Global Smart Glass Market Size, Share, Trends, Growth Forecast Report by Technology (Suspended Particle Display, Electrochromic, Liquid Crystal, Photochromic, Thermochromic), Application (Architecture, Transportation, Consumer Electronics), & Region - Industry Forecast From 2025 to 2033

Global Smart Glass Market Size

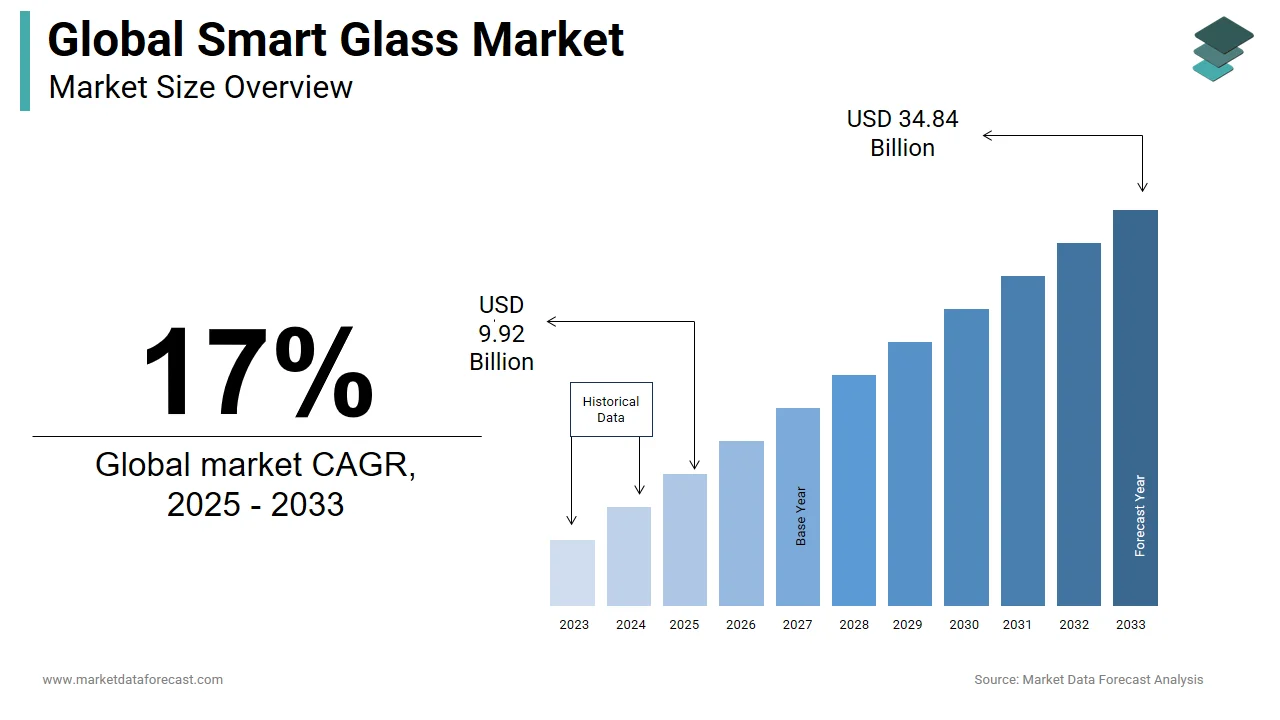

The global smart glass market was valued at USD 8.48 billion in 2024. The global market is expected to reach USD 9.92 billion in 2025 and USD 34.84 billion by 2033, growing at a CAGR of 17% during the forecast period.

Smart glass is a electrochromic, thermochromic, or suspended particle devices that dynamically modulate light and heat transmission and is no longer experimental. It is being deployed at scale in federal buildings, corporate headquarters, and high-performance hospitals to reduce HVAC demand. These are energy-adaptive systems that redefine the boundary between structure and intelligence. According to the U.S. Department of Energy, buildings account for 40% of total U.S. energy consumption, with glazing responsible for nearly 30% of heating and cooling loads in commercial structures.

MARKET DRIVERS

Net-Zero Building Codes and Energy Efficiency Mandates

The proliferation of stringent net-zero building standards across U.S. municipalities has transformed smart glass from a luxury feature into a compliance imperative, which surges the growth rate of the smart glass market. Major federal agencies, including the General Services Administration, require electrochromic glass in all new construction projects under the Biden administration’s Executive Order on Climate Resilient Infrastructure. The result, architects are no longer choosing smart glass for aesthetics, they are selecting it because code violations carry financial penalties exceeding a notable amount per non-compliant facade. This regulatory burden has turned smart glass into infrastructure, not ornamentation.

Healthcare Demand for Dynamic Light Therapy and Patient Well-Being

In healthcare facilities, smart glass is emerging as a clinical tool, not merely an energy saver, which contributes to the growth ofthe smart glass market. According to a study, patients in hospital rooms equipped with tunable electrochromic windows experienced a reduction in sleep disruption and a decrease in delirium episodes compared to those in static-light environments, due to circadian-aligned light modulation.

MARKET RESTRAINTS

High Upfront Cost and Lack of Financing Mechanisms for Retrofit Projects

The capital expenditure for smart glass remains prohibitive for most retrofit markets, which is a major factor impeding the expansion of the smart glass market. According to the research, installing electrochromic glazing in an existing mid-rise office building costs per square foot than the cost of conventional double-glazed units. Lifecycle analyses show payback periods of several years through energy and HVAC savings. However, few property owners can justify such outlays without third-party financing. Unlike solar panels, which benefit from federal tax credits, smart glass qualifies for neither investment tax credits nor accelerated depreciation, as per the study. As per a study, a portion of building owners abandoned smart glass retrofits due to a lack of accessible capital, even when the projected ROI exceeded. Smart glass remains locked out of the vast majority of existing buildings. Its impact could be greatest there.

Performance Variability Under Real-World Environmental Conditions

The underperformance outside controlled lab conditions affects confidence in their reliability, which in turn degrades the growth of the smart glass market. Extreme environmental factors, such as prolonged direct sunlight and high temperatures, can negatively affect the operational performance and long-term reliability of electrochromic windows. These conditions can impact switching speed, accelerate degradation over time, and cause internal heating of the glass. In Phoenix and Las Vegas, thermal stress caused delayed switching cycles for several minutes, while humidity-induced fogging compromised clarity in coastal regions like Miami. These failures are rarely covered under warranties, and maintenance requires specialized technicians; fewer certified professionals exist nationwide. When performance falters under real-world stress, trust erodes, and adoption stalls.

MARKET OPPORTUNITIES

Integration with AI-Powered Building Management Systems for Predictive Optimization

Its evolution from a standalone component into a node within intelligent building networks is serving as an enabler for new opportunities in the smart glass market. Companies like View Inc. and SageGlass now embed machine learning algorithms into their glass controllers that analyze real-time weather forecasts, occupancy sensors, and grid load data to preemptively adjust transparency, reducing peak demand before it occurs. According to a study, AI-driven smart glass in public housing towers can reduce grid strain during summer heatwaves by shifting tint schedules minutes ahead of predicted load spikes, lowering peak power draw without manual intervention. This integration enables smart glass to function not just as a passive filter, but as an active participant in grid resilience, earning participation credits in demand-response programs.

Military and Aerospace Applications for Adaptive Camouflage and Thermal Regulation

The rising importance in the defense and aerospace sectors, where survivability demands dynamic optical control, is unlocking fresh opportunities for the expansion of the smart glass market. Also, Thermochromic materials are being investigated for various space applications, including variable emittance coatings for spacecraft thermal control.NASA is developing technologies to protect astronauts and hardware from the harsh lunar environment, including intense solar radiation and abrasive dust. Boeing’s 787 Dreamliner already employs smart dimmable windows throughout the entire cabin, reducing cabin lighting per flight. These applications bypass consumer price sensitivity entirely. Here, performance and safety override cost, which accelerates R&D that eventually trickles down to commercial markets.

MARKET CHALLENGES

Supply Chain Vulnerability of Rare Iridium and Tungsten Oxides

The production of high-performance electrochromic layers, which relies on scarce materials, is a challenge impacting the smart glass market. The material is primarily iridium oxide and tungsten trioxide, which are concentrated in geopolitically unstable regions. According to the study, a portion of the global iridium supply originates from South Africa and Russia, with a lesser share produced domestically. Iridium, essential for stable ion exchange in electrochromic films, is listed as a critical material by the EU and a critical material for energy by the U.S. No viable substitute exists yet; alternatives like nickel oxide lack durability under repeated cycling. The entire market hinges on a material more valuable than platinum and harder to secure than rare earths.

Fragmented Standards and Lack of Interoperability Across Proprietary Platforms

The lack of interoperability limits the expansion of the smart glass market. Each manufacturer uses proprietary control protocols, communication interfaces, and calibration thresholds, rendering systems incompatible with third-party building automation platforms. Architects designing holistic façades often abandon smart glass altogether because integrating View, SageGlass, and EControl products simultaneously requires separate control panels, software licenses, and training modules. The absence of open standards forces contractors into vendor lock-in, which inflates lifecycle costs and stifles innovation. Smart glass lacks a unified protocol like Wi-Fi or USB-C.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Application, Technology, and Region |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Smartglass International Limited, SAGE Electrochromics, Asahi Glass Corporation, View, Inc., Shenzhen Hongjia Glass Product Co, Dupont, Saint-Gobain SA, Guangdong Kangde Xin Window Film Co., Ltd, and Others. |

SEGMENTAL ANALYSIS

By Application Insights

The architecture segment outpaced other segments in the smart glass market by capturinga substantial share in 2024 due to the convergence of energy codes, corporate sustainability mandates, and the premium placed on occupant well-being in high-value real estate. Beyond aesthetics, smart glass reduces glare on screens, eliminates blinds and shades, and creates uninterrupted views, all vital for productivity in knowledge economies. Architecture doesn’t just use smart glass; it depends on it to meet regulatory, economic, and human performance benchmarks simultaneously.

The transportation segment is estimated to register the fastest CAGR of 31.2% from 2025 to 2033. The aerospace, rail, and automotive innovations demanding adaptive visibility, thermal regulation, and safety enhancements are boosting the expansion of the transportation segment in the global market. Boeing’s 787 Dreamliner features electrochromic dimmable windows across all passenger cabins that reduce cabin lighting energy use per flight and improve passenger circadian alignment, according to a study. Major high-speed rail manufacturers like Siemens and Alstom are integrating smart glass technology to manage light and heat, but they primarily use advanced electrochromic and Suspended Particle Device (SPD) glazing. Transport is no longer a passive vessel; it is a responsive interface, and smart glass is becoming its nervous system.

By Technology Insights

The electrochromic glass segment captured the leading share of the smart glass market by accounting for 56.6% share of the global market in 2024. Precision control, durability, and seamless integration into building automation systems are all main factors behind the growth of the electrochromic glass segment in the global market. Unlike photochromic or thermochromic variants that respond passively to light or heat, electrochromic glass allows dynamic, user-driven modulation of visible light transmission, from a percentage clarity to under less opacity, with minimal power consumption (typically less than 1 watt per square meter). In commercial architecture, it is mandated for high-performance façades due to their ability to reduce HVAC loads.

The thermochromic smart glass segment is set to grow at the highest CAGR of 24.7% during the forecast period. The swift expansion of the can be attributed to its passive, maintenance-free operation, ideal for regions with extreme climates and limited access to building management infrastructure. Unlike electrochromic systems requiring wiring and controllers, thermochromic glass changes tint automatically when surface temperature crosses a threshold (typically 25–30°C), eliminating the need for external power or software. This growth here isn’t about luxury; it’s about accessibility. Thermochromic glass brings dynamic performance to markets where electricity, expertise, and budgets are scarce.

REGIONAL ANALYSIS

North America Market Analysis

North America was the top performer in the smart glass market in 2024 and accounted for 42.5% of the market share in 2024. The prominence of North America in the global market is largely propelled by aggressive policy, technological maturity, and institutional adoption. California accounts for a portion of North American demand, driven by Title 24 mandates requiring dynamic glazing. Federal agencies require electrochromic glass in all new construction under Biden’s climate resilience executive orders. Corporate campuses have turned smart glass into architectural signatures by demonstrating that performance can be aesthetic. Yet this dominance masks a hidden divide. North America leads not because it’s universal. It leads because it enforces excellence. Here, smart glass isn’t optional; it’s contractual.

Europe Market Analysis

Europe was a major player right after the dominant region in the glass market and captured 31.7% of the share in 2024. The EU’s Energy Performance of Buildings Directive (EPBD) requires all public buildings to achieve nearly zero-energy status by 2030, pushing architects toward intelligent fenestration solutions that outperform static glazing. Germany leads in integration, with a portion of new office developments incorporating electrochromic systems synchronized. Scandinavia pioneers sustainability-driven innovation. Crucially, Europe promotes lifecycle assessments for all smart materials under REACH regulations, forcing manufacturers to disclose energy inputs, material sourcing, and end-of-life recyclability by creating a market where transparency equals competitiveness. Europe doesn’t chase trends. It codifies them into law, which makes smart glass not a feature, but a legal requirement for modern architecture.

Asia Pacific Market Analysis

Asia Pacific is expected to be the most lucrative region in the global market, with China, Japan, and South Korea driving growth. China’s rapid urbanization has created a massive retrofit opportunity. Beijing offers incentives for green buildings that can include technologies like smart glass. Japan excels in precision engineering. South Korea supplies a portion of the world’s liquid crystal films used in automotive smart glass, supplying Hyundai and Kia for panoramic roof systems. In the Asia Pacific, scale meets speed. Governments deploy smart glass not as a luxury but as infrastructure. This accelerates adoption through subsidies, standardized specifications, and state-backed R&D partnerships.

Latin America Market Analysis

Latin America experienced gradual growth in the smart glass market. Brazil and Mexico are leading regional adoption, propelled by rising temperatures and energy insecurity. São Paulo and other Brazilian cities have faced significant challenges from heatwaves and climate change, leading to increased political and public discussion on climate adaptation, as per a study. However, penetration remains limited by affordability. A smaller share of private developers can afford full smart glass façades, which leads to widespread use of low-cost, non-integrated films with short lifespans. Latin America’s market is nascent but urgent. Smart glass here is not a design statement; it is a public health intervention.

Middle East and Africa Market Analysis

Middle East and Africa are anticipated to expand in the smart glass market over the forecast period. Its impact is disproportionately strategic due to extreme environmental conditions. The UAE and Saudi Arabia lead in deployment, with smart glass integrated into a portion of hotels and government complexes to manage solar gain in ambient temperatures exceeding 50°C. In sub-Saharan Africa, programs are testing low-power thermochromic coatings on refugee shelter windows, where passive temperature control reduces reliance on diesel-powered AC units, according to research. The region’s growth is not consumer-driven; it is survival-driven. Smart glass here doesn’t enhance comfort. It enables habitability. It transforms glass from a barrier into a shield against climate extremes, which makes it one of the most vital technologies for human resilience in the hottest corners of the planet.

COMPETITIVE LANDSCAPE

The competition in the smart glass market has transcended product superiority; it is now a contest over integration, ethics, and systemic influence. The leaders no longer compete on tint speed or color range; they compete by embedding their technology into the DNA of buildings, vehicles, and human health protocols. Winning means making smart glass invisible: not as a feature, but as a necessity woven into code, climate policy, medical outcomes, and national security.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global smart glass market include

- Smartglass International Limited

- SAGE Electrochromics

- Asahi Glass Corporation

- View, Inc.

- Shenzhen Hongjia Glass Product Co.

- DuPont

- Saint-Gobain SA

- Guangdong Kangde Xin Window Film Co., Ltd

GLOBAL SMART GLASS MARKET NEWS

- In January 2018, Fisker introduced its new Fisker E-motion with an advanced four-segment SPD SmartGlass roof at CES 2018. In addition, the firm also envisions providing SPD-SmartGlass technology for the side windows of their new electric vehicles.

- Spirit Lake Casino and Resort, an elegant restaurant in North Dakota, has installed smart glass to provide (customers) with spectacular views of the natural environment despite the problem of the sun's rays. The technology also helps the restaurant save money by reducing the cooling load due to weather conditions on sunny days.

MARKET SEGMENTATION

This research report on the global smart glass market has been segmented and sub-segmented based on the application, technology, and region.

By Application

- Architecture

- Transportation

- Consumer Electronics

By Technology

- Suspended Particle Display

- Electrochromic

- Liquid Crystal

- Photochromic

- Thermochromic

By Region

- North America

- Europe

- Asia Pacific

- Latin Americ

- Middle East and Africa

Frequently Asked Questions

How does smart glass contribute to energy conservation on a global scale?

Smart glass technologies help reduce energy consumption by controlling the amount of light and heat entering a building or vehicle, thereby reducing the need for artificial heating, cooling, and lighting.

What technological advancements are driving innovation in the global smart glass market?

Advancements in materials science, such as the development of electrochromic, thermochromic, and photochromic technologies, along with integration with IoT (Internet of Things) platforms for smart control and automation, are driving innovation in the smart glass market.

What are the key challenges hindering the widespread adoption of smart glass worldwide?

High initial costs, concerns regarding durability and reliability, and the complexity of integrating smart glass technologies with existing infrastructure are some of the key challenges hindering widespread adoption.

What are the emerging trends shaping the future of the smart glass market on a global scale?

Emerging trends include the integration of smart glass with IoT platforms for enhanced functionality, the development of self-tinting and self-cleaning smart glass solutions, and the increasing focus on sustainability and eco-friendly materials.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com