Global Wind Turbine Scrap Market Size, Share, Trends, & Growth Forecast Report – Segmented By Service (Collection and Segregation, Recycling, and Disposal), Product Type (Iron and Steel, Plastic, Precious Metals, Fiber Glass, and Others), & Region - Industry Analysis From 2026 to 2034

Global Wind Turbine Scrap Market Size

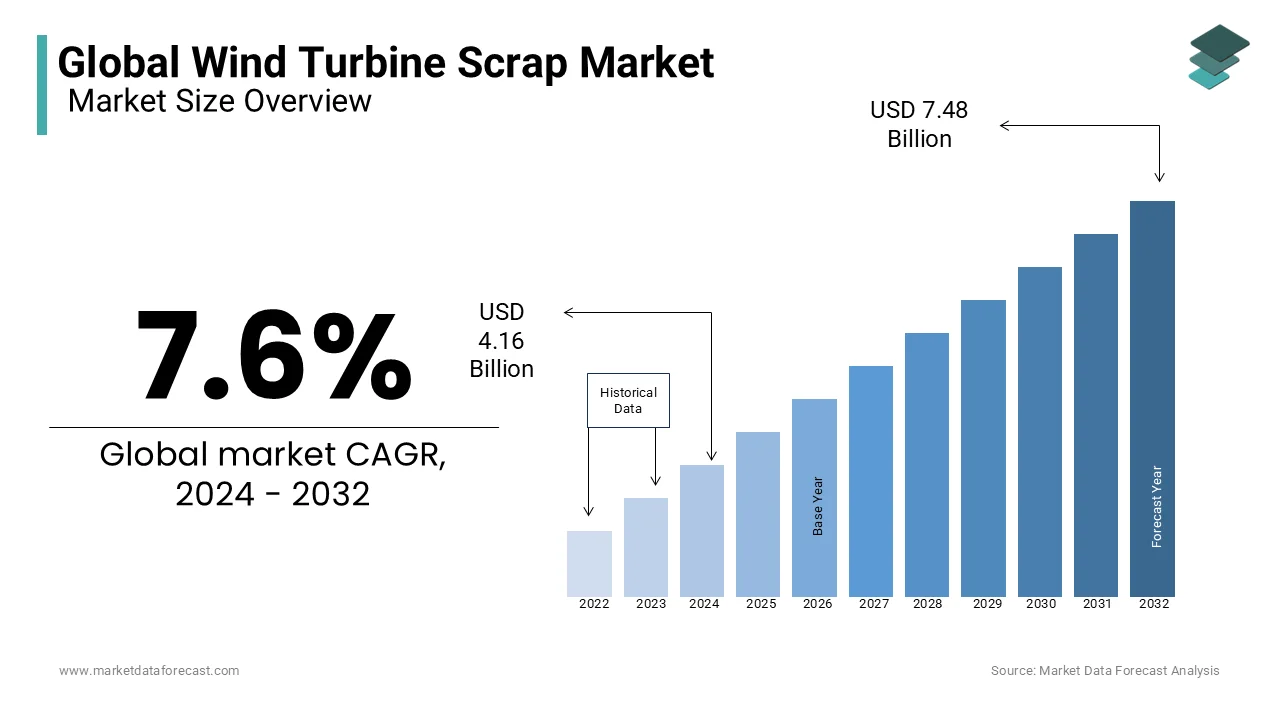

The Global Wind Turbine Scrap Market was worth USD 4.16 billion in 2024 and is anticipated to reach a valuation of USD 8.05 billion by 2033 from USD 4.48 billion in 2025 and it is predicted to register a CAGR of 7.6% during the forecast period 2025 to 2033.

The need for wind turbines has increased notably in recent years. Wind turbines are cheaper and cleaner substitutes for crude oil. As a result, the need for wind turbines is predicted to improve markedly over the next year. The wind turbine has a typical useful life of 20 to 23 years. After that, the particular turbine is recharged or deactivated. As part of the deactivated process, recyclable substances such as steel and various expensive metals are recovered. Recycling the substance reduces waste and also provides productive benefits. Onshore wind energy has become one of the most valued sustainable energy sources in the world. The accumulated volume of onshore wind energy is predicted to see an addition of 8.34% in 2020 compared to the volume of the previous year. On the other hand, the offshore area is powered by worldwide wind power and is predicted to see the fastest development in the next year.

MARKET TRENDS

Onshore wind energy has become one of the most valued sustainable energy sources in the world. The accumulated volume of onshore wind energy is predicted to see an addition of 8.34% in 2020 compared to the volume of the previous year. On the other hand, the offshore area is powered by worldwide wind power and is predicted to see the fastest development in the next year.

MARKET DRIVERS

Rapid industrialization and urbanization are key drivers of the worldwide market for wind turbine scrap.

The increase in the number of industries stimulates the call for electricity. Wind turbines are being considered to meet this call. Therefore, the increase in the number of wind turbines is predicted to generate more wind turbine scrap. Therefore, industrialization and urbanization are predicted to drive the worldwide market for wind turbine scrap during the foreseen period. The implementation of strict government regulations to reduce carbon emissions is one of the main drivers of the worldwide market for wind scrap. Government incentive programs to promote wind turbine installation are also boosting the market. Additionally, most industries and government agencies are focusing on wind turbines for power generation due to environmental concerns. Therefore, the implementation of strict government regulations to reduce carbon emissions is likely to be a key driver of the worldwide market for wind turbine scrap.

MARKET RESTRAINTS

The lack of technology to recover fiberglass composites from blades is a major factor limiting the worldwide market for wind turbine scrap.

MARKET OPPORTUNITIES

Wind turbine blades are made of composite glass fibers, which are relatively difficult to recycle or reuse.

Currently, these slides are thrown into landfills, which are not ecological solutions. Therefore, companies are now focusing on providing better solutions or methods by which the recovery of these shovels is easy, environmentally friendly, and economical. Recent automation makes it difficult to recover the fiberglass blend from the edges. In addition, it would require significant spending on research and development to advance automation. Therefore, the inaccessibility of automation to recover the glass fiber blend is a major factor hampering the worldwide market for wind turbine scrap. It is possible to reuse the expensive complex substance by refining the cement using this procedure; The raw cement materials are moderately displaced by the fiber optic and padding of the suit, and the organic fragments return the carbon as energy.

MARKET CHALLENGES

Current technology makes it difficult to recover fiberglass composites from blades. In addition, significant investments in R&D would be necessary to develop the technology. Therefore, the lack of technology to recover fiberglass composites is a major factor hampering the worldwide market for wind turbine scrap.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 7.6% |

| Segments Covered | By Service, Product Type, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Belson Steel Center Scrap Inc., Global Fiberglass Solutions, Veolia, Renewable Parts Ltd., Acciona S.A, Nordex SE, Dewind Co., Senvion S.A, and Others. |

SEGMENT ANALYSIS

By Service Insights

The inaccessibility of automation to recover the fibreglass combination of the blades is a major element hampering the worldwide market for wind turbine scrap. Recent automation makes it difficult to recover the fibreglass blend from the edges. In addition, it would require significant spending on research and development to advance automation. Therefore, the inaccessibility of automation to recover the glass fibre blend is a major factor hampering the worldwide market for wind turbine scrap.

REGIONAL ANALYSIS

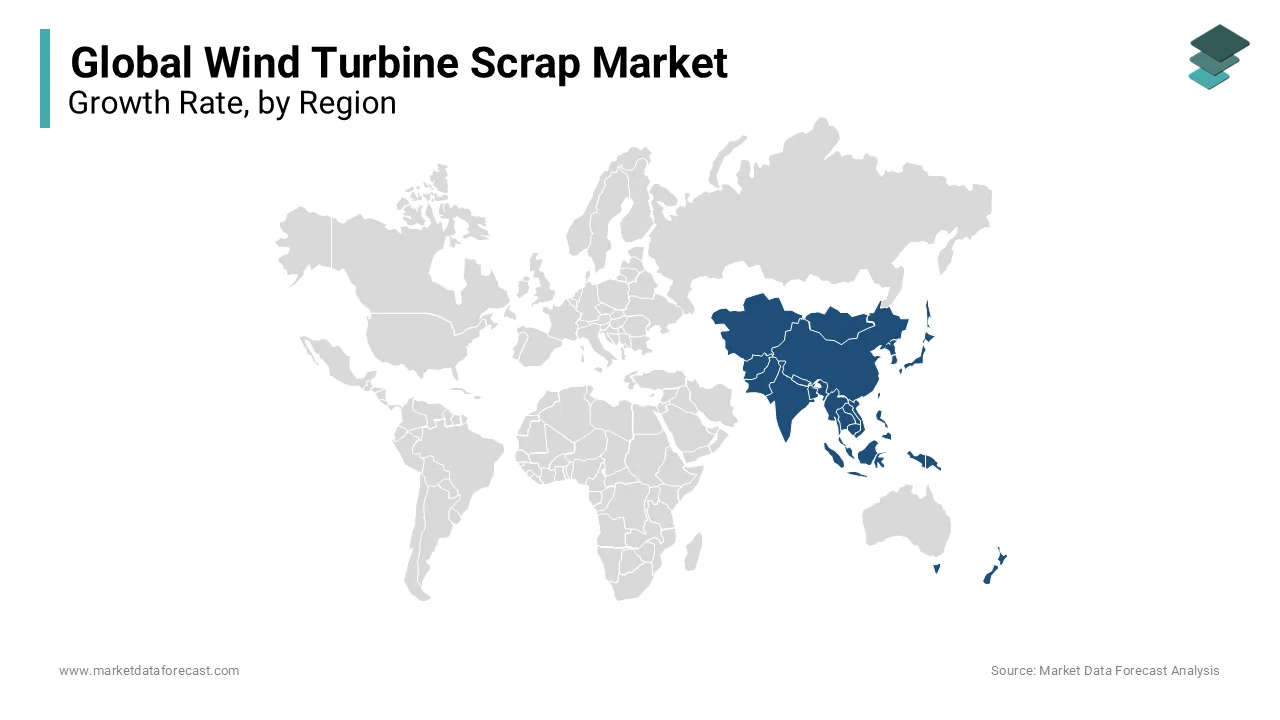

The dominance of Asia-Pacific can be attributed to the advancement of a new wind facility in the area. Furthermore, the advancement of the infrastructure framework related to wind energy is advancing rapidly in the Asia-Pacific region. China records the government's share of the Asia-Pacific wind turbine scrap market in 2020 mainly due to the expansion of wind power generation in the country. The nation is predicted to provide a remarkable boost in wind power creation next year. This is estimated to explode the wind turbine scrap market in China during the foreseen period. In terms of market development, Europe is supporting Asia-Pacific in the worldwide wind scrap market. Increased government regulations to encourage wind power manufacturing in Europe are predicted to boost the market for scrap wind turbines in the area over the foreseen period. India is also focusing on offshore developments. In July 2020, India called for a semblance of attention to the country's first offshore wind activity being structured in the Gulf of Khambat, off the coast of Gujarat state.

Asia-Pacific is predicted to dominate the worldwide wind turbine scrap market during the foreseen period. The dominance of Asia-Pacific can be attributed to the development of new wind farms in the region. Furthermore, the development of infrastructure related to wind farms is escalating at a rapid pace in Asia-Pacific. China had the largest share of the Asia-Pacific wind turbine scrap market in 2018, mainly due to the increase in the number of wind farms in the country. It is estimated that the country will invest significantly in wind generation in the near future. This is predicted to boost the wind turbine scrap market in China during the foreseen period. In terms of market share, Europe follows Asia-Pacific in the worldwide market for wind turbine scrap. Increased government policies to promote wind power generation in Europe are predicted to boost the wind scrap market in the region during the foreseen period.

KEY MARKET PLAYERS

Companies that play a notable role in the global wind turbine scrap market include Belson Steel Center Scrap Inc., Global Fiberglass Solutions, Veolia, Renewable Parts Ltd., Acciona S.A, Nordex SE, Dewind Co., Senvion S.A, and Others.

RECENT MARKET HAPPENINGS

- Vestas introduces the latest low wind turbine variant for the Indian industry. A wind company Vestas based in Denmark declared on Tuesday that it has introduced the latest turbine variant optimized for low and ultra-low wind project conditions in the region of India.

- A cross-sector consortium, involving LM Wind Power, has declared a pioneering project to make and produce the wind industry's first 100% recyclable wind turbine blade.

MARKET SEGMENTATION

This research report on the global wind turbine scrap market has been segmented and sub-segmented based on service, product type, and region.

By Service

- Collection and Segregation

- Recycling

- Disposal

By Product Type

- Iron and Steel

- Plastic

- Precious Metals

- Fiber Glass

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East & Africa

Frequently Asked Questions

What is the Wind Turbine Scrap Market growth rate during the projection period?

The Global Wind Turbine Scrap Market is expected to grow with a CAGR of 7.6% between 2025 and 2033.

2. What can be the total Wind Turbine Scrap Market value?

The Global Wind Turbine Scrap Market size is expected to reach a revised size of USD 8.05 billion by 2033.

Name any three Wind Turbine Scrap Market key players?

Renewable Parts Ltd., Acciona S.A., and Nordex SE are the three Wind Turbine Scrap Market key players.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com