Global Wooden Toys Market Size, Share, Trends and Growth Forecast Report - Segmented By Age group (Infants, Toddlers, Pre-Schoolers and Older Children), Product (Building Blocks, Puzzles, Dolls, Vehicles, Educational Toys and Others), Distribution channel (Physical Stores, Online and Both), and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa) - Industry Analysis (2026 to 2034)

Market Size, 2025

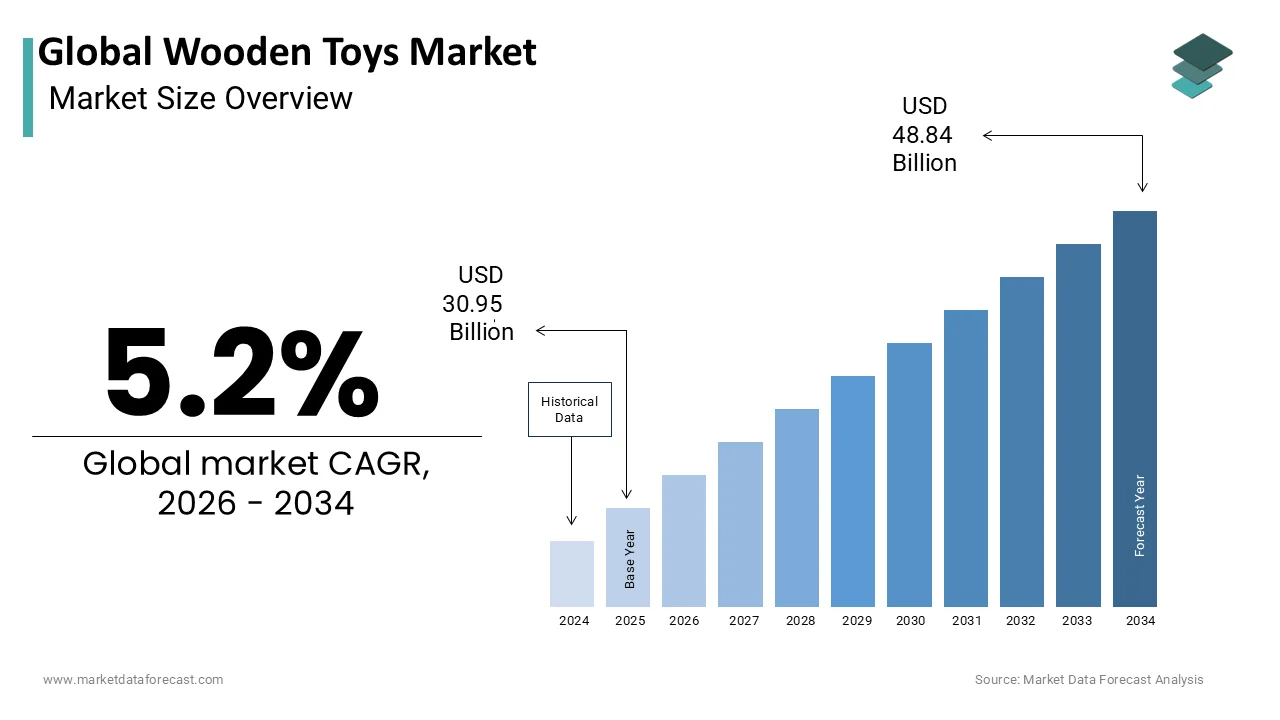

$30.95 BnMarket Estimate, 2026

$32.56 BnMarket Forecast, 2034

$48.84 BnCAGR, 2026–2034

5.2%Global Wooden Toys Market Size

The global wooden toys market was valued at USD 30.95 billion in 2025. The market size is expected to grow at a CAGR of 5.2% from 2026 to 2034 and be worth USD 48.84 billion by 2034 from USD 32.56 billion in 2026.

Wooden toys are playthings constructed primarily from natural wood rather than synthetic materials like plastic. This market exhibits a conscious consumer choice aligned with ecological stewardship and child safety priorities across European households. According to Eurostat demographic indicators, the European Union records over 3.7 million live births annually, establishing a substantial baseline population that shapes consumer demand for early childhood and pediatric sector products. The median age of the EU population stands at 44.7 years, indicating a mature consumer base where parents often possess higher disposable income and place a premium on quality and safety for their offspring. Heightened parental awareness regarding the environmental impact of electronic and plastic waste has accelerated a commercial consumer trend toward sustainable children's products, driving increased demand for biodegradable and ethically sourced wooden alternatives. The market is deeply rooted in a cultural renaissance of traditional craftsmanship, where toys are viewed as heirlooms rather than transient goods. Unlike mass-produced plastic items, wooden toys in Europe are frequently associated with forest stewardship, with a significant portion of raw material sourced from sustainably managed forests certified under schemes like FSC. This alignment with ecological values defines the market identity, positioning it as a conscious choice for families seeking to minimize their environmental footprint while providing safe, non-toxic play experiences for children.

MARKET DRIVERS

Escalating Parental Preference for Non-Toxic and Safe Materials

Parents are increasingly demanding chemical-free playthings, which makes safety the top driver for the wooden toys market. This shift is fueled by a desire to avoid synthetic hazards like phthalates, bisphenol A, and microplastics. Modern European consumers are increasingly educated about the potential health risks associated with prolonged exposure to plasticizers and volatile organic compounds, leading to a decisive shift toward natural materials. According to the European Chemicals Agency, hundreds of chemical substances have been formally identified as being of very great concern due to their hazardous properties, triggering strict regulatory tracking obligations for manufacturers and importers. Many of these chemicals have historically been used in plastic toy manufacturing, leading to increased caution among parents and caregivers regarding synthetic materials. In response, families are actively seeking products made from solid wood finished with water-based, non-toxic paints and natural oils. Research indicates that an increasing majority of parents in Western Europe closely evaluate material composition and chemical safety certifications when selecting toys for young children, driving a prominent market shift toward eco-friendly alternatives. This demand is further amplified by strict EU regulations such as the Toy Safety Directive, which mandates rigorous testing, yet parents often perceive wood as inherently safer due to its natural origin and lack of industrial additives. The tactile warmth and absence of sharp edges in well-crafted wooden toys also reduce physical injury risks, appealing to safety-conscious demographics. Consequently, manufacturers who certify their products as free from harmful chemicals and utilize organic finishes are witnessing robust sales growth, as trust in natural materials becomes a primary purchasing determinant in the regional marketplace.

Growing Alignment with Montessori and Waldorf Educational Philosophies

The widespread adoption of child-centered educational methodologies like Montessori and Waldorf further boosts the growth of the wooden toys market. These programs explicitly advocate for the use of simple, open-ended wooden playthings to stimulate imagination and cognitive growth. These pedagogical approaches argue that toys with fixed functions or electronic distractions limit creative potential, whereas wooden blocks, figures, and puzzles encourage active problem solving and sensory exploration. The steady global proliferation of Montessori and Waldorf-inspired early childhood education facilities has intensified demand for specialized, tactile wooden learning aids and open-ended educational toys in both institutional and domestic settings. Parents influenced by these philosophies prioritize toys that can be used in multiple ways, such as a wooden block serving as a car, a building element, or a food item, thereby extending the product lifecycle and value. Consumer purchasing patterns demonstrate that households adopting alternative early childhood development philosophies frequently exhibit a strong preference for durable, high-quality, and sustainably sourced products, prioritizing a toy's developmental longevity over a large volume of low-cost disposable items. This trend is not limited to private schools but has permeated mainstream parenting culture, with public discourse increasingly favoring slow play and digital detoxification for young children. The emphasis on sustainability within these educational frameworks further reinforces the preference for wood, as it aligns with teachings about nature and respect for the environment. This philosophical shift ensures a steady and growing stream of demand for wooden toys that support developmental milestones without relying on batteries or screens.

MARKET RESTRAINTS

Substantial Price Disparity Compared to Plastic Alternatives

The significantly higher price point of wooden toys, relative to plastic alternatives, remains the principal barrier to broader market penetration across the wooden toys market. As a result, market expansion is restricted within price-sensitive demographic segments, particularly among middle-income households. The production of wooden toys involves expensive raw materials, labor-intensive crafting processes, and stringent quality control measures to ensure smooth finishes and safety, all of which inflate the final retail price. According to European forestry sector analyses, global supply chain disruptions alongside surging demand from the construction and furniture sectors have driven notable cost increases for sustainably sourced timber, applying financial pressure on downstream wooden product manufacturers. The economic reality confines the wooden toy market largely to affluent demographics or special occasion gifts, preventing it from becoming an everyday staple for the majority of European families. Consumer research indicates that high-quality wooden toys generally command a pricing premium over basic mass-produced plastic items, a structural cost differential that actively influences family purchasing decisions during periods of consumer economic uncertainty. This price sensitivity is particularly pronounced in Southern and Eastern European markets, where disposable household income is comparatively lower. High prices currently restrict volume growth and market share expansion, and this dynamic will continue until production efficiencies lower costs or consumer willingness to pay a premium becomes more widespread across socioeconomic groups. Until then, the wooden toys sector risks remaining a niche premium category rather than achieving mainstream adoption.

Vulnerability to Environmental Degradation and Moisture Damage

The inherent susceptibility of natural wood to environmental factors represents a critical technical constraint affecting the growth of the wooden toys market. Factors such as moisture, humidity, and temperature fluctuations can compromise product integrity and safety over time. Unlike plastic, which is impervious to water and resistant to warping, wood can swell, crack, or develop mold if not properly treated or stored, posing potential hygiene risks for children. Climate tracking data indicates that multiple regions across Northern and Western Europe experience prolonged seasonal rainfall and high relative humidity, creating challenging atmospheric conditions for organic wood products exposed to outdoor environments or damp play spaces. Toy manufacturers utilize specialized sealing, non-toxic varnishing, and treatment processes to protect wooden items from moisture-induced degradation, increasing baseline processing requirements and production complexity. Despite these treatments, there remains a consumer perception that wooden toys are less durable in wet environments, limiting their use in bathrooms, gardens, or sandboxes where plastic dominates. Incidents of splintering or finish degradation due to improper care can lead to safety recalls and reputational damage for brands. Furthermore, the maintenance requirements for wooden toys, such as occasional oiling or cleaning with specific agents, may deter busy parents seeking low-maintenance solutions. This vulnerability restricts the functional versatility of wooden toys compared to the all-weather resilience of plastics, confining them primarily to indoor dry play scenarios and narrowing their application scope in diverse European climates.

MARKET OPPORTUNITIES

Integration of Smart Technology with Traditional Wooden Designs

The hybridization of traditional wooden aesthetics with embedded smart technology paves the way for substantial growth within the wooden toys market. These phygital toys blend tactile play with digital interactivity to appeal to modern tech-savvy families seeking balanced development tools. This innovation allows manufacturers to retain the eco-friendly and sensory benefits of wood while incorporating features like augmented reality, sound sensors, or connectivity apps that enhance educational value without compromising the natural feel. Companies can develop wooden puzzles that trigger animated stories on tablets when solved or build sets that interact with virtual worlds, bridging the gap between screen time and physical play. Research on modern early childhood development reveals a strong and growing interest among parents for interactive toys that seamlessly combine physical manipulation with purposeful, non-passive digital features to guide early learning. This approach addresses parental concerns about excessive device usage by making technology a supplementary tool rather than the primary focus. By leveraging technologies like NFC chips or QR codes embedded discreetly within wooden structures, brands can offer downloadable content, progress tracking, and personalized learning paths. This fusion opens new revenue streams through software subscriptions and content updates, transforming a one-time hardware purchase into an ongoing service relationship. It positions wooden toys as forward-thinking and relevant in a digital age, attracting a broader demographic that might otherwise dismiss traditional wood as outdated. Market trends in Northern and Western Europe demonstrate that hybrid wooden educational toys, which integrate tactile structures with embedded learning technology, experience favorable adoption rates due to their high developmental value.

Expansion of Circular Economy Models and Toy Rental Services

The burgeoning circular economy movement offers a lucrative opportunity for the global wooden toys market. This opportunity arises from the establishment of rental and subscription services that capitalize on the durability and longevity of wooden products. Given that wooden toys are designed to withstand generations of use, they are ideally suited for sharing economies where items are circulated among multiple families, reducing waste and lowering the cost barrier for consumers. Startups and established brands can launch platforms where parents subscribe to receive curated boxes of high-quality wooden toys, returning them as children outgrow specific developmental stages. According to broader circular economy trends, the toy rental and subscription market across Europe is experiencing notable expansion, driven by environmentally conscious and cost-aware parents who favor product-as-a-service models over traditional ownership. This model democratizes access to premium wooden toys, allowing families to enjoy high-end products without the prohibitive upfront cost. It also aligns perfectly with the sustainability ethos of the wooden toy sector, emphasizing resource efficiency and waste reduction. Companies can build loyal customer bases and create recurring revenue streams by implementing robust sanitization and logistics networks. These measures insulate them from the volatility of traditional retail sales while fostering community engagement around shared play experiences. Commercial pilots for toy subscription and circular reuse frameworks in Western Europe have validated the long-term economic viability of resource-efficient models, supported by high consumer loyalty and strong community repeat-participation.

MARKET CHALLENGES

Stringent Regulatory Compliance and Certification Complexities

The intricate and rigorous landscape of regulatory compliance presents a significant hurdle to the expansion of the wooden toys market. This is particularly true regarding chemical safety, sourcing certification, and labeling requirements that vary across member states. Manufacturers must navigate a complex web of standards, including the EU Toy Safety Directive, REACH regulations, and FSC or PEFC certification for wood sourcing, each demanding extensive documentation and testing. Furthermore, discrepancies in national enforcement and interpretation of these rules can lead to market fragmentation, where a product approved in one country faces rejection in another. The constant evolution of safety standards, driven by emerging scientific data on toxicology, forces companies to continuously update their processes and formulations, risking obsolescence of existing inventory. Failure to maintain perfect compliance can result in severe penalties, product recalls, and irreversible brand damage. This regulatory intensity favors large corporations with dedicated legal and quality assurance teams, potentially stifling innovation from smaller artisanal producers who form the heart of the traditional wooden toy sector. The administrative burden alone consumes a notable share of operational budgets for independent European wooden toy manufacturers, diverting resources from design and market expansion.

Supply Chain Volatility and Raw Material Sourcing Constraints

Securing a consistent and affordable supply of high-quality, sustainably sourced timber amidst global supply chain disruptions and competing industrial demands remains a persistent impediment to the wooden toys market. The availability of specific wood types like beech, maple, and rubberwood, which are preferred for their grain and hardness, is increasingly constrained by deforestation concerns, climate change impacts on forestry, and competition from the construction and bioenergy sectors. European manufacturers relying on imported timber are particularly vulnerable to geopolitical tensions, trade tariffs, and logistical bottlenecks that inflate costs and extend lead times. The push for local sourcing to reduce carbon footprints often clashes with the limited capacity of European forests to meet industrial demand without compromising biodiversity goals. Fluctuations in raw material prices make long-term pricing strategies difficult, forcing companies to either absorb margins or pass costs to consumers, risking demand erosion. Additionally, the verification of sustainable sourcing credentials requires robust traceability systems, which can be complex and costly to implement across international supply chains. This instability threatens the reliability of production schedules and the ability to meet growing market demand, posing a strategic risk to the sector's scalability and long-term competitiveness.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Age group, Product, Distribution Channel, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East & Africa |

| Market Leader Profiled | Hape International, Plan Toys, Melissa & Doug, Grimms Spiel und Holz Design, Sevi, Brio, Manhattan Toy, EverEarth, Teg,u and Janod |

SEGMENTAL ANALYSIS

By Distribution Channel

The physical stores segment led the global wooden toys market and captured a 43.9% share in 2025. This leading position of the segment was credited to consumers valuing tactile evaluation before purchase, especially for premium wooden products, where finish quality, weight, and safety features require hands-on assessment. Specialty toy retailers and department stores provide curated selections that educate parents about developmental benefits, while in-store demonstrations allow children to engage with products, creating emotional connections that drive conversion. Consumer survey data indicates that a significant majority of parents in Western Europe prefer visiting physical retail stores when purchasing toys for children under five, prioritizing the ability to manually inspect material quality and verify official safety certifications before buying. Furthermore, physical retail environments enable impulse purchases during seasonal shopping periods. The experiential nature of physical shopping aligns with the premium positioning of wooden toys, where storytelling, brand heritage, and artisanal craftsmanship are best communicated through personal interaction with knowledgeable staff.

On the other hand, the online distribution channel segment is likely to experience the fastest CAGR of 6.3% from 2026 to 2034. This acceleration of the segment is propelled by shifting consumer behaviors toward digital convenience, expanded product discovery, and personalized shopping experiences. Various studies show that online toy sales across Europe continue to expand, with sustainably sourced wooden toys representing an active growth subcategory as digital platforms provide detailed product transparency and environmental compliance details to consumers. Parents increasingly rely on peer reviews, educational content, and video demonstrations available exclusively online to evaluate wooden toy suitability for specific developmental stages. Research on modern digital shopping habits demonstrates that a vast majority of millennial parents actively utilize social media platforms and online creator content to research products, enabling direct-to-consumer brands to leverage targeted advertising to reach audiences interested in Montessori or Waldorf-aligned educational items. The online channel also enables subscription models and curated bundles that increase customer lifetime value while reducing inventory risks for manufacturers.

By Product Insights

The educational toys segment dominated the global wooden toys market and accounted for a 28.8% share in 2025. This dominance of the segment was driven by strong institutional adoption in preschools and kindergartens across Europe and North America, where wooden puzzles, counting blocks, and shape sorters are integrated into early childhood curricula. Comparative early childhood education studies show that accredited preschool programs across Germany, France, and Scandinavia heavily prioritize natural and wooden educational materials because they align with play-based learning philosophies, durability needs, and strict regional safety regulations. Consumer tracking data indicates that parents increasingly view high-quality wooden toys as valuable investments in early cognitive development, leading to a steady increase in household spending on premium educational toys. The versatility of educational wooden toys, which support multiple developmental domains including fine motor skills, spatial reasoning, and language acquisition, ensures repeat purchases as children progress through age stages. Manufacturers benefit from extended product lifecycles and premium pricing power, as educational wooden toys are often gifted for milestones and holidays, reinforcing their market dominance.

However, the puzzles segment is expected to exhibit a noteworthy CAGR of 6.2% during the forecast period due to rising parental recognition of puzzles as effective tools for developing problem-solving abilities, patience, and hand-eye coordination in young children. Developmental psychology research demonstrates that young children who regularly engage with shapes and puzzles during early childhood develop significantly stronger spatial reasoning and problem-solving skills later in life compared to peers with limited puzzle exposure. The tactile feedback and satisfying completion experience of wooden puzzles also support emotional regulation and confidence building, attributes increasingly valued by parents navigating digital saturation concerns. Data from European product safety registries indicates that premium wooden toys exhibit excellent safety profiles with low chemical recall rates, reinforcing long-term consumer trust and driving repeat purchasing behavior among parents. Furthermore, puzzle manufacturers are innovating with layered difficulty levels, thematic designs tied to popular children's media, and augmented reality integration that maintains traditional wooden construction while adding digital enhancement options, appealing to tech-conscious families seeking balanced play experiences.

By Age Group Insights

The preschooler segment held the majority share of 30.1% of the wooden toys market in 2025. This supremacy of the segment was credited to the critical developmental window where children transition from parallel play to cooperative interactions, requiring toys that support imagination, social skills, and foundational academic concepts. Parents of preschoolers demonstrate a higher willingness to invest in quality wooden products. The preschool segment also benefits from institutional procurement, as kindergartens and daycare centers across Europe and North America increasingly standardize wooden toy inventories to meet safety and sustainability mandates. Additionally, preschool-aged children exhibit longer engagement periods with open-ended wooden toys, reducing replacement frequency and enhancing perceived value among cost-conscious families.

But the toddler segment is predicted to witness the highest CAGR of 7.1% between 2026 and 2034. This quick surge of the segment is fuelled by heightened parental focus on early sensory development and safe exploration during critical neurological formation periods. According to sources, wooden rattles, stacking rings, and simple shape sorters designed for toddlers demonstrate superior safety profiles with zero reported choking hazards when manufactured to EN71 standards, building strong consumer confidence. The toddler segment also benefits from gifting traditions, with wooden toys representing preferred choices for first birthdays and holiday presents due to their heirloom quality and developmental appropriateness. Manufacturers are responding with innovative designs featuring soft edges, non-toxic finishes, and modular components that grow with the child, extending product relevance and encouraging brand loyalty from the earliest purchasing decisions.

COUNTRY LEVEL ANALYSIS

Asia Pacific Wooden Toys Market Analysis

Asia Pacific outperformed other regions in the global wooden toys market and accounted for a 39.9% share in 2025. This dominance of the APAC market was driven by robust manufacturing infrastructure in China and Vietnam, combined with rapidly expanding domestic consumption driven by rising middle-class incomes and growing environmental awareness. According to data from the Asian Development Bank, steady economic expansion and rising middle-class disposable incomes across emerging Asian economies have increased familial purchasing power, enabling higher household spending on premium educational and developmental children's products. The China Toy and Juvenile Products Association documents that China remains a dominant force in global toy manufacturing, while surging domestic demand from urban parents seeking premium, sustainable alternatives to plastic is driving a major expansion of the domestic wooden toy market. Japan and South Korea contribute through high-value artisanal segments, where traditional woodworking craftsmanship commands premium pricing. Consumer data from the Asia-Pacific region indicates that an expanding majority of parents actively prioritize eco-credentials, natural materials, and chemical safety when purchasing products for young children, directly accelerating the adoption of premium wooden toys. Regional e-commerce platforms like Alibaba and Shopee further accelerate market access, connecting manufacturers with consumers across diverse cultural contexts while maintaining quality standards.

Europe Wooden Toys Market Analysis

Europe was the next prominent region in the global market and captured a 30.1% share in 2025. This position of the European market was supported by deep cultural appreciation for craftsmanship, stringent safety regulations, and early adoption of sustainability principles across consumer and institutional segments. European forestry and environmental frameworks dictate strict compliance guidelines for timber products, pushing wooden toy manufacturers across the continent to increasingly prioritize FSC or PEFC-certified timber to reinforce responsible sourcing practices. Germany, France, and the Nordic countries drive premium segment growth, where artisanal brands command significant price premiums based on heritage and design excellence. European retail trends reveal sustained consumer demand for curated, high-quality, and open-ended play offerings, driving independent specialty toy stores to expand their physical and digital shelf space for premium wooden educational product lines. Educational policy alignment further supports market expansion, as national curricula in countries like Finland and Denmark explicitly incorporate wooden manipulatives for early mathematics and language development. Cross-border e-commerce within the European Union facilitates brand expansion while maintaining regulatory compliance through harmonized safety standards.

North America Wooden Toys Market Analysis

North America plays a major role in the global wooden toys market due to high disposable incomes, strong parental focus on developmental outcomes, and robust retail infrastructure supporting both mass market and premium segments. A study indicates that American households with young children allocate a reliable portion of their discretionary budgets to toys and early learning materials annually, with sustainably sourced and wooden educational products emerging as highly active growth subcategories. Canada contributes through sustainability-conscious consumers who prioritize locally sourced wooden toys, with domestic manufacturers benefiting from government incentives for green production methods. Educational institution partnerships further drive demand, as preschools and early learning centers across the United States increasingly specify wooden materials for safety and durability. Direct-to-consumer brands leverage digital marketing to reach niche audiences interested in Montessori or Waldorf-aligned products, expanding market reach beyond traditional retail channels.

Latin America Wooden Toys Market Analysis

Latin America witnessed a consistent growth in the global wooden toy market. Growth in this region is because of expanding middle-class populations in Brazil and Mexico, increasing awareness of child development principles, and growing preference for sustainable products among urban consumers. Local manufacturers in Brazil and Argentina are developing regionally inspired wooden toy designs that incorporate cultural motifs and traditional play patterns, differentiating offerings from imported alternatives. Government initiatives promoting early childhood education in countries like Chile and Colombia create institutional demand for durable, safe wooden learning materials. Challenges remain regarding distribution infrastructure and price sensitivity, but the region's demographic youthfulness and economic trajectory support long-term expansion potential.

Middle East and Africa Wooden Toys Market Analysis

The Middle East and Africa region is predicted to expand notably in the global wooden toys market over the forecast period, owing to urbanization, rising education investments, and increasing environmental consciousness among affluent consumers. The United Arab Emirates and Saudi Arabia lead premium segment adoption, where international wooden toy brands benefit from high disposable incomes and strong retail infrastructure in luxury shopping destinations. Local artisans in countries like Morocco and Tunisia contribute unique handcrafted wooden toys that appeal to both domestic and export markets, leveraging traditional woodworking skills. Educational reforms across Sub-Saharan Africa, emphasizing play-based learning, create institutional opportunities for durable wooden educational materials. While challenges regarding import costs and distribution logistics persist, the region's young population profile and economic diversification efforts support gradual market expansion.

COMPETITIVE LANDSCAPE

The wooden toys market features a moderately fragmented competitive landscape where artisanal producers coexist with established global brands. Leading companies differentiate through sustainability credentials, educational alignment, and design innovation rather than price competition alone. Market entry barriers remain moderate due to specialized manufacturing requirements and safety certification processes, yet numerous small-scale artisans thrive by serving niche segments with handcrafted offerings. Competition intensifies around digital marketing capabilities, as brands leverage social media and influencer partnerships to reach millennial parents prioritizing eco-friendly products. Institutional procurement channels, including preschools and early learning centers,s represent significant battlegrounds where safety certifications and curriculum alignment determine supplier selection. Cross-regional expansion presents both opportunities and challenges, as brands navigate varying regulatory environments and cultural preferences regarding play patterns and educational philosophies. Innovation cycles accelerate as companies integrate technology thoughtfully without compromising the tactile, screen-free experiences that define wooden toy appeal. Consolidation trends emerge as larger players acquire artisanal brands to expand design portfolios while maintaining authentic craftsmanship narratives that resonate with conscious consumers seeking meaningful play experiences for their children.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Global Wooden Toys Market include

- Hape International

- Plan Toys

- Melissa & Doug

- Grimms Spiel und Holzdesign

- Sevi

- Brio

- Manhattan Toy

- EverEarth

- Tegu

- Janod

TOP LEADING PLAYERS IN THE MARKET

- Hape International AG operates as a global leader in sustainable wooden toy design and manufacturing with facilities across Europe and Asia. The company emphasizes FSC-certified materials, water-based finishes, and child development research to create products that align with educational philosophies worldwide. Hape recently expanded its STEM-focused collections targeting preschool-aged children, integrating engineering concepts into traditional wooden building systems. The company strengthened its market position through strategic distribution partnerships in emerging markets and enhanced digital engagement platforms that showcase product safety credentials and developmental benefits. Hape maintains rigorous quality control protocols exceeding international toy safety standards, reinforcing consumer trust and institutional adoption across public and private early childhood education settings.

- Melissa and Doug has established itself as a trusted brand for wooden and sustainable toys through consistent focus on open-ended imaginative play and developmental appropriateness. The company recently launched innovative product lines, including Sticker WO, which combines traditional wooden construction with collectible sticker elements, appealing to modern families seeking balanced play experiences. Melissa and Doug strengthened its market presence through expanded retail partnerships and enhanced e-commerce capabilities that provide detailed product information and age-appropriate recommendations. The company maintains strong brand loyalty through commitment to durability, safety certifications, and screen-free play values that resonate with parents concerned about digital saturation. Recent investments in sustainable packaging and carbon-neutral shipping initiatives further align the brand with environmentally conscious consumer preferences.

- PlanToys pioneered sustainable wooden toy manufacturing through innovative use of rubberwood from trees no longer producing latex, establishing industry benchmarks for circular economy practices. PlanToys strengthened its market position through strategic collaborations with early childhood education organizations to develop products aligned with Montessori learning principles. The company maintains rigorous non-toxic finishing processes and minimal packaging approaches that appeal to environmentally conscious consumers. PlanToys continues to innovate through modular designs that support multiple play patterns and developmental stages, extending product relevance and encouraging brand loyalty among families prioritizing sustainable consumption and child-centered play experiences.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the wooden toys market prioritize sustainability certifications and transparent sourcing to build consumer trust and differentiate premium offerings. Companies invest heavily in research and development to create innovative designs that blend traditional craftsmanship with modern educational principles, particularly STEM and Montessori-aligned features. Strategic distribution partnerships with specialty retailers and e-commerce platforms expand market reach while maintaining brand positioning. Leading manufacturers emphasize direct consumer engagement through digital content that showcases product safety, developmental benefits, and environmental credentials. Many companies pursue vertical integration to control quality across the supply chain from sustainable forestry to finished product delivery. Collaborations with educational institutions and child development experts enhance product credibility and institutional adoption. Premium pricing strategies supported by heirloom quality positioning allow manufacturers to maintain margins despite higher production costs associated with sustainable materials and ethical labor practices.

MARKET SEGMENTATION

This research report on the wooden toys market has been segmented & sub-segmented based on the distribution channel, product, age group, and region.

By Distribution Channel

- Physical stores

- Online

- others

By Product

- Building blocks

- Puzzles

- Dolls

- Vehicles

- Educational toys

- Others

By Age group

- Infants

- Toddlers

- Preschoolers

- Older children

- Others

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is the Wooden Toys Market?

The wooden toys market refers to the industry that produces toys primarily made from wood, which come in various shapes and sizes for children of different age groups.

What is the market size of the Wooden Toys Market?

The wooden toy market was valued at around USD 26.56 billion in 2022 and is expected to reach USD 35.24 billion at a CAGR of 5.2% by the end of 2028.

What are the opportunities in the Wooden Toys Market?

The opportunities in the wooden toys market include the growing demand for sustainable and eco-friendly options, the increasing demand for educational toys, and the aesthetic appeal of wooden toys combined with their durability and longevity.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com