives reinforce its leadership in sustainable waste solutions and drive long term value creation for stakeholders while maintaining operational excellence across its diverse service portfolio.

- Veolia Environnement S.A. is a global leader in ecological transformation specializing in water waste and energy management. The company contributes to the global market by providing innovative solutions for resource recovery and environmental protection. Veolia recently strengthened its market position by acquiring key assets in the hazardous waste and industrial cleaning sectors to expand its service offerings. In June 2022 the company launched new digital platforms to optimize waste collection and treatment processes for urban clients. Veolia prioritizes circular economy principles by transforming waste into valuable resources such as energy and raw materials. The organization collaborates with cities and industries to develop customized sustainability strategies. Its extensive international presence allows it to implement best practices across diverse regulatory environments. These actions enhance its competitive edge and support its mission to accelerate the transition to a more sustainable and resource efficient economy worldwide.

- Republic Services Inc is a major provider of non hazardous solid waste collection transfer recycling and disposal services. The company contributes to the global market by offering integrated waste management solutions that prioritize environmental stewardship. Republic Services recently strengthened its market position by investing in advanced recycling facilities and renewable energy projects. In September 2023 the company expanded its landfill gas to energy capabilities to generate clean electricity from waste. Republic Services focuses on innovation through the deployment of automated side loader trucks and smart bin technologies. The organization emphasizes safety and sustainability in its operations aiming to reduce its carbon footprint. Its strategic partnerships with municipalities and businesses ensure reliable and efficient waste management services. These efforts solidify its reputation as a trusted partner in environmental services and drive growth through sustainable practices and technological advancements in the waste management industry.

Top Strategies Used by the Key Market Participants

Key players in the Waste Management Market employ several strategic initiatives to maintain competitiveness and drive growth. Mergers and acquisitions are central as companies consolidate fragmented markets to achieve economies of scale and expand geographic reach. Investment in technology such as artificial intelligence and robotics enhances sorting efficiency and operational productivity. Diversification into renewable energy sources like landfill gas and waste to energy creates new revenue streams. Strategic partnerships with municipalities and industrial clients secure long term contracts and stable cash flows. Companies focus on sustainability branding to align with environmental regulations and consumer preferences. Expansion of recycling capabilities addresses the growing demand for circular economy solutions. Digital transformation improves customer experience through real time tracking and billing transparency. Regulatory compliance drives innovation in hazardous waste handling and disposal methods. These multifaceted strategies enable key participants to navigate complex market dynamics and sustain their leadership positions effectively in the evolving waste management landscape.

Global Waste Management Market News

- In March 2023, Waste Management Inc expanded its recycling capabilities through advanced sorting technologies to improve material recovery rates and strengthen the Waste Management Market presence

- In June 2022, Veolia Environnement S.A. launched new digital platforms to optimize waste collection and treatment processes for urban clients and strengthen the Waste Management Market presence

- In September 2023, Republic Services Inc expanded its landfill gas to energy capabilities to generate clean electricity from waste and strengthen the Waste Management Market presence

- In January 2023, Veolia Environnement S.A. acquired key assets in the hazardous waste sector to expand service offerings and strengthen the Waste Management Market presence

- In November 2022, Waste Management Inc invested heavily in renewable natural gas projects to convert landfill methane into clean energy and strengthen the Waste Management Market presence

MARKET SEGMENTATION

This research report on the global waste management market has been segmented and sub-segmented based on type, service, recycling, end-user, and region.

By Waste Type

- Municipal solid waste (MSW)

- Industrial waste

- Hazardous waste

- Medical waste

- Others

By Service Type

- Collection

- Transportation

- Sorting

- Recycling

- Disposal

- Energy recovery

By Recycling

- Organic

- Plastic

- Paper

- Metal

By End User

- Residential

- Commercial

- Industrial

By Region

- North America

- Latin America

- Europe

- Asia Pacific

- Middle East and Africa

Frequently Asked Questions

1.What is the waste management market?

The waste management market includes the collection, transportation, processing, recycling, and disposal of municipal, industrial, and hazardous waste.

2.What factors are driving growth in the waste management market?

Market growth is driven by urbanization, population growth, stricter environmental regulations, and increasing focus on recycling and sustainability.

3.What are the main types of waste managed in the market?

Major waste types include municipal solid waste, industrial waste, hazardous waste, electronic waste, and biomedical waste.

4.How does recycling contribute to the waste management market?

Recycling reduces landfill usage, conserves natural resources, and supports circular economy initiatives.

5.What role do government regulations play in waste management?

Government regulations enforce proper waste disposal, promote recycling, and encourage adoption of environmentally friendly waste treatment methods.

6.What technologies are commonly used in waste management?

Common technologies include waste to energy, composting, material recovery facilities, incineration, and sanitary landfills.

7.What industries are major contributors to waste generation?

Major contributors include residential, commercial, industrial, healthcare, and construction sectors.

8.Which regions dominate the global waste management market?

North America, Europe, and Asia Pacific dominate the market due to high waste generation and advanced waste management infrastructure.

9.Who are the key players in the waste management market?

Key players include Veolia, Waste Management Inc., SUEZ, Republic Services, and Clean Harbors.

10.What challenges does the waste management market face?

Challenges include high operational costs, landfill capacity limitations, and lack of recycling awareness in some regions.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com